India Shipping Container Market Size, Share, Trends and Forecast by Product, Container Size, Application, and Region, 2026-2034

India Shipping Container Market Size, Share, Trends & Forecast (2026-2034)

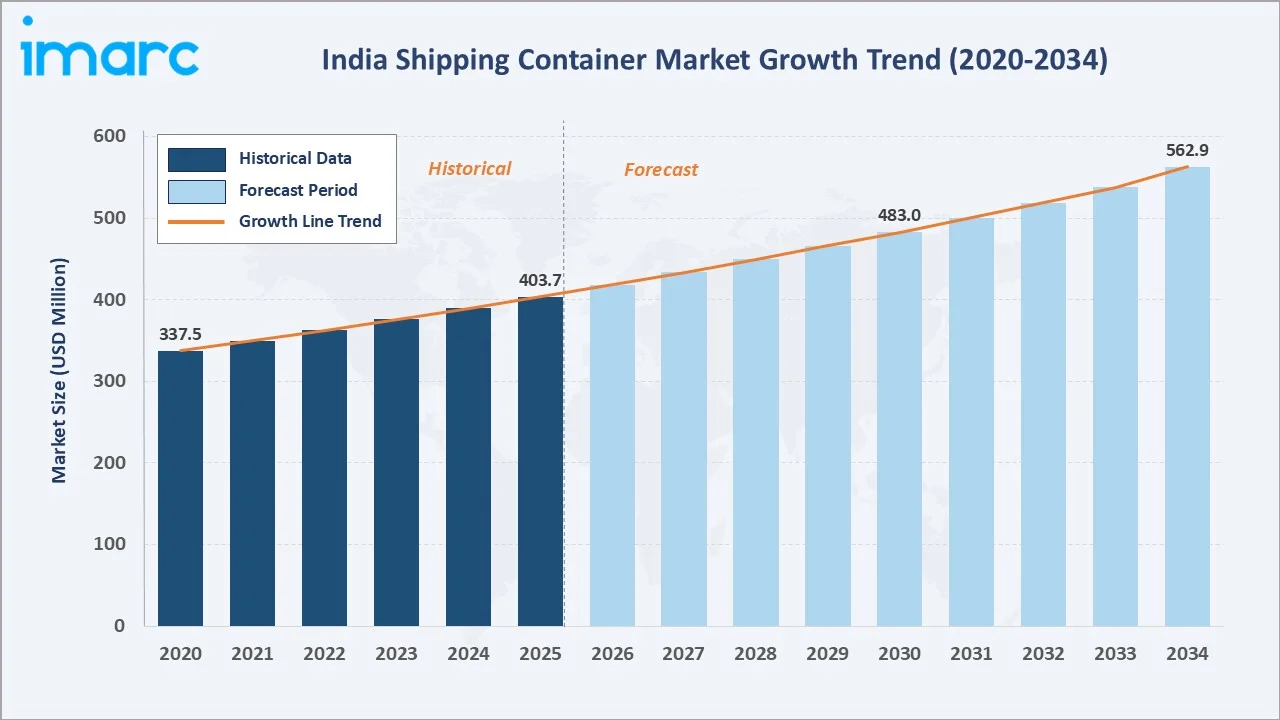

The India shipping container market reached USD 403.7 Million in 2025 and is projected to reach USD 562.9 Million by 2034, growing at a CAGR of 3.65% during 2026-2034. The increasing growth of e-commerce, rising containerized trade driven by expanding free trade agreements, large-scale port modernization under the Sagarmala Program, and the launch of the Bharat Container Shipping Line are the primary growth catalysts.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 403.7 Million |

|

Forecast Market Size (2034) |

USD 562.9 Million |

|

CAGR (2026-2034) |

3.65% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

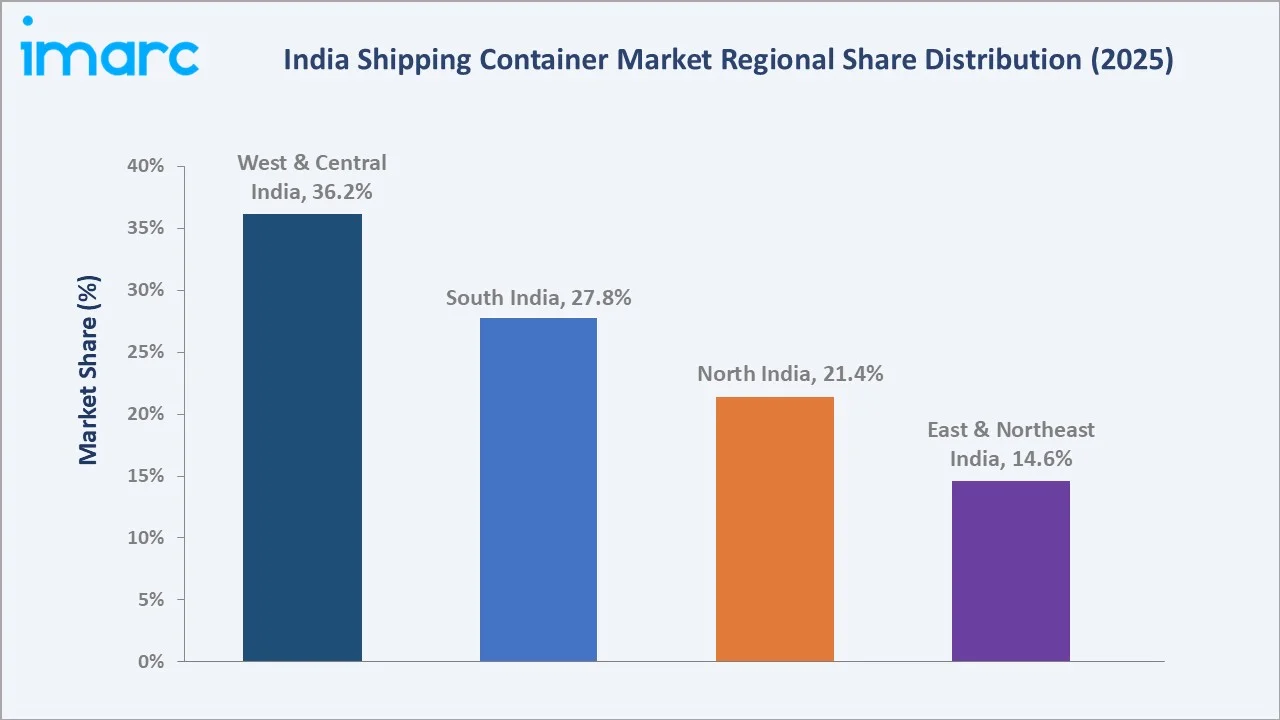

West and Central India leads regionally, holding a 36.2% market share in 2025, anchored by the Jawaharlal Nehru Port Trust (JNPT) in Mumbai, India’s largest container port handling approximately 50% of national containerized cargo. Dry storage containers command the dominant 46.8% product share, driven by their universal suitability for general cargo, manufactured goods, and consumer products across India’s primary export categories.

To get more information on this market, Request Sample

India’s shipping container market is underpinned by three structural forces: the government’s Sagarmala and PM Gati Shakti infrastructure programs accelerating port and multimodal logistics investment, India’s expanding EXIM trade facilitated by FTAs with the UAE, Australia, and EFTA nations, and the domestic container manufacturing initiative supporting import substitution. Each force independently drives container demand across product and size categories.

Executive Summary

The India shipping container market is experiencing steady, broad-based expansion driven by the convergence of rising trade volumes, port infrastructure investment, and the growth of temperature-sensitive and e-commerce logistics. The market was valued at USD 403.7 Million in 2025 and is forecast to reach USD 562.9 Million by 2034, growing at a CAGR of 3.65%.

Dry storage containers dominate with a 46.8% product share in 2025, while large containers (40 feet) hold a 44.9% size share. West and Central India lead regionally at 36.2%, driven by JNPT’s dominant throughput position. Key global and domestic players, including APPL Containers Limited, Jupiter Wagons, Retveyraaj Cargo Shipping Containers, and Dhruv Container Line Pvt. Ltd., collectively shape the competitive landscape.

Key Market Insights

|

Insight |

Data |

|

Largest Product Segment |

Dry Storage Containers – 46.8% share (2025) |

|

Fastest Growing Product Segment |

Refrigerated Containers – ~4.8% CAGR (2026-2034) |

|

Largest Container Size Segment |

Large Containers (40 feet) – 44.9% share (2025) |

|

Fastest Growing Container Size Segment |

High Cube Containers – ~4.5% CAGR (2026-2034) |

|

Leading Region |

West and Central India – 36.2% share (2025) |

|

Top Companies |

APPL Containers Limited, Jupiter Wagons, Retveyraaj Cargo Shipping Containers, and Dhruv Container Line Pvt. Ltd. |

Key Analytical Observations Supporting the Above Data:

- Dry storage containers’ 46.8% share (2025) reflects India’s export mix dominated by engineered goods, textiles, chemicals, and pharmaceuticals, all standard-cargo categories best served by 20TEU and 40TEU general-purpose containers.

- Large 40-foot containers’ 44.9% share (2025) reflects the global shift toward high-volume, per-TEU cost-optimized container logistics. Indian shippers increasingly prefer 40-foot units for general cargo, automotive parts, and consumer goods exports, reducing the total number of container movements required per shipment.

- Refrigerated containers’ fastest-growth trajectory (~4.8% CAGR) is driven by India’s growing seafood, pharmaceutical, and perishable food export sectors. India is the world’s second-largest seafood exporter and a major pharmaceutical exporter, both categories requiring temperature-controlled container logistics that are growing faster than the broader dry container segment.

- West and Central India’s 36.2% share (2025) reflects Mumbai’s dominance as India’s primary container gateway, with JNPT handling the majority of India’s containerized exports and imports. Maharashtra and Gujarat’s concentration of pharmaceutical, chemical, and engineering exports further reinforces the region’s container demand leadership.

India Shipping Container Market Overview

Shipping containers are standardized, reusable steel boxes used for the intermodal transport of goods across sea, rail, and road networks. In India, the market encompasses the procurement, leasing, and operation of dry storage containers, refrigerated (reefer) containers, flat rack containers, special purpose containers, and others, serving applications from general merchandise and automotive to pharmaceutical and perishable cargo.

Macroeconomic drivers include India’s merchandise exports targeting USD 2 Trillion by 2030-31, the Ministry of Ports, Shipping and Waterways’ Sagarmala Program targeting INR 5.48 Lakh Crore in port and logistics investment, and the PM Gati Shakti National Master Plan providing multimodal infrastructure connectivity to 35 major ports. India’s container handling capacity is targeted to reach 40 million TEUs by 2030, directly driving demand for container procurement and leasing.

Market Dynamics

To evaluate market opportunities, Request Sample

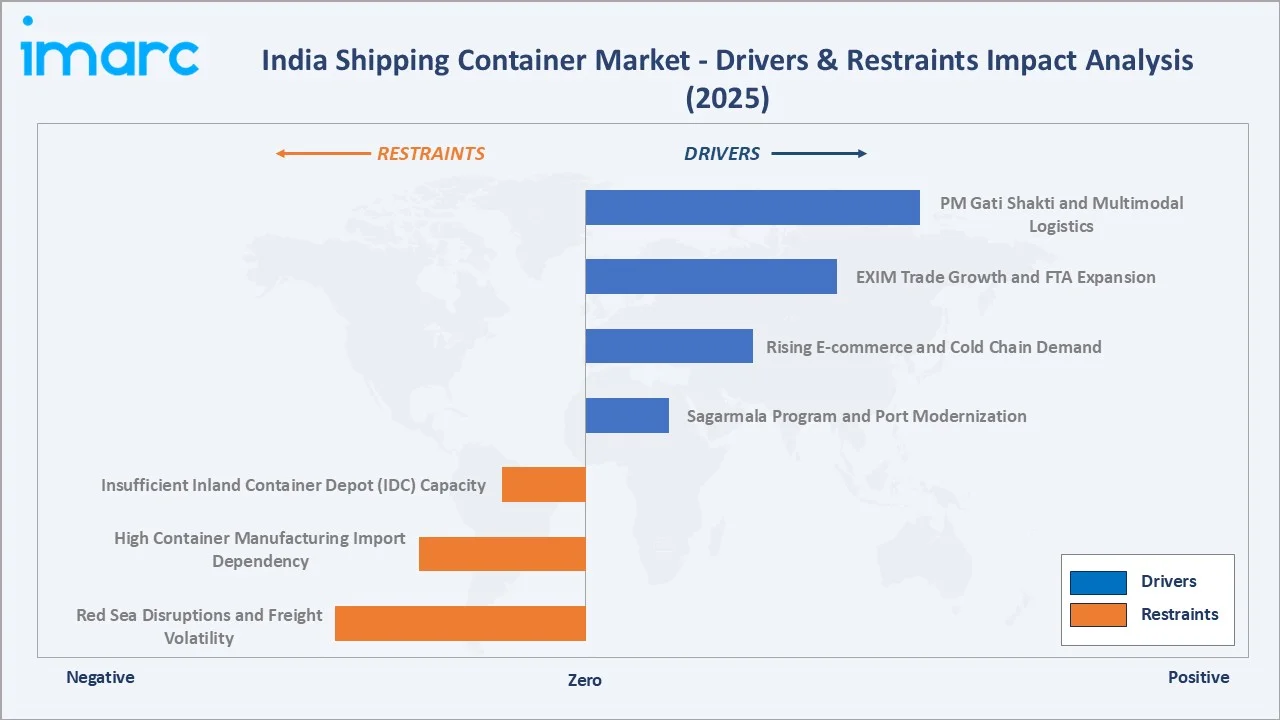

Market Drivers

- Sagarmala Program and Port Modernization: India’s Sagarmala Program has committed INR 5.48 Lakh Crore to port development, port-led industrialization, and coastal community development through 2035. Capacity additions at JNPT (targeting 10+ million TEUs capacity), Mundra, Visakhapatnam, and Kattupalli directly expand the physical infrastructure for container handling and storage, creating sustained demand for container procurement.

- Rising E-commerce and Cold Chain Demand: India’s e-commerce market, projected to reach USD 280-300 Billion by 2030, requires efficient last-mile and cross-border container logistics. Cold chain demand, driven by seafood, pharmaceutical, and dairy export growth, is accelerating the adoption of refrigerated containers and specialized container leasing programs.

- EXIM Trade Growth and FTA Expansion: India’s containerized trade recorded a 13% export and 20% import surge in 2025. New FTAs with the UAE, Australia, and the EFTA bloc, alongside ongoing negotiations with the EU and UK, are projected to further accelerate containerized trade volumes.

- PM Gati Shakti and Multimodal Logistics: National master plan coordinates port, rail, and road infrastructure connectivity, reducing India’s logistics cost from approximately 13–14% of GDP toward the government’s target of 8–9%. Improved multimodal infrastructure directly enhances container utilization efficiency and reduces dwell time, making containerized logistics more cost-competitive versus bulk transport alternatives.

Market Restraints

- High Container Manufacturing Import Dependency: India imports approximately 70-80% of its container requirements from China, making domestic operators vulnerable to CNY/INR currency movements, Chinese production cycles, and global container supply imbalances.

- Red Sea Disruptions and Freight Volatility: Geopolitical disruptions in the Red Sea since late 2023 have forced vessel operators to reroute via the Cape of Good Hope, adding 10–14 days to Europe-India transit times and creating container equipment shortages at key Indian ports.

- Insufficient Inland Container Depot (ICD) Capacity: India’s ICD network, serving inland origins and destinations that lack direct port connectivity, remains underdeveloped relative to the country’s geographic size and manufacturing concentration in landlocked regions.

Market Opportunities

- Bharat Container Shipping Line (BCSL) Launch: India launched the Bharat Container Shipping Line (BCSL) in October 2025 with an initial fleet of 51 ships and a USD 6.9 Billion investment, specifically targeting the consolidation of domestic shipping capability and reducing India’s dependence on foreign carriers for transshipment.

- Smart Container Technology Adoption: The adoption of IoT-enabled smart containers, incorporating GPS tracking, temperature and humidity sensors, shock detection, and door-open alerts, is accelerating across India’s pharmaceutical, perishable food, and high-value electronics export supply chains.

Market Challenges

- Container Imbalance and Repositioning Costs: India’s trade imbalance, with import volumes significantly exceeding exports at several major ports, creates structural container imbalances. Empty container repositioning costs India’s logistics industry around INR 12,000 crore annually, reducing the economic efficiency of container fleet management.

- Port Congestion at Major Gateways: India’s container ports, particularly JNPT and Mundra, periodically experience congestion during peak trade seasons and geopolitical freight disruptions, leading to container berth waiting times of 2–5 days and elevated detention and demurrage charges for shippers.

Emerging Market Trends

1. Smart Container Technology and IoT Integration

The integration of IoT telematics into shipping containers is transforming cargo visibility and risk management across India’s export supply chains. GPS trackers, AI-enabled anomaly detection nodes, and real-time temperature monitoring systems are being adopted across pharmaceutical, perishable food, and high-value electronics container logistics. Hapag-Lloyd standardized telematics across its entire 1.6 million unit dry and reefer fleet, creating a global smart container standard that Indian port operators and shipping lines are aligning with.

2. Refrigerated Container Expansion for Cold Chain Logistics

Marine product exports more than doubled, rising from INR 30,213 crore in 2013-14 to INR 62,408 crore in 2024-25, with 90%+ transported in refrigerated containers. Rising pharmaceutical exports (USD 28 Billion till February 2026) requiring validated cold-chain transport, growing frozen food export demand from Gulf, European, and American markets, and the expansion of India’s domestic cold chain network are collectively driving refrigerated container fleet expansion at above-market growth rates.

3. High Cube Container Adoption for E-commerce and Retail Logistics

High Cube containers, offering 30 cm greater interior height versus standard containers, are gaining adoption in India’s e-commerce, furniture, and bulky consumer goods export logistics. The 15.8% size segment share of high cube containers in 2025 is projected to grow as Indian e-commerce exporters targeting markets in the US, UK, and UAE increasingly specify High Cube units for volumetric efficiency in low-density, high-value cargo shipments.

4. Coastal Shipping Revival and Cabotage Relaxation

India’s Cabotage Policy relaxation since 2018, allowing foreign vessels to participate in India’s coastal shipping trade, combined with the Sagarmala Program’s coastal berth development investments, is reviving coastal containerized shipping as a cost-effective alternative to road and rail for domestic cargo movement.

Industry Value Chain Analysis

The India shipping container value chain spans steel raw material procurement through end-user cargo transport, with each stage characterized by specific competitive dynamics, technical standards, and regulatory frameworks.

|

Stage |

Description |

|

Raw Material Procurement |

Corten steel coils, aluminum alloys, flooring timber, and sealant compounds |

|

Container Manufacturing |

ISO-standard container production including cutting, welding, painting, and assembly; CSC (Container Safety Convention) plate installation |

|

Quality Inspection and Certification |

CSC certification, load testing, water-tightness validation, and structural inspection |

|

Port Operations and Handling |

Container stacking, crane operations, gate-in/gate-out processing, customs examination, and documentation handling |

|

Shipping and Multimodal Logistics |

Ocean liner services, inland rail movement via CONCOR and private operators, and road haulage to ICDs |

|

End-User Sectors |

Food & beverages, pharmaceuticals, consumer goods, engineered products, automotive components, textiles, and e-commerce exports & imports |

Technology Landscape in the India Shipping Container Industry

Standard ISO General Purpose Containers (20TEU and 40TEU)

Standard dry containers conforming to ISO 668 specifications, available in 20-foot (TEU) and 40-foot (FEU) configurations, represent the backbone of India’s containerized trade. These containers are constructed from Corten (weathering) steel, providing corrosion resistance, fitted with wooden hardwood or bamboo composite floors, and certified under the Container Safety Convention (CSC) for intermodal transport.

Refrigerated Container Technology (Reefers)

Modern refrigerated containers are self-powered, microprocessor-controlled units capable of maintaining cargo temperatures from -30°C to +30°C with precision of ±0.1°C. Leading reefer technology providers include Carrier Transicold, Daikin, and Thermo King, with units increasingly incorporating CA (controlled atmosphere) technology for fruit and vegetable exports. India’s pharmaceutical export logistics require 2–8°C validated cold chain containers certified under GDP (Good Distribution Practice) guidelines.

High Cube and Specialized Container Formats

High Cube (HC) containers offer 2.69- 2.89 m interior height versus 2.39 m for standard containers, enabling greater cubic volume utilization for light, bulky cargo such as furniture, garments, and packaged consumer goods. Flat rack containers, open-sided platforms suitable for over-dimensional machinery, vehicles, and project cargo, are widely used for India’s engineering equipment and capital goods export sectors.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Product |

Dry Storage Containers |

46.8% |

2025 |

|

Container Size |

Large Containers (40 feet) |

44.9% |

2025 |

|

Application |

🔒 |

🔒 |

2025 |

|

Region |

West and Central India |

36.2% |

2025 |

By Product

Dry storage containers dominate the India shipping container market with a 46.8% share in 2025. The dry container segment’s dominance reflects India’s export profile, which is heavily weighted toward non-perishable manufactured goods and agricultural commodities that do not require temperature-controlled transport.

To access detailed market analysis, Request Sample

Refrigerated containers, at 21.7%, are the fastest-growing product segment, driven by India’s world-leading seafood export sector, growing pharmaceutical exports requiring validated cold chain transport, and expanding frozen and chilled food exports to the Gulf, Europe, and North America. Flat rack containers at 14.2% serve India’s engineering equipment, automobile, and over-dimensional project cargo exports.

By Container Size

Large containers (40 feet) command a 44.9% share of India’s shipping container market in 2025, reflecting the global logistics industry’s preference for 40-foot FEU units that offer superior per-ton capacity efficiency for standard cargo. Indian shippers exporting textiles, engineering goods, and consumer products to North America and Europe predominantly use 40-foot containers, which account for the majority of JNPT, Mundra, and Chennai’s container throughput.

Small containers (20 feet), at 32.6%, remain widely used for heavy cargo including chemicals, minerals, and machinery where the weight limit of a 40-foot container would be exceeded before the volume limit is reached. High cube containers at 15.8% are the fastest-growing container size segment, driven by the expansion of e-commerce export logistics, furniture, and volumetrically bulky consumer goods shipments.

Regional Market Insights

West and Central India’s market leadership (36.2%, 2025) is underpinned by the Jawaharlal Nehru Port Trust (JNPT) in Navi Mumbai, India’s largest container port handling approximately 55–60% of national containerized cargo volume. Maharashtra’s dominant pharmaceutical, chemical, and engineering export sectors, combined with Gujarat’s Mundra port, create the country’s highest concentration of containerized trade activity.

|

Region |

Share (2025) |

Key Growth Drivers |

|

West & Central India |

36.2% |

Dominant pharmaceutical and chemical export hubs, high container throughput concentration, and significant engineering goods export activity |

|

South India |

27.8% |

Chennai Port and Kattupalli terminal serving automotive and electronics exports, Visakhapatnam for steel and project cargo, significant seafood exports from Andhra Pradesh |

|

North India |

21.4% |

Landlocked manufacturing hubs served by ICDs, significant textiles and handicrafts exports, and growing use of CONCOR’s rail-linked ICD network |

|

East & Northeast India |

14.6% |

Kolkata/Haldia port serving tea, jute, and eastern India manufacturing exports, and emerging connectivity to Southeast Asia under the Act East Policy |

South India at 27.8% is a high-growth container market, driven by Chennai’s position as India’s dominant automotive export gateway, Visakhapatnam’s growth as a major container port, and the rapid expansion of Andhra Pradesh’s seafood export sector. The state governments of Tamil Nadu, Andhra Pradesh, and Kerala are actively investing in port capacity and multimodal logistics connectivity to compete with West India’s established container dominance.

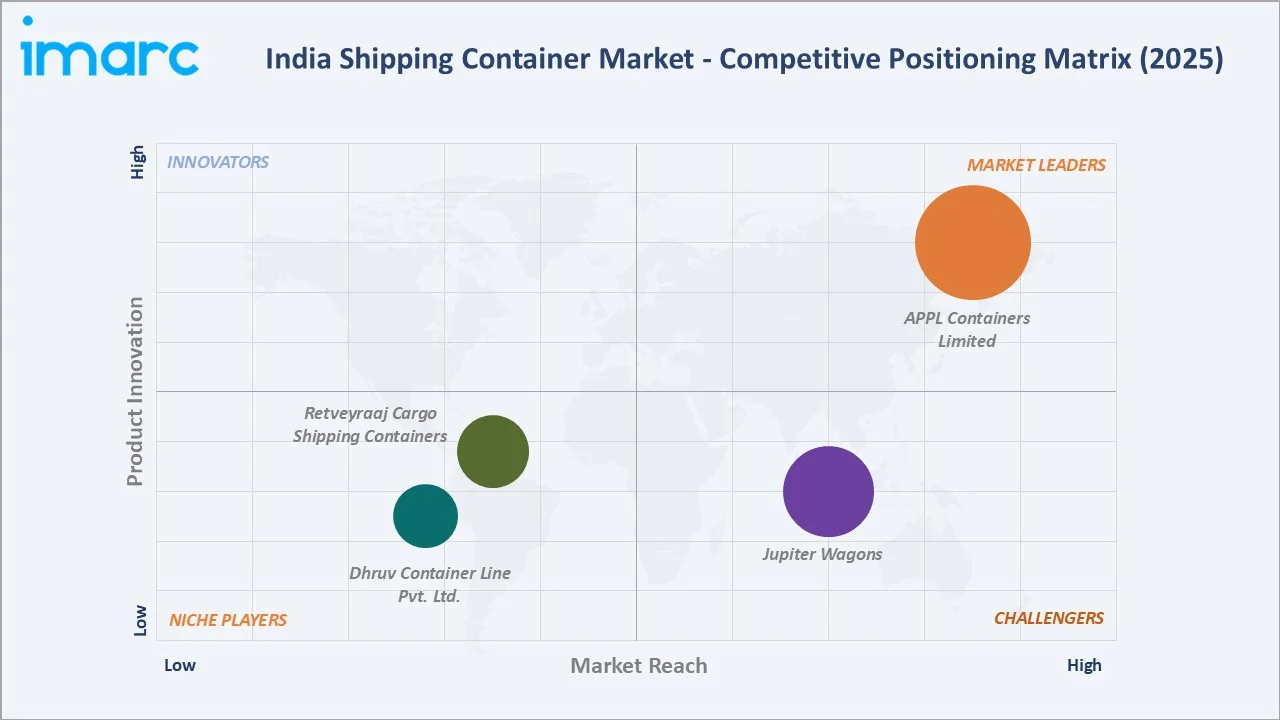

Competitive Landscape

India’s shipping container market exhibits moderate concentration, with APPL Containers Limited, Jupiter Wagons, Retveyraaj Cargo Shipping Containers, and Dhruv Container Line Pvt. Ltd. competing through port connectivity, multimodal logistics, container availability, turnaround time, and digital tracking capabilities.

|

Company Name |

Brand Name |

Market Position |

Core Strength |

|

APPL Containers Limited |

APPL Containers |

Market Leader |

Established 2021 under Make in India initiative; TUV NORD, T.I.R., and C.S.C. certified; manufacturing hub at Bhavnagar, Gujarat |

|

Jupiter Wagons |

JWL |

Challenger |

BSE-listed, headquartered in Kolkata; diversified into marine containers, refrigerated containers, and cold chain transport solutions alongside its core railway wagon business. |

|

Retveyraaj Cargo Shipping Containers |

Ritveyraaj Cargo Shipping Containers |

Niche Player |

Mumbai-based manufacturer and supplier with operations since 1970; offers specialized containers. |

|

Dhruv Container Line Pvt. Ltd. |

Dhruv Container |

Niche Player |

Uttar Pradesh-based manufacturer and supplier of cargo containers; offers customized container houses. |

Companies are increasingly investing in inland container depots, rail-linked logistics parks, refrigerated containers, and container repair and leasing services to support growing demand from agriculture, pharmaceuticals, chemicals, automotive, textiles, and marine exports.

Key Company Profiles

APPL Containers Limited

APPL Containers Limited, headquartered in Bhavnagar, Gujarat, is India's pioneering Make in India shipping container manufacturer, established in 2021 under the government's Atmanirbhar Bharat initiative.

- Product Portfolio: Standard ISO containers (10ft, 20ft, 40ft general purpose and high cube), open-top containers (20ft and 40ft), specialized containers including coil containers, lashing bin containers, both-end open containers.

- Recent Development: In February 2026, APPL Containers received SEBI approval to launch its IPO. The IPO includes a fresh issue of 12.5 lakh shares and an offer-for-sale of 25.6 lakh shares, with proceeds planned for working capital, debt repayment and general corporate purposes.

- Strategic Focus: Diversification into container leasing to build a stable recurring revenue stream alongside manufacturing; expansion of BESS container production for India's growing renewable energy and data center markets.

Jupiter Wagons

Jupiter Wagons, headquartered in Kolkata and incorporated in 1979, is a comprehensive mobility solutions manufacturer. The company operates manufacturing facilities across Kolkata, Jamshedpur, Indore, Jabalpur, Bengaluru, and Aurangabad.

- Product Portfolio: ISO marine containers (standardized 20ft and 40ft); supplies specialized containers to Adani and DP World.

- Strategic Focus: Scaling BESS container manufacturing at JEM's Indore plant from 1 GWh to 5 GWh annually by 2028; first 20ft BESS unit export to Africa (October 2025) establishing an international container export footprint.

Market Concentration Analysis

India’s shipping container market exhibits moderate concentration at the leasing and operations level, with the top players collectively holding approximately 40–50% of market revenue. Global container leasing companies (Triton International, Textainer, Seaco) collectively own approximately 40% of the world’s container fleet and supply the majority of containers deployed in Indian trade lanes through lease arrangements with Indian and global shipping lines.

Consolidation in India’s domestic container logistics segment is occurring through CONCOR’s expanding ICD and CFS network and through private sector investments in container freight stations near major port gateways.

Investment & Growth Opportunities

Fastest Growing Segments

Refrigerated containers (~4.8% CAGR), High Cube containers (~4.5% CAGR), and smart/IoT-enabled container fleet investment (~8–10% CAGR) represent the highest-growth investment vectors through 2034. Cold chain container logistics, driven by pharmaceutical and seafood export growth, offers a USD 60–70 Million incremental opportunity within the Indian market by 2034.

Emerging Market Expansion

India’s emerging port cities – Kattupalli (Tamil Nadu), Gangavaram (Andhra Pradesh), Dighi (Maharashtra), and Sagarmala greenfield ports under development – collectively represent incremental container throughput capacity of 10–12 million TEUs beyond existing gateway ports by 2034. Entry strategies for container suppliers targeting these emerging hubs include long-term supply agreements with port operators and container leasing partnerships with new regional shipping lines.

Venture and Institutional Investment Trends

- India’s Sagarmala Program port infrastructure investment pipeline of INR 5.48 Lakh Crore through 2035 includes dedicated container berth capacity additions at 12 major ports, directly translating to container procurement demand as new terminal capacity is commissioned.

- The Bharat Container Shipping Line’s USD 6.9 Billion fleet investment program, targeting 51 vessels in its initial fleet, will create substantial domestic demand for container procurement and leasing, reducing India’s dependence on foreign liner operators for transshipment cargo management.

Future Market Outlook (2026-2034)

India’s shipping container market is positioned for sustained, above-GDP-growth expansion through 2034. From a base of USD 403.7 Million in 2025, the market is projected to reach USD 562.9 Million by 2034, representing incremental value creation of USD 159.2 Million at a CAGR of 3.65%. This trajectory is structurally supported by India’s merchandise export ambition targeting USD 2 Trillion by 2030, the government’s massive port and logistics infrastructure investment program, and the progressive localization of container manufacturing under Atmanirbhar Bharat.

The technology transition toward smart, IoT-enabled container fleets will define the market’s composition by 2034. Cold chain container demand, driven by pharmaceutical and seafood exports, will grow faster than the overall market. The launch of BCSL and the maturation of India’s domestic container manufacturing ecosystem could structurally reduce the country’s import dependency for containers, improving supply chain resilience.

Research Methodology

Primary Research

Primary research comprised structured interviews with over 100 industry participants in 2024–2025, including container shipping line operators, leasing companies, port terminal operators, ICD and CFS operators, customs clearing agents, and institutional investors across India, Singapore, and China.

Secondary Research

Secondary research encompassed company annual reports, Ministry of Ports, Shipping and Waterways data, JNPT and major port trust annual reports, Shipping Corporation of India disclosures, DGFT trade data, Indian Ports Association statistics, and trade publications including Lloyd’s List, Journal of Commerce, and Container News.

Forecasting Models

Market size estimations were derived using top-down and bottom-up forecasting, incorporating India’s containerized trade volume growth rates, average container procurement and leasing values, fleet utilization and replacement cycles, and port capacity expansion timelines. A base-case CAGR of 3.65% reflects consensus estimates validated against EXIM trade data and port throughput indicators from 2020 to 2025.

India Shipping Container Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Products Covered | Dry Storage Containers, Flat Rack Containers, Refrigerated Containers, Special Purpose Containers, Others |

| Container Sizes Covered | Small Containers (20 feet), Large Containers (40 feet), High Cube Containers, Others |

| Applications Covered | Food and Beverages, Consumer Goods, Healthcare, Industrial Products, Vehicle Transport, Others |

| Regions Covered | North India, West and Central India, South India, East and Northeast India |

| Companies Covered | APPL Containers Limited, Jupiter Wagons, Retveyraaj Cargo Shipping Containers, Dhruv Container Line Pvt. Ltd., etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the India shipping container market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the India shipping container market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the India shipping container industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the India Shipping Container Market Report

The India shipping container market reached USD 403.7 Million in 2025 and is projected to reach USD 562.9 Million by 2034.

The market is expected to grow at a CAGR of 3.65% during 2026-2034, driven by rising EXIM trade volumes, port modernization, cold chain logistics expansion, and the launch of the Bharat Container Shipping Line.

West and Central India leads with a 36.2% share in 2025, anchored by JNPT in Navi Mumbai and Mundra port in Gujarat, which together handle the majority of India’s containerized trade.

Dry storage containers dominate with a 46.8% share in 2025, serving the majority of India’s general merchandise exports including textiles, chemicals, engineering goods, and consumer products.

Large containers (40 feet) hold the largest share at 44.9%, driven by the global logistics preference for 40-foot FEU units that offer superior per-ton capacity efficiency for standard dry cargo.

Key players include APPL Containers Limited, Jupiter Wagons, Retveyraaj Cargo Shipping Containers, and Dhruv Container Line Pvt. Ltd.

Refrigerated containers are growing at approximately 4.8% CAGR because India’s seafood export sector (the world’s second-largest), expanding pharmaceutical cold chain logistics, and growing frozen food exports.

Key challenges include high import dependency on Chinese-manufactured containers (approximately 95%), Red Sea geopolitical disruptions creating freight volatility, and container imbalance between import-surplus and export-intensive ports.

The BCSL, launched in October 2025 with an initial fleet of 51 ships and a USD 6.9 Billion investment, is strategically significant as it aims to consolidate India’s domestic shipping capability and reduce dependence on foreign carriers.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)