How AI is Transforming Australia Semiconductor Industry?

Australia Semiconductor Market Overview:

Recent projections indicate that Australia semiconductor market, including services, is growing at a steady compound annual growth rate as the nation deepens its tech infrastructure. The importance of semiconductors spans electronics, defense systems, telecommunications, and emerging AI applications, which position the local ecosystem as strategically vital for growth.

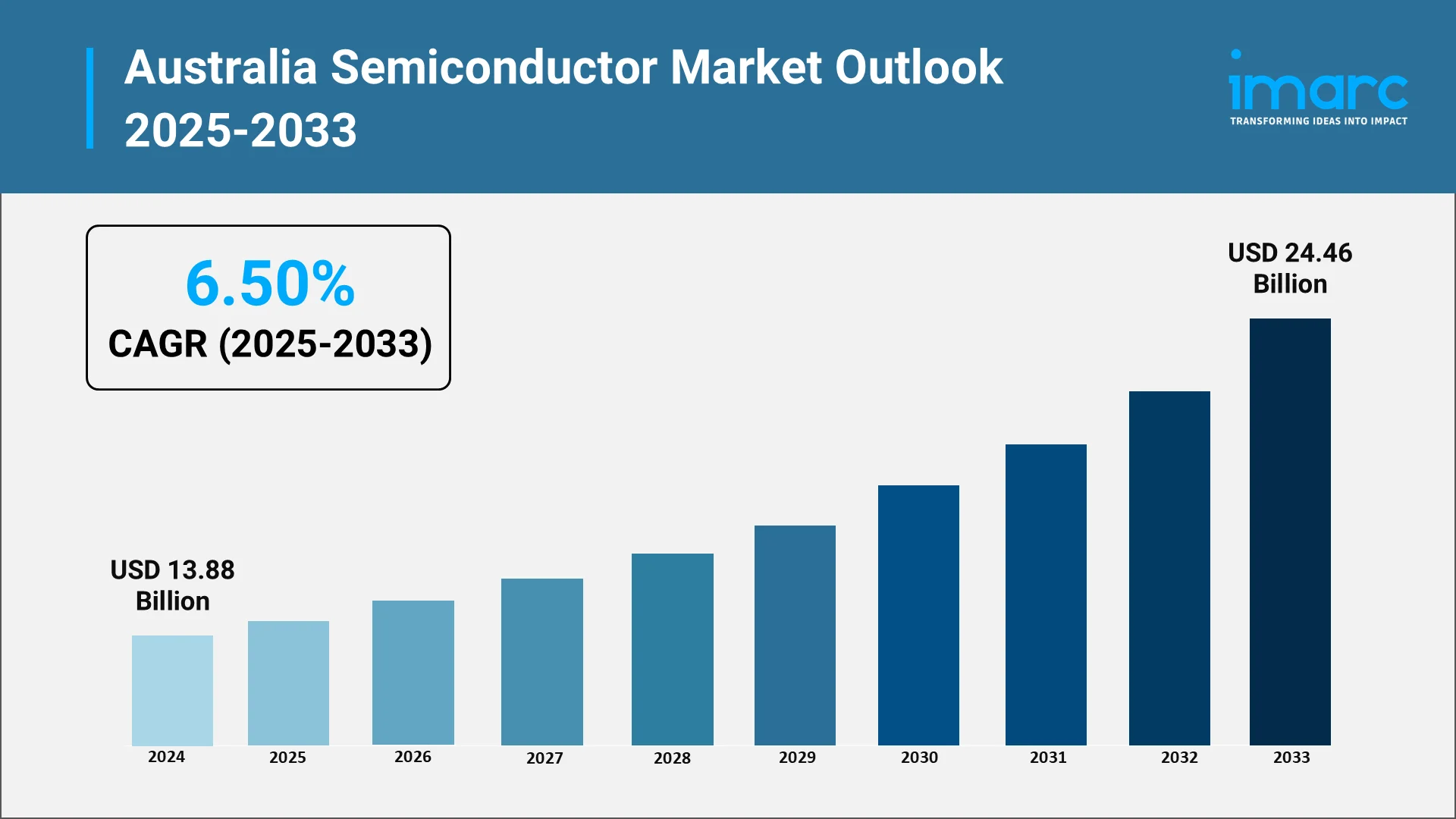

The Australia semiconductor market size reached USD 13.88 Billion in 2024. Looking forward, IMARC Group expects the market to reach USD 24.46 Billion by 2033, exhibiting a growth rate (CAGR) of 6.50% during 2025-2033. The market is being driven by strong government incentives, increased research and development (R&D) investments, a skilled STEM workforce, rising demand for consumer electronics and the Internet of Things (IoT) devices, and strategic efforts to enhance local manufacturing and further integrate the country with global supply chains.

Explore in-depth findings for this market, Request Sample

Government Support: Fueling the Chip Engine

Australia’s federal and state governments are investing in semiconductor capabilities through programs that focus on pilot-scale facilities and tooling. The National Reconstruction Fund (NRF) and the 2024–25 Federal Budget allocated money for chip production lines, testing infrastructure, and equipment upgrades. In August 2025, the National Reconstruction Fund Corporation (NRFC) was set up to invest up to AUD 15 Billion across seven priority areas, including value-added manufacturing that touches chips, power electronics, and advanced systems. The NRFC has begun deploying capital and can invest through debt, equity, and guarantees.

New South Wales supports chip design and prototyping through its Semiconductor Sector Service Bureau (S3B), which offers subsidized software, multi-project wafer runs, and engineering help. Recent S3B updates show 2025 activity around MPW and tool subsidies that lower entry barriers for startups and researchers.

These efforts aim to strengthen supply chain independence, keep strategic manufacturing onshore, and open new export paths for Australian-made chips.

Policies that Propel: National Strategies and Incentives

Policy is the backbone of long-term industry development. Australia has designated semiconductors as a “sovereign industrial capability” in its Defence Industry Development Strategy, giving local suppliers a clear advantage in defense tenders. This ensures that chips used in secure communications, radar, and other mission-critical systems can be trusted and traceable.

In March 2025, the federal government committed USD 39.8 Million to Simcoa Operations in Western Australia to expand local silicon production, a core upstream material in chip manufacturing. Export facilitation measures are also opening new markets in Europe and Asia for high-reliability components made in Australia.

These actions signal that the government is not aiming to compete with global megafabs, but rather to cultivate a strong, specialized semiconductor foundry industry in Australia focused on mature-node, niche, and secure production.

AI in Chips: Smarter Design, Sharper Production

Artificial intelligence is revolutionizing chip design and production in Australia. AI-driven design tools automatically optimize circuit layouts, significantly shortening development time. These tools enhance efficiency and performance, reducing the need for manual adjustments. In manufacturing, AI-powered vision systems detect microscopic defects during pilot runs, increasing precision and boosting yield rates. This reduces waste, improves production efficiency, and ensures higher-quality chips. By automating complex processes and enhancing quality control, AI is reshaping the semiconductor industry, accelerating innovation, and enabling more sustainable production practices. AI’s impact on chipmaking is driving both technological advancements and cost reductions in the industry.

In July 2025, CSIRO engineers showcased a breakthrough using quantum-AI techniques in semiconductor fabrication, opening the door for faster and more accurate production processes. Local toolmakers are embedding machine learning into inspection and test systems, which is creating momentum in the semiconductor equipment industry in Australia.

Homegrown Innovators: Australia’s Chip Champions

Following is a list of some of the Australian semiconductor innovators:

- Morse Micro (Sydney) develops Wi-Fi HaLow chips for long-range, low-power IoT. Its MM8108 SoC earned IoT Emerging Technology and Industrial IoT Product of the Year awards in 2025.

- Silanna Semiconductor (Brisbane) makes power-management and RF ICs, serving international markets. In June 2025, the company launched the SL2002 FirePower laser-driver IC and has been active at major power electronics events since 2024.

- BluGlass (Silverwater) specializes in GaN lasers and photonics. In March 2025, it set a world record for a single-mode GaN laser at 1,250 mW, 67 percent higher than its previous output. It also showcased a 16 percent improvement in GaN laser efficiency (43 percent QCW power conversion) at the ICNS-15 conference in July 2025. BluGlass won its first AUD 230,000 order from India’s Ministry of Defence that same month.

- Hendon Semiconductors (Adelaide) produces hybrid thick-film circuits for healthcare and defense use. Grants since 2023 have supported facility upgrades aligned to defense and medical production.

These semiconductor companies in Australia are proving strong in niche fields like connectivity, power electronics, photonics, and secure assemblies.

Rising Demand: Who Needs Australian Chips?

Several sectors are driving local chip demand:

- Defense and Security Electronics: Australia is investing in secure communications, sensors, and guidance systems. Procurement settings under the sovereign priority framework, and headline defense projects, are increasing scope for local component design, hybrid thick-film circuits, and trusted assembly lines.

- Energy Transition: Grid-scale conversion, EV charging, renewables, and industrial drives are moving to wide-bandgap devices. National agencies note a push toward high-efficiency power electronics as part of broader net-zero programs, which in turn raises local interest in GaN, SiC, and power modules.

- Space and Critical Infrastructure: Universities and startups tied to satellite programs require radiation-tolerant parts and custom ASICs. The niche is small, but the spec is exacting, which favors specialist prototyping and test services in Australia’s research network.

- Industrial and IoT Connectivity: Sydney-based Morse Micro continues to commercialize Wi-Fi HaLow SoCs for long-range, low-power links, accumulating 2025 industry awards and traction with OEMs. This validates domestic chip design capabilities and lifts downstream module and test activity.

R&D Powerhouses: Where Innovation Happens

Australia’s research fabric remains the country’s superpower.

- ANFF Network: Access to 500-plus tools across 21 locations improves prototyping throughput and training. Nodes at UNSW, University of Sydney, and South Australia provide lithography, deposition, etch, characterization, and device packaging options.

- GaN and Power Devices: Research groups continue to push GaN and SiC device physics and thermal management, aligning with the energy transition. Global literature highlights GaN’s gains in efficiency and frequency, which Australian teams and firms are translating into lasers and power modules. BluGlass’s July 2025 ICNS-15 results are a timely proof point on GaN device performance and manufacturability.

- AI-Enabled Design and Inspection: University-industry collaboration around AI for defect detection and yield management is growing, supported by national AI institutes and CSIRO initiatives.

Advanced assembly is also gaining attention. As chiplets, 2.5D and 3D stacks proliferate, Australia can stake out competencies in substrate technologies, RF modules, and secure system-in-package for defense and space. This ties to the semiconductor packaging industry in Australia, where small-lot, high-assurance builds matter more than sheer volume.

Obstacles Ahead: Challenges to Overcome

The Australian semiconductor industry faces significant challenges that must be addressed for long-term growth and competitiveness:

- Scale and Capex: Advanced semiconductor fabs require massive investments, limiting Australia’s ability to compete at the global level. The nation can only remain a niche player unless it adopts a focused approach, transitioning from pilot to production stages. Policy reports have openly acknowledged these constraints, signaling that substantial financial backing and targeted development will be needed.

- Talent Shortage: The scarcity of engineers with expertise in device physics, tool maintenance, and high-reliability manufacturing presents a major barrier. The Australian Strategic Policy Institute (ASPI) has pointed out that a lack of skilled workforce is a key bottleneck. It emphasized the necessity of scaling up training programs to build a robust talent pipeline to sustain growth in this sector.

- Supply-Chain Challenges: Australia lacks local production for essential components like photoresist, reticles, and specialty gases. This dependence on international suppliers exposes the industry to vulnerabilities, especially in a high-interest-rate environment. Companies must secure reliable import channels and long-term vendor contracts, creating additional capital pressures.

Addressing these hurdles will require coordinated efforts across government, academia, and industry to ensure the sector’s sustainable growth.

.webp)

Opportunity Zones: Where Australia Can Shine

Australia’s chance lies in specialized segments:

- Defense-Grade and Harsh-Environment Electronics: The procurement framework for sovereign industrial capability, paired with defense programs, provides predictable demand for secure assemblies, RF modules, and radiation-tolerant components. Hendon’s grants and upgrades illustrate how small manufacturers can pivot to this standard.

- Power and Photonics: GaN lasers and power devices have global runways. BluGlass’s recent results and capital access show a credible path from Australian labs to export markets.

- AI-Enabled Manufacturing Services: Embedding ML models in inspection and metrology will differentiate local toolmakers and integrators. CSIRO’s programs and 2025 quantum-AI demonstration can be leveraged to create service offerings for domestic and regional customers.

Rising local orders and prototyping work are strengthening the case for Australia computer chip manufacturers that specialize in high-assurance, low-volume builds for defense, energy, and space customers.

Strategic Ripple Effects: Economic and Security Gains

Building a semiconductor ecosystem brings both economic and strategic advantages. It creates high-skilled jobs in research and development, manufacturing, and systems integration. It also strengthens supply chains, reduces reliance on imports, and boosts national security. Industries like medical devices, automation, and energy benefit from secure, local sources of components, prioritizing trusted procurement.

Over time, Australia could position itself as a reliable supplier of specialized chips in the Asia Pacific region. This could start with the semiconductor packaging industry and related services, helping to meet growing demand and enhance the country’s role in the global tech supply chain. By developing this sector, Australia would not only improve its economic resilience but also play a significant role in regional tech security, ensuring a more stable and secure supply of critical technologies. This ecosystem would provide lasting benefits across multiple industries, from healthcare to energy.

How IMARC Can Help:

IMARC Group provides actionable insights and strategic guidance to businesses navigating the rapidly evolving Australian semiconductor industry. Our services empower companies to stay ahead of emerging technologies, competitor developments, and market trends.

Our capabilities include:

- Market size forecasts for key semiconductor segments

- Feasibility studies for investment and ROI analysis

- Industry benchmarking, competitive landscape assessment, and SWOT analysis

- Mapping of regional and market-based opportunities

- Support for regulatory compliance and market entry strategies

- Technology evaluation and partner selection assistance

Whether you're looking to enter the Australian market, scale operations, or explore new technologies, IMARC helps you reduce risk and unlock growth opportunities.

Conclusion:

The Australian semiconductor industry in 2025 is driven by rapid technological advancements, increased demand for electronic devices, and government support for innovation. The demand for microchips, processors, and sensors in industries like automotive, healthcare, and telecommunications is surging, alongside the rise of AI and IoT. With regulatory frameworks evolving and local players gaining prominence, companies need to adopt forward-thinking strategies to navigate competition and capitalize on emerging opportunities.

IMARC offers tailored intelligence and advisory services to help you stay competitive, optimize your operations, and drive sustainable growth in the Australian semiconductor market.

Our Clients

Contact Us

Have a question or need assistance?

Please complete the form with your inquiry or reach out to us at

Phone Number

+91-120-433-0800+1-201-971-6302

+44-753-714-6104

Previous Post

Fiber optic cables are high-tech communications cables that carry information like bursts of light along extremely thin glass or plastic strands, providing high-speed, high-bandwidth connectivity with little loss of signal. Fiber optic cables make up the foundation of contemporary telecommunications, carrying internet, cloud computing, 5G networks, and smart infrastructure.

CAT (Category) cables are twisted-pair Ethernet cables utilized for copper-based wired network communications, varying from CAT5e to CAT8 standards. The cables carry data through copper conductors, but with different speeds (up to 40 Gbps for CAT8) and bandwidths, supporting networks such as LANs, data centers, and smart buildings.

India's semiconductor industry is undergoing a revolutionary phase driven by rising demand from industries like consumer electronics, automotive technologies, industrial automation, and telecom infrastructure.

USB data cables are critical elements of contemporary digital connectivity, enabling high-speed and consistent data transfer and power supply for a broad scope of electronic products. They provide the foundation for charging and synchronizing smartphones, tablets, laptops, and other peripherals, with significant applications in consumer electronics, industrial automation, and new technologies. With technologies like USB-C, the cables today carry faster data speeds, more power output, and universal compatibility, making them essential in a world that is connected.

Thin-film-transistor (TFT) liquid-crystal display (LCD) is a type of display technology used in many electronic devices, such as smartphones, tablets, laptops, and televisions (TVs). A backlight, colour filters, a thin-film transistor array, and a liquid crystal layer are among the layers that make up this flat-panel display. TFT LCDs are made to produce sharp images with superb viewing angles, strong contrast, and accurate colour reproduction. They are made up of thousands of tiny transistors that regulate how much light enters each pixel. This makes it possible for the display to generate crisp, detailed images at rapid refresh rates. TFT LCD technology's low power consumption is one of its main benefits, which makes it perfect for battery-operated gadgets.

Polycrystalline solar photovoltaic (PV) modules are a key component of solar energy systems, harnessing sunlight and converting it into electricity through the photovoltaic effect. These modules are composed of multiple interconnected solar cells, each made from polycrystalline silicon. Polycrystalline solar panels are renowned for their efficiency, affordability, and versatility, making them a popular choice for various applications such as solar installations, commercial and industrial projects, off-grid systems and solar farms.

The LED chip is the core component of an LED bulb, comprising semiconductor layers that enable the free flow of protons and electrons. Employed in all LED lighting fixtures—from bulbs to tubes—the LED chip fundamentally determines light quality, with variations in brightness, voltage, and wavelength. These chips are manufactured through a process called MOCVD (metal-organic chemical vapor deposition), which creates the semiconductor layers that facilitate electric flow. Major applications of these chips include backlighting, illumination, automotive lighting, signs, and signals.

Semiconductors are crucial components in the modern electronics industry, used in electronic equipment and devices to manage and control the flow of electricity. They are found in consumer items like smartphones, wearables, smart TVs, and advanced equipment used in industrial applications, defense, and aerospace. Semiconductors are further divided into four broad categories: optoelectronics, discrete components, integrated circuits, and sensors. Memory devices, logic devices, analog ICs, MPUs, discrete power devices, MCUs, and sensors are some of the major components of semiconductors.