India Commercial Real Estate Market Size, Share, Trends and Forecast by Type, End Use, and Region, 2026-2034

India Commercial Real Estate Market Size, Share, Trends & Forecast (2026-2034)

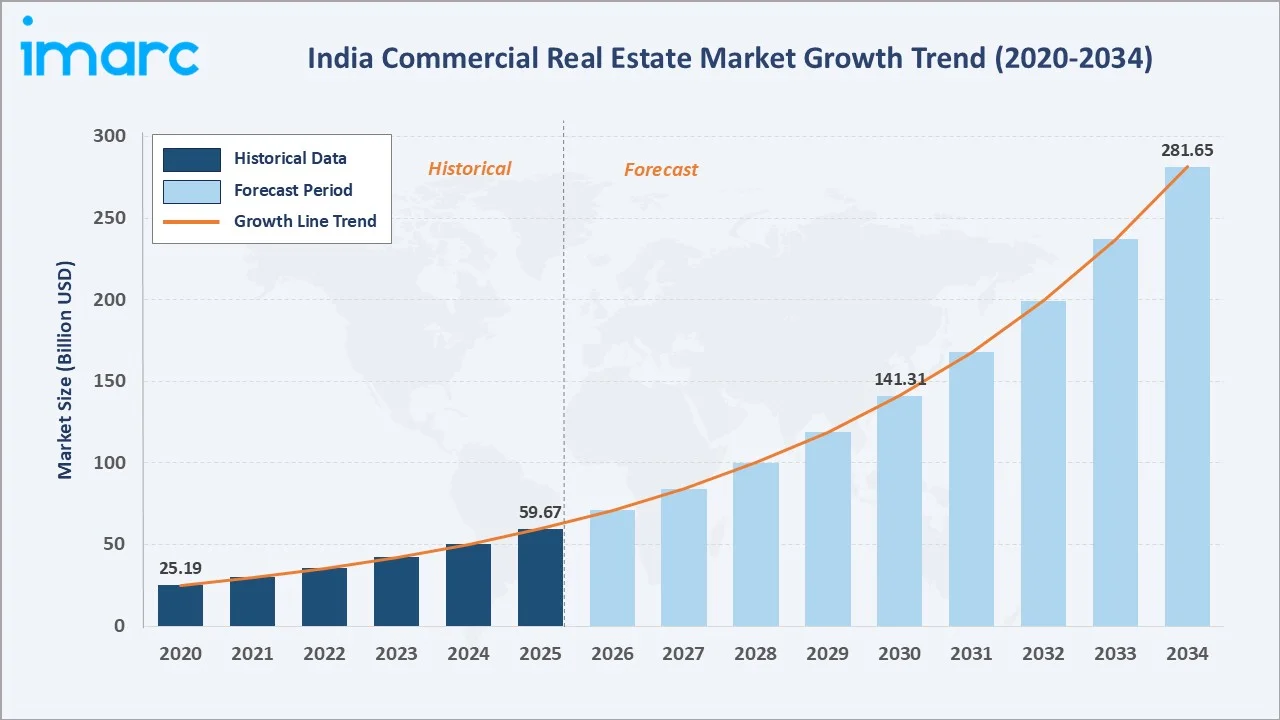

The India commercial real estate (CRE) market reached USD 59.67 Billion in 2025 and is projected to reach USD 281.65 Billion by 2034, growing at a CAGR of 18.82% during 2026-2034. India's Global Capability Centers (GCCs), GDP accelerating toward a USD 5 Trillion economy, REIT market expansion unlocking institutional capital, Grade A office supply surge, and premium retail mall renaissance anchor the market's exceptional 18.82% CAGR through 2034. Rental dominates at 64.8% market share. Offices lead end-user demand at 46.3%. West India commands 34.5% of market revenues.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 59.67 Billion |

|

Forecast Market Size (2034) |

USD 281.65 Billion |

|

CAGR (2026-2034) |

18.82% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Dominant Type |

Rental (64.8%, 2025) |

|

Dominant End Use |

Offices (46.3%, 2025) |

|

Leading Region |

West India (34.5%, 2025) |

The market expanded from USD 25.19 Billion in 2020 to USD 59.67 Billion in 2025, anchored at USD 141.31 Billion in 2030, and forecast to reach USD 281.65 Billion by 2034. COVID-19's temporary WFH disruption of 2020-2021 proved a false signal, India's commercial real estate market rebounded with exceptional vigor as GCC demand surged in 2022, demonstrating that India's knowledge economy growth, a structural driver, was more powerful than any pandemic-induced temporary behavioral change, establishing the 18.82% CAGR trajectory observed through 2025.

To get more information on this market, Request Sample

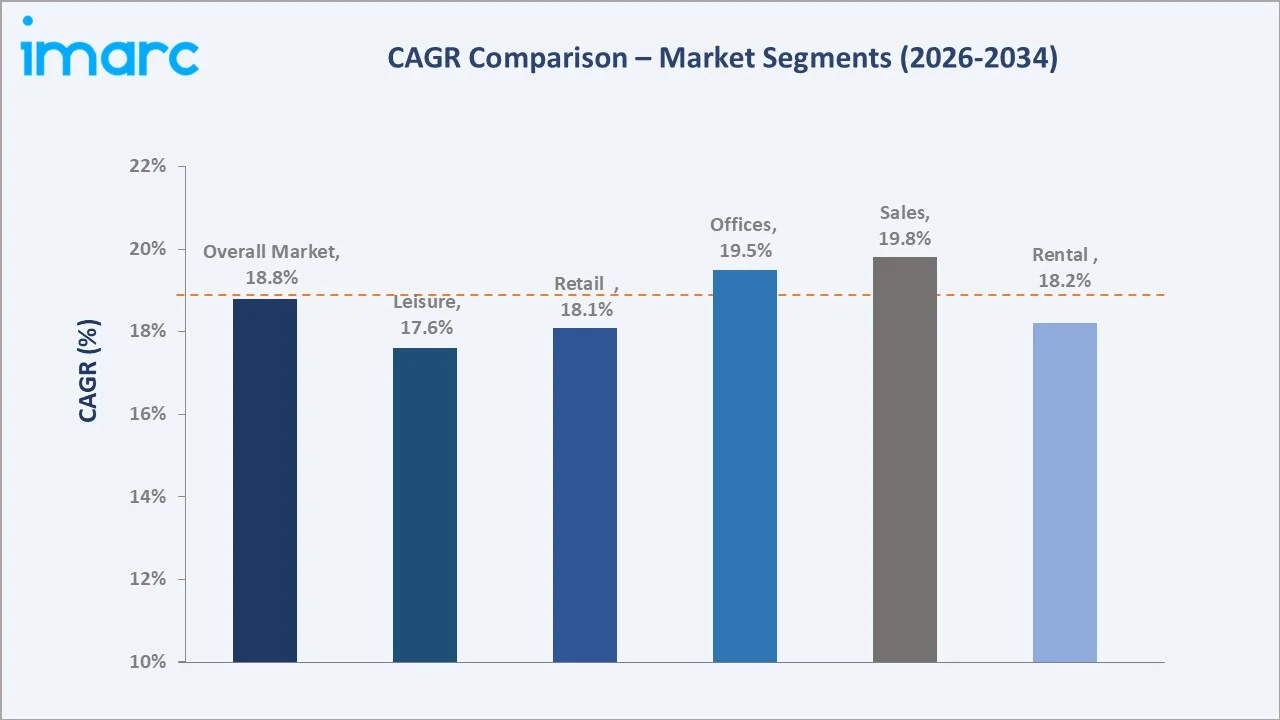

Sales grow fastest at ~19.8% CAGR (2026-2034), driven by strata sales of Grade A office floors to SME and HNI investors, REIT unit appreciation creating investor demand for commercial property exposure, and data center capital assets being sold to infrastructure funds. Offices grow at ~19.5% CAGR as India's GCC sector employees, creating additional Grade A office demand that surpasses all current India Grade A office stock combined.

Executive Summary

The India commercial real estate market reached USD 59.67 Billion in 2025, establishing India as Asia's third-largest CRE market by transaction value and the world's most rapidly expanding major CRE market by CAGR, growing at 18.82% versus Asia Pacific's and the global CRE market growth. India's CRE market is structurally different from mature Western markets in that its growth is simultaneously demand-driven and supply-driven. The market is projected to reach USD 281.65 Billion by 2034 at 18.82% CAGR.

Rental at 64.8% dominates as India's CRE market is fundamentally a lease market with multinational GCCs and India-headquartered IT/BFSI companies prefer long-term lease structures over ownership for their office campuses, preserving capital for core business investment. Offices at 46.3% are the engine of demand, driven by India's unstoppable knowledge economy expansion. West India at 34.5% leads through Mumbai's unmatched financial capital CRE demand and Pune's GCC concentration.

Key Market Insights

|

Insight |

Data |

|

Dominant Type |

Rental - 64.8% share (2025) |

|

Dominant End Use |

Offices - 46.3% market share (2025) |

|

Leading Region |

West India - 34.5% market share (2025) |

Key Analytical Observations Supporting the Above Data:

- Rental at 64.8%, reflecting India's lease-dominated Grade A office market structure: India's Grade A office rental market generates new leasing, driven by GCC expansions.

- Offices at 46.3% are driven by India's GCC sector, representing the single largest demand driver in global office real estate: India hosts 1,800+ GCCs (Global Capability Centers) employing high-knowledge workers and occupying more Grade A office space.

- West India at 34.5% through Mumbai's irreplaceable financial capital CRE premium and Pune's GCC concentration: Mumbai's BKC Grade A office commands high, reflecting the BFSI, consulting, media, and MNC headquarters demand for Mumbai's financial capital address.

India Commercial Real Estate Market Overview

India's commercial real estate market encompasses all non-residential built properties and land used for business purposes, including Grade A, B, and C office spaces; premium and mid-tier retail malls and high streets; business parks and IT parks; data centers and industrial warehouses; hospitality and hotel assets; mixed-use developments; and co-working/flex office spaces. The market spans both rental (lease) transactions and outright sales, serving multinational corporations, India-headquartered enterprises, retail occupiers, government entities, and financial investors seeking real estate exposure.

The ecosystem integrates landowners and government authorities, developers and construction companies, REIT sponsors and institutional investors, property management and facility services firms, commercial real estate brokers, regulatory authorities, and occupier/tenant categories including GCCs, domestic IT firms, BFSI enterprises, retail brands, and leisure operators. Macroeconomic factors include strong GDP growth, rising corporate hiring, infrastructure expansion, urbanization, and higher institutional capital inflows.

Market Dynamics

To evaluate market opportunities, Request Sample

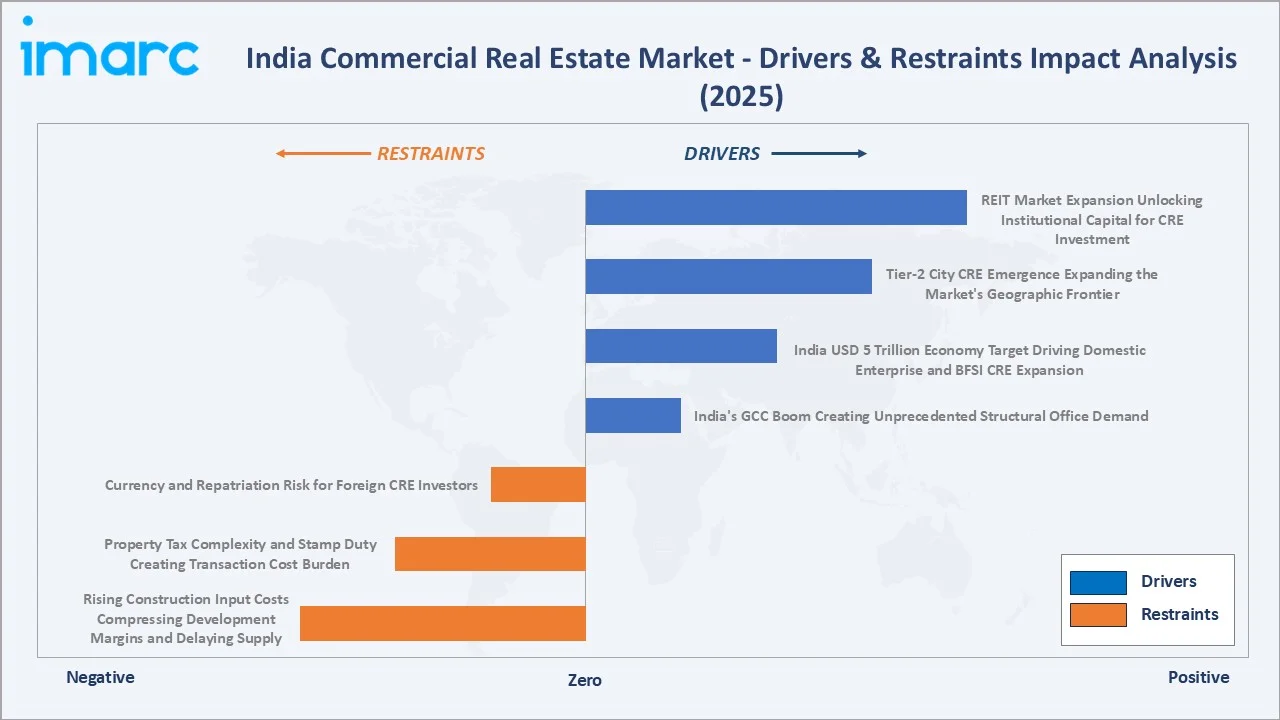

Market Drivers

- India's GCC Boom Creating Unprecedented Structural Office Demand: India's 1,800+ GCCs and by 2030, India is expected to host over 2,500 GCCs employing 2.8-2.9 million professionals, contributing an impressive USD 105 billion in revenue to the global economy and representing the single largest structural demand driver for India's Grade A office market globally.

- India USD 5 Trillion Economy Target Driving Domestic Enterprise and BFSI CRE Expansion: India's GDP growth trajectory toward USD 5 Trillion by 2027 is generating proportional domestic enterprise expansion requiring commercial real estate. India's banking sector expanding branch networks; insurance companies opening regional offices; domestic IT services companies are scaling delivery centers; and India's booming startup ecosystem collectively generates CRE demand independent of MNC GCC activity.

- Tier-2 City CRE Emergence Expanding the Market's Geographic Frontier: India's Tier-2 cities are experiencing CRE market formalization as domestic enterprises, GCC satellite offices, and retail chains expand beyond the six traditional metros.

Market Restraints

- Rising Construction Input Costs Compressing Development Margins and Delaying Supply: India's construction cost index rose during 2021-2025. This cost inflation is delaying some speculative office development and incentivizing developers to prioritize pre-leased development over speculative supply, potentially creating supply shortfalls in preferred micro-markets despite strong demand fundamentals.

- Property Tax Complexity and Stamp Duty Creating Transaction Cost Burden: Commercial property stamp duty in India ranges from 5-7% of transaction value across states, creating significant transaction costs on CRE purchases that reduce investment returns compared to REIT unit purchases.

Market Opportunities

- Data Center Real Estate Creating New CRE Asset Class: India’s data centre operational capacity to double to 2,000-2,100 MW by FY2027 requires additional data center infrastructure investment. Institutional investors are actively seeking India data center CRE exposure, creating a new institutional capital category for this specialized asset class.

- Green Building Premium and ESG-Mandated CRE Investment Creating Sustainability Premium Market: India's IGBC (Indian Green Building Council) certified 15.79 Billion sq.ft. of green building space, one of the world's largest green building markets by area.

Market Challenges

- Infrastructure Dependency Creating Market Concentration Risk: India's Grade A CRE market is concentrated in 8 cities because those cities have reliable power supply, metro rail connectivity, airport access, and talent availability, prerequisites for MNC occupier decision-making. Bengaluru's traffic congestion is already affecting occupier location decisions for new CRE campus requirements, creating structural demand pressure for alternative micro-markets that require new infrastructure investment.

- Currency and Repatriation Risk for Foreign CRE Investors: Foreign institutional investors accounting for 40-50% of India's Grade A CRE investment face INR/USD exchange rate risk on their India portfolio returns.

Emerging Market Trends

1. Flex and Managed Office Spaces Reshaping Commercial Lease Structures

Flex and managed office spaces are reshaping India’s commercial lease structures by shifting demand from long-term fixed leases to shorter, scalable, and service-led occupancy models. Corporates, startups, and GCCs are increasingly choosing plug-and-play spaces to manage headcount uncertainty, reduce upfront capex, and expand quickly across key business hubs. This trend is pushing landlords to offer more flexible terms, revenue-sharing models, fitted-out offices, and managed workspace partnerships instead of traditional bare-shell leasing.

2. Mixed-Use Developments Creating 18-Hour Urban Destinations

Mixed-use developments combining offices, retail, hospitality, entertainment, and residential spaces within integrated urban districts. These projects are creating “18-hour” destinations where people can work, shop, dine, socialize, and live in the same location, improving footfall and asset utilization beyond regular office hours. Developers are increasingly using this model to attract occupiers, premium retailers, and institutional investors seeking diversified revenue streams and stronger long-term occupancy.

3. GCC-Driven Build-to-Suit Office Development Creating Pre-Leased Supply Dominance

GCC-driven build-to-suit office development is emerging as a major trend in India’s commercial real estate market as global capability centers seek customized, secure, and scalable campuses. Large occupiers are increasingly preferring pre-leased or tailor-made office assets with advanced infrastructure, ESG features, data security, and employee-centric amenities. This is strengthening pre-commitment leasing, reducing vacancy risk for developers, and creating supply dominance in key GCC hubs such as Bengaluru, Hyderabad, Pune, Chennai, and NCR.

4. Data Center and Digital Infrastructure Real Estate as New CRE Category

Data centers and digital infrastructure are driven by cloud adoption, AI workloads, OTT platforms, fintech, e-commerce, and data localization needs. Unlike traditional office or retail assets, these facilities require high power availability, fiber connectivity, cooling systems, land parcels, and strong disaster-resilient infrastructure. This trend is attracting developers, hyperscalers, private equity investors, and REIT-style platforms, positioning data centers as a high-growth, infrastructure-led CRE asset class in key markets such as Mumbai, Chennai, Hyderabad, Pune, Bengaluru, and NCR.

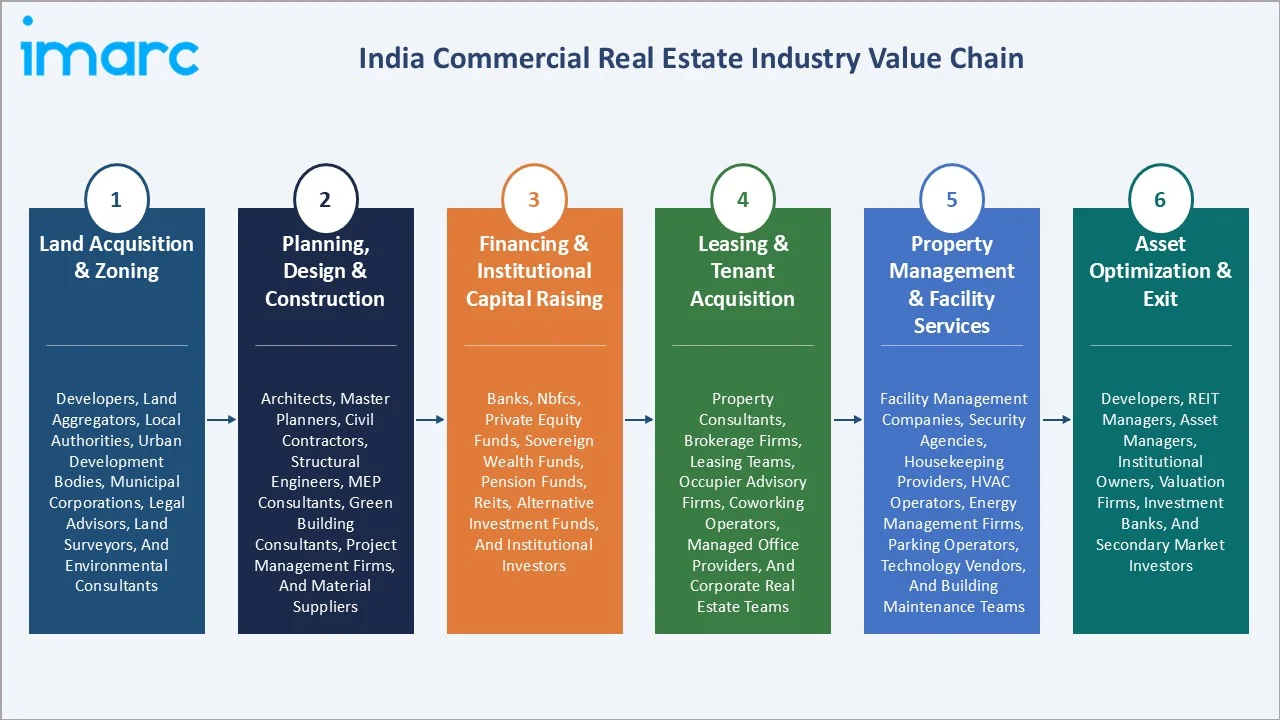

Industry Value Chain Analysis

India's commercial real estate value chain integrates land acquisition, Grade A development, institutional capital raising, tenant leasing, operational property management, and asset optimization. Developer EBITDA margins range from 20-30% for Grade A office on land acquired at historical cost to 12-18% for build-to-suit at current land prices in premium micro-markets. REIT sponsors earn management and performance fees of 1-2% AUM annually; property management firms earn 5-8% of rental revenue; and CRE brokers earn 15-25% of the first year's rent (one-time transaction fee) on office leases above 100,000 sq.ft.

|

Stage |

Key Participants |

|

Land Acquisition & Zoning |

Developers, land aggregators, local authorities, urban development bodies, municipal corporations, legal advisors, land surveyors, and environmental consultants. |

|

Planning, Design & Construction |

Architects, master planners, civil contractors, structural engineers, MEP consultants, green building consultants, project management firms, and material suppliers. |

|

Financing & Institutional Capital Raising |

Banks, NBFCs, private equity funds, sovereign wealth funds, pension funds, REITs, alternative investment funds, and institutional investors. |

|

Leasing & Tenant Acquisition |

Property consultants, brokerage firms, leasing teams, occupier advisory firms, coworking operators, managed office providers, and corporate real estate teams. |

|

Property Management & Facility Services |

Facility management companies, security agencies, housekeeping providers, HVAC operators, energy management firms, parking operators, technology vendors, and building maintenance teams. |

|

Asset Optimization & Exit |

Developers, REIT managers, asset managers, institutional owners, valuation firms, investment banks, and secondary market investors. |

The institutional capital tier has transformed India's CRE value chain by providing developers with efficient exit mechanisms that enable recycling of development capital into new projects rather than long-term asset holding.

Technology Landscape in the India Commercial Real Estate Industry

Smart Building Management Systems (BMS) and IoT Integration

Smart building management systems and IoT integration enable centralized control of HVAC, lighting, elevators, access systems, energy use, and indoor air quality. IoT sensors and analytics platforms help landlords monitor occupancy patterns, reduce operating costs, improve preventive maintenance, and meet ESG-linked efficiency goals. This is making Grade A offices, IT parks, data centers, and mixed-use assets more intelligent, tenant-friendly, and competitive in cities such as Bengaluru, Hyderabad, Mumbai, Pune, Chennai, and NCR.

PropTech and CRE Transaction Platforms

PropTech and CRE transaction platforms digitizing property discovery, leasing, valuation, due diligence, and deal execution. These platforms help occupiers, brokers, developers, and investors compare assets, track market rents, manage documentation, and improve transparency in commercial property transactions. With rising institutional investment and demand for faster leasing decisions, digital CRE platforms are becoming important tools for office, retail, warehousing, coworking, and mixed-use asset transactions.

Green Building Technology and Net-Zero Achievement

Green building technology and net-zero achievement are shaping India’s commercial real estate technology landscape through energy-efficient HVAC systems, smart lighting, renewable power integration, low-carbon materials, and water-saving solutions. Developers and occupiers are increasingly adopting LEED, IGBC, GRIHA, and WELL-aligned buildings to reduce operating costs, improve ESG performance, and attract global tenants. This is pushing Grade A offices, IT parks, business parks, and mixed-use assets toward carbon monitoring, green certifications, solar integration, and net-zero-ready building operations.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Type |

Rental |

64.8% |

2025 |

|

End-Use |

Offices |

46.3% |

2025 |

|

Region |

West India |

34.5% |

2025 |

By Type

Rental dominates at 64.8% market share (2025). India's Grade A office rental market generates lease transactions with an average weighted rental across the top 8 cities of INR 85/sq.ft./month and rental growth of 8-12% in prime micro-markets (Mumbai BKC, Bengaluru ORR CBD, Hyderabad Financial District). Long-term lease commitments by GCCs create predictable income streams that justify institutional REIT ownership.

To access detailed market analysis, Request Sample

Sales at 35.2% are growing fastest at ~19.8% CAGR through three sub-channels: strata sale of Grade A office floors and REIT unit market trading on NSE/BSE.

By End Use

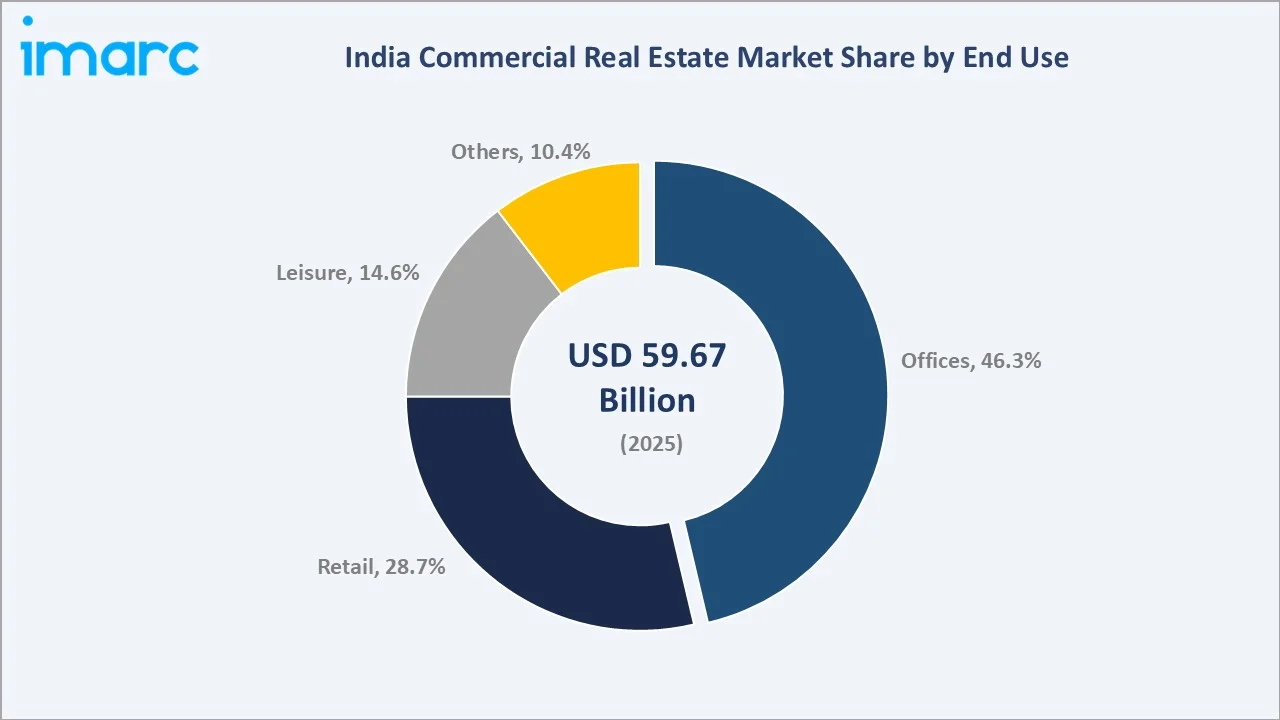

Offices lead at 46.3% market share (2025). India's high annual Grade A office absorption is concentrated across Bengaluru, Hyderabad, Mumbai, Pune, Delhi NCR, Chennai, Kolkata, and Ahmedabad/Hyderabad secondary markets. Technology sector, BFSI, and Engineering/Manufacturing/GCC are the three largest office demand categories.

Retail at 28.7% serves India's premium mall, high street, and lifestyle retail CRE market. Leisure at 14.6% encompasses hotels and hospitality real estate, entertainment venues, sports facilities, and gym/fitness spaces within mixed-use CRE. Others at 10.4% cover healthcare facilities, educational institutions, data centers, and logistics parks categorized as commercial real estate in the broader SEBI CRE investment framework.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers & Characteristics |

|

West India |

34.5% |

Supported by strong corporate activity, premium office demand, organized retail growth, logistics expansion, and institutional investment. The region benefits from mature business districts, high-quality infrastructure, and steady demand from finance, consulting, technology, media, and manufacturing occupiers. |

|

South India |

28.6% |

Strong demand from technology companies, global capability centers, research and development units, manufacturing firms, and flexible workspace operators. The region is characterized by large office campuses, competitive rentals, skilled talent availability, and growing demand for Grade A commercial assets. |

|

North India |

24.2% |

Expanding office, retail, coworking, and warehousing activity, supported by infrastructure development, metro connectivity, expressway-led growth, and rising corporate occupier demand. The region is gaining traction for business parks, mixed-use projects, and commercial developments near transport corridors and emerging urban centers. |

|

East India |

12.7% |

Supported by affordable rentals, improving infrastructure, growing retail activity, public-sector presence, and rising demand from small and mid-sized businesses. The region is gradually attracting commercial development through IT parks, logistics facilities, healthcare, education, and mixed-use projects. |

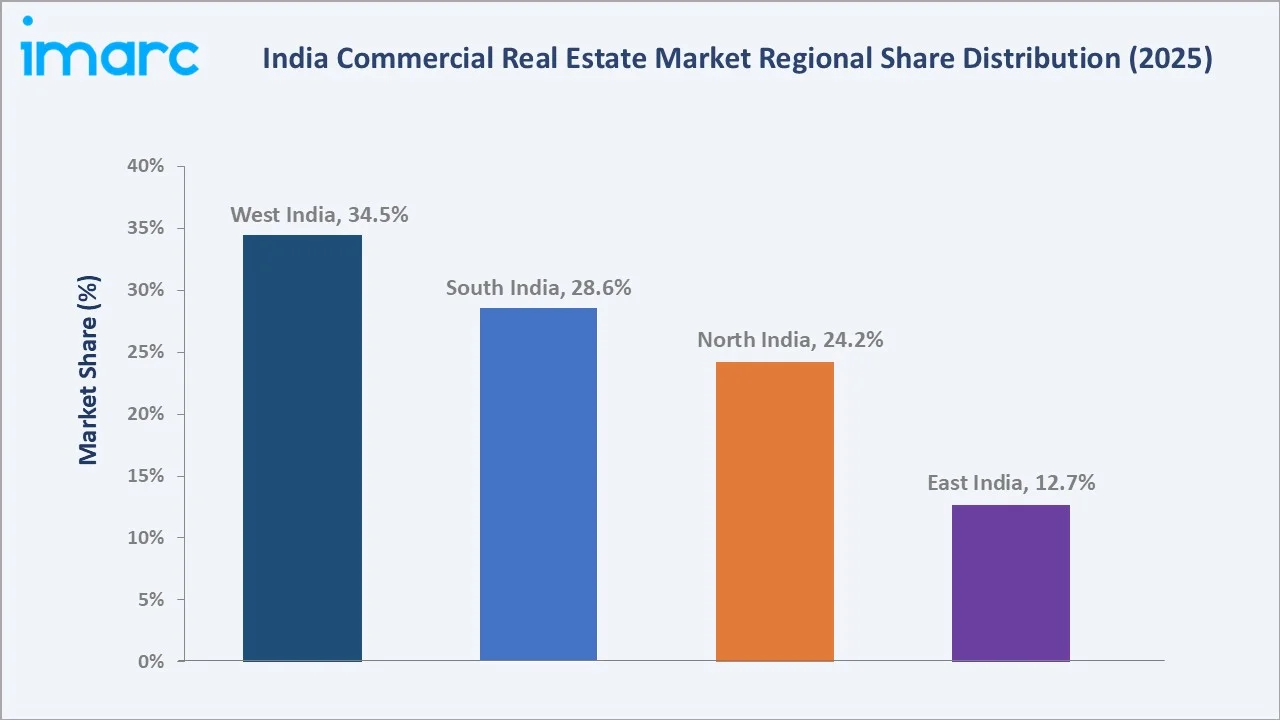

West India's 34.5% leadership is cemented by Mumbai's position as India's financial capital, generating the country's highest absolute CRE transaction values. Mumbai's BFSI sector generates high office demand concentration that skews West India's market value disproportionately above its floor area share. Pune's addition of GCC centers, making it India's GCC capital by number of centers amplifies West India's dominance in the GCC-driven demand cycle.

South India's 28.6%, growing fastest, reflects Bengaluru and Hyderabad's combined high annual office absorption. Bengaluru's irreplaceable talent concentration and Hyderabad's rising competitive advantage sustain South India's fastest-growing regional share trajectory. North India's 24.2% is anchored by Gurugram's DLF-dominated Grade A premium and Delhi Aerocity's emerging mixed-use CRE cluster. East India's 12.7% represents India's most significant CRE market development opportunity for 2026-2034, as Kolkata's cost advantage and Odisha-West Bengal infrastructure investment create new demand foundations.

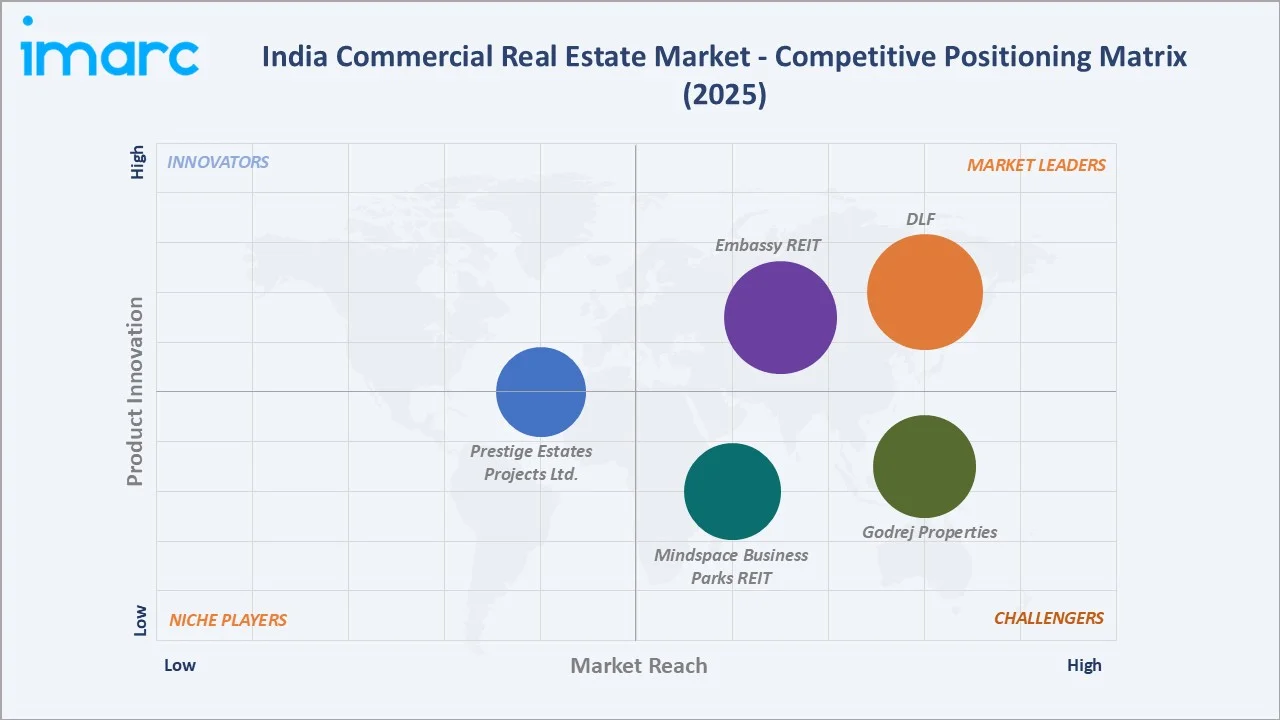

Competitive Landscape

India's commercial real estate market is moderately concentrated at the institutional ownership and REIT level, with the four listed REITs managing Grade A CRE representing approximately 16-18% of India's total Grade A commercial stock.

|

Company Name |

Portfolio |

Market Position |

Core Strength |

|

DLF |

DLF Offices, DLF Malls, DLF Hospitality |

Market Leader |

With over 70 years of real estate investment, development, and management experience, DLF has an unparalleled scale of delivery and an unmatched track record of customer-centric service excellence in India. |

|

Embassy REIT |

Embassy Manyata Business Park, Express Towers, Embassy Quadron, Embassy Galaxy, Embassy Splendid TechZone |

Market Leader |

Embassy REIT owns and operates a 50+ million square feet portfolio of 14 infrastructure-like office parks in India’s best-performing office markets of Bengaluru, Mumbai, Pune, and the National Capital Region and Chennai. |

|

Godrej Properties |

Nexspace, Godrej Carnival, Godrej Avenue 9, Godrej Square, Godrej One, Godrej BKC, Godrej Eternia |

Strong Challenger |

Godrej Properties received over 400 awards and recognitions, including Developer of the Year at the GRI India Awards, the Porter Prize, and recognition as India’s Most Trusted Real Estate Brand. |

|

Mindspace Business Parks REIT |

Mindspace Airoli, Mindspace Commerzone Raidurg, Madhapur, Commerzone Yerawada, Gera Commerzone Kharadi |

Strong Challenger |

Present in Mumbai Region, Hyderabad, Pune and Chennai, the key office markets of India. |

|

Prestige Estates Projects Ltd. |

Forum South Bengaluru, Forum Rex Walk, Twenty Four Hotel, |

Established Player |

Over the last decade, the Prestige Group has firmly established itself as one of the leading and most successful developers of real estate in India by imprinting its indelible mark across all asset classes. |

The competitive landscape is being reshaped by the REIT-driven institutional ownership model's expansion as more developers consider REIT or private placement of commercial portfolios, the institutional ownership share of Grade A CRE will increase from the current 18-20% toward 40%+ by 2034. Foreign PE funds will remain the largest institutional capital providers, while domestic institutional investors increase CRE allocation through REIT units and SM-REITs.

Key Company Profiles

DLF

DLF is India's largest and most prestigious commercial real estate developer. With more than 70 years of real estate investment, development, and management experience, DLF has an unparalleled scale of delivery and an unmatched track record of customer-centric service excellence in India.

- Portfolio: DLF Offices, DLF Malls, DLF Hospitality

- Recent Developments: In April 2026, DLF Mall of India launched TAG Heuer’s first franchise boutique in India in collaboration with Kapoor Watch Company. The new 517 sq. ft. store strengthens the mall’s premium retail portfolio and enhances its positioning as a luxury shopping destination.

- Strategic Focus: Expanding premium office, retail, and mixed-use assets through Grade A developments, luxury-led positioning, institutional leasing, and high-quality tenant partnerships.

Embassy REIT

Embassy REIT is India’s first publicly listed Real Estate Investment Trust. Embassy REIT owns and operates a 51.2 million square feet portfolio of 14 infrastructure-like office parks in India’s best-performing office markets of Bengaluru, Mumbai, Pune, and the National Capital Region (NCR) and Chennai. Embassy REIT’s portfolio comprises 40.4 msf of completed operating area and is home to 274 of the world’s leading companies.

- Portfolio: Embassy Manyata Business Park, Express Towers, Embassy Quadron, Embassy Galaxy, Embassy Splendid TechZone.

- Recent Developments: In December 2025, Embassy Office Parks REIT entered into definitive agreements to acquire a 0.3 million square feet marquee office property located within Embassy GolfLinks Business Park, one of Bengaluru’s most sought-after office markets. The transaction, valued at ₹8,520 million, aligns with Embassy REIT’s strategy of disciplined, accretive growth.

- Strategic Focus: Owning, operating, and expanding Grade A office parks and business campuses with strong institutional tenants, high occupancy, and stable rental income.

Market Concentration Analysis

India's Grade A commercial real estate market exhibits moderate concentration at the institutional ownership level and high concentration in specific micro-markets. BKC Mumbai is effectively controlled by three landlords, creating oligopoly pricing power that sustains INR 200-350/sq.ft./month Grade A rentals. At the national level, the top 10 Grade A office park developers control approximately 45-50% of India's total Grade A office stock, a concentration that reflects the high capital intensity and expertise requirements of Grade A development rather than regulatory barriers.

Concentration is expected to increase through 2034 as the REIT market matures, with 8-10 listed REITs projected by 2030 (including potential SM-REIT listings) managing 25-30% of total Grade A stock, with institutional PE funds controlling an additional 20-25% through unlisted fund structures. The combined institutional ownership share of 45-55% by 2034 will create a more transparent, liquid, and efficiently priced CRE market resembling mature APAC markets.

Investment & Growth Opportunities

Fastest Growing Segments

Sales type (~19.8% CAGR), office end-user (~19.5% CAGR), data center specialized CRE (~35%+ CAGR from smaller base), SM-REIT instrument (~30%+ CAGR creating new market tier), and South India regional market (~20%+ CAGR from GCC concentration) represent India's highest-growth CRE investment vectors.

Emerging Market Opportunities

East India's CRE market represents India's single largest geographic white space opportunity. Kolkata's Grade A market commands a 30-50% discount to comparable quality in Bengaluru or Pune, creating a structural cost advantage for back-office, BFSI operations, and IT delivery centers seeking operational cost optimization. Kolkata has 40%+ of India's skilled legal and accounting professional base, the West Bengal government's active IT investment promotion, and improving metro rail connectivity.

Investment Themes

- Data center real estate as regulated infrastructure investment: India's data center target requires USD 20-25 Billion in infrastructure investment with a 30-40% real estate component. Data center shell-and-core development near major cities and leasing to hyperscalers and colocation operators on 15-20 year triple-net leases generates superior risk-adjusted returns versus conventional Grade A office.

- GCC build-to-suit development in emerging Tier-2 GCC cities: Coimbatore (emerging semiconductor GCC hub), Kochi (finance and IT GCC), Nagpur (logistics and manufacturing GCC), and Jaipur (IT services and BFSI GCC) are receiving new GCC investments annually as companies seek cost optimization versus Bengaluru and Hyderabad.

Future Market Outlook (2026-2034)

The India commercial real estate market is projected to grow from USD 59.67 Billion in 2025 to USD 281.65 Billion by 2034, delivering an 18.82% CAGR over the forecast period. The market's anchor value of USD 141.31 Billion in 2030 represents a CRE landscape where India's REIT market has scaled to total market capitalization, GCC office demand has created new Grade A absorption across 2026-2030, and premium retail CRE has established institutional-grade operating metrics across 50+ Tier-1 and Tier-2 city mall assets.

Three structural forces define India's CRE market trajectory with high certainty through 2034: the GCC expansion wave reaching its structural peak creating new Grade A office demand that will sustain above-19% CAGR in the office end-user segment regardless of global economic cycles given the diversity of MNC nationalities represented in India's GCC ecosystem; the REIT market's deepening institutional liquidity enabling PE funds and developers to deploy into India Grade A CRE development confident of institutional exit mechanisms through both listed REIT acquisition and secondary institutional transactions; and India's consumption economy growth driving premium retail CRE's structural improvement creating the demand depth for 100+ new premium mall projects viable for Tier-2 city development.

Research Methodology

Primary Research

Primary research comprised structured interviews with 70+ industry stakeholders (2025), including Head of Commercial Leasing executives from DLF, Embassy Group, Prestige Group, and Godrej Properties; REIT fund managers from Embassy REIT, Mindspace REIT, and others; commercial brokerage heads from CBRE India, JLL India, Knight Frank India, and Colliers India; GCC real estate decision-makers from 15+ MNCs setting up or expanding India GCCs; SEBI REIT division officials; state government HMDA (Hyderabad), CIDCO (Mumbai), and Invest Karnataka officials; and institutional investors from GIC Singapore's India CRE team.

Secondary Research

Secondary research encompassed Embassy REIT, Mindspace REIT, Brookfield India REIT, and Nexus Select Trust investor presentations and annual reports (FY2023-FY2025); NASSCOM India GCC Landscape Report 2025; IBEF India Real Estate Report 2025; MCA REIT registration database; SEBI annual reports; India Budget 2025-26 infrastructure allocation analysis; PropEquity commercial transaction database. Over 120 secondary sources were reviewed.

Forecasting Models

Market revenue forecasts were developed using bottom-up type x end-user models calibrated against the CBRE India leasing transaction database, JLL India Net Absorption data by city and micro-market, REIT portfolio NAV growth trajectories, Vahan commercial property registration data, and IMF India GDP projections correlated with CRE demand intensity models. Key inputs include NASSCOM GCC employee growth projections, India retail consumption growth by income quintile, SEBI SM-REIT market size projections, data center MW deployment targets, and grade A office construction pipeline completions by city.

India Commercial Real Estate Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Types Covered | Rental, Sales |

| End Uses Covered | Offices, Retail, Leisure, Others |

| Regions Covered | North India, South India, East India, West India |

| Companies Covered | DLF, Embassy REIT, Godrej Properties, Mindspace Business Parks REIT, Prestige Estates Projects Ltd., etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the India commercial real estate market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the India commercial real estate market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the India commercial real estate industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the India Commercial Real Estate Market Report

The India CRE market reached USD 59.67 Billion in 2025, driven by India's GCC offices, record annual Grade A office absorption, REIT market scaling, premium retail CRE recovery to 97%+ occupancy in Grade A malls, and India's GDP growth toward USD 5 Trillion, creating structural commercial real estate demand.

The market grows at 18.82% CAGR during 2026-2034, reaching USD 281.65 Billion by 2034, driven by GCC expansion, SM-REIT market democratization, data center real estate emergence, Tier-2 city CRE formalization, and India's GDP economy generating domestic enterprise CRE demand.

Rental leads at 64.8% through Embassy REIT's portfolio, DLF rental assets, and Grade A leasing at INR 85/sq.ft./month average weighted rental.

Offices lead at 46.3%, driven by India's 1,800+ GCCs employing more knowledge workers requiring MSF Grade A space.

West India leads at 34.5%, anchored by Mumbai BKC's Grade A rental hosting BFSI, consulting, and MNC headquarters, and Pune's GCC centers generating high MSF annual Grade A absorption at competitive premium micro-markets.

Leading companies include DLF, Embassy REIT, Godrej Properties, Mindspace Business Parks REIT, and Prestige Estates Projects Ltd., among others.

The market is projected to reach approximately USD 141.31 Billion by 2030, with REIT market capitalization, Grade A office stock, South India overtaking West India in office absorption, and dedicated data center REITs emerging as a standalone institutional CRE category.

India's 1,800+ GCCs project to host over 2,500 GCCs employing 2.8-2.9 million professionals by 2030, generating additional Grade A demand. GCCs prefer BTS Grade A campuses on 5-10 year leases with LEED/IGBC certification requirements, commanding 15-25% rental premium over speculative supply and creating the recurring rental income streams that sustain REIT distribution yields.

Bengaluru and Hyderabad combined generate high annual office absorption versus NCR's 8-10 MSF (North India), driven by Bengaluru's IT professional talent pool, Hyderabad's record MSF absorption from HSBC GCC, Microsoft, and TCS expansions, and Telangana and Karnataka state government policy proactively attracting GCC investment with dedicated CRE parks and single-window clearance.

Three priority opportunities: data center shell-and-core development near major cities at INR 3,000-8,000/sq.ft./year to hyperscalers on long-term leases; Tier-2 city GCC BTS development in Coimbatore, Kochi, Nagpur, and Jaipur at 18-22% IRR from cost-competitive construction and pre-committed GCC leases; and SM-REIT listing of premium Tier-2 city malls providing 9-12% NOI yield retail CRE exposure currently inaccessible to institutional capital through conventional REIT thresholds.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)