India Freight Forwarding Market Size, Share, Trends and Forecast by Mode of Transport, Customer Type, Service, Application, and Region, 2026-2034

India Freight Forwarding Market Size, Share, Trends & Forecast (2026-2034)

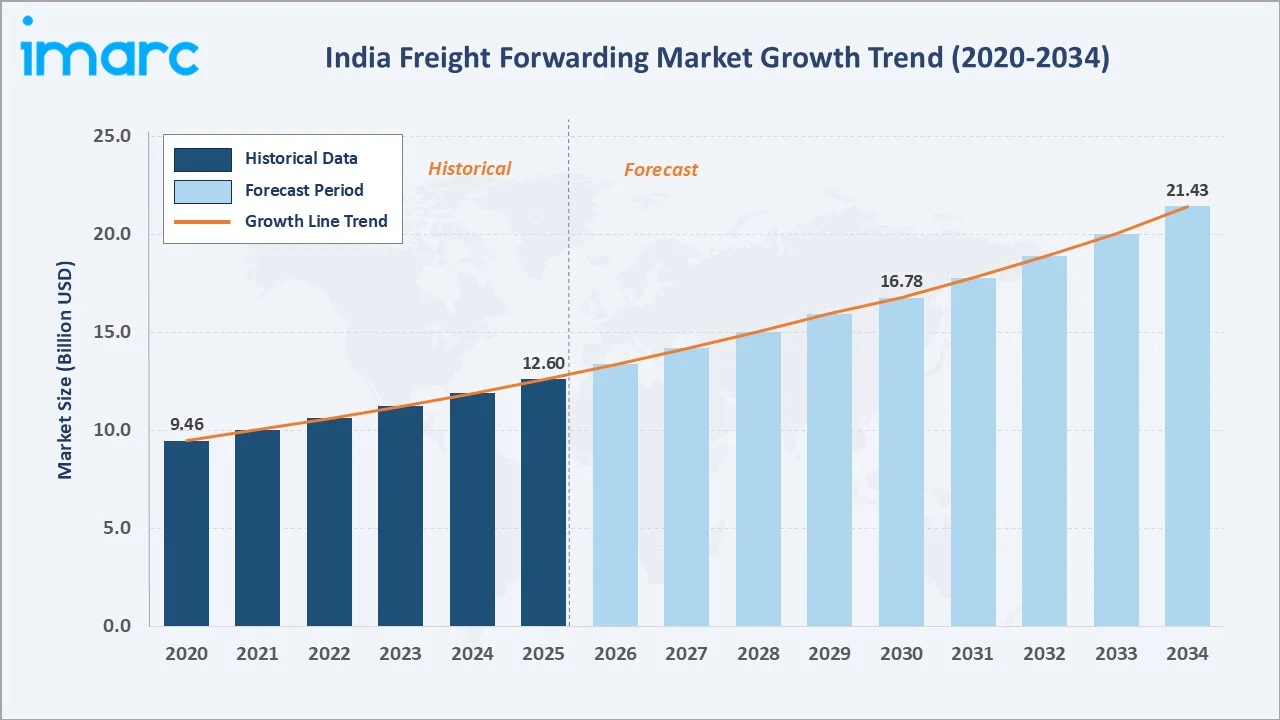

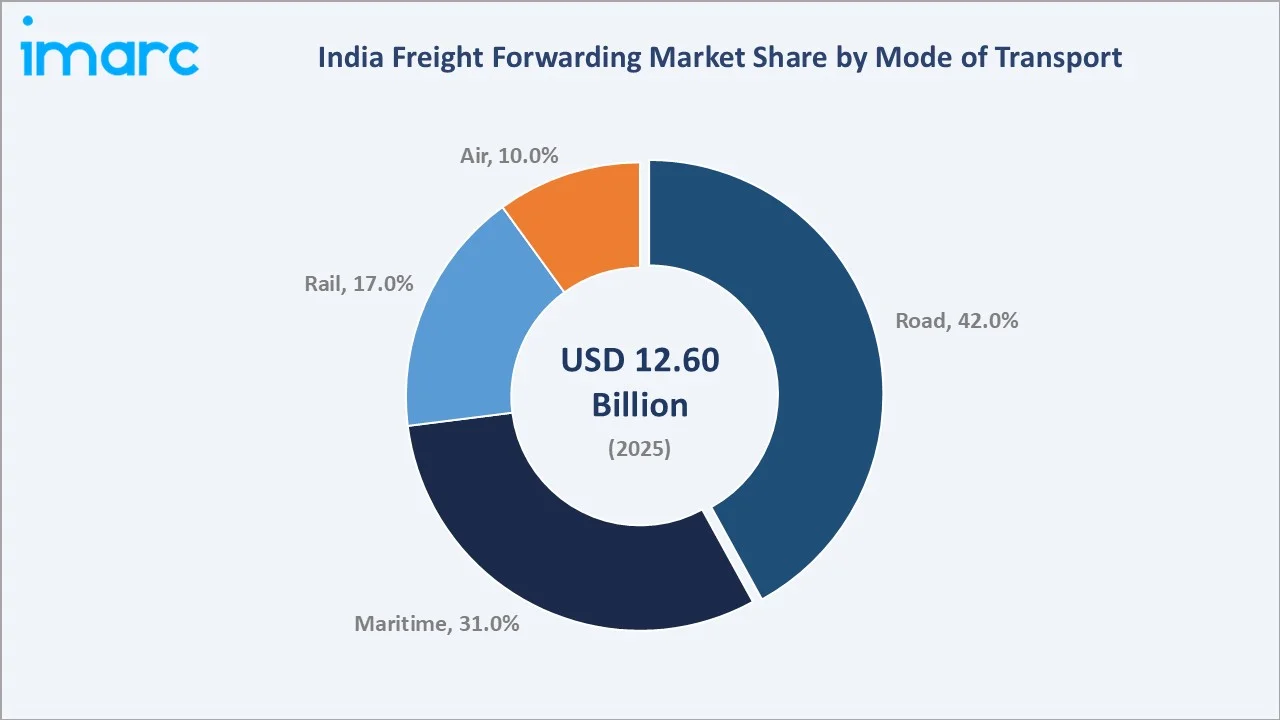

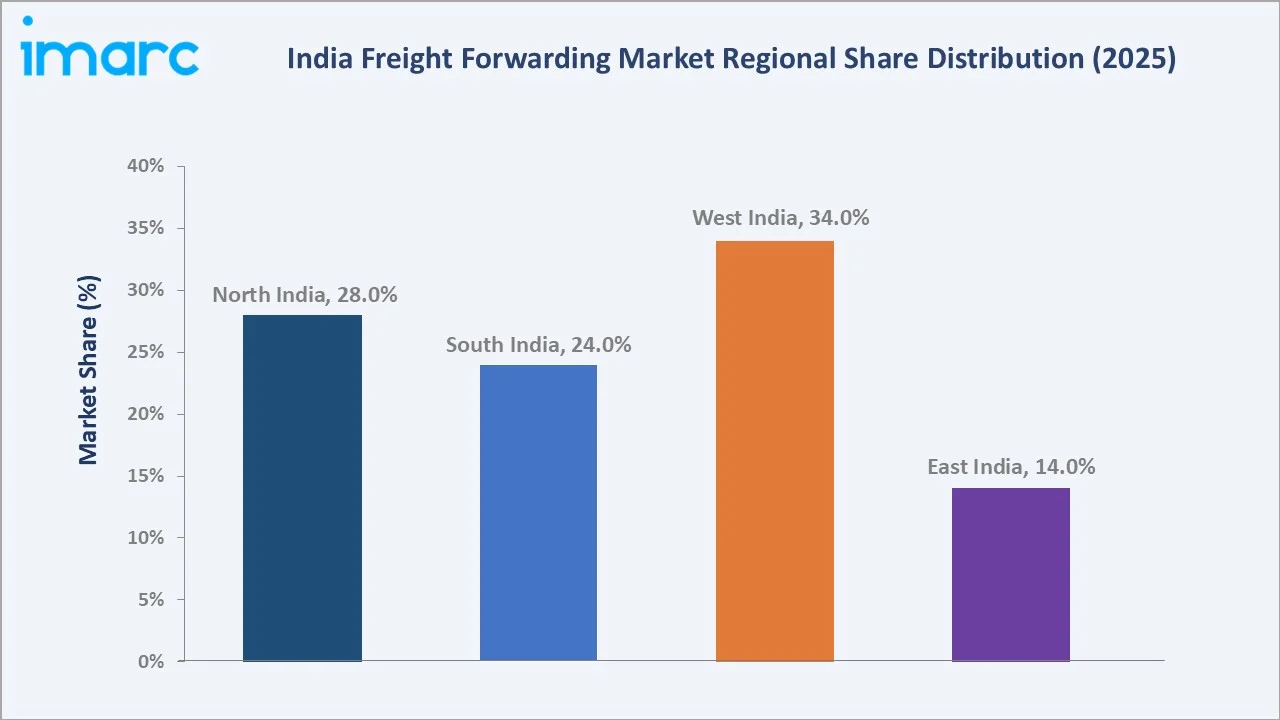

The India freight forwarding market reached USD 12.60 Billion in 2025 and is projected to reach USD 21.43 Billion by 2034, growing at a CAGR of 5.90% during 2026-2034. Market expansion is driven by rapid e-commerce growth, government infrastructure push through Dedicated Freight Corridors (DFCs), and the Make in India and PLI schemes accelerating manufacturing exports. India's container port throughput crossed 20 million TEUs in 2024, reflecting rising trade volumes. Road freight leads at 42.0%, followed by Maritime at 31.0%, Rail at 17.0%, and Air at 10.0%. B2B customers represent 78.0% of market demand. West India commands 34.0% of the national market.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 12.60 Billion |

|

Forecast Market Size (2034) |

USD 21.43 Billion |

|

CAGR (2026-2034) |

5.90% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Dominant Mode |

Road (42.0%, 2025) |

|

Dominant Customer Type |

B2B (78.0%, 2025) |

|

Leading Region |

West India (34.0%, 2025) |

India freight forwarding market expanded from USD 9.46 Billion in 2020 to USD 12.60 Billion in 2025, anchored at USD 16.78 Billion in 2030, and forecast to reach USD 21.43 Billion by 2034. The market is commercially supported by India's position as the world's fastest-growing major economy, ongoing port and DFC infrastructure development, and the government's Sagarmala Programme connecting industrial clusters to ports. India's logistics sector contributes approximately 8% of GDP, and the National Logistics Policy 2022 targets reducing logistics costs from 13% to 8% of GDP, directly driving freight forwarding demand growth.

To get more information on this market, Request Sample

Air freight forwarding, though the smallest mode at 10.0%, registers the fastest segment growth driven by pharmaceutical exports, time-sensitive e-commerce shipments, and India's expanding air cargo infrastructure. Maritime freight benefits from Sagarmala's 200+ port modernisation projects, while rail freight is being transformed by the Eastern and Western DFCs.

Executive Summary

India freight forwarding market at USD 12.60 Billion in 2025 is one of South Asia's largest logistics markets by value, reflecting the country's rising manufacturing capacity, growing international trade, and strategic government support for logistics infrastructure modernisation. The market is projected to reach USD 21.43 Billion by 2034, delivering a CAGR of 5.90% over the forecast period. India's emergence as a global manufacturing hub under the Production Linked Incentive (PLI) scheme covering 14 key sectors is structurally increasing freight volumes across road, rail, maritime, and air modes.

Road freight dominates at 42.0%, supported by an extensive national highway network and broad-based last-mile connectivity across India's industrial heartland. Maritime freight at 31.0% is benefiting from India's USD 82 Billion Sagarmala Programme and the addition of new cargo berths at major ports between 2021 and 2025. Rail freight, at 17.0%, is being transformed by the 2,843 km Eastern and Western Dedicated Freight Corridors that reduced transit times by up to 40% for containerised cargo as of 2025. Air freight at 10.0%, while smallest in share, is growing fastest due to rising pharma exports and e-commerce demand for time-definite delivery.

B2B customers dominate at 78.0% through large manufacturing, retail, and industrial clients requiring regular freight forwarding contracts, customs management, and multimodal coordination. West India leads regionally at 34.0% through Mumbai's status as India's largest port gateway and Nhava Sheva's role as the busiest container port. The competitive landscape is consolidating through major players such as DHL Group, Kuehne+Nagel International AG, CMA CGM Group, Delhivery Limited, and A.P. Moller – Maersk, strengthening India operations alongside domestic specialists.

Key Market Insights

|

Insight |

Data |

|

Dominant Mode |

Road - 42.0% share (2025) |

|

Dominant Customer Type |

B2B - 78.0% market share (2025) |

|

Leading Region |

West India - 34.0% share (2025) |

|

Fastest Growing Mode |

Air Freight (~8.1% CAGR, 2026-2034) |

|

Market Opportunity |

DFC-driven rail modal shift; pharma cold-chain logistics; e-commerce last-mile expansion; digital freight platform investment |

Key Analytical Observations Supporting The Above Data:

- Road at 42.0%: Road freight dominates due to India's 1.45 lakh km national highway network providing last-mile access to industrial zones, manufacturing clusters, and tier-2 cities unreachable by rail or maritime modes. Trucking industry employs over 7 million people and supports everyday domestic and cross-border freight movement.

- B2B at 78.0%: B2B customers dominate because large manufacturers, retailers, and exporters require contractual freight forwarding, multimodal coordination, customs clearance, and documentation services that form the core offering of organised freight forwarders in India.

- West India at 34.0%: West India leads due to Mumbai and JNPA's role as India's primary container gateway handling over 50% of India's container traffic, alongside Gujarat's Mundra Port and Kandla Port driving export-driven freight volumes.

- Air Freight growing fastest: Pharmaceutical exports worth USD 30.47 Billion in FY2024-25, perishable agri-exports, and same-day e-commerce are structurally increasing demand for air freight forwarding services at India's 24 international cargo-enabled airports.

- B2C expanding at 22.0%: D2C brands, cross-border e-commerce exports, and growing consumer imports through courier-mode shipments are driving B2C freight forwarding demand, with India's e-commerce market projected to reach USD 345 Billion by 2030.

India Freight Forwarding Market Overview

India freight forwarding market is the structured ecosystem of logistics intermediaries that coordinate the movement of goods across domestic and international corridors via road, rail, maritime, and air modes. Freight forwarders act as intermediaries between shippers and carriers, managing customs documentation, cargo consolidation, route optimisation, warehousing, and last-mile delivery. India's freight forwarding ecosystem integrates global 3PL providers, domestic logistics specialists, customs house agents, port-based freight handlers, and digital freight platforms. The market's commercial structure is shaped by India's merchandise trade, government infrastructure programmes, and the National Logistics Policy 2022 targeting logistics cost reduction to 8% of GDP.

Market Dynamics

To evaluate market opportunities, Request Sample

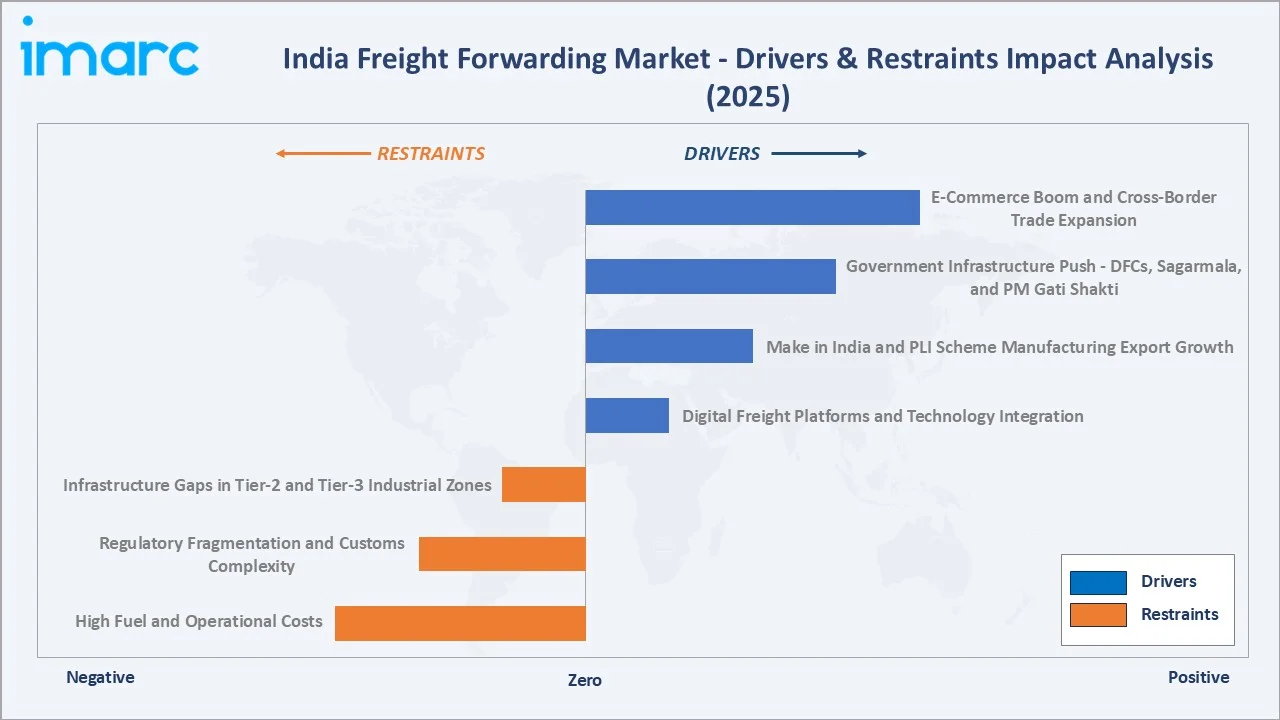

Market Drivers

- E-Commerce Boom and Cross-Border Trade Expansion: India's e-commerce market grew at 19-21% in 2025, driving demand for express freight, last-mile delivery, and international parcel forwarding. Cross-border e-commerce exports are expanding through Flipkart, Meesho, and global platforms. India's merchandise exports reached USD 400+ Billion in FY2025, requiring scalable freight forwarding services for documentation, customs, and multimodal routing across 15 major export product categories.

- Government Infrastructure Push - DFCs, Sagarmala, and PM Gati Shakti: The Eastern and Western Dedicated Freight Corridors reduced transit time for containerised rail cargo by up to 40% and logistics costs by 20-30% on key corridors. The Sagarmala Programme is modernising 200 port projects and activating 30+ inland waterway routes. PM Gati Shakti National Master Plan integrates 16 ministries to eliminate infrastructure bottlenecks. The Ministry of Ports, Shipping and Waterways reported 15% growth in major port cargo volumes in FY2024-25.

- Make in India and PLI Scheme Manufacturing Export Growth: PLI schemes across 14 sectors including mobile phones, pharmaceuticals, textiles, and auto components are creating structural demand for outbound freight forwarding. India's mobile phone exports reached USD 30+ Billion in FY2025. Pharmaceutical exports from India, the world's largest generic drug supplier, exceeded USD 30.4 Billion in FY2025, requiring specialised temperature-controlled air freight forwarding.

- Digital Freight Platforms and Technology Integration: AI-driven route optimisation, blockchain-based documentation, and real-time cargo tracking are improving freight forwarder efficiency and client satisfaction. Container Corporation of India (CONCOR) integrated its rail moves with FOIS (Freight Operations Information System) giving exporters real-time box tracking at 60 inland depots. Mandatory FASTag tolling generates 1.2 billion road data points monthly, enabling load-matching and reducing empty truck trips.

Market Restraints

- Infrastructure Gaps in Tier-2 and Tier-3 Industrial Zones: Despite national highway expansion, last-mile connectivity to industrial clusters in tier-2 cities remains constrained by inadequate road quality, insufficient warehousing, and limited cold-chain infrastructure. Multi-modal logistics parks, while increasing, remain concentrated in tier-1 hubs.

- Regulatory Fragmentation and Customs Complexity: India's multi-state tax compliance environment, varying state-level entry taxes, and complex customs documentation requirements increase operational friction for freight forwarders. Despite GST simplification, compliance costs for cross-border clearance remain above peer markets.

- High Fuel and Operational Costs: Diesel prices directly affect road freight rates, which constitute 42% of freight volumes. India's high fuel taxes and logistics cost structure at 8-13% of GDP (National Logistics Policy 2022 targets) versus 6-8% in developed markets constrains margin growth for freight forwarders.

Market Opportunities

- Pharmaceutical and Cold-Chain Freight Forwarding: India's pharma export growth and domestic cold-chain demand create opportunities for specialised freight forwarders. The cold-chain logistics market is growing at 15-20% CAGR per NCCD. Government’s Vision 2047 targets 50,000 km temperature-controlled expressways and high-speed corridors.

- Multimodal Integration and Rail Freight Modal Shift: DFC-driven rail freight reliability is enabling modal shift from road to rail for bulk and containerised cargo over 500 km routes, creating new multimodal freight forwarding opportunities. CONCOR's 60 inland container depots and expanding private freight terminal network support intermodal growth.

Market Challenges

- Port Congestion and Vessel Turnaround Delays: Major ports including JNPA experience periodic congestion affecting maritime freight forwarder reliability and costs. JNPA vessel turnaround averaged 1.1 days in 2024, above Singapore's 0.6 days benchmark, impacting time-definite export commitments.

- Talent Shortage in Specialised Logistics and Customs Operations: India's freight forwarding sector faces skilled talent shortages in customs compliance, multimodal coordination, and digital logistics management, increasing operational costs and limiting scalability for mid-size forwarders.

Emerging Market Trends

1. Digital Freight Platforms and AI-Driven Route Optimisation

Digital freight platforms are transforming how shippers book, track, and manage cargo across India's multimodal freight network. AI-powered route optimisation reduces empty miles and improves asset utilisation. In May 2025, ADRA India signed an MoU with DHL Group to boost emergency relief logistics effectiveness across India, with DHL providing free logistics support including handling, sorting, and inventory management at key airport entry points. Technology adoption is accelerating across both global 3PLs and domestic freight specialists.

2. Dedicated Freight Corridor-Driven Rail Modal Shift

The Eastern and Western Dedicated Freight Corridors are structurally shifting cargo from road to rail on India's highest-volume trade corridors. Cargo transported via DFC railways has 64-80% lower carbon emissions than road-equivalent routes. Freight forwarders are developing integrated rail-road multimodal products to capture DFC benefits, with CONCOR recording 10-12% volume growth on DFC-connected routes in 2024-25.

3. Pharmaceutical and Healthcare Specialised Logistics Growth

Rising pharma export volumes require temperature-controlled, GDP-compliant air and surface freight forwarding. In April 2025, a new 90,000 sq ft frozen warehouse opened in Detroj, Gujarat, dedicated to pharmaceutical cold-chain needs, reflecting growing infrastructure investment in specialised freight. India's pharmaceutical logistics segment is growing at 18-20% annually, well above the market average, creating premium-margin opportunities for specialised forwarders.

4. E-Commerce Cross-Border Export Forwarding

India's D2C and e-commerce brands are expanding international exports through courier-mode and air freight forwarding. The government's e-commerce export hub scheme and RBI's enhanced e-commerce export limits are enabling more SME exporters to access organised freight forwarding. Cross-border e-commerce volumes from India grew over 40% in FY2025, creating structured demand for international parcel forwarding, customs clearance, and last-mile overseas delivery partnerships.

5. Green Logistics and ESG-Driven Supply Chain Decarbonisation

Global shipper ESG commitments are driving demand for low-carbon freight forwarding solutions. DFC rail mode's 65% lower carbon footprint versus road is being actively marketed by freight forwarders to multinational shippers with Scope 3 emission reduction targets. Electric vehicle-based urban last-mile delivery by logistics firms including Blue Dart and Delhivery is also growing.

Industry Value Chain Analysis

India freight forwarding value chain integrates cargo origin, freight booking, customs and documentation, multimodal transport and transit, port and hub operations, and last-mile delivery to the consignee. Freight forwarders operate as value-adding intermediaries across all stages, consolidating cargo, managing regulatory compliance, and coordinating carriers across modes. The value chain's commercial structure enables both asset-heavy and asset-light freight forwarding models, with global players maintaining owned fleets while domestic specialists leverage carrier partnerships.

|

Stage |

Key Participants |

|

Cargo Origin & Shippers |

Exporters, manufacturers, retailers, and trading companies generating freight demand across industrial zones and SEZs |

|

Freight Booking & Planning |

Freight forwarders, customs house agents, and digital freight platforms managing cargo booking, documentation, and route planning |

|

Customs & Compliance |

Customs house agents, DGFT-licensed exporters, and compliance teams managing import-export documentation, duty payments, and regulatory clearances |

|

Transport & Transit |

Road carriers, CONCOR/DFC rail operators, shipping lines, and airlines transporting cargo across domestic and international corridors |

|

Port & Hub Operations |

Port Trust authorities, private terminal operators, inland container depots, air cargo terminals managing cargo handling and consolidation |

|

Warehousing & 3PL |

Third-party logistics providers, bonded warehouses, and multi-modal logistics parks providing storage, consolidation, and value-added services |

Customs and compliance represent the freight forwarding value chain's most commercially consequential regulatory stage, where documentation errors create costly delays. India's SWIFT 2.0 (Single Window Interface for Facilitating Trade) system processed over various customs clearances per month,

Technology Landscape in the India Freight Forwarding Industry

Digital Freight Platforms and Booking Automation

Digital freight platforms are enabling real-time rate comparison, instant booking, and automated documentation for both international and domestic freight forwarding. These platforms reduce transaction costs, eliminate manual paperwork, and improve shipper-to-forwarder communication efficiency. Cloud-based freight management systems allow forwarders to manage multi-leg shipments, carrier coordination, and compliance tracking from centralised dashboards.

AI and Predictive Analytics for Route Optimisation

AI-driven route optimisation tools analyse traffic patterns, port congestion data, weather conditions, and carrier performance to recommend optimal routing. GPS-guided dispatch systems have reduced empty truck runs to 19% for leading carriers. Machine learning models improve demand forecasting and capacity allocation, reducing operational inefficiencies in multi-modal freight operations. Container Corporation of India's FOIS integration enables real-time container tracking at 60 inland depots.

Blockchain and IoT for Supply Chain Visibility

Blockchain-based documentation platforms are reducing bill of lading fraud and enabling faster letter of credit processing for export freight. IoT sensors provide real-time temperature, humidity, and location monitoring for pharmaceutical and perishable cargo. Blue Dart connected IoT trackers across its 18,000-vehicle fleet, cutting customer queries by 31%. Mandatory FASTag tolling generates 1.2 billion road data points monthly, enabling load-matching engines to curb empty miles.

Green Technology and Emission Tracking

Carbon footprint calculation tools are being integrated into freight management systems to help shippers track and report Scope 3 emissions from logistics. Electric vehicle fleets for urban last-mile delivery are growing, with Delhivery and Blue Dart deploying EVs across major metros. DFC rail's 65% lower carbon emissions per tonne-km versus road are being leveraged in ESG reporting by multinationals sourcing from India.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Mode of Transport |

Road |

42.0% |

2025 |

|

Customer Type |

B2B |

78.0% |

2025 |

|

Service |

🔒 |

🔒 |

2025 |

|

Application |

🔒 |

🔒 |

2025 |

|

Region |

West India |

34.0% |

2025 |

By Mode of Transport

Road leads at 42.0% (2025). India's national highway network of 1.45 lakh km supports road freight's dominance across all industrial and commercial freight corridors. Road freight serves both short-haul urban distribution and long-haul inter-state cargo movement, making it the most versatile mode across the freight forwarding value chain.

To access detailed market analysis, Request Sample

Maritime at 31.0% reflects India's growing export volumes through 12 major ports handling over 900 million tonnes in FY2025-26. Rail at 17.0% is growing at approximately 6.8% CAGR driven by DFC operational benefits, with containerised rail freight growing fastest. Air at 10.0% is the fastest-growing mode at approximately 8.1% CAGR through pharmaceutical, high-value, and time-sensitive cargo demand.

By Customer Type

B2B leads at 78.0% (2025). Large manufacturing companies, retail chains, and export-oriented enterprises requiring regular multimodal freight forwarding contracts represent the core of India's freight forwarding demand. B2B clients demand end-to-end customs management, documentation, and supply chain visibility that organised freight forwarders provide as core service offerings.

B2C at 22.0% is growing fastest through India's direct-to-consumer e-commerce exports, international parcel delivery growth, and rising consumer imports via courier-mode freight. Delhivery processed 752 million shipments delivered in FY25 with 2% YoY growth, reflecting B2C freight volume growth. The B2C segment is structurally expanding as more Indian SMEs access global markets through e-commerce platforms.

Regional Market Insights

|

Region |

Share (2025) |

Key India Freight Forwarding Market Drivers & Characteristics |

|

West India |

34.0% |

JNPA handles over 50% of India's container traffic; Mumbai Airport is one of the largest air cargo gateways; Gujarat's Mundra and Kandla ports drive export freight volumes; major petrochemical and manufacturing industrial clusters. |

|

North India |

28.0% |

Delhi-NCR's industrial and commercial hub status; Western DFC running through Rajasthan, Haryana, and UP improving rail freight; major road freight corridors linking North India to western ports; strong FMCG and automotive parts export flows. |

|

South India |

24.0% |

Chennai, Tuticorin, and Kochi ports handling automotive, electronics, and textile exports; Bengaluru and Hyderabad's technology manufacturing creating high-value air freight demand; strong pharma cluster in Hyderabad driving temperature-controlled freight. |

|

East India |

14.0% |

Kolkata Port Trust and Haldia Dock Complex serving Eastern India and landlocked Northeastern states; growing coal, steel, and agri-commodity freight from Jharkhand, Odisha, and West Bengal; Eastern DFC improving rail freight from the eastern industrial belt. |

West India's 34.0% market leadership reflects JNPA's role as India's premier container port, handling over 8 million TEUs annually, making it the commercial centre of India's maritime freight forwarding. Gujarat's Mundra Port (ADANI Ports), India's largest private port, adds further freight forwarding volume through petrochemical, automotive, and agri-commodity exports. Mumbai's Chhatrapati Shivaji Maharaj International Airport remains India's largest air cargo hub by value. North India's 28.0% is anchored by the Western DFC's operational efficiency improvements and Delhi's role as the largest EXIM trade centre by value.

South India's 24.0% reflects Hyderabad's pharmaceutical export cluster generating premium air freight demand, Chennai's automotive manufacturing feeding ocean freight to global markets, and Kochi's growing position as a transshipment hub. East India's 14.0% is the commercially developing region, with Eastern DFC connectivity improving from 2024 onwards, Haldia Dock expansion underway, and increasing manufacturing in the Odisha-Jharkhand industrial belt creating new freight forwarding demand.

Competitive Landscape

India freight forwarding competitive landscape is highly fragmented at the domestic level with over 3,000 active freight forwarding companies, while the top-tier global players - DHL Group, Kuehne+Nagel International AG, CMA CGM Group, Delhivery Limited, and A.P. Moller - Maersk - command an estimated 40-45% of the organised market by revenue. Competition is shifting from rate-based competition to reliability, real-time tracking, multimodal agility, and customs compliance as the primary differentiators for enterprise B2B clients.

|

Company |

Key Brands / Divisions |

Market Position |

Core Strength |

|

DHL Group |

DHL Global Forwarding |

Market Leader |

World's largest logistics company with full-service freight forwarding, IoT tracking, and pharma-certified air freight capabilities. |

|

Kuehne+Nagel International AG |

Kuehne+Nagel Private Limited |

Strong Challenger |

Provides logistical services to nearly 400,000 customers worldwide with strong India sea and air freight forwarding operations. |

|

CMA CGM Group |

CEVA Logistics India |

Innovator |

Operates CEVA Logistics; dedicated ocean and air freight routes; advanced contract logistics and local fulfilment. |

|

Delhivery Limited |

Delhivery |

Innovator |

Strong technology platform for domestic express and cross-border freight forwarding. |

|

A.P. Moller - Maersk |

Maersk |

Strong Challenger |

End-to-end logistics solutions covering ocean freight, air freight, inland transportation, and customs clearance; strong international presence and advanced digital tools for export-oriented clients. |

The competitive landscape's most commercially significant dynamic is digital differentiation - global players investing in AI-driven freight platforms, blockchain documentation, and IoT cargo visibility are creating competitive moats against fragmented domestic forwarders.

Key Company Profiles

DHL Group

DHL Group is the world's leading logistics company and one of India's dominant freight forwarding players through DHL Global Forwarding.

- Key Division: DHL Global Forwarding (international air and ocean freight)

- Recent Developments: In May 2025, ADRA India signed an MoU with DHL Group to boost emergency relief logistics, with DHL providing free logistics support including cargo handling, sorting, inventory management, and temporary storage at airport entry points across India.

- Strategic Focus: Expanding pharmaceutical-certified air freight forwarding, deploying 4,000+ EVs for urban last-mile delivery, and investing in digital freight platforms to deepen enterprise client relationships across India's major industrial corridors.

Kuehne+Nagel International AG

Kuehne+Nagel International AG is a global logistics company founded in 1890 and headquartered in Switzerland, providing logistical services to nearly 400,000 customers worldwide with a significant India operation.

- Key Division: Kuehne+Nagel India Logistics Solutions

- Recent Developments: In February 2026, Kuehne+Nagel opened a built-to-suit 3,500 sqm Container Freight Station (CFS) in Mumbai to strengthen the sea logistics capabilities in India and supports the country’s expanding trade ecosystem.

- Strategic Focus: Leveraging global network scale to support India's manufacturing exporters with end-to-end multimodal freight management, customs clearance, and supply chain visibility solutions.

Market Concentration Analysis

India freight forwarding market is highly fragmented at the aggregate level with over 3,000 active freight forwarding companies, yet commercially concentrated at the top-end with global players - DHL Group, Kuehne+Nagel International AG, CMA CGM Group, Delhivery Limited, and A.P. Moller - Maersk - commanding approximately 40-45% of the organised sector by revenue. The top 10 players collectively hold an estimated 55-60% of organised market revenue, with the remaining 40-45% distributed among hundreds of regional and local freight forwarders.

Market concentration is increasing through M&A activity. CEVA's 21-city India expansion reflects global players investing in scale and geographic reach. Delhivery, India's largest domestic logistics company by market cap, represents the most credible large-scale domestic challenger to global players in B2C and SME freight forwarding.

Fragmentation in the domestic freight forwarding market creates pricing pressure in commodity road and ocean forwarding, while specialised segments (pharma, cold-chain, project cargo) support premium margins. The National Logistics Policy 2022's formalisation push is gradually reducing the share of unorganised, undocumented freight forwarding, benefiting organised players' market share growth.

Investment & Growth Opportunities

Highest Growth Segments

Air freight forwarding (~8.1% CAGR through pharmaceutical and e-commerce export growth), maritime freight (~7.2% CAGR through port modernisation and export volume growth), rail freight multimodal integration (~6.8% CAGR through DFC commercial ramp-up), cold-chain and pharma specialised logistics (~18-20% CAGR), digital freight platforms (~25-30% CAGR from a small base), and B2C cross-border e-commerce forwarding (~20-25% CAGR) represent India's highest-growth freight forwarding investment vectors through 2034.

Emerging Investment Opportunities

India's pharmaceutical cold-chain air freight forwarding market, growing at 18-20% annually, represents the highest premium-margin opportunity in India's freight forwarding sector. The pharma cold-chain segment's growth is driven by India's USD 30+ Billion pharmaceutical export base, growing biosimilar and temperature-sensitive drug exports, and regulatory requirements for GDP-compliant air freight handling at dedicated pharma cargo terminals being developed at Hyderabad, Bangalore, and Mumbai airports.

Investment Themes

- Digital freight platform investment capturing India's technology-driven freight forwarding transition: India's freight forwarding sector is undergoing structural digitisation, with AI route optimisation, blockchain documentation, and IoT visibility becoming competitive table stakes. Investment in digital freight platforms serves as an infrastructure layer enabling both global players and domestic mid-market forwarders to scale efficiently.

- DFC-integrated rail-road multimodal freight terminals: Inland Container Depot and multimodal logistics park investments adjacent to DFC corridors represent infrastructure investment with structural demand support from the National Logistics Policy 2022. The government's PM Gati Shakti programme is coordinating 16 ministries to develop multi-modal logistics infrastructure across 35+ major industrial clusters.

- Cold-chain logistics infrastructure for pharmaceutical and agri-export forwarding: India's cold-chain logistics market is growing at 15-20% CAGR per NCCD, driven by pharmaceutical exports, processed food exports, and fresh agri-produce. GDP-compliant air cargo terminals and temperature-controlled road freight fleets represent investment opportunities with premium pricing power above commodity forwarding.

Future Market Outlook (2026-2034)

India freight forwarding market is projected to grow from USD 12.60 Billion in 2025 to USD 21.43 Billion by 2034, delivering a 5.90% CAGR over the forecast period. The market's anchor value of USD 16.78 Billion in 2030 represents a structural inflection point where DFC full operational ramp-up, National Logistics Policy cost reduction targets, and India's USD 1 Trillion merchandise export ambition by 2030 (Ministry of Commerce) converge to create a step-change in freight forwarding volumes and service quality requirements.

Three structural forces define India freight forwarding market growth through 2034: India's manufacturing export acceleration through PLI schemes creating structural demand for specialised multimodal freight forwarding; logistics infrastructure modernisation through DFCs, port expansion, and PM Gati Shakti reducing logistics costs and improving freight reliability; and digital technology adoption enabling scale and service quality improvements that support market formalisation and organised player revenue growth.

Air freight forwarding is expected to grow above market average at ~8.1% CAGR driven by pharmaceutical exports, high-value electronics, and e-commerce time-definite cargo. Maritime forwarding will benefit from Sagarmala's port capacity additions and India's growing manufacturing export base. Rail freight forwarding will transform through DFC commercial maturity, with containerised rail growing above 10% CAGR as forwarders develop integrated DFC multimodal products. Road freight will grow at a steady ~5.0-5.5% CAGR as highway infrastructure improves last-mile connectivity to industrial clusters.

Research Methodology

Primary Research

Primary research comprised structured interviews with India freight forwarding industry stakeholders, including logistics directors at large manufacturing exporters, senior management at global freight forwarding companies, customs house agents and DGFT compliance specialists, port operations managers at major Indian ports, and digital freight platform founders and technology providers. Consumer and shipper survey data from export-oriented enterprises across North, West, South, and East India industrial clusters were incorporated into the market size and segment share analysis.

Secondary Research

Secondary research encompassed Ministry of Ports, Shipping and Waterways annual reports, DGFT (Directorate General of Foreign Trade) export-import statistical data, Container Corporation of India (CONCOR) operational reports, CBIC (Central Board of Indirect Taxes and Customs) clearance time and volume data, National Logistics Policy 2022 documentation, Sagarmala Programme project updates, JNPA and Mundra Port annual traffic reports, company annual reports of listed logistics firms, and National Skill Development Corporation logistics sector data. Over 60 secondary sources were reviewed.

Forecasting Models

Market revenue forecasts were developed using a bottom-up model: India's merchandise and services trade volumes by corridor multiplied by average freight forwarding revenue per tonne, segmented by mode, customer type, and region. DFC operational ramp-up curves, port capacity addition timelines from Sagarmala, and PLI scheme manufacturing output projections were used as structural demand multipliers across forecast years.

India Freight Forwarding Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Mode of Transports Covered | Road, Maritime, Rail, Air |

| Customer Types Covered | B2B, B2C |

| Services Covered | Transportation and Warehousing, Value Added Services, Packaging, Others |

| Applications Covered | Retail and E-Commerce, Healthcare, Food and Beverages, Media and Entertainment, Industrial and Manufacturing, Oil and Gas, Others |

| Regions Covered | North India, South India, East India, West India |

| Companies Covered | DHL Group, Kuehne+Nagel International AG, CMA CGM Group, Delhivery Limited, A.P. Moller - Maersk, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the India freight forwarding market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the India freight forwarding market.

- Porter's Five Forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the India freight forwarding industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the India Freight Forwarding Market Report

India freight forwarding market reached USD 12.60 Billion in 2025. Growth is driven by rising export volumes, DFC infrastructure, e-commerce expansion, and government initiatives including the Make in India scheme and National Logistics Policy 2022 targeting logistics cost reduction.

India freight forwarding market grows at 5.90% CAGR during 2026-2034, reaching USD 21.43 Billion by 2034. Growth is sustained by PLI manufacturing exports, port modernisation, DFC operational maturity, and digital freight platform adoption across organised and mid-market forwarders.

Road leads at 42.0% through India's 1.45 lakh km national highway network supporting domestic and cross-border freight across manufacturing clusters, retail distribution, and last-mile connectivity to tier-2 and tier-3 industrial zones.

B2B leads at 78.0% through large manufacturers, exporters, and retail chains requiring contractual multimodal freight forwarding, customs management, documentation services, and supply chain visibility that organised freight forwarders provide.

West India leads at 34.0% through JNPA's 50% share of India's container traffic, Mumbai Airport as one of the largest air cargo hubs, and Gujarat's Mundra and Kandla ports driving petrochemical and manufacturing export freight volumes.

Leading companies include DHL Group, Kuehne+Nagel International AG, CMA CGM Group, Delhivery Limited, and A.P. Moller – Maersk, among others.

India freight forwarding market is projected to reach USD 16.78 Billion by 2030, anchored by full DFC operational ramp-up improving rail freight reliability, Sagarmala port modernisation supporting maritime freight growth, and PLI scheme manufacturing export volumes sustaining demand across all modes.

Key drivers include e-commerce expansion, DFC and Sagarmala infrastructure investment, Make in India PLI scheme manufacturing export growth, digital freight platform adoption, pharmaceutical cold-chain logistics demand, and National Logistics Policy 2022 logistics cost reduction targets.

Dedicated Freight Corridors (2,843 km Eastern and Western DFCs) reduced containerised rail transit times by up to 40% and cargo transported via DFC railways has 65% lower carbon emissions than road equivalents, enabling modal shift for bulk and containerised cargo over 500 km routes.

Key opportunities include pharmaceutical cold-chain air freight forwarding, digital freight platform investment, DFC-integrated multimodal logistics parks, B2C cross-border e-commerce forwarding, and specialised project cargo logistics for India's growing infrastructure and industrial construction sectors.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)