India Agrochemicals Market Size, Share, Trends and Forecast by Type, Application, and Region, 2026-2034

India Agrochemicals Market Size, Share, Trends & Forecast (2026-2034)

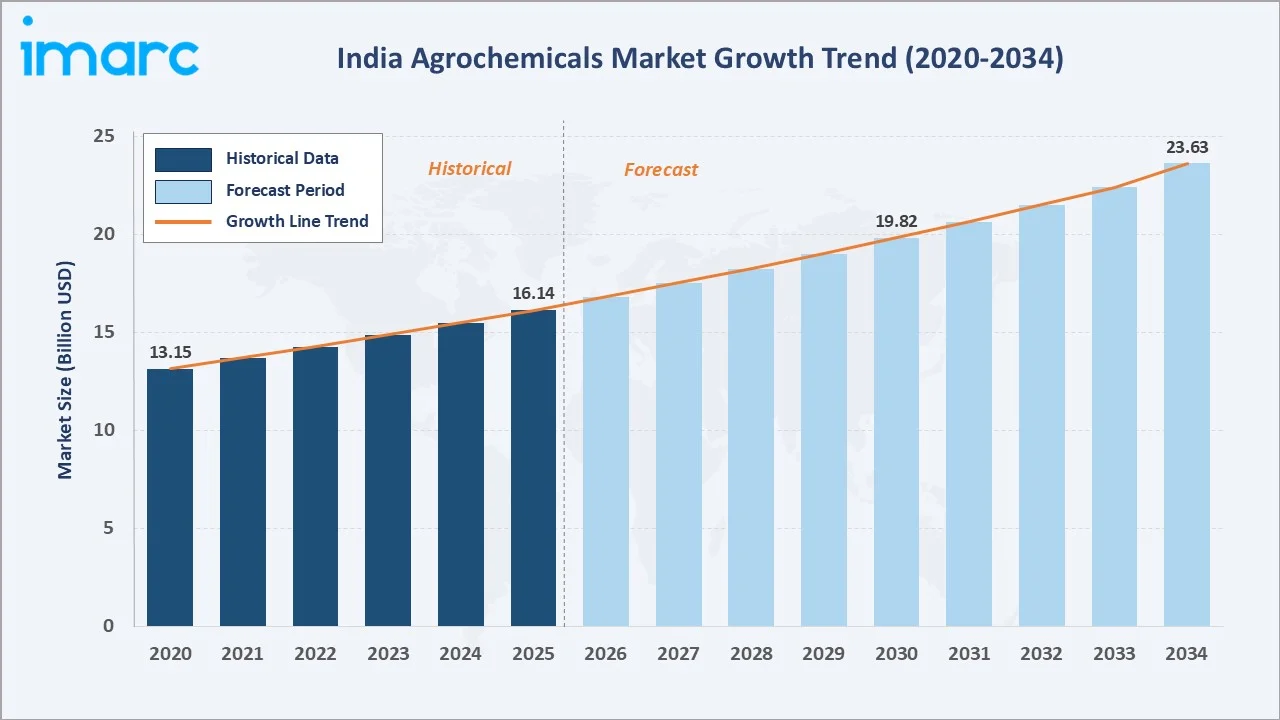

The India agrochemicals market reached USD 16.14 Billion in 2025 and is projected to reach USD 23.63 Billion by 2034, growing at a CAGR of 4.19% during 2026-2034. Rising food demand, expansion of irrigation infrastructure, growing adoption of precision agriculture, and government support through PM-KISAN and Pradhan Mantri Fasal Bima Yojana (PMFBY) are driving consistent investment in crop-input technologies across all major farming states.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 16.14 Billion |

|

Forecast Market Size (2034) |

USD 23.63 Billion |

|

CAGR (2026-2034) |

4.19% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

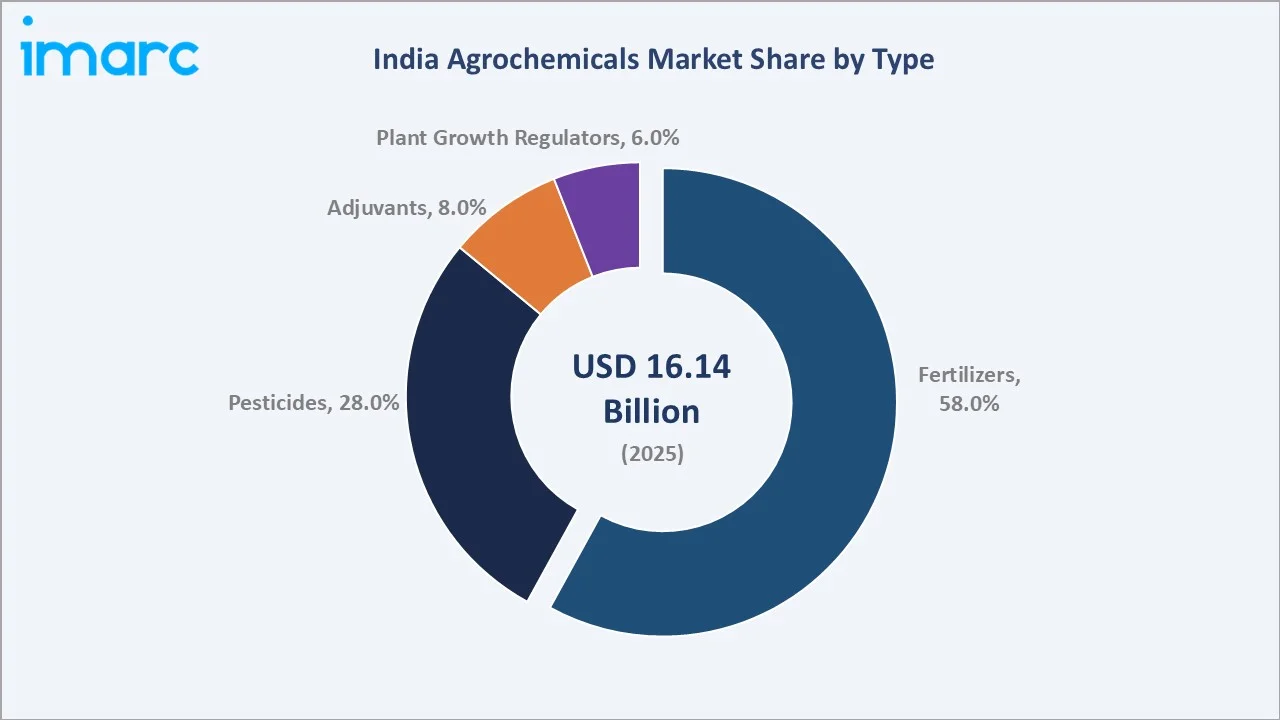

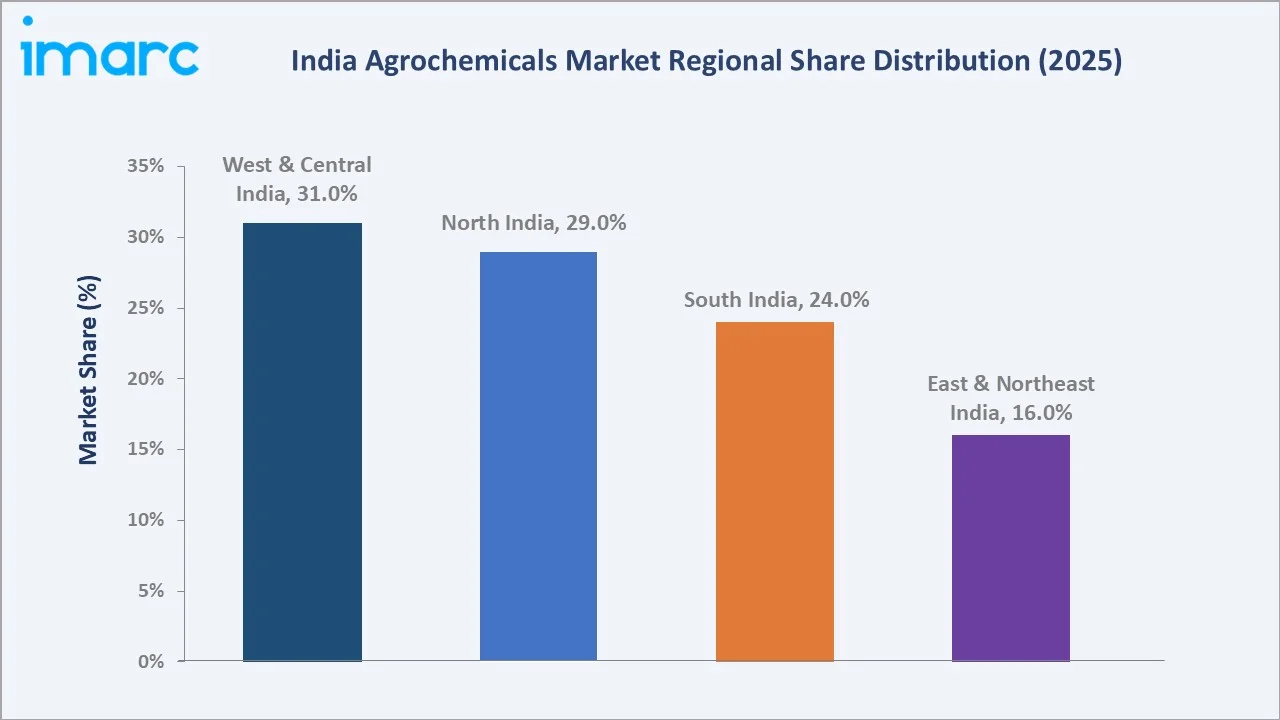

West and Central India lead regionally with a 31.0% market share in 2025, anchored by Maharashtra's cotton belt and Gujarat's groundnut-growing districts. Fertilizers dominate at 58.0%, reflecting the scale of cereal and oilseed cultivation. Pesticides contribute 28.0%, driven by rising pest resistance and increased kharif crop area.

To get more information on this market, Request Sample

India's agrochemicals market demonstrates steady structural growth sustained by three forces: the country's 104 million hectares of kharif crop area till August 2025, escalating farm-gate input demand driven by 140 million smallholder farmers, and the government's 2024–25 fertilizer subsidy budget of INR 1.64 lakh crore. These factors provide a durable demand floor, ensuring above-trend growth through the forecast period.

Executive Summary

India's agrochemicals market is expanding steadily at a 4.19% CAGR, supported by rising food security imperatives, a maturing farm-input ecosystem, and progressive policy backing. The market grew from USD 13.15 Billion in 2020 to USD 16.14 Billion in 2025 and is forecast to reach USD 23.63 Billion by 2034, adding USD 7.49 Billion in incremental value over the forecast period.

Fertilizers retain the top product share at 58.0% in 2025, as India's urea and DAP consumption continues to be subsidized and policy-driven. Pesticides contribute 28.0%, with insecticides and herbicides seeing consistent demand growth driven by rising labor costs and the adoption of herbicide-tolerant crop varieties. Adjuvants represent 8.0% of the market, the fastest-growing type, as precision agriculture adoption creates demand for efficacy-enhancing formulation additives.

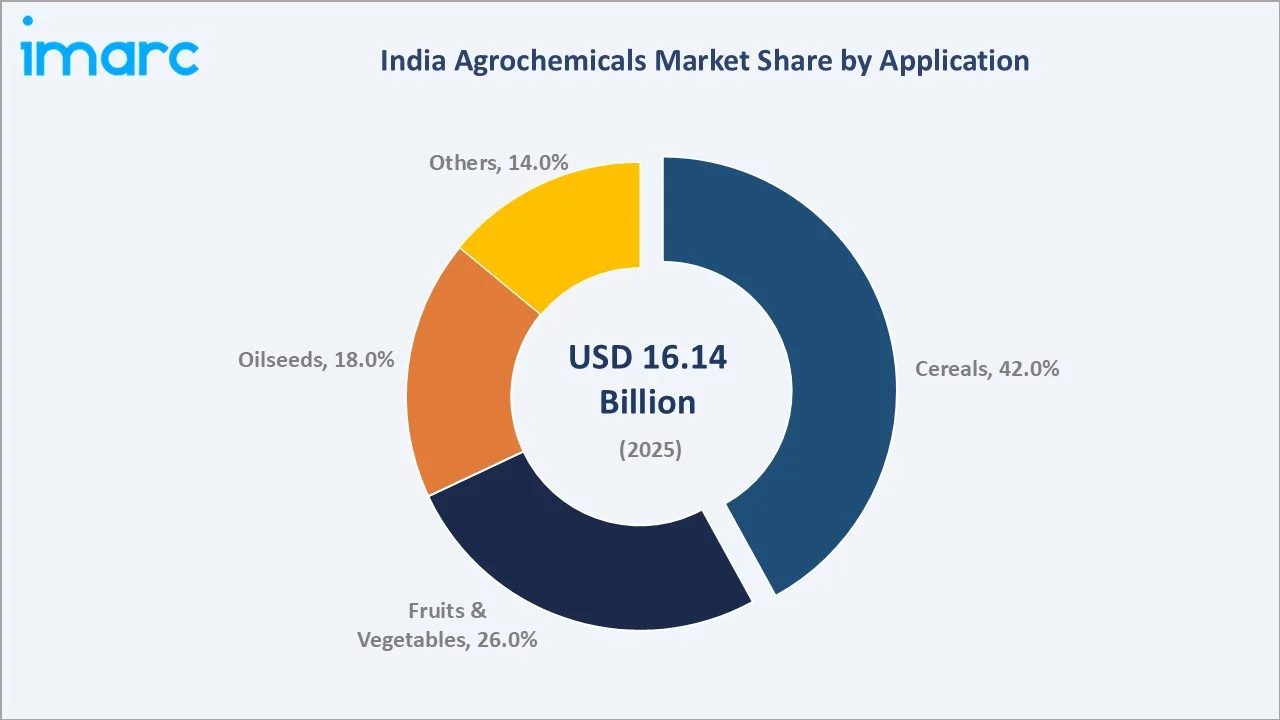

Cereals lead the application segment at 42.0%, driven by India’s wheat production, which recorded strong growth, reaching 1,179.45 lakh tons in 2024-25, up by 46.53 lakh tons from 1,132.92 lakh tons in the previous year. North India commands 29.0% regional share, while West and Central India lead at 31.0%. Key players, including UPL, Bayer AG, BASF, and PI Industries, are expanding their specialty and bio-agrochemical portfolios to capture premium-tier demand.

Key Market Insights

|

Insight |

Data |

|

Largest Type |

Fertilizers – 58.0% share (2025) |

|

Fastest Growing Type |

Adjuvants – ~5.2% CAGR (2026-2034) |

|

Largest Application |

Cereals – 42.0% share (2025) |

|

Fastest Growing Application |

Fruits and Vegetables – ~4.8% CAGR (2026-2034) |

|

Leading Region |

West and Central India – 31.0% share (2025) |

|

Top Companies |

UPL, Bayer AG, BASF, PI Industries |

Key Analytical Observations Supporting The Above Data:

- Fertilizers at 58.0% (2025) dominate due to India's subsidy-driven consumption of urea, DAP, and complex NPK fertilizers. The government's soil health card scheme, covering 10+ million farmers, is gradually shifting consumption toward balanced nutrition, sustaining fertilizer volume growth at 3.5–4.0% annually.

- Cereals at 42.0% (2025) lead applications as India procured 34.2 million tons of wheat during the rabi marketing season (April–June 2026) as of May 2026, up from 29.7 million tons in the previous year and close to the government’s target of 34.5 million tons. This directly sustains agrochemical application rates in Punjab, Haryana, and UP.

- West and Central India's 31.0% (2025) regional share reflects Maharashtra's status as India's largest pesticide-consuming state, with cotton and soybean crops requiring 5–7 spray cycles per season. Gujarat's groundnut area of 1.8 million hectares adds further baseline demand.

- Adjuvants at ~5.2% CAGR represent the market's fastest-growing category as tank-mix adjuvants, surfactants, and stickers improve pesticide bioavailability by 20–35%, reducing active ingredient usage and improving efficacy per application.

- The overall market's 4.19% CAGR through 2034 is underpinned by India's farm area under horticulture crossing 29.488 million hectares in 2024–25, creating sustained demand for specialty fungicides, plant growth regulators, and micro-nutrient formulations beyond commodity fertilizers.

India Agrochemicals Market Overview

Agrochemicals encompass fertilizers, pesticides (insecticides, herbicides, fungicides), plant growth regulators, and adjuvants used to enhance crop yield, quality, and resilience against biotic and abiotic stress. India's market spans technical-grade manufacturing, domestic formulation, and retail distribution through 2.82 lakh registered agri-input dealers and a rapidly expanding e-commerce channel serving 140 million smallholder farm households.

India's Green Revolution legacy has cemented fertilizer dependence across Northern and Central farming belts, while post-2016 herbicide adoption in paddy and wheat has structurally shifted the pesticide demand curve. The PLI Scheme for agrochemical technical manufacturing is catalyzing domestic active ingredient (AI) production, reducing reliance on Chinese imports that currently represent ~35% of technical-grade pesticide supply.

Market Dynamics

To evaluate market opportunities, Request Sample

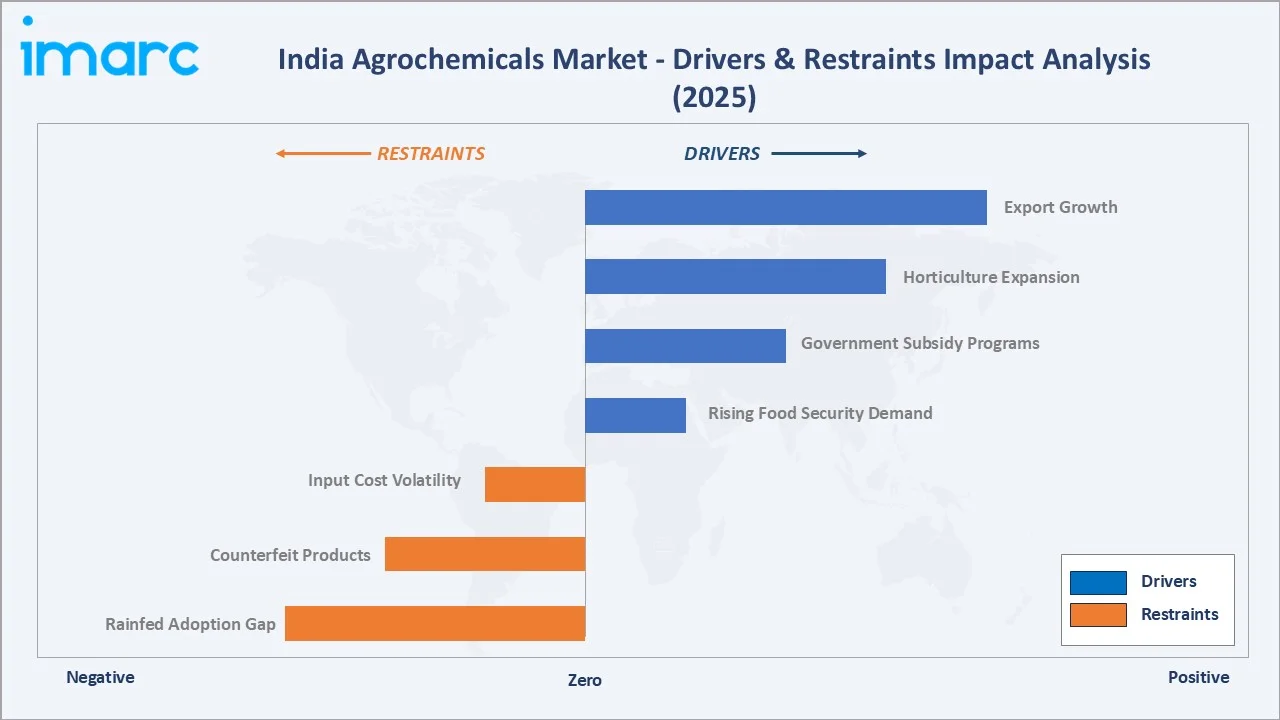

Market Drivers

- Rising Food Security Demand: India's growing population, projected to reach 1.67 billion by 2050, will lead to 481 million tons of food grain production. This drives proportionate increases in agrochemical input intensity, particularly in irrigated areas.

- Government Subsidy Programs: The PM-KISAN direct benefit transfer of INR 6,000 per year is transferred in three equal instalments of INR 2,000, directly into the farmers’ bank accounts, improving agri-input affordability.

- Horticulture Expansion: India’s horticulture output at 362.08 MT in 2024-25 creates high-value demand for specialty fungicides, bio-pesticides, and plant growth regulators. Grapes, mangoes, and vegetables command 8–12 spray applications per season versus 3–5 for cereals, driving per-hectare agrochemical intensity.

- Export Growth: India is the world's fourth-largest agrochemical producer and a top exporter of generic formulations. India’s agrochemical exports increased from US$1.3 billion in FY15 to US$3.3 billion in FY25. Export demand creates scale benefits that lower domestic formulation costs.

Market Restraints

- Input Cost Volatility: Urea and DAP prices remain subject to global gas price fluctuations, with India importing a significant volume of fertilizers, totaling 28.2 million tons and valued at over USD 14.5 billion in FY 2025–26. Rising raw material costs for pesticides, linked to China API pricing, compress manufacturer margins.

- Counterfeit Products: CIB&RC estimates 20–25% of pesticide products in retail circulation are adulterated or mislabeled. Counterfeit agrochemicals undermine crop protection efficacy, create regulatory enforcement burdens, and erode brand value for legitimate manufacturers.

- Rainfed Adoption Gap: India's 51% of cultivated area classified as rainfed sees significantly lower agrochemical intensity than irrigated tracts. Income risk aversion among rainfed farmers and irregular purchase patterns limit market penetration in Odisha, Jharkhand, and Chhattisgarh.

Market Opportunities

- Bio-Pesticides and Sustainable Agro-Inputs: India's bio-pesticide market is projected to grow at 10.49% CAGR from 2026 to 2034, driven by export quality requirements, EU pesticide residue limits, and domestic consumer demand for safe produce.

- Precision Agriculture and AI-Driven Input Optimization: Digital farm management platforms, including DeHaat, Cropin, and ESRI India's agri-GIS, are enabling variable-rate agrochemical application, reducing input waste by 15–30%. Drone-based spraying is growing at 40%+ annually and creates demand for UAV-compatible formulations.

Market Challenges

- Regulatory Compliance and Pesticide Re-evaluation: The CIB&RC's ongoing re-evaluation of 66 pesticides under the 2013 task force mandate creates product registration uncertainty. Companies with pending renewals face temporary market access risks while compliance documentation requirements escalate.

- Climate Variability Impacting Seasonal Demand: Irregular monsoon patterns in 2022 and 2023 suppressed kharif season agrochemical purchases by 8–12% in affected states. Climate-driven demand volatility makes inventory planning challenging for distributors and manufacturers alike.

Emerging Market Trends

.webp)

1. Surge in Bio-Agrochemicals and Integrated Pest Management

The India biopesticides market reached a value of USD 286.8 million in 2025. According to IMARC Group, the market is projected to grow to USD 703.8 million by 2034, registering a CAGR of 10.49% during 2026 to 2034. Neem-based formulations, Trichoderma bio-fungicides, and Bacillus thuringiensis insecticides are gaining adoption among export-oriented farmers needing EU MRL compliance. UPL's acquisition of Arysta LifeScience Inc. has accelerated bio-formulation access across India's rural distribution network.

2. Drone-Based Precision Spraying Adoption

The government has approved the ‘Namo Drone Didi’ scheme as a Central Sector Scheme with an outlay of INR 1,261 crore for the period 2023–24 to 2025–26. The scheme aims to provide drones to selected Women Self-Help Groups (SHGs), enabling them to offer rental services to farmers for agricultural activities such as fertilizer and pesticide application.

3. Nano-Fertilizers and Micronutrient Formulations

IFFCO launched Nano Urea (liquid) commercially in 2021, with cumulative sales exceeding 17 crore bottles by 2023. Nano Urea requires 50–60% less product per hectare versus conventional granular urea while delivering equivalent nitrogen efficiency. Government mandates requiring blending of nano urea with soil-test-based NPK recommendations are creating structural demand displacement within the fertilizer segment toward value-added micronutrient products.

4. Direct-to-Farmer Digital Distribution

E-commerce platforms, including DeHaat (3 million farmer subscribers) and AgroStar (9 million users) are disrupting traditional agri-dealer networks. In FY2024–25, digital agri-input sales crossed INR 2,500 crore, growing at 35% year-on-year. Companies like Bayer, with its Better Life Farming alliance and UPL's OpenAg digital channel, are integrating agronomy advisory with e-commerce to increase per-farm wallet share.

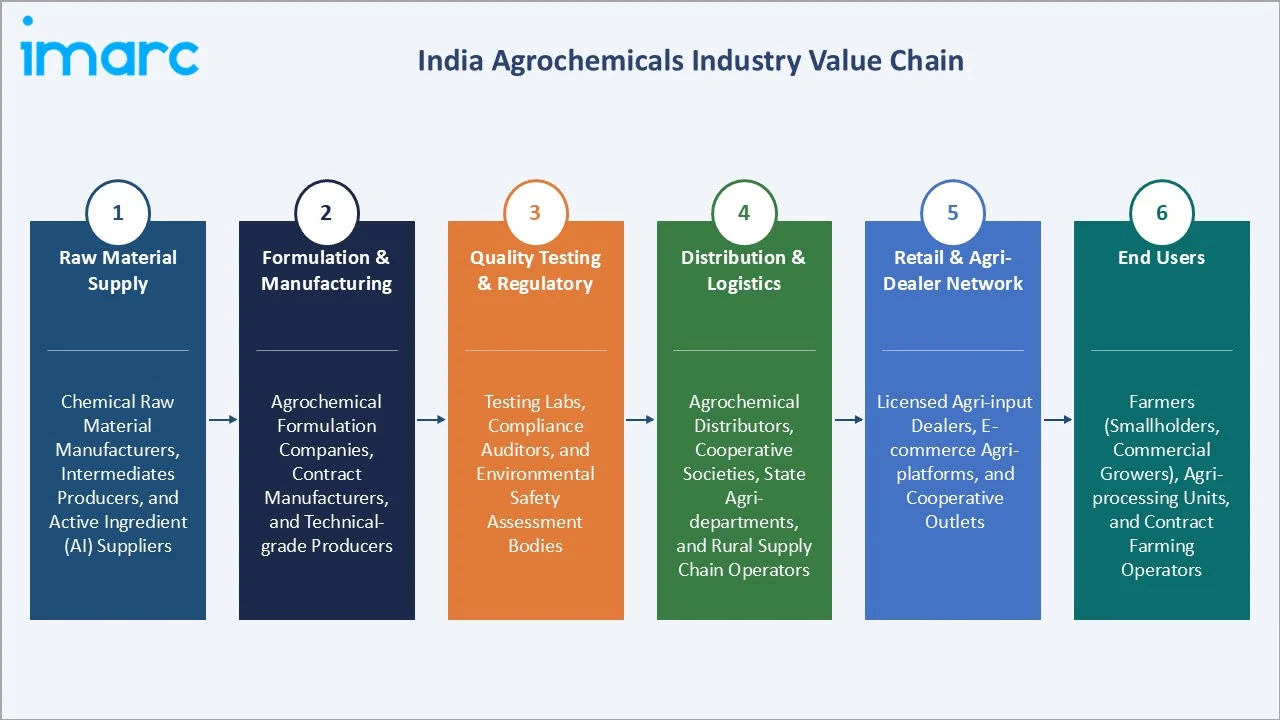

Industry Value Chain Analysis

India's agrochemicals value chain spans raw chemical procurement through farm-gate delivery, with each stage occupied by specialized manufacturers, formulators, and distributors whose efficiency directly influences product availability, pricing, and crop outcome.

|

Stage |

Key Players / Examples |

|

Raw Material Supply |

Chemical raw material manufacturers, intermediates producers, and active ingredient (AI) suppliers |

|

Formulation & Manufacturing |

Agrochemical formulation companies, contract manufacturers, and technical-grade producers |

|

Quality Testing & Regulatory |

Testing labs, compliance auditors, and environmental safety assessment bodies |

|

Distribution & Logistics |

Agrochemical distributors, cooperative societies, state agri-departments, and rural supply chain operators |

|

Retail & Agri-Dealer Network |

Licensed agri-input dealers, e-commerce agri-platforms, and cooperative outlets |

|

End Users |

Farmers (smallholders, commercial growers), agri-processing units, and contract farming operators |

Technology Landscape in the India Agrochemicals Industry

Novel Active Ingredient Molecule Development and Generic Off-Patent Pipeline

India's agrochemical R&D pipeline is bifurcated: MNCs like Bayer AG and BASF drive novel molecule launches, while domestic companies like PI Industries and Dhanuka focus on off-patent generics and new formulation technologies. PI Industries' custom synthesis and manufacturing (CSM) division handles 35+ novel agrochemical molecules for global innovator clients, positioning India as a critical link in the global agro-innovation supply chain.

Biological and Microbiome-Based Crop Protection

Biostimulants and bio-pesticide formulations utilizing Pseudomonas fluorescens, Beauveria bassiana, and Metarhizium anisopliae are gaining commercial traction. The market for bio-stimulants in India is projected to reach USD 319.7 Million by 2034, driven by export market demands and PMFBY-linked quality standards. Companies including Biostadt, Multiplex Bio-Tech, and Camson Bio Technologies are scaling up fermentation capacity to meet demand from organic and export-oriented farming clusters.

Smart Formulations and Controlled-Release Technology

Polymer-coated controlled-release fertilizers (CRFs) and encapsulated pesticides reduce leaching, improve active ingredient bioavailability, and extend residual efficacy. ITC Agribusiness, Coromandel International, and Yara India are expanding their polymer-coated urea and sulfur-coated DAP portfolios, reducing per-hectare nutrient wastage by 15–20% versus conventional granules.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Type |

Fertilizers |

58.0% |

2025 |

|

Application |

Cereals |

42.0% |

2025 |

|

Region |

West and Central India |

31.0% |

2025 |

By Type

Fertilizers command a 58.0% share in 2025. This dominance reflects India's urea production, which increased from 22.715 million metric tons in 2013–14 to 30.667 million metric tons in 2024–25, registering a growth of 35%. Complex fertilizers (NPK blends) are the fastest-growing sub-category within fertilizers, growing at 5.5% CAGR as soil health card recommendations shift consumption toward balanced nutrition.

To access detailed market analysis, Request Sample

Pesticides at 28.0% are driven by rising insecticide demand for paddy stem borer and cotton bollworm management, with herbicide adoption accelerating at 6.2% annually as labor cost inflation makes manual weeding uneconomical. Adjuvants (8.0%) and plant growth regulators (6.0%) are gaining share as precision agriculture and export-oriented farming increase demand for formulation optimization products.

By Application

Cereals dominate at 42.0% in 2025. India's wheat and paddy cultivated area, exceeding 107 million hectares, sustains baseline agrochemical demand through mandated MSP procurement and government extension services. Punjab and Haryana alone consume over 25% of India's total pesticide volume.

Fruits and vegetables at 26.0% are the highest-value application segment, generating premium demand for specialty fungicides and bio-pesticides. Oilseeds at 18.0% sustain soybean and groundnut herbicide and fungicide demand from Maharashtra, Rajasthan, and Gujarat.

Regional Market Insights

West and Central India's market leadership (31.0%, 2025) reflects Maharashtra's position as India's largest pesticide-consuming state and Gujarat's dominant groundnut and cotton belts. Maharashtra's cultivated area (17.43 million ha) and the government’s subsidy for balanced fertilizer use sustain high agrochemical expenditure per farmer household.

North India at 29.0% (2025) is anchored by Punjab, Haryana, and Uttar Pradesh's wheat-paddy rotation cycle, which requires the highest per-hectare pesticide and fertilizer application rates in India. South India at 24.0% benefits from diverse high-value crop profiles, including paddy, sugarcane, coffee, and spices, requiring multiple spray interventions per season.

| Region | Share (2025) | Key Growth Drivers |

|---|---|---|

| West & Central India | 31.0% | Dominant cotton and soybean belt; Maharashtra and Gujarat command large pesticide and fertilizer demand; strong agri-dealer network and crop-intensive farming practices. |

| North India | 29.0% | India's largest wheat and rice production zone; Punjab, Haryana, and Uttar Pradesh drive fertilizer consumption; extensive Kharif and Rabi cropping cycles sustain steady agro-input demand. |

| South India | 24.0% | Diverse crop portfolio including paddy, sugarcane, and spices; Andhra Pradesh and Telangana are top pesticide consumers; Tamil Nadu drives bio-pesticide and specialty agrochemical adoption. |

| East & Northeast India | 16.0% | Emerging agrochemical frontier; rising paddy cultivation in West Bengal, Odisha, and Assam; government subsidy programs and PM-KISAN investments increase farm input accessibility. |

Competitive Landscape

India's agrochemicals market is moderately concentrated, with UPL, Bayer AG, BASF, and PI Industries collectively holding approximately 40–48% of the organized market revenue in 2025. Domestic companies, including Dhanuka Agritech, Rallis India, and Insecticides (India), dominate the branded generics segment.

| Company Name | Key Brands | Market Position | Core Strength |

|---|---|---|---|

| UPL | Brucia, Attack, Centurion EZ, Oorja, Karobiz, Spruce, Avancer Glow, Laurel, Tridium, Uthane M 45, Saaf | Market Leader | Broadest portfolio; strong crop nutrition and crop protection lineup; deep rural distribution network across India |

| Bayer AG | Bicota, Yeoval, Felujit, CAMALUS | Market Leader | Pioneer in herbicides and fungicides; seed treatment expertise; digital farming integration via Climate FieldView |

| BASF | Basagran, Basta, Duvelon, Facet, Kifix, Odyssey, Acrisio, Acrobat, Acrobat Complete, Cabrio Top, Merivon | Strong Challenger | Specialty fungicides and herbicides; innovation in biological and low-residue formulations; strong B2B pharma-agro synergies |

| PI Industries | Osheen, Keefun, Header, Visma, Awkira, Nominee Gold, BIOVITA, HUMESOL | Challenger | CSM export leadership; strong domestic branded generics; R&D-driven pipeline with novel molecules |

Key Company Profiles

UPL

UPL is one of the global agrochemical leaders operating across multiple countries. In India, UPL holds the largest retail distribution network and a comprehensive portfolio spanning crop protection, crop nutrition, and biological formulations.

- Product Portfolio: Brucia, Attack, Centurion EZ, Oorja, Karobiz, Spruce, Avancer Glow, Laurel, Tridium, Uthane M 45, Saaf, among others.

- Recent Developments: In May 2026, UPL, through its subsidiary SWAL, secured FCO registration for Bioclassic in India, enabling the biostimulant to be made available to farmers nationwide. The product is designed to improve branching, photosynthesis, plant vigor, stress tolerance, and yield, while supporting UPL’s broader expansion in sustainable biological solutions.

- Strategic Focus: OpenAg digital channel; bio-pesticide and OpenAg portfolio scaling; debt reduction and margin improvement; specialty crop herbicide pipeline.

Bayer AG

Bayer AG’s subsidiary Bayer CropScience India is one of India's top three agrochemical companies by revenue, with a product portfolio spanning insecticides, fungicides, herbicides, and seed treatment products serving Indian farmers.

- Product Portfolio: Bicota, Yeoval, Felujit, CAMALUS.

- Recent Developments: In August 2025, Bayer AG launched Camalus, a dual-mode insecticide for Indian horticulture farmers, targeting both chewing and sucking pests in crops such as tomato, brinjal, chilli, cabbage, and okra. The product offers long-lasting pest protection, supports Integrated Pest Management, and reduces repeated spray needs.

- Strategic Focus: Climate FieldView digital agronomy integration; biological and sustainable crop protection pipeline; herbicide resistance management in wheat and cotton.

Market Concentration Analysis

India's agrochemicals market exhibits moderate concentration. The top global MNCs (Bayer AG, BASF, UPL) collectively hold approximately 25–30% of organized market revenue, while domestic companies led by UPL, PI Industries, Rallis, and Dhanuka hold 30–35%. The remaining 35–40% is fragmented across 800+ regional formulators and branded generic players.

Consolidation is accelerating through acquisition: UPL's acquisition of Arysta LifeScience Inc. (2019) and BASF's integration of Bayer's divested seed and herbicide businesses are reshaping global competitive dynamics in the India market.

Investment & Growth Opportunities

Fastest Growing Segments

Adjuvants (~5.2% CAGR), bio-pesticides (~10% CAGR), plant growth regulators (~4.9% CAGR), and specialty fungicides (~5.5% CAGR) represent the highest-return investment vectors through 2034. Together, these categories address an incremental market of approximately USD 3.5 Billion by 2034, above 2025 levels, driven by export quality requirements, horticulture expansion, and drone-compatible formulation demand.

Emerging Market Expansion

East and Northeast India's 16.0% regional share represents the highest upside geography for agrochemical penetration, as farm mechanization improves in West Bengal, Odisha, and Assam. PM-KISAN and Kisan Credit Card adoption in eastern India is converting subsistence farmers into regular commercial agri-input buyers, with per-farm input spending growing at 8.5% annually.

Venture and Institutional Investment Trends

- India's agri-tech investment ecosystem attracted USD 900+ Million in FY2024–25, with precision agriculture, drone services, and bio-input startups receiving Series A–C rounds. Agribusiness platforms using agrochemical integration are creating new distribution channels with 30–40% lower cost-to-serve versus traditional dealer networks.

- PLI Scheme for agrochemical technical grade manufacturing (INR 3,500 crore allocation) is enabling domestic AI production in Dahej, Navi Mumbai, and Hyderabad chemical clusters, with import substitution opportunities for 15+ priority molecules currently sourced from China.

Future Market Outlook (2026-2034)

India's agrochemicals market will expand from USD 16.14 Billion in 2025 to USD 23.63 Billion by 2034 at a 4.19% CAGR. Fertilizer volumes will moderate as nano-urea adoption reduces per-hectare quantities, but value growth will be sustained by specialty nutrition products. Pesticide market expansion will be driven by herbicide growth as farm labor costs rise.

By 2034, bio-agrochemicals will represent 12–15% of total market value, driven by EU and US import residue limits compelling Indian export horticulture to adopt integrated pest management. India's agrochemical sector will increasingly pivot toward sustainability, with the government's national target of reducing chemical pesticide use by 50% by 2047 creating structural demand for bio-inputs, precision application technology, and agronomic advisory services bundled with crop protection products.

Research Methodology

Primary Research

Primary research comprised structured interviews with over 90 industry participants, including agrochemical company sales managers, licensed agri-input dealers, farm extension officers, CIB&RC regulatory consultants, and institutional agri-finance representatives across Delhi, Mumbai, Hyderabad, and Pune.

Secondary Research

Secondary research encompassed FAO crop production statistics, CIB&RC pesticide registration databases, IFFCO and NFL annual reports, Department of Agriculture and Farmers' Welfare data, APEDA export statistics, NABARD financial inclusion reports, and industry publications including AgriBusiness & Food Industry magazine and Agropages India.

Forecasting Models

Market size estimations used bottom-up and top-down forecasting, incorporating crop area data, per-hectare application rates, price trend modeling, and company revenue benchmarking. A CAGR of 4.19% reflects consensus validated against CIB&RC registration trends and IMARC's primary expert panel through 2034.

India Agrochemicals Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Types Covered | Fertilizers, Pesticides, Adjuvants, Plant Growth Regulators |

| Applications Covered | Cereals, Oilseeds, Fruits and Vegetables, Others |

| Regions Covered | North India, West and Central India, South India, East and Northeast India |

| Companies Covered | UPL, Bayer AG, BASF, PI Industries, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the India agrochemicals market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the India agrochemicals market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the India agrochemicals industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the India Agrochemicals Market Report

The market reached USD 16.14 Billion in 2025 and is forecast to reach USD 23.63 Billion by 2034 at a 4.19% CAGR.

Fertilizers lead at 58.0% in 2025, driven by India's subsidized urea and DAP distribution and government soil health card initiatives promoting balanced nutrition.

Cereals dominate at 42.0% in 2025, reflecting India's 107 million hectares of wheat and paddy cultivation and government MSP-backed procurement policies.

West and Central India lead at 31.0% in 2025, anchored by Maharashtra's cotton-soybean belt, Gujarat's groundnut farming districts, and Madhya Pradesh's soybean cultivation clusters.

Key players include UPL, Bayer AG, BASF, and PI Industries, competing through product innovation, distribution depth, and digital agronomy platforms.

Adjuvants are the fastest-growing type at ~5.2% CAGR, driven by drone-compatible formulation demand, precision agriculture adoption, and export quality requirements for low-residue crop protection.

Rising food demand, government farm income support (PM-KISAN, PMFBY), horticulture area expansion, growing herbicide adoption driven by labor cost inflation, and bio-pesticide uptake for export compliance are the primary growth catalysts.

Counterfeit and sub-standard products, raw material price volatility tied to China API supply, slow rainfed agriculture adoption, climate variability impact on seasonal demand, and regulatory re-evaluation risk under CIB&RC's pesticide review mandate.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)