India Biopesticides Market Size, Share, Trends and Forecast by Type, Source, Mode of Application, Crop Type, and Region, 2026-2034

India Biopesticides Market Size, Share, Trends & Forecast (2026-2034)

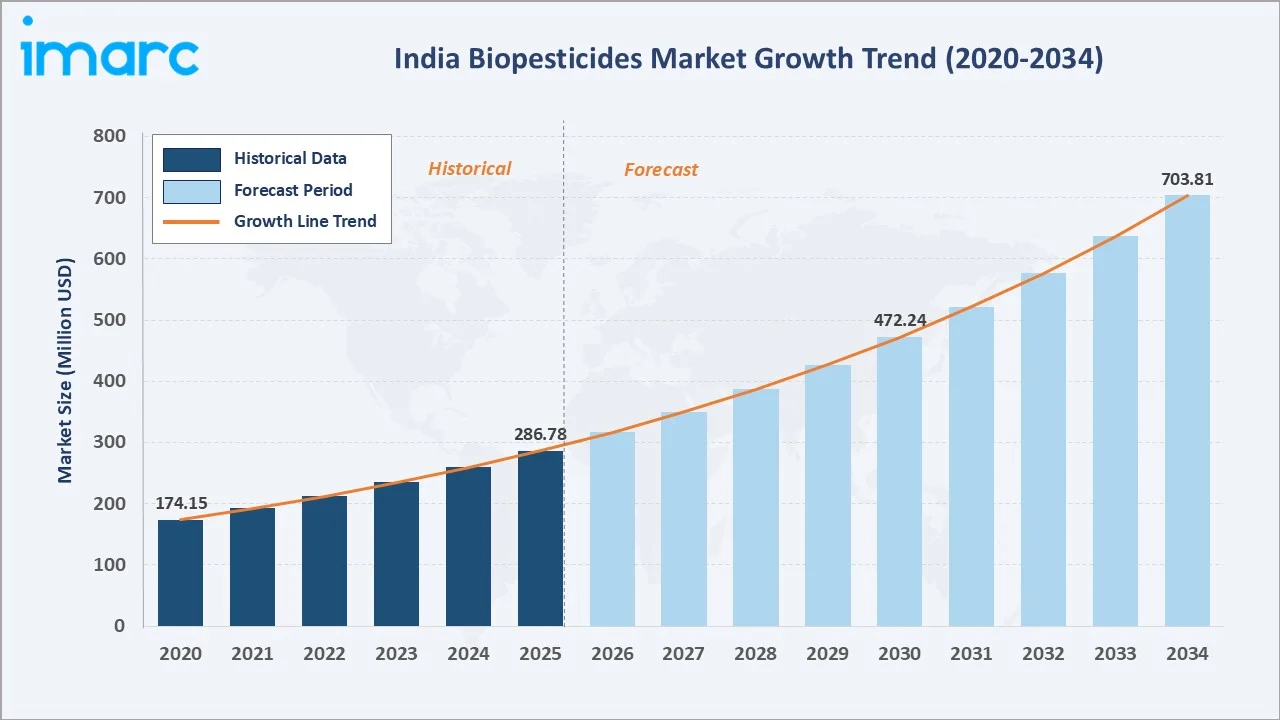

The India biopesticides market was valued at USD 286.78 Million in 2025 and is projected to reach USD 703.81 Million by 2034, exhibiting a CAGR of 10.49% during 2026-2034. Accelerating demand for residue-free agricultural produce, mounting pressure to reduce synthetic chemical dependency, and expanding government incentive programs are the primary drivers shaping the market growth.

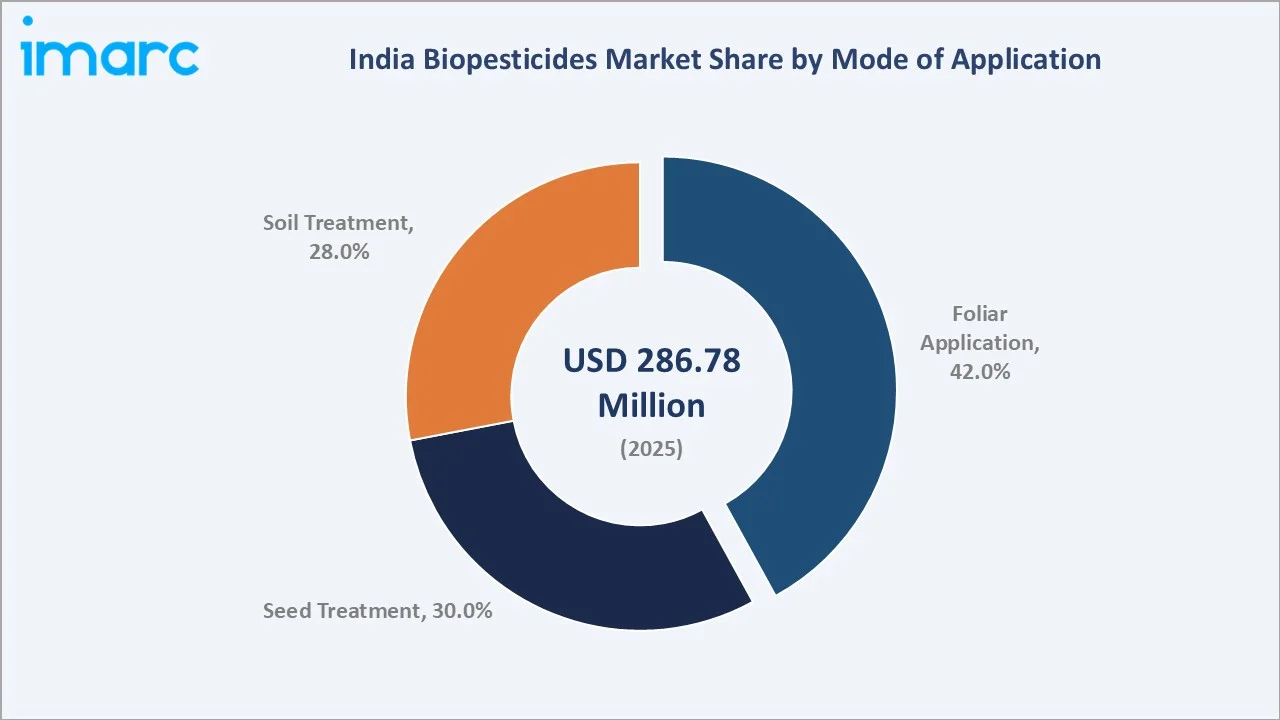

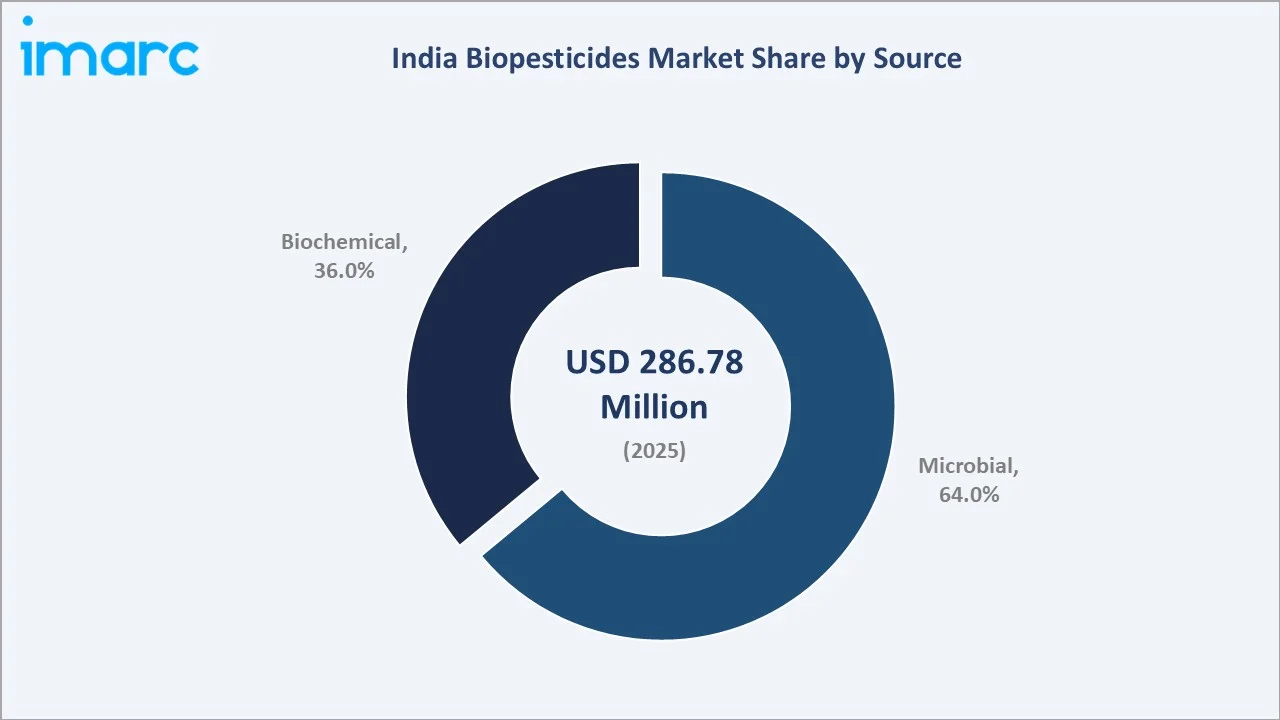

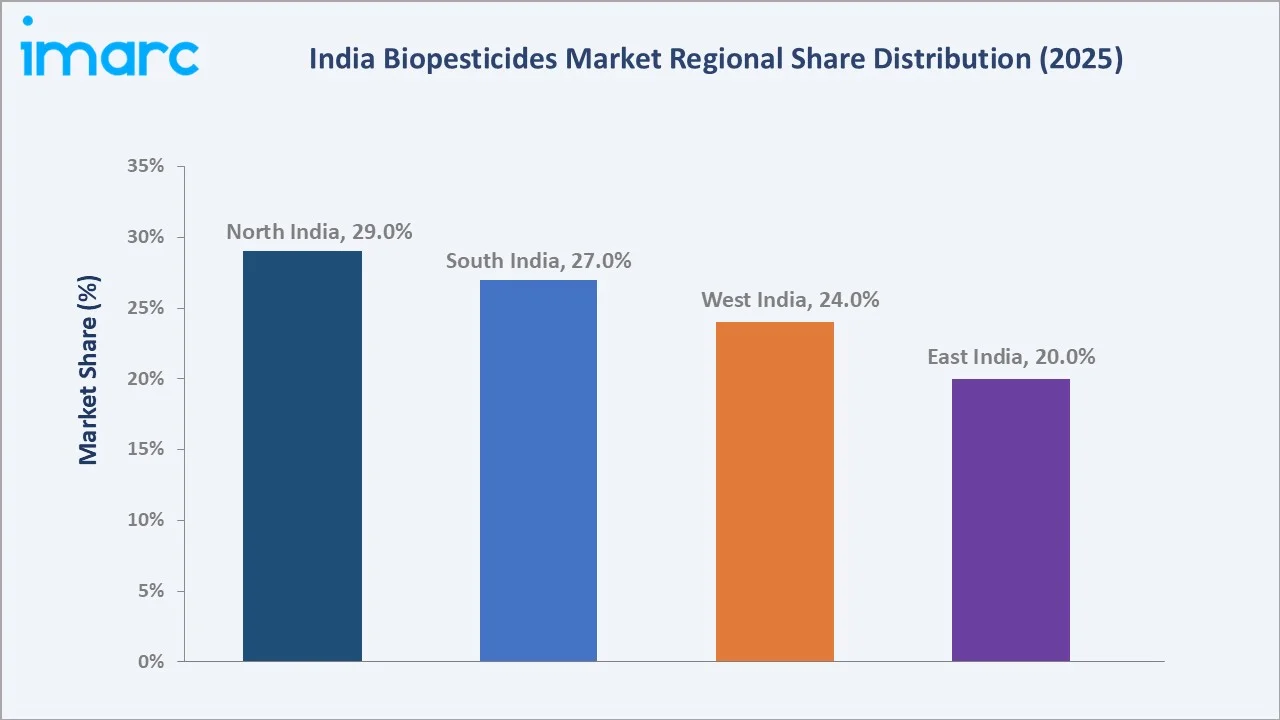

Foliar application commands a 42.0% majority share in the mode of application segment, microbial leads the source segment at 64.0%, and North India holds a 29.0% regional share.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 286.78 Million |

|

Forecast Market Size (2034) |

USD 703.81 Million |

|

CAGR (2026-2034) |

10.49% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

North India (29.0%, 2025) |

|

Fastest Growing Region |

South India (~11.8% CAGR, 2026-2034) |

|

Leading Mode of Application |

Foliar Application (42.0%, 2025) |

|

Leading Source |

Microbial (64.0%, 2025) |

The India biopesticides market expanded from USD 174.15 Million in 2020 to USD 286.78 Million in 2025, reflecting consistent double-digit growth driven by rising organic farming mandates, government subsidy programs for bio-inputs, and strengthening distribution networks reaching tier-2 and tier-3 agricultural districts. Anchored at USD 472.24 Million in 2030, the forecast to USD 703.81 Million by 2034 is underpinned by broader crop coverage, next-generation microbial strain development, and the accelerating transition away from chemical pesticides in export-oriented agriculture.

To get more information on this market, Request Sample

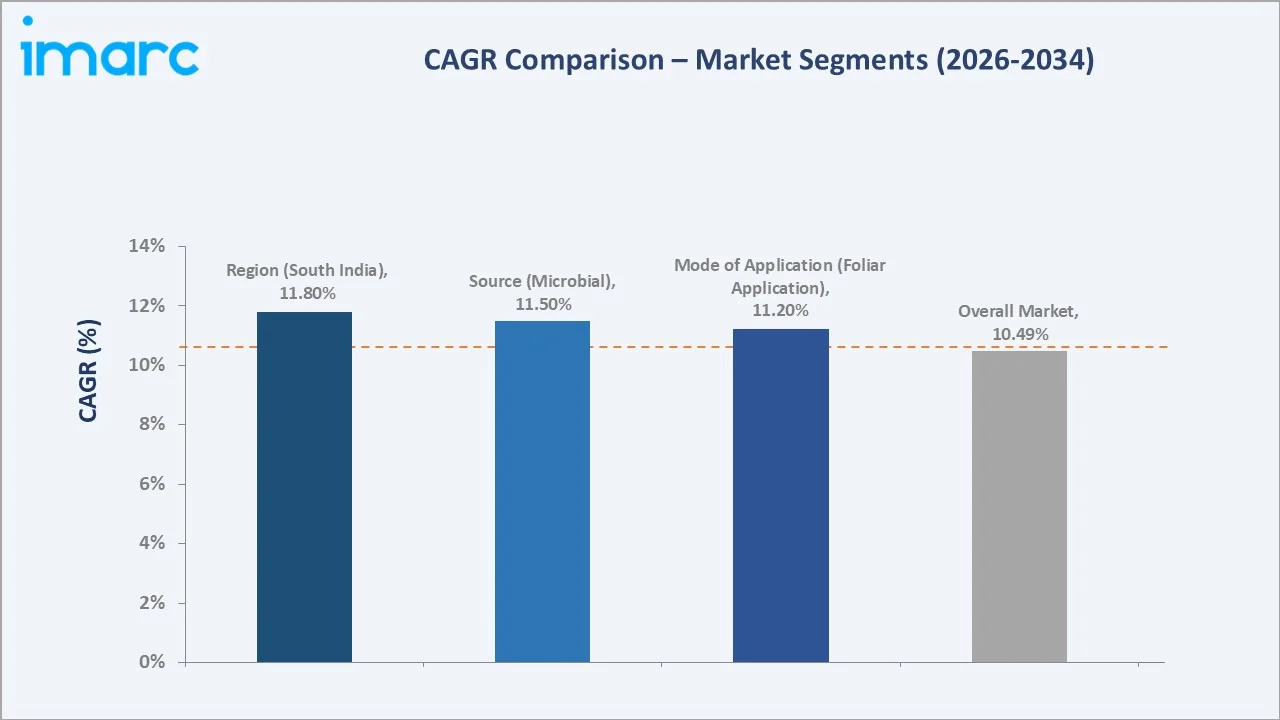

CAGR trajectories across mode of application and source sub-segments indicate that microbial and foliar application are expanding faster than the overall 10.49% market CAGR, driven by broader fungicide and insecticide replacement opportunities and ease of field adoption across smallholder and commercial farming operations.

Executive Summary

The India biopesticides market is on a sustained growth trajectory from USD 174.15 Million in 2020 to USD 703.81 Million by 2034. The segment has transitioned from niche adoption among organic-certified farms to mainstream integration across diverse crop systems, including cereals, horticulture, cotton, and oilseeds. Increasing consumer preference for residue-free food, stricter maximum residue limits (MRLs) for export markets, and supportive Central Insecticides Board and Registration Committee (CIBRC) registration frameworks are reinforcing mainstream adoption.

Foliar application dominates at 42.0%, reflecting ease of integration into existing spray programs. Microbial leads the source segment at 64.0% in 2025, supported by cost-competitive fermentation manufacturing, strong agronomic efficacy data, and an expanding portfolio of Bacillus thuringiensis-, Trichoderma-, and Pseudomonas-based formulations across Indian agri-input channels. North India commands 29.0% of regional share, anchored by diverse cropping systems and deep agri-input distribution networks.

Key Market Insights

|

Insight |

Data |

|

Leading Mode of Application |

Foliar Application - 42.0% share (2025) |

|

Second Largest Mode of Application |

Seed Treatment - 30.0% share (2025) |

|

Leading Source |

Microbial - 64.0% share (2025) |

|

Second Largest Source |

Biochemical - 36.0% share (2025) |

|

Leading Region |

North India - 29.0% share (2025) |

|

Fastest Growing Region |

South India - ~11.8% CAGR (2026-2034) |

|

Top Companies |

Bayer AG, BASF, Corteva, UPL, Biostadt |

Key Analytical Observations Expanding on the Data Above:

- Foliar application dominance at 42.0% reflects the ease of integrating biopesticide sprays into existing field equipment and conventional spray programs, reducing adoption barriers for first-time users across smallholder and commercial farming operations.

- Seed treatment at 30.0% is supported by the ability to deliver targeted biological protection at germination stage, reducing input volumes while improving crop emergence health, particularly in pulse, soybean, and maize cultivation.

- Microbial leadership at 64.0% is underpinned by competitive cost of goods, well-documented field efficacy, and a robust domestic manufacturing base in states, such as Tamil Nadu, Maharashtra, and Andhra Pradesh.

- Biochemical at 36.0% is gaining traction in precision IPM programs and organic export supply chains demanding non-synthetic residue profiles.

- North India at 29.0% leads regional share, supported by high crop diversity across cereals, horticulture, and cash crops, a dense agri-input retail network, and growing awareness programs under state-level organic farming missions. In June 2025, in a significant effort to advance large-scale natural farming in Haryana and educate farmers, Chief Minister Sh Nayab Singh Saini declared the creation of natural and organic markets in Gurugram and Hisar. The Gurugram mandi would serve produce like wheat, paddy, and pulses, whereas the Hisar mandi would emphasize fruits and vegetables cultivated using natural and organic techniques.

India Biopesticides Market Overview

Biopesticides are pest control agents derived from natural materials including microorganisms, plant extracts, and beneficial biochemicals, offering selective, environmentally compatible alternatives to synthetic chemical pesticides across a broad range of crop protection applications. The India biopesticides market encompasses microbial insecticides, fungicides, and nematicides as well as biochemical products including pheromones, plant growth regulators with pesticidal properties, and mineral-based formulations registered under CIBRC guidelines.

The Indian ecosystem integrates fermentation-based raw material producers, formulation manufacturers, contract testing laboratories, regulatory bodies, agri-input distributors, and farmer advisory networks. Collectively, these stakeholders enable the delivery of biological crop protection solutions within India's evolving IPM and organic farming regulatory framework.

Market Dynamics

To evaluate market opportunities, Request Sample

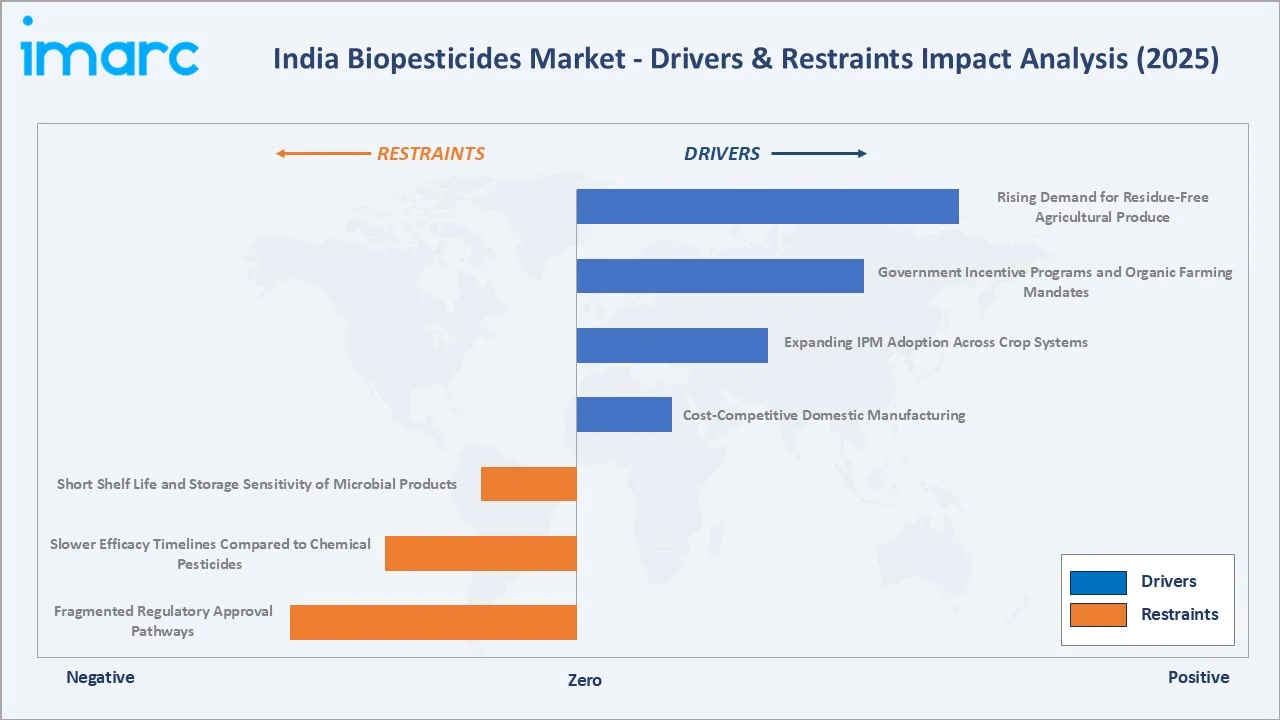

Market Drivers

- Rising Demand for Residue-Free Agricultural Produce: The growing domestic consumer preference for pesticide-safe food is compelling farmers and exporters to adopt biopesticide-based crop protection programs that meet residue compliance standards without compromising crop protection efficacy.

- Government Incentive Programs and Organic Farming Mandates: Central and state government programs are actively incentivizing bio-input adoption among smallholder farmers. As per IMARC Group, the India organic farming market size was valued at USD 6,133.68 Million in 2025. These programs provide subsidized access to biopesticide products, reducing first-time adoption cost barriers across marginal farming communities.

- Expanding IPM Adoption Across Crop Systems: The nationwide scale-up of IPM programs through Krishi Vigyan Kendras (KVKs) and state agricultural universities is systematically training farmers in biopesticide use as part of multi-tactic pest control strategies, creating structured demand across rice, wheat, cotton, and vegetable cultivation systems.

- Cost-Competitive Domestic Manufacturing: India has developed a robust domestic manufacturing base for microbial biopesticides, with production costs significantly lower than import-equivalent chemical pesticides for specific pest targets, enabling price-competitive market positioning across tier-2 and tier-3 agri-input distribution channels.

Market Restraints

- Short Shelf Life and Storage Sensitivity of Microbial Products: Living microorganism-based biopesticides require controlled storage conditions and have limited shelf lives compared to synthetic alternatives, creating cold-chain logistics challenges in rural distribution networks and contributing to product quality inconsistency at the last-mile retail level.

- Slower Efficacy Timelines Compared to Chemical Pesticides: Biopesticides typically require repeated applications and show slower visible pest knockdown compared to fast-acting synthetic insecticides, limiting adoption among farmers experiencing acute pest infestations where immediate crop protection is critical, particularly in large-scale commercial farming operations.

- Fragmented Regulatory Approval Pathways: Variability in CIBRC registration timelines and limited data-sharing provisions between state and central authorities create registration delays for new formulations, slowing the pace of commercial product launches and increasing compliance costs for manufacturers bringing novel strains to market.

Market Opportunities

- Next-Generation Microbial Strain Development: Advances in genomics, fermentation engineering, and delivery systems are enabling the development of high-efficacy microbial biopesticides with improved shelf stability, broader pest spectra, and enhanced field performance, opening new addressable markets in commercial horticulture, floriculture, and high-value export crops.

- Combination Product Formulations: Integrated biostimulant-biopesticide combination products are emerging as high-value segment extensions, enabling manufacturers to offer dual plant health and crop protection benefits, commanding premium pricing and generating new revenue pools in the organic and specialty crop segments.

Market Challenges

- Limited Farmer Awareness and Agronomic Training: In many rural districts, inadequate access to product application guidance, incorrect dosage practices, and low awareness of biopesticide compatibility within integrated spray programs reduce product efficacy and contribute to suboptimal user experience, creating adoption hesitancy among first-time users.

- Competition from Generic Chemical Pesticides: Price competition from off-patent generic synthetic pesticides, particularly in the insecticide segment, continues to pressure biopesticide market penetration in price-sensitive smallholder farming communities where immediate cost savings often outweigh long-term sustainability considerations.

Emerging Market Trends

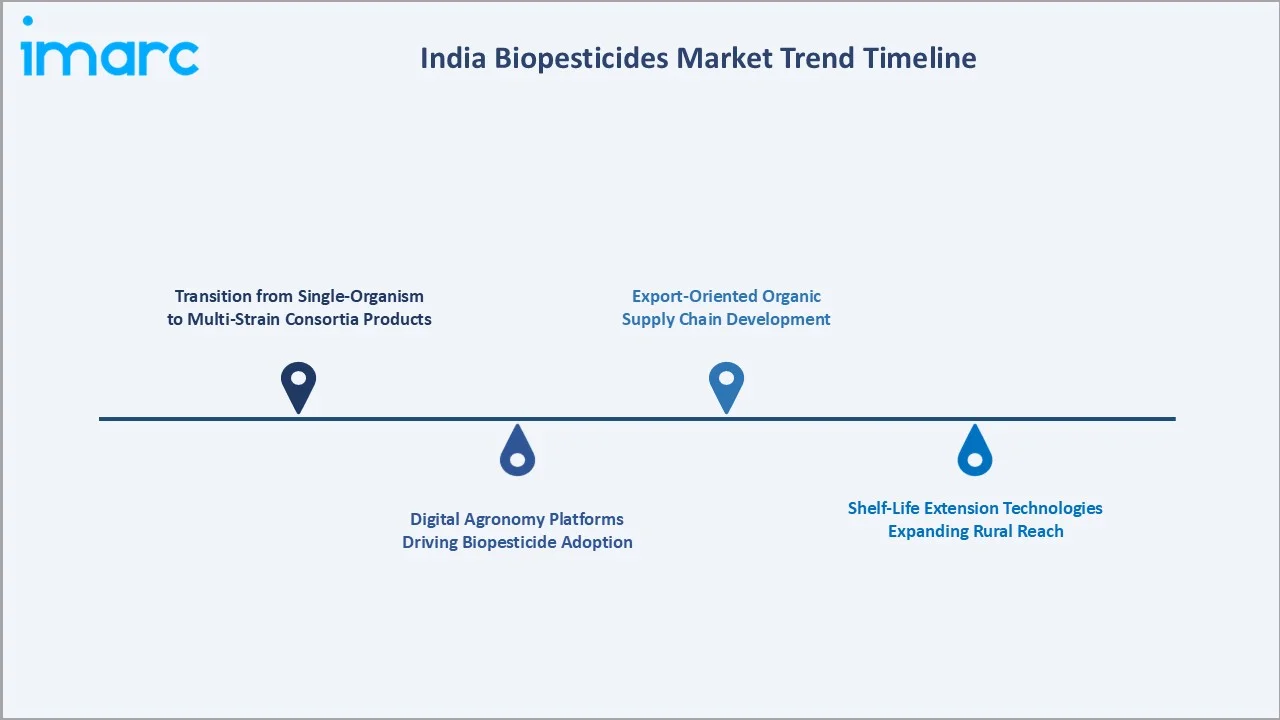

1. Transition from Single-Organism to Multi-Strain Consortia Products

Manufacturers are moving from single-active microbial formulations toward multi-strain consortia products that combine bacterial, fungal, and biochemical actives to deliver broader pest and disease spectrum coverage. This approach reduces the number of applications required per season and improves compatibility with conventional IPM programs, accelerating adoption in commercial fruit, vegetable, and spice cultivation.

2. Digital Agronomy Platforms Driving Biopesticide Adoption

Agri-tech platforms providing AI-powered crop advisory services are increasingly recommending biopesticide protocols as default crop protection choices for pest-pressure management, creating structured digital demand channels. These platforms aggregate farmer data, pest incidence reports, and weather patterns to prescribe timely biopesticide applications, improving product efficacy and farmer confidence across emerging digital agriculture markets.

3. Export-Oriented Organic Supply Chain Development

Rising demand from international buyers for residue-free fresh produce is compelling organized farmer producer organizations (FPOs) and agri-exporters to formalize biopesticide-based production protocols as part of global food safety compliance programs. This is creating structured, repeatable demand from professionally managed supply chains that value consistency and certification compatibility over per-unit cost minimization.

4. Shelf-Life Extension Technologies Expanding Rural Reach

Microencapsulation, oil dispersion formulation technologies, and wettable granule formats are significantly extending biopesticide shelf lives under ambient storage conditions, addressing the cold-chain dependency limitation and enabling deeper penetration into rural retail networks without product quality degradation, particularly for temperature-sensitive bacterial and fungal formulations.

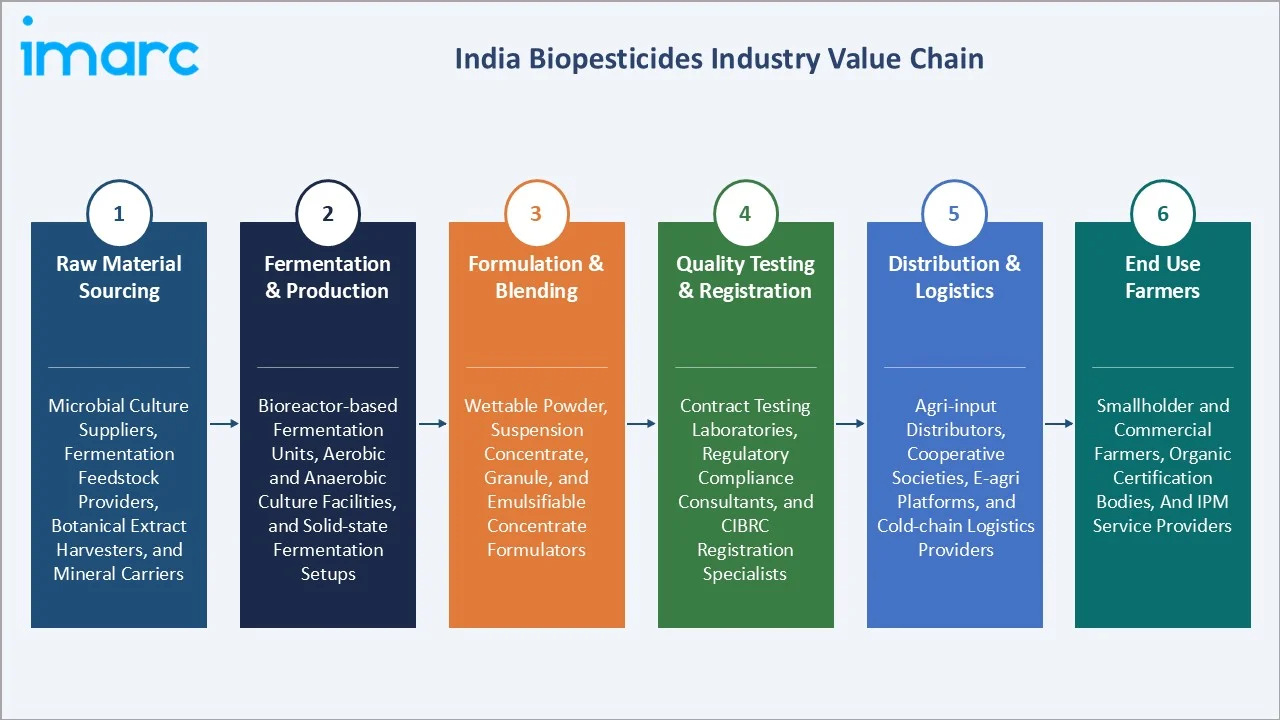

Industry Value Chain Analysis

The India biopesticides value chain spans six integrated stages from raw material sourcing through end use farmer adoption. Fermentation-based production, formulation technology, and quality testing infrastructure capture the highest value-add, while logistics optimization and last-mile distribution capabilities increasingly determine market reach and competitive differentiation across India's fragmented agri-input retail landscape.

|

Stage |

Key Players / Examples |

|

Raw Material Sourcing |

Microbial culture suppliers, fermentation feedstock providers, botanical extract harvesters, and mineral carriers supporting biopesticide production |

|

Fermentation & Production |

Bioreactor-based fermentation units, aerobic and anaerobic culture facilities, and solid-state fermentation setups for fungal and bacterial biopesticide manufacturing |

|

Formulation & Blending |

Wettable powder, suspension concentrate, granule, and emulsifiable concentrate formulators adapting active biologicals into field-ready products |

|

Quality Testing & Registration |

Contract testing laboratories, regulatory compliance consultants, and CIBRC registration specialists ensuring product safety and efficacy validation |

|

Distribution & Logistics |

Agri-input distributors, cooperative societies, e-agri platforms, and cold-chain logistics providers ensuring biopesticide shelf-life integrity |

|

End Use Farmers |

Smallholder and commercial farmers, organic certification bodies, and IPM service providers driving field adoption |

Technology Landscape in the India Biopesticides Industry

Fermentation and Upstream Bioprocess Engineering

Advanced submerged fermentation and solid-state fermentation platforms are enabling manufacturers to produce high-concentration microbial biomass at lower cost per unit, supporting competitive pricing in the commercial market. Continuous fermentation systems with in-line quality monitoring are improving batch consistency and regulatory compliance for product standardization under CIBRC norms.

Formulation Science and Encapsulation Technologies

Polymer-based microencapsulation, oil suspension concentrates, and wettable granule formulations are extending the field stability and shelf life of living microbial actives, reducing cold-chain dependency and enabling wider distribution across rural retail networks. These formulation innovations are also improving rainfastness and UV tolerance of foliar biopesticide applications, enhancing efficacy under tropical field conditions.`

Genomics-Driven Strain Discovery and Optimization

Next-generation sequencing and functional genomics tools are enabling biotech firms to identify high-potency microbial strains with novel modes of action against target pest species, accelerating new product development pipelines. Computational biology platforms are shortening strain screening timelines from multi-year programs to sub-12-month development cycles, reducing time-to-market for next-generation biopesticide launches.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Type |

🔒 |

🔒 |

2025 |

|

Source |

Microbial |

64.0% |

2025 |

|

Mode of Application |

Foliar Application |

42.0% |

2025 |

|

Crop Type |

🔒 |

🔒 |

2025 |

|

Region |

North India |

29.0% |

2025 |

By Mode of Application

Foliar application commands a 42.0% majority share in 2025, driven by ease of integration into conventional spray equipment, compatibility with broad-acre crop protection schedules, and proven efficacy across fungicide, insecticide, and bactericide use-cases in field crops, horticulture, and plantation agriculture. The segment benefits from familiarity among farmers already trained in liquid spray application methods and from the wide availability of foliar-compatible microbial and biochemical formulations.

To access detailed market analysis, Request Sample

Seed treatment at 30.0% in 2025 delivers targeted biological protection at the critical germination and early root development stage, maximizing biological efficacy with minimal input volumes. The segment is growing fastest in pulse, legume, soybean, and maize cultivation where seed-applied microbial inoculants provide both pest protection and nitrogen-fixing or phosphate-solubilizing benefits simultaneously.

By Source

Microbial dominates with a 64.0% share in 2025, anchored by the commercial maturity of Bacillus thuringiensis (Bt) insecticides, Trichoderma spp. fungicides, and Beauveria bassiana mycoinsecticides. The segment benefits from a well-established domestic manufacturing infrastructure, competitive cost of goods, and a broad portfolio covering insect, fungal, bacterial, and nematode pest categories across diverse crop systems.

Biochemical at 36.0% encompasses plant-derived insecticides, such as neem-based azadirachtin formulations, pheromone traps and mating disruption systems, and mineral-based copper and sulfur compounds. The segment is gaining traction in organic export supply chains and precision IPM programs requiring non-synthetic residue profiles and compatibility with beneficial insect populations.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

|

North India |

29.0% |

High agricultural activity, widespread organic farming awareness, diverse crop portfolio requiring pest management, and growing government support for biological inputs |

|

South India |

27.0% |

Expanding horticultural base, strong IPM adoption in rice and vegetable cultivation, growing export-oriented farms demanding residue-free produce |

|

West India |

24.0% |

Established agri-input distribution networks, large cotton and soybean farming areas, progressive adoption of biopesticides as chemical-alternative inputs |

|

East India |

20.0% |

Rising awareness of eco-friendly farming, expanding paddy cultivation, increasing smallholder participation in organic certification programs |

North India at 29.0% in 2025 leads the regional landscape, anchored by Uttar Pradesh, Punjab, Haryana, Madhya Pradesh, and Rajasthan. Diverse cropping systems spanning wheat, rice, vegetables, and oilseeds, combined with dense agri-input retail penetration and active state government promotion of organic and bio-input programs, support sustained regional leadership.

South India, the fastest growing region at approximately 11.8% CAGR through 2034, is expanding rapidly. States, including Tamil Nadu, Karnataka, Andhra Pradesh, and Telangana, host significant export-oriented horticulture and spice cultivation, driving structured demand for biopesticide-based residue-free production protocols through 2034. Government initiatives and IPM extension programs in rice and vegetable belts are further accelerating regional market growth.

Competitive Landscape

The India biopesticides market is moderately fragmented, with global agri-input majors leading in product portfolio breadth and regulatory capability while domestic specialty manufacturers compete on localized strain knowledge, distribution depth, and cost competitiveness. R&D investment, formulation quality, CIBRC registration pipeline, and farmer service capabilities form the key competitive differentiators in this market.

|

Company Name |

Brand / Key Product |

Position |

Strategic Focus |

|

Bayer AG |

SERENADE, BioAct |

Leader |

Integrated biological and conventional crop protection with a broad global product pipeline |

|

BASF |

Serifel |

Leader |

Biofungicide and bionematicide development with strong formulation and registration capabilities |

|

Corteva |

Bexfond |

Challenger |

Biological fungicide and bioinsecticide portfolio targeting sustainable crop protection systems |

|

UPL |

Bioclassic |

Challenger |

Broad-based biologicals platform under NPP with strong India distribution and registration network |

|

Biostadt |

Biozyme |

Emerging |

India-focused biologicals company delivering microbial biopesticides through agri-retail channels |

Key players include Bayer AG, BASF, Corteva, UPL, and Biostadt, among others.

Key Company Profiles

Bayer AG

Bayer AG is a global life sciences company headquartered in Leverkusen, Germany, with operations across pharmaceuticals, consumer health, and crop science. The company maintains a strong presence across major agricultural markets, supported by extensive R&D capabilities focused on crop protection, seeds, and sustainable farming solutions.

- Product Portfolio: SERENADE (Bacillus amyloliquefaciens QST 713) biofungicide for broad-spectrum foliar disease control in fruits, vegetables, and broad-acre crops.

- Recent Development: In July 2025, Bayer signed an exclusive distribution agreement with France-based M2i Group, granting rights to distribute pheromone-based mating disruption gel products across Asia-Pacific, Latin America, and the United States, further expanding its biological crop protection footprint.

- Strategic Focus: Expanding an integrated biologicals portfolio combining biofungicides, bionematicides, and pheromone-based biocontrol solutions to serve organic, residue-reduction, and integrated pest management markets globally.

BASF

BASF is a leading global chemical and agricultural solutions company headquartered in Ludwigshafen, Germany, with an established presence in biological crop protection. The company serves growers across major agricultural regions through an extensive network of research facilities, manufacturing sites, and distribution channels supporting crop protection and sustainable farming practices.

- Product Portfolio: Serifel (Bacillus amyloliquefaciens strain MBI600) biofungicide for broad-spectrum foliar and root disease management.

- Recent Development: BASF continues to expand its biological crop protection portfolio through product innovation, strategic collaborations, and regulatory approvals, reinforcing its commitment to integrated and sustainable crop management solutions across key agricultural markets.

- Strategic Focus: Building a comprehensive platform integrating biological fungicides, nematicides, and seed treatments as complementary tools within integrated crop protection and sustainable agriculture programs across global and Indian markets.

Corteva

Corteva is an independent, pure-play agriculture company headquartered in Indianapolis, United States, with operations spanning crop protection and seeds. The company leverages advanced research, breeding technologies, and crop protection expertise to develop solutions that enhance farm productivity, crop resilience, and sustainable agricultural practices worldwide.

- Product Portfolio: Bexfond, supporting root zone protection against soil-borne diseases across a range of crops and growing systems.

- Recent Development: Corteva continues to strengthen its biologicals platform through new product introductions, research investments, and commercial partnerships aimed at broadening the adoption of nature-based crop protection solutions in global agriculture.

- Strategic Focus: Advancing a science-based biologicals portfolio that integrates biofungicides and bioinsecticides as complementary tools with conventional chemistry, supporting resistance management and residue-reduction goals for export-oriented crop systems.

Market Concentration Analysis

The India biopesticides market is moderately concentrated. The top two players, Bayer AG and BASF, account for a significant share of premium segment sales, particularly in formulated microbial biofungicides and bioinsecticides for export-oriented and commercial horticulture applications. Domestic manufacturers are competitive in the price-sensitive tier-2 and tier-3 distribution channels.

Barriers to entry include the need for CIBRC registration expertise, formulation manufacturing capability, cold-chain-compliant distribution infrastructure, and agronomic service capacity for product performance support. These factors favor established players with existing regulatory portfolios and farmer trust networks.

Consolidation is gradually increasing as global agrochemical majors acquire biologicals-focused startups and expand their biological product pipelines. Strategic partnerships between global firms and Indian contract manufacturers are also reshaping the competitive structure, enabling faster market access at lower capital investment.

Investment & Growth Opportunities

Fastest-Growing Segments

Microbial expands the fastest among source segments at approximately 11.5% CAGR through 2034, driven by broader crop coverage, new strain registrations, and growing farmer acceptance of microbial-based pest management protocols. Seed treatment is the fastest-growing mode of application, supported by rising mechanized farming adoption and demand for systemic root-zone biological protection in commercial crop systems.

Emerging Markets

South India, growing at approximately 11.8% CAGR through 2034, is one of the fastest-growing regions, anchored by export-driven horticulture growth in Karnataka, Tamil Nadu, and Andhra Pradesh. These states represent significant untapped opportunity for operators with certified organic and residue-free production protocol capability, particularly in spice, grape, mango, and vegetable export supply chains.

Venture & Investment Trends

Investment is concentrated in fermentation technology scaleups, formulation innovation companies, and agri-tech platforms integrating biological input advisory with digital agronomy services. Capital is also flowing into genomics-driven strain discovery platforms and novel delivery system developers targeting shelf-life extension and rural distribution reach for microbial biopesticide products.

Future Market Outlook (2026-2034)

The India biopesticides market is forecast to expand from USD 286.78 Million in 2025 to USD 703.81 Million by 2034 at a CAGR of 10.49%, adding approximately USD 417 Million in incremental annual market value over the forecast period.

Four forces will shape the market through 2034: expanding government-mandated organic farming programs reducing chemical pesticide dependency; next-generation microbial strain development improving product efficacy and field versatility; deepening digital agronomy advisory channels accelerating biopesticide adoption among first-time users; and growing global demand for residue-free Indian agricultural exports creating structured, export-driven demand.

By 2034, the India biopesticides market is expected to be characterized by broad-spectrum combination products, digital-enabled farmer advisory integration, and a deepened domestic manufacturing base capable of competing globally across microbial, biochemical, and delivery system innovation categories.

Research Methodology

Primary Research

Primary research included structured interviews with biopesticide manufacturers, formulators, CIBRC registration specialists, state agricultural department officers, farmer producer organization representatives, and agri-input distributors, validating market sizing, segment mix, regional demand patterns, and adoption driver dynamics.

Secondary Research

Secondary sources included Ministry of Agriculture and Farmers Welfare reports, CIBRC registration databases, National Centre of Organic Farming publications, state agriculture department organic farming area data, company annual reports, press releases, investor presentations, and trade association publications from the Pesticides Manufacturers and Formulators Association of India (PMFAI).

Forecasting Models

Market forecasts used bottom-up and top-down modeling combining registered product volumes, active ingredient production capacity, crop-wise adoption rate trajectories, government subsidy disbursement data, and macroeconomic variables. Scenario analysis addressed regulatory pace, organic farming area expansion rates, and export demand variability.

India Biopesticides Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Types Covered | Bioinsecticides, Biofungicides, Bionematicides, Others |

| Sources Covered | Microbial, Biochemical |

| Mode of Applications Covered | Foliar Application, Seed Treatment, Soil Treatment |

| Crop Types Covered | Cereals, Oilseeds, Fruits and Vegetables, Others |

| Regions Covered | North India, South India, East India, West India |

| Companies Covered | Bayer AG, BASF, Corteva, UPL, Biostadt, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the India biopesticides market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the India biopesticides market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the India biopesticides industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the India Biopesticides Market Report

The India biopesticides market was valued at USD 286.78 Million in 2025, driven by expanding organic farming mandates, government bio-input subsidy programs, and rising demand for residue-free produce across domestic and export markets.

The market is projected to grow at a CAGR of 10.49% from 2026 to 2034, reaching USD 703.81 Million, supported by next-generation microbial product launches and expanding IPM program adoption across Indian crop systems.

Foliar application leads with 42.0% share in 2025, driven by compatibility with existing spray equipment, broad crop application flexibility, and proven efficacy across major pest categories in field and horticultural crops.

Microbial dominates with 64.0% share in 2025, anchored by Bt insecticides, Trichoderma fungicides, and Beauveria-based mycoinsecticides with strong domestic manufacturing and CIBRC registration support.

North India commands a 29.0% share in 2025, led by Uttar Pradesh, Punjab, and Haryana, supported by diverse crop systems, dense agri-input networks, and active state-level organic farming promotion programs.

Key drivers include rising demand for residue-free agricultural produce, government organic farming mandates, expanding IPM adoption, cost-competitive domestic manufacturing, and tightening MRL regulations for Indian agricultural exports.

Leading companies include Bayer AG, BASF, Corteva, UPL, and Biostadt, among others.

Key challenges include short shelf life of microbial products, cold-chain dependency in rural distribution, slower efficacy compared to chemical alternatives, and fragmented CIBRC approval pathways for new formulations.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)