India IT Services Market Size, Share, Trends and Forecast by Type, Enterprise Size, Deployment Mode, End Use Industry and Region, 2026-2034

India IT Services Market Size, Share, Trends & Forecast (2026-2034)

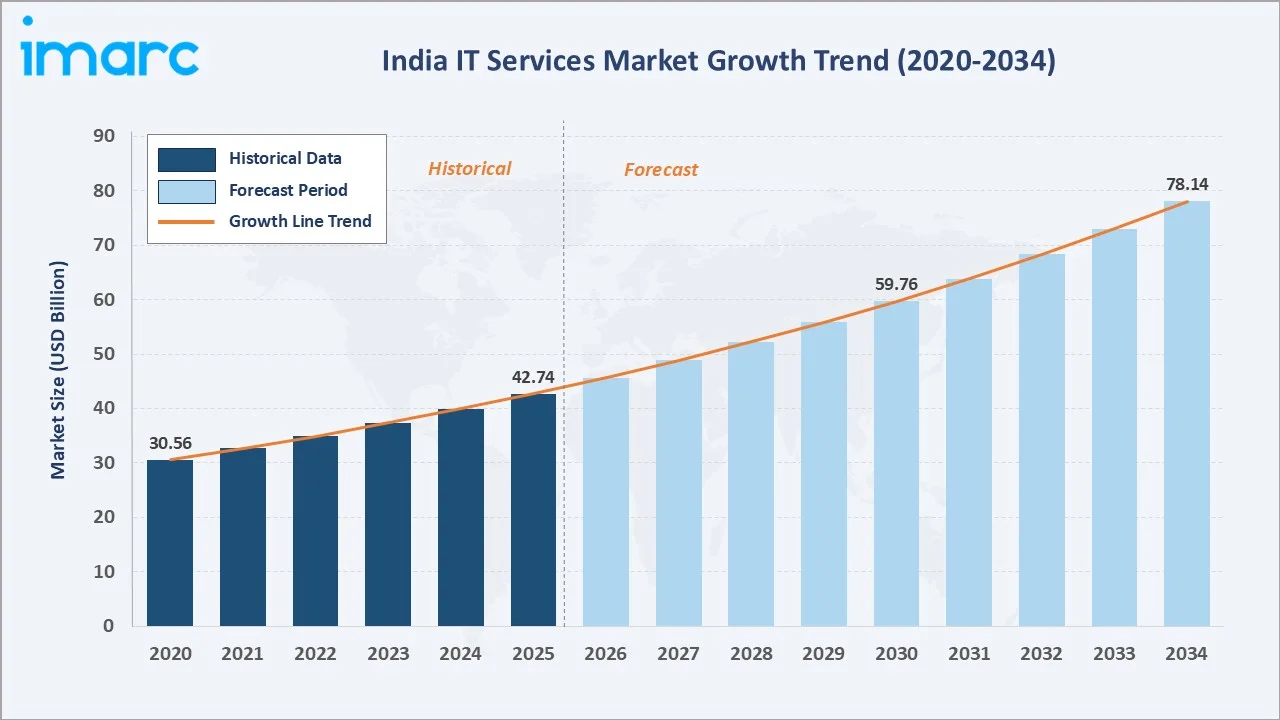

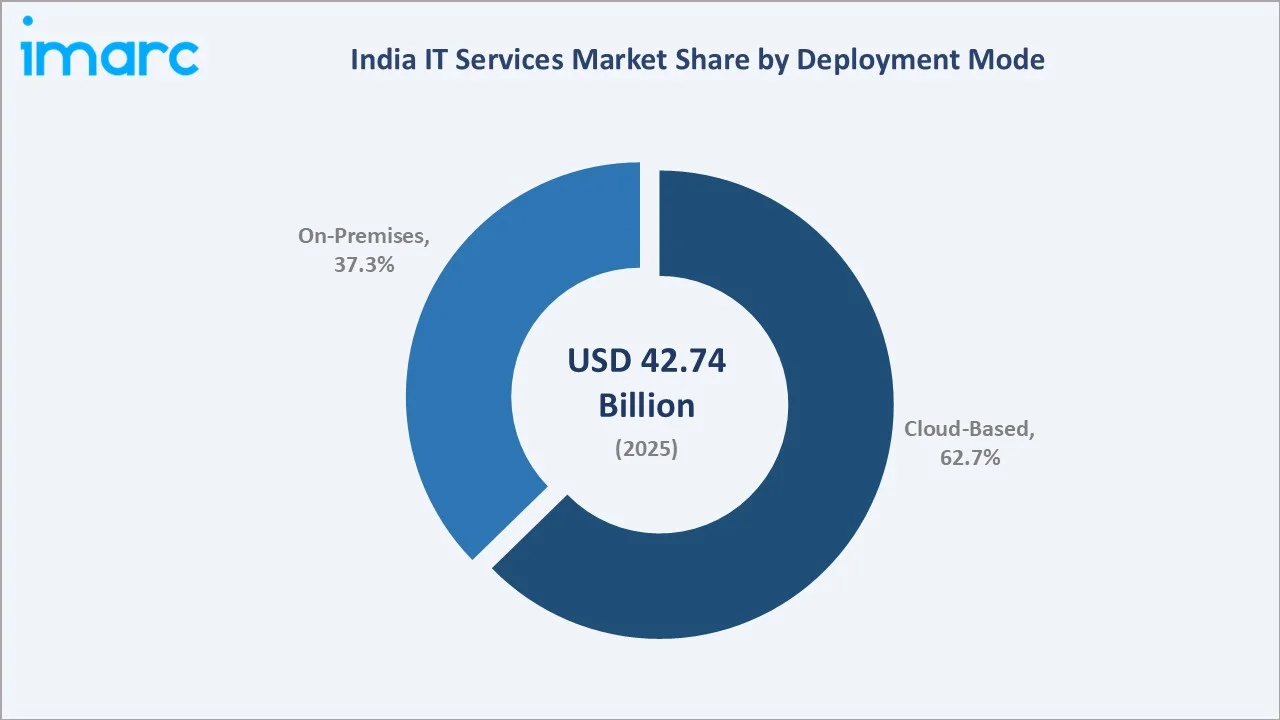

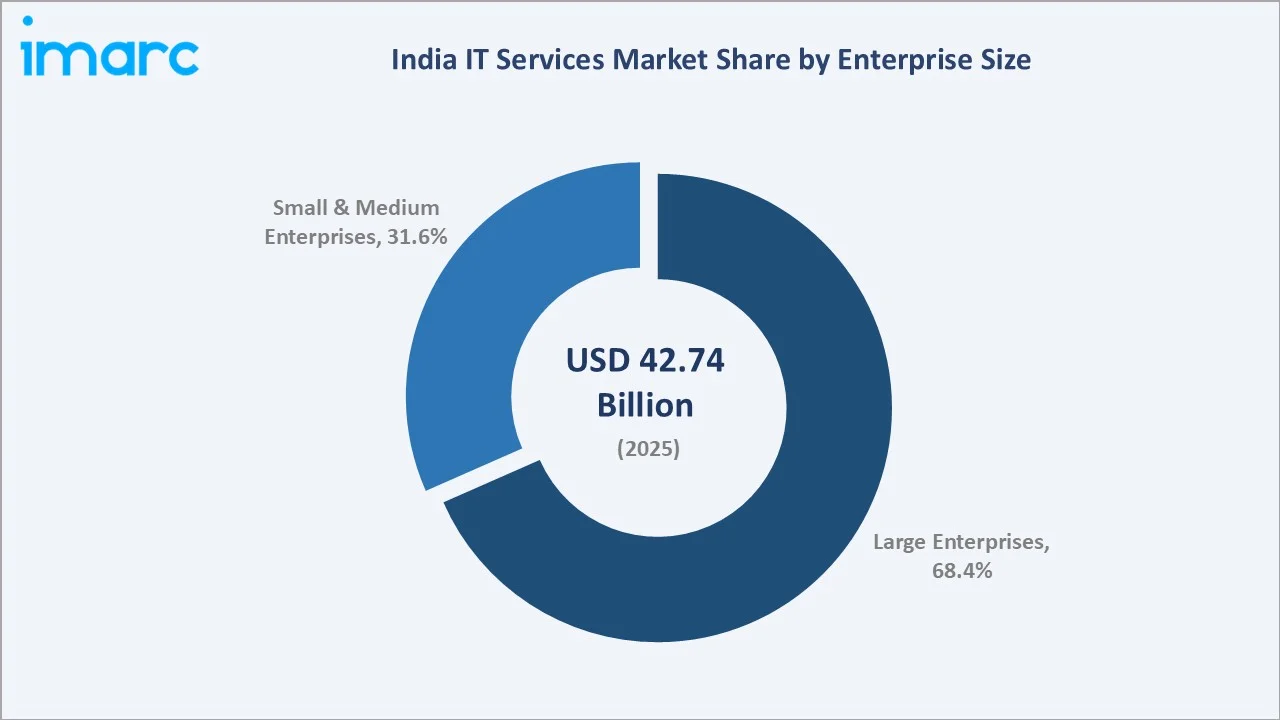

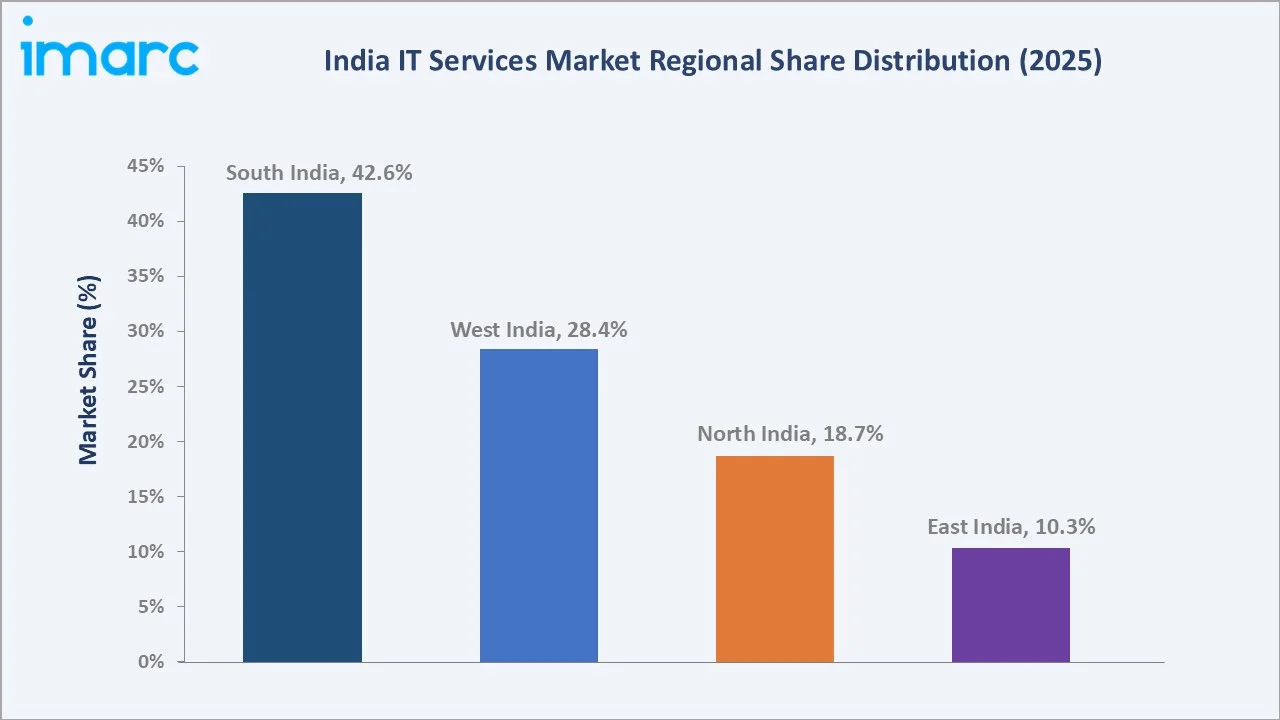

The India IT services market size reached USD 42.74 Billion in 2025 and is projected to reach USD 78.14 Billion by 2034, exhibiting a CAGR of 6.94% during 2026-2034. Accelerating digital transformation across enterprises, rapid cloud computing adoption with hybrid and multi-cloud environments, and the growing integration of AI and automation technologies are the primary forces driving India IT services market growth.

Cloud-based deployment dominates at 62.7% in 2025, while large enterprises lead the enterprise size segment at 68.4%. South India commands a dominant 42.6% regional share in 2025, reflecting Bengaluru, Hyderabad, and Chennai's unparalleled IT ecosystem concentration.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 42.74 Billion |

|

Forecast Market Size (2034) |

USD 78.14 Billion |

|

CAGR (2026-2034) |

6.94% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

South India (42.6% share, 2025) |

|

Second Largest Region |

West India (28.4% share, 2025) |

|

Leading Deployment Mode |

Cloud-Based (62.7%, 2025) |

|

Leading Enterprise Size |

Large Enterprises (68.4%, 2025) |

The India IT services market growth trajectory from 2020 through 2034, with the historical expansion to USD 42.74 Billion in 2025, reflects consistent digital transformation demand, while the forecast to USD 78.14 Billion captures accelerating cloud adoption, AI integration, and enterprise modernization.

To get more information on this market, Request Sample

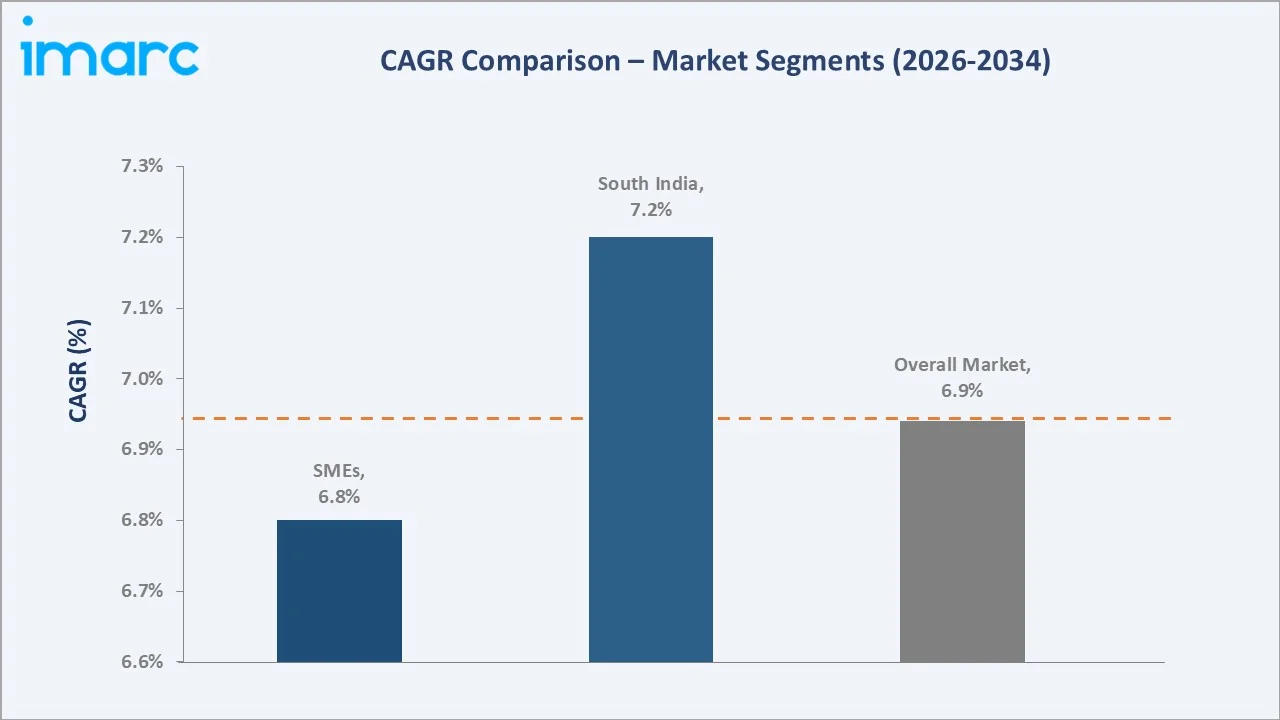

The CAGR trajectories across key deployment, enterprise, and regional sub-segments, with cloud-based deployment at ~7.8% CAGR and large enterprises at ~7.4% CAGR, are the fastest-growing categories within the India IT services industry analysis through 2034.

Executive Summary

The India IT services market is on a sustained growth trajectory from USD 42.74 Billion in 2025 to USD 78.14 Billion by 2034. IT services, encompassing consulting, system integration, managed services, cloud solutions, and digital transformation services, benefit from India's position as a global technology hub.

Cloud-based deployment dominates at 62.7% in 2025, owing to enterprise migration to SaaS, PaaS, and IaaS models that offer scalability, cost optimization, and operational flexibility. On-premises deployment (37.3%) serves industries with stringent data sovereignty and regulatory compliance requirements, particularly in banking and government sectors.

Large enterprises lead at 68.4% in 2025, reflecting their extensive digital transformation budgets and multi-year managed services contracts. Small and medium-sized enterprises (31.6%) represent the fastest-growing segment as cloud-native solutions and subscription-based pricing models democratize access to enterprise-grade IT capabilities.

South India dominates at 42.6% in 2025, anchored by Bengaluru's position as India's technology capital and the established IT corridors in Hyderabad and Chennai. West India (28.4%) and North India (18.7%) follow, driven by Mumbai's financial services demand and Delhi-NCR's government and enterprise technology spending.

Key Market Insights

|

Insight |

Data |

|

Largest Deployment Mode |

Cloud-Based - 62.7% share (2025) |

|

Leading Enterprise Size |

Large Enterprises - 68.4% share (2025) |

|

Leading Region |

South India - 42.6% share (2025) |

|

Second Largest Region |

West India - 28.4% share (2025) |

|

Top Companies |

TATA Consultancy Services Limited, Infosys Limited, Wipro, HCL Technologies Limited, Tech Mahindra Limited, Cognizant, Accenture, Capgemini, L&T Technology Services Limited |

Key Analytical Observations Expanding on the Above Data:

- Cloud-based deployment, with 62.7% in 2025, dominates because of its superior scalability, cost-efficiency, and ability to support remote and hybrid work models that became standard post-COVID-19 across Indian enterprises.

- Large enterprises, with 68.4% in 2025, lead because they possess dedicated IT budgets, multi-year digital transformation roadmaps, and the organizational scale to justify comprehensive managed services and consulting engagements.

- South India's 42.6% dominance in 2025 reflects Bengaluru's concentration of over 400 global capability centers (GCCs), Hyderabad's HITEC City ecosystem, and Chennai's established IT corridor hosting major technology campuses.

- West India, with 28.4% in 2025, benefits from Mumbai's position as India's financial capital generating substantial BFSI IT services demand, and Pune's growing technology hub attracting IT companies expanding beyond Bengaluru.

India IT Services Market Overview

IT services encompass a broad range of technology-driven professional and managed services including consulting, system integration, application development and maintenance, infrastructure management, cloud migration, cybersecurity, data analytics, and digital transformation advisory. Service delivery models span onshore, offshore, and nearshore configurations.

The India IT services ecosystem integrates global technology companies, domestic IT majors, mid-tier specialists, cloud hyperscalers, cybersecurity firms, data center operators, system integrators, and diverse end-use industries spanning BFSI, telecommunications, healthcare, retail, manufacturing, and government.

Market Dynamics

To evaluate market opportunities, Request Sample

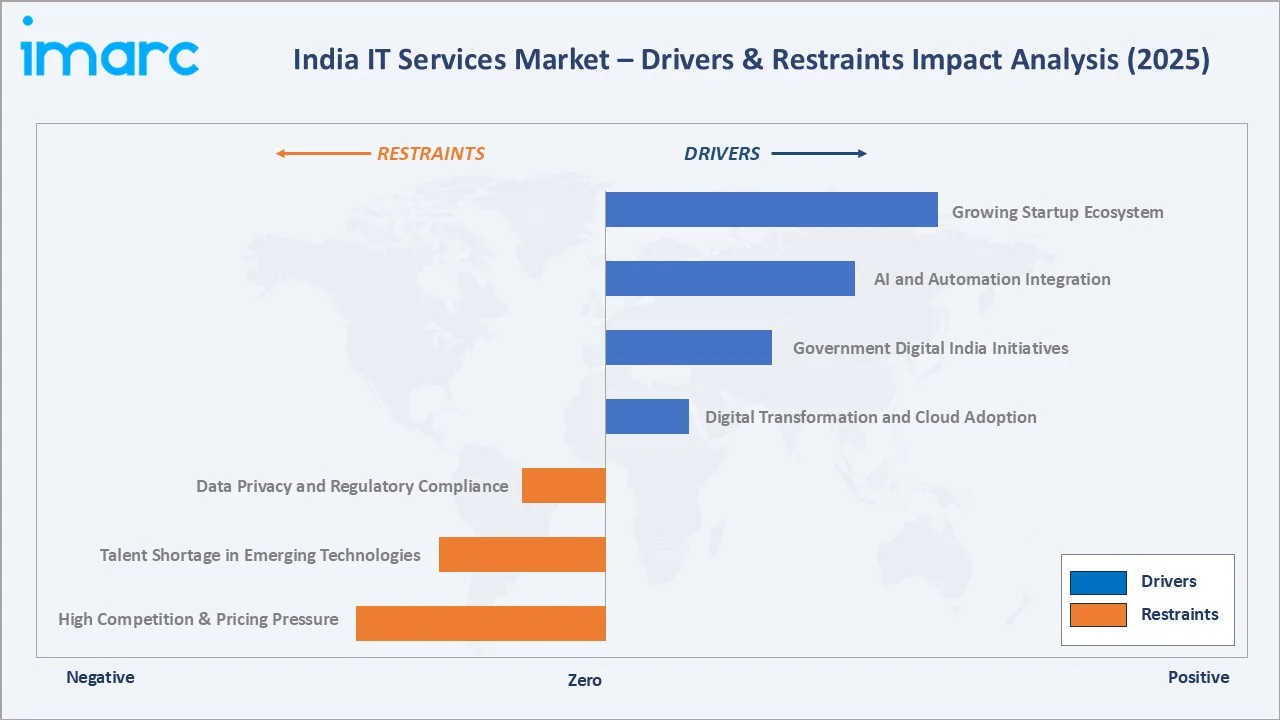

Market Drivers

- Digital Transformation and Cloud Adoption: India's enterprise digital transformation spending exceeded USD 85 Billion by 2026, with organizations accelerating migration to cloud-native architectures, AI-driven operations, and data analytics platforms to enhance competitiveness and operational efficiency.

- AI and Automation Integration: The integration of artificial intelligence, machine learning, and robotic process automation into enterprise IT operations is generating significant demand for specialized consulting, implementation, and managed services across Indian industries.

- Government Digital India Initiatives: Government programs including Digital India, BharatNet, and the National Digital Health Mission are creating substantial public sector IT services procurement, driving technology adoption across government agencies and public service delivery.

Market Restraints

- Data Privacy and Regulatory Compliance: The evolving regulatory landscape, including the Digital Personal Data Protection Act (DPDP Act 2023), creates compliance complexity for IT service providers managing cross-border data flows and multi-jurisdictional operations.

- Talent Shortage in Emerging Technologies: Despite a large workforce base, there are notable gaps in advanced and emerging skill sets, with demand for niche expertise outpacing available supply; this imbalance can slow innovation, increase hiring costs, and create challenges in scaling high-tech capabilities, while organizations often need to invest significantly in upskilling and reskilling initiatives to bridge these gaps, and increased competition for skilled professionals can lead to higher attrition rates and talent retention challenges across the industry.

Market Opportunities

- GenAI and Enterprise AI Services: Generative AI adoption across Indian enterprises is creating new service categories including AI strategy consulting, LLM fine-tuning, prompt engineering, and AI governance, representing a high-growth opportunity for IT service providers.

- GCC Expansion and Captive Center Growth: India hosts over 1,700 global capability centers (GCCs) in 2025, with 50-60 new centers being established annually, each generating significant IT infrastructure, application development, and managed services demand.

Market Challenges

- Pricing Pressure and Margin Compression: Intensifying competition from mid-tier IT firms, offshore delivery centers in competing geographies, and enterprise cost optimization drives are compressing IT services margins across traditional engagement models.

- Client Insourcing and GCC Competition: The growth of enterprise captive centers in India enables clients to insource technology functions previously outsourced to IT service providers, creating competitive pressure on traditional outsourcing revenue streams.

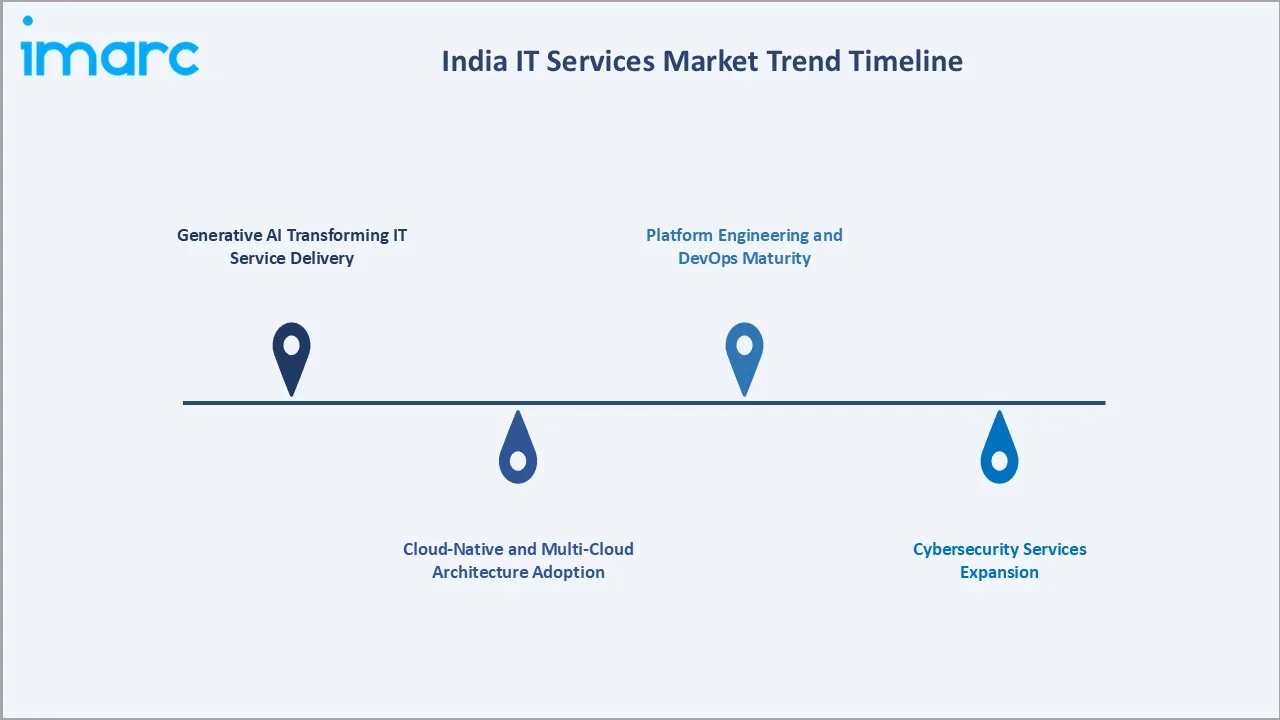

Emerging Market Trends

1. Generative AI Transforming IT Service Delivery

Generative AI adoption is reshaping IT service delivery models, with major Indian IT companies investing heavily in AI-powered code generation, automated testing, and intelligent operations platforms. TCS, Infosys, and Wipro have launched dedicated GenAI practice units serving enterprise clients across industries.

2. Cloud-Native and Multi-Cloud Architecture Adoption

Enterprise migration to cloud-native architectures utilizing containerization, microservices, and serverless computing is driving demand for specialized cloud consulting and implementation services. Multi-cloud strategies spanning AWS, Azure, and GCP are becoming standard across large Indian enterprises.

3. Cybersecurity Services Expansion

India's cybersecurity services market is growing at over 30% annually, driven by increasing cyber threats, regulatory compliance requirements, and enterprise zero-trust architecture adoption. Managed security services and security operations center (SOC) offerings are expanding rapidly.

4. Platform Engineering and DevOps Maturity

Platform engineering practices combining internal developer platforms, DevOps automation, and site reliability engineering (SRE) are being adopted by Indian enterprises to accelerate software delivery velocity and improve application reliability.

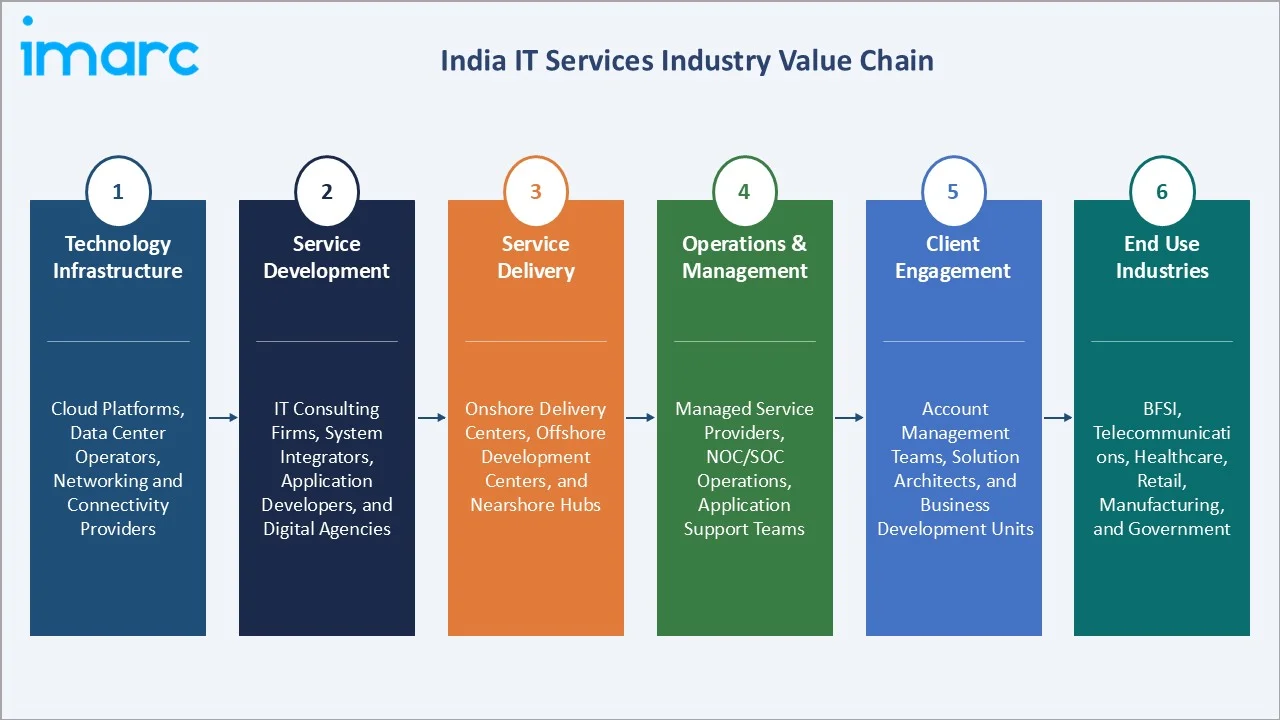

Industry Value Chain Analysis

The India IT services value chain spans six stages from technology infrastructure through end-use industry delivery. Service development and delivery capture the highest value-add margins, while client engagement and managed operations generate recurring revenue streams.

|

Stage |

Key Players / Examples |

|

Technology Infrastructure |

Cloud platforms, data center operators, networking and connectivity providers |

|

Service Development |

IT consulting firms, system integrators, application developers, digital agencies |

|

Service Delivery |

Onshore delivery centers, offshore development centers, nearshore hubs |

|

Operations & Management |

Managed service providers, NOC/SOC operations, application support teams |

|

Client Engagement |

Account management teams, solution architects, business development units |

|

End Use Industries |

BFSI, telecommunications, healthcare, retail, manufacturing, government |

Vertically integrated IT service providers with strong offshore delivery capabilities, proprietary AI platforms, and deep industry domain expertise achieve superior margins compared to generalist providers relying on commoditized labor arbitrage models.

Technology Landscape in the India IT Services Industry

Cloud Computing: Hybrid and Multi-Cloud Architectures

Cloud computing forms the backbone of modern IT service delivery in India. Enterprise adoption of hybrid cloud architectures combining private and public cloud environments enables organizations to balance security, compliance, and scalability requirements while optimizing infrastructure costs.

Artificial Intelligence and Machine Learning Platforms

AI and ML platforms including TensorFlow, PyTorch, and enterprise-grade solutions from AWS SageMaker and Azure ML are being integrated into IT service delivery workflows. Indian IT companies are developing proprietary AI platforms for automated code generation, testing, and operations management.

Cybersecurity Technology Stack

Advanced cybersecurity technologies including zero-trust architecture, extended detection and response (XDR), cloud-native application protection platforms (CNAPP), and AI-powered threat intelligence are being deployed by Indian IT service providers to protect enterprise client environments.

DevOps and Platform Engineering

Kubernetes-based container orchestration, infrastructure-as-code (IaC) using Terraform and Pulumi, and CI/CD pipeline automation are standard technology components in modern IT service delivery, enabling faster deployment cycles and improved operational reliability.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Service Type |

🔒 |

🔒 |

2025 |

|

Enterprise Size |

Large Enterprises |

68.4% |

2025 |

|

Deployment Mode |

Cloud-Based |

62.7% |

2025 |

|

End Use Industry |

🔒 |

🔒 |

2025 |

|

Region |

South India |

42.6% |

2025 |

By Deployment Mode

Cloud-based deployment commands a 62.7% majority share in 2025 owing to its fundamental advantages in scalability, cost optimization, and operational agility. The widespread adoption of SaaS applications, IaaS infrastructure, and PaaS development environments drives enterprises to prioritize cloud-first IT strategies across all industry verticals.

To access detailed market analysis, Request Sample

On-premises deployment at 37.3% 2025 serves industries with stringent data sovereignty requirements, regulatory compliance mandates, and latency-sensitive applications. Banking, defense, and government sectors maintain significant on-premises infrastructure due to data localization requirements under Indian regulatory frameworks.

By Enterprise Size

Large enterprises dominate the market at 68.4% in 2025, representing organizations with dedicated IT budgets exceeding and multi-year digital transformation roadmaps. India's IT spending is expected to reach $176.3 billion in 2026. These enterprises engage IT service providers for comprehensive managed services, consulting, and system integration projects.

Small and medium-sized enterprises at 31.6% in 2025 represent the fastest-growing segment, driven by cloud-native IT solutions, subscription pricing models, and government programs like Startup India and MSME Digital that facilitate technology adoption among smaller businesses.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

|

South India |

42.6% |

Technology hub concentration; GCC ecosystem; Skilled IT workforce |

|

West India |

28.4% |

Financial services demand; Emerging tech hub; Startup ecosystem |

|

North India |

18.7% |

Government IT procurement; Enterprise spending; IT corridor growth |

|

East India |

10.3% |

Emerging tech hub; Digital India penetration; Cost-competitive delivery |

South India's 42.6% market dominance in 2025 is driven by the region's position as India's primary technology hub, hosting the highest concentration of IT service providers, global capability centers, and a deep pool of skilled IT professionals across software engineering, cloud architecture, and AI development disciplines.

West India, with 28.4% in 2025, benefits from the concentration of financial services institutions generating substantial BFSI IT services demand and the region's growing technology hub attracting IT companies expanding their delivery footprint beyond traditional locations.

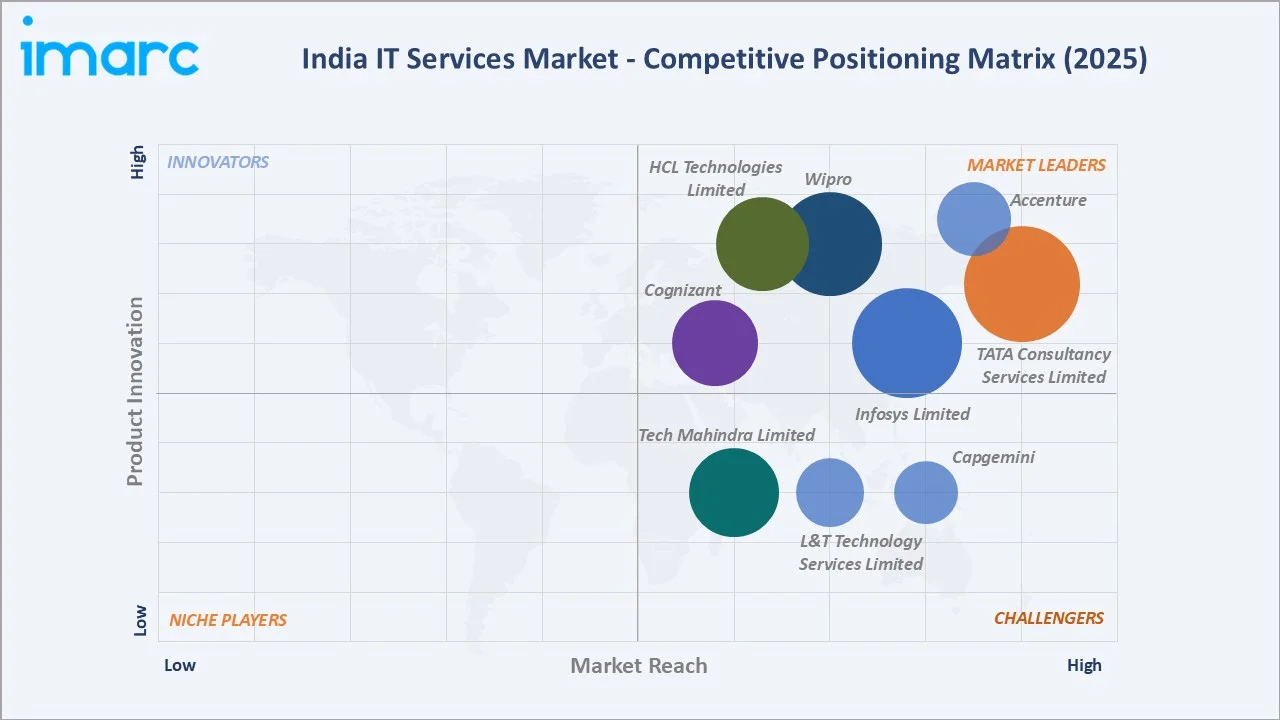

Competitive Landscape

The India IT services market is moderately consolidated, with the top five domestic IT companies commanding significant market share while facing increasing competition from global consulting firms, mid-tier specialists, and captive technology centers established by multinational enterprises.

|

Company Name |

Key Services |

Position |

Strategic Focus |

|

TATA Consultancy Services Limited |

AI and data & analytics, AI-led Data Centres, Cloud, Cybersecurity, Network Solutions and Services, Consulting |

Leader |

Market leader; Full-stack digital; Global delivery |

|

Infosys Limited |

Digital, Cloud, AI, Consulting, BPM |

Leader |

Digital-first strategy; Cobalt cloud; AI-led growth |

|

Wipro |

Cloud, Cybersecurity, Consulting, Data & Analytics, Product Engineering |

Leader |

AI360 platform; FullStride Cloud; Engineering R&D |

|

HCL Technologies Limited |

AI and Generative AI, Engineering and R&D Services, Cloud, Cybersecurity |

Leader |

AI Force platform; Mode 1-2-3 strategy; Products |

|

Tech Mahindra Limited |

Artificial Intelligence, Cloud and Infrastructure Services, Digital Enterprise Applications, Engineering Services, Network Services |

Challenger |

Telecom expertise; Scale at Speed strategy |

|

Cognizant |

Digital Engineering, AI, Cloud, Cybersecurity, Data and AI, IoT & Engineering |

Leader |

Digital engineering; Health sciences focus |

|

Accenture |

Cloud, Cybersecurity, AI and data, Digital engineering and manufacturing |

Leader |

Consulting premium; Global capability centers |

|

Capgemini |

Cloud, Data, AI, Cybersecurity |

Challenger |

Engineering focus; Intelligent Industry |

|

L&T Technology Services Limited |

Digital Engineering & Consulting, Product Engineering, Manufacturing Engineering, Plant Engineering |

Challenger |

Engineering niche; Digital manufacturing |

Key players include TATA Consultancy Services Limited, Infosys Limited, Wipro, HCL Technologies Limited, Tech Mahindra Limited, Cognizant, Accenture, Capgemini, L&T Technology Services Limited, and others.

Key Company Profiles

TATA Consultancy Services Limited

Tata Consultancy Services is India's largest IT services company and a global leader in technology consulting and digital solutions. TCS operates in 50+ countries with around 600,000 employees, delivering services spanning consulting, cognitive business operations, and cloud infrastructure to clients across major industries.

- Product Portfolio: TCS offers consulting, application development, cloud migration, AI/ML solutions, cybersecurity, managed infrastructure services, and industry-specific digital platforms.

- Recent Developments: In January 2024, Tata Consultancy Services enhanced its focus on building an AI-ready workforce by launching a new AI Experience Zone, designed to provide employees with hands-on exposure to artificial intelligence and generative AI technologies. The initiative follows large-scale foundational training efforts and enables employees to experiment with advanced tools, develop innovative use cases, and collaborate globally within a structured and responsible AI framework, thereby strengthening the company’s overall AI capabilities and innovation ecosystem.

- Strategic Focus: TCS leverages its deep industry domain expertise, global delivery network, and proprietary AI platforms to compete on total value delivery, focusing on large transformational deals and expanding its cloud and AI service portfolio.

Infosys Limited

Infosys Limited is India's second-largest IT services company, recognized globally for its digital transformation capabilities. The company focuses on AI-first strategies and cloud-native solutions, serving clients across financial services, manufacturing, retail, and healthcare verticals.

- Product Portfolio: Infosys offers digital consulting, cloud services via Infosys Cobalt, AI solutions through Infosys Topaz, engineering services, and business process management.

- Recent Developments: In May 2026, Infosys announced the completion of its acquisition of Optimum Healthcare IT, a U.S.-based healthcare digital transformation and consulting firm, as part of its strategy to strengthen its presence in the healthcare provider segment. The acquisition enhances Infosys’ domain expertise, expands client relationships, and boosts its capabilities in cloud, data, and AI-driven transformation, while enabling the integration of Optimum’s specialized healthcare experience with Infosys’ platforms to deliver large-scale, end-to-end digital solutions that improve patient outcomes and operational efficiency.

- Strategic Focus: Infosys differentiates through its AI-first approach with the Topaz platform, cloud-native delivery through Cobalt, and strategic acquisitions that expand geographic presence and capability depth in high-growth technology domains.

Wipro

Wipro is a leading global IT services company headquartered in Bengaluru, India. The company serves clients across six continents with capabilities spanning cloud transformation, cybersecurity, engineering R&D, and AI-powered business solutions.

- Product Portfolio: Wipro offers cloud services via FullStride Cloud, AI solutions through ai360, cybersecurity, digital engineering, and enterprise application services.

- Recent Developments: In April 2026, Wipro Limited announced the launch of a dedicated AI-Native Business and Platforms Unit to complement its core services and accelerate innovation-led growth, aligning with the shift toward a “services-as-software” model. The new unit focuses on building scalable, enterprise-grade AI platforms and solutions, while strengthening consulting-led, AI-driven transformation capabilities to enhance competitiveness and drive long-term growth in an increasingly AI-first digital landscape.

- Strategic Focus: Wipro focuses on large deal momentum, AI-led transformation services, and strategic client partnerships, leveraging its ai360 platform to embed artificial intelligence across all service delivery engagements.

Market Concentration Analysis

The India IT services market exhibits moderate concentration at the national level, with the top five domestic IT companies (TCS, Infosys, Wipro, HCL Technologies, and Tech Mahindra) collectively commanding a significant share of total market revenue. However, the market remains competitive with over 50,000 registered IT companies across India.

Regional concentration patterns differ significantly. South India, particularly Bengaluru, hosts the highest concentration of IT service providers and global capability centers. The Delhi-NCR and Mumbai-Pune corridors represent secondary concentration zones with distinct client industry profiles.

Investment & Growth Opportunities

Fastest-Growing Segments

Cloud-based IT services at ~7.8% CAGR through 2034 represent the highest-growth deployment segment, driven by enterprise cloud-first strategies and the rapid adoption of SaaS, PaaS, and IaaS models across Indian industries. AI and automation services represent the broadest-based growth opportunity.

Emerging Markets

East India at ~8.2% CAGR represents the fastest-growing region for IT services through 2034. Tier-2 cities including Bhubaneswar, Jaipur, Indore, and Coimbatore are emerging as alternative IT delivery locations, driven by lower operational costs and government technology park incentives.

Venture & Investment Trends

Private equity and venture capital investment in Indian IT services continues to accelerate, with particular focus on AI/ML startups, cybersecurity specialists, and cloud-native platform companies. Strategic investments in upskilling and reskilling programs are enabling IT service providers to build capabilities in GenAI, quantum computing, and edge computing.

Future Market Outlook (2026-2034)

The India IT services market is forecast to expand from USD 42.74 Billion in 2025 to USD 78.14 Billion by 2034 at a CAGR of 6.94%, adding USD 35.40 Billion in incremental annual market value over the forecast period. This growth reflects the structural nature of digital transformation demand across Indian enterprises.

Three technological forces will most significantly shape the India IT services landscape through 2034. Generative AI integration across enterprise operations will create new service categories and transform existing delivery models. Edge computing and IoT platform services will expand IT service delivery beyond traditional data center and cloud environments. Quantum computing readiness services will emerge as enterprise clients begin preparing for post-quantum cryptography and quantum-advantage computing applications.

Research Methodology

Primary Research

Primary research encompassed over 50 structured interviews in 2024-2025 with IT services industry stakeholders, including senior technology executives, CIOs, cloud architects, NASSCOM leadership, and IT procurement specialists across Indian enterprises. Primary data validated market sizing, deployment mode and enterprise size segment shares, regional demand estimates, and technology adoption timelines.

Secondary Research

Key secondary sources include NASSCOM Strategic Review publications (2020-2025), RBI annual reports on services sector performance, MeitY Digital India programme reports, Gartner IT Services market data, IDC India IT spending forecasts, and industry publications including Dataquest India and CIO India.

Forecasting Models

Market size estimations and growth projections were derived using a combination of top-down and bottom-up forecasting models, incorporating GDP growth rates, enterprise IT spending patterns, cloud adoption indices, and historical market evolution. Scenario analysis was performed to account for macroeconomic uncertainty.

India IT Services Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Types Covered | Professional Services (System Integration and Consulting), Managed Services |

| Enterprise Sizes Covered | Small and Medium-Sized Enterprises, Large Enterprises |

| Deployment Modes Covered | On-Premises, Cloud-Based |

| End Use Industries Covered | BFSI, Telecommunication, Healthcare, Retail, Manufacturing, Government, Others |

| Regions Covered | North India, South India, East India, West India |

| Companies Covered | TATA Consultancy Services Limited, Infosys Limited, Wipro, HCL Technologies Limited, Tech Mahindra Limited, Cognizant, Accenture, Capgemini, L&T Technology Services Limited, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the India IT services market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the India IT services market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the India IT services industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the India IT Services Market Report

The India IT services market reached USD 42.74 Billion in 2025, reflecting consistent demand from enterprise digital transformation, cloud adoption, and AI integration across industries.

The market is projected to reach USD 78.14 Billion by 2034, growing at a CAGR of 6.94% during 2026-2034, driven by cloud-first enterprise strategies, GenAI adoption, and expanding GCC ecosystem.

Cloud-based deployment leads with a 62.7% share in 2025, valued for its scalability, cost-efficiency, and alignment with hybrid work models, serving many enterprise IT requirements.

Large enterprises lead at 68.4% in 2025, representing organizations with significant IT budgets, multi-year transformation roadmaps, and comprehensive managed services engagements.

South India commands a dominant 42.6% market share in 2025, driven by its technology hub concentration, global capability center ecosystem, and deep pool of skilled IT professionals.

Cloud-based IT services represent the fastest-growing segment at ~7.8% CAGR through 2034, driven by enterprise SaaS adoption and cloud-native architecture migration.

Leading companies include TATA Consultancy Services Limited, Infosys Limited, Wipro, HCL Technologies Limited, Tech Mahindra Limited, Cognizant, Accenture, Capgemini, L&T Technology Services Limited, and others.

Key applications include cloud migration and managed services, digital transformation consulting, AI and automation implementation, cybersecurity operations, application development and maintenance, and enterprise system integration.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)