India Plant-Based Milk Market Size, Share, Trends and Forecast by Product, Formulation, Category, Form, Distribution Channel, and Region, 2026-2034

India Plant-Based Milk Market Size, Share, Trends & Forecast (2026-2034)

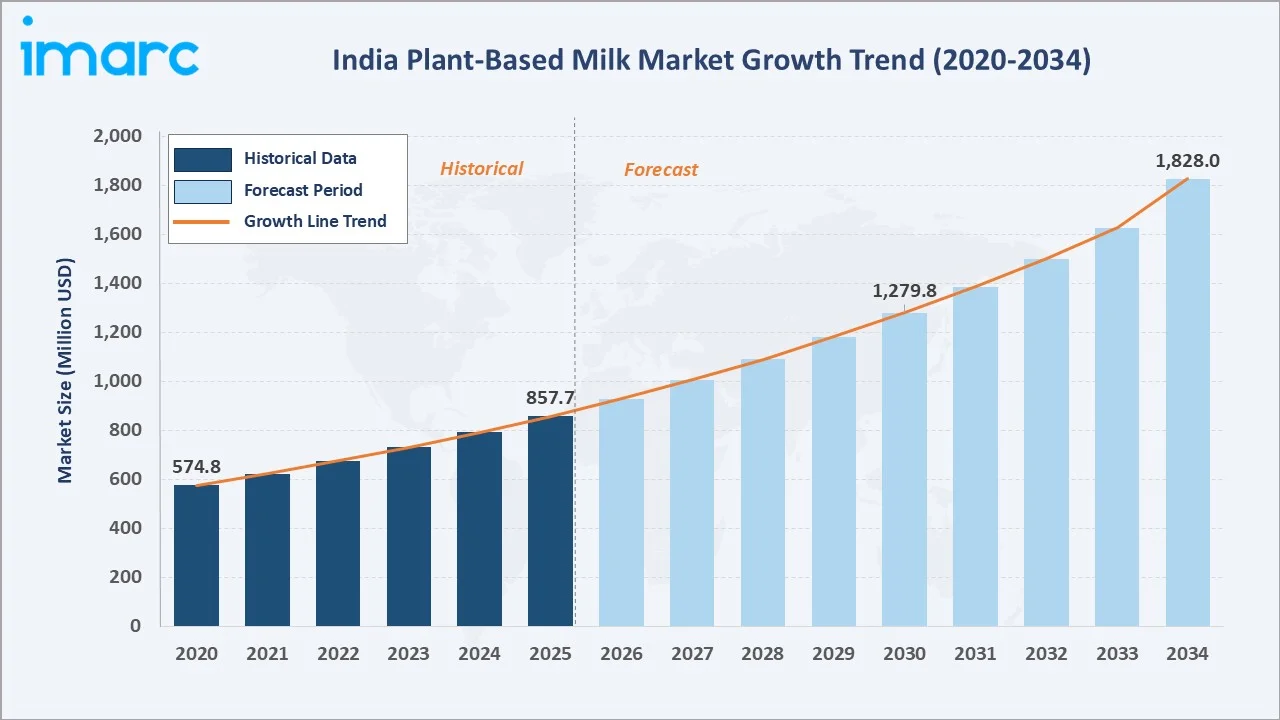

The India plant-based milk market reached USD 857.7 Million in 2025 and is projected to reach USD 1,828.0 Million by 2034, growing at a CAGR of 8.33% during 2026-2034. Growth is driven by rising lactose intolerance, health and wellness awareness, vegan diet adoption, and expanding product innovation.

The market is anchored by Unflavored formulations at 58.4% and Conventional category at 74.2%, while Flavored and Organic variants represent high-growth sub-segments. North India leads regionally at 28.9%, supported by strong urban consumption in Delhi NCR and Chandigarh.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 857.7 Million |

|

Forecast Market Size (2034) |

USD 1,828.0 Million |

|

CAGR (2026-2034) |

8.33% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Dominant Formulation |

Unflavored (58.4%, 2025) |

|

Dominant Category |

Conventional (74.2%, 2025) |

|

Leading Region |

North India (28.9%, 2025) |

To get more information on this market, Request Sample

The market expanded from USD 574.8 Million in 2020 to USD 857.7 Million in 2025, nearly doubling in five years, driven by heightened health awareness. The market is anchored at USD 1,279.8 Million in 2030 and projected to reach USD 1,828.0 Million by 2034.

Executive Summary

The India plant-based milk market reached USD 857.7 Million in 2025, representing one of Asia's fastest-growing dairy alternative categories driven by rising lactose intolerance, expanding vegan lifestyles, and accelerating urban health consciousness among millennials and Gen Z consumers.

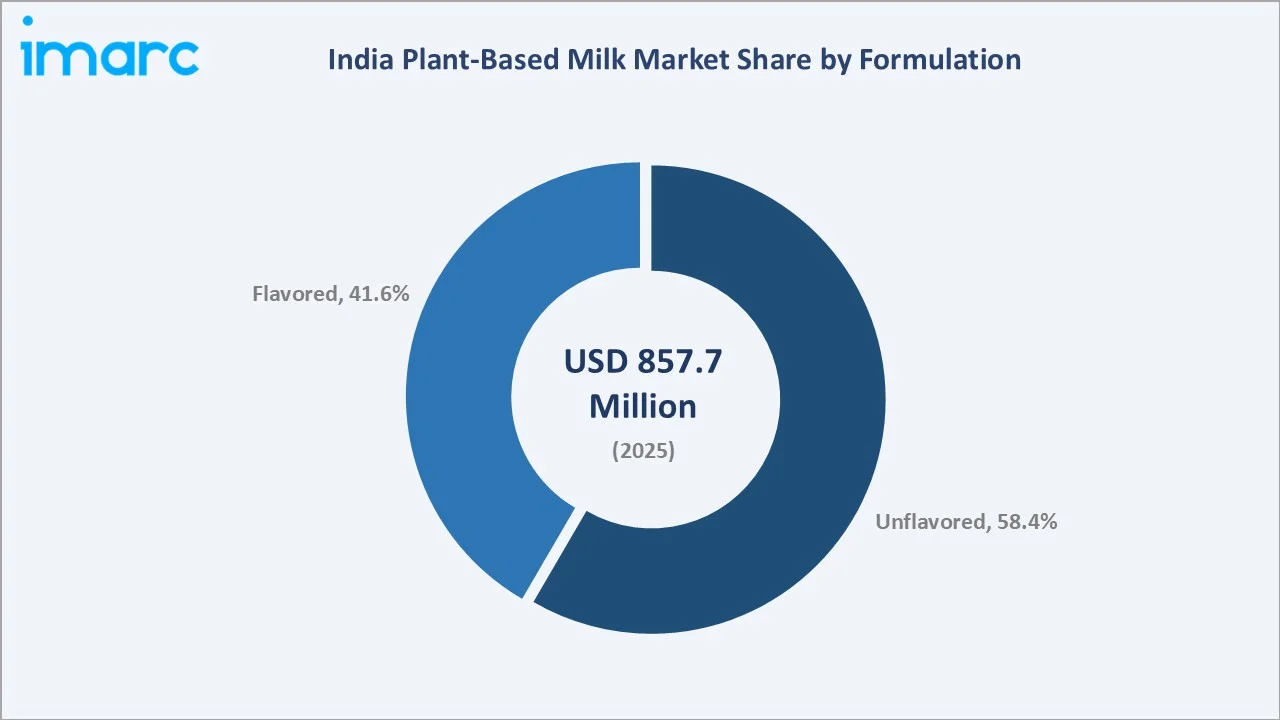

Unflavored formulations dominate at 58.4% through their versatility in cooking and beverage applications, while the conventional category leads at 74.2% through accessibility and price competitiveness.

North India leads at 28.9%, driven by strong metropolitan consumption in Delhi NCR, while West and Central India at 27.6% reflects robust demand from Mumbai and Pune's health-conscious consumer base across modern retail channels.

Key Market Insights

|

Insight |

Data |

|

Dominant Formulation |

Unflavored – 58.4% share (2025) |

|

Fastest Growing Formulation |

Flavored – ~9.1% CAGR (2026-2034) |

|

Dominant Category |

Conventional – 74.2% market share (2025) |

|

Fastest Growing Category |

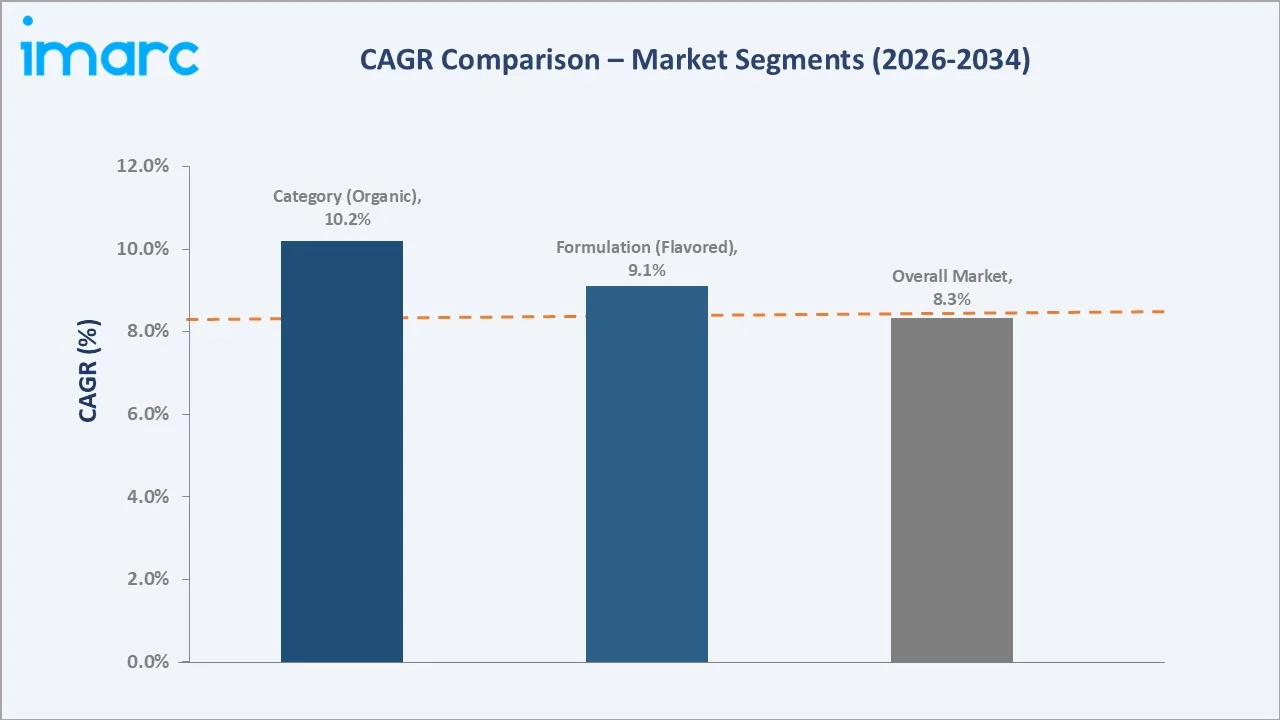

Organic – ~10.2% CAGR (2026-2034) |

|

Leading Region |

North India – 28.9% share (2025) |

|

Market Opportunity |

Organic premiumisation; Flavored innovation; Tier-2 city penetration |

India Plant-Based Milk Market Overview

The India plant-based milk market encompasses soy milk, almond milk, coconut milk, rice milk, oat milk, and other plant-derived milk substitutes marketed across unflavored and flavored formulations in both conventional and organic categories through B2B and B2C distribution channels.

The ecosystem integrates raw material suppliers, processing and blending manufacturers, packaging companies, cold chain logistics providers, organised retail chains, e-commerce platforms, and D2C brands serving health-conscious urban consumers.

Market Dynamics

To evaluate market opportunities, Request Sample

Market Drivers

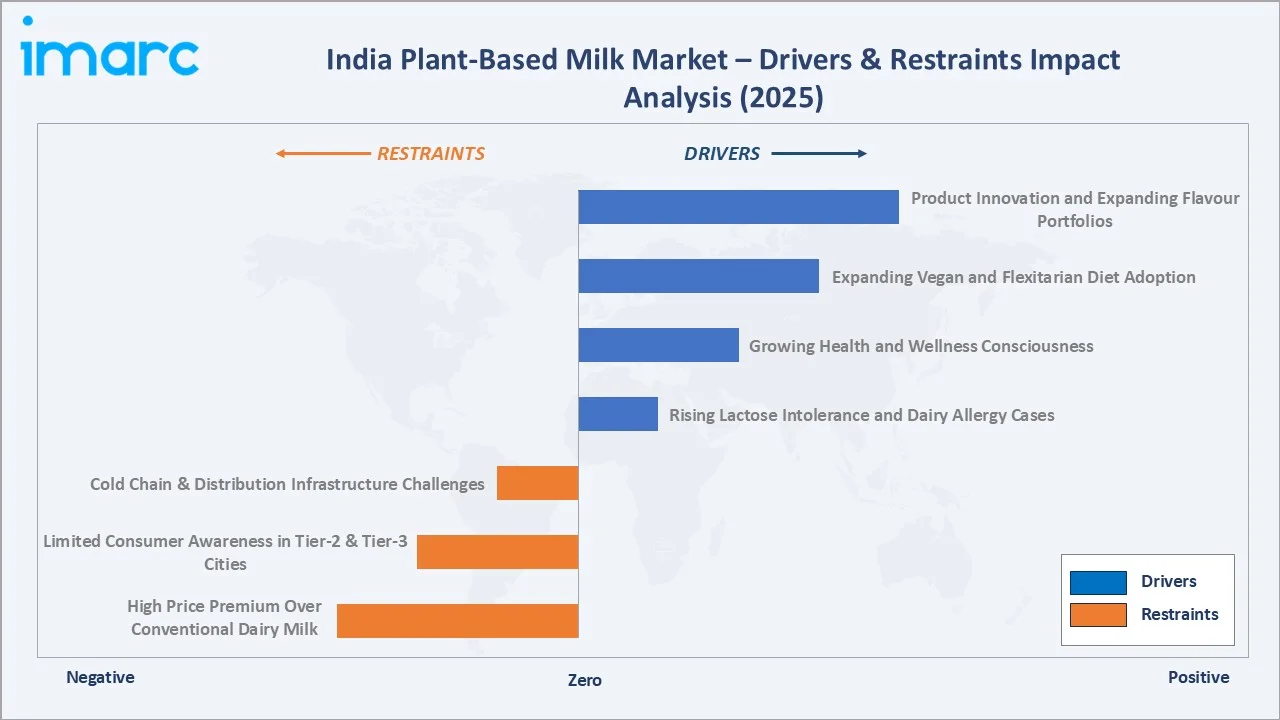

- Rising Lactose Intolerance and Dairy Allergy Cases: India has a high prevalence of lactose intolerance, with estimates suggesting around 65%–90% of Indian adults have some degree of lactose intolerance. This structural demand driver is accelerating adoption of plant-based milk alternatives including soy, oat, almond, and coconut milk across urban and semi-urban consumer segments.

- Growing Health and Wellness Consciousness Among Consumers: Urban Indian consumers, particularly millennials and Gen Z, are increasingly prioritising low-cholesterol, high-protein, and fortified dairy alternatives. Plant-based milk's positioning as a cleaner nutritional option is driving premiumisation and repeat purchase behaviour across modern retail channels.

- Expanding Vegan and Flexitarian Diet Adoption: India's growing vegan and flexitarian population is structurally expanding the plant-based milk addressable market. Ethical consumption, environmental awareness, and celebrity endorsement of vegan lifestyles are reinforcing this shift, particularly among younger, digitally engaged urban demographics.

- Product Innovation and Expanding Flavour Portfolios: Manufacturers are launching fortified, flavoured, and functional variants including protein-enriched oat milk and turmeric-infused almond milk, expanding the category beyond niche health food to mainstream household consumption and increasing trial frequency across income segments.

Market Restraints

- High Price Premium Over Conventional Dairy Milk: Plant-based milk products command a 3-5x price premium over conventional dairy milk, significantly constraining adoption among price-sensitive middle and lower-income segments and limiting mass-market penetration beyond tier-1 urban consumers despite growing awareness.

- Limited Consumer Awareness in Tier-2 and Tier-3 Cities: Despite urban growth, awareness and availability of plant-based milk remain low in smaller cities and rural markets, where dairy milk retains overwhelming consumer preference and brand trust, creating a significant geographic adoption barrier for manufacturers and brands.

- Cold Chain and Distribution Infrastructure Challenges: Many plant-based milk products require refrigerated storage and distribution, which remains inadequate across India's non-metro supply chains, leading to higher spoilage rates, limited shelf life, and restricted geographic availability for expanding brands.

Market Opportunities

- Organic Segment Premiumisation: The Organic category at 25.8% is growing fastest segment as health-conscious consumers seek certified, chemical-free alternatives. Brands investing in organic certification and clean-label positioning can command significant price premiums across high-value urban consumer segments.

- Café and Foodservice Channel Expansion: The rapidly growing café culture in India, with specialty coffee chain expansion, is creating significant B2B demand for oat and almond milk barista variants, offering manufacturers a high-visibility, premium-margin market development opportunity across metro India.

Market Challenges

- FSSAI Regulatory Standardisation: The absence of finalized FSSAI-specific standards for plant-based milk labelling and nutritional claims creates compliance uncertainty for manufacturers, potentially limiting product launch velocity and consumer trust-building across organised retail channels.

- Raw Material Price Volatility: Fluctuating prices of key inputs including almonds, oats, soybeans, and coconuts, driven by seasonal variability and global commodity cycles, create margin pressure for manufacturers, particularly smaller D2C brands without long-term procurement agreements.

Emerging Market Trends

1. Oat Milk Emergence as the Fastest-Growing Plant-Based Format

Oat milk is gaining rapid traction in India's premium café segment and among health-conscious consumers. In June 2025, Country Delight launched its Oat Beverage using Australian oats with no preservatives, targeting lactose-intolerant and vegan consumers through its D2C app.

2. D2C and Quick-Commerce Channel Acceleration

Brands like GoodMylk Co. and Only Earth are leveraging Swiggy Instamart, Blinkit, and proprietary D2C platforms to bypass traditional cold-chain limitations, reaching urban consumers directly with subscription models and improving margin realisation and customer retention.

3. Protein-Enriched and Functional Plant-Based Milk Innovation

Brands are launching fortified variants with added protein, calcium, Vitamin D, and omega-3. In June 2025, HRX launched oat milk protein shakes with 25g protein per 200ml serving, targeting fitness-conscious consumers seeking dairy-free high-protein alternatives in India.

4. Organic and Clean-Label Positioning as Premium Differentiator

Growing consumer demand for transparent ingredient lists and organic certifications is driving brands to prioritise clean-label formulations. This trend is most pronounced in North and West India's affluent urban markets, supporting the Organic sub-segment's above-market growth trajectory.

Industry Value Chain Analysis

The India plant-based milk value chain integrates raw material sourcing, processing and blending, quality testing, packaging, cold chain logistics, and distribution across modern trade, e-commerce, and direct-to-consumer channels to reach health-conscious end consumers nationally.

|

Stage |

Key Participants |

|

Raw Material Sourcing |

Primary agricultural suppliers providing key plant-based raw materials including soy, oats, almonds, coconuts, and rice for processing |

|

Processing & Blending |

Dedicated manufacturers engaged in blending, homogenising, pasteurising, and fortifying raw plant ingredients into finished beverage formats |

|

Quality Testing & Safety |

Accredited food testing laboratories and in-house quality assurance teams validating nutritional claims and food safety compliance standards |

|

Packaging & Labelling |

Packaging material suppliers providing ambient tetra-pack and refrigerated PET bottle formats for retail and institutional distribution channels |

|

Distribution & Logistics |

Cold chain logistics providers and third-party distributors enabling national market reach across metro and emerging city markets |

|

Retail & E-Commerce |

Modern grocery chains, specialty health stores, online grocery platforms, and D2C apps connecting products with urban end consumers |

The processing and blending stage represent the highest value-addition tier, with fortification, flavouring, and organic certification decisions determining final product positioning, price point, and target consumer segment across India's rapidly evolving plant-based beverage market.

Technology Landscape in the India Plant-Based Milk Industry

Ultra-High Temperature (UHT) Processing Technology

UHT processing enables ambient-shelf-stable plant-based milk, eliminating refrigeration requirements and expanding distribution reach into tier-2 and tier-3 Indian markets. This technology is a primary enabler of scale and geographic penetration for leading manufacturers in India.

Enzyme-Based Blending and Fortification Technology

Advanced enzymatic processing improves plant-based milk's taste profile, mouthfeel, and nutritional density, addressing key consumer barriers to adoption. Fortification with calcium, Vitamin B12, and plant-based proteins through precision blending enables manufacturers to match conventional milk nutritional claims.

Cold-Press and Minimal-Processing Technology

Cold-press technology is being adopted by premium D2C brands to preserve natural enzymes, flavour profiles, and nutritional integrity in almond and cashew milk variants. This commands a significant price premium and is driving Organic segment premiumisation at approximately 10.2% CAGR through 2034.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Product |

🔒 |

🔒 |

2025 |

|

Formulation |

Unflavored |

58.4% |

2025 |

|

Category |

Conventional |

74.2% |

2025 |

|

Form |

🔒 |

🔒 |

2025 |

|

Distribution Channel |

🔒 |

🔒 |

2025 |

|

Region |

North India |

28.9% |

2025 |

By Formulation

The Unflavored segment dominates at 58.4% in 2025, driven by its versatility across cooking, beverage, and hot drink applications. Unflavored plant-based milk serves as a direct dairy substitute across household and foodservice channels with strong repeat purchase driven by functional utility.

To access detailed market analysis, Request Sample

The Flavored segment at 41.6% is growing at approximately 9.1% CAGR, driven by chocolate, vanilla, and mango variants appealing to younger consumers and children. Flavored plant-based milk is expanding trial among non-vegan consumers seeking dairy-free indulgence across modern retail channels.

By Category

The Conventional segment leads at 74.2% in 2025, dominating through wider price accessibility and extensive retail availability. Conventional plant-based milk serves the broadest consumer base across health-conscious, flexitarian, and lactose-intolerant segments seeking affordable dairy alternatives.

.webp)

The Organic segment at 25.8% is the fastest-growing category at approximately 10.2% CAGR, driven by premium positioning, clean-label consumer demand, and rising environmental consciousness. Organic plant-based milk commands a 25-40% price premium over conventional variants across organised retail.

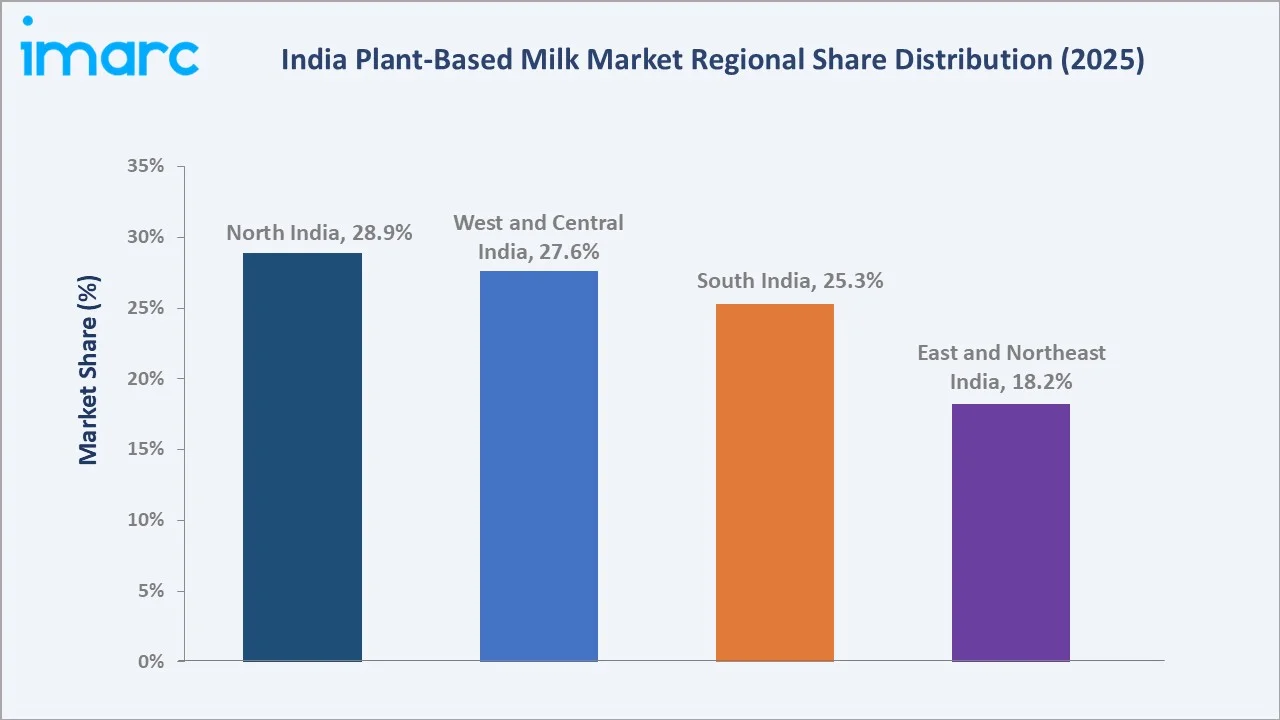

Regional Market Insights

|

Region |

Share (2025) |

Key India Plant-Based Milk Market Drivers & Characteristics |

|

North India |

28.9% |

Largest regional share; driven by high health awareness in Delhi NCR; strong café culture and D2C channel penetration among millennial consumers |

|

West and Central India |

27.6% |

Driven by an affluent consumer base in Mumbai and Pune; strong modern retail presence; growing fitness and wellness culture across metropolitan cities |

|

South India |

25.3% |

Strong vegetarian and vegan population; traditional coconut milk consumption supporting adoption; expanding organised retail in Bengaluru and Chennai |

|

East and Northeast India |

18.2% |

Emerging market with growing awareness; expanding modern trade in Kolkata; lower per-capita consumption with an accelerating growth trajectory |

North India, at 28.9%, leads through the large metropolitan consumer base of Delhi NCR and high online retail penetration. West and Central India, at 27.6%, reflects Mumbai's premiumisation trend and Maharashtra's expanding health food market across urban consumers.

South India, at 25.3%, benefits from a culturally embedded tradition of coconut milk and a large vegetarian population in Tamil Nadu and Karnataka. East and Northeast India, at 18.2%, represents the highest-growth emerging opportunity as modern trade and e-commerce penetration accelerate.

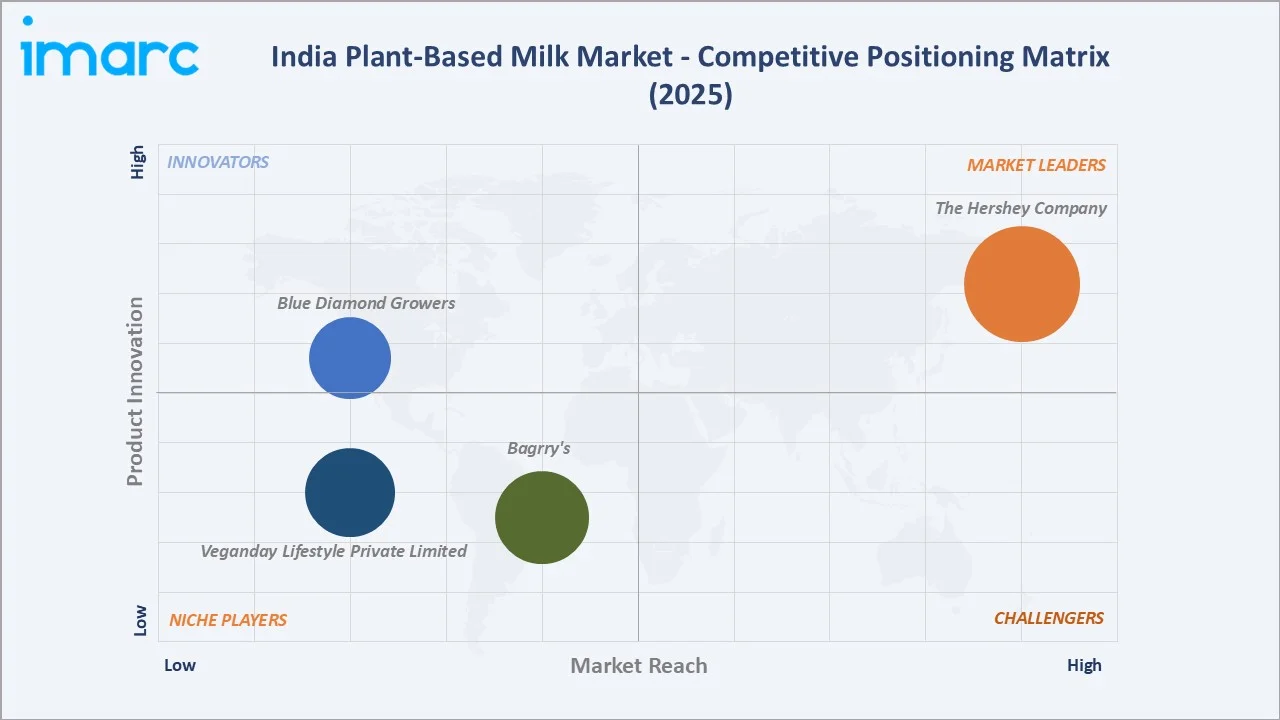

Competitive Landscape

The India plant-based milk market competitive landscape is moderately fragmented, with global multinationals competing alongside domestic D2C brands, serving premium urban consumers.

|

Company Name |

Key Products |

Market Position |

Core Strength |

|

The Hershey Company |

Sofit Soya Drink |

Market Leader |

Pioneer of branded soy milk in India through Sofit; widest cold-chain distribution network across modern retail nationally |

|

Veganday Lifestyle Private Limited |

Coconut Milk, Almond Milk, Cashew Milk, Soya Milk, Oat Milk |

Niche Player |

India-born D2C plant milk base brand; broad product range; affordable and freshness-focused positioning |

|

Blue Diamond Growers |

Almond Breeze Almond Milk |

Emerging Player |

Global leader in almond-based beverages; expanding India distribution through premium import channels and modern grocery |

|

Bagrry's |

Almond milk, Oat Milk |

Niche Player |

Established Indian health food brand leveraging oats expertise to expand into plant-based milk with strong brand trust |

Key players include The Hershey Company, Veganday Lifestyle Private Limited, Blue Diamond Growers, Bagrry's, and others.

Key Company Profiles

The Hershey Company

The Hershey Company is a global confectionery and beverage corporation headquartered in Hershey, Pennsylvania, USA. The plant-based milk segment, through its Sofit brand of soy-based beverages across modern retail.

- Key Products: Sofit Soya Drink

- Strategic Focus: Defending Sofit's market leadership through distribution deepening into tier-2 cities, expanding SKU portfolio with functional variants, and leveraging Hershey India's nationwide salesforce for organised retail penetration.

Bagrry's

The company is the second-largest Indian brand in breakfast cereals, with over 50 years of family expertise in grain milling and food processing. It entered the plant-based milk segment by leveraging its established oats and grain expertise.

- Key Products: Almond milk, Oat Milk

- Strategic Focus: Leveraging its established supplier relationships with Nestlé, Britannia, and ITC and its multi-location manufacturing facilities in Delhi, Baddi, Newai, and Bulandshahr to expand plant-based milk distribution across organised retail and health food channels, building on its existing brand trust in the breakfast and health food segment.

Market Concentration Analysis

The India plant-based milk market is moderately fragmented, with the top two players commanding the largest branded market share through their first-mover advantage in organised retail distribution. Global players collectively hold approximately 40-50% of branded market revenue.

Domestic D2C brands are collectively gaining share through digital-first strategies, particularly among premium urban consumers aged 25-40 who prioritise clean-label and organic credentials over established brand trust.

Investment & Growth Opportunities

Highest Growth Segments

- Organic Category (~10.2% CAGR): Clean-label consumer demand, organic certification premium, and health-conscious premiumisation are driving Organic as the fastest-growing segment, offering above-market margins for brands investing in certified supply chains.

- Flavored Formulation (~9.1% CAGR): Chocolate, vanilla, and regional flavour variants are expanding trial among non-vegan consumers and children, broadening the addressable market significantly beyond the core health-food consumer base across urban India.

- Oat Milk Sub-Category: Oat milk is gaining the fastest momentum through café channel adoption and protein-shake positioning, with brands like Country Delight and HRX validating consumer demand for oat-based functional beverages across India.

Emerging Investment Opportunities

Café and foodservice channel development represents the highest-margin emerging opportunity, with specialty coffee chains and restaurant groups actively sourcing barista-quality oat and almond milk. Manufacturers developing foodservice-grade plant-based milk formats access premium institutional pricing with lower retail competition intensity.

Investment Themes

- Local Raw Material Procurement Infrastructure: Building domestic oat, almond, and soy procurement networks in Punjab, Rajasthan, and Maharashtra reduces import dependency and enables cost-competitive pricing for mass-market penetration, the single largest barrier to plant-based milk adoption in India.

- Quick-Commerce and Subscription Model Investment: The rapid growth of Swiggy Instamart, Blinkit, and Zepto creates a significant low-capex distribution channel for plant-based milk brands, enabling national reach without cold-chain capital investment and building recurring subscription revenue.

Future Market Outlook (2026-2034)

The India plant-based milk market is projected to grow from USD 857.7 Million in 2025 to USD 1,828.0 Million by 2034, delivering an 8.33% CAGR. Growth will be driven by lactose intolerance prevalence, vegan diet expansion, D2C channel maturation, and increasing café sector demand.

The Organic segment will outpace overall market growth, approaching 30-35% category share by 2034 as clean-label awareness deepens. Flavored variants will narrow the gap with Unflavored as innovation expands consumption occasions beyond cooking into daily beverage and snacking applications.

North India will maintain regional leadership while South India accelerates through coconut-milk tradition alignment. East and Northeast India represents the highest-growth emerging opportunity as modern retail and e-commerce penetration expands into smaller cities through 2034.

Research Methodology

Primary Research

Primary research comprised structured interviews with 50+ industry stakeholders, including plant-based milk manufacturers, modern trade category managers, D2C brand founders, and food technologists advising on plant-based nutrition across India's major metropolitan markets.

Secondary Research

Secondary research encompassed FSSAI notifications on food standards, company annual reports, IMARC's proprietary food and beverage databases, India plant-based food industry association publications, and e-commerce platform sales trend analyses. Over 55 secondary sources reviewed.

Forecasting Models

Market revenue forecasts developed using bottom-up models: (i) product type volume forecasts by consumer segment; (ii) average realisation per litre by formulation and category; (iii) distribution channel penetration rates; (iv) regional consumption growth adjustment factors applied.

India Plant-Based Milk Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Products Covered | Soy Milk, Almond Milk, Coconut Milk, Rice Milk, Oat Milk, Others |

| Formulations Covered | Unflavored, Flavored |

| Categories Covered | Organic, Conventional |

| Forms Covered | Liquid, Powder |

| Distribution Channels Covered |

|

| Regions Covered | North India, West and Central India, South India, East and Northeast India |

| Companies Covered | The Hershey Company, Veganday Lifestyle Private Limited, Blue Diamond Growers, Bagrry's, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the India plant-based milk market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the India plant-based milk market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the India plant-based milk industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the India Plant-Based Milk Market Report

The India plant-based milk market reached USD 857.7 Million in 2025, driven by Unflavored formulation at 58.4%, Conventional category at 74.2%, and North India leading regionally at 28.9% through high metropolitan health-conscious consumer demand.

The market grows at 8.33% CAGR during 2026-2034, reaching USD 1,828.0 Million by 2034, reflecting rising lactose intolerance, expanding vegan adoption, D2C channel growth, and increasing product innovation in fortified and organic formulations.

Unflavored formulation dominates at 58.4% in 2025, driven by its versatility across cooking and hot beverage applications as a direct dairy substitute across household and foodservice channels throughout India.

Conventional category leads at 74.2% in 2025 through wider price accessibility and extensive retail availability. Organic is the fastest-growing category at approximately 10.2% CAGR through 2034 driven by premiumisation trends.

North India leads at 28.9% through high health awareness in Delhi NCR, strong café culture, and leading D2C and online channel penetration among India's millennial and Gen Z consumers in metropolitan cities.

Leading companies include The Hershey Company, Veganday Lifestyle Private Limited, Blue Diamond Growers, and Bagrry's, among others operating in India.

The market is projected to reach approximately USD 1,279.8 Million by 2030, driven by oat milk emergence, Organic segment growth, café channel expansion, and deepening quick-commerce distribution infrastructure across India.

Three priority opportunities: local raw material procurement infrastructure development, quick-commerce and subscription model investment for D2C brands, and café and foodservice barista-grade plant-based milk format development.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)

Related Reports

Choose your plan

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Single User License

- 1 User License, Access on 2 Devices

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- No Printing Rights

- 10% Free Report Customization

- 10–12 Weeks of Analyst Support

Five User License

- Access for 5 Users, 2 Devices per User

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- Dedicated Account Manager

- 12–14 Weeks of Analyst Support

- No Printing Rights

- 15% Free Report Customization

- 25% Discount on Your Next Purchase

Corporate User License

- Unlimited User Access (Within Your Organization)

- PDF Report + Excel Dataset

- Lifetime Access

- Dedicated Account Manager

- 14–20 Weeks of Analyst Support

- No Printing Rights

- 20% Free Report Customization

- 30% Discount on Your Next Purchase

Essential Insights

What's included:

3 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 2 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Professional Access

What's included:

5 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 8 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Business Advantage

What's included:

8 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 14 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Enterprise Intelligence

What's included:

10 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 20 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade