India Crop Protection Chemicals Market Size, Share, Trends and Forecast by Product Type, Origin, Crop Type, Form, Mode of Application, and Region, 2026-2034

India Crop Protection Chemicals Market Size, Share, Trends & Forecast (2026-2034)

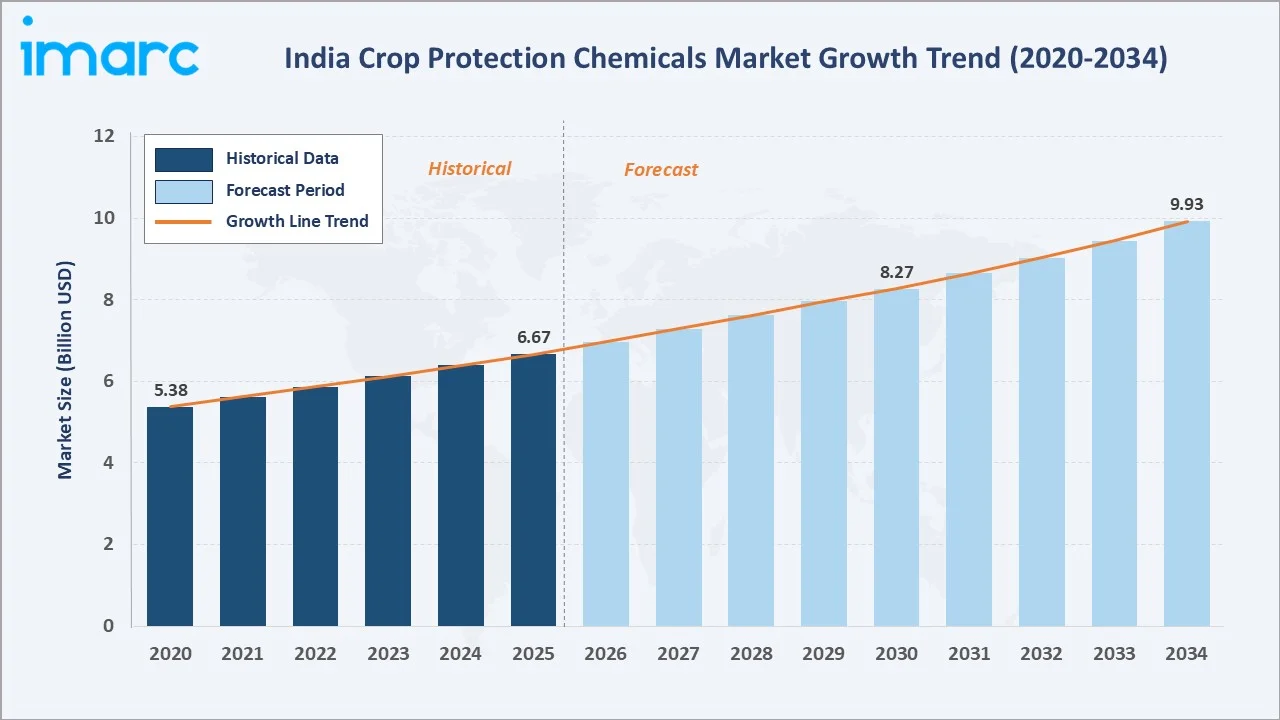

The India crop protection chemicals market size reached USD 6.67 Billion in 2025 and is projected to reach USD 9.93 Billion by 2034, exhibiting a CAGR of 4.38% during 2026-2034. The development of pest resistance to existing chemicals, expanding cultivable areas, rising food security imperatives, and government support for modern agricultural inputs are the primary forces driving market growth.

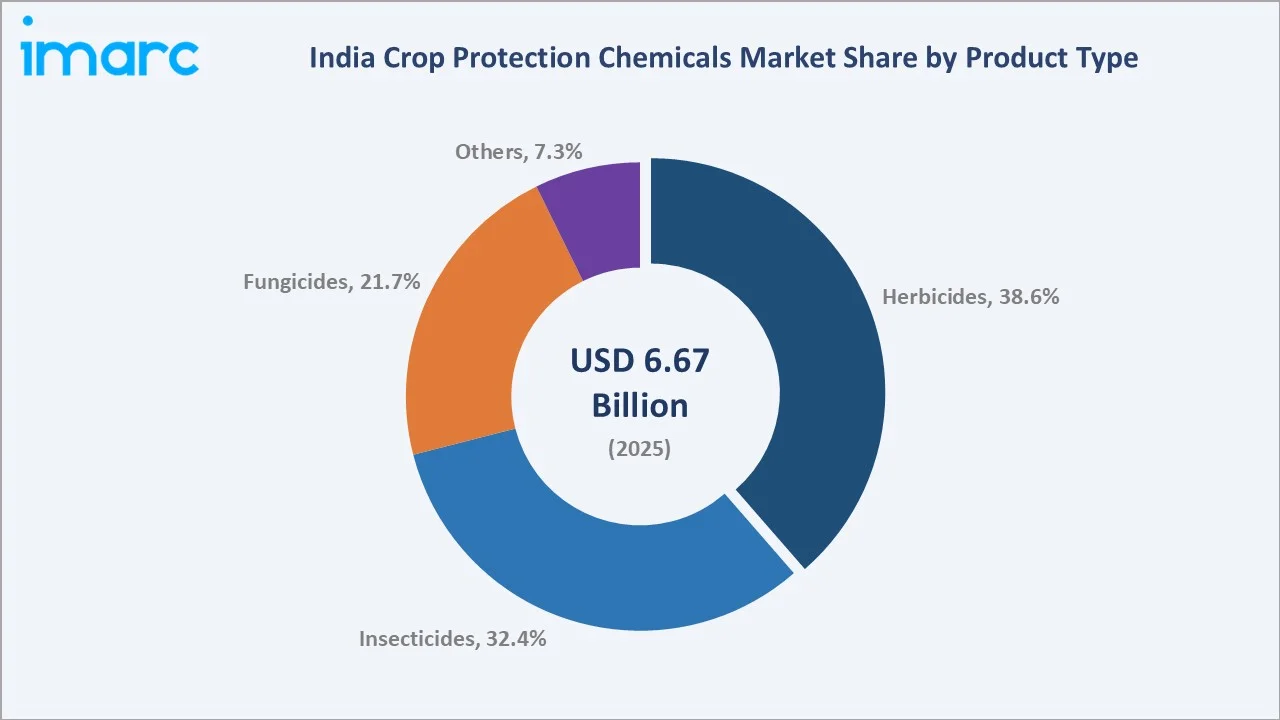

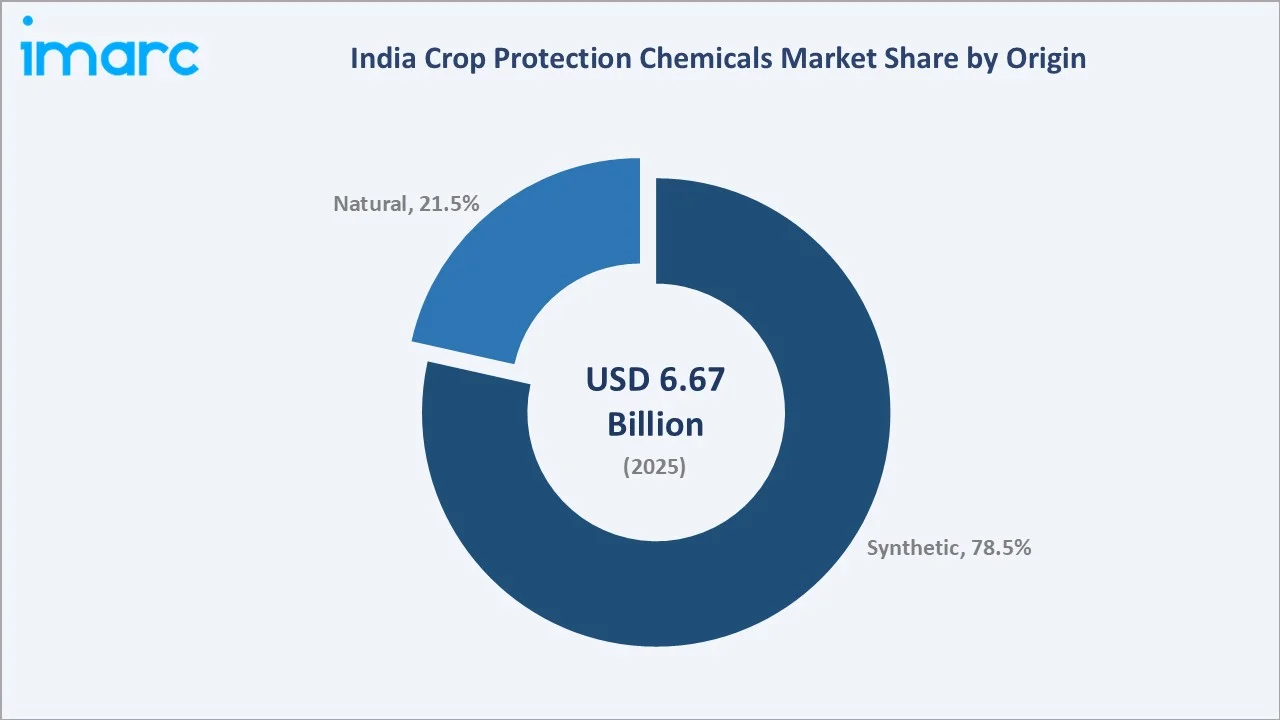

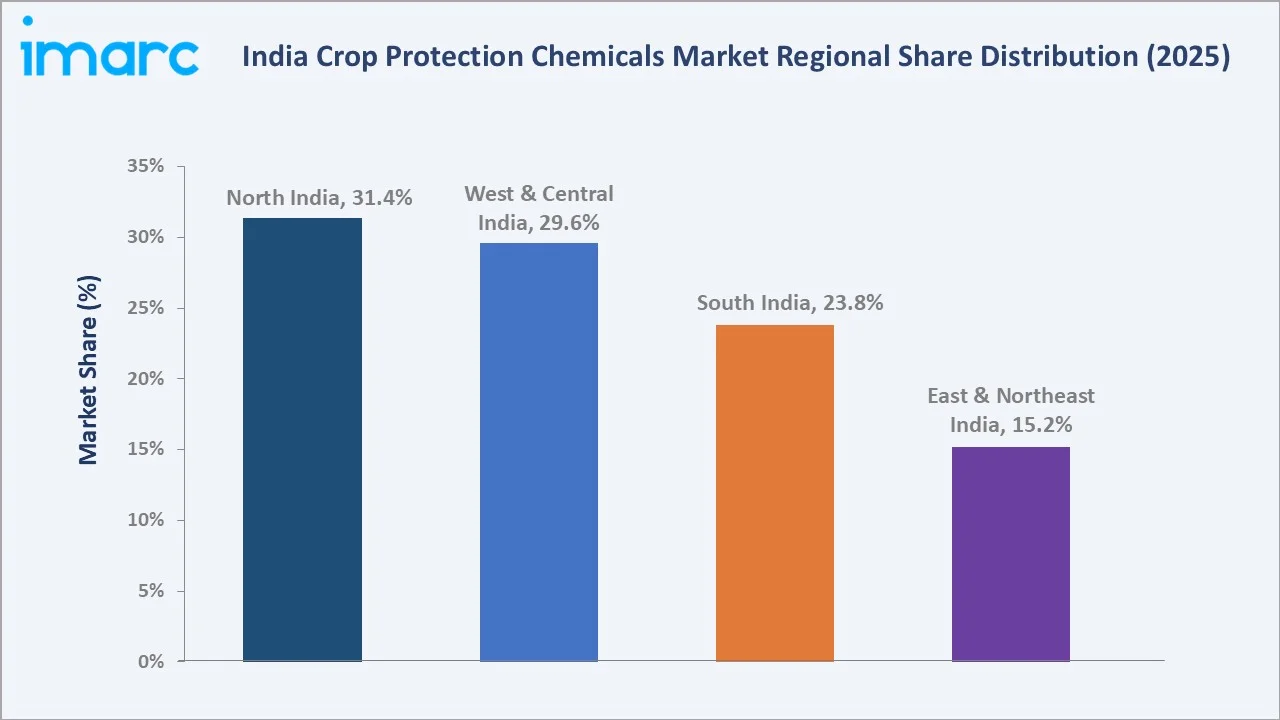

Herbicides dominate product type at 38.6% in 2025, while synthetic origin leads at 78.5%. North India commands the largest regional share at 31.4% in 2025.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 6.67 Billion |

|

Forecast Market Size (2034) |

USD 9.93 Billion |

|

CAGR (2026-2034) |

4.38% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Product Type |

Herbicides (38.6% share, 2025) |

|

Leading Origin |

Synthetic (78.5% share, 2025) |

|

Largest Region |

North India (31.4% share, 2025) |

|

Second Largest Region |

West and Central India (29.6% share, 2025) |

The India crop protection chemicals market growth trajectory from 2020 through 2034, with historical expansion to USD 6.67 Billion in 2025, reflects consistent agricultural-driven demand, while the forecast to USD 9.93 Billion captures accelerating precision farming adoption, biopesticide integration, and intensifying food production requirements across India's diverse agro-climatic zones.

To get more information on this market, Request Sample

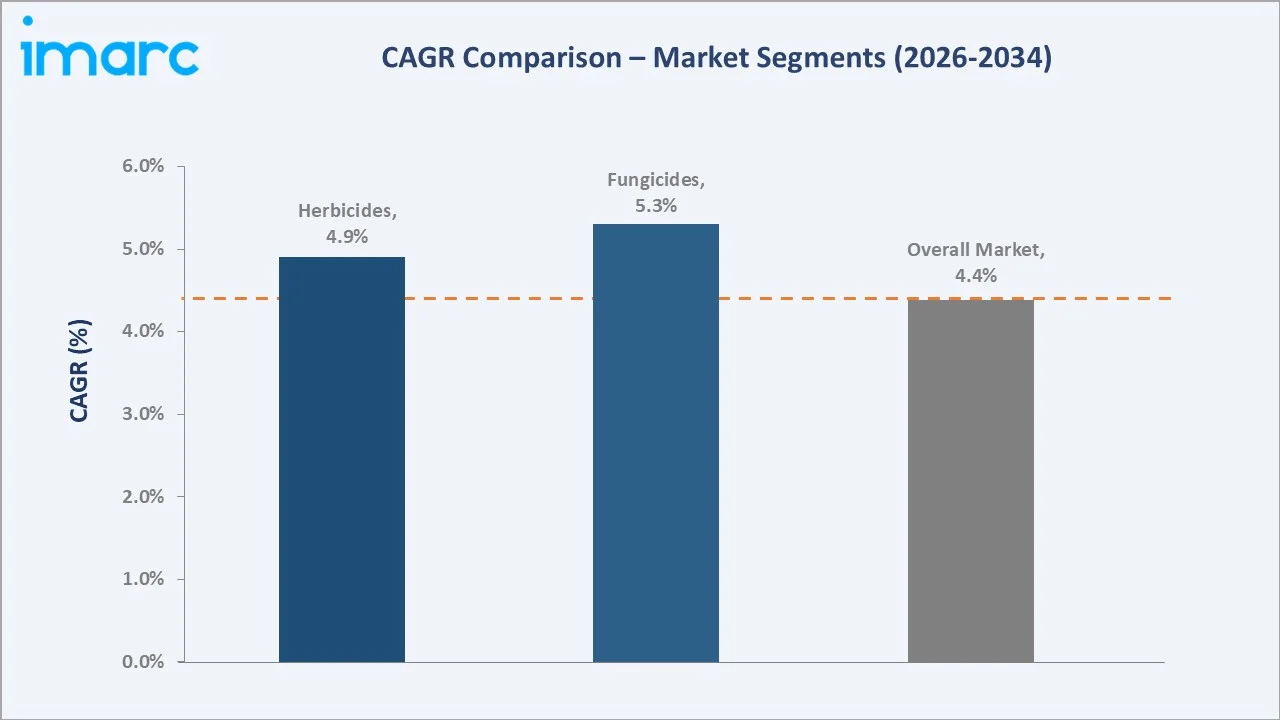

The CAGR trajectories across key product type, origin, and regional sub-segments, with fungicides at ~5.3% CAGR and natural origin at ~6.8% CAGR, are the fastest-growing categories within the India crop protection chemicals industry analysis through 2034.

Executive Summary

The India crop protection chemicals market is on a sustained growth trajectory from USD 6.67 Billion in 2025 to USD 9.93 Billion by 2034. Crop protection chemicals, essential for safeguarding India's food production from pests, diseases, and weeds, benefit from non-discretionary agricultural demand driven by the country's 140-million-hectare cultivated area.

Herbicides dominate product type at 38.6% in 2025, driven by rising weed management needs in cereal and oilseed crops. Insecticides hold 32.4%, essential for combating diverse pest species across India's tropical and subtropical agricultural belts. Fungicides (21.7%) are growing fastest, driven by intensifying climate-linked fungal disease pressure across rice, wheat, and horticulture.

Synthetic chemicals lead origin at 78.5% in 2025, reflecting cost efficiency and broad-spectrum efficacy. Natural/bio-based crop protection products (21.5%) are the fastest-growing segment, supported by PM-PRANAM and government sustainability mandates across all regions.

North India commands a 31.4% regional share, driven by the wheat-rice cropping belt and high chemical adoption in Punjab and Haryana. West and Central India (29.6%) follows, powered by Maharashtra cotton and Gujarat cash crop demand for intensive crop protection inputs.

Key Market Insights

|

Insight |

Data |

|

Largest Product Type |

Herbicides – 38.6% share (2025) |

|

Leading Origin |

Synthetic – 78.5% share (2025) |

|

Leading Region |

North India – 31.4% share (2025) |

|

Second Leading Region |

West and Central India – 29.6% share (2025) |

|

Top Companies |

Bayer AG, BASF, Corteva, UPL, Rallis India Limited, Insecticides India, Crystal Crop Protection Ltd., ADAMA |

Key Analytical Observations Expanding on the Above Data:

- Herbicides, with 38.6% in 2025, dominate because of rising labor costs and weed pressure in rice-wheat and maize cropping systems, making chemical weed control economically superior to manual weeding across India's large agricultural holdings.

- Synthetic chemicals, with 78.5% in 2025, lead due to their cost advantage, established regulatory approval status, and broad-spectrum efficacy for high-volume field crop applications across India's diverse agro-climatic zones.

- North India's 31.4% dominance reflects high-input intensive agriculture of Punjab, Haryana, and Uttar Pradesh, where chemical adoption rates are among the highest in the country due to commercial cereal farming.

- West and Central India, with 29.6% in 2025, benefits from Maharashtra's large cotton acreage requiring intensive insecticide application and Gujarat's expanding cash crop cultivation base.

India Crop Protection Chemicals Market Overview

Crop protection chemicals, encompassing herbicides, insecticides, fungicides, and other pesticides, are substances applied in agriculture to manage pests, diseases, and weeds threatening crop yield and quality. They are classified by product type, origin (synthetic or natural), crop application, formulation form, and mode of application across India's diverse agricultural regions.

The India crop protection chemicals ecosystem integrates global agrochemical innovators, domestic formulators, active ingredient manufacturers, agri-distributors, cooperative input networks, regulatory bodies, and diverse end-use segments spanning cereals, horticulture, oilseeds, pulses, and commercial crops across India's varied agro-climatic zones.

Market Dynamics

To evaluate market opportunities, Request Sample

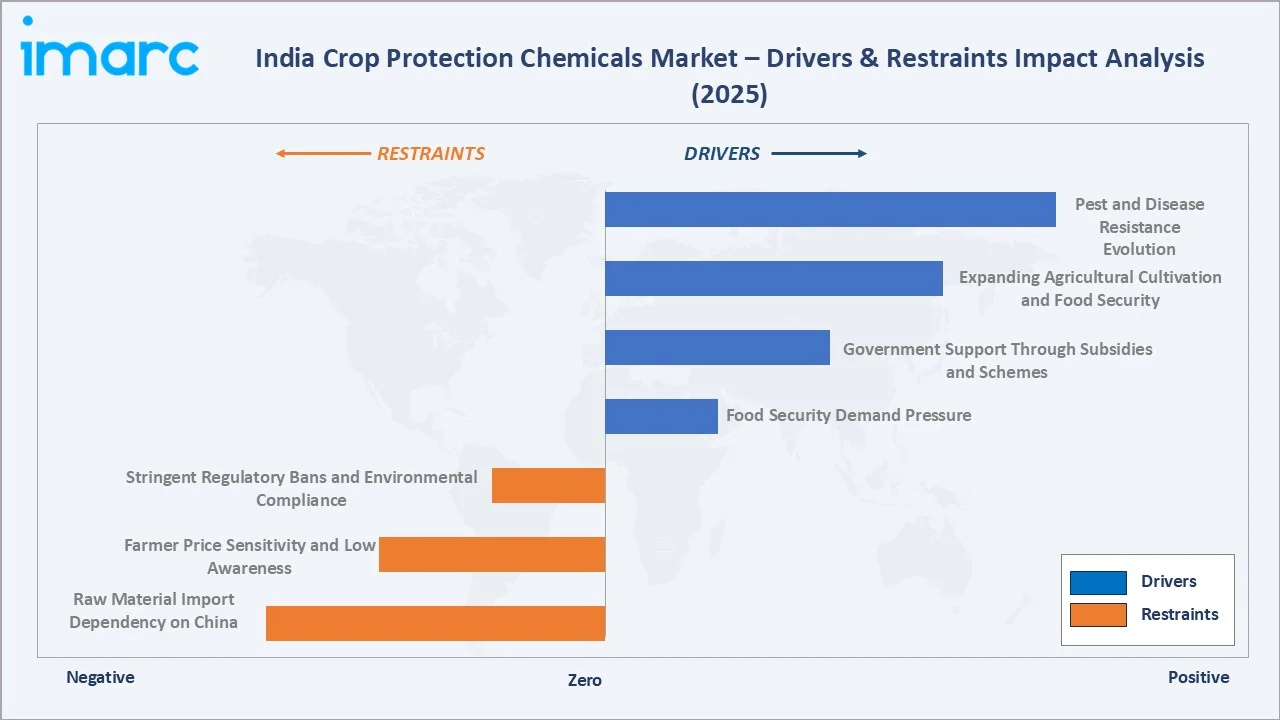

Market Drivers

- Pest and Disease Resistance Evolution: Resistance of pests and pathogens to existing chemicals necessitates continuous introduction of novel active ingredients. India's regulatory authority approved 27 new crop protection products in July 2025, reflecting intensifying resistance management pressure across all major cropping systems.

- Expanding Agricultural Cultivation and Food Security Demand: India's agricultural area exceeds 140 million hectares. Rising food demand from a 1.46 billion population creates sustained pressure to protect yields, driving per-hectare crop protection chemical consumption growth across all crop categories.

- Government Support Through Subsidies and Agricultural Schemes: Government subsidies on agrochemical inputs and dedicated farm support schemes promoting responsible chemical use are expanding market access and farmer adoption of regulated crop protection solutions across all agro-climatic regions.

Market Restraints

- Stringent Regulatory Bans and Environmental Compliance: India has banned more than 27 pesticides in recent years. Ongoing regulatory reviews create product discontinuation risks for manufacturers and constrain market growth by removing established formulations from the active ingredient portfolio.

- Farmer Price Sensitivity and Low Awareness: A significant proportion of India's farm households operate marginal landholdings. High input costs relative to farm income limit adoption of premium crop protection products, particularly among smallholder farmers in rain-fed and tribal agricultural regions.

Market Opportunities

- Biopesticide and Natural Origin Segment Growth: The crop protection market is witnessing increasing demand for bio-based and natural alternatives, driven by rising awareness around food safety, environmental concerns, and evolving regulatory standards in export markets. This shift is encouraging manufacturers to expand their portfolios toward eco-friendly solutions and invest in sustainable product development. Supportive policy frameworks and incentives are further accelerating the adoption of biological inputs over conventional chemical-based products.

- Precision Agriculture and Drone-Based Application Expansion: India's drone spraying policy liberalization has opened a high-efficiency application channel. Drone-enabled precision spraying reduces chemical dosage by 20-30% while improving coverage uniformity, expanding effective market reach across large-scale farms.

Market Challenges

- Raw Material Import Dependency on China: The domestic crop protection industry remains significantly dependent on imports for key raw materials and intermediates, exposing manufacturers to external supply chain disruptions. Factors such as geopolitical tensions, currency fluctuations, and logistical constraints can lead to cost volatility and supply uncertainties. This reliance impacts production planning and pricing stability for formulators. In response, companies are increasingly exploring backward integration, supplier diversification, and localization strategies to enhance supply security and reduce dependency on imports.

- Counterfeit and Sub-Standard Product Proliferation: The penetration of spurious and adulterated pesticides through informal distribution channels undermines farmer confidence, creates crop damage liability risks, and distorts genuine market demand growth across rural agricultural regions.

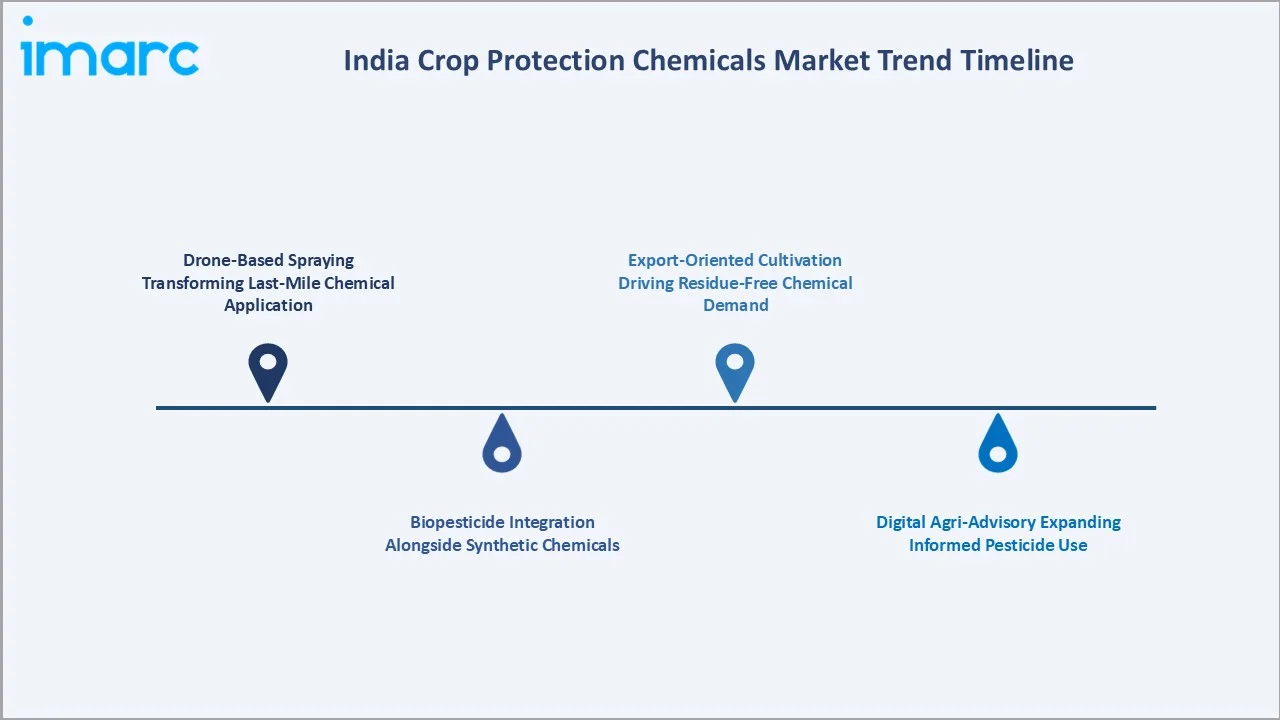

Emerging Market Trends

1. Drone-Based Spraying Transforming Last-Mile Chemical Application

Government-approved drone spraying programs are transforming how crop protection chemicals reach farm fields. Drone application improves penetration, reduces drift, and enables precision dosage, driving demand for compatible formulations and expanding effective market penetration in remote agricultural areas.

2. Biopesticide Integration Alongside Synthetic Chemicals

Integrated Pest Management strategies are driving co-adoption of synthetic and biological crop protection products. Formulators are developing combination products that deliver synthetic efficacy with reduced residue profiles, addressing export market regulatory requirements and domestic sustainability mandates.

3. Digital Agri-Advisory Expanding Informed Pesticide Use

Digital platforms and government-backed mobile applications are delivering pest identification, weather-based spray advisories, and product recommendations directly to farmers, increasing informed and targeted crop protection chemical usage while reducing over-application and associated environmental impacts.

4. Export-Oriented Cultivation Driving Residue-Free Chemical Demand

India's growing agricultural export ambitions are compelling farmers in horticulture belts to adopt export-compliant, low-residue crop protection formulations meeting international Maximum Residue Limit standards set by importing countries in Europe and North America for fresh produce.

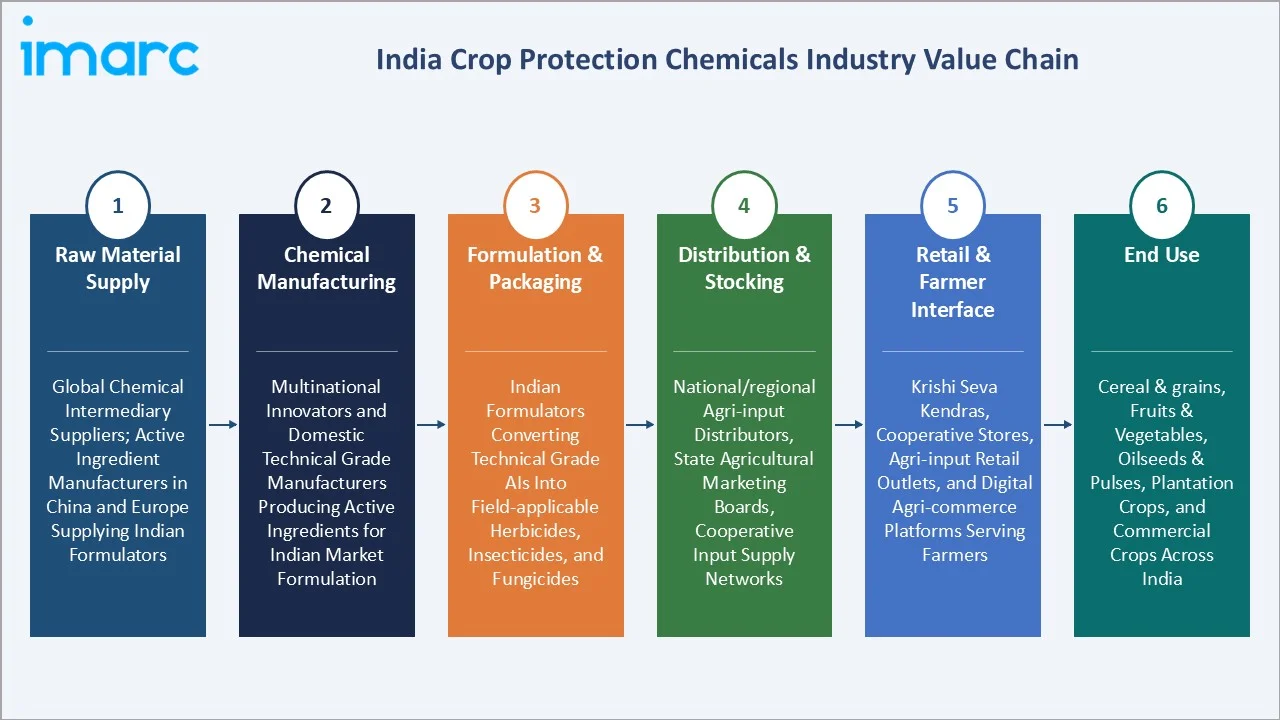

Industry Value Chain Analysis

The crop protection chemicals value chain in India spans six stages from raw material supply through end-use application. Formulation and packaging stages capture the highest value-add margins, while multi-tier distribution logistics through agri-input networks require substantial working capital from manufacturers and distributors across the agricultural supply ecosystem.

|

Stage |

Key Players / Examples |

|

Raw Material Supply |

Global chemical intermediary suppliers; active ingredient manufacturers in China and Europe supplying Indian formulators |

|

Chemical Manufacturing |

Multinational innovators and domestic technical grade manufacturers producing active ingredients for Indian market formulation |

|

Formulation & Packaging |

Indian formulators converting technical grade active ingredients into field-applicable herbicides, insecticides, and fungicides |

|

Distribution & Stocking |

National and regional agri-input distributors, state agricultural marketing boards, and cooperative input supply networks |

|

Retail & Farmer Interface |

Krishi Seva Kendras, cooperative stores, agri-input retail outlets, and digital agri-commerce platforms serving farmers |

|

End Use |

Cereal and grains, fruits and vegetables, oilseed and pulses, plantation crops, and commercial crops across India |

Integrated companies combining active ingredient synthesis with formulation capabilities and proprietary distribution networks achieve meaningfully lower cost structures than formulators relying entirely on imported active ingredient procurement, providing a sustainable competitive advantage in the market.

Technology Landscape in the India Crop Protection Chemicals Industry

Novel Molecule Development: Diamide and SDHI Chemistry

Diamide insecticides and SDHI fungicides represent the frontier of crop protection chemistry, offering superior selectivity, lower dosage rates, and reduced mammalian toxicity profiles compared to legacy organophosphate and carbamate chemistries that have been progressively banned across Indian agricultural markets.

Formulation Technology: Nano-Emulsions and Water-Dispersible Granules

Advanced formulation technologies including nano-emulsions, suspension concentrates, and water-dispersible granules are improving bioavailability, reducing solvent usage, and enabling precise dosage delivery that meets evolving regulatory requirements for safer and more effective crop protection product applications.

Biological and Fermentation-Based Active Ingredients

Microbial biopesticides based on Bacillus thuringiensis, Beauveria bassiana, Trichoderma, and Nuclear Polyhedrosis Virus are gaining registration and commercial adoption as complementary tools within integrated pest management programs across diverse Indian cropping systems and agro-climatic regions.

AI-Driven Pest Prediction and Decision Support Systems

Machine learning models integrating satellite imagery, weather data, and historical pest outbreak records are enabling predictive pest management. Early warning systems reduce reactive over-spraying and optimize chemical application timing for maximum crop protection efficacy with minimum environmental impact.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Product Type |

Herbicides |

38.6% |

2025 |

|

Origin |

Synthetic |

78.5% |

2025 |

|

Crop Type |

🔒 |

🔒 |

2025 |

|

Mode of Application |

🔒 |

🔒 |

2025 |

|

Region |

North India |

31.4% |

2025 |

By Product Type

Herbicides command a 38.6% majority share in 2025 owing to rising weed management challenges in high-value cereal, oilseed, and commercial crops. Labor cost escalation across India's agricultural sector makes chemical weed control economically superior to manual weeding across large holdings.

To access detailed market analysis, Request Sample

Insecticides at 32.4% in 2025 remain essential across India's tropical cropping systems where diverse pest species require season-long management. Fungicides (21.7%) are growing fastest, driven by increasing rice blast, wheat rust, and vegetable fungal disease pressure linked to climate variability. Others (7.3%) include nematicides, rodenticides, and plant growth regulators across specialty crops.

By Origin

Synthetic origin dominates at 78.5% in 2025, reflecting established regulatory frameworks, cost efficiency, and broad-spectrum efficacy across India's high-pest-pressure agricultural environment. Synthetic products benefit from extensive farmer familiarity, decades of application experience, and deep distribution infrastructure reaching even remote rural agricultural markets effectively.

Natural/bio-based products at 21.5% in 2025 are growing at approximately 6.8% CAGR, the fastest segment, driven by export market residue requirements, organic farming expansion, government biopesticide promotion programs, and growing farmer awareness of resistance management through chemical alternation.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

|

North India |

31.4% |

Wheat-rice belt; high chemical adoption; Punjab and Haryana commercial farming |

|

West and Central India |

29.6% |

Maharashtra cotton; Gujarat cash crops; Madhya Pradesh soybean cultivation |

|

South India |

23.8% |

Horticulture clusters; rice paddy fungicide demand; vegetable growing belts |

|

East and Northeast India |

15.2% |

Emerging market; rice cultivation; tea plantation fungicide adoption potential |

North India's 31.4% market dominance in 2025 is driven by the structurally exceptional combination of high-intensity cereal cultivation in the Indo-Gangetic Plain, well-developed agrochemical distribution infrastructure, and historically high chemical adoption rates among commercial farmers.

West and Central India, with 29.6% in 2025, is driven by Maharashtra's dominant cotton acreage requiring intensive bollworm insecticide management and Gujarat's expanding vegetable and groundnut cultivation generating strong herbicide and fungicide demand across the regional agricultural belt.

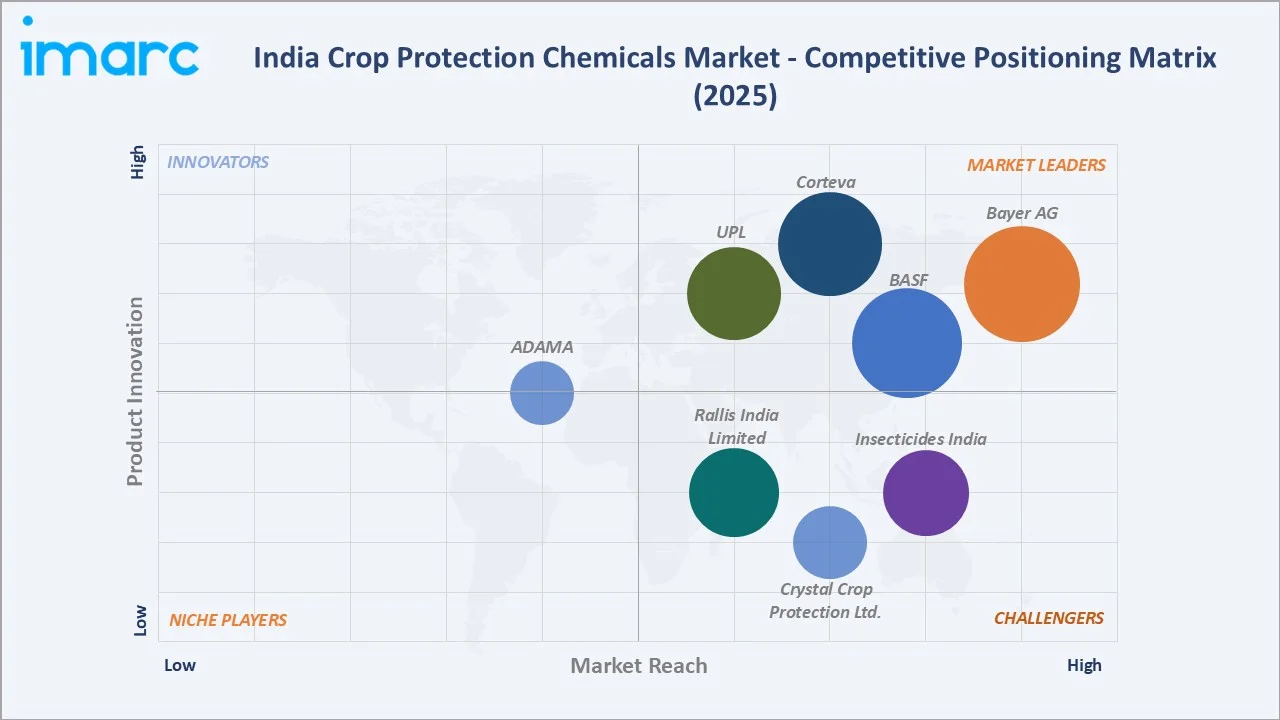

Competitive Landscape

The India crop protection chemicals market is moderately concentrated, with global multinationals holding premium-priced innovation-driven positions alongside strong domestic companies competing on price, distribution reach, and farmer trust in the economy and generic formulation segments.

|

Company Name |

Key Products |

Market Position |

Global Strategic Focus |

|

Bayer AG |

Curbix Pro, Decis, Nativo, Movento, Roundup, Serenade, Sivanto |

Leader |

Broad portfolio; strong R&D; digital agri-integration |

|

BASF |

Acrisio, Acrobat, Merivon, Basagran, Basta, Efficon, Exponus, Imunit |

Leader |

Fungicide strength; sustainable agriculture programs |

|

Corteva |

Almix, Assert, Equation Pro, Galileo, Loyant, Novlect |

Leader |

Novel molecules; seed treatment focus; innovation pipeline |

|

UPL |

Brucia, Karobiz, Avancer Glow, Tridium, Saaf, Reinster |

Leader |

India-origin global leader; cost-efficient formulations |

|

Rallis India Limited |

Taffy, Tata Mida, Zygant, Trot, Patang, Trimbo, Taarak, Tata Pinda, Headwin, Themifit, Castello, Capstone |

Challenger |

Rural distribution strength; Tata Group brand trust |

|

Insecticides India |

Brahmos, Centran SC, Altair, Amuse |

Challenger |

Strong domestic brand; economical segment focus |

|

Crystal Crop Protection Ltd. |

Abacin, Apex-50, ACM-9, Allquit, Avtaar, Bango, Azotrix, Bavistin, Kyoto |

Challenger |

Fast-growing Indian company; innovative product pipeline |

|

ADAMA |

Blasil, Blastogan, Bumper, Agil, Atranex, Dekel |

Emerging |

Generic formulations; competitive pricing positioning |

Key players include Bayer AG, BASF, Corteva, UPL, Rallis India Limited, Insecticides India, Crystal Crop Protection Ltd., ADAMA, and others.

Key Company Profiles

Bayer AG

Bayer AG is a global life sciences leader with a major presence in India's crop protection market through Bayer CropScience India. The company leads in insecticides, herbicides, and fungicide innovation across India's rice, cotton, vegetable, and cereal cropping systems with a comprehensive portfolio.

- Product Portfolio: Curbix Pro, Decis, Nativo, Movento, Roundup, Serenade, Sivanto, and others

- Recent Developments: In May 2023, Bayer partnered with agri-tech startup Superplum to develop a sustainable crop protection model aimed at improving productivity and quality for fruit growers across key agricultural regions in India. The collaboration focuses on integrating scientific crop protection practices with a digitally enabled, traceable supply chain to enhance farm-level outcomes and market linkages.

- Strategic Focus: Bayer's strategy leverages its global R&D pipeline to introduce novel molecules to the Indian market while expanding digital agri-advisory tools that build farmer loyalty and optimize chemical use efficiency across diverse cropping systems.

UPL

UPL is India's largest and globally positioned agrochemical company, manufacturing and marketing a broad portfolio of generic and patented crop protection products across domestic and international markets with a strong distribution network reaching India's rural agricultural communities.

- Product Portfolio: Brucia, Karobiz, Avancer Glow, Tridium, Saaf, Reinster, and others.

- Recent Developments: In May 2022, UPL Limited India has partnered with Koppert India to advance sustainable agriculture practices across the country. As part of this collaboration, UPL will distribute a biofertilizer developed by Koppert under its Natural Plant Protection (NPP) division. This product is designed to improve soil quality, support stronger plant growth, and ultimately increase agricultural output.

- Strategic Focus: UPL's strategy combines generic cost leadership with accelerating biological and specialty chemical innovation, building an integrated portfolio that serves both price-sensitive smallholders and premium commercial farming segments across Indian and global markets.

Rallis India Limited

Rallis India Limited is one of India's oldest and most respected domestic agrochemical companies, operating under the Tata Group umbrella. It serves the full crop protection chemicals spectrum with a particular strength in domestic distribution depth and farmer brand recognition across rural markets.

- Product Portfolio: Taffy, Tata Mida, Zygant, Trot, Patang, Trimbo, Taarak, Tata Pinda, Headwin, Themifit, Castello, Capstone, and others.

- Recent Developments: In November 2025, Rallis India Limited has entered a strategic partnership with Paryan Alliance Pvt. Ltd. to introduce FullPage, an herbicide-tolerant rice technology, in India. Under this agreement, Rallis India will serve as the licensed partner responsible for bringing FullPage technology to Indian farmers. The system combines advanced herbicide-tolerant seeds, suitable crop protection products, and optimized agronomic practices to improve farming efficiency.

- Strategic Focus: Rallis focuses on combining its deep rural distribution infrastructure with portfolio upgrades toward newer-chemistry molecules, leveraging Tata Group brand trust to compete effectively against multinational companies in the Indian agrochemical market.

Market Concentration Analysis

The India crop protection chemicals market is moderately concentrated, with global multinationals collectively holding the majority of value share in premium segments, while domestic players dominate the economy and generic formulation segments through distribution network advantages across India's rural agricultural markets and cooperative input supply channels.

Consolidation is accelerating as multinational companies pursue inorganic growth through acquisitions of domestic formulators, while Indian companies scale internationally. This dual consolidation trend is reshaping competitive dynamics across both premium innovation-led and cost-competitive generic segments of the India crop protection chemicals market through the forecast period.

Investment & Growth Opportunities

Fastest-Growing Segments

Natural/bio-based crop protection at approximately 6.8% CAGR through 2034 is the highest-growth segment, driven by export market residue compliance requirements, organic farming expansion, and government incentive programs promoting integrated pest management across India's diverse cropping systems.

Emerging Markets

East and Northeast India represents the fastest-growing regional market opportunity through 2034. Assam tea plantations, West Bengal rice cultivation, and Northeast India's expanding horticulture acreage are creating significant untapped crop protection chemical demand from underserved agricultural regions.

Venture & Investment Trends

Private equity interest in Indian agrochemical companies is growing, driven by India's strategic position as the fourth-largest global pesticide producer and an expanding domestic consumption market. Agricultural fintech integration enabling credit-backed input procurement is expanding effective demand by bridging the capital gap for smallholder farmers across India's rural agricultural communities.

Future Market Outlook (2026-2034)

The India crop protection chemicals market is forecast to expand from USD 6.67 Billion in 2025 to USD 9.93 Billion by 2034 at a CAGR of 4.38%, adding USD 3.26 Billion in incremental annual market value over the forecast period, reflecting consistent demand from India's large agricultural sector.

Three forces will most significantly shape the India crop protection chemicals industry through 2034: the biopesticide transition driven by export market residue regulations and domestic sustainability mandates; digital agriculture integration creating precision application efficiency; and the regulatory environment's progressive removal of older chemistries, accelerating product innovation and registration cycles.

Research Methodology

Primary Research

Primary research encompassed structured interviews with crop protection chemicals industry stakeholders including agrochemical company sales managers, agricultural extension officers, farm input distributors, regulatory professionals, and farmer cooperative representatives across North, West, South, and East India. Primary data validated market sizing, segment shares, regional demand estimates, and technology adoption timelines across India's diverse agro-climatic zones.

Secondary Research

Key secondary sources include IMARC Group industry databases, Directorate of Plant Protection Quarantine & Storage pesticide usage data, FAO agricultural statistics, Ministry of Agriculture & Farmers' Welfare reports, CIB&RC registration records, Pesticides Manufacturers and Formulators Association of India data, and trade publications including Agrochemicals India and AgriBusiness Global.

Forecasting Models

Market size estimations and growth projections were derived using a combination of top-down and bottom-up forecasting models, incorporating agricultural GDP growth rates, cultivated area expansion indices, per-hectare chemical consumption trends, and historical market evolution patterns. Scenario analysis was performed to account for regulatory and macroeconomic uncertainty throughout the forecast period.

India Crop Protection Chemicals Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Product Types Covered | Herbicides, Fungicides, Insecticides, Others |

| Origins Covered | Synthetic, Natural |

| Crop Types Covered | Cereal and Grains, Fruits and Vegetables, Oilseed and Pulses, Others |

| Forms Covered | Liquid, Solid |

| Mode of Applications Covered | Foliar Spray, Seed Treatment, Soil Treatment, Others |

| Regions Covered | North India, West and Central India, South India, East and Northeast India |

| Company Covered | Bayer AG, BASF, Corteva, UPL, Rallis India Limited, Insecticides India, Crystal Crop Protection Ltd., ADAMA, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the India crop protection chemicals market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the India crop protection chemicals market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the India crop protection chemicals industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the India Crop Protection Chemicals Market Report

The India crop protection chemicals market reached USD 6.67 Billion in 2025, reflecting consistent demand from India's large agricultural sector, rising pest resistance challenges, and government support for modern agricultural input adoption across all major agro-climatic regions.

The market is projected to reach USD 9.93 Billion by 2034, growing at a CAGR of 4.38% during 2026-2034, driven by pest resistance evolution, expanding cultivable area, intensifying food security imperatives, and growing precision farming adoption across India's agricultural sector.

Herbicides lead with a 38.6% product share in 2025, valued for managing weed pressure in cereal, oilseed, and commercial crop production systems across India's diverse agro-climatic regions with rising labor costs making chemical weed control economically essential.

Synthetic origin dominates at 78.5% in 2025, reflecting cost efficiency, regulatory approval depth, established farmer familiarity, and broad-spectrum efficacy across India's high-pest-pressure agricultural landscape spanning multiple crop categories and regions.

North India commands a dominant 31.4% market share in 2025, driven by high-input wheat-rice cultivation in Punjab, Haryana, and Uttar Pradesh with among the highest per-hectare chemical application rates and well-developed agrochemical retail distribution infrastructure.

Natural/bio-based crop protection is the fastest-growing origin segment at approximately 6.8% CAGR through 2034, supported by export residue regulations, organic farming growth, and government biopesticide incentive programs across India's agricultural regions.

Leading companies include Bayer AG, BASF, Corteva, UPL, Rallis India Limited, Insecticides India, Crystal Crop Protection Ltd., ADAMA, and others.

Key drivers include pest and disease resistance evolution necessitating new product introduction, expanding agricultural cultivation area, rising food security demand from a growing population, government subsidy support, and growing adoption of modern precision farming practices.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)