Europe Textile Market Size, Share, Trends and Forecast by Raw Material, Product, Application, and Country, 2026-2034

Europe Textile Market Size, Share, Trends & Forecast (2026-2034)

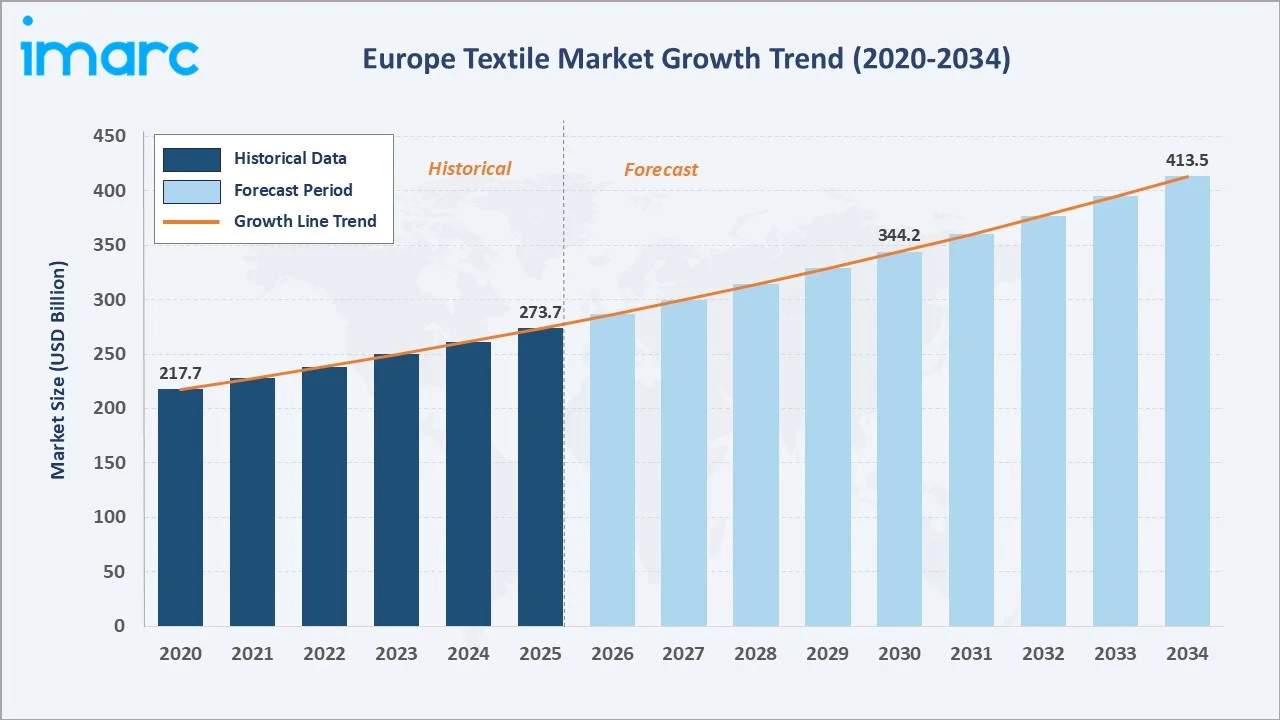

The Europe textile market size reached USD 273.7 Billion in 2025 and is projected to reach USD 413.5 Billion by 2034, exhibiting a CAGR of 4.69% during 2026-2034. Rising consumer preference for sustainable and eco-friendly fabrics, robust EU regulatory support through the European Green Deal, rapid adoption of digital textile printing, and the strong foothold of luxury and technical textile industries are the primary drivers.

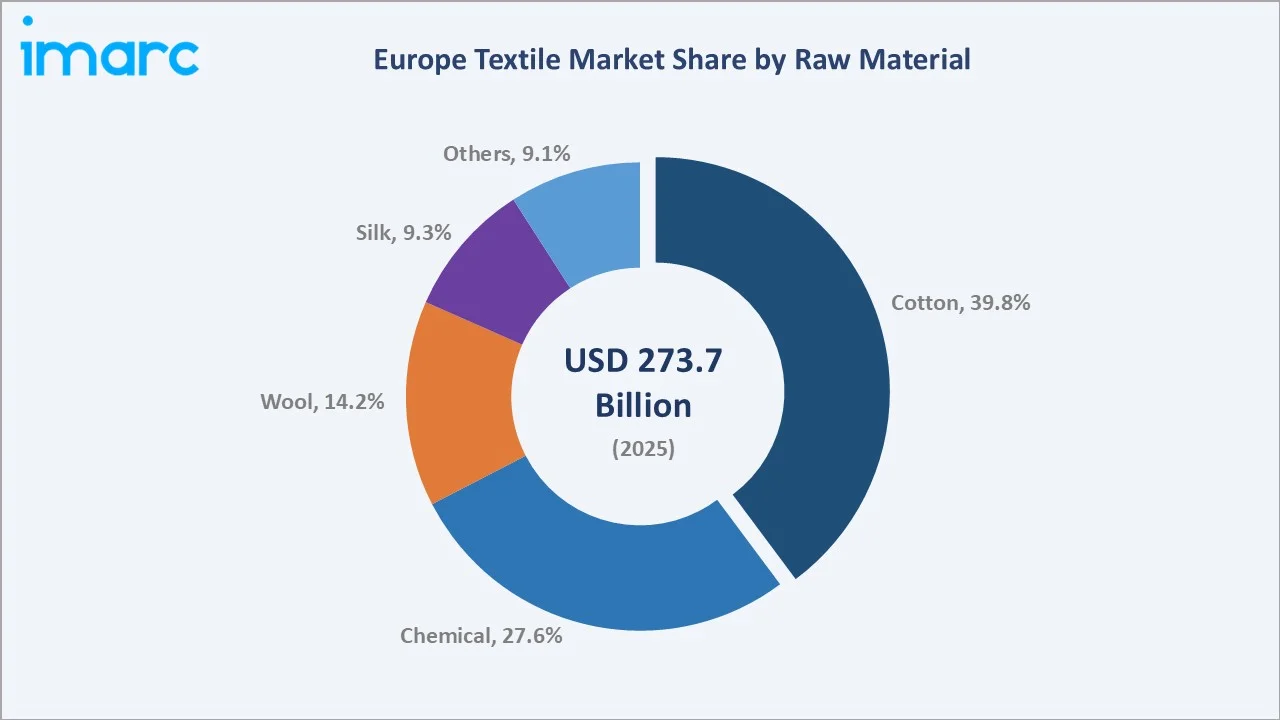

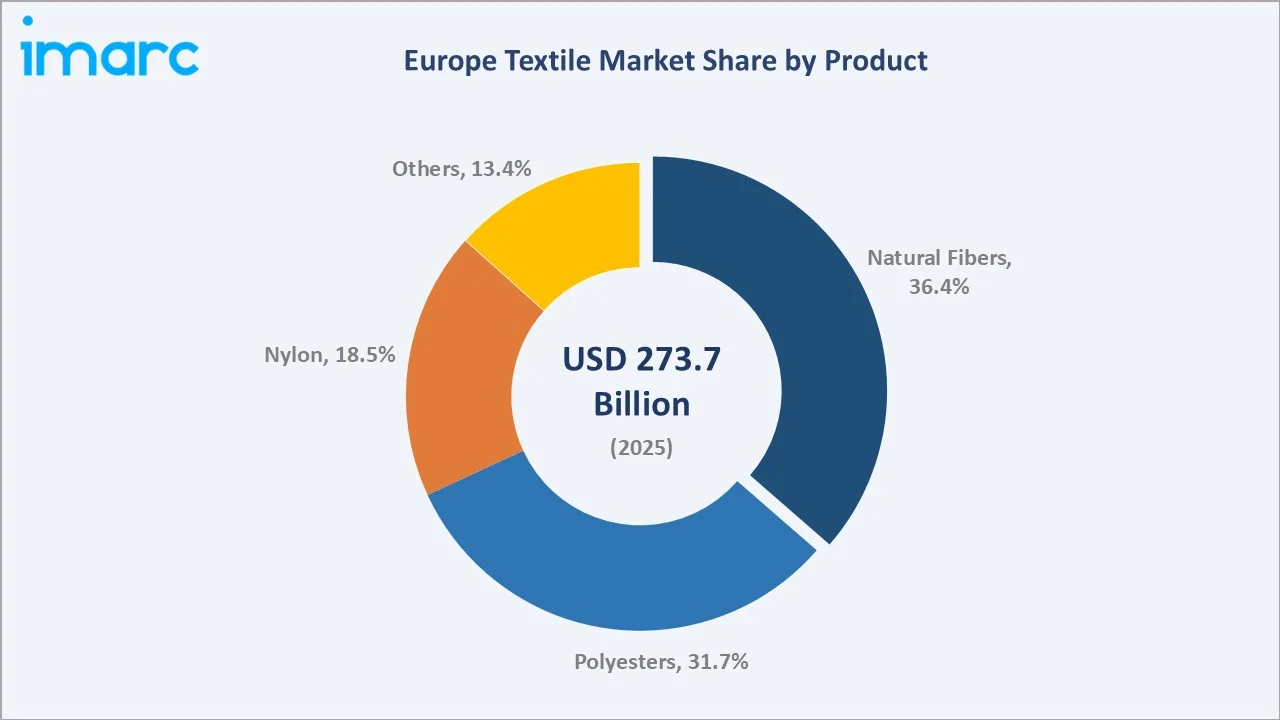

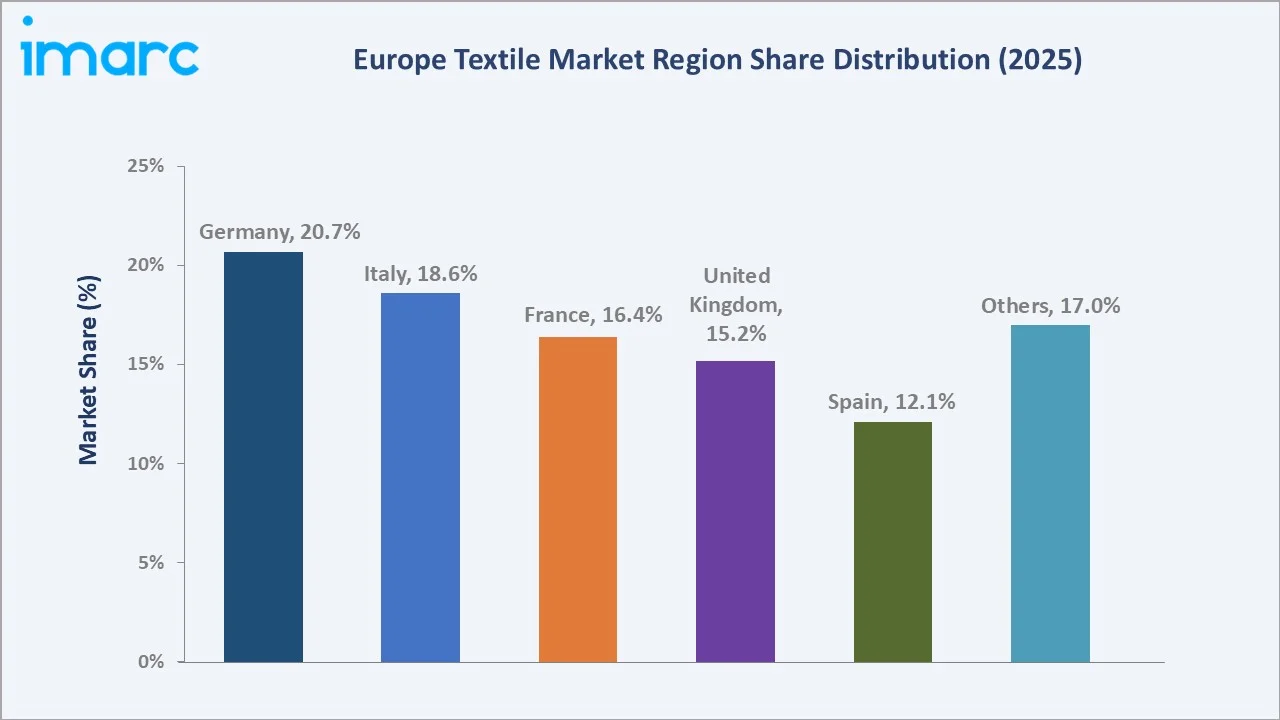

Cotton leads raw material at 39.8% in 2025, while natural fibers lead the product segment at 36.4%. Germany commands a 20.7% region share in 2025, underpinned by its advanced manufacturing infrastructure and extensive export network.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 273.7 Billion |

|

Forecast Market Size (2034) |

USD 413.5 Billion |

|

CAGR (2026-2034) |

4.69% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

Germany (20.7% share, 2025) |

|

Second Largest Region |

Italy (18.6% share, 2025) |

|

Leading Raw Material |

Cotton (39.8%, 2025) |

|

Leading Product |

Natural Fibers (36.4%, 2025) |

The Europe textile market growth trajectory from 2020 through 2034 reflects consistent demand driven by sustainable fashion mandates, industrial textile innovation, and premiumization trends. The forecast to USD 413.5 Billion captures accelerating circular economy adoption, smart textile integration, and nearshoring-driven manufacturing investment.

To get more information on this market, Request Sample

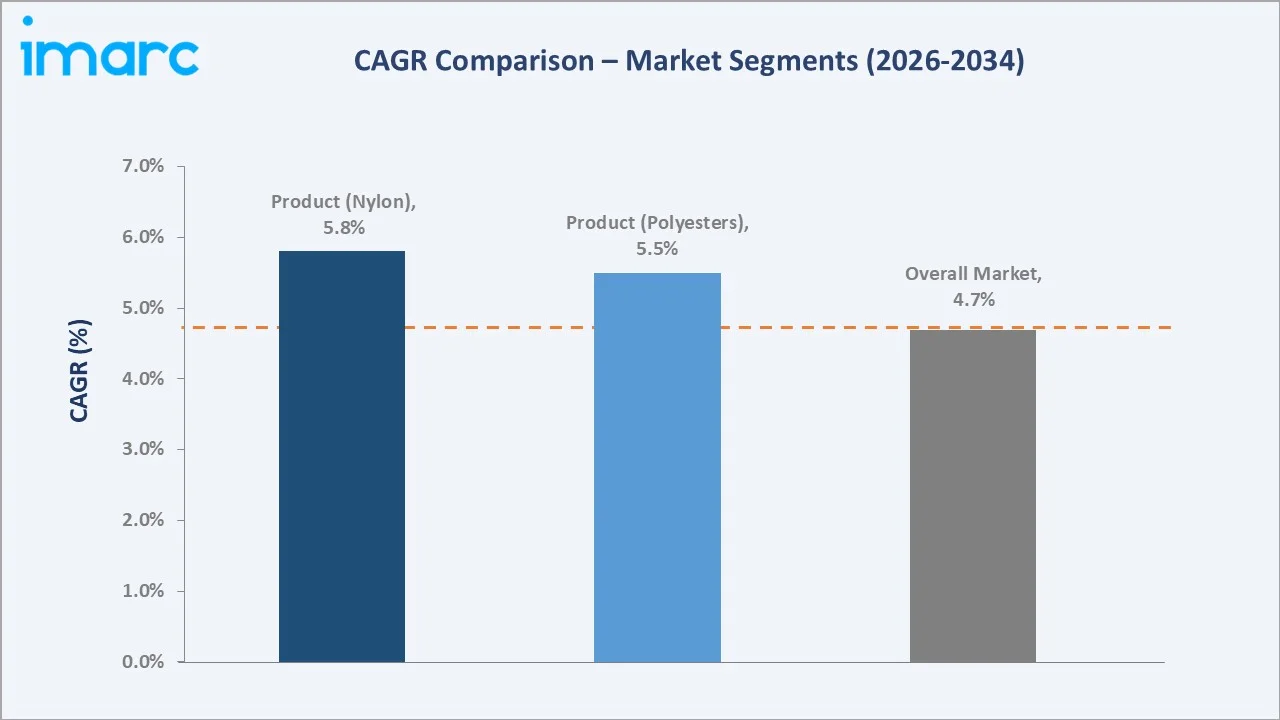

CAGR trajectories across raw material, product, and region sub-segments indicate Nylon at ~5.8% CAGR and Polyesters at ~5.5% CAGR are the fastest-growing categories within the Europe textile market through 2034.

Executive Summary

The Europe textile market is on a sustained growth trajectory from USD 273.7 Billion in 2025 to USD 413.5 Billion by 2034. Textiles are indispensable across apparel, home furnishings, automotive, healthcare, and industrial applications, benefiting from consistently non-discretionary demand across multiple end-use verticals.

Cotton dominates raw materials at 39.8% in 2025, owing to its natural breathability, versatility across seasons, and alignment with EU sustainability mandates under GOTS and OEKO-TEX certification frameworks. Chemical fibers at 27.6% are rising due to cost-performance advantages in technical applications. Wool (14.2%) retains premium positioning in luxury outerwear, while Silk (9.3%) anchors high-end couture.

Natural Fibers lead the product segment at 36.4% in 2025, driven by persistent consumer demand for breathable, sustainably sourced fabrics. Polyesters (31.7%) dominate the synthetic product segment, driven by sportswear and activewear applications. Nylon (18.5%) demonstrates the fastest product growth trajectory through 2034.

Germany leads at 20.7% in 2025, anchored by its technical textile manufacturing and machinery export infrastructure. Italy (18.6%) and France (16.4%) follow, driven by luxury fashion heritage and high-end textile craftsmanship concentrated in world-renowned manufacturing districts.

Key Market Insights

|

Insight |

Data |

|

Largest Raw Material |

Cotton – 39.8% share (2025) |

|

Leading Product |

Natural Fibers – 36.4% share (2025) |

|

Leading Region |

Germany – 20.7% share (2025) |

|

Second Largest Region |

Italy – 18.6% share (2025) |

|

Top Companies |

H&M Group, Coats Group plc, Kering, Mango, Beaulieu International Group |

Key Analytical Observations Expanding on the Above Data:

- Cotton at 39.8% in 2025 dominates because of its all-season applicability and alignment with EU sustainability mandates under GOTS and OEKO-TEX certification frameworks that continue to drive organic cotton procurement across major European apparel brands.

- Natural Fibers at 36.4% in 2025 lead the product segment because of their direct alignment with the EU Farm-to-Fiber sustainability agenda and consumer preference for GOTS-certified, biodegradable fabrics across mass-market and luxury tiers.

- Germany's 20.7% dominance in 2025 reflects its dual role as Europe's largest textile machinery exporter and a significant producer of technical and home textiles, with companies like Freudenberg Group driving industry innovation across automotive, construction, and healthcare segments.

- Italy's 18.6% share in 2025 is sustained by Milan's global fashion capital status, the concentration of luxury textile manufacturing in Biella and Como, and strong export demand for premium woolen and silk fabrics from high-net-worth global consumers.

Europe Textile Market Overview

Textiles encompass a broad range of fiber-based materials manufactured through spinning, weaving, knitting, felting, or chemical processes to produce yarns, fabrics, and finished goods for apparel, home furnishings, industrial, and technical applications. The European textile ecosystem integrates fiber producers, spinning mills, weaving and knitting manufacturers, dyeing and finishing facilities, garment construction workshops, and a diverse end-use base spanning fashion, automotive, healthcare, and construction.

Europe's textile industry is deeply embedded in the region's cultural and economic heritage, particularly in Italy, France, and Germany, where artisanal craftsmanship traditions coexist with advanced industrial manufacturing. The EU's Textiles Strategy for a Circular and Sustainable Economy and the European Green Deal mandate increasingly circular production models, establishing Europe as the global regulatory frontier for sustainable textile manufacturing standards.

Market Dynamics

To evaluate market opportunities, Request Sample

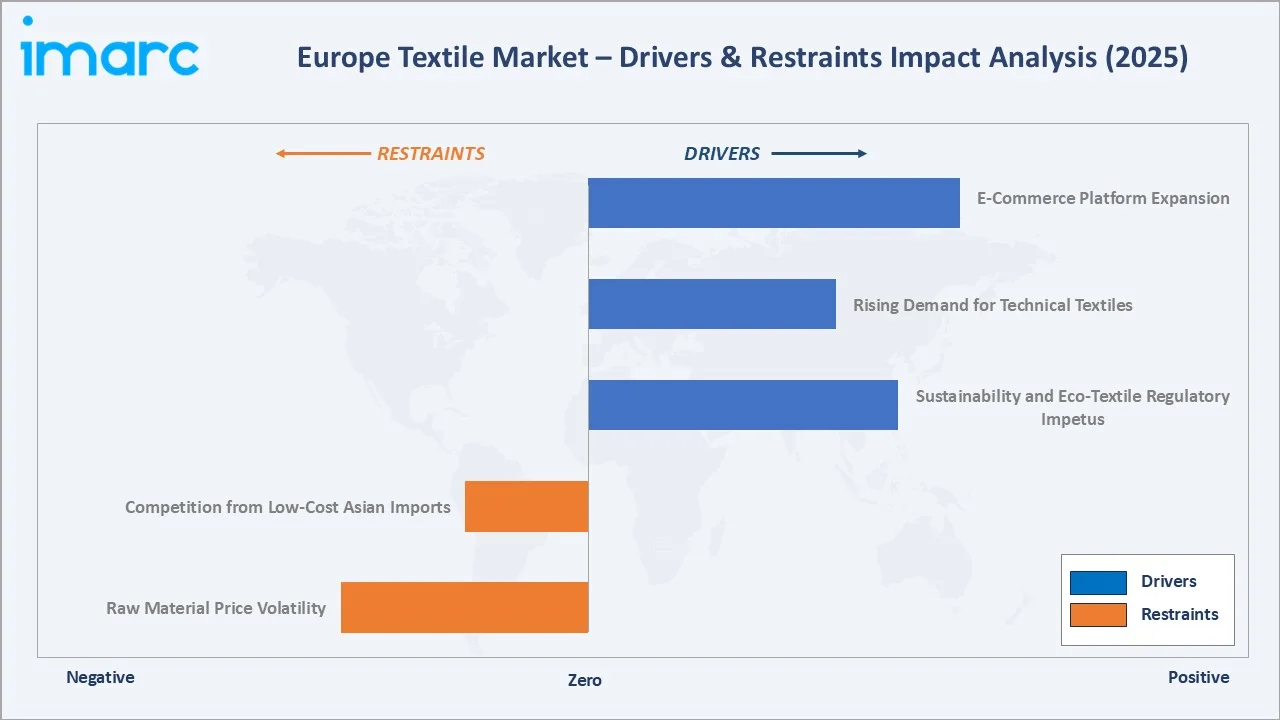

Market Drivers

- Sustainability and Eco-Textile Regulatory Impetus: The EU's European Green Deal and Textile Strategy mandate Extended Producer Responsibility (EPR), minimum recycled content requirements, and mandatory eco-design standards for textiles by 2030, creating significant procurement shifts toward certified sustainable fabrics across all market tiers.

- Rising Demand for Technical Textiles: Technical textiles used in automotive interiors, medical devices, construction membranes, and filtration applications are growing at above-market CAGRs, supported by Euratex data indicating expanding technical textile value share within the overall European textile market.

- E-Commerce Platform Expansion: Digital retail channels account for a growing share of European textile and apparel sales, with cross-border e-commerce enabling SME textile brands to access pan-European markets without traditional distribution infrastructure, broadening demand reach significantly.

Market Restraints

- Raw Material Price Volatility: Cotton futures exhibited a significant price swing between 2020 and 2024, driven by climate-induced crop disruptions and shipping cost escalation. Chemical fiber feedstock prices, linked to petrochemical markets, further amplify input cost unpredictability for European manufacturers across all production tiers.

- Competition from Low-Cost Asian Imports: EU textile imports from Bangladesh, Vietnam, and Cambodia have grown substantially, with Asian origin accounting for over 55% of total EU apparel imports by value, intensifying price competition for European manufacturers in the mid-market segment.

Market Opportunities

- Circular Economy and Textile Recycling Infrastructure: The EU's requirement for mandatory separate collection of textiles by 2025 is catalyzing investment in textile-to-textile recycling capacity, creating new demand for recycled-content feedstocks and enabling circular business models that reduce virgin material dependence.

- Smart Textiles and Wearable Technology: Smart textiles integrating conductive yarns, biosensing capabilities, and responsive materials are penetrating healthcare monitoring, sports performance, and military protective equipment segments, creating a premium high-growth sub-market within the broader European textile landscape.

Market Challenges

- REACH Chemical Regulation Compliance Costs: The European Chemicals Agency's REACH framework imposes stringent restrictions on hazardous substances in textiles, including azo dyes and PFAS-based water-repellent finishes, creating reformulation and compliance testing costs that disproportionately burden smaller manufacturers.

- Skilled Workforce Shortages in Traditional Manufacturing Regions: The decline of vocational textile training programs across Italy, Germany, and France is creating skills gaps in traditional craftsmanship areas including hand-weaving, jacquard programming, and specialty finishing, constraining premium production capacity.

Emerging Market Trends

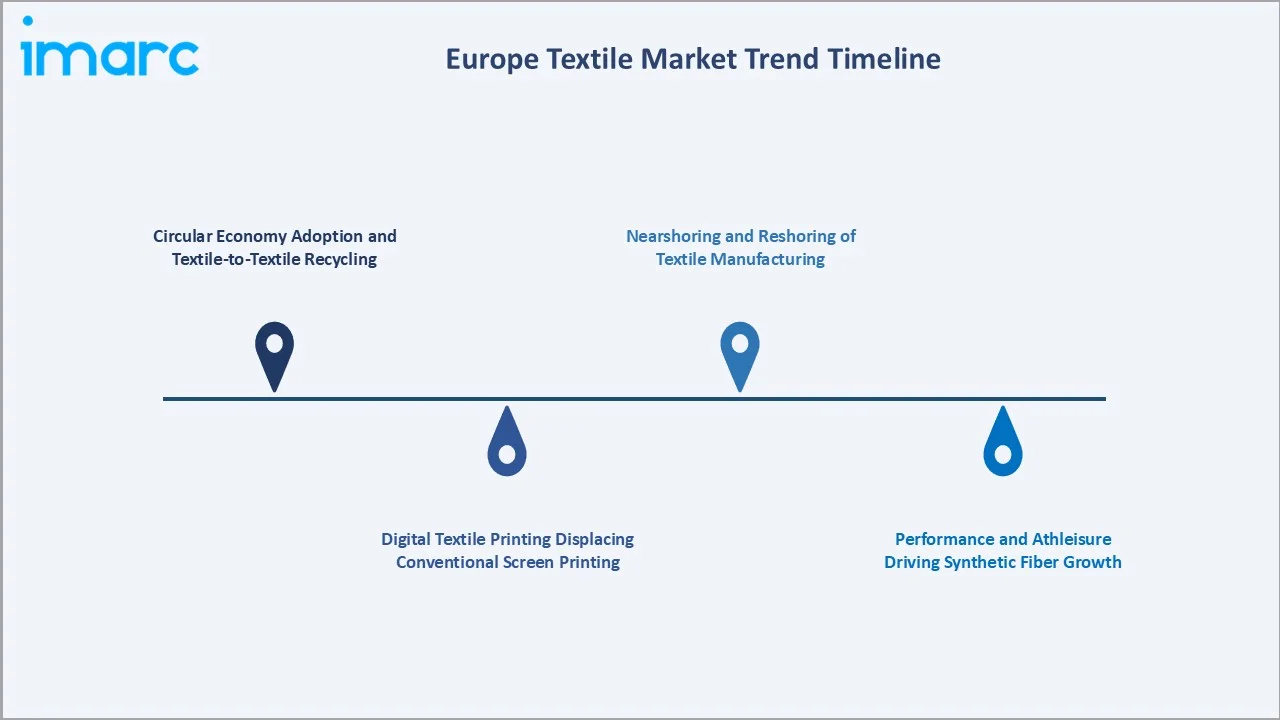

1. Circular Economy Adoption and Textile-to-Textile Recycling

The EU's Textile Strategy and EPR mandates are driving unprecedented investment in closed-loop textile recycling. Chemical recycling technologies are enabling true textile-to-textile regeneration, targeting 30% recycled content in EU textile products by 2030 and generating entirely new material supply chains that redefine sourcing economics for major brands.

2. Digital Textile Printing Displacing Conventional Screen Printing

Digital textile printing adoption is accelerating across Europe, with digital's share of total fabric print output growing steadily. On-demand printing capabilities enable mass customization, reduce water and chemical consumption by 40-60% versus screen printing, and eliminate minimum order quantity constraints for apparel and home textile brands.

3. Performance and Athleisure Driving Synthetic Fiber Growth

Consumer lifestyle shifts toward health and wellness are sustaining strong growth in performance textile applications. Moisture management, UV protection, anti-odor, and compression functionality requirements are driving polyester and nylon specification in activewear, creating premium price positioning opportunities for European technical fabric mills.

4. Nearshoring and Reshoring of Textile Manufacturing

Post-pandemic supply chain vulnerabilities and rising Asian labor costs are stimulating selective reshoring of time-sensitive textile manufacturing to European locations. Countries including Portugal, Romania, and Bulgaria are attracting nearshoring investment from Western European fashion brands seeking shorter lead times and EU-origin sustainability compliance.

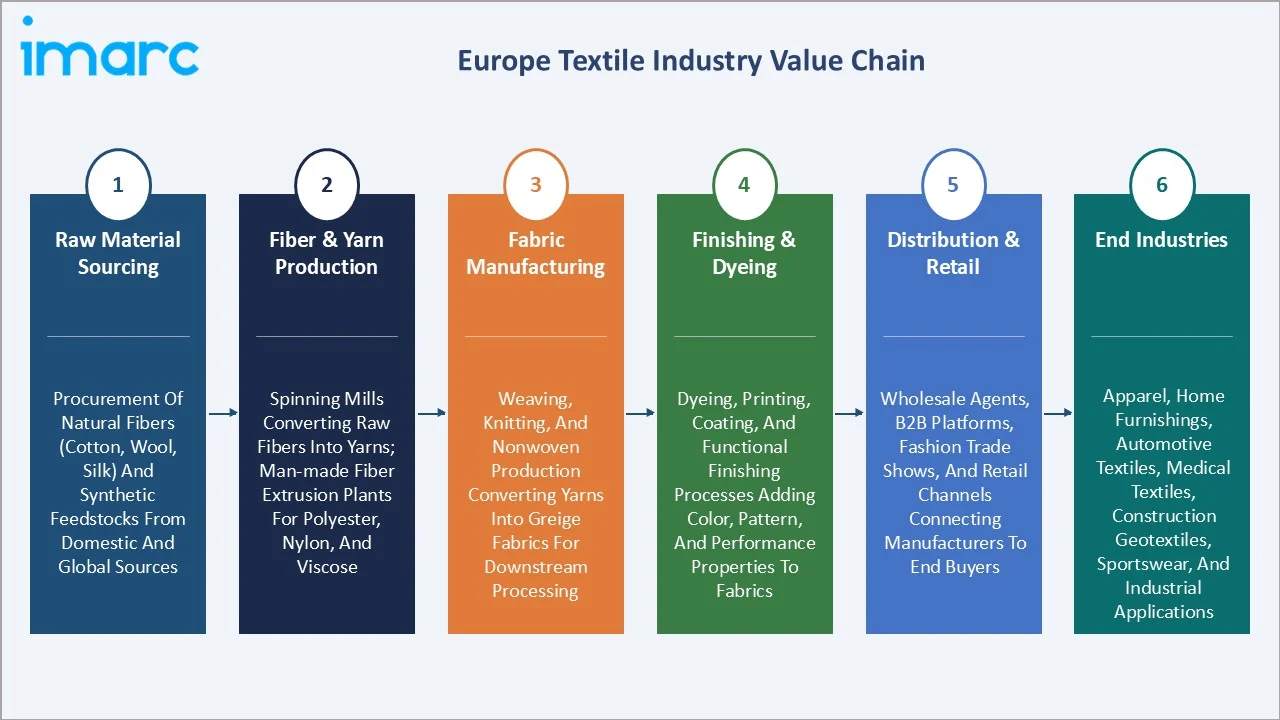

Industry Value Chain Analysis

The Europe textile value chain spans six stages from raw material procurement through end-consumer retail. Finishing, dyeing, and specialty coating operations capture the highest value-add margins, while retail and e-commerce channels command the largest revenue capture at the consumer-facing end of the chain.

|

Stage |

Description |

|

Raw Material Sourcing |

Procurement of natural fibers (cotton, wool, silk) and chemical/synthetic feedstocks from domestic and global sources |

|

Fiber & Yarn Production |

Spinning mills converting raw fibers into yarns; man-made fiber extrusion plants producing polyester, nylon, and viscose |

|

Fabric Manufacturing |

Weaving, knitting, and nonwoven production converting yarns into greige fabrics for downstream processing |

|

Finishing & Dyeing |

Dyeing, printing, coating, and functional finishing processes adding color, pattern, and performance properties to fabrics |

|

Distribution & Retail |

Wholesale agents, B2B platforms, fashion trade shows, and retail channels including e-commerce connecting manufacturers to end buyers |

|

End Industries |

Apparel, home furnishings, automotive textiles, medical textiles, construction geotextiles, sportswear, and industrial applications |

Vertically integrated manufacturers controlling fiber production through finishing achieve structural cost and quality consistency advantages over pure-play converters relying on external fiber procurement, particularly in commodity market segments where price competition is intense.

Technology Landscape in the Europe Textile Industry

Digital Textile Printing and Industry 4.0 Integration

Digital textile printing using reactive, acid, pigment, and sublimation inkjet technologies is transforming fabric decoration, enabling single-unit customization, reducing pre-press lead times from weeks to hours, and achieving certified low-impact ink formulations. AI-driven pattern generation tools are accelerating design-to-market timelines for European fashion brands significantly.

High-Performance Fiber Innovation

Advances in bio-based fibers, including Lyocell from wood pulp, PLA biopolymer fibers, and algae-derived materials, are addressing sustainability mandates while maintaining technical performance. High-tenacity polyamide and ultra-high-molecular-weight polyethylene fibers are expanding performance textile applications in protective equipment and composites markets.

Surface Treatment and Functional Finishing Technology

Plasma treatment technology is replacing conventional chemical pre-treatment processes for surface activation, reducing water consumption significantly and eliminating wastewater treatment costs. Durable Water Repellent reformulation away from PFAS compounds, driven by EU regulatory pressure, is accelerating adoption of silicone and wax-based alternatives across the European finishing industry.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Raw Material |

Cotton |

39.8% |

2025 |

|

Product |

Natural Fibers |

36.4% |

2025 |

|

Application |

🔒 |

🔒 |

2025 |

|

Country |

Germany |

20.7% |

2025 |

By Raw Material

Cotton commands a 39.8% majority share in 2025 owing to its fundamental versatility across all textile application segments and deep alignment with European consumer preferences for natural, breathable fabrics. The EU's growing emphasis on organic cotton certification and the proliferation of GOTS-certified supply chains are sustaining cotton's dominant position despite rising synthetic competition.

To access detailed market analysis, Request Sample

Chemical fibers at 27.6% in 2025, growing robustly, are indispensable in performance sportswear, automotive technical textiles, and industrial nonwovens where natural fiber performance limits are encountered. Wool (14.2%) maintains premium positioning in luxury menswear, outerwear, and carpet sectors. Silk (9.3%) serves the luxury couture and accessories segment, with French and Italian mills retaining global prestige positioning.

By Product

Natural Fibers lead the product segment at 36.4% in 2025, reflecting persistent consumer demand for breathable, sustainably sourced fabrics and strong retail premium positioning for organic and natural-fiber certified products across EU markets. The EU Farm-to-Fiber sustainability framework and GOTS certification infrastructure are reinforcing natural fiber preference across mass and premium segments.

Polyesters at 31.7% in 2025 dominate the synthetic product segment, driven by sportswear, activewear, home furnishings, and automotive textile applications where moisture management, dimensional stability, and cost efficiency are prioritized. Nylon at 18.5% demonstrates the fastest product growth trajectory, underpinned by hosiery, performance footwear, outerwear shells, and industrial technical applications.

Regional Market Insights

|

Country |

Share (2025) |

Key Growth Drivers |

|

Germany |

20.7% |

Technical textile leadership, automotive supplier base, machinery export strength |

|

Italy |

18.6% |

Luxury fashion heritage, premium wool and silk manufacturing, Como and Biella clusters |

|

France |

16.4% |

Paris luxury fashion ecosystem, technical nonwovens, high-end apparel innovation |

|

United Kingdom |

15.2% |

Heritage wool brands, performance sportswear, smart textile R&D investment |

|

Spain |

12.1% |

Fast fashion manufacturing, technical textile growth, nearshoring hub capability |

|

Others |

17.0% |

Portugal nearshoring, Romanian garment manufacturing, Belgian technical textiles |

Germany's 20.7% market leadership in 2025 is anchored by its world-class technical textile manufacturing in nonwovens, filtration media, and automotive interior textiles, supported by a highly developed textile machinery production cluster that exports globally and drives domestic production efficiency standards.

Italy, with 18.6% in 2025, leverages its concentrated luxury textile manufacturing districts in Biella (wool), Como (silk), and Prato (recycled fibers) to command premium global export pricing. France at 16.4% benefits from Paris's fashion capital status, LVMH and Kering's global luxury demand generation, and investment in performance nonwovens and technical fabric production across key industrial regions.

Competitive Landscape

The Europe textile market is moderately fragmented, with global fashion conglomerates competing alongside specialist technical textile manufacturers and regional premium fabric producers.

|

Company Name |

Key Products |

Market Position |

Strategic Focus |

|

H&M Group |

Apparel, Activewear, Home Textiles |

Leader |

Circular fashion; garment collection; bio-based material adoption |

|

Coats Group plc |

Industrial Thread, Performance Fibers |

Leader |

Industrial thread leadership; performance application growth |

|

Kering |

Luxury Apparel, Leather, Silk Goods |

Leader |

Luxury sustainability; carbon-neutral collection targets |

|

Mango |

Fast-Premium Apparel, Accessories |

Challenger |

Mediterranean design identity; nearshoring supply chain |

|

Beaulieu International Group |

Flooring Textiles, Fibers and yarns, Polymers |

Challenger |

European flooring leadership; sustainable fibres & polymers portfolio |

Key players include H&M Group, Coats Group plc, Kering, Mango, Beaulieu International Group, and others.

Key Company Profiles

H&M Group

H&M Group, headquartered in Stockholm, Sweden, is one of the largest fashion retailers with stores and significant online operations. H&M has positioned sustainability as its core strategic differentiator, with the Conscious Collection and garment take-back program representing flagship circular economy initiatives.

- Product Portfolio: Apparel, activewear, home textiles, and others.

- Recent Developments: In March 2024, H&M Group, in partnership with Vargas Holding, announced the launch of Syre, a new venture focused on scaling textile-to-textile recycled polyester production. The initiative aims to accelerate the transition toward circular fashion manufacturing by reducing reliance on virgin polyester and expanding large-scale recycled textile solutions across the apparel industry.

- Strategic Focus: H&M's strategy focuses on transitioning to circular business models, scaling recycled and bio-based material sourcing to reduce virgin fiber dependence, and leveraging digital transparency tools to substantiate sustainability claims to increasingly regulation-aware European consumers and regulators.

Coats Group plc

Coats Group, headquartered in London, UK, is the world's one of the leading industrial thread manufacturer and a significant producer of performance materials, serving apparel, footwear, automotive, and specialty industrial applications.

- Product Portfolio: Industrial thread, performance fibers, and others.

- Strategic Focus: Coats' strategy focuses on deepening penetration in high-growth performance materials segments including composites and specialty industrial applications, while sustaining thread market share leadership through recycled content product development aligned with brand sustainability procurement commitments globally.

Market Concentration Analysis

The Europe textile market is moderately fragmented at the overall market level, with significant sub-segment concentration among national or regional specialists. The luxury segment shows higher concentration, with LVMH, Kering, and comparable conglomerates commanding disproportionate value share. Technical textile sub-segments demonstrate strong niche concentration, with Freudenberg, Trelleborg, and Ahlstrom-Munksjö holding dominant positions in specific application verticals.

Consolidation is progressing through two vectors: large fashion conglomerates acquiring heritage textile brands to deepen vertical integration, and private equity platforms aggregating regional technical textile specialists to achieve European distribution scale. EU sustainability regulations are accelerating consolidation as compliance investment requirements favor larger, better-capitalized operators over independent family-owned mills in traditional manufacturing regions.

Investment & Growth Opportunities

Fastest-Growing Segments

Nylon at ~5.8% CAGR through 2034 is the highest-growth product segment, driven by performance sportswear, activewear, and technical applications. Chemical fibers at ~5.2% CAGR represent the broadest-based synthetic growth opportunity. Smart textiles integrating biosensing, temperature regulation, and conductive properties are growing at above 10% CAGR from a smaller base, representing a premium opportunity for specialty manufacturers.

Emerging Growth Areas

Portugal and Romania are the fastest-growing manufacturing destinations within the European textile ecosystem, driven by nearshoring investment from Western European brands and expanding technical textile production capacity. Technical medical textiles, including wound care, surgical draping, and implantable textile-based devices, represent a high-value, regulatory-protected growth segment growing at 7-9% CAGR through 2034.

Venture & Investment Trends

Venture capital investment in textile-to-textile recycling technology reached EUR 1.2 Billion in Europe in 2023-2024, with multiple companies attracting institutional backing for enzymatic and chemical PET and cellulosic textile recycling platforms. Digital fashion and virtual textile sampling platforms, reducing physical sample production by up to 90%, are attracting growth equity investment targeting EU market sustainability compliance tools.

Future Market Outlook (2026-2034)

The Europe textile market is forecast to expand from USD 273.7 Billion in 2025 to USD 413.5 Billion by 2034 at a CAGR of 4.69%, adding USD 139.8 Billion in incremental annual market value over the forecast period. This sustained growth reflects alignment with EU Green Deal investment cycles, luxury consumer resilience, and technical textile demand expansion across multiple industrial verticals.

Three structural forces will most significantly shape the Europe textile industry landscape through 2034. EU mandatory textile EPR and separate collection requirements will transform waste textile volumes into recycled feedstock streams, enabling new circular business models and changing material sourcing economics fundamentally. Smart textile convergence with healthcare monitoring will open a regulated premium market segment of significant scale. Nearshoring expansion will redistribute European textile manufacturing geography toward Eastern European and North African proximity manufacturing hubs.

Research Methodology

Primary Research

Primary research encompassed over 45 structured interviews in 2024-2025 with Europe textile industry stakeholders, including senior commercial managers at major EU fashion brands, European Apparel and Textile Confederation (EURATEX) industry analysts, EU Green Deal textile policy advisors, and technical textile application engineers at automotive and healthcare OEMs. Primary data validated market sizing, segment shares, sustainability adoption timelines, and technology commercialization trajectories.

Secondary Research

Key secondary sources include EURATEX European Textile and Clothing Statistics (2020-2024), European Environment Agency textile waste data, European Commission EU Textile Strategy documentation, Eurostat industrial production indices, Textile Exchange Preferred Fiber and Materials Market Report (2024), ITC Trade Map bilateral textile trade statistics, Première Vision market trend reports, and trade publications including Textile World and Textile Outlook International.

Forecasting Models

Market size estimations and growth projections were derived using a combination of top-down and bottom-up forecasting models, incorporating EU GDP growth rates, consumer expenditure indices, regulatory investment timelines, sustainability adoption curves, and historical market evolution patterns across the 2020-2025 base period. Scenario analysis across base, optimistic, and conservative cases was performed to account for macroeconomic uncertainty throughout the forecast horizon.

Europe Textile Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Raw Materials Covered | Cotton, Chemical, Wool, Silk, Others |

| Products Covered | Natural Fibers, Polyesters, Nylon, Others |

| Applications Covered | Household, Technical, Fashion and Clothing, Others |

| Countries Covered | Germany, France, United Kingdom, Italy, Spain, Others |

| Companies Covered | H&M Group, Coats Group plc, Kering, Mango, Beaulieu International Group, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the Europe textile market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the Europe textile market.

- Porter's Five Forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the Europe textile industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Europe Textile Market Report

The Europe textile market reached USD 273.7 Billion in 2025, reflecting consistent demand from sustainable fashion adoption, technical textile expansion, and the robust presence of luxury fashion industries across Germany, Italy, France, and the United Kingdom.

The market is projected to reach USD 413.5 Billion by 2034, growing at a CAGR of 4.69% during 2026-2034, driven by EU sustainability regulation investment, circular economy adoption, performance textile growth, and nearshoring-led manufacturing expansion across Southern and Eastern Europe.

Germany leads the Europe textile market with a 20.7% share in 2025, driven by its world-class technical textile manufacturing excellence, automotive supplier base, and the strong presence of high-performance nonwovens and functional textile producers serving global industrial markets.

Cotton dominates with a 39.8% share in 2025, owing to its broad applicability across apparel, home textiles, and industrial uses, strong consumer preference for natural breathable fibers, and alignment with GOTS and OEKO-TEX sustainability certification frameworks widely adopted by European brands.

Key growth drivers include rising consumer demand for sustainable and eco-certified textiles, EU Green Deal and Textile Strategy regulatory momentum, expansion of technical and smart textile applications, digital transformation in textile printing and manufacturing, and the resilient growth of European luxury fashion and home textile exports to global high-net-worth consumer markets.

Key players include H&M Group, Coats Group plc, Kering, Mango, Beaulieu International Group, and others.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)