India Battery Recycling Market Size, Share, Trends and Forecast by Type, Source, End Use, Material, and Region, 2026-2034

India Battery Recycling Market Size, Share, Trends & Forecast (2026-2034)

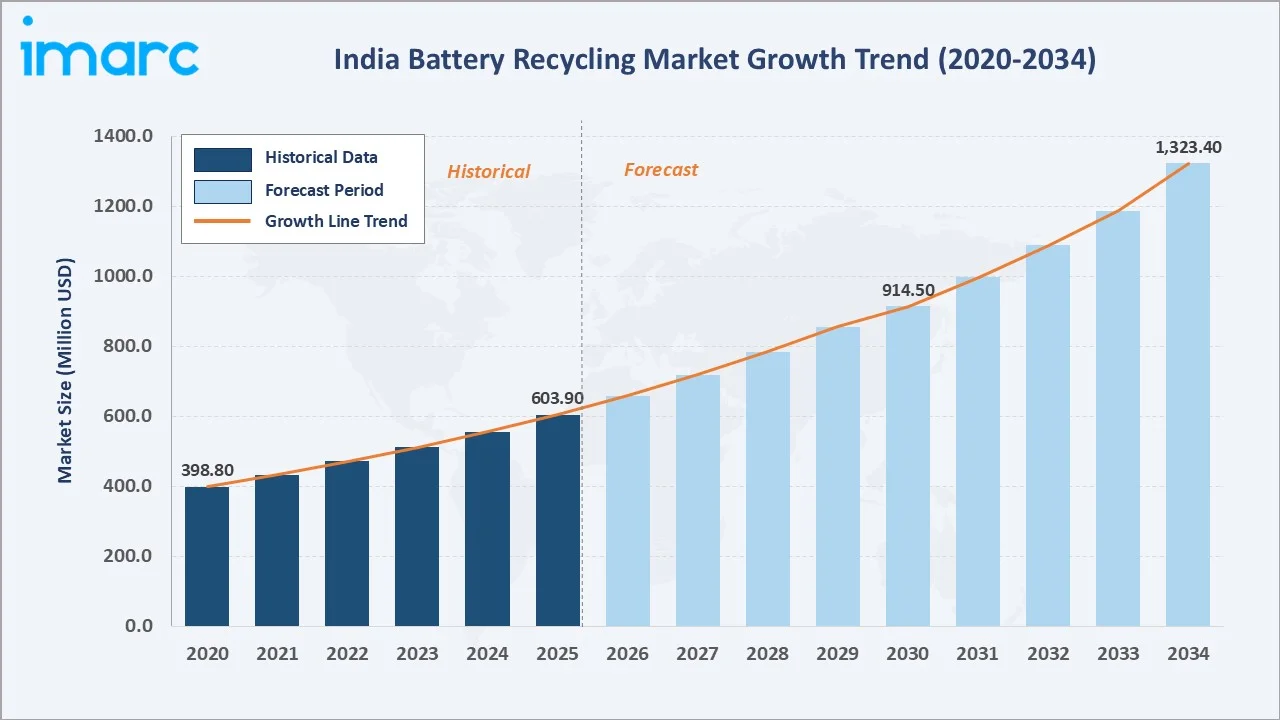

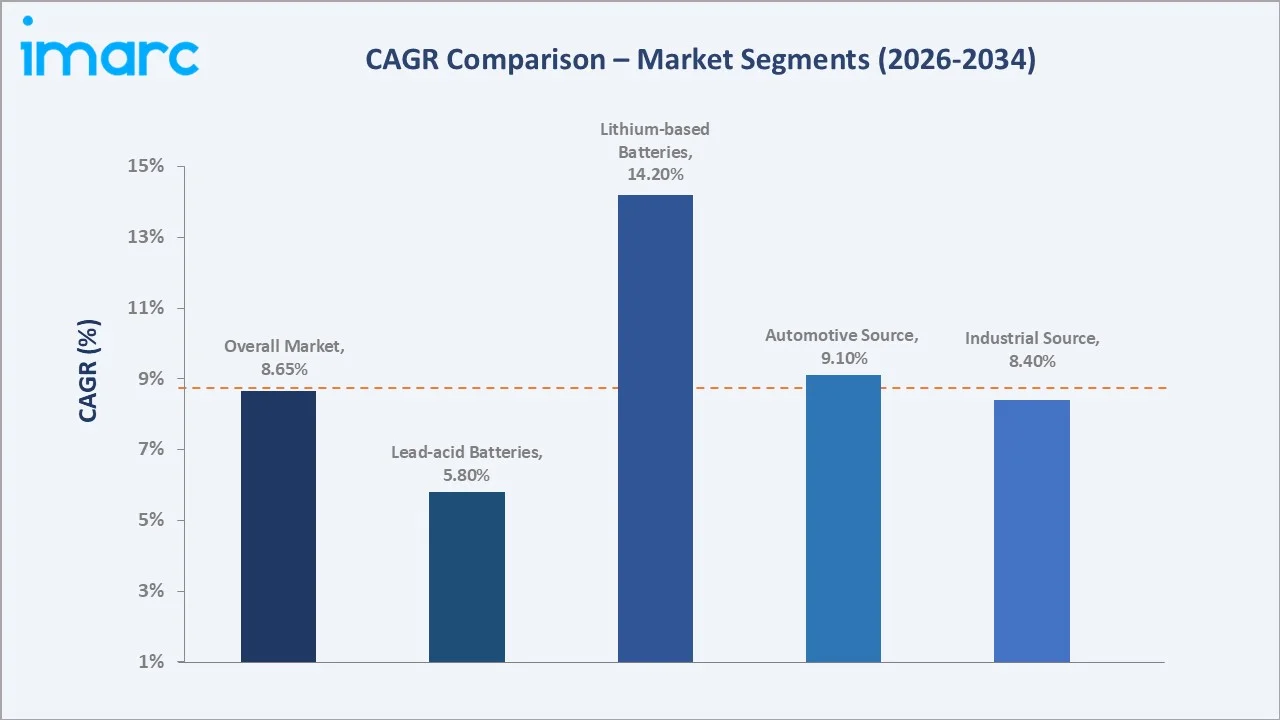

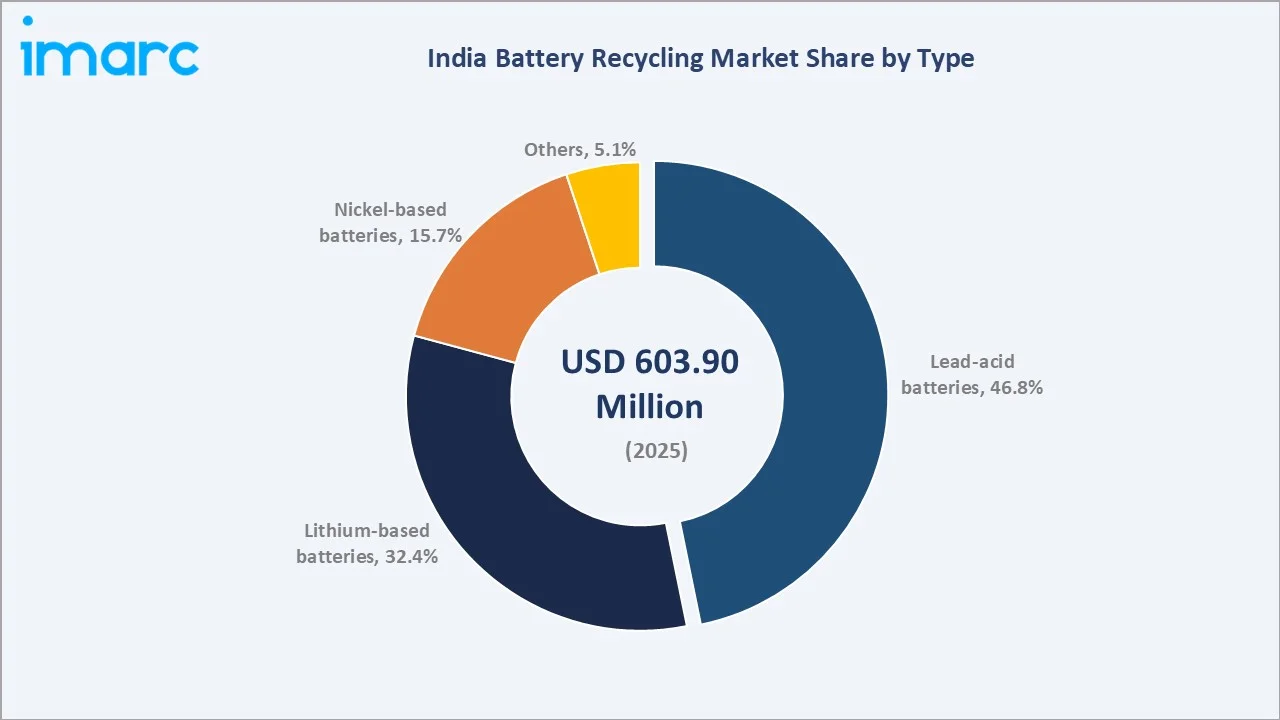

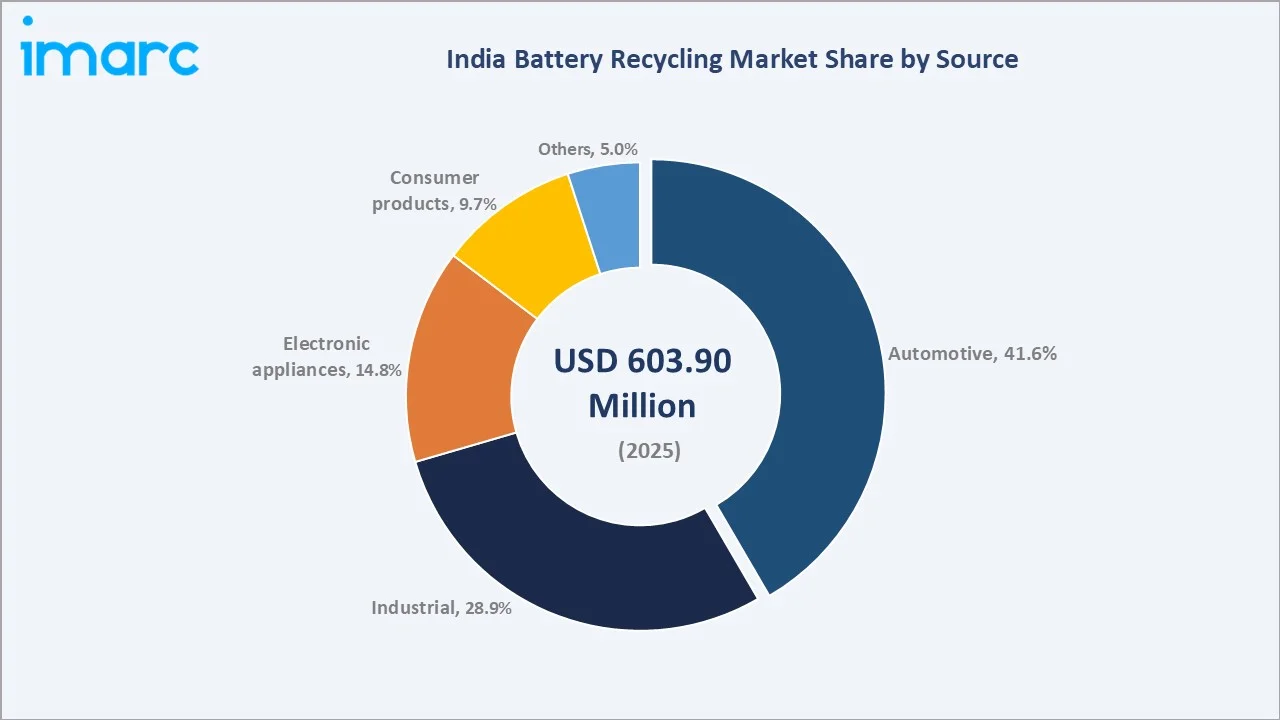

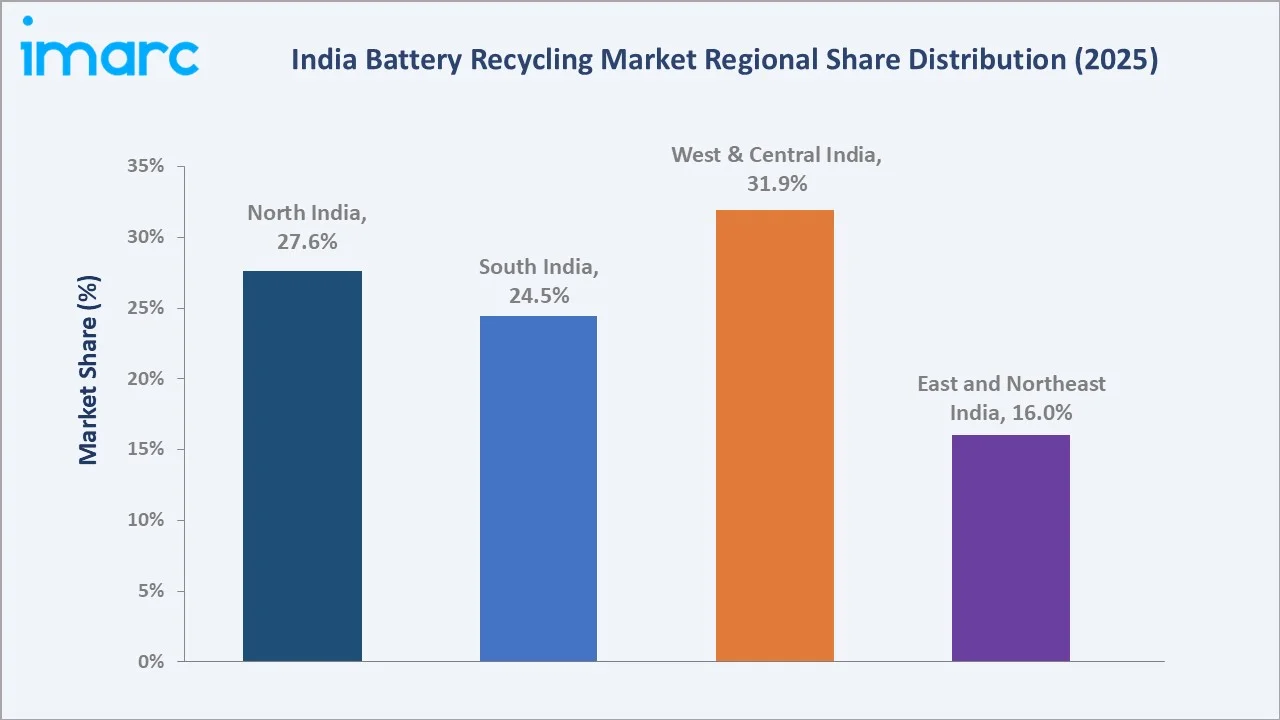

The India battery recycling market reached USD 603.9 Million in 2025 and is projected to reach USD 1,323.4 Million by 2034, growing at a CAGR of 8.65% during 2026-2034. Rising electric vehicle (EV) adoption, stringent Battery Waste Management Rules (BWMR 2022), and surging demand for critical minerals are the primary growth drivers. Lead-acid batteries command the largest share at 46.8% (2025). The automotive source leads at 41.6% (2025). West and Central India accounts for the highest regional share at 31.9%.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 603.9 Million |

|

Forecast Market Size (2034) |

USD 1,323.4 Million |

|

CAGR (2026-2034) |

8.65% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Dominant Type |

Lead-acid Batteries (46.8%, 2025) |

|

Dominant Source |

Automotive (41.6%, 2025) |

|

Leading Region |

West & Central India (31.9%, 2025) |

|

Market Size in 2020 |

USD 398.8 Million |

|

Market Size in 2030 |

USD 914.5 Million |

The India battery recycling market expanded from USD 398.8 Million in 2020 to USD 603.9 Million in 2025, anchored at USD 914.5 Million in 2030, and forecast to reach USD 1,323.4 Million by 2034. India is one of the fastest-growing battery recycling markets in Asia, driven by the convergence of EV proliferation, extended producer responsibility (EPR) regulations, and growing strategic interest in domestic critical mineral recovery.

To get more information on this market, Request Sample

Lithium-based batteries, currently at 32.4% share (2025), are forecast to grow at the highest CAGR among battery types - driven by EV battery retirements and consumer electronics waste. Lead-acid batteries remain dominant due to the vast installed base of vehicles and industrial UPS systems.

Executive Summary

The India battery recycling market is valued at USD 603.9 Million in 2025, reflecting the country's rapid transition toward electrified mobility and the regulatory push for responsible battery lifecycle management. The market expanded from USD 398.8 Million in 2020, growing at a historical CAGR of approximately 8.6%. The market is projected to reach USD 1,323.4 Million by 2034, supported by India's Battery Waste Management Rules (BWMR) 2022 and subsequent 2025 amendments, which mandate Extended Producer Responsibility (EPR) targets for battery collection and recycling.

Lead-acid batteries lead the type segment at 46.8% in 2025, driven by widespread automotive, telecom, and industrial UPS applications. Lithium-based batteries, holding 32.4% in 2025, are the fastest-growing segment owing to accelerating EV adoption, India recorded electric two-wheeler sales of approximately 1.28 million units in 2025 per Vahan Dashboard data. The automotive source commands 41.6% share, reflecting the centrality of vehicle battery waste in the recycling ecosystem. Key companies include Attero Recycling Pvt. Ltd., Lohum Cleantech Pvt. Ltd., Gravita India Ltd., and Exigo Recycling Pvt. Ltd. West and Central India leads at 31.9% share, anchored by Maharashtra's industrial battery volumes and Gujarat's recycling infrastructure.

Key Market Insights

|

Insight |

Data |

|

Dominant Type |

Lead-acid Batteries - 46.8% share (2025) |

|

Dominant Source |

Automotive - 41.6% market share (2025) |

|

Leading Region |

West & Central India - 31.9% share (2025) |

|

Market Opportunity |

EV battery recycling scale-up; critical mineral recovery; second-life battery applications |

|

Top Companies |

Attero Recycling Pvt. Ltd., Lohum Cleantech Pvt. Ltd., Gravita India Ltd., and Exigo Recycling Pvt. Ltd |

Key Analytical Observations Supporting The Above Data:

- Lead-acid Batteries at 46.8%: Lead-acid batteries dominate due to the vast installed base of conventional vehicles, industrial UPS systems, and telecom towers. Recovery of lead from recycled batteries is commercially viable and well-established in India, with companies like Gravita India Ltd. operating at scale.

- Lithium-based Batteries as Fastest Growing: With India's EV sales crossing 2.5 million units annually and battery lifespans of 8-10 years, the EV battery retirement wave is approaching. NITI Aayog projects 128 GWh of recyclable batteries by 2030, of which EVs will comprise approximately 46%.

- Automotive Source at 41.6%: The automotive sector is the single largest source of battery waste due to the enormous fleet of conventional vehicles and the rapidly growing EV fleet. OEM-recycler partnerships are formalizing this channel.

- West & Central India at 31.9%: Maharashtra's large industrial and automotive base, combined with Gujarat's chemical processing expertise, make this region the largest battery recycling hub. The region hosts multiple authorized recycling facilities with significant capacity.

- Market Opportunity: The gap between India's current recycling capacity (~60,000-80,000 tonnes/year) and the projected 128 GWh battery waste by 2030 represents a structural investment opportunity. Critical mineral recovery, particularly lithium, cobalt, and nickel, is driving strategic interest from domestic and global investors.

India Battery Recycling Market Overview

The India battery recycling market encompasses the collection, processing, and material recovery of end-of-life batteries across lead-acid, lithium-based, nickel-based, and other chemistries. The ecosystem integrates battery waste generators (automotive OEMs, industrial users, electronics manufacturers), formal recyclers, material refiners, and secondary material consumers (battery manufacturers, chemical companies).

Macroeconomic factors driving the market include India's EV adoption push under PM E-DRIVE (INR 10,900 crore allocation), government-mandated EPR targets under BWMR 2022 (amended 2025), India's strategic need to reduce import dependence on critical minerals like lithium and cobalt and rising environmental awareness. The market is expanding from a largely informal sector to a formalized, technology-driven industry.

Market Dynamics

To evaluate market opportunities, Request Sample

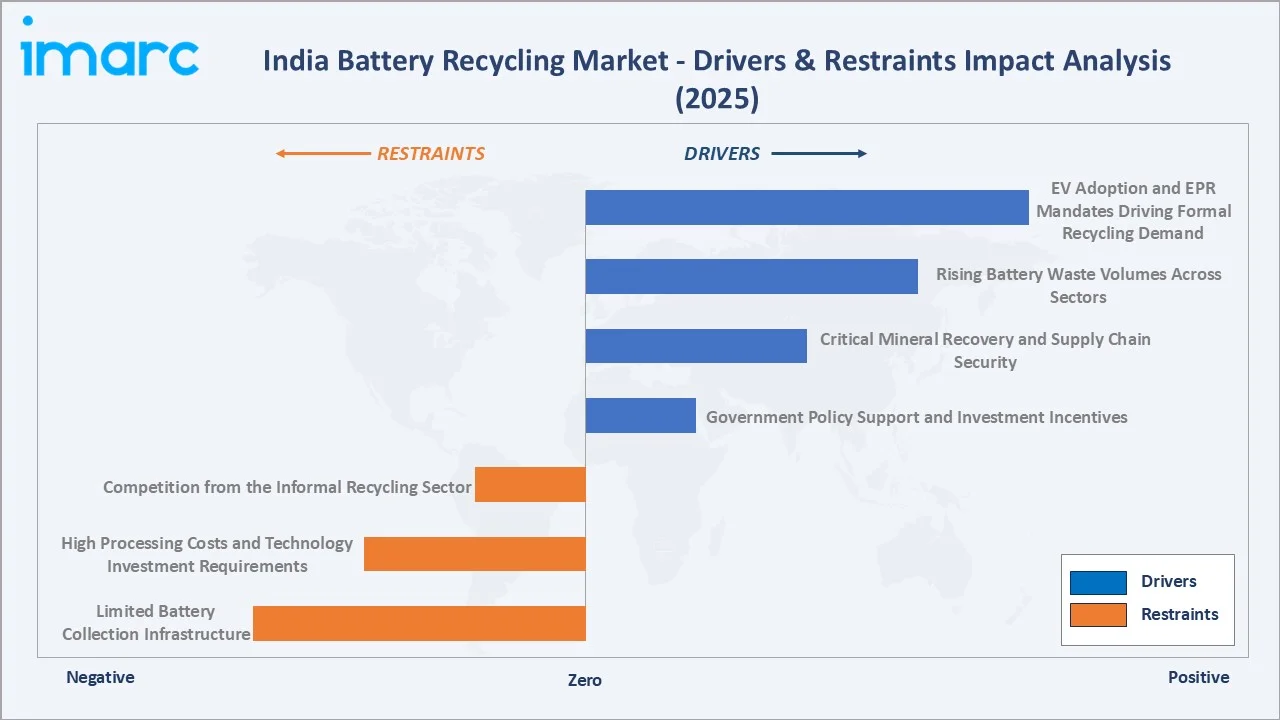

Market Drivers

- EV Adoption and EPR Mandates Driving Formal Recycling Demand: India's EV sales are accelerating sharply. Electric two-wheeler sales reached 1.28 million units as of 2025 per Vahan Dashboard data, while three-wheelers reached 1.11 million units. The typical lithium-ion battery lifespan in EVs is 8-10 years, meaning batteries from the initial EV adoption wave are now approaching end-of-life. The BWMR 2022 mandates manufacturers to meet EPR targets, creating structured demand for formal battery recycling. EPR collection targets begin from 2027-28, providing a regulatory deadline that is spurring preemptive capacity investment.

- Rising Battery Waste Volumes Across Sectors: India's battery waste volumes are growing across automotive (lead-acid and lithium-ion), industrial (UPS, telecom towers), and consumer electronics segments. The Electronics and Information Technology Ministry projected approximately 250 million smartphones sold annually in 2025, each generating battery waste. Telecom tower UPS batteries generate substantial lead-acid waste. Karnataka alone has 32 registered battery recyclers with authorized capacity of approximately 419,056 metric tonnes annually (2025), indicating the industrial scale of waste volumes.

- Critical Mineral Recovery and Supply Chain Security: India imports nearly 100% of its lithium and cobalt requirements. Battery recycling offers a domestic pathway to recover these materials - India's current recycling ecosystem produces about 3,000 tonnes of lithium carbonate annually. Given that NITI Aayog projects 128 GWh of recyclable batteries by 2030, this recovery volume can scale significantly. Government policy under the National Critical Mineral Mission emphasizes domestic material recovery as a strategic priority.

- Government Policy Support and Investment Incentives: The BWMR 2022 and 2025 amendments created a comprehensive framework for battery lifecycle management. PM E-DRIVE allocated INR 10,900 crore to promote EV adoption, directly expanding the future battery recycling addressable market. Financial incentives for companies investing in recycling infrastructure are further accelerating capacity expansion, with Attero Recycling committing ₹8,300 crore over five years (announced May 2024) for e-waste and battery recycling capacity.

Market Restraints

- Competition from the Informal Recycling Sector: India's informal recycling sector handles a significant portion of battery waste - particularly lead-acid batteries - at lower cost structures due to regulatory non-compliance. The Federation of Indian Chambers of Commerce & Industry (FICCI) reported that as of 2023, only 25% of collected batteries were processed using advanced methods. Informal recyclers compete on price, making it difficult for formal operators to capture waste volumes at economically viable collection rates.

- High Processing Costs and Technology Investment Requirements: Hydrometallurgical and pyrometallurgical processing of lithium-ion batteries requires significant capital investment. LICO Materials' Bengaluru facility, announced in December 2024, represents a ₹250 crore investment for 17,500 metric ton capacity. The capital intensity creates a high entry barrier and makes unit economics challenging, particularly for smaller recyclers without economies of scale.

- Limited Battery Collection Infrastructure: Despite the EPR framework, collection infrastructure remains underdeveloped outside major urban centers. Batteries from semi-urban and rural areas often enter informal channels. The absence of standardized take-back programs across all battery categories limits the volume of batteries entering formal recycling streams.

Market Opportunities

- EV Battery Second-Life Applications: An EV battery retains 70-80% of its capacity at end-of-automotive-life. For 8-10 more years, it can power stationary applications - grid storage, solar rooftop systems, rural microgrids - before requiring full material recycling. India's grid stress, rural electrification needs, and rising solar adoption make second-life applications uniquely compelling, creating a high-value intermediate use case that enhances overall battery lifecycle economics.

- Critical Mineral Processing and Export Potential: India can position itself as a regional hub for critical mineral recovery from battery black mass. Processed lithium, cobalt, and nickel compounds command premium global prices. Companies achieving high recovery rates (Attero and Lohum report over 95% material recovery using hydrometallurgical processes) can target export markets, particularly as global battery manufacturers seek supply chain diversification away from China-dominated processing.

Market Challenges

- EPR Implementation Complexity: While the EPR framework is legislated, implementation across India's diverse and fragmented battery distribution ecosystem is complex. Tracking battery sales and ensuring EPR obligation compliance across thousands of importers, manufacturers, and assemblers is administratively challenging. Enforcement capacity at the state pollution control board level is uneven.

- Technology Standardization for Multi-Chemistry Processing: India's battery recycling market spans multiple chemistries (lead-acid, lithium NMC, LFP, lithium cobalt oxide, nickel-metal hydride) each requiring different processing approaches. Recyclers capable of handling only one chemistry face volume constraints. Multi-chemistry processing capability requires significant R&D investment and operational complexity, limiting scalability for smaller players.

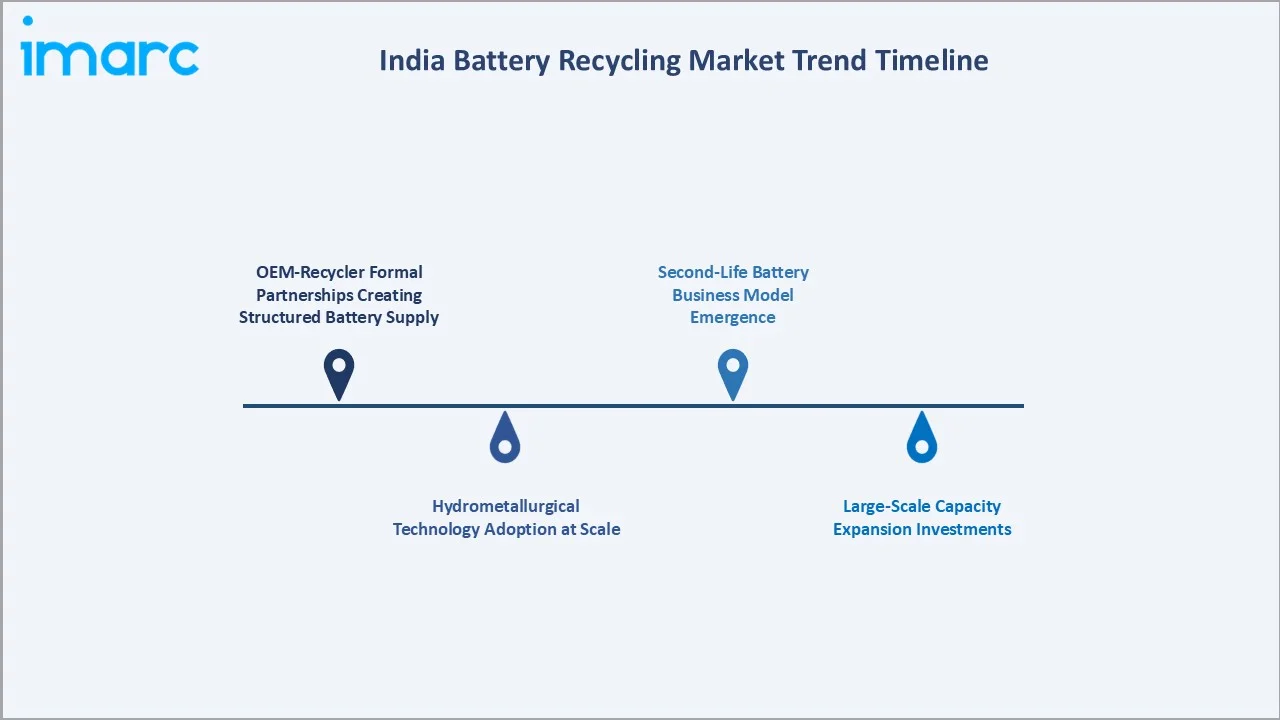

Emerging Market Trends

1. OEM-Recycler Formal Partnerships Creating Structured Battery Supply

Major automotive manufacturers including Tata Motors, MG Motor, and Hyundai have established partnerships with recycling companies such as Attero and Lohum to ensure compliant end-of-life battery management. Attero has partnerships with approximately 90% of Indian auto OEMs. These alliances formalize the battery supply chain for recyclers, providing predictable waste volumes and reducing collection costs, fundamentally transforming battery recycling economics.

2. Hydrometallurgical Technology Adoption at Scale

Seven major Indian companies now employ hydrometallurgical methods for lithium-ion battery recycling, achieving over 95% material recovery rates. In January 2026, the sector recorded expanded investments in hydromet capacity. This technology shift - from pyrometallurgical smelting to chemical leaching and precipitation - enables recovery of a broader range of materials including lithium carbonate, which was previously uneconomical to recover.

3. Second-Life Battery Business Model Emergence

Companies like Lohum Cleantech and Ziptrax Cleantech are developing integrated solutions for both recycling and second-life applications, assessing battery health and determining optimal pathways between refurbishment, repurposing, and recycling. In January 2024, Lohum announced a partnership with Tork Motors to collect and recycle lithium-ion batteries from Tork's Kratos R electric motorcycles. This model maximizes value extraction from the battery lifecycle.

4. Large-Scale Capacity Expansion Investments

In May 2024, Attero Recycling committed ₹8,300 crore over five years to ramp up e-waste and battery recycling capacity to 300,000 metric tons. Lohum Cleantech targets 50,000 TPA capacity by 2026, having raised USD 127 million across 13 funding rounds. Private equity and strategic investors are active in this space.

5. Digital EPR Compliance Platforms and Blockchain Traceability

The complexity of EPR compliance across multi-tier battery supply chains is driving the development of digital tracking platforms. Blockchain-based battery passports and IoT-enabled battery health monitoring systems are being piloted. These platforms enable transparent reporting of battery collection and recycling volumes, facilitating EPR target verification and creating data infrastructure for future circular economy regulation.

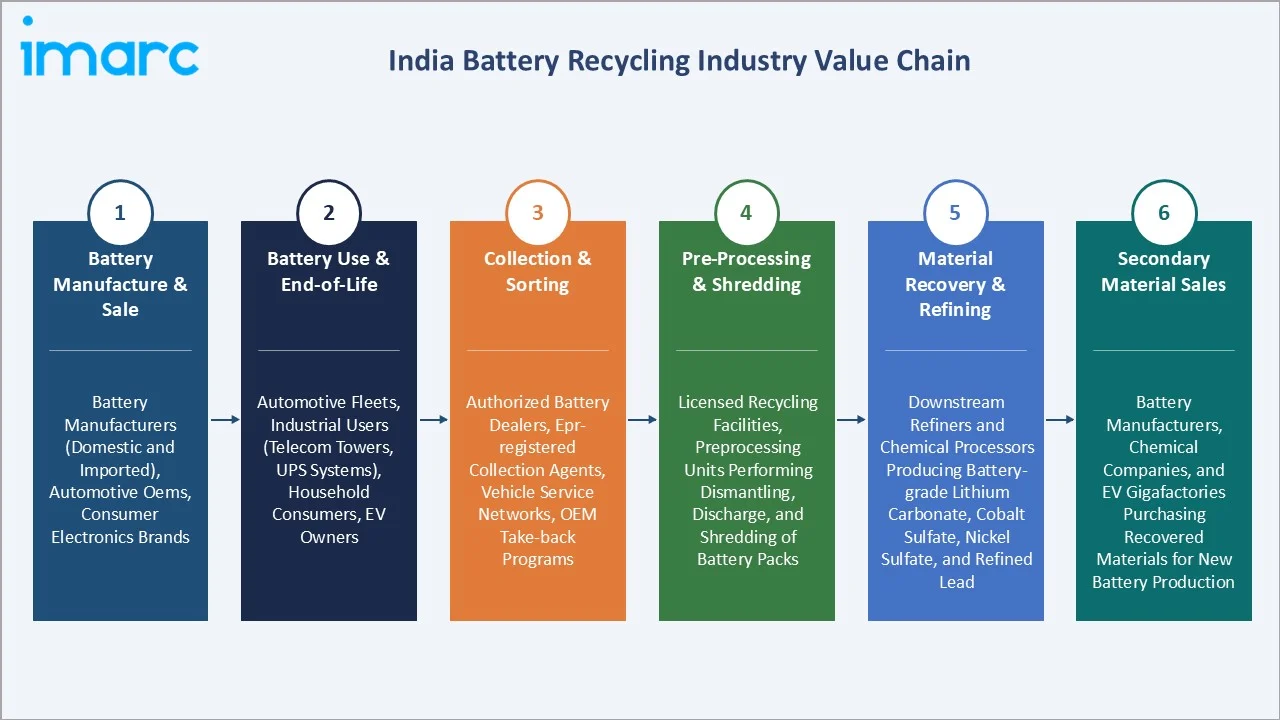

Industry Value Chain Analysis

The India battery recycling value chain spans battery manufacture and sale through end-of-life collection, processing, material recovery, and secondary material reintegration. The value chain is transitioning from informal fragmentation to organized, technology-driven operations driven by EPR mandates.

|

Stage |

Key Participants |

|

Battery Manufacture & Sale |

Battery manufacturers (domestic and imported), automotive OEMs, consumer electronics brands |

|

Battery Use & End-of-Life |

Automotive fleets, industrial users (telecom towers, UPS systems), household consumers, EV owners |

|

Collection & Sorting |

Authorized battery dealers, EPR-registered collection agents, vehicle service networks, OEM take-back programs |

|

Pre-Processing & Shredding |

Licensed recycling facilities, preprocessing units performing dismantling, discharge, and shredding of battery packs |

|

Material Recovery & Refining |

Downstream refiners and chemical processors producing battery-grade lithium carbonate, cobalt sulfate, nickel sulfate, and refined lead |

|

Secondary Material Sales |

Battery manufacturers, chemical companies, and EV gigafactories purchasing recovered materials for new battery production |

The collection and sorting stage is India battery recycling value chain's most commercially critical bottleneck. Informal channels divert significant battery volumes away from formal processors. EPR regulations are gradually formalizing this stage. The material recovery stage offers the highest value addition - companies achieving battery-grade output from recycled material command significant price premiums over commodity-grade output.

Technology Landscape in the India Battery Recycling Industry

Hydrometallurgical Recycling Technology

Hydrometallurgical processing is the dominant advanced technology in India's battery recycling sector. The process employs chemical leaching, solvent extraction, and precipitation to recover lithium, cobalt, nickel, and manganese from battery black mass. Leading companies Attero Recycling and Lohum Cleantech have achieved over 95% material recovery rates using proprietary hydrometallurgical processes. Attero holds over 45 global patents for in-house recycling technologies. The LICO Materials facility in Bengaluru uses hydrometallurgy to produce battery-grade metal salts for gigafactories.

Pyrometallurgical Recycling Technology

Pyrometallurgical processing - high-temperature smelting of battery components - is used extensively for lead-acid battery recycling, where Gravita India Ltd. has established leadership leveraging its global smelting expertise. While effective for recovering cobalt, nickel, and copper from lithium-ion batteries, pyrometallurgy has limited lithium recovery efficiency. The technology remains commercially relevant for multi-chemistry processing facilities handling mixed battery waste streams.

Battery State-of-Health Assessment Technology

Prior to recycling or repurposing, advanced battery health assessment technologies determine the remaining useful life of end-of-life batteries. Electrochemical impedance spectroscopy, machine learning-based degradation models, and IoT sensor integration are being deployed by companies like Ziptrax Cleantech and Lohum Cleantech to identify batteries eligible for second-life applications versus direct recycling. This technology optimization significantly enhances the economic return from battery end-of-life management.

Direct Recycling and Cathode Regeneration

Emerging direct recycling technologies aim to restore cathode active materials without complete chemical breakdown, preserving the crystalline structure and reducing processing energy. Tata Chemicals is pioneering cathode regeneration approaches in India, leveraging its chemical engineering expertise. This technology, while at early commercial stage, could reduce recycling costs by 30-40% compared to full hydrometallurgical processing for certain lithium-ion chemistries.

Market Segmentation Analysis

The report covers the following key segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Type |

Lead-acid Batteries |

46.8% |

2025 |

|

Source |

Automotive |

41.6% |

2025 |

|

End Use |

🔒 |

🔒 |

2025 |

|

Material |

🔒 |

🔒 |

2025 |

|

Region |

West & Central India |

31.9% |

2025 |

By Type

Lead-acid batteries lead the India battery recycling market at 46.8% share in 2025. The segment's dominance reflects India's vast fleet of conventional internal combustion engine vehicles, industrial UPS systems, and telecom backup power installations - all relying on lead-acid batteries with a typical replacement cycle of 3-5 years. Lead recovery from these batteries is commercially mature, with established smelting and refining infrastructure.

To access detailed market analysis, Request Sample

Lithium-based batteries hold 32.4% share in 2025 and are the fastest-growing segment, driven by EV battery retirements, consumer electronics waste growth, and industrial energy storage system deployments. Nickel-based batteries at 15.7% serve industrial and specialized applications. The "Others" category at 5.1% includes alkaline and zinc-based batteries.

By Source

The automotive source segment leads at 41.6% in 2025, driven by the country's massive vehicle fleet and the growing EV battery retirement pipeline. India's over 300 million registered vehicles generate continuous lead-acid battery replacement demand, while the nascent but rapidly growing EV fleet is creating the foundation for future lithium-ion battery recycling volumes. Formal OEM-recycler partnerships are consolidating this supply channel.

Industrial sources account for 28.9% - driven by telecom tower UPS batteries (India has over 700,000 telecom towers), data center backup systems, and manufacturing UPS installations. Electronic appliances contribute 14.8%, reflecting the scale of India's consumer electronics market with approximately 250 million smartphones sold annually. Consumer products follow at 9.7%, with others comprising 5.0%.

Regional Market Insights

|

Region |

Share (2025) |

Key Drivers & Characteristics |

|

West & Central India |

31.9% |

Largest regional market anchored by Maharashtra's automotive and industrial battery volumes. Gujarat's chemical processing expertise supports downstream material refining. Mumbai's financial ecosystem supports investment in recycling infrastructure. |

|

North India |

27.6% |

Delhi-NCR's dense automotive and consumer electronics market generates high battery waste volumes. The Noida-Gurugram industrial corridor hosts major recycling companies including Attero and Lohum. Uttar Pradesh and Punjab's manufacturing bases contribute industrial battery waste. |

|

South India |

24.5% |

Bengaluru's EV adoption is among India's highest. Tamil Nadu's automotive manufacturing and Hyderabad's industrial base contribute to battery waste generation. |

|

East & Northeast India |

16.0% |

Smallest but growing regional market. West Bengal's Kolkata industrial base and Odisha's mining and industrial sector generate meaningful battery waste. Northeastern states are in early stages of formal battery recycling infrastructure development. |

West and Central India's 31.9% leadership reflects Maharashtra's concentration of automotive OEMs (Tata Motors, Mahindra), industrial battery users, and the state's progressive recycling infrastructure policy. North India's 27.6% is underpinned by the Delhi-NCR's role as India's largest consumer market and the presence of leading battery recycling companies headquartered in the Noida-Gurugram corridor.

South India's 24.5% reflects Karnataka's advanced battery recycling regulatory environment and Bengaluru's rapid EV adoption (Karnataka leads with approximately 6,097 EV charging stations as of mid-2025). East and Northeast India at 16.0% is currently underdeveloped but is growing above the overall market CAGR as industrial development and rising consumer electronics penetration drive battery waste volumes.

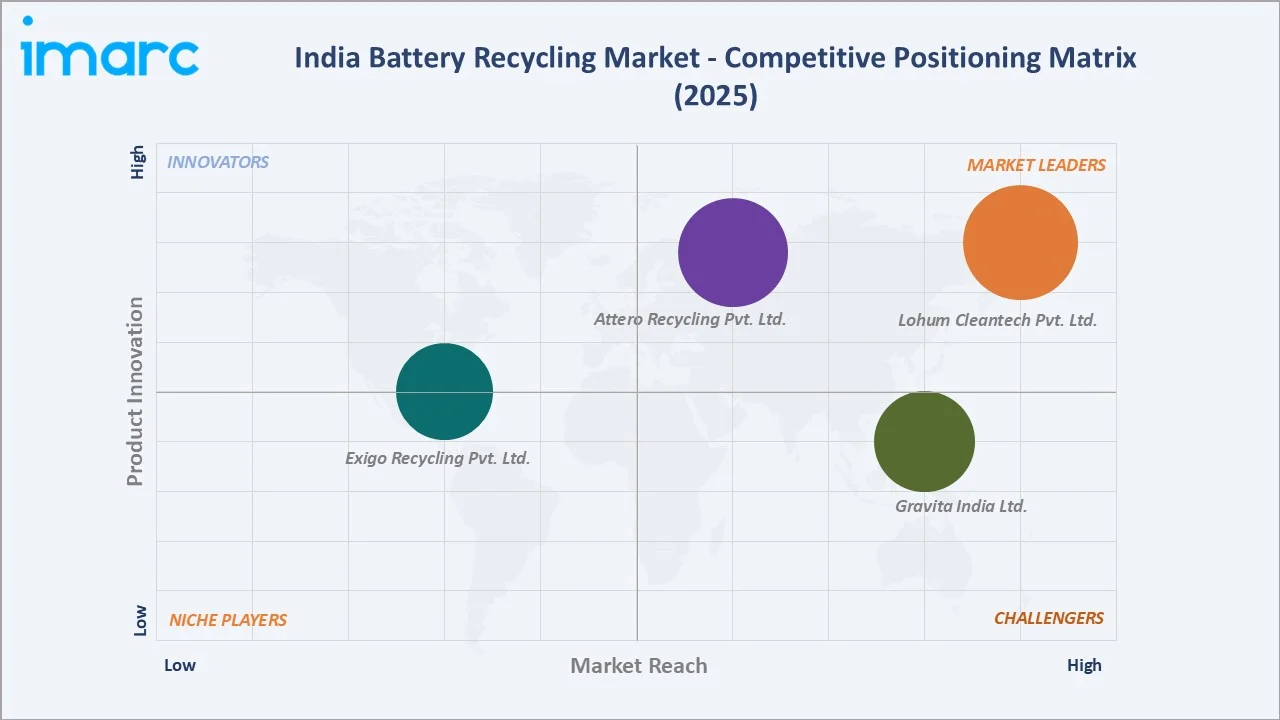

Competitive Landscape

The India battery recycling competitive landscape is evolving from a fragmented, largely informal market to a structured industry with identifiable leaders. The formal sector is dominated by technology-driven companies with proprietary processing capabilities, regulatory compliance infrastructure, and OEM partnerships. Competition is intensifying as EPR mandates formalize battery waste flows and EV battery volumes approach commercial scale for recycling.

|

Company |

Key Specialization |

Market Position |

Core Strength |

|

Attero Recycling Pvt. Ltd. |

Li-ion & e-waste battery recycling |

Market Leader |

Proprietary, patented deep-tech processes that achieve industry-leading recovery rates while maintaining a strict commitment to a zero-carbon footprint. |

|

Lohum Cleantech Pvt. Ltd. |

Hydrometallurgical recycling & second-life applications |

Market Leader |

Circular-economy battery lifecycle management, NEETM Technology |

|

Gravita India Ltd. |

Lead-acid & Li-ion battery recycling |

Strong Challenger |

Vertically integrated; global smelting expertise; publicly listed with strong balance sheet |

|

Exigo Recycling Pvt. Ltd. |

Multi-chemistry battery recycling |

Emerging Player |

Growing EPR compliance capabilities; expanding collection network across metros |

The competitive landscape's most significant dynamic is the race to scale capacity ahead of the projected EV battery retirement wave (2027-2030). Companies investing now in hydrometallurgical processing capability and OEM partnerships are positioning for structural first-mover advantage, as battery waste supply contracts with major OEMs are being established on multi-year terms.

Key Company Profiles

Attero Recycling Pvt. Ltd.

Attero Recycling is India's largest e-waste and lithium-ion battery recycling company, headquartered in Noida, Uttar Pradesh, with primary processing operations in Uttarakhand. The company is globally recognized as one of the most advanced lithium-ion battery recycling enterprises.

- Key Specialization: Hydrometallurgical recycling of lithium-ion batteries; e-waste processing; cathode active material recovery.

- Recent Developments: In December 2025, Attero announced ₹150 crore to enhance e-waste recycling capacity by 1 lakh tonnes annually, increasing the total capacity to 2,44,000 tonnes.

- Strategic Focus: Becoming India's largest and most technologically advanced battery recycling facility; leveraging 45+ global patents to achieve industry-leading recovery rates; expanding OEM partnerships across the automotive sector.

Lohum Cleantech Pvt. Ltd.

Lohum Cleantech is a leading clean energy materials company focused on battery recycling and second-life battery applications. Headquartered in Greater Noida, Lohum has positioned itself as a leader in the circular economy for lithium-ion batteries.

- Key Specialization: Integrated hydrometallurgical recycling; second-life battery assessment and repurposing; critical mineral recovery (lithium, cobalt, nickel).

- Recent Developments: In November 2025, LOHUM announced to raise INR 131.4 crore (about USD 15 million) in a pre-Series C funding round. The investment was led by Growth I9 Opportunity LLP, along with existing investors such as Baring Private Equity, Singularity Growth, Asiana Fund and others.

- Strategic Focus: Scaling to 50,000 TPA capacity by 2026; targeting four million metric tonnes of battery recycling; expanding second-life battery business for grid storage and industrial applications.

Market Concentration Analysis

The India battery recycling market is highly fragmented overall, with the formal sector dominated by a small number of technologically advanced players and the informal sector comprising thousands of small operators. In the formal lithium-ion battery recycling segment, Lohum Cleantech commands approximately 70% market share (as of 2025 estimates). Attero Recycling and Gravita India Ltd. are the other significant formal players.

In lead-acid battery recycling, the market is more fragmented with both formal and informal operators. Gravita India leads the organized lead-acid recycling segment, while numerous smaller smelters operate in the informal economy. The informal sector handles a significant portion of lead-acid battery waste due to established dealer networks and lower regulatory compliance costs.

Market concentration is evolving through consolidation. EPR mandates favor larger, compliant operators with the systems to report collection and recycling volumes. OEM partnerships are channeling battery waste to established formal recyclers. Investment inflows (Lohum's USD 127 million, Attero's ₹8,300 crore commitment) are widening the gap between formal sector leaders and informal operators, accelerating market formalization and concentration.

Investment & Growth Opportunities

Highest Growth Segments

Lithium-based battery recycling offers the highest growth trajectory, driven by EV battery retirements projected to generate 128 GWh of recyclable batteries by 2030 per NITI Aayog estimates. Second-life battery applications represent a high-value intermediate market. Critical mineral recovery, particularly battery-grade lithium carbonate (currently priced at USD 10,000-15,000 per tonne globally), offers significant revenue upside for companies achieving high-purity output. Hydrometallurgical processing capacity expansion represents the capital deployment priority.

Emerging Investment Opportunities

- EV Battery Collection Infrastructure: The EPR framework creates demand for formal, technology-enabled battery collection platforms. Investment in collection logistics, battery health assessment, and digital EPR compliance systems addresses a structural infrastructure gap.

- Hydrometallurgical Processing Capacity: The 40x scale-up gap between current capacity (~60,000-80,000 tonnes/year) and 2030 recycling demand (128 GWh equivalent) requires significant investment in hydrometallurgical plants. Companies achieving gigafactory-grade output quality can secure long-term supply contracts with domestic and global battery manufacturers.

- Second-Life Battery Applications: Grid storage, solar microgrids, and EV charging infrastructure represent high-demand markets for repurposed EV batteries.

- Critical Mineral Refining: Downstream refining of black mass processing output into battery-grade lithium carbonate, cobalt sulfate, and nickel sulfate is a high-value, strategically important opportunity. India's National Critical Mineral Mission may provide policy support for domestic refining capacity.

Future Market Outlook (2026-2034)

The India battery recycling market is projected to grow from USD 603.9 Million in 2025 to USD 1,323.4 Million by 2034, delivering an 8.65% CAGR over the forecast period. The market's anchor value of USD 914.5 Million in 2030 represents a structural inflection - the point at which EV battery retirement volumes from India's early EV adoption cohort begin contributing meaningfully to recycling throughput.

Three structural forces define market growth through 2034: India's EV adoption trajectory creating the world's fastest-growing lithium-ion battery recycling pipeline; EPR regulation creating structured, formal demand for compliant recycling services; and global critical mineral supply chain realignment creating export demand for India-recovered materials. The lithium-based battery segment is expected to surpass lead-acid in market share by approximately 2030-2032, fundamentally reshaping the competitive landscape.

Technology advancement will be a key differentiator. Companies achieving battery-grade output from hydrometallurgical processing will command significant price premiums. Direct recycling technologies, if commercially proven, could reduce processing costs by 30-40%. Consolidation is expected to accelerate, with two to three dominant formal sector players emerging by 2030, while the informal sector faces increasing regulatory pressure.

Research Methodology

Primary Research

Primary research comprised structured interviews with India battery recycling industry stakeholders including recycling facility directors, EPR compliance officers, battery manufacturer representatives, automotive OEM sustainability managers, and government regulatory officials. Interviews covered battery waste volumes, collection efficiency, processing technology performance, and market pricing.

Secondary Research

Secondary research encompassed India Battery Waste Management Rules (2022 and 2025 amendments) from the Ministry of Environment, Forest and Climate Change; Vahan Dashboard EV sales data; NITI Aayog battery recycling projections; company annual reports (Gravita India Ltd., Lohum Cleantech); FICCI reports on battery recycling industry; BDO India capacity assessments; and Karnataka State Pollution Control Board authorized recycler data. Over 50 secondary sources were reviewed.

Forecasting Models

Market revenue forecasts were developed using a battery waste volume model: India's registered vehicle fleet by type multiplied by battery replacement frequency and average battery value per unit, aggregated across battery chemistries. EV adoption projections applied battery life cycle timing to forecast lithium-ion recycling volumes. EPR target multipliers applied to formal sector capture rates. Bottom-up segment models reconciled to top-down macroeconomic growth constraints.

India Battery Recycling Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Types Covered | Lead-acid Batteries, Nickel-based Batteries, Lithium-based Batteries, Others |

| Sources Covered | Industrial, Automotive, Consumer Products, Electronic Appliances, Others |

| End Uses Covered | Reuse, Repackaging, Extraction, Others |

| Materials Covered | Manganese, Iron, Lithium, Nickel, Cobalt, Lead, Aluminium, Others |

| Regions Covered | North India, West and Central India, South India, East and Northeast India |

| Companies Covered | Attero Recycling Pvt. Ltd., Lohum Cleantech Pvt. Ltd., Gravita India Ltd., Exigo Recycling Pvt. Ltd., etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the India battery recycling market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the India battery recycling market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the India battery recycling industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the India Battery Recycling Market Report

The India battery recycling market reached USD 603.9 Million in 2025, driven by EV adoption, Battery Waste Management Rules 2022 EPR mandates, and rising demand for critical mineral recovery from end-of-life batteries.

The India battery recycling market grows at a CAGR of 8.65% during 2026-2034, reaching USD 1,323.4 Million by 2034, driven by EV battery retirements, EPR regulation, and critical mineral recovery demand.

Lead-acid batteries lead at 46.8% share in 2025, driven by India's vast vehicle fleet, telecom UPS systems, and industrial backup power. Lead-acid recycling infrastructure is commercially mature and well-established.

The automotive source dominates at 41.6% in 2025, driven by India's 300+ million registered vehicles generating continuous battery replacement demand and the growing EV fleet creating future lithium-ion recycling volumes.

West and Central India leads at 31.9% in 2025, anchored by Maharashtra's automotive and industrial battery waste volumes and Gujarat's chemical processing expertise supporting downstream material refining.

Leading companies include Attero Recycling Pvt. Ltd., Lohum Cleantech Pvt. Ltd., Gravita India Ltd., and Exigo Recycling Pvt. Ltd., among others operating in the formal recycling sector.

The India battery recycling market is projected at USD 914.5 Million in 2030, representing a structural inflection as EV battery retirements begin contributing meaningfully to lithium-ion recycling throughput.

The Battery Waste Management Rules (BWMR) 2022 and its 2025 amendments govern battery recycling in India, mandating EPR targets for manufacturers, with formal collection targets beginning from FY 2027-28.

The India battery recycling market was valued at USD 398.8 Million in 2020, anchoring the historical period (2020-2025) baseline from which the market expanded to USD 603.9 Million by 2025.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)