India Soft Skills Training Market Size, Share, Trends and Forecast by Soft Skill Type, Channel Provider, Sourcing, Delivery Mode, End Use Industry, and Region, 2026-2034

India Soft Skills Training Market Size, Share, Trends & Forecast (2026-2034)

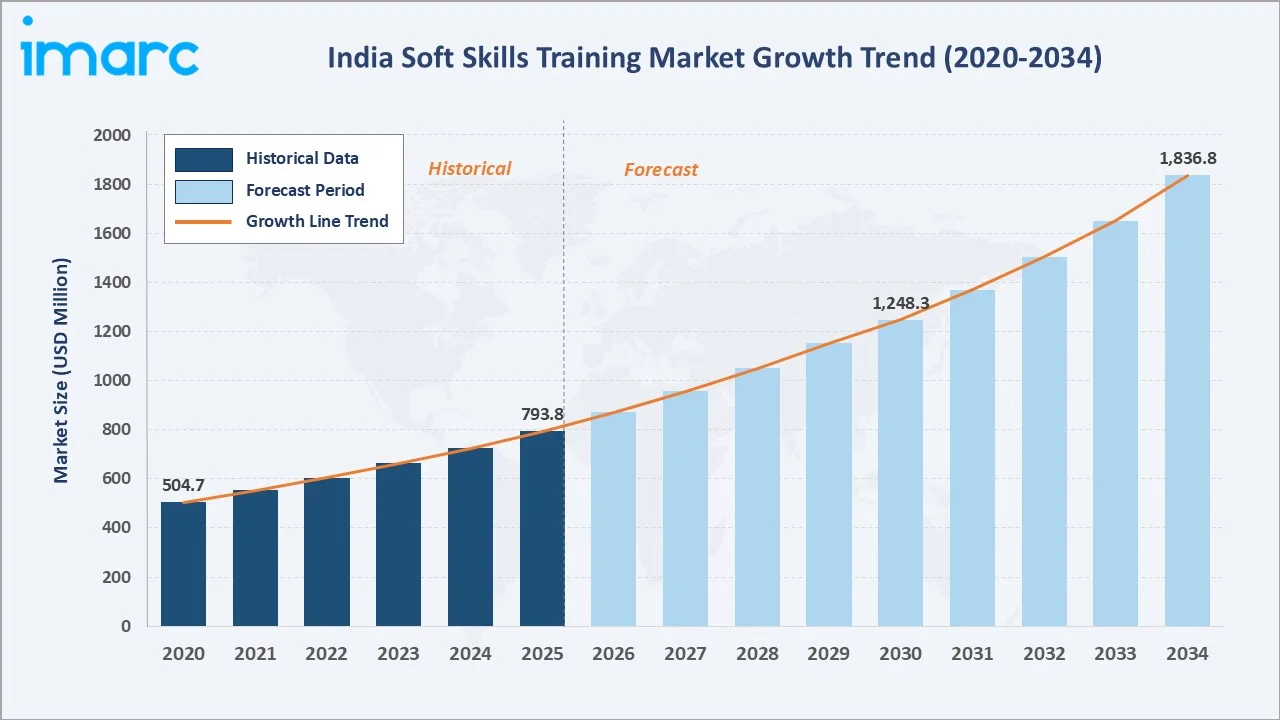

The India soft skills training market size reached USD 793.8 Million in 2025 and is projected to reach USD 1,836.8 Million by 2034, exhibiting a CAGR of 9.48% during 2026-2034. Growing corporate investment in holistic employee development, rapid SME expansion, and increasing adoption of technology-enabled learning platforms are the primary forces driving market growth.

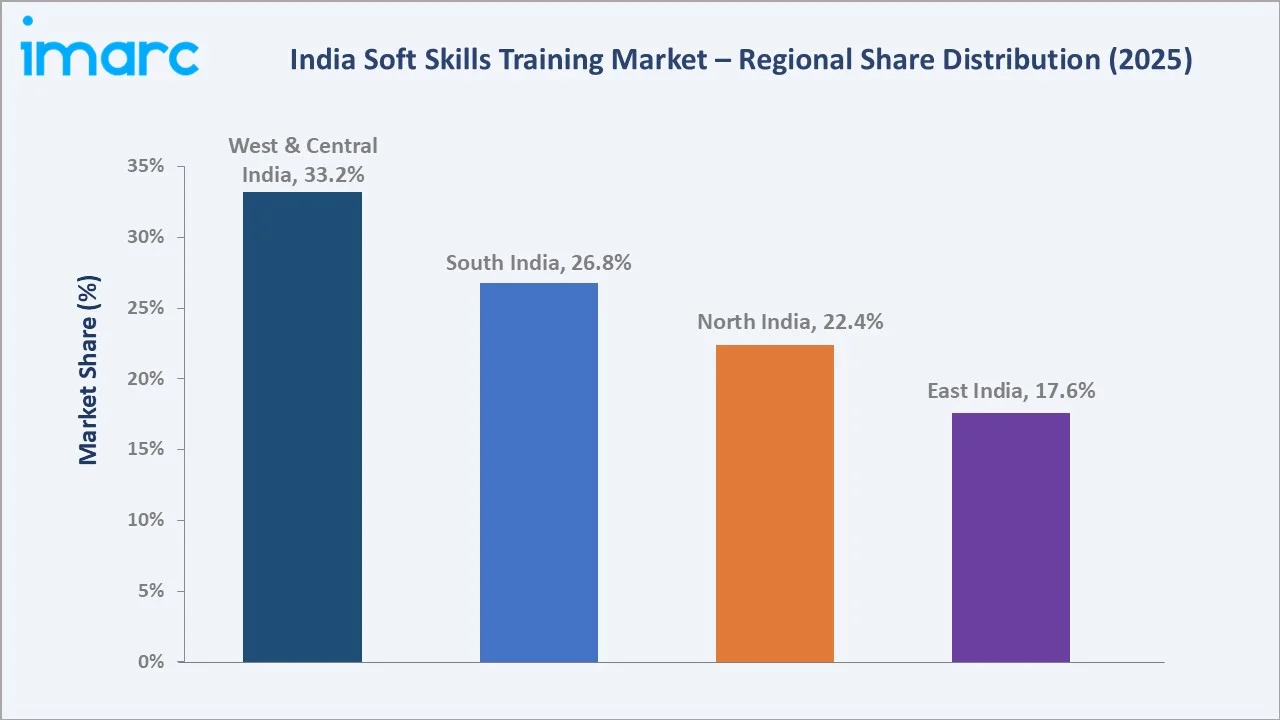

Outsourced training dominates the sourcing segment at 61.3% in 2025, while offline delivery leads at 57.8%. West and Central India commands a dominant 33.2% regional share, reflecting its concentration of corporate headquarters, BFSI institutions, and manufacturing hubs.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 793.8 Million |

|

Forecast Market Size (2034) |

USD 1,836.8 Million |

|

CAGR (2026-2034) |

9.48% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

West & Central India (33.2% share, 2025) |

|

Second Largest Region |

South India (26.8% share, 2025) |

|

Leading Sourcing Mode |

Outsourced (61.3%, 2025) |

|

Leading Delivery Mode |

Offline (57.8%, 2025) |

The India soft skills training market growth trajectory from 2020 through 2034, with the historical expansion from USD 504.7 Million in 2020 to USD 793.8 Million in 2025, reflects consistent workforce development demand, while the forecast to USD 1,836.8 Million captures accelerating EdTech adoption, AI-powered learning integration, and rapid SME professionalization across all four regions of India.

To get more information on this market, Request Sample

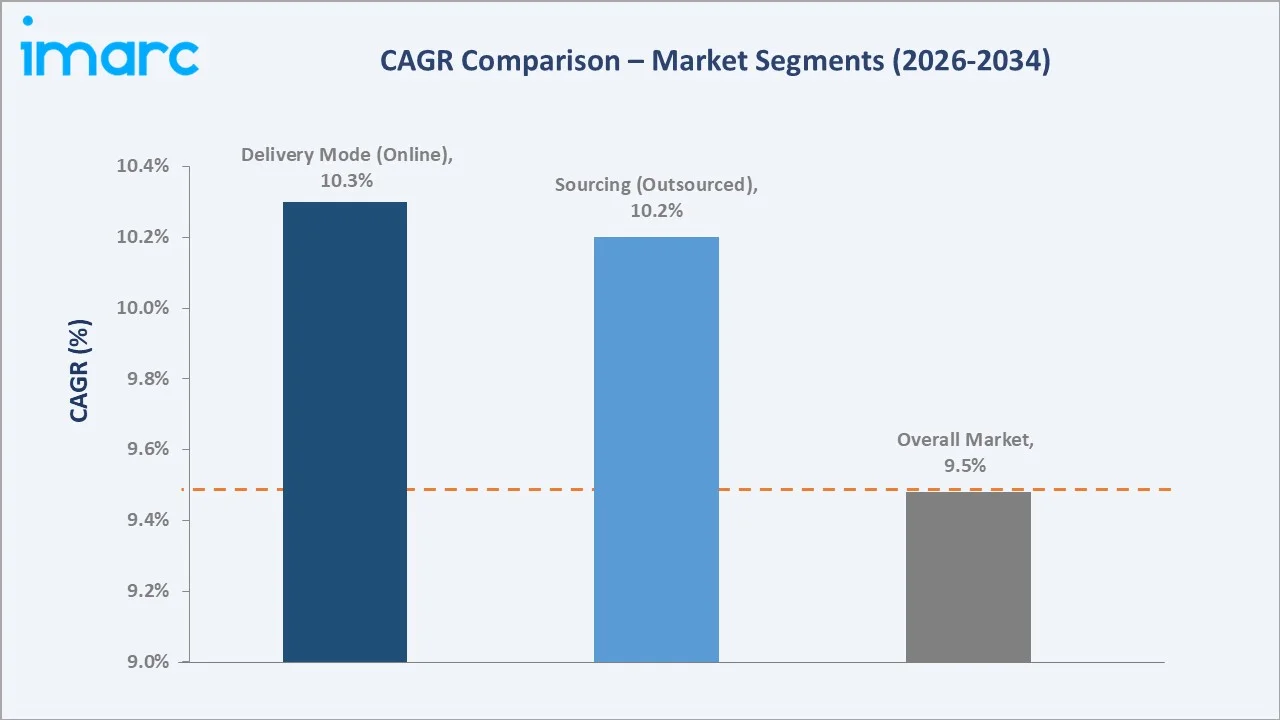

The CAGR trajectories across key sourcing, delivery mode, and regional sub-segments, with online delivery at ~10.3% CAGR and outsourced training at ~10.2% CAGR, are the fastest-growing categories within the India soft skills training industry analysis through 2034.

Executive Summary

The India soft skills training market is on a sustained growth trajectory from USD 793.8 Million in 2025 to USD 1,836.8 Million by 2034. Soft skills training, encompassing communication, leadership, teamwork, and interpersonal effectiveness, has transitioned from a discretionary HR expenditure to a core strategic workforce investment across Indian enterprises.

Outsourced training dominates the sourcing segment at 61.3% in 2025, reflecting the preference among corporate clients for specialist external providers offering globally benchmarked curricula, certified facilitators, and scalable delivery frameworks. In-house training (38.7%) remains significant among large enterprises with mature L&D infrastructure and proprietary competency models.

Offline delivery leads at 57.8% in 2025, driven by the demonstrated effectiveness of face-to-face experiential learning in developing interpersonal and behavioral competencies. Online delivery (42.2%) is growing at ~10.3% CAGR through 2034, driven by enterprise demand for flexible and scalable training across distributed workforces.

West and Central India dominates at 33.2% in 2025, anchored by Mumbai's financial services concentration, Pune's manufacturing and IT clusters, and Ahmedabad's expanding corporate sector. South India (26.8%) is the second-largest region driven by Bengaluru's IT and GCC ecosystem.

Key Market Insights

|

Insight |

Data |

|

Leading Sourcing Mode |

Outsourced – 61.3% share (2025) |

|

Leading Delivery Mode |

Offline – 57.8% share (2025) |

|

Leading Region |

West & Central India – 33.2% share (2025) |

|

Second Largest Region |

South India – 26.8% share (2025) |

|

Top Companies |

Dale Carnegie & Associates Global, Inc., Pearson, Momentum Training Solutions, Franklin Covey Co. |

Key Analytical Observations Expanding on the Above Data:

- Outsourced training, with 61.3% in 2025, dominates because specialist providers bring globally benchmarked curricula, certified trainers, and proprietary competency frameworks that are difficult to replicate in-house, particularly for SMEs and mid-sized organizations lacking dedicated L&D functions.

- Offline delivery, with 57.8% in 2025, leads because behavioural skill development, leadership presence, conflict resolution, public speaking, benefits most from real-time facilitator feedback, role-play simulation, and group dynamics that digital platforms cannot fully replicate.

- West and Central India’s 33.2% dominance in 2025reflects India’s financial and manufacturing capital concentration in Maharashtra, hosting the highest density of BFSI, retail, and manufacturing employers with structured annual training budgets.

- South India, with 26.8% in 2025, benefits from Bengaluru’s status as India’s IT capital and the rapid expansion of GCC and technology services ecosystems across Chennai and Hyderabad, which are major consumers of communication and leadership programs.

India Soft Skills Training Market Overview

Soft skills training programs are structured learning interventions designed to develop non-technical competencies including communication, leadership, teamwork, emotional intelligence, time management, and critical thinking. Programs are delivered through instructor-led classroom sessions, virtual instructor-led training (VILT), e-learning modules, experiential workshops, and blended learning formats tailored to corporate, academic, and government segments.

The Indian market ecosystem integrates international training methodology providers, domestic corporate training specialists, EdTech platforms, academic institutions, and government-sponsored skill development initiatives under the National Skill Development Corporation (NSDC) framework, serving corporate enterprises, SMEs, and government departments across all major industries.

Market Dynamics

To evaluate market opportunities, Request Sample

Market Drivers

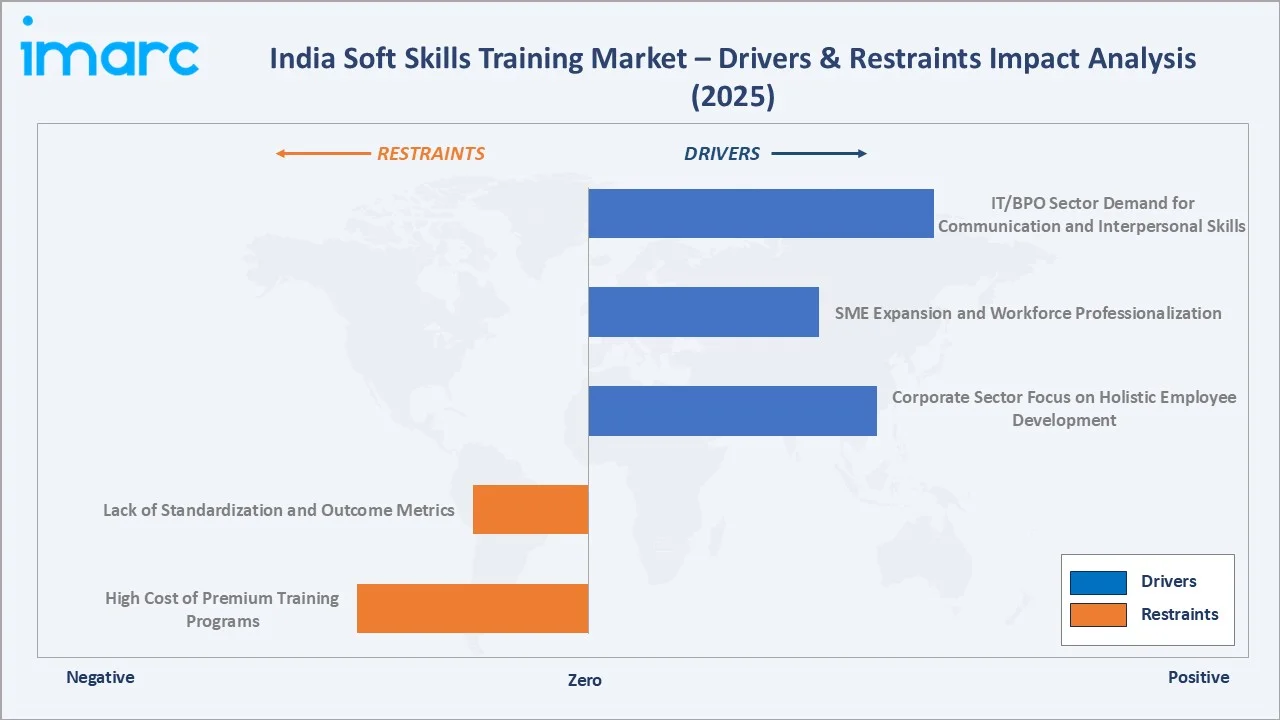

- Corporate Sector Focus on Holistic Employee Development: The shifting priorities of Indian enterprises toward comprehensive workforce effectiveness beyond technical skills is the primary structural driver. Large corporations across BFSI, IT, retail, and manufacturing sectors have institutionalized annual soft skills training budgets targeting communication excellence, leadership pipeline development, and client management capabilities.

- SME Expansion and Workforce Professionalization: India’s estimated 63 million SMEs are increasingly adopting structured training programs as they scale operations, compete for professional talent, and target institutional clients requiring certified workforce capabilities. Government’s Skill India Mission directs targeted funding toward SME workforce development programs.

- IT/BPO Sector Demand for Communication and Interpersonal Skills: India’s IT services and BPO sector, employing over five million professionals, requires advanced English communication, client management, and cross-cultural effectiveness programs, creating the largest concentrated demand pool for soft skills training in any single Indian industry vertical.

Market Restraints

- High Cost of Premium Training Programs: Globally benchmarked soft skills training programs often involve substantial per-participant investments, creating budget constraints for many mid-sized and growing organizations, especially where measuring and demonstrating training ROI remains challenging.

- Lack of Standardization and Outcome Metrics: The absence of a universally recognized national soft skills certification framework creates difficulty in benchmarking program quality, measuring skill transfer to job performance, and justifying training expenditure, limiting budget approvals in cost-conscious organizations.

Market Opportunities

- AI and Technology-Augmented Learning: The integration of AI-powered coaching bots, natural language processing for communication feedback, VR-based scenario simulations, and adaptive learning algorithms is creating scalable, personalized soft skills training products. These solutions address cost and scalability constraints of instructor-led training for mass deployment across geographically distributed workforces.

- Government Skill Development Programs: NSDC and Skill India Digital platform initiatives are expanding the addressable market for soft skills training to non-corporate segments, including frontline workers, school and college graduates, and rural youth, creating new B2G revenue streams for established training providers.

Market Challenges

- Demonstrating Measurable ROI: Quantifying the business impact of soft skills training on productivity, employee retention, and revenue generation remains methodologically challenging, making it difficult for L&D professionals to defend training investments against competing capital allocation priorities during budget cycles.

- Trainer Quality and Scalability at Scale: Delivering consistent, high-quality behavioral training requires certified facilitators with deep domain expertise and experiential backgrounds, creating a talent bottleneck as the market grows and constraining capacity expansion among established providers.

Emerging Market Trends

1. AI-Powered Personalized Learning Transforming Soft Skills Development

Artificial intelligence is enabling real-time, individualized feedback on communication patterns, presentation delivery, and interpersonal interactions. AI coaching platforms analyze speech, word choice, and tone, generating personalized improvement recommendations that accelerate skill development beyond periodic classroom interventions.

2. Gamification and Experiential Learning Driving Higher Engagement

Gamified learning platforms incorporating scenario-based challenges, peer competitions, and point systems demonstrate significantly higher completion rates and knowledge retention than traditional e-learning, driving rapid corporate adoption across large enterprises seeking measurable training engagement outcomes.

3. Outcome-Linked Training Contracts Emerging in Enterprise Segment

Large enterprises are structuring soft skills training contracts with performance-based outcome clauses linking trainer compensation to measurable post-training behavioral improvements, reducing customer churn, or improvements in employee engagement scores, shifting commercial models toward shared accountability.

4. Vernacular Language Training Unlocking Tier-2 and Tier-3 Markets

Providers offering soft skills programs in Hindi, Tamil, Telugu, Marathi, and other regional languages are accessing previously underserved markets of mid-level professionals and frontline workers outside metropolitan centers, significantly expanding total addressable markets beyond English-medium instruction.

Industry Value Chain Analysis

The soft skills training value chain spans six stages from content development through individual learner outcome measurement. Delivery and facilitation capture the highest value-add margins, while technology platform development and outcome assessment represent the fastest-growing value-capture opportunities as enterprise buyers demand demonstrable learning effectiveness.

|

Stage |

Description |

|

Content Development |

Design and production of soft skills curricula, assessments, facilitator guides, and digital learning assets aligned with industry competency frameworks. |

|

Platform & Technology |

Cloud-based LMS, mobile learning applications, VR simulation tools, and AI coaching platforms enabling scalable digital delivery and learner progress tracking. |

|

Training Delivery |

Instructor-led classroom, virtual instructor-led training (VILT), blended learning, and self-paced e-learning delivered by certified facilitators across corporate and academic segments. |

|

L&D Departments |

Corporate HR and L&D functions managing training needs analysis, program procurement, scheduling, participant management, and training effectiveness measurement. |

|

Assessment & Certification |

Pre- and post-training competency assessments, skill gap measurement, certification of completion, and integration with HRMS performance management systems. |

|

Regulatory Framework |

National Skill Development Corporation (NSDC), Ministry of Skill Development & Entrepreneurship, Sector Skill Councils, and UGC guidelines governing vocational and professional training standards. |

Technology Landscape in the India Soft Skills Training Industry

Learning Management Systems and Digital Delivery Platforms

Cloud-based LMS platforms have become the infrastructure backbone of corporate soft skills training programs in India, enabling centralized program administration, learner progress tracking, content management, and performance analytics. Mobile-first LMS designs support self-paced micro-learning modules deliverable across smartphones, addressing India’s high mobile internet penetration across all regions.

Virtual Reality and Immersive Simulation Technologies

VR-based simulations are enabling learners to practice high-stakes behavioral scenarios including difficult conversations, public speaking, and conflict resolution in psychologically safe virtual environments. Early enterprise adopters in India’s IT and BFSI sectors report measurable improvements in learning transfer rates compared to traditional role-play exercises with manual facilitator feedback.

Artificial Intelligence Coaching and Conversational Assessment

AI-powered speech analytics tools that analyze tone, vocabulary, pace, and filler word usage enable objective, scalable communication skills assessment. These tools, integrated with video-based practice platforms, provide immediate and specific feedback that accelerates skill development in communication, presentation, and interview readiness programs across large enterprise deployments.

Blended Learning Architecture and Microlearning Design

The dominant delivery architecture for enterprise soft skills training is evolving toward structured blended learning combining short online video modules, virtual group coaching sessions, peer learning cohorts, and periodic in-person experiential workshops, optimizing learning effectiveness against the time constraints of working professionals across all Indian metro centers.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Soft Skill Type |

🔒 |

🔒 |

2025 |

|

Channel Provider |

🔒 |

🔒 |

2025 |

|

Sourcing |

Outsourced |

61.3% |

2025 |

|

Delivery Mode |

Offline |

57.8% |

2025 |

|

End Use Industry |

🔒 |

🔒 |

2025 |

|

Region |

West and Central India |

33.2% |

2025 |

By Sourcing

Outsourced training commands a 61.3% majority share in 2025, reflecting the fundamental preference among Indian organizations for specialist external providers who deliver internationally validated competency frameworks, certified facilitators with deep domain experience, and scalable delivery capabilities that in-house teams cannot economically match.

To access detailed market analysis, Request Sample

In-house training at 38.7% in 2025 remains a significant and resilient segment, serving primarily large enterprises with established L&D functions, dedicated internal trainers, and proprietary organizational competency models. Large technology and services companies maintain extensive internal training academies delivering standardized soft skills programs to large workforces cost-effectively at enterprise scale.

By Delivery Mode

Offline delivery dominates at 57.8% in 2025, reflecting the established preference for face-to-face learning environments in behavioral skills development. Instructor-led classroom programs create immersive learning spaces where facilitators can observe body language, provide real-time coaching, and generate interpersonal dynamics essential for practicing leadership, negotiation, and communication competencies.

Online delivery at 42.2% in 2025 is the fastest-growing segment at ~10.3% CAGR through 2034, driven by corporate demand for scalable, cost-efficient learning solutions deployable across geographically distributed workforces without travel and venue costs. The pandemic permanently accelerated VILT and e-learning adoption, demonstrating that effective soft skills development can be achieved through well-designed digital channels.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

|

West & Central India |

33.2% |

BFSI concentration; manufacturing hubs; corporate HQs; Mumbai, Pune, Ahmedabad metros |

|

South India |

26.8% |

IT and GCC ecosystem; Bengaluru, Hyderabad, Chennai tech sectors; communication skills demand |

|

North India |

22.4% |

Delhi NCR corporates; retail and FMCG; government enterprises; expanding manufacturing base |

|

East India |

17.6% |

Kolkata BFSI; emerging IT hubs; manufacturing sector growth; rising SME adoption of training |

West and Central India’s 33.2% market dominance in 2025 reflects its position as India’s financial and manufacturing capital. Mumbai hosts India’s largest concentration of BFSI employers, while the Pune-Mumbai corridor anchors automotive, pharmaceutical, and IT services clusters, each sector generating structured annual soft skills training demand. Maharashtra’s high corporate density means training providers consistently generate their highest per-region revenues here.

South India, with 26.8% in 2025, is driven by Bengaluru’s position as India’s technology capital and the highest concentration of IT professionals in the country. Communication, leadership, and cross-cultural effectiveness programs are mandatory components of GCC workforce development strategies, creating deep and recurring demand from employers across the region.

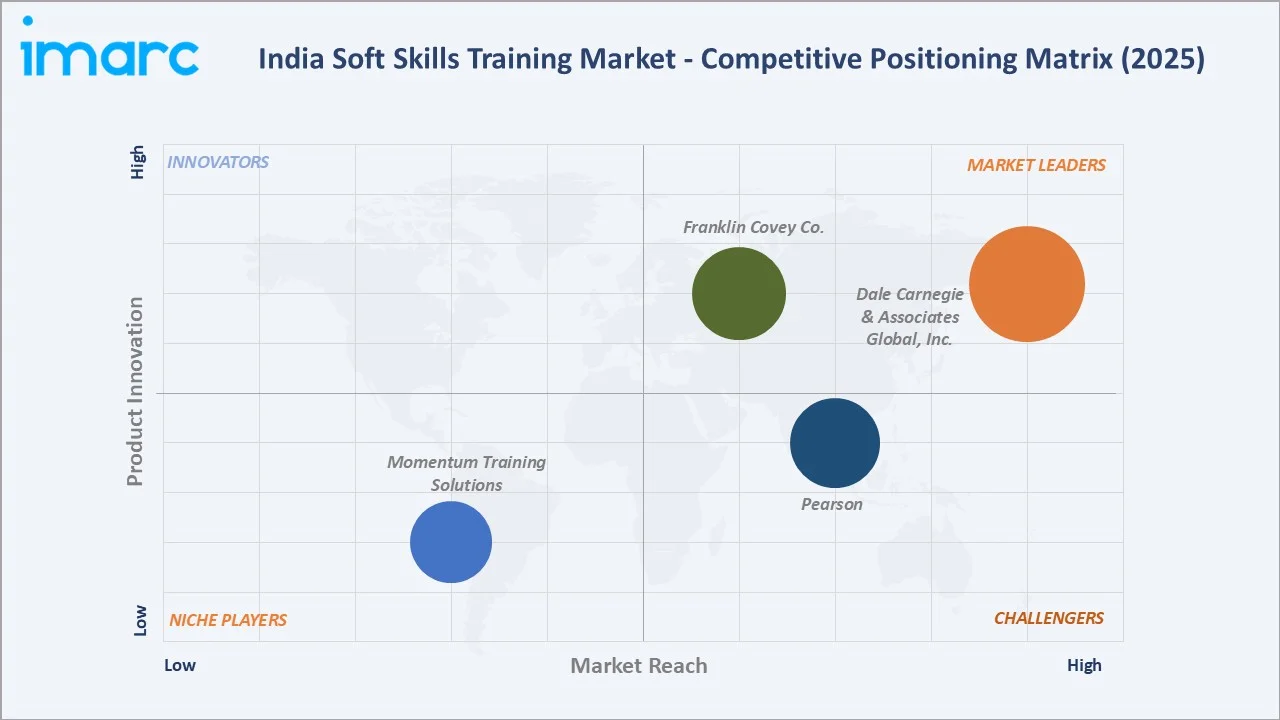

Competitive Landscape

The India soft skills training market is moderately fragmented, with international training brands holding strong positions in premium corporate segments while domestic specialists serve mid-market and government-linked clients.

|

Company Name |

Key Programs |

Market Position |

India Strategic Focus |

|

Dale Carnegie & Associates Global, Inc. |

Public Speaking, Leadership, Sales Effectiveness, People Skills |

Leader |

Premium corporate; leadership and communication programs; metro-focused delivery |

|

Pearson |

Business Communication, English Skills, Professional Development |

Challenger |

Academic-to-corporate pipeline; assessment-linked certification programs |

|

Momentum Training Solutions |

Soft Skills Training, Behavioural Training, Leadership Training, Executive Coaching |

Niche |

Customised experiential interventions for India corporates; mid-market and MNC clients |

|

Franklin Covey Co. |

7 Habits, 4 Disciplines of Execution, Leading at the Speed of Trust |

Leader |

Senior leadership; organizational culture transformation; productivity frameworks |

Key players include Dale Carnegie & Associates Global, Inc., Pearson, Momentum Training Solutions, Franklin Covey Co., and others.

Key Company Profiles

Dale Carnegie & Associates Global, Inc.

Dale Carnegie & Associates is a global leader in professional and organizational development, operating in India through a licensed training partner network with over a century of expertise in communication, interpersonal effectiveness, and sales performance training. Its programs serve senior corporate professionals across Mumbai, Delhi, Bengaluru, and other major Indian metropolitan centers.

- Product Portfolio: Offers public speaking, leadership, sales effectiveness, people skills, and others.

- Recent Developments: In September 2024, Dale Carnegie Training expanded its presence in India with the launch of a new franchise in Gujarat. The move is aimed at strengthening access to leadership, communication, and workplace effectiveness programs for businesses and professionals across the region. The expansion reflects rising demand for corporate learning and soft skills development in emerging business hubs.

- Strategic Focus: Dale Carnegie’s strategy maintains premium brand positioning in India’s corporate market through globally benchmarked programs delivered by certified trainers, targeting C-suite and senior management development where its century-old methodology and global alumni network create strong preference advantages over domestic competitors.

Pearson

Pearson is one of the world’s leading lifelong learning companies headquartered in London. Pearson operates through its Workforce Skills division, delivering English communication, business communication, vocational qualifications, and assessment-linked certification programs across corporate, academic, and government segments.

- Product Portfolio: Offers business communication, English skills, professional development, and others.

- Recent Developments: In July 2025, Pearson and HCLTech announced a multi-year strategic partnership to co-develop AI-powered learning programs, workforce analytics, and career development tools for enterprises and higher education institutions in India, including a dedicated AI Innovation Lab leveraging HCLTech’s Career Shaper and AI Force platforms.

- Strategic Focus: Pearson’s strategy in the India soft skills training market centres on its unique position as both a content provider and assessment authority, creating an end-to-end academic-to-corporate pipeline through BTEC qualifications, English communication programs, and Pearson VUE certifications. The company targets the growing demand for globally recognized outcomes-linked professional credentials among India’s expanding GCC workforce, IT services professionals, and university graduates.

Market Concentration Analysis

The India soft skills training market is moderately fragmented at the national level, with no single provider commanding more than 8-10% of total market revenue. The premium corporate segment shows higher concentration among globally recognized brands, while the mid-market features intense competition among domestic training companies, independent facilitators, and EdTech platforms serving diverse price points and delivery preferences.

Consolidation in the EdTech segment is accelerating as well-funded platforms acquire specialized content libraries and boutique training companies to build comprehensive soft skills training portfolios. The overall market structure continues to favor providers combining established brand equity, certified trainer networks, outcome measurement capabilities, and robust digital delivery infrastructure.

Investment & Growth Opportunities

Fastest-Growing Segments

Online delivery at ~10.3% CAGR through 2034 is the highest-growth delivery mode, driven by enterprise demand for scalable and cost-efficient programs deployable across distributed workforces. Outsourced training at ~10.2% CAGR through 2034 represents the broadest-based growth opportunity as SME adoption of specialist training providers accelerates through the forecast period.

Emerging Markets

East India represents the most compelling emerging regional opportunity as Kolkata’s diversified economy and emerging IT hubs in Odisha and West Bengal drive first-generation professional workforce development. Northeast India’s inclusion in the national skill development agenda is also creating public-private training partnership opportunities for established providers.

Venture and Investment Trends

EdTech platforms offering AI-powered soft skills training are attracting significant venture investment, with personalized communication coaching, VR-based experiential learning, and outcome-linked corporate training platforms receiving funding rounds. Private equity interest in consolidating the fragmented mid-market training segment is growing, targeting platform acquisitions with recurring enterprise training contracts and measurable outcome data.

Future Market Outlook (2026-2034)

The India soft skills training market is forecast to expand from USD 793.8 Million in 2025 to USD 1,836.8 Million by 2034 at a CAGR of 9.48%, adding USD 1,043.0 Million in incremental annual market value over the forecast period. This robust growth reflects India’s expanding corporate workforce, rising professionalization of its 63 million SMEs, and sustained government-backed skill development investment.

Three structural forces will most significantly shape the market through 2034: AI-powered personalization enabling scalable, individualized skill development at lower per-learner costs; the expansion of GCCs requiring cross-cultural and global communication capabilities in their Indian talent pools; and the systematic professionalization of India’s SME base creating a vast new addressable market for structured soft skills training programs.

Research Methodology

Primary Research

Primary research encompassed structured interviews with corporate L&D heads, HR directors, independent training facilitators, EdTech platform executives, and sector skill council representatives across India. Primary data validated market sizing, sourcing and delivery mode segment shares, regional demand distribution, and technology adoption patterns across the training ecosystem.

Secondary Research

Key secondary sources include NASSCOM workforce and talent reports, National Skill Development Corporation (NSDC) annual reports, Ministry of Skill Development & Entrepreneurship data, CII and FICCI human capital development publications, SHRM India research, and trade journals covering corporate L&D, EdTech, and workforce development sectors in India.

Forecasting Models

Market size estimations and growth projections were derived using a combination of top-down and bottom-up forecasting models incorporating GDP growth rates, corporate workforce expansion data, SME sector growth projections, technology adoption curves, and historical training expenditure per employee benchmarks. Scenario analysis across base, optimistic, and conservative cases was performed to account for macroeconomic uncertainty.

India Soft Skills Training Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Soft Skill Types Covered | Management and Leadership, Administration and Secretarial, Communication and Productivity, Personal Development, Teamwork, Others |

| Channel Providers Covered | Corporate/ Enterprise, Academic/ Education, Government |

| Sourcing Covered | In-house, Outsourced |

| Delivery Modes Covered | Online, Offline |

| End Use Industries Covered | BFSI, Hospitality, Healthcare, Retail, Media and Entertainment, Others |

| Region Covered | North India, West and Central India, South India, East India |

| Companies Covered | Dale Carnegie & Associates Global, Inc., Pearson, Momentum Training Solutions, Franklin Covey Co., etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the India Soft Skills Training Market Report

The India soft skills training market reached USD 793.8 Million in 2025, reflecting consistent demand from corporate workforce development, SME professionalization, and expanding technology-enabled training adoption across all regions.

The market is projected to reach USD 1,836.8 Million by 2034, growing at a CAGR of 9.48% during 2026-2034, driven by expanding corporate L&D budgets, AI-powered learning adoption, and rapid SME sector growth.

Outsourced training leads with a 61.3% market share in 2025, driven by preference for specialist external providers offering globally benchmarked curricula, certified trainers, and scalable delivery frameworks unavailable in-house.

Offline delivery dominates at 57.8% in 2025, owing to the superior effectiveness of face-to-face experiential learning for developing interpersonal and behavioral competencies. Online delivery at 42.2% is the fastest-growing mode.

West and Central India commands a dominant 33.2% share in 2025, driven by the region’s concentration of BFSI headquarters, manufacturing clusters, and corporate offices in Mumbai, Pune, and Ahmedabad.

East India represents the highest-growth regional opportunity, driven by emerging IT hubs, expanding BFSI operations, and first-generation professional workforces in Kolkata and other East Indian centers requiring structured soft skills training.

Leading companies include Dale Carnegie & Associates Global, Inc., Pearson, Momentum Training Solutions, Franklin Covey Co., and others.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)