Hardware Encryption Market Size, Share, Trends and Forecast by Algorithm and Standard, Architecture, Product, Application, and Region, 2026-2034

Hardware Encryption Market Size and Share:

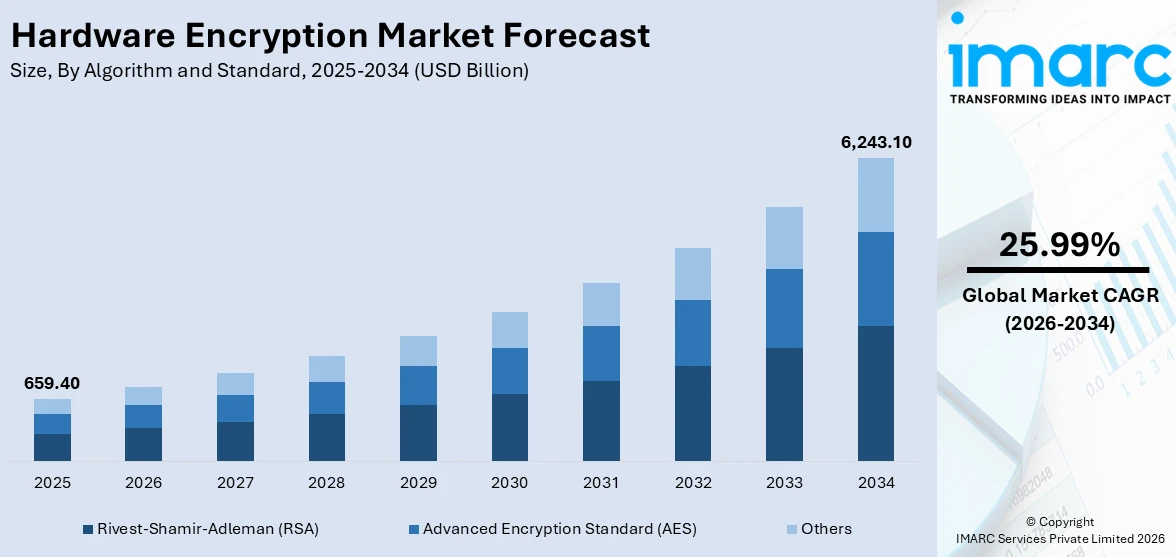

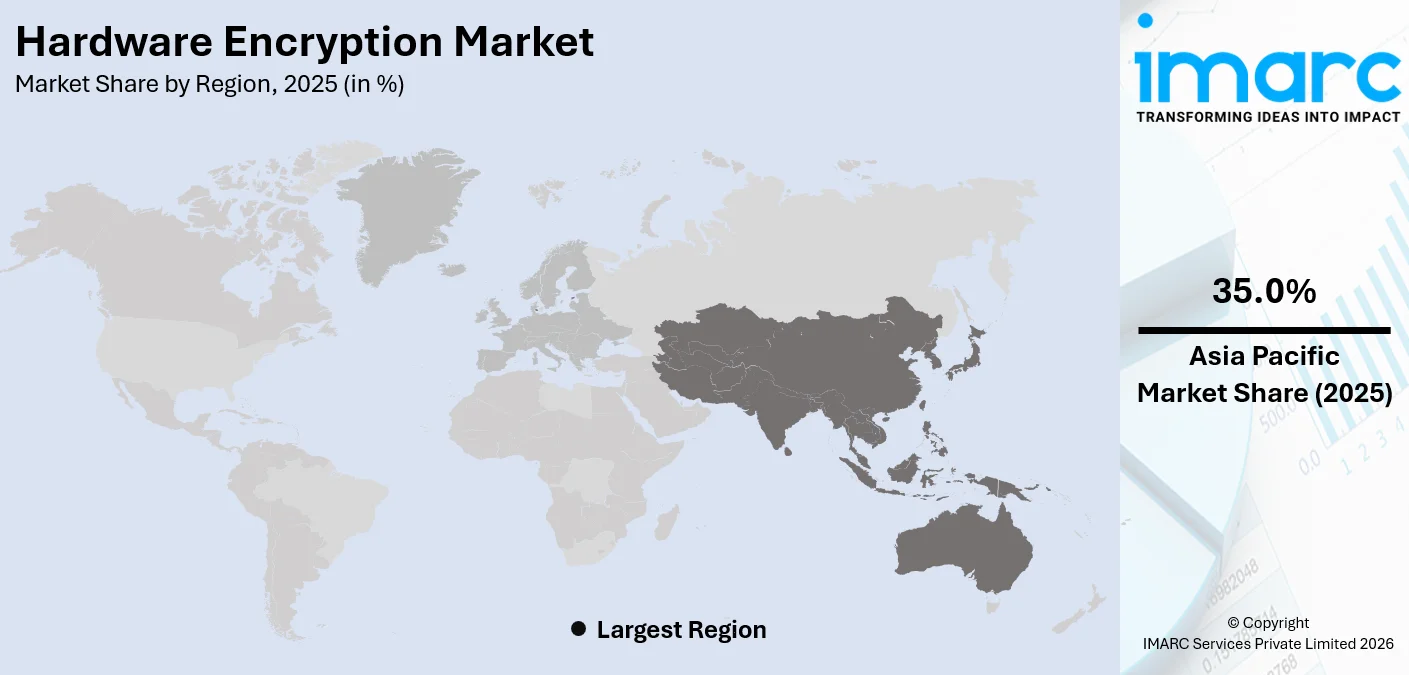

The global hardware encryption market size was valued at USD 659.40 Billion in 2025. Looking forward, IMARC Group estimates the market to reach USD 6,243.10 Billion by 2034, exhibiting a CAGR of 25.99% from 2026-2034. Asia Pacific currently dominates the market, holding a market share of 35.0% in 2025. The region benefits from rapid industrialization, expanding digital infrastructure, increasing adoption of cloud-based services, and growing investments in data security solutions across major economies, which collectively strengthen demand for advanced encryption technologies and reinforce the hardware encryption market share.

The global hardware encryption market is propelled by the escalating volume of sensitive data generated across industries, the rising incidence of cyberattacks and data breaches, and the increasing regulatory mandates requiring robust data protection mechanisms. The expanding adoption of connected devices and Internet of Things (IoT) ecosystems further amplifies the need for hardware-based security solutions that provide tamper-resistant encryption capabilities. Additionally, the growing reliance on cloud computing and hybrid work environments has heightened the demand for encrypted storage devices and secure communication channels. The proliferation of digital payment systems and online financial transactions also necessitates stringent encryption protocols, thereby supporting the hardware encryption market growth.

The United States has emerged as a major region in the hardware encryption market owing to many factors. The country maintains a robust regulatory framework, including federal mandates for data protection across government agencies, defense organizations, and healthcare institutions, which drives consistent demand for certified hardware encryption solutions. In June 2025, Futurex became the only hardware security module (HSM) provider with post-quantum cryptography (PQC) support to be PCI HSM validated, underscoring U.S. industry leadership in deploying encryption hardware that meets evolving security standards. The presence of leading technology corporations and semiconductor manufacturers contributes to continuous innovation in encryption hardware, including self-encrypting drives and encrypted USB devices.

To get more information on this market Request Sample

Hardware Encryption Market Trends:

Growing Demand for Quantum-Resistant Encryption Solutions

The increasing awareness of quantum computing threats is accelerating the development of quantum-resistant hardware encryption solutions. As quantum processors advance in capability, traditional cryptographic algorithms face the risk of being rendered obsolete, prompting organizations to invest in post-quantum encryption hardware that can withstand future computational attacks. In August 2024, the National Institute of Standards and Technology finalized its first post-quantum cryptography standards (ML-KEM and ML-DSA), formally initiating the transition toward quantum-resistant encryption frameworks across federal systems. Government agencies and defense establishments are leading the transition toward quantum-safe standards, encouraging manufacturers to develop encryption modules capable of supporting lattice-based and hash-based cryptographic schemes.

Expansion of Encrypted Storage in Cloud Environments

The rapid migration of enterprise workloads to cloud platforms is fueling the demand for hardware-encrypted storage solutions that ensure data confidentiality across distributed environments. Organizations are increasingly deploying self-encrypting drives within data centers and hybrid cloud architectures to maintain end-to-end data protection without relying solely on software-based encryption layers. In January 2025, Google Cloud announced expanded Confidential GKE Nodes and Confidential VMs with hardware-based trusted execution environments, enabling encryption of data in use across more cloud workloads and reinforcing secure cloud adoption. Moreover, the growing adoption of confidential computing frameworks, which leverage hardware-based trusted execution environments, further reinforces the need for integrated encryption capabilities at the storage and processor level, which is positively influencing the hardware encryption market outlook.

Integration of Encryption in IoT and Edge Devices

The proliferation of Internet of Things devices and edge computing infrastructure is creating substantial demand for lightweight hardware encryption solutions tailored to resource-constrained environments. As billions of connected devices generate and transmit sensitive data across industrial, automotive, healthcare, and smart city applications, the need for embedded encryption modules that operate efficiently within limited power and processing constraints has intensified. In April 2024, NXP Semiconductors launched the EdgeLock SE052F secure element, the first hardware secure element certified to FIPS 140-3 Level 3, strengthening device-level encryption and authentication for IoT deployments. Manufacturers are developing compact encryption chips and secure microcontrollers designed to protect data at the device level, preventing unauthorized access and ensuring data integrity throughout the communication chain.

Hardware Encryption Industry Segmentation:

IMARC Group provides an analysis of the key trends in each segment of the global hardware encryption market, along with forecast at the global, regional, and country levels from 2026-2034. The market has been categorized based on algorithm and standard, architecture, product, and application.

Analysis by Algorithm and Standard:

- Advanced Encryption Standard (AES)

- Rivest-Shamir-Adleman (RSA)

- Others

Rivest-shamir-adleman (RSA) holds 48.5% of the market share. RSA remains a foundational asymmetric encryption standard widely deployed in hardware security modules, digital signature verification, and secure key exchange protocols across enterprise and government environments. The algorithm's established presence in public key infrastructure systems ensures sustained demand for RSA-compatible hardware encryption products that facilitate secure authentication, certificate management, and encrypted communications. Organizations across banking, defense, and telecommunications sectors rely on RSA-based hardware solutions to protect sensitive transactions and classified information. The continued integration of RSA with complementary encryption standards within multi-algorithm hardware platforms enhances its versatility and relevance. Additionally, the ongoing development of higher key-length RSA implementations addresses evolving security requirements, enabling the hardware encryption market forecast to remain positive while maintaining backward compatibility with existing infrastructure deployments across global markets.

Analysis by Architecture:

- Field-Programmable Gate Arrays (FPGA)

- Application-Specific Integrated Circuits (ASIC)

Application-specific integrated circuits (ASIC) lead the market with a share of 57.6%. ASIC-based hardware encryption solutions offer superior performance, power efficiency, and cost-effectiveness for high-volume encryption processing applications compared to general-purpose alternatives. These purpose-built circuits are optimized for specific cryptographic operations, enabling faster data throughput and lower latency in demanding environments such as data centers, network infrastructure, and military communications systems. The fixed-function nature of ASICs provides inherent resistance to side-channel attacks and firmware-level vulnerabilities, making them particularly suitable for applications requiring stringent security certifications. The growing demand for dedicated encryption processing in storage controllers, network interface cards, and secure communication equipment continues to drive ASIC adoption. Furthermore, advancements in semiconductor fabrication processes enable the development of increasingly compact and energy-efficient ASIC designs, supporting their deployment across a widening range of hardware encryption applications.

Analysis by Product:

- External Hard Disk Drives

- Internal Hard Disk Drives

- Inline Network Encryptors

- USB Flash Drives

- Others

External hard disk drives dominate the market, with a share of 35.5%. External hard disk drives with built-in hardware encryption provide portable and secure data storage solutions for professionals, enterprises, and government agencies that require data protection beyond the confines of internal network security. These devices incorporate self-encrypting drive technology that automatically encrypts all stored data without requiring software installation or user intervention, ensuring consistent protection regardless of the operating environment. In July 2024, Western Digital launched 6TB WD My Passport portable hard drives featuring built-in 256-bit AES hardware encryption and password protection, strengthening secure portable storage options for enterprise and professional users. The increasing mobility of the workforce and the growing practice of transporting sensitive data between locations and organizations elevate the importance of encrypted external storage devices. Compliance requirements across industries such as healthcare, finance, and legal services mandate the use of encrypted portable storage for handling personally identifiable information and confidential business data.

Analysis by Application:

Access the comprehensive market breakdown Request Sample

- Consumer Electronics

- IT & Telecom

- Transportation

- Aerospace and Defense

- Healthcare

- BFSI

- Others

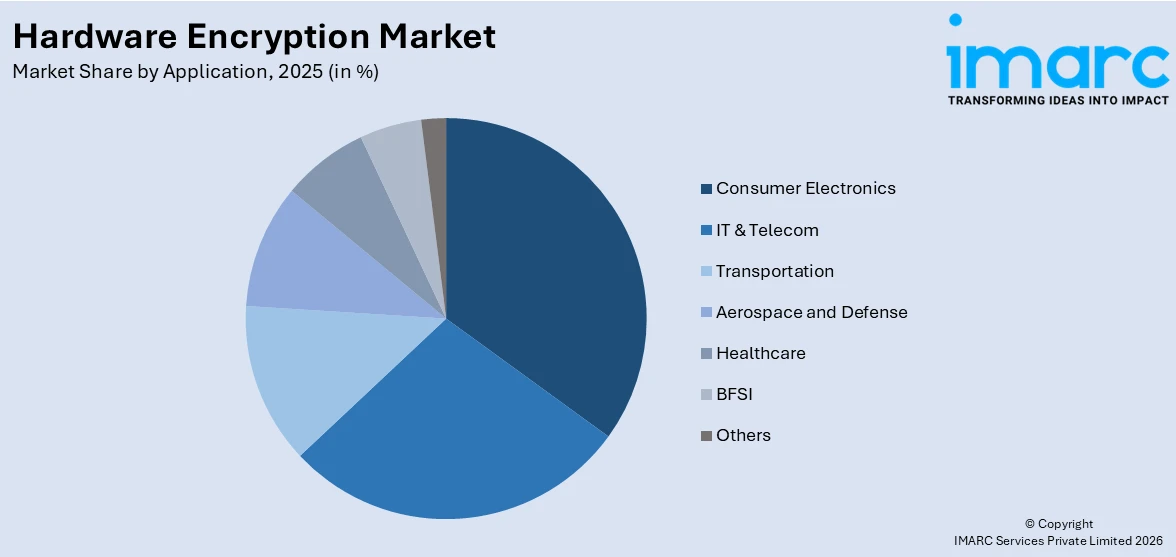

Consumer electronics represents the leading segment, with a market share of 32.8%. The consumer electronics segment drives significant demand for hardware encryption through the widespread adoption of smartphones, tablets, laptops, wearable devices, and smart home systems that process and store personal and financial information. The increasing consumer awareness regarding data privacy and the growing volume of sensitive transactions conducted through personal devices amplify the requirement for embedded encryption hardware that operates seamlessly within consumer product architectures. As per sources, Apple Inc. unveiled the A17 Pro chip with an enhanced Secure Enclave to strengthen on-device encryption for biometric authentication and sensitive user data protection in its latest iPhone models. Manufacturers integrate encryption chips and secure enclaves into device processors to protect biometric data, payment credentials, and personal communications from unauthorized access. Additionally, evolving privacy regulations and consumer protection standards across various jurisdictions encourage device manufacturers to implement certified encryption solutions, contributing to the sustained expansion of the hardware encryption market trends within the consumer electronics domain.

Regional Analysis:

To get more information on the regional analysis of this market Request Sample

- Asia Pacific

- China

- Japan

- India

- South Korea

- Australia

- Indonesia

- Others

- North America

- United States

- Canada

- Europe

- Germany

- France

- United Kingdom

- Italy

- Spain

- Russia

- Others

- Latin America

- Brazil

- Mexico

- Argentina

- Colombia

- Chile

- Peru

- Others

- Middle East and Africa

- Turkey

- Saudi Arabia

- Iran

- United Arab Emirates

- Others

Asia Pacific, accounting for 35.0% of the share, maintaining the leading position in the market. The region's dominance is attributed to the rapid digital transformation occurring across major economies, the expansion of cloud computing infrastructure, the increasing penetration of smartphones and connected devices, and the growing emphasis on cybersecurity investments by both government entities and private enterprises. Several leading economies in the region are investing heavily in semiconductor manufacturing capabilities and data protection frameworks that support the adoption of hardware encryption solutions across diverse industries. The region's manufacturing ecosystem enables cost-effective production of encryption hardware, facilitating broader market penetration. Government initiatives promoting digital economy development and data localization requirements further drive encryption adoption. The expansion of 5G networks and smart city projects across Asia Pacific also creates additional demand for hardware-based security solutions throughout the regional digital infrastructure.

Key Regional Takeaways:

North America Hardware Encryption Market Analysis

North America represents a significant market for hardware encryption, driven by the region's advanced technological infrastructure, stringent regulatory environment, and high concentration of enterprises operating in data-sensitive industries. The presence of major technology companies, defense contractors, and financial institutions creates consistent demand for certified encryption hardware across storage, networking, and communication applications. Federal mandates requiring encryption of classified and sensitive government data continue to support market expansion, while private sector organizations increasingly adopt hardware encryption to comply with industry-specific regulations governing data protection and privacy. The region's leadership in semiconductor innovation facilitates the development of advanced encryption chipsets and security processors that set global performance benchmarks. The growing frequency of ransomware attacks and sophisticated cyber threats targeting critical infrastructure reinforces the strategic importance of hardware-based encryption solutions. Additionally, the expansion of data center capacity and edge computing deployments across North America generates sustained demand for encrypted storage and processing hardware throughout the enterprise technology ecosystem.

United States Hardware Encryption Market Analysis

The United States maintains a dominant position in the hardware encryption market, supported by a comprehensive regulatory framework that mandates encryption across federal agencies, defense operations, and critical infrastructure sectors. The country's advanced technology ecosystem fosters continuous innovation in encryption hardware, including self-encrypting drives, hardware security modules, and encrypted communication devices. As per sources, the U.S. Cybersecurity and Infrastructure Security Agency (CISA) launched the Post-Quantum Cryptography Initiative to coordinate federal and industry action on quantum-resistant encryption standards and secure critical infrastructure. Growing concerns over intellectual property theft, corporate espionage, and state-sponsored cyberattacks drive sustained investment in hardware-level security solutions across both public and private sector organizations. The healthcare industry's compliance with data protection mandates further strengthens demand for encrypted storage and communication devices that safeguard patient records and medical research data. Financial services firms increasingly deploy hardware encryption to protect transaction processing systems and customer data repositories from sophisticated threat actors.

Europe Hardware Encryption Market Analysis

Europe represents a substantial market for hardware encryption, underpinned by the region's rigorous data protection legislation and the growing emphasis on digital sovereignty across member states. The implementation of comprehensive privacy regulations has established stringent requirements for data encryption across industries, compelling organizations to adopt hardware-based solutions that ensure compliance with mandated security standards. The region's defense and aerospace sectors maintain significant demand for certified encryption hardware to protect classified communications and sensitive operational data. Financial institutions across European economies invest in hardware encryption to secure payment processing systems, customer databases, and cross-border transaction networks. The increasing digitalization of public services and the expansion of smart infrastructure projects across major European economies further drive adoption of encryption hardware. Additionally, the European semiconductor industry's focus on developing sovereign encryption technologies reduces dependence on external suppliers and supports the growth of locally manufactured hardware encryption solutions.

Asia Pacific Hardware Encryption Market Analysis

Asia Pacific leads the global hardware encryption market owing to the rapid expansion of digital infrastructure, increasing government investments in cybersecurity frameworks, and the growing adoption of encrypted devices across consumer and enterprise segments. The region's large-scale semiconductor manufacturing capabilities enable cost-competitive production of encryption hardware components, supporting broad market penetration. Government initiatives promoting data localization, digital economy development, and national cybersecurity strategies drive sustained demand for hardware-based encryption solutions. The expanding deployment of 5G networks, cloud computing platforms, and IoT ecosystems across the region further amplifies the need for embedded encryption capabilities. Rising awareness of data privacy among consumers and businesses, coupled with increasing regulatory requirements across multiple jurisdictions, continues to strengthen the adoption of hardware encryption products throughout the Asia Pacific region.

Latin America Hardware Encryption Market Analysis

Latin America is experiencing gradual growth in hardware encryption adoption, driven by the increasing digitalization of financial services, expanding e-commerce platforms, and growing awareness of cybersecurity threats across the region. Governments in major economies are implementing data protection regulations that encourage organizations to adopt encrypted storage and communication solutions. The banking and financial services sector represents a primary demand driver, as institutions invest in hardware encryption to protect transaction systems and customer information from rising cyber threats. The expansion of cloud computing adoption and mobile device penetration further supports market growth across the region.

Middle East and Africa Hardware Encryption Market Analysis

The Middle East and Africa region is witnessing growing demand for hardware encryption solutions, supported by increasing investments in digital infrastructure, smart city initiatives, and national cybersecurity programs across key economies. Government agencies and defense organizations represent primary consumers of certified encryption hardware for protecting classified data and secure communications. The expanding financial services sector and the digitalization of oil and gas operations further contribute to encryption hardware adoption. Rising awareness of data protection requirements and the implementation of cybersecurity regulations across the region are encouraging both public and private sector organizations to integrate hardware-based encryption into their security architectures.

Competitive Landscape:

The competitive landscape of the global hardware encryption market is characterized by the presence of established technology corporations, specialized security solution providers, and semiconductor manufacturers that compete on the basis of product performance, certification compliance, and integration capabilities. Major players invest in research and development to advance encryption algorithms, improve processing speeds, and enhance power efficiency in their hardware security offerings. Strategic partnerships between encryption hardware manufacturers and cloud service providers, device manufacturers, and system integrators expand market reach and enable the delivery of comprehensive security solutions across diverse application environments. The market also witnesses consolidation through mergers and acquisitions as larger technology companies seek to strengthen their encryption product portfolios and gain access to specialized expertise.

The report provides a comprehensive analysis of the competitive landscape in the hardware encryption market with detailed profiles of all major companies, including:

- Gemalto NV

- IBM Corp.

- Imation Corp.

- Maxim Integrated Products

- Micron Technology

- Netapp

- Samsung Electronics

- SanDisk Corporation

- Seagate Technology

- Thales

- Toshiba Corp.

- Western Digital Corp.

- Western Digital Technologies

- Winmagic

Latest News and Developments:

- In January 2026, IDEMIA Secure Transactions introduced the Sphere HSM, a decentralized hardware security module designed for finance, government, healthcare, and cloud environments. The solution supports post-quantum cryptography, reduces power consumption by 50%, eliminates single points of failure, and complies with India’s IT Act and RBI cybersecurity guidelines.

- In November 2025, Nextorage introduced the NX-PFS1PRO external SSD, offering up to 2 GB/s speeds, built-in hardware encryption, and an auto-erase security feature. The portable drive features real-time health monitoring, NFC-based unlocking, IP54 dust and water resistance, and capacities ranging from 1TB, 2TB, 4TB, and 8TB.

Hardware Encryption Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Algorithms and Standards Covered | Advanced Encryption Standard (AES), Rivest-Shamir-Adleman (RSA), Others |

| Architectures Covered | Field-Programmable Gate Arrays (FPGA), Application-Specific Integrated Circuits (ASIC) |

| Products Covered | External Hard Disk Drives, Internal Hard Disk Drives, Inline Network Encryptors, USB Flash Drives, Others |

| Applications Covered | Consumer Electronics, IT & Telecom, Transportation, Aerospace and Defense, Healthcare, BFSI, Others |

| Region Covered | Asia Pacific, North America, Europe, Latin America, Middle East and Africa |

| Countries Covered | China, Japan, India, South Korea, Australia, Indonesia, United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, Brazil, Mexico, Argentina, Colombia, Chile, Peru, Turkey, Saudi Arabia, Iran, United Arab Emirates |

| Companies Covered | Gemalto NV, IBM Corp., Imation Corp., Maxim Integrated Products, Micron Technology, Netapp, Samsung Electronics, SanDisk Corporation, Seagate Technology, Thales, Toshiba Corp., Western Digital Corp., Western Digital Technologies, Winmagic, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the hardware encryption market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the global hardware encryption market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's Five Forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the hardware encryption industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Hardware Encryption Market Report

The hardware encryption market was valued at USD 659.40 Billion in 2025.

The hardware encryption market is projected to exhibit a CAGR of 25.99% during 2026-2034, reaching a value of USD 6,243.10 Billion by 2034.

The hardware encryption market is driven by the escalating volume of sensitive digital data, rising incidence of cyberattacks and data breaches, increasing regulatory mandates for data protection, growing adoption of cloud computing and IoT devices, and advancements in quantum-resistant cryptographic methods that necessitate robust hardware-based encryption solutions.

Asia Pacific currently dominates the hardware encryption market, accounting for a share of 35.0%. The region benefits from rapid digital transformation, expanding cloud infrastructure, large-scale semiconductor manufacturing, and increasing government investments in cybersecurity frameworks.

Some of the major players in the hardware encryption market include Gemalto NV, IBM Corp., Imation Corp., Maxim Integrated Products, Micron Technology, Netapp, Samsung Electronics, SanDisk Corporation, Seagate Technology, Thales, Toshiba Corp., Western Digital Corp., Western Digital Technologies, Winmagic, etc.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)