GCC Personal Luxury Goods Market Report by Type (Accessories, Apparel, Watch and Jewellery, Luxury Cosmetics, and Others), Gender (Female, Male), Distribution Channel (Mono-brand Stores, Specialty Stores, Departmental Stores, Online Stores, and Others), and Country 2026-2034

Market Overview:

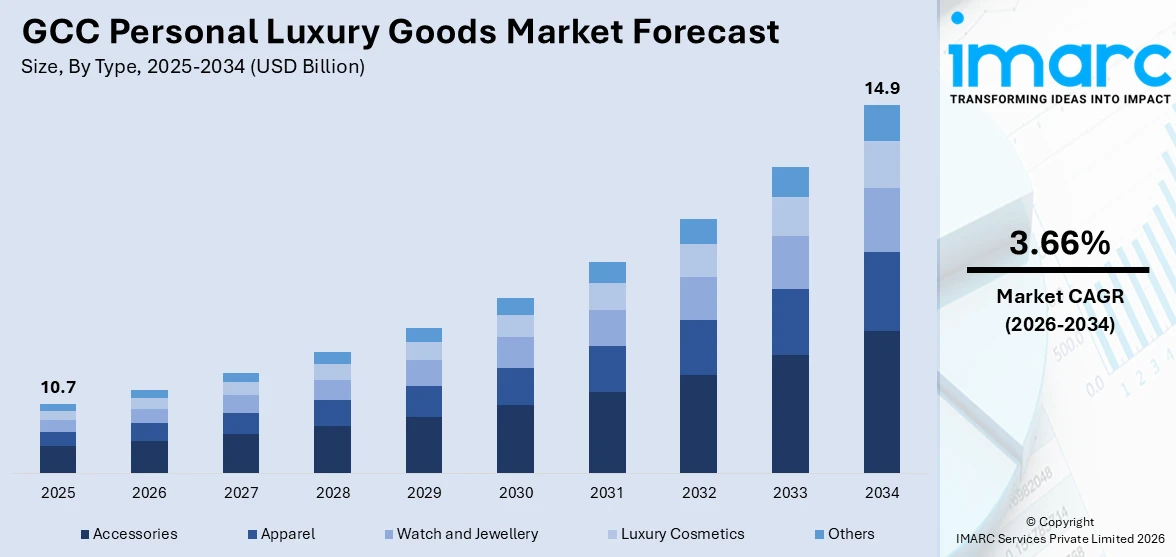

The GCC personal luxury goods market size reached USD 10.7 Billion in 2025. The market is projected to reach USD 14.9 Billion by 2034, exhibiting a growth rate (CAGR) of 3.66% during 2026-2034. The demand for personal luxury goods in the GCC region is rising due to increasing disposable incomes and the growing young population. Cultural affinity for high-end fashion, rising tourism activities, and expanding retail infrastructure are further supporting the market growth, making the GCC a key destination for luxury goods usage and brand expansion.

|

Report Attribute

|

Key Statistics

|

|---|---|

|

Base Year

|

2025 |

|

Forecast Years

|

2026-2034 |

|

Historical Years

|

2020-2025

|

| Market Size in 2025 | USD 10.7 Billion |

| Market Forecast in 2034 | USD 14.9 Billion |

| Market Growth Rate 2026-2034 | 3.66% |

Personal luxury goods refer to the high-end and premium items, including apparel, watches, jewelry, cosmetics, bags, fashion accessories, etc. These branded products offer premium quality materials, superior craftsmanship, and high-value aesthetics. Most of the personal luxury goods are highly durable with extended warranty period, thereby being heavily priced. In the GCC region, rapid globalization along with the wide presence of international luxury brands is currently bolstering the market growth.

To get more information on this market Request Sample

The rising consumer living standards supported by their increasing disposable income levels are augmenting the sales of personal luxury goods in the GCC region. Moreover, the high prevalence of western fashion trends coupled with the rising working women population is also catalyzing the product demand. The expanding tourism sector, particularly in Dubai and UAE, along with the relaxed trade barriers with several developed countries, is also driving the market growth. For instance, the GCC member states signed the European Free Trade Agreement (EFTA), allowing the trade of personal luxury goods from countries like Italy and France. Besides this, the wide availability of personal luxury goods on online retail platforms is also propelling the market growth in the region. The growing number of celebrity endorsements and the high prevalence of social media marketing are also driving the demand of personnel luxury goods in the region. Apart from this, the rising popularity of limited capsule collections and fashion drops have also fueled the market for secondhand luxury goods. Moreover, various personal luxury platforms are increasingly investing in authentication procedures and quality checks for providing a safe and reliable environment for customers. Several innovative technologies are being adopted to maintain brand value and minimize the risk of product replication by counterfeiters.

The sudden outbreak of COVID-19 across the GCC region in early 2020 has negatively impacted the growth of the personal luxury goods market.

GCC Personal Luxury Goods Market Trends:

Rising young population

The growing young population is offering a favorable market outlook in the GCC region. According to the 2024 Saudi Family Statistics Report by the General Authority for Statistics (GASTAT), approximately 71% of Saudi Arabia's population was younger than 35 years old. This demographic shows a strong preference for high-end fashion, accessories, and beauty products as expressions of individuality and social status. Many young users in the region benefit from relatively high disposable incomes, allowing them to spend freely on luxury goods. Additionally, the region’s youth often view luxury items not only as lifestyle choices but also as status symbols. Their enthusiasm for shopping, both online and in luxury malls, continues to reshape demand patterns and encourages brands to target this influential user group.

Growing tourism activities

Increasing tourism activities are fueling the market growth in the GCC region. As per the Qatar Tourism Reports, during the first half of 2025, Qatar attracted 2.6 Million international visitors. Tourists, especially from high-spending countries, are drawn to the region’s luxury malls, tax-free shopping, and world-renowned hospitality. Cities like Dubai, Abu Dhabi, and Doha have become global retail destinations where international visitors seek premium fashion, jewelry, watches, and perfumes. The presence of flagship stores of luxury brands in these cities caters directly to tourist demand. High-end shopping is often part of travel itineraries, with luxury purchases serving as souvenirs or personal indulgences. Additionally, events like shopping festivals and tourism campaigns aid in attracting international visitors, who are contributing significantly to sales in the luxury sector. The growing footfall from tourists continues to generate new opportunities for numerous luxury brands operating in the GCC region.

Increasing digital influence

Rising digital influence is significantly bolstering the growth of the market in the GCC region. With increasing internet penetration and widespread use of social media platforms, people are becoming more aware about global fashion trends, luxury brands, and celebrity endorsements. As per the datareportal, at the beginning of 2024, the UAE recorded 9.46 Million internet users. Influencers and content creators showcase high-end products through engaging content, creating aspirational value among young and affluent buyers. Luxury brand websites are also improving digital shopping experiences, offering virtual try-ons, live consultations, and exclusive online launches. This digital exposure is not only enhancing brand visibility but also encouraging impulse and planned purchases. Additionally, luxury brands are investing in digital marketing and collaborations with local influencers to reach target audiences effectively.

Key Growth Drivers of GCC Personal Luxury Goods Market:

Growing high-end gifting culture

Rising high-end gifting culture in the GCC region is positively influencing the market. Gifting luxury items during festivals, weddings, business events, and religious occasions, such as Eid, has become deeply rooted in the region’s social fabric. People often prefer premium products like designer accessories, watches, perfumes, and jewelry as gifts to reflect prestige and social status. This tradition is driving consistent demand throughout the year, especially during peak festive seasons. Luxury brands also curate exclusive gift collections and packaging to cater to this cultural preference, making gifting a key sales strategy. Moreover, high disposable incomes and a desire to maintain social ties and honor traditions are encouraging lavish spending on gifts. This culturally driven gifting behavior continues to boost sales in the GCC region.

Increasing demand for customization

Rising demand for customization is propelling the market growth, as people are seeking unique and personalized experiences. In a region where individuality, prestige, and exclusivity are highly valued, personalized luxury products, such as engraved watches, monogrammed handbags, and bespoke fragrances, are gaining strong appeal. Individuals are willing to pay a premium for items that reflect their personal style, identity, and social status. Luxury brands are responding by offering customization options both in-store and online, enhancing customer engagement and brand loyalty. Additionally, the integration of advanced digital tools is making customization more accessible and seamless. This trend is supporting long-term growth by deepening emotional connections between buyers and brands in the market.

Broadening of e-commerce portals

The expansion of e-commerce portals is making high-end products more accessible across urban and remote areas. Online platforms allow luxury brands to showcase their collections to a broader audience without the need for physical presence in every location. People enjoy the convenience of browsing, comparing, and purchasing luxury items from the comfort of their homes, which boosts engagement and conversion rates. Advanced technologies like virtual try-ons, high-resolution imagery, and personalized recommendations are further enhancing the online luxury shopping experience. Additionally, e-commerce enables brands to implement targeted marketing strategies, loyalty programs, and limited-edition online exclusives, attracting both new and repeat buyers. This digital expansion is supporting cross-border luxury sales and strengthening brand visibility.

Key Market Segmentation:

IMARC Group provides an analysis of the key trends in each sub-segment of the GCC personal luxury goods market report, along with forecasts at the regional and country level from 2026-2034. Our report has categorized the market based on type, gender and distribution channel.

Breakup by Country:

- Saudi Arabia

- United Arab Emirates

- Qatar

- Kuwait

- Oman

- Bahrain

Breakup by Type:

- Accessories

- Apparel

- Watch and Jewellery

- Luxury Cosmetics

- Others

Breakup by Gender:

- Female

- Male

Breakup by Distribution Channel:

Access the comprehensive market breakdown Request Sample

- Mono-brand Stores

- Specialty Stores

- Departmental Stores

- Online Stores

- Others

Competitive Landscape:

The competitive landscape of the industry has also been examined with some of the key players being Burberry Group PLC, Chanel S.A., Estee Lauder Companies, Giorgio Armani SpA, Kering S.A., Loreal, LVMH Moët Hennessy Louis Vuitton SE, Mulberry Group PLC, Prada Group, Cie Financiere Richemont SA, The Swatch Group, and Versace.

GCC Personal Luxury Goods Market News:

- In August 2025, Arif Mohammad, the founder of the multinational conglomerate 4AM Group, revealed the debut of a luxury watch brand worth USD 83 Million, in partnership with one of the globe’s most legendary Swiss watch manufacturers. This innovative premium brand was set to provide Swiss accuracy and striking design, accessible via exclusive flagship stores in Dubai, Riyadh, London, and Mumbai.

- In July 2025, Titan Company obtained a 67% ownership interest in Damas LLC, a luxury jeweler located in Dubai. The agreement was valued at USD 283.2 Million. This purchase would enhance Titan's footprint in the Gulf Cooperation Council nations.

- In January 2025, the Cultural Development Fund of Saudi Arabia, together with the Fashion Commission, welcomed luxury fashion designer Brunello Cucinelli to AlUla, Saudi Arabia. The event bolstered the Fund's aim to aid creatives and entrepreneurs in the cultural industry by encouraging knowledge sharing and promoting sustainability.

- In January 2025, Sotheby’s was set to showcase a collection of luxury jewelry at its inaugural auction in Saudi Arabia, featuring a pair of diamond earrings anticipated to sell for as much as USD 800,000. The set designed by Graff included a pear-shaped, 9.39-carat, D-color, VVS1-clarity diamond that could potentially be internally flawless.

- In November 2024, Al Majed Jewellery, a prominent name in luxury watches and jewelry in Doha, Qatar, launched a new timepiece influenced by the realm of comedy from the Swiss-French watchmaker Reservoir: the limited edition Reservoir Popeye, with only 30 pieces. This exclusive version, drawing inspiration from Qatar, represented the golden sand dunes of its desert and the native wildlife, personified by the falcon and the oryx.

- In September 2024, in a significant tribute to celebrate Saudi Arabia's 94th National Day, TAG Heuer, the prestigious Swiss luxury watchmaker, launched two exclusive limited edition watches ‘the TAG Heuer Carrera Day Date KSA Limited Edition 41mm and the TAG Heuer Carrera Date KSA Limited Edition 29mm’, which embodied the country’s vibrant cultural legacy and enduring traditions. The TAG Heuer Carrera Day Date KSA Limited Edition 41mm showcased a dial with a green, smoked sunray-brushed pattern that evoked the Kingdom's varied terrains.

Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Segment Coverage | Type, Gender, Distribution Channel, Country |

| Countries Covered | Saudi Arabia, United Arab Emirates, Qatar, Kuwait, Oman, Bahrain |

| Companies Covered | Burberry Group PLC, Chanel S.A., Estee Lauder Companies, Giorgio Armani SpA, Kering S.A., Loreal, LVMH Moët Hennessy Louis Vuitton SE, Mulberry Group PLC, Prada Group, Cie Financiere Richemont SA, The Swatch Group, Versace |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the GCC Personal Luxury Goods Market Report

The GCC personal luxury goods market was valued at USD 10.7 Billion in 2025.

We expect the GCC personal luxury goods market to exhibit a CAGR of 3.66% during 2026-2034.

The emerging western fashion trends, along with the growing number of celebrity endorsements, are primarily driving the GCC personal luxury goods market.

The sudden outbreak of the COVID-19 pandemic has led to the changing consumer inclination from conventional brick-and-mortar distribution channels towards online retail platforms for purchasing personal luxury goods across the GCC.

Based on the type, the GCC personal luxury goods market can be categorized into accessories, apparel, watch and jewellery, luxury cosmetics, and others. Among these, accessories currently account for the majority of the total market share.

Based on the gender, the GCC personal luxury goods market has been segregated into female and male, where female currently holds the largest market share.

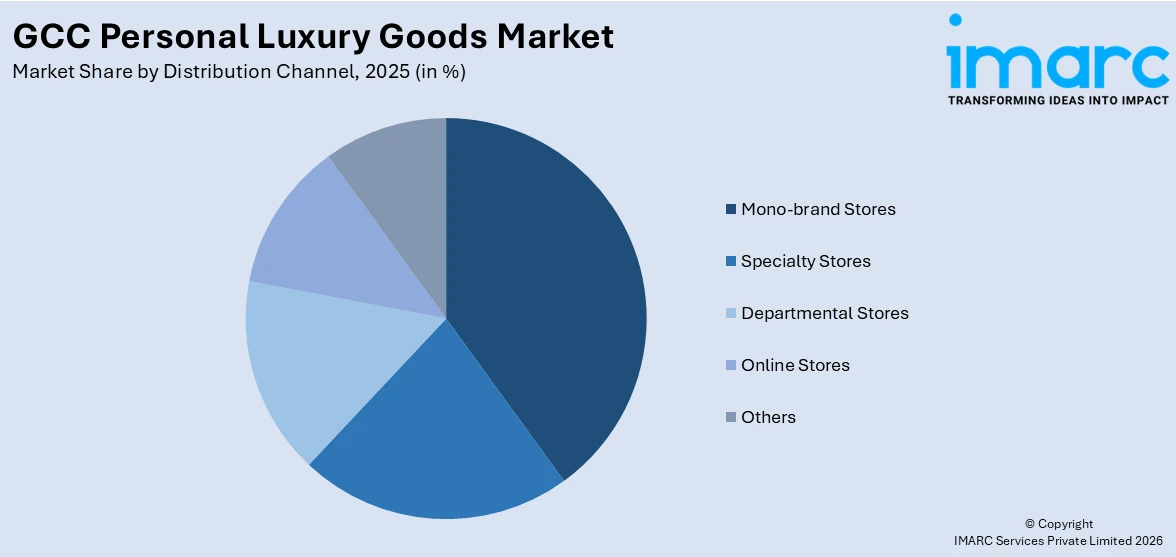

Based on the distribution channel, the GCC personal luxury goods market can be bifurcated into mono-brand stores, specialty stores, departmental stores, online stores, and others. Currently, mono-brand stores exhibit a clear dominance in the market.

On a regional level, the market has been classified into Saudi Arabia, United Arab Emirates, Qatar, Kuwait, Oman, and Bahrain, where United Arab Emirates currently dominates the GCC personal luxury goods market.

Some of the major players in the GCC personal luxury goods market include Burberry Group PLC, Chanel S.A., Estee Lauder Companies, Giorgio Armani SpA, Kering S.A., Loreal, LVMH Moët Hennessy Louis Vuitton SE, Mulberry Group PLC, Prada Group, Cie Financiere Richemont SA, The Swatch Group, and Versace.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)