India Esports Market Size, Share, Trends and Forecast by Revenue Source, Games, Platform, and Region, 2026-2034

India Esports Market Summary:

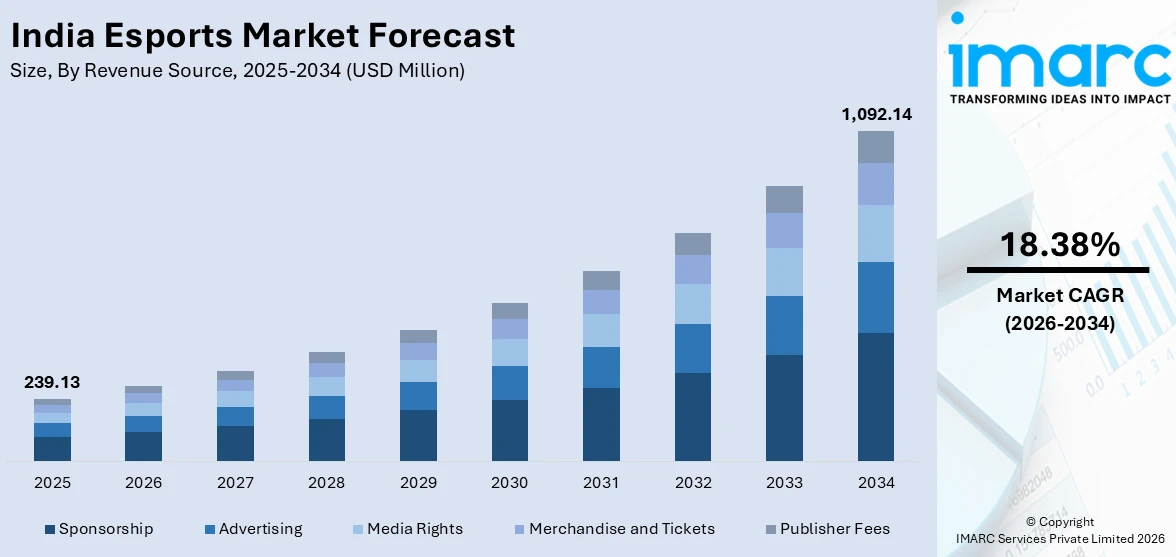

The India esports market size was valued at USD 239.13 Million in 2025 and is projected to reach USD 1,092.14 Million by 2034, growing at a compound annual growth rate of 18.38% from 2026-2034.

The India esports market is experiencing rapid growth fueled by rising internet penetration, affordable smartphone access, and increasing youth engagement with competitive gaming. The growing government recognition, professionalization of esports leagues, rising cross-industry sponsorship investments, and the proliferation of mobile-first tournament formats are reshaping the competitive landscape. The emergence of streaming platforms, content creator economies, and institutional support from educational bodies are strengthening the ecosystem, positioning India as a key growth market for next-generation digital entertainment and competitive gaming.

Key Takeaways and Insights:

- By Revenue Source: Sponsorship dominates the market with a share of 32% in 2025, owing to the increasing brand investments in tournament partnerships, team affiliations, and influencer collaborations targeting the youth demographic.

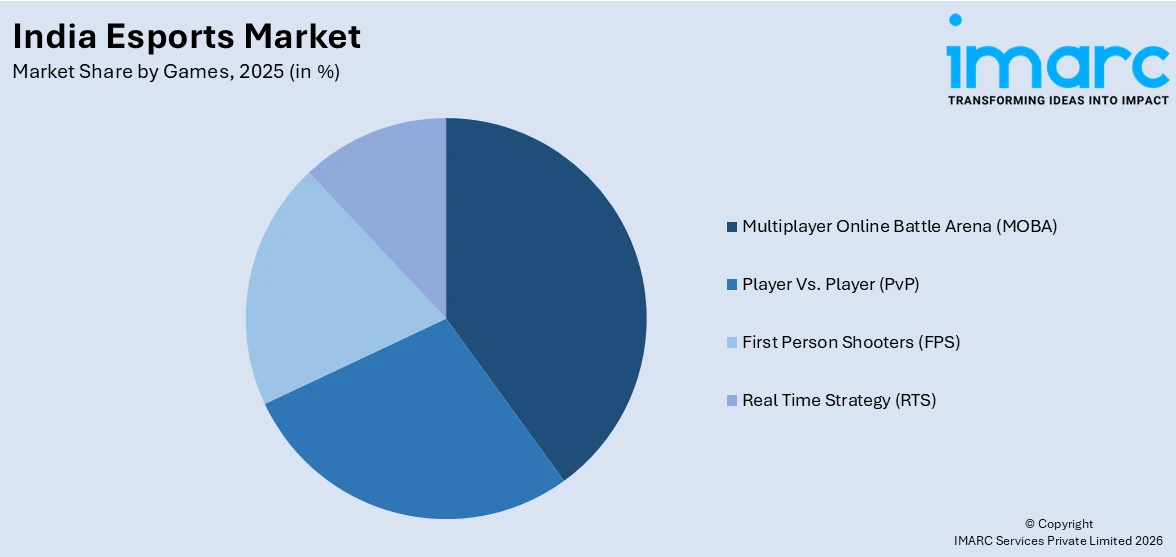

- By Games: Multiplayer online battle arena (MOBA) leads the market with a share of 28% in 2025, supported by the genre's strong community engagement, team-based competitive appeal, and widespread mobile accessibility across India.

- By Platform: Mobile and tablets represent the largest segment with a market share of 45% in 2025, reflecting India's mobile-first gaming culture enabled by affordable smartphones, low data tariffs, and accessible competitive formats.

- By Region: North India dominates the market with a share of 30% in 2025, driven by expanding viewership, the growing amateur participation, and increasing digital infrastructure development across major metropolitan areas.

- Key Players: The India esports market features an increasingly competitive landscape with domestic tournament organizers, international publishers, streaming platforms, and professional esports teams vying for viewership, sponsorship revenue, and content creation dominance.

To get more information on this market Request Sample

The India esports market is growing due to widespread smartphone adoption, affordable data access, and a young population increasingly drawn to competitive digital entertainment. The rise of organized leagues, campus tournaments, and creator-driven events is strengthening participation and building structured pathways for emerging talent. Sponsorship activity and diversified monetization models are improving financial sustainability for teams, platforms, and tournament organizers. Streaming growth and improved production standards are also enhancing audience engagement and mainstream acceptance. Media companies are beginning to view esports as a strategic extension of digital outreach, as reflected in 2025 when Zee Media Corporation Limited launched the “Zee Media Gaming Tournament: Arena of Champions” with a ₹10 lakh prize pool to connect with Gen Z and millennial viewers. Continued investment in dedicated arenas, professional team ecosystems, and supportive industry formalization is expected to reinforce long-term growth across India’s esports landscape.

India Esports Market Trends:

Localization of Global Esports Experience Standards

A major trend influencing the India esports market is the growing entry of global production and fan engagement firms aiming to enhance event quality and audience experiences. As competitive gaming becomes more organized, there is a rise in the demand for professionally delivered tournaments, immersive live formats, and integrated brand partnerships aligned with individual preferences in India. This development was evident in 2025 when OS Studios established operations in Bengaluru, New Delhi, and Mumbai to address the “experience gap” in the domestic gaming sector. Through its Fan Z Operating System and international expertise, the company reflects the broader shift toward global standards shaping India’s evolving esports ecosystem.

Rise of Creator-Led Competitive Esports Events

The growing influence of digital creators is reshaping India’s esports landscape by blending competitive gaming with entertainment and community engagement. Creator-led tournaments attract large fan bases while offering aspiring players accessible entry points into organized competition. This direction gained prominence in 2025 when JioBLAST introduced “JioBLAST ALL STARS vs India” at GamingCon Bharat, incorporating open qualifiers alongside creator participation to connect grassroots talent with established personalities. Such initiatives highlight the incrasing role of influencers as central figures in event promotion, audience retention, and brand collaboration, expanding esports beyond conventional league-based formats into more interactive and creator-centric ecosystems.

Expansion of Campus-Centric Esports Ecosystems

The institutionalization of collegiate esports is emerging as a significant development in India’s competitive gaming ecosystem, reinforcing grassroots talent cultivation and structured competition pathways. Universities are increasingly organizing formal tournaments and campus leagues to engage student gamers and provide clear progression routes into professional circuits. This trend was strengthened in 2025 with the launch of the UniPin Campus Championship India, conducted across eight cities with offline rounds leading to a national finale. Such initiatives underscore the growing recognition of academic institutions as foundational pillars of the esports ecosystem, supporting early talent identification and long-term industry sustainability.

Market Outlook 2026-2034:

The India esports market revenue demonstrates exceptional growth potential throughout the forecast period, underpinned by favorable demographics, expanding digital infrastructure, and the growing institutional recognition. The market generated a revenue of USD 239.13 Million in 2025 and is projected to reach a revenue of USD 1,092.14 Million by 2034, growing at a compound annual growth rate of 18.38% from 2026-2034. Rising sponsorship investments, mobile gaming proliferation across underserved regions, professionalization of tournament structures, and increasing international participation of Indian esports organizations are expected to sustain robust revenue growth throughout the forecast horizon.

India Esports Market Report Segmentation:

|

Segment Category |

Leading Segment |

Market Share |

|

Revenue Source |

Sponsorship |

32% |

|

Games |

Multiplayer Online Battle Arena (MOBA) |

28% |

|

Platform |

Mobile and Tablets |

45% |

|

Region |

North India |

30% |

Revenue Source Insights:

- Advertising

- Media Rights

- Merchandise and Tickets

- Publisher Fees

- Sponsorship

Sponsorship dominates with a market share of 32% of the total India esports market in 2025.

Sponsorship represents the largest segment owing to the growing interest of brands in reaching young, digitally engaged audiences. Esports events attract high viewership across streaming platforms, offering strong visibility and targeted marketing opportunities. Companies invest in team partnerships, tournament branding, and influencer collaborations to enhance brand recall. The expanding fan base and rising popularity of competitive gaming create attractive promotional channels. As a result, sponsorship agreements contribute the largest share of revenue within India’s evolving esports ecosystem.

Another reason for sponsorship dominance is the scalable nature of esports content and events. Brands can integrate seamlessly through event naming rights, team partnerships, and in-stream advertising, while also benefiting from measurable audience engagement. Corporate participation continues to expand across technology and consumer sectors, reinforcing funding inflows. This trend was highlighted in 2025 when Samsung became the title sponsor for College Rivals Season 3 with Ampverse DMI, integrating the Galaxy S25 Ultra into match play and event content. Such partnerships strengthen esports’ financial foundation.

Games Insights:

Access the comprehensive market breakdown Request Sample

- Multiplayer Online Battle Arena (MOBA)

- Player Vs. Player (PvP)

- First Person Shooters (FPS)

- Real Time Strategy (RTS)

Multiplayer online battle arena (MOBA) leads with a market share of 28% of the total India esports market in 2025.

Multiplayer online battle arena (MOBA) dominates the market due to its highly competitive structure and strong player engagement. This game emphasizes teamwork, strategy, and fast paced gameplay, making it attractive for both casual players and professional tournaments. MOBA titles support large online communities and regular competitive events, which drive consistent participation. Its accessibility on mobile platforms further increases popularity in India, where smartphone gaming dominates the esports landscape and encourages widespread adoption.

Another factor behind MOBA dominance is the strong spectator appeal and streaming potential of this genre. The format’s team-based gameplay and structured ranking systems sustain long-term player interest while attracting sponsors seeking consistent viewership. Tournament organizers frequently prioritize this genre because of its competitive intensity and audience retention. This growing shift toward strategy-driven esports was evident in 2025 when prominent Indian gaming creators Rai Star and Gyan Gaming entered the MOBA segment through MOBA Legends 5v5, reinforcing the genre’s rising prominence in the competitive landscape.

Platform Insights:

- PC-Based Esports

- Consoles-Based Esports

- Mobile and Tablets

Mobile and tablets exhibit a clear dominance with a 45% share of the total India esports market in 2025.

Mobile and tablets lead the market attributed to their widespread accessibility and affordability. A large share of India’s population relies on smartphones as the primary device for digital entertainment, making mobile gaming the most convenient entry point into esports. Affordable data plans and expanding 4G and 5G coverage support smooth online gameplay and competitive participation. Mobile platforms also offer a wide range of popular multiplayer titles, encouraging mass adoption and sustained engagement across diverse user groups.

Another reason for the dominance of mobile and tablets is the low barrier to entry compared to console or PC gaming. Players can easily join tournaments, stream content, and participate in competitive events without investing in expensive hardware. Game developers and esports organizers focus heavily on mobile based leagues due to the larger user base. The integration of in game purchases, digital wallets, and streaming platforms further strengthens monetization. As mobile technology improves, mobile esports continue to hold the largest market share in India.

Regional Insights:

- North India

- West and Central India

- South India

- East India

North India dominates with a market share of 30% of the total India esports market in 2025.

North India holds the biggest market share driven by its large youth population, strong internet penetration, and the growing gaming culture in urban centers. The region is witnessing rapid expansion in competitive gaming communities, supported by increasing smartphone usage and affordable data access. Major cities provide better connectivity, gaming cafés, and organized tournament ecosystems that encourage participation. Rising interest in digital entertainment and multiplayer gaming further boosts regional demand, making North India a key contributor to India’s esports growth.

Another factor supporting North India’s dominance is the increasing presence of esports organizations, event organizers, and sponsorship activity. The region hosts a growing number of gaming influencers and content creators who attract large audiences and promote competitive gaming. Educational institutions and private platforms are also supporting esports through leagues and structured competitions. For instance, in 2026, Times Network and Digit announced the grand finale of the SKOAR! College Cup – Delhi Edition 2025, billed as India’s largest college esports tournament. The two-day LAN event, scheduled for Feb 19–20 at Bennett University, Greater Noida, will feature student teams competing in BGMI and Valorant for a Rs 30 lakh prize pool, with participation from over 200 colleges and 2,000+ teams, highlighting the rapid rise of campus esports in India.

Market Dynamics:

Growth Drivers:

Why is the India Esports Market Growing?

Rising Smartphone Penetration and Affordable Internet Access

The rapid adoption of smartphones and widespread availability of affordable high-speed internet are fundamental drivers of India esports market expansion. Improved network infrastructure and lower data costs have enabled seamless multiplayer gaming and real-time tournament participation across both urban and rural regions. Access to increasingly powerful mobile devices has broadened the competitive player base without requiring high-cost hardware investments. This digital penetration is underscored by the 2025 Comprehensive Modular Survey: Telecom, which reported smartphone ownership among youth aged 15–29 at 95.5% in rural areas and 97.6% in urban centers. Such connectivity levels continue to support steady growth in esports participation and viewership nationwide.

Youth Demographics and Changing Entertainment Preferences

India’s large youth population and shifting entertainment preferences are influencing the market, as younger audiences increasingly prioritize interactive digital experiences over traditional media. Competitive gaming provides social connectivity, skill development, and peer recognition, strengthening its appeal among digitally engaged demographics. This demographic advantage is reflected in National Youth Policy estimates, which define youth as individuals aged 15 to 29 and reported India’s youth population at approximately 420 million in 2024, representing nearly 29% of the total population. As cultural acceptance improves and professional opportunities become more visible, these youth-driven dynamics continue to generate sustained demand for esports platforms, tournaments, and organized competitive ecosystems nationwide.

Development of Dedicated Esports Arenas and Physical Infrastructure

The development of specialized esports arenas marks a significant evolution in India’s competitive gaming ecosystem, reflecting the growing investment in structured physical infrastructure. Purpose-built venues equipped with high-performance gaming systems, professional streaming setups, and dedicated tournament zones are strengthening both player development and audience engagement. In 2025, CyberPowerPC partnered with Orangutan to equip the ApeCity esports arena in Navi Mumbai with advanced hardware and integrated event spaces, reinforcing this transition toward professional-grade facilities. Such arena-based environments enhance training quality, host large-scale competitions, and foster community interaction, contributing to higher competitive standards and long-term industry maturity across India’s esports landscape.

Market Restraints:

What Challenges the India Esports Market is Facing?

Regulatory Uncertainty and Fragmented State-Level Policies

The Indian esports market faces regulatory complexity as various states implement differing laws regarding online gaming and competitive esports. Inconsistent policy frameworks across state jurisdictions create operational challenges for tournament organizers and discourage investment, as businesses must navigate a fragmented legal landscape that introduces compliance costs and uncertainty for stakeholders.

Digital Infrastructure Limitations in Rural and Semi-Urban Areas

Despite steady progress in internet access across India, rural and semi-urban regions still face major digital infrastructure gaps that limit esports expansion. Many areas continue to experience unreliable broadband connectivity, slower mobile data speeds, and frequent network disruptions. These challenges reduce the quality of online gameplay and restrict participation in competitive tournaments.

Monetization Constraints and Revenue Sustainability Challenges

Generating sustainable revenue remains a fundamental challenge for the India esports ecosystem, particularly for emerging tournament organizers and professional teams. Limited advertising yields, relatively nascent media rights valuations, and constrained merchandise revenue streams compared to traditional sports create financial pressures that affect long-term viability and investment attractiveness for industry stakeholders.

Competitive Landscape:

The India esports market features an increasingly dynamic competitive landscape characterized by the presence of domestic tournament organizers, international game publishers, professional esports teams, and digital streaming platforms competing for viewership, sponsorship revenue, and content dominance. Market dynamics reflect strategic positioning across mobile-first competitive formats and emerging PC-based tournament ecosystems. Competition is driven by investments in intellectual property development, regional tournament infrastructure, content creator partnerships, and international market expansion. The landscape is evolving rapidly as organizations diversify revenue streams through media rights acquisitions, brand-funded prize pools, and broadcast partnerships while investing in grassroots talent development and collegiate esports programs to sustain long-term competitive growth.

Recent Developments:

- February 2026: Ant Esports announced the launch of its Influencer Program to support emerging gaming and tech creators across India. The initiative offers a structured platform for collaborations through product reviews, content integrations, and community campaigns, with perks like early product access, merchandise, and event invitations.

- February 2026: The Indian Institute of Creative Technologies (IICT), Mumbai hosted the first IICT Esports Premier League (IEPL) to promote esports as part of India’s growing Orange Economy. The event aligned with the Union Budget’s ₹250 crore push for AVGC talent development, including plans for creator labs in thousands of schools and colleges. Supported by major industry partners, IEPL drew over 1,000 students and is set to become an annual platform linking gaming, education, and future digital careers.

India Esports Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Revenue Sources Covered | Advertising, Media Rights, Merchandise and Tickets, Publisher Fees, Sponsorship |

| Games Covered | Multiplayer Online Battle Arena (MOBA), Player Vs. Player (PvP), First Person Shooters (FPS), Real Time Strategy (RTS) |

| Platforms Covered | PC-Based Esports, Consoles-Based Esports, Mobile and Tablets |

| Region Covered | North India, West and Central India, South India, East India |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the India Esports Market Report

The India esports market size was valued at USD 239.13 Million in 2025.

The India esports market is expected to grow at a compound annual growth rate of 18.38% from 2026-2034 to reach USD 1,092.14 Million by 2034.

Sponsorship holds the largest revenue share of 32% in 2025, driven by increasing brand investment in competitive gaming partnerships, tournament title sponsorships, team affiliations, and content creator collaborations targeting India's digitally engaged youth population.

Key factors driving the India esports market include the growing institutionalization of collegiate competitions, exemplified by the 2025 UniPin Campus Championship India held across eight cities, which strengthens grassroots talent development and structured pathways into professional competitive gaming.

Major challenges include regulatory uncertainty and fragmented state-level policies, digital infrastructure limitations in rural and semi-urban areas, monetization constraints affecting revenue sustainability, and limited standardized frameworks for player development and career progression in competitive gaming.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)