Food Flavors Market Size, Share, Trends and Forecast by Type, Form, End User, and Region, 2026-2034

Global Food Flavors Market Size, Share, Trends & Forecast (2026-2034)

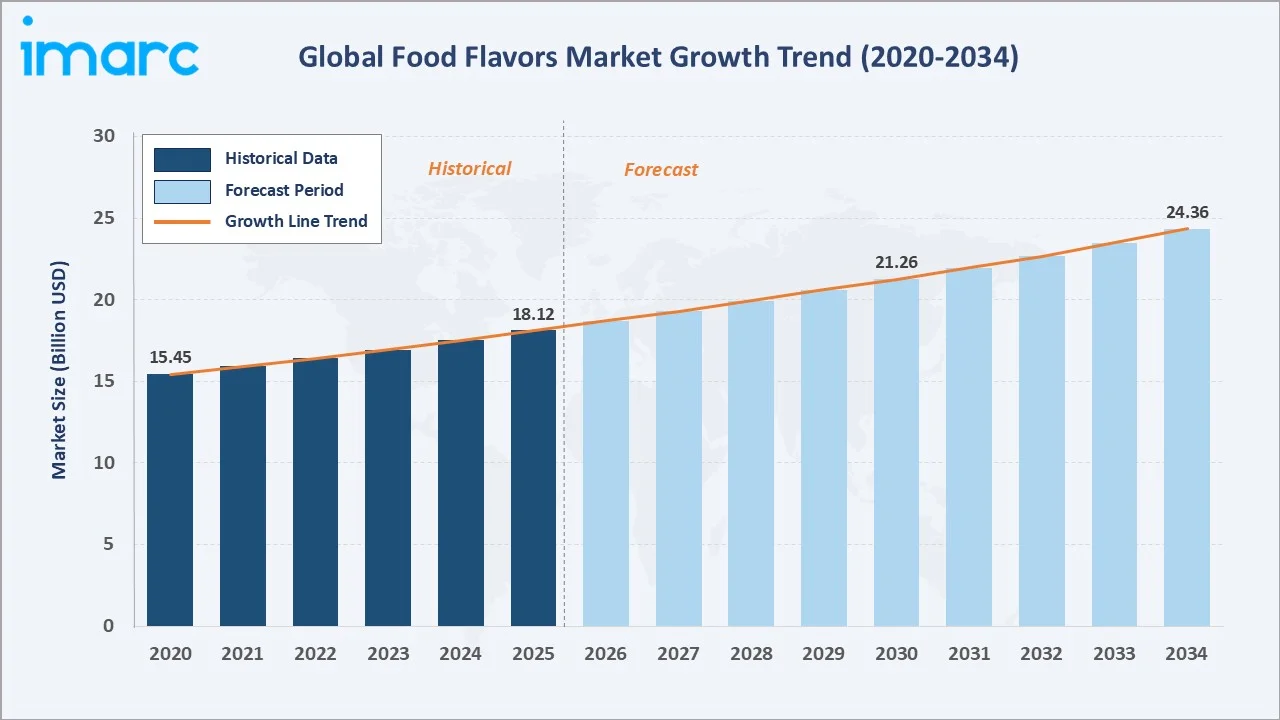

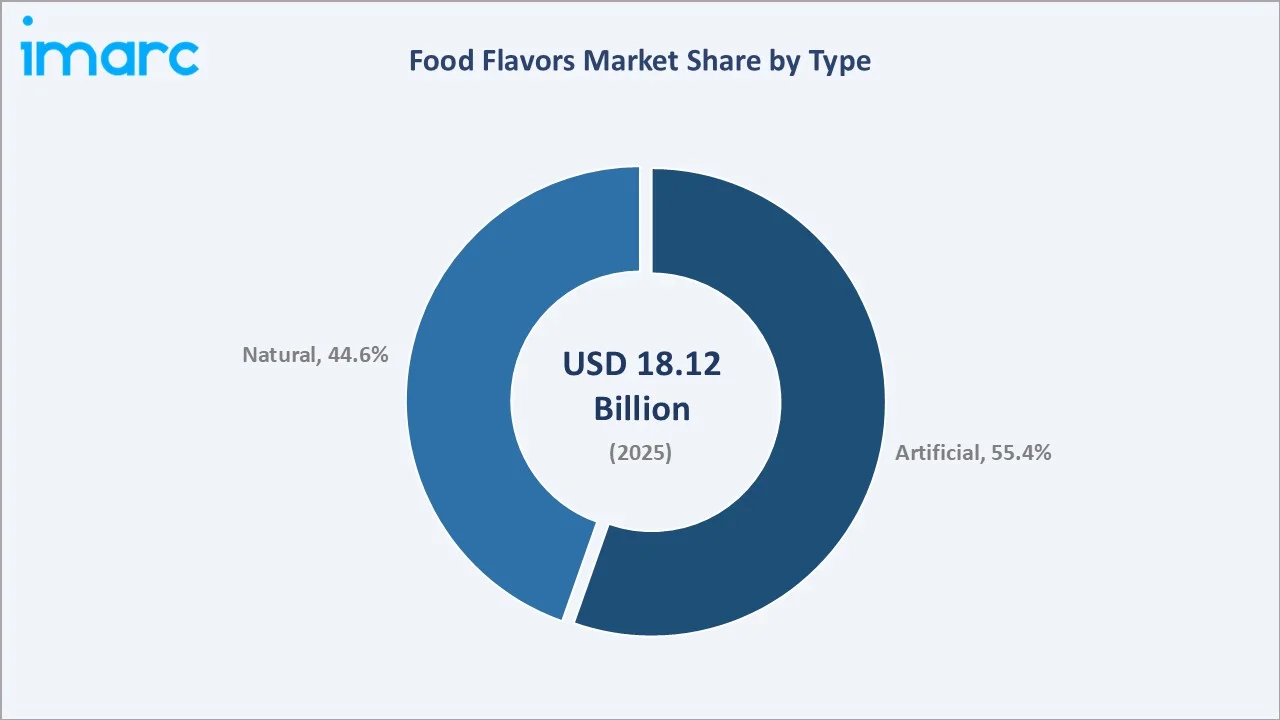

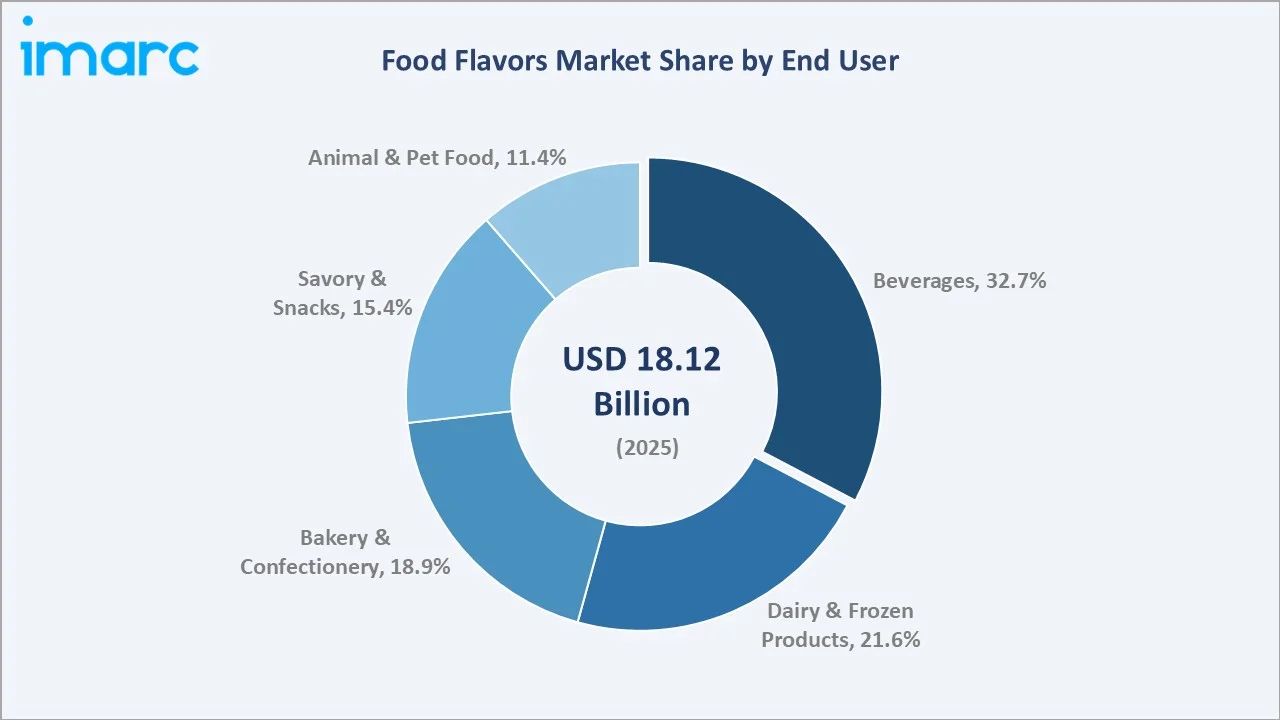

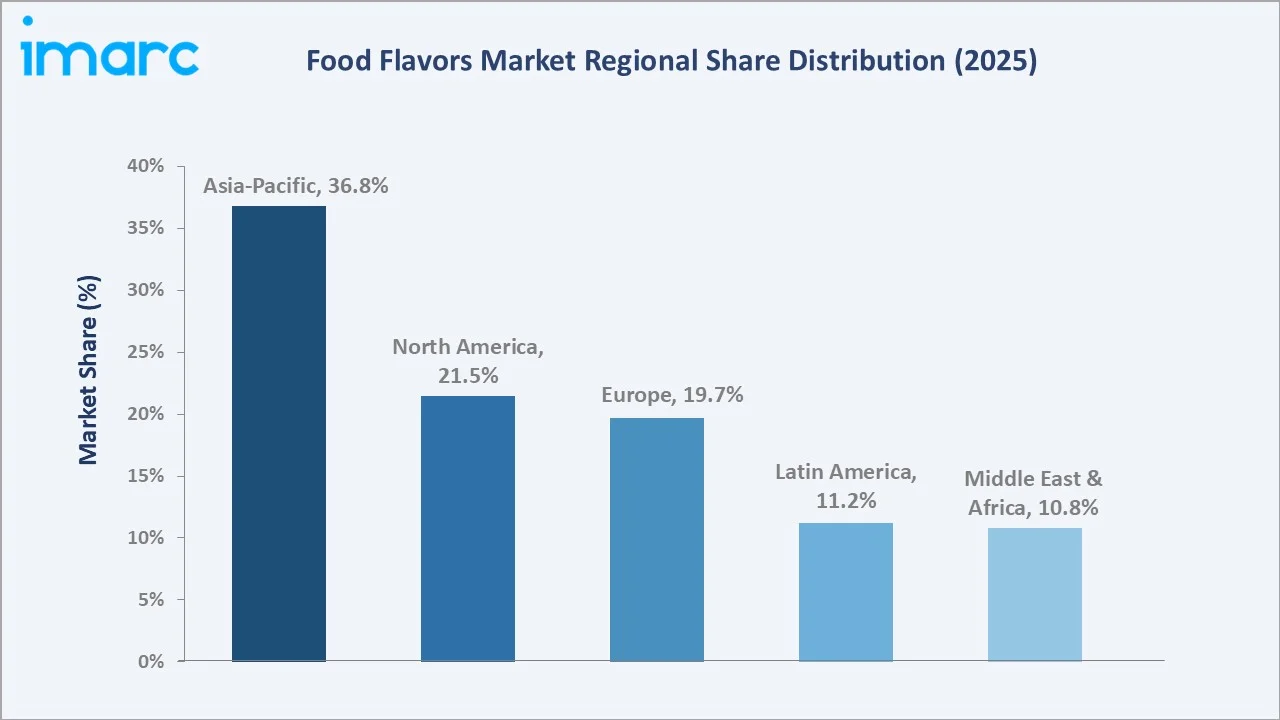

The global food flavors market size was valued at USD 18.12 Billion in 2025 and is projected to reach USD 24.36 Billion by 2034, exhibiting a CAGR of 3.24% during the forecast period 2026-2034. Rising consumer demand for diverse taste experiences, rapid expansion of the global processed food industry, and the surge in beverage innovation are key growth catalysts. Artificial flavors dominated in 2025 with a 55.4% share. Beverages led all end-user categories at 32.7% in 2025. Asia-Pacific holds the largest regional share at 36.8% in 2025.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 18.12 Billion |

|

Forecast Market Size (2034) |

USD 24.36 Billion |

|

CAGR (2026-2034) |

3.24% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

Asia-Pacific (36.8% share, 2025) |

|

Fastest Growing Region |

Asia-Pacific |

|

Largest Segment (by Type) |

Artificial (55.4%, 2025) |

|

Largest Segment (by End User) |

Beverages (32.7%, 2025) |

The global food flavors market growth trajectory from 2020 through 2034, contrasting historical expansion against a sustained forecast curve powered by processed food consumption growth, clean-label adoption, and expanding beverage industry investment across residential and commercial segments.

To get more information on this market, Request Sample

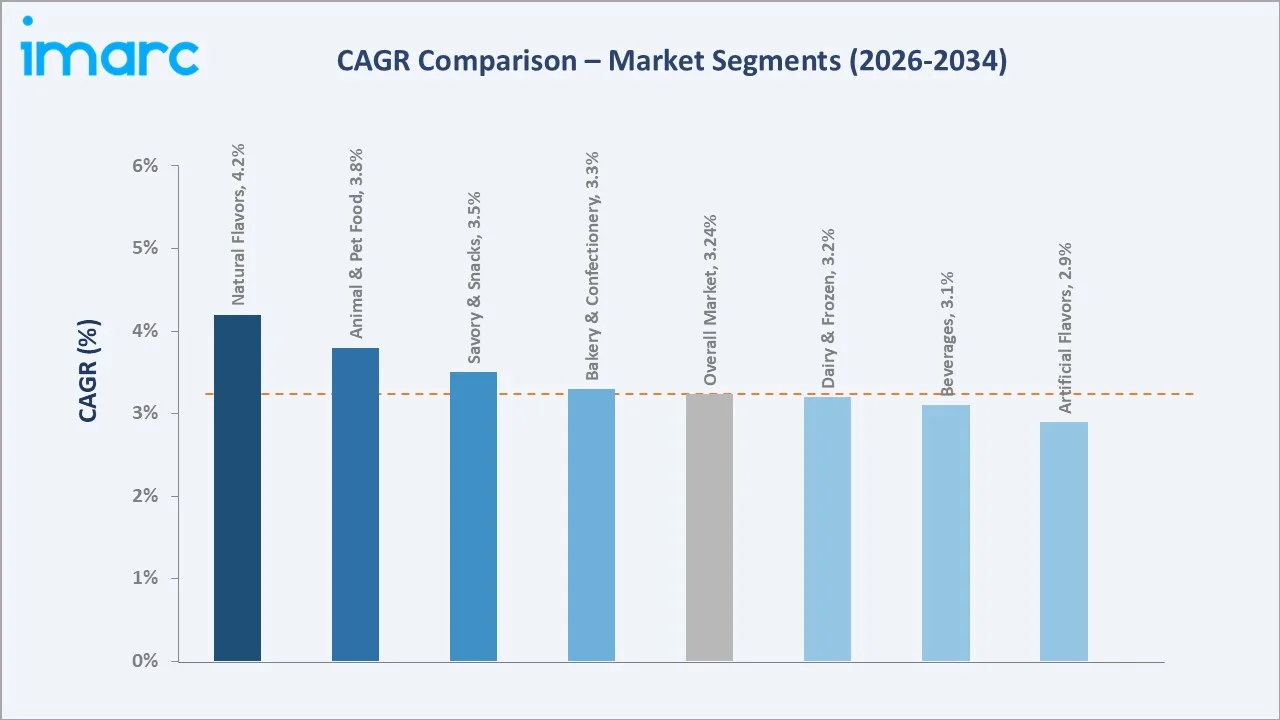

Segment-level CAGR comparisons highlighting natural flavor adoption and animal and pet food as the fastest-growing sub-categories within the global food flavors market forecast through 2034.

Executive Summary

The global food flavors market is undergoing a significant transformation, driven by clean-label consumer preferences, sustainability mandates, and rapid technological innovation. Valued at USD 18.12 Billion in 2025, the market is forecast to reach USD 24.36 Billion by 2034 at a CAGR of 3.24%. The market grew steadily from USD 15.45 Billion in 2020, reflecting a stable demand-led expansion across all major food and beverage end-use categories.

Artificial flavors command a 55.4% share in 2025, driven by cost efficiency and thermal stability in high-volume processed food manufacturing. The natural flavors segment holds 44.6% of global demand, with growth accelerating as regulatory pressure and consumer health awareness intensify. Beverages represent 32.7% of end-user demand in 2025, the single largest application category globally.

Asia-Pacific leads with 36.8% global revenue share in 2025. North America holds 21.5% and Europe 19.7%. The food flavors market outlook remains positive as fermentation-based natural flavor development, AI-assisted R&D, and functional food innovation converge across all major markets.

Key Market Insights

|

Insight |

Data |

|

Largest Segment (by Type) |

Artificial - 55.4% share (2025) |

|

Largest Segment (by End User) |

Beverages - 32.7% share (2025) |

|

Leading Region |

Asia-Pacific - 36.8% revenue share (2025) |

|

Fastest Growing Segment |

Natural Flavors - ~4.2% CAGR (2026-2034) |

|

Fastest Growing End User |

Animal & Pet Food - ~3.8% CAGR (2026-2034) |

|

Top Companies |

Givaudan, IFF, DSM-Firmenich, Symrise, Kerry Group |

|

Market Opportunity |

Functional & fermentation-based natural flavors |

Key Analytical Observations Supporting the Above Data:

- Artificial flavors' 55.4% dominance in 2025 reflects their 30-60% cost advantage over natural equivalents and superior performance in high-temperature food processing applications such as baked goods, snacks, and beverages.

- Natural flavors' 44.6% share is growing faster than artificial, driven by clean-label regulations in North America (FDA 21 CFR 101.22) and EU (Regulation EC 1334/2008), with over 55% of 2024 product launches carrying natural flavor declarations.

- Beverages' 32.7% end-use dominance is supported by over 18,00 new RTD and beverage SKU launches globally in 2024, each requiring differentiated flavor profiles across fruit, botanical, and functional categories.

- Asia-Pacific's 36.8% global leadership reflects China's USD 2.5 trillion food processing industry and India’s 1.2 trillion food processing Industry are creating the world's largest regional demand center for flavor compounds.

- Animal & pet food at 11.4% is the fastest-growing end-user sub-segment, propelled by the USD 132.5 billion global pet food market (2024) and the humanization trend driving demand for premium natural palatability enhancers.

- The global market will add over USD 6.24 billion in absolute revenue between 2025 and 2034, creating substantial investment opportunities in emerging markets and functional flavor technologies.

Global Food Flavors Market Overview

Food flavors are chemical substances - either naturally derived or synthetically produced - added to food and beverages to impart, modify, or enhance taste and aroma profiles. The global market encompasses a broad portfolio including natural extracts, essential oils, oleoresins, aroma chemicals, and spray-dried encapsulated flavors, serving virtually every food and beverage product category worldwide.

The industry operates at the convergence of food science, consumer behavior, regulatory compliance, and sustainable sourcing. Growth is supported by macroeconomic drivers such as rising disposable incomes fueling premiumization in food, rapid urbanization expanding processed food consumption in developing markets, and increasingly stringent regulations mandating clean-label and natural ingredient transparency. The market is simultaneously undergoing a structural shift toward biotechnology-derived and fermentation-based flavor production that is redefining innovation and cost structures globally.

Market Dynamics

To evaluate market opportunities, Request Sample

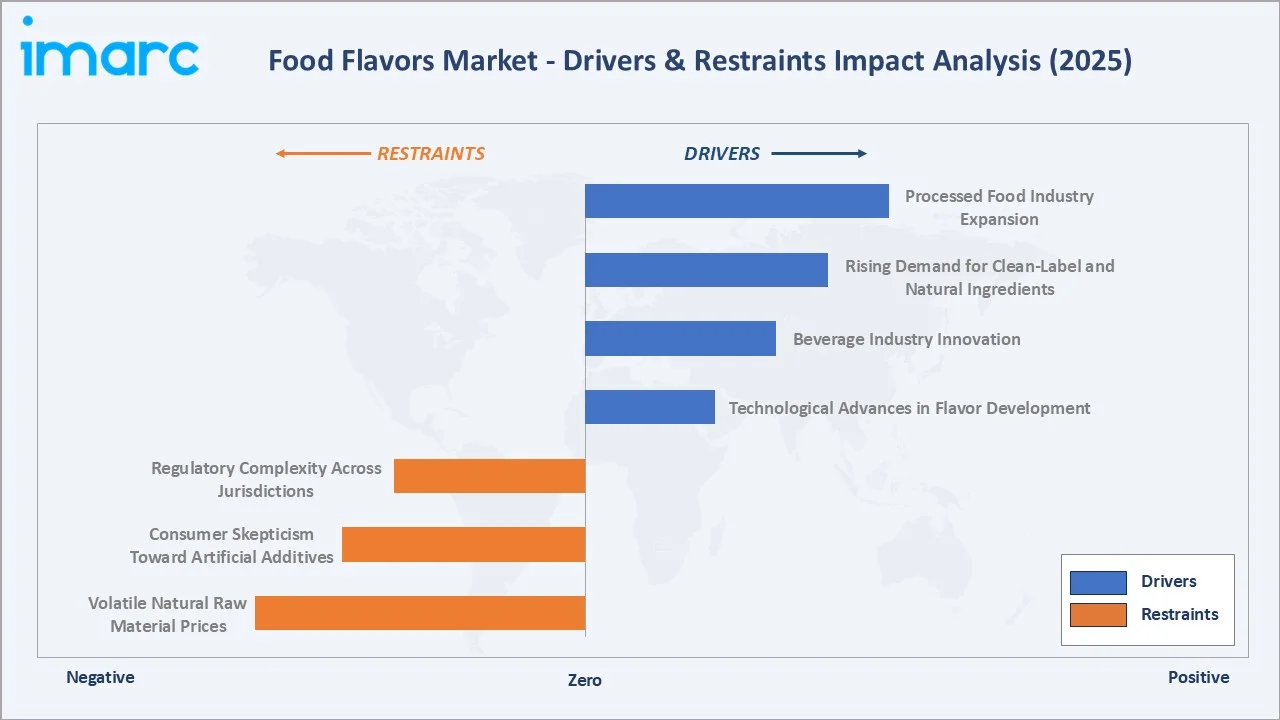

Market Drivers

- Processed Food Industry Expansion: The global processed food market surpassed USD 7.3 trillion in 2025, generating sustained demand for both artificial and natural flavor additives. Every packaged food SKU launch requires unique flavor differentiation, creating consistent volume demand across all flavor types.

- Rising Demand for Clean-Label and Natural Ingredients: Over 60% of consumers in North America and Europe actively seek natural ingredient labels in 2024. This shift is accelerating the transition from artificial to natural flavor systems across premium food and beverage segments.

- Beverage Industry Innovation: The global non-alcoholic beverage segment generated approximately USD 1.8 trillion in revenue in 2024, serving as the single largest consumer of food flavors. RTD tea, functional beverages, and energy drinks are the fastest-growing flavor-intensive sub-categories.

- Technological Advances in Flavor Development: AI-assisted flavor formulation and precision fermentation are reducing development timelines, enabling faster, more cost-efficient launches of differentiated flavor systems, particularly in natural and functional applications.

Market Restraints

- Regulatory Complexity Across Jurisdictions: Divergent flavor labeling and approval requirements between the US FDA, EU EFSA, and Asia-Pacific regulatory bodies create compliance costs that disproportionately affect small and mid-sized flavor manufacturers operating across regions.

- Volatile Natural Raw Material Prices: Key natural flavor raw materials including vanilla beans (price swings of 20-30% annually), citrus oils, and botanical extracts are subject to climate-related supply disruptions, creating significant margin pressure for natural flavor producers.

- Consumer Skepticism Toward Artificial Additives: Growing consumer backlash against synthetic ingredients in premium food segments is gradually eroding the market position of artificial flavors, compelling manufacturers to reformulate with natural alternatives at higher cost.

Market Opportunities

- Functional Flavor Development: The functional food and nutraceuticals market, valued at over USD 300 billion in 2024, requires sophisticated flavor masking for protein supplements, vitamins, and bioactive ingredients, creating high-margin specialty growth opportunities.

- Emerging Market Penetration: Latin America (11.2% share in 2025) and Middle East and Africa (10.8%) remain under-penetrated with rapidly expanding urban food processing sectors, offering significant volume growth potential for flavor manufacturers through 2034.

- Sustainable and Biotech-Derived Flavors: Fermentation‑focused alternative protein companies secured around USD 1.7 billion in investment in 2021, reflecting strong venture funding activity in fermentation technologies, including precision fermentation, is creating new market segments that qualify as "natural" under regulatory definitions while offering cost-competitive manufacturing.

Market Challenges

- Supply Chain Vulnerabilities: Climate change-related disruptions to natural flavor raw material supply chains - including Madagascar vanilla, Brazilian citrus, and Indian spice crops - pose ongoing procurement risk and traceability challenges for ingredient-transparent brands.

- Intense Competitive Fragmentation: With over 400 flavor manufacturers operating globally, the market exhibits significant price competition in commodity flavor segments, compressing margins for mid-sized producers without differentiated technology platforms.

- Shelf-Life Limitations of Natural Formulations: Natural flavor formulations often exhibit shorter shelf lives compared to artificial counterparts, limiting adoption in long-shelf-life product categories such as canned goods, shelf-stable snacks, and military rations.

Emerging Market Trends

1. Clean-Label and Natural Flavor Transition

Consumer demand for transparent ingredient declarations is fundamentally reshaping flavor portfolios globally. Most of new food product launches in 2024 carried natural flavor declarations. This is compelling manufacturers to invest in botanical extraction, enzymatic production, and fermentation-based natural flavor development at commercial scale.

2. Precision Fermentation-Based Flavor Production

Precision fermentation is emerging as a transformative technology, enabling bio-identical production of complex flavor compounds such as vanillin, dairy notes, and meat analogs without traditional plant or animal extraction. Givaudan has significantly expanded its biotechnology and fermentation capabilities to support the development of sustainable flavor and ingredient technologies, including dedicated innovation platforms and new biotech R&D centers.

3. AI-Driven Flavor Innovation

Artificial intelligence platforms are accelerating flavor R&D by predicting consumer acceptance with over 85% accuracy in controlled trials. International Flavors & Fragrances (IFF) actively leverages AI‑driven formulation and predictive modeling tools to accelerate flavor development, aiming to reduce development time and improve efficiency in bringing new taste solutions to market. Symrise's AI-powered PHILINE platform and Givaudan's digital sensory tools are setting new industry benchmarks for development efficiency.

4. Functional and Bioactive Flavor Systems

Flavors with dual functionality - masking off-notes in protein-enriched foods while contributing health benefits - are gaining significant traction. The global protein supplement market, valued at USD 30 billion in 2025, is driving demand for sophisticated bitterness masking and sweetness modulation systems, with applications expanding into functional beverages and fortified dairy.

5. Regional and Exotic Flavor Profiles

Globalization of culinary culture is driving demand for Korean, Middle Eastern, African, and Southeast Asian flavor profiles in Western food and beverage markets. Over 1,800 new products featuring regional flavor themes launched globally in 2024, representing a 22% year-on-year increase. Key growth flavors include yuzu, gochujang, sumac, tamarind, and pandan extracts.

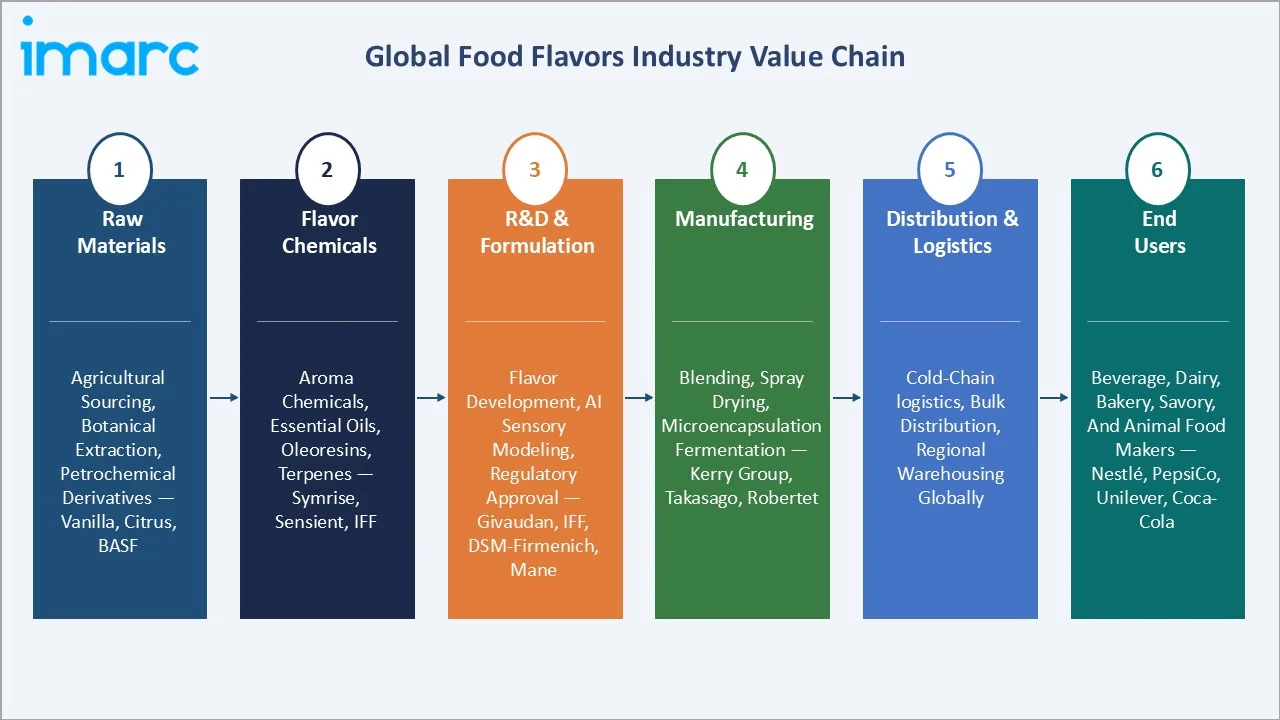

Industry Value Chain Analysis

|

Stage |

Key Activities |

Key Players / Examples |

|

Raw Materials |

Agricultural sourcing, botanical extraction, petrochemical derivatives |

Vanilla farmers (Madagascar), Citrus growers (Brazil, Spain), BASF SE |

|

Flavor Chemicals |

Synthesis of aroma chemicals, essential oils, oleoresins, terpenes |

Symrise , Sensient Technologies, International Flavors & Fragrances Inc |

|

R&D & Formulation |

Flavor development, AI sensory modeling, regulatory approval, encapsulation design |

Givaudan, IFF, DSM-Firmenich, Mane SA |

|

Manufacturing |

Blending, spray drying, microencapsulation, fermentation production |

Kerry Group, Takasago International Corporation, Robertet Group |

|

Distribution & Logistics |

Cold-chain logistics, bulk distribution, regional warehousing globally |

Regional distributors across North America, Europe, Asia-Pacific |

|

End Users |

Beverage, dairy, bakery, savory, and animal food manufacturers |

Nestle, PepsiCo, Unilever, Coca-Cola, General Mills, Mars |

Technology Landscape in the Food Flavors Industry

Biotechnology and Precision Fermentation

Precision fermentation and enzymatic bioconversion are enabling commercial-scale production of complex flavor compounds at costs competitive with synthetic manufacturing while qualifying as "natural" under US and EU regulations. Givaudan's EverNatural platform and Evolva's fermentation-derived vanillin are commercial benchmarks.

Microencapsulation and Controlled Release

Encapsulation technologies - including spray drying, fluid bed coating, and coacervation - improve flavor stability, mask off-notes, and enable controlled release in high-temperature processed foods. The global flavor encapsulation market is estimated at USD 3.6 billion in 2025, growing at approximately 5% CAGR through 2030. Leading technologies include cyclodextrin inclusion complexes and lipid-based microencapsulation systems.

AI and Machine Learning in Flavor R&D

AI platforms analyzing vast sensory databases predict consumer acceptance of new flavor profiles with good accuracy. Symrise's PHILINE platform and IFF's Jafra digital tools are reducing R&D cycle times and formulation costs significantly. AI is particularly impactful in bitterness masking, sweetness modulation, and cross-cultural flavor adaptation for global product launches.

Green Chemistry and Sustainable Extraction

Supercritical CO2 extraction, cold-press processes, and solvent-free techniques are producing premium natural flavor extracts with higher purity and superior sensory profiles, supporting the clean-label trend. These technologies also reduce environmental impact, aligning with corporate sustainability commitments and ESG-linked procurement requirements.

Market Segmentation Analysis

The report covers the following segments:

| Segment Category | Leading Segment | Market Share | Year |

|---|---|---|---|

| Type | Artificial | 55.4% | 2025 |

| Form | 🔒 | 🔒 | 2025 |

| End User | Beverages | 32.7% | 2025 |

| Region | Asia-Pacific | 36.8% | 2025 |

Market Breakup by Type

To access detailed market analysis, Request Sample

The food flavors market is segmented by type into artificial and natural flavors. Each segment exhibits distinct demand dynamics driven by regulatory, cost, and consumer preference factors across different food and beverage application categories.

|

Segment |

Market Share (2025) |

Key Drivers |

Outlook |

|

Artificial |

55.4% |

Cost efficiency, heat stability, wide application range in processed foods |

Stable; faces gradual pressure in premium segments from natural transition |

|

Natural |

44.6% |

Clean-label trend, regulatory support, consumer health preferences globally |

Faster growth; projected to gain share through 2034 at 4.2% CAGR |

Artificial flavors maintained a 55.4% share in 2025. Their cost advantage - typically cheaper than natural equivalents - and superior thermal stability make them the preferred choice in baked goods, snacks, and carbonated beverage applications. Manufacturers such as Givaudan and IFF continue to invest in high-performance artificial flavor systems for savory, snack, and beverage segments with demanding processing conditions.

Natural flavors, capturing 44.6% of the 2025 market, are driven by the global clean-label revolution and regulatory alignment. In North America, FDA's definition of "natural flavor" (21 CFR 101.22) supports a broad product range. Europe's stricter Regulation EC 1334/2008 is pushing investment in genuine botanical extracts. Key players including Firmenich, Mane SA, and Robertet Group source directly from farming communities, building supply chain traceability critical for premium brand positioning.

Market Breakup by End User

End-user segmentation reveals beverages as the clear demand leader, followed by dairy and frozen products, bakery and confectionery, savory and snacks, and animal and pet food. Together these five categories represent the complete 2025 market.

|

End-Use Segment |

Market Share (2025) |

Key Applications |

Key Trend |

|

Beverages |

32.7% |

Carbonated drinks, energy drinks, RTD tea/coffee, juices |

Sugar reduction masking; natural citrus flavors |

|

Dairy & Frozen Products |

21.6% |

Ice cream, yogurt, cheese, frozen desserts |

Exotic fruit profiles; reduced-sugar formulations |

|

Bakery & Confectionery |

18.9% |

Bread, cakes, chocolates, gums, hard candies |

Clean-label bakery; natural vanilla demand surge |

|

Savory & Snacks |

15.4% |

Chips, crackers, seasonings, sauces, marinades |

Ethnic flavor profiles; umami and fermented notes |

|

Animal & Pet Food |

11.4% |

Palatability enhancers, kibble coatings, treats |

Pet humanization; premium natural meat flavors |

The beverages segment, at 32.7% in 2025, is the dominant end-use category globally. RTD beverage launches exceeded 18,00 SKUs globally in 2024, each requiring unique flavor differentiation. Energy drink brands including Red Bull, Monster, and emerging Asian RTD brands are expanding flavor portfolios rapidly, driving volume demand for tropical, botanical, and functional flavor systems.

Dairy and frozen products captured 21.6% of the 2025 market. The global ice cream market, valued at approximately USD 121.35 billion in 2024, represents a large and stable flavor demand base. The trend toward artisanal and exotic ice cream profiles including matcha, black sesame, and lavender is opening premium flavor opportunities that command higher margins compared to standard vanilla and chocolate applications.

Regional Market Insights

|

Region |

Market Share (2025) |

Key Drivers |

|

Asia-Pacific |

36.8% |

Rapid food processing expansion; urbanization; rising middle-class consumption |

|

North America |

21.5% |

Clean-label demand; beverage innovation; strong R&D infrastructure |

|

Europe |

19.7% |

Regulatory push for natural flavors; premium food culture; sustainability |

|

Latin America |

11.2% |

Growing processed food sector; expanding beverage industry in Brazil, Mexico |

|

Middle East & Africa |

10.8% |

Halal food growth; food processing investment in UAE, Saudi Arabia |

Asia-Pacific (36.8%)

Asia-Pacific is the world's largest food flavors market by regional share. China's USD 2.5 trillion food processing industry and India’s 1.2 trillion food processing Industry, generates the highest single-country flavor demand. Southeast Asian nations are rapidly expanding domestic food manufacturing capacity, with ASEAN food processing investment exceeding USD 37 billion in 2025.

North America (21.5%)

North America is characterized by high per-capita flavor consumption and a mature regulatory framework. The US accounts for over 85% of regional demand. Natural flavor sales in the US is growing rapidly every year. Craft beverage innovation and the functional food sector are key growth drivers.

Europe (19.7%)

Europe's market is shaped by strict EU flavor regulations and a strong tradition of premium food culture. Germany, France, and the UK are the three largest national markets. The region shows the highest demand for authentic natural flavors and regional culinary heritage profiles. Robertet Group and Givaudan's European operations are leading investment in sustainable, traceable flavor sourcing.

Latin America (11.2%)

Latin America represents a growing opportunity market. Brazil and Mexico account for approximately 70% of regional demand. The expansion of modern retail and quick-service restaurant chains is driving processed food consumption. Tropical fruit flavors - guava, passion fruit, and acai - are distinctive high-growth sub-segments unique to this region's flavor demand profile.

Middle East & Africa (10.8%)

The region is growing driven by halal food certification requirements and rising food processing investments under Saudi Arabia's Vision 2030 initiative and UAE food security programs. Plant-derived and spice-based flavor compounds represent distinctive regional high-growth opportunities.

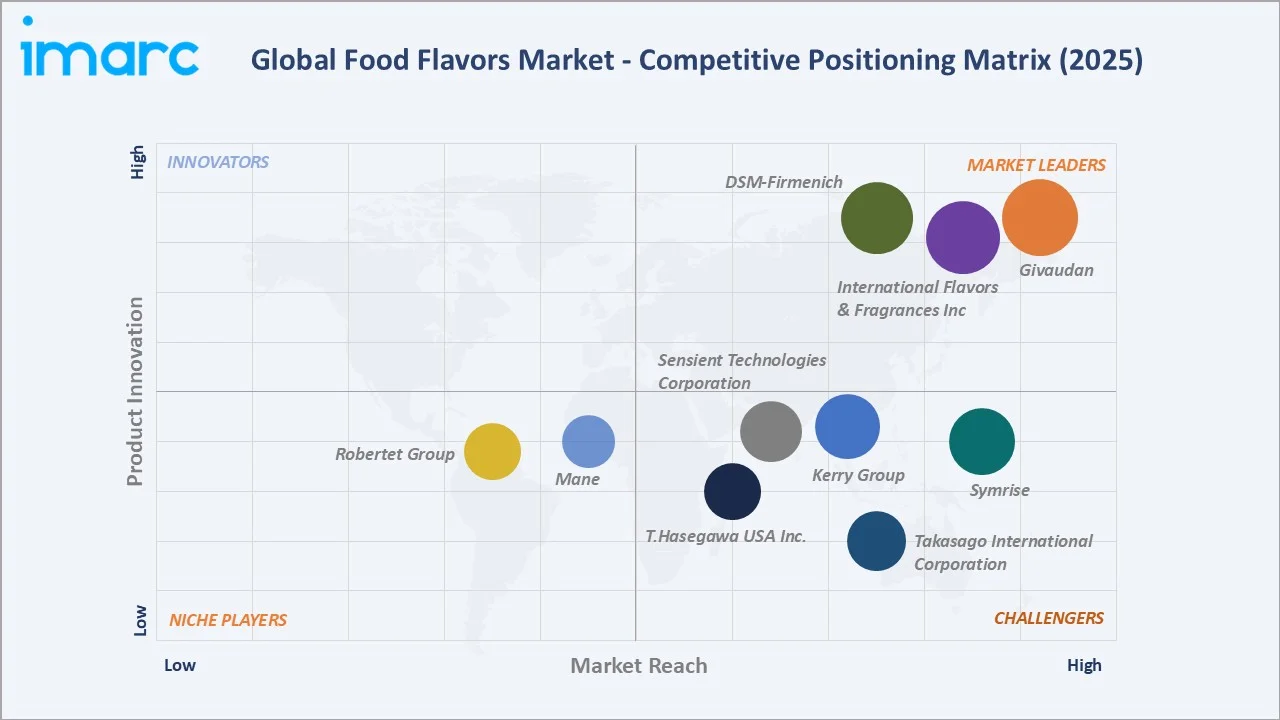

Competitive Landscape

|

Parent Company |

Brand / Division |

Market Position |

Core Strength |

|

Givaudan |

Taste Wellbeing |

Leader |

World’s largest flavor and fragrance house with deep R&D investment, broad portfolio across food, beverage and sensory experiences, strong natural and sustainable solutions. |

|

International Flavors & Fragrances Inc |

IFF |

Leader |

Comprehensive flavor innovation with technology-enabled solutions, decades of taste expertise and global footprint across food, beverage, and nutrition. |

|

DSM-Firmenich |

DSM-Firmenich |

Leader |

Combined strength from DSM and Firmenich merger — innovation across nutrition, health and flavors with large R&D and sustainability focus. |

|

Symrise |

Symrise |

Challenger |

Strong global presence with sustainability‑led product lines, diversified taste and nutrition solutions, and innovation network. |

|

Kerry Group plc |

Kerry Taste |

Challenger |

Global taste & nutrition leader focused on healthy, clean‑label innovations, functional ingredients and sensory solutions. |

|

Sensient Technologies Corporation |

Sensient flavors and extracts |

Challenger |

Custom flavor and ingredient solutions with strong specialty portfolio across food, beverage, bakery and natural segments. |

|

Takasago International Corporation |

Takasago Flavors |

Challenger |

Long-standing expertise in flavor and fragrance creation; global network across 28 countries; strong R&D in sensory solutions and aroma ingredients; tailored solutions for diverse industries like food, beverage, and personal care. |

|

Mane |

Mane Flavors |

Niche |

Long history of sensory expertise with strengths in natural flavors and tailored taste innovations for diverse markets. |

|

Robertet Group |

Robertet Flavors |

Niche |

Specialist in natural raw materials and flavors with strong heritage, sustainability focus, and artisanal sensory excellence. |

|

T.Hasegawa USA Inc. |

T.Hasegawa Flavors |

Challenger |

Century‑old custom flavor innovator prioritizing creative, technical flavor solutions for global food and beverage brands. |

Key Company Profiles

Givaudan

Givaudan is the world's largest flavor and fragrance company, with annual sales exceeding CHF 7.4 billion in 2024. The Flavor & Beverage and Food & Dairy divisions cover taste, texture, and nutrition solutions for leading global food brands. Recent developments include a strategic partnership with Chr. Hansen to expand fermentation-based natural flavor capabilities. The EverNatural platform targets fast-growing natural and functional flavor segments. Strategic focus: sustainability, biotechnology, and digital consumer insights.

International Flavors & Fragrances Inc (IFF)

IFF is a global leader with USD 11.8 billion in revenue in 2023 following its merger with DuPont Nutrition & Biosciences. The Nourish division focuses on flavor and texture solutions for food and beverage manufacturers. In 2024, IFF launched several AI-developed flavor systems for the plant-based protein and RTD beverage sectors. The company operates 38 manufacturing sites globally. Strategic focus: AI-driven product development, natural flavors, and portfolio optimization.

DSM-Firmenich

Following the merger with Royal DSM in 2023, DSM-Firmenich became a major force in taste, nutrition, and health. The flavors division provides solutions across beverages, dairy, savory, and confectionery. The MastiX bitterness masking technology platform is an industry benchmark. Strategic focus: naturals, health and wellness innovation, and sustainable flavor sourcing.

Market Concentration Analysis

The global food flavors market exhibits a moderately fragmented structure. The top five players - Givaudan, IFF, DSM-Firmenich, Symrise, and Kerry Group - reflecting a semi-consolidated competitive environment with significant share remaining among hundreds of regional specialists.

Consolidation trends are clearly evident across the sector. Between 2019 and 2024, the flavor and fragrance industry witnessed over 35 notable mergers and acquisitions. DSM-Firmenich's 2023 merger, IFF's acquisition of DuPont Nutrition and Biosciences, and Kerry Group's continuous bolt-on acquisition strategy all underscore industry consolidation direction.

Investment & Growth Opportunities

Fastest Growing Segments

- Natural Flavors: Projected to grow at a CAGR of approximately 4.5-5% through 2034, outpacing the overall market rate of 3.24%. The segment is driven by clean-label product proliferation globally and regulatory incentives for plant-based and fermentation-derived flavor compounds.

- Functional Flavor Masking: Demand from the USD 300+ billion functional food market for bitterness masking and taste modulation represents a high-margin specialty growth segment with limited competition from commodity flavor suppliers.

- Pet Food Flavors: The global pet food market, valued at USD 148 billion in 2024 and growing at approximately 5% annually, is driving premium demand for natural meat-analog and palatability flavor systems in the rapidly expanding humanized pet nutrition segment.

Emerging Markets

- India: India's packaged food sector is expanding, with urban consumers driving demand for international and regional flavor profiles. India represents one of the highest individual-country growth markets within Asia-Pacific through 2034.

- Southeast Asia: Combined ASEAN food processing investment exceeded USD 37 billion in 2023-2024, creating significant flavor demand across beverage, dairy, and snack categories. Indonesia, Vietnam, and the Philippines are the three fastest-growing sub-markets within the region.

- Saudi Arabia & UAE: Food security initiatives under Saudi Vision 2030 and the UAE National Food Security Strategy are driving domestic food processing capacity investments, creating new halal-certified flavor demand centers within Middle East and Africa.

Venture Investment Trends

Global investment in food technology, including flavor biotechnology, exceeded USD 15 billion in 2023. Precision fermentation start-ups targeting vanillin, saffron analog, and botanical flavor compounds. Corporate venture arms of Givaudan, IFF, and Firmenich are actively scouting biotech flavor companies in Israel, the US, and Singapore for acquisition and partnership.

Future Market Outlook (2026-2034)

The global food flavors market is projected to grow from USD 18.12 billion in 2025 to USD 24.36 billion by 2034, at a CAGR of 3.24% during 2026-2034. This trajectory is underpinned by steady growth across all major end-use categories and geographies, with urbanization, processed food expansion, and clean-label adoption as the three primary structural demand drivers.

Technological disruptions in precision fermentation and AI-assisted flavor development will reshape cost structures and innovation timelines through the forecast period. Natural flavor cost parity with artificial equivalents in key compounds, expected by approximately 2030, will be a transformative development potentially accelerating the natural segment's market share gain beyond current projections of 44.6% in 2025.

Asia-Pacific will maintain its position as the dominant regional market through 2034, with its share potentially expanding from 36.8% in 2025 to approximately 39-40% by 2034. Latin America and the Middle East and Africa will demonstrate above-average growth rates as food processing infrastructure continues to develop, supported by government food security initiatives and rising urban food consumption.

Research Methodology

Primary Research

Primary research comprised in-depth interviews and structured surveys with over 150 industry stakeholders including flavor chemists, R&D directors, procurement managers, and marketing executives at leading food and beverage manufacturers during 2024-2025. Interviews were conducted across North America, Europe, Asia-Pacific, and Latin America, with cross-validation of market share data and regional demand estimates against practitioner-sourced intelligence.

Secondary Research

Secondary research encompassed over 500 data sources including annual reports of publicly listed flavor companies, trade publications (Perfumer & Flavorist, Food Technology), regulatory databases (FDA, EFSA, FSANZ), patent databases, and industry association reports from the International Organization of the Flavor Industry (IOFI) and the Flavor and Extract Manufacturers Association (FEMA).

Forecasting Models

Market estimates were developed using both bottom-up and top-down forecasting approaches. Bottom-up methodology aggregated end-use demand across five application categories and five regions. Econometric modeling incorporated GDP growth rates, food expenditure elasticities, and processing sector capacity expansion indices. Monte Carlo simulation was applied to generate CAGR confidence intervals and probability-weighted market size ranges.

Food Flavors Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Types Covered | Natural, Artificial |

| Forms Covered | Dry, Liquid |

| End Users Covered | Beverages, Dairy and Frozen Products, Bakery and Confectionery, Savory and Snacks, Animal and Pet Food |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | Givaudan, International Flavors & Fragrances Inc, DSM-Firmenich, Symrise, Kerry Group plc, Sensient Technologies Corporation, Takasago International Corporation, Mane, Robertet Group, T.Hasegawa USA Inc., etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the food flavors market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the global food flavors market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's five forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the food flavors industry and its attractiveness.

- The competitive landscape allows stakeholders to understand their competitive environment and provides insight into the current positions of key players in the market.

Frequently Asked Questions About the Food Flavors Market Report

The global food flavors market was valued at USD 18.12 Billion in 2025 and is forecast to reach USD 24.36 Billion by 2034, growing at a CAGR of 3.24% during 2026-2034.

Primary drivers include rising processed food consumption, clean-label and natural ingredient trends, beverage industry innovation, and AI-driven flavor development advances in precision fermentation technology.

Artificial flavors dominated in 2025 with a 55.4% share due to cost advantages and thermal stability. Natural flavors at 44.6% are growing faster, driven by clean-label consumer demand globally.

Beverages held the largest end-user share at 32.7% in 2025. Dairy and frozen products ranked second at 21.6%, followed by bakery and confectionery at 18.9% of total market demand.

Asia-Pacific leads with a 36.8% market share in 2025, backed by large-scale food processing industries in China, India, and Southeast Asia. North America follows with a 21.5% share.

The food flavors market is projected to reach USD 24.36 Billion by 2034, up from USD 18.12 Billion in 2025, representing absolute revenue growth of approximately USD 6.24 Billion over the forecast period.

Key players include Givaudan, IFF, DSM-Firmenich, Symrise AG, Kerry Group, Sensient Technologies, Takasago International, Mane SA, Robertet Group, and T.Hasegawa USA Inc.

The food flavors market is projected to grow at a CAGR of 3.24% during 2026-2034, with natural flavors and animal and pet food applications growing at above-average segment rates.

Key challenges include regulatory complexity, volatile natural raw material prices, supply chain vulnerabilities for botanical ingredients, and growing consumer backlash against artificial food additives.

Natural flavors accounted for 44.6% of the total food flavors market in 2025, translating to approximately USD 8.08 billion, with projected faster-than-market growth through 2034.

AI platforms reduce flavor development cycle times by 30-40%, predict consumer acceptance with over 85% accuracy. IFF, Symrise, and Givaudan have deployed production-scale AI flavor development tools.

Asia-Pacific represented approximately USD 6.67 Billion of the global food flavors market in 2025 at a 36.8% share, expected to reach approximately USD 9.5 Billion by 2034.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)