Japan Digital Printing Market Size, Share, Trends and Forecast by Type, Ink Type, Application, and Region, 2026-2034

Japan Digital Printing Market Size, Share, Trends & Forecast (2026-2034)

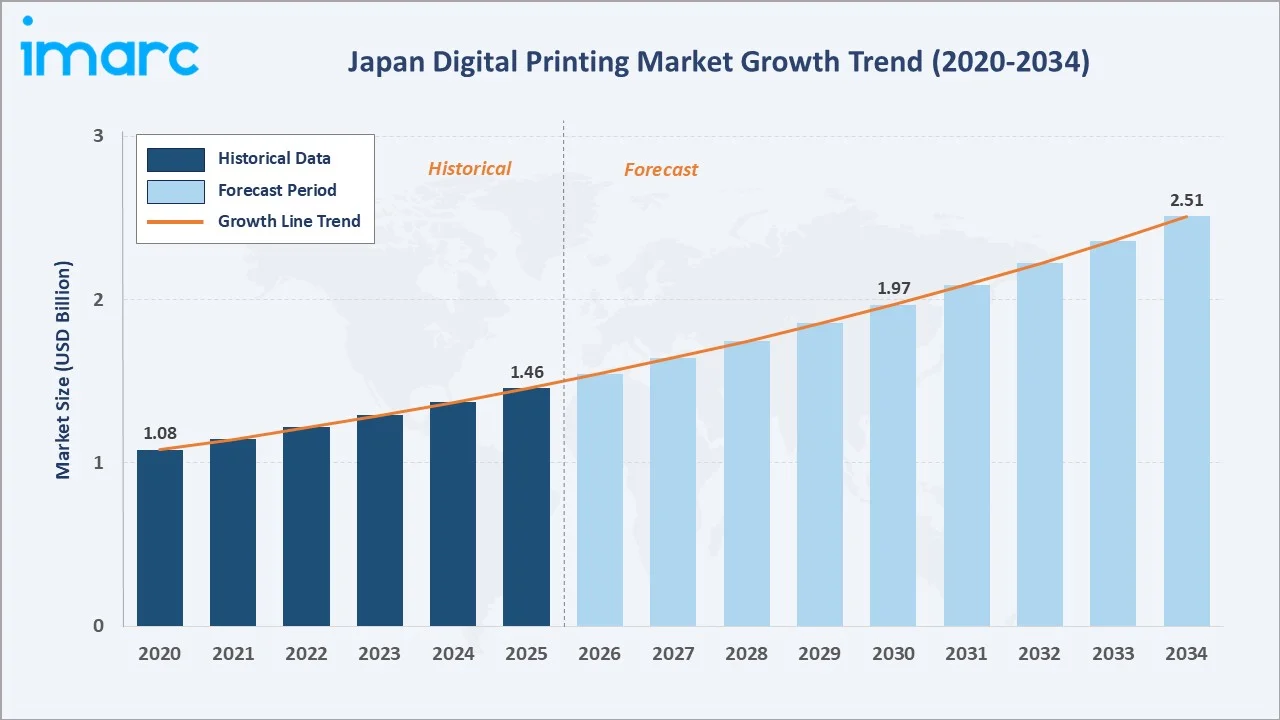

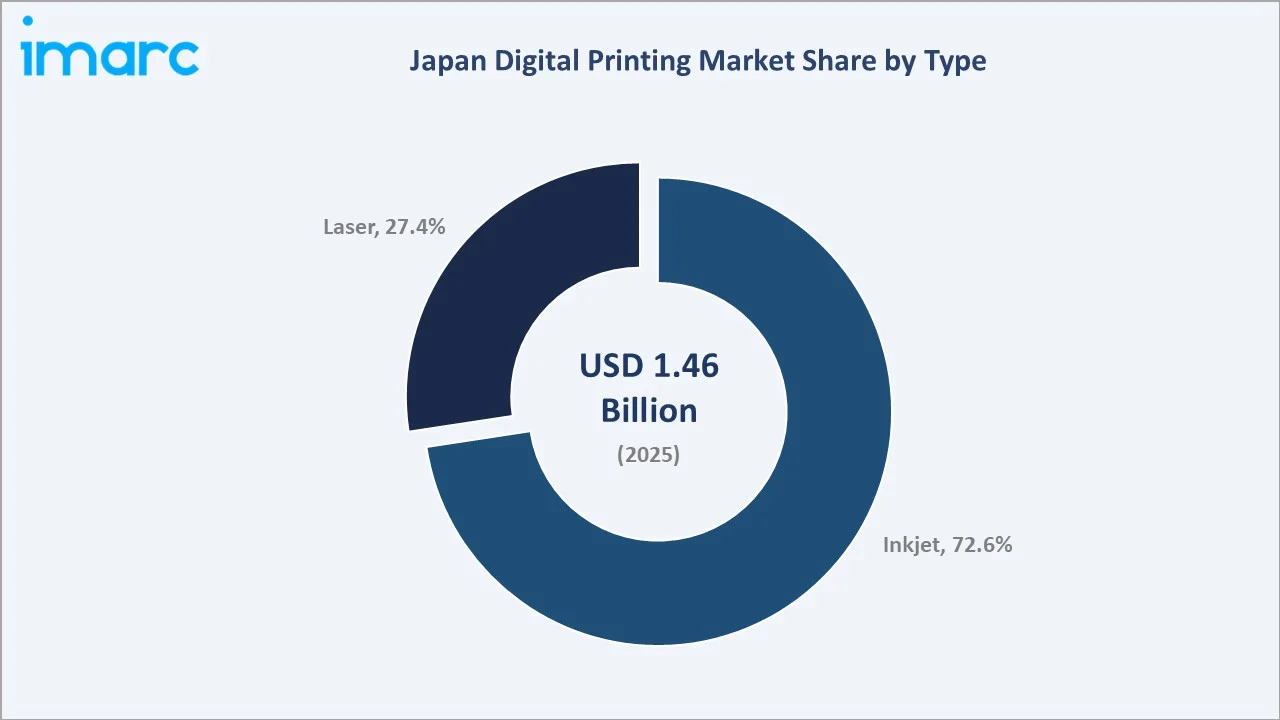

The Japan digital printing market size was valued at USD 1.46 Billion in 2025 and is projected to reach USD 2.51 Billion by 2034, exhibiting a CAGR of 6.24% during 2026-2034. Rising adoption of personalized packaging in e-commerce, growing demand for short-run and on-demand print jobs, expanding fabric and ceramic printing applications, and steady investment in eco-friendly inkjet platforms are driving market growth. Inkjet technology dominates with a 72.6% share in 2025, while paper and books remain the largest application segment at 28.9%. The Kanto Region leads regional demand with a 38.7% share in 2025.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 1.46 Billion |

|

Forecast Market Size (2034) |

USD 2.51 Billion |

|

CAGR (2026-2034) |

6.24% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

Kanto Region (38.7% share, 2025) |

|

Fastest Growing Region |

Kansai/Kinki Region |

|

Leading Type Segment |

Inkjet (72.6%, 2025) |

|

Leading Application |

Paper/Books (28.9%, 2025) |

The chart below shows Japan digital printing market growth from 2020-2034, supported by short-run printing demand, packaging diversification, and rising textile applications across the forecast period.

To get more information on this market, Request Sample

CAGR analysis shows inkjet technology, fabric, and ceramic application segments as the strongest growth contributors in the Japan digital printing market through 2034, with the overall market expanding at 6.24% CAGR.

.webp)

Executive Summary

The Japan digital printing market is undergoing steady transformation, supported by rising e-commerce packaging demand, customization trends, and continuous improvements in inkjet print quality. Valued at USD 1.46 Billion in 2025, the industry is projected to reach USD 2.51 Billion by 2034, growing at a 6.24% CAGR. Short-run flexibility, lower setup costs, and faster turnaround times are accelerating digital adoption across publishing, packaging, fabric, and signage applications nationwide.

Inkjet technology leads the market with a 72.6% share in 2025, supported by superior versatility across substrates and ongoing investments by Japanese OEMs in industrial inkjet platforms. Paper and books represent the largest application segment at 28.9%, followed by plastic film or foil at 21.7% and fabric at 18.6%. Key emerging trends include UV-cured ink adoption, sustainable water-based formulations, smart workflow automation, and rising demand for variable data printing in marketing and packaging.

The Kanto Region commands 38.7% of the Japan digital printing market in 2025, anchored by Tokyo's publishing, advertising, and electronics packaging clusters. The Kansai/Kinki Region holds 18.5%, supported by Osaka and Kyoto industrial textile and ceramic printing demand. The Central/Chubu Region accounts for 13.4%, with Nagoya's automotive packaging and graphic printing ecosystems contributing meaningfully to incremental market growth through 2034.

Key Market Insights

|

Insight |

Data |

|

Largest Type Segment |

Inkjet - 72.6% share (2025) |

|

Second Type Segment |

Laser - 27.4% share (2025) |

|

Leading Application |

Paper/Books - 28.9% share (2025) |

|

Second Application |

Plastic Film or Foil - 21.7% share (2025) |

|

Leading Region |

Kanto Region - 38.7% revenue share (2025) |

|

Top Companies |

SCREEN Graphic Solutions Co., Ltd., Tokyo Kikai Seisakusho, Ltd., CTC Japan, LTD., and Kido Packaging |

Key Analytical Observations Supporting the Above Data:

- Inkjet's 72.6% dominance in 2025 reflects its versatility across paper, fabric, plastic, and ceramic substrates, making it the preferred technology for short-run and customized print jobs in Japan.

- Laser printing holds 27.4% in 2025, sustained by office documentation, transactional printing, and high-volume monochrome jobs where text precision and speed are valued over color flexibility.

- Paper and books at 28.9% in 2025 reflect Japan's mature publishing industry. Short-print-run titles and on-demand textbook production support continued digital migration from offset platforms.

- Plastic film and foil at 21.7% in 2025 highlight the role of digital printing in flexible packaging. Rising demand from food, cosmetics, and pharmaceutical brands drives short-run SKU printing.

- The Kanto Region's 38.7% share in 2025 reflects Tokyo's concentration of publishers, ad agencies, packaging converters, and corporate headquarters, anchoring nearly four out of every ten print jobs.

- Top operators including Screen Graphic Solutions and Tokyo Kikai Seisakusho continue to invest in industrial inkjet platforms, driving technology localization and supporting sustained mid-single-digit market growth.

Japan Digital Printing Market Overview

Digital printing transfers digital files directly onto substrates such as paper, fabric, plastic, glass, and ceramic without traditional printing plates. The ecosystem covers ink suppliers, press OEMs, software vendors, print service providers, packaging converters, publishers, and end clients across consumer goods, advertising, and industrial sectors.

.webp)

Applications span book publishing, magazine and brochure production, label and flexible packaging, textile and fashion printing, ceramic tile decoration, and architectural glass printing. Growth is supported by Japan's premium product packaging culture, e-commerce expansion, sustainability push toward water-based inks, and the country's strong domestic OEM base in printing technology.

Market Dynamics

To evaluate market opportunities, Request Sample

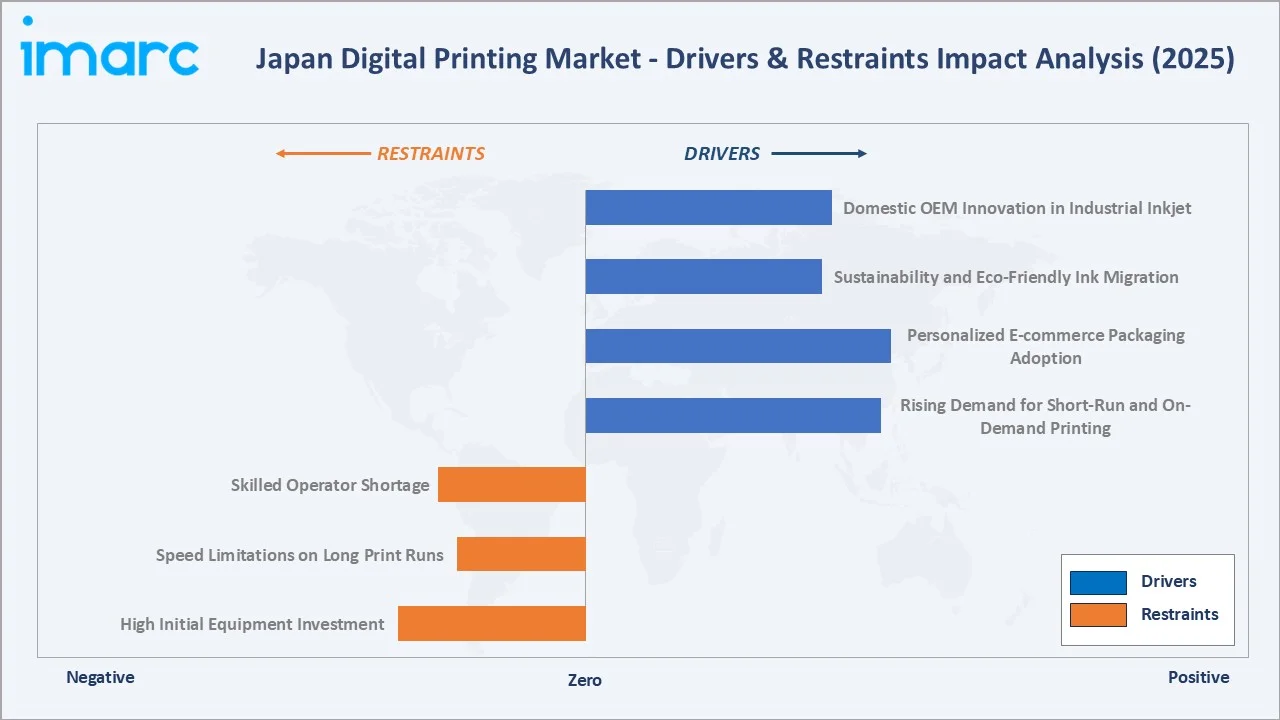

Market Drivers

- Rising Demand for Short-Run and On-Demand Printing: Demand for short-run, fast-turnaround printing is increasing across publishing and packaging in Japan, driven by customization and reduced inventory needs. Digital printing lowers setup costs versus offset, making economical small-batch production viable.

- Personalized E-commerce Packaging Adoption: METI estimates the B2C market is $176.8 billion and the C2C market is $18 billion and the survey reports that Japan’s eCommerce market in 2024 continues to grow steadily, fuels demand for personalized boxes, labels, and flexible films. Digital printing enables variable artwork at scale across cosmetics, food, and gifting brands.

- Sustainability and Eco-Friendly Ink Migration: Brand owners are shifting toward water-based, UV-cured, and latex inks to meet ESG goals. Reduced VOC emissions and lower waste help digital presses replace solvent-heavy traditional methods, particularly across food packaging.

- Domestic OEM Innovation in Industrial Inkjet: Japanese press makers including Screen Graphic Solutions and Konica Minolta continue launching production-class inkjet systems with higher speeds and wider format support, anchoring localized adoption among print service providers.

Market Restraints

- High Initial Equipment Investment: Industrial digital printing systems require substantial upfront capital investment, limiting adoption among small and mid-sized print providers. Extended payback periods continue to slow wider penetration beyond major urban printing hubs such as Tokyo and Osaka.

- Speed Limitations on Long Print Runs: For high-volume print runs, conventional offset printing remains more cost-efficient and faster per unit, limiting digital printing adoption in large-scale applications such as newspapers, catalogs, and mass commercial printing.

- Skilled Operator Shortage: Operating color management, RIP software, and substrate-handling on industrial inkjet platforms requires specialized training. Japan's aging printing workforce creates persistent talent constraints across mid-tier print service firms.

Market Opportunities

- Industrial Textile and Fabric Printing Expansion: Digital textile printing is expanding in Japan, driven by demand for apparel customization, short production cycles, and reduced water usage versus traditional dyeing. Growth is supported by fashion, home textiles, and on-demand production trends.

- Ceramic Tile Decoration Adoption: Digital inkjet technology is increasingly used in ceramic tile decoration, enabling high-resolution, customizable designs for residential and commercial interiors. Adoption is rising with demand for premium and personalized construction materials.

- 3D Printing and Hybrid Press Convergence: Integrated digital workflows combining 2D inkjet and additive manufacturing create new commercial use cases in prototype packaging, premium gift items, and architectural model production across Japanese design studios.

Market Challenges

- Substrate Compatibility and Ink Adhesion: Digital ink adhesion on certain plastic and metallic substrates still requires primers or post-coating, raising operational complexity for packaging converters serving food and pharmaceutical clients.

- Color Consistency Across Print Runs: Maintaining brand color accuracy across multiple devices and substrates remains a recurring quality control challenge, particularly for premium cosmetics and fashion clients with strict CMYK tolerances.

- Pressure from Imported Equipment Competition: HP Indigo, Xerox, and Heidelberg digital systems continue capturing share in Japan's high-end commercial print segment, intensifying pricing competition for domestic OEMs in label and packaging press categories.

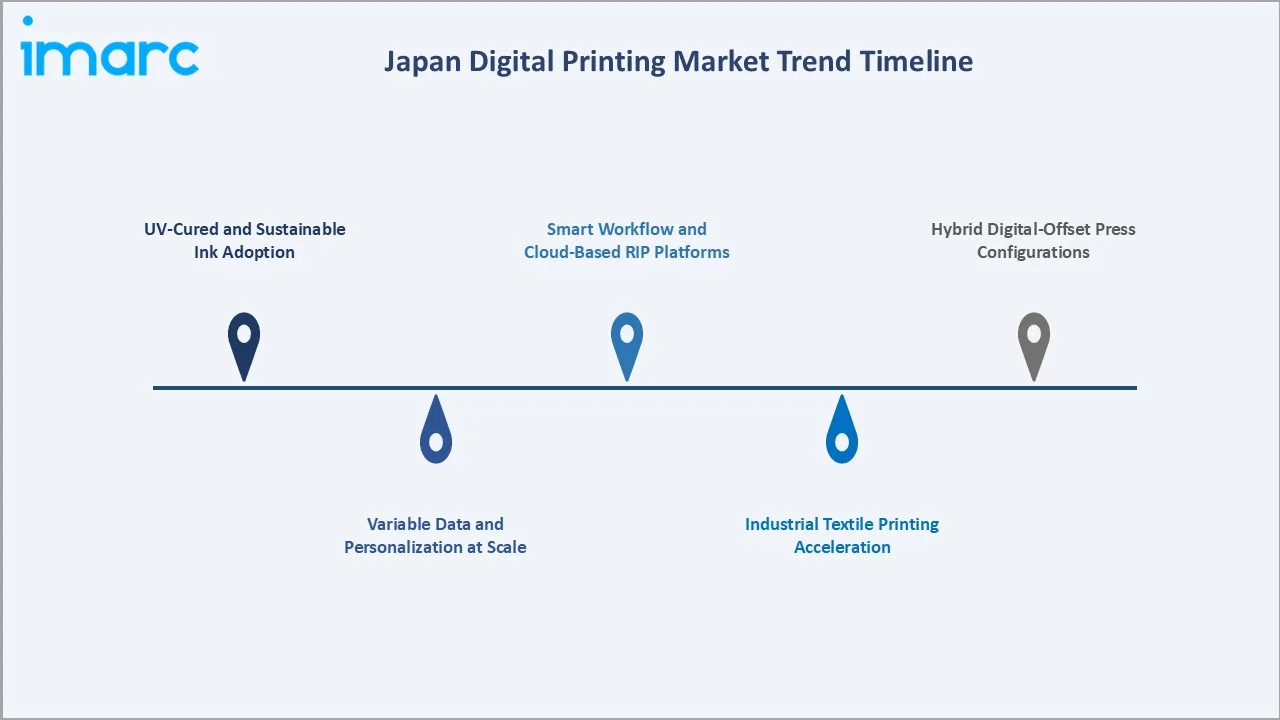

Emerging Market Trends

1. UV-Cured and Sustainable Ink Adoption

Japanese converters are migrating from solvent-based to UV-cured and water-based inks. UV inks improve durability and reduce drying time, while water-based formulations support food-contact packaging compliance under Japan's positive list system.

2. Variable Data and Personalization at Scale

Digital presses now print unique codes, names, and artwork on every package. Cosmetics brands like Shiseido and food brands across konbini channels increasingly use variable data printing for limited-edition SKUs and regional promotions.

3. Industrial Textile Printing Acceleration

Direct-to-fabric inkjet printing is expanding across Japanese apparel and home textile producers. The technology enables short-run customized fashion lines, supporting domestic D2C brands and reducing inventory risk in seasonal collections.

4. Smart Workflow and Cloud-Based RIP Platforms

Cloud-based RIP, automation tools, and AI-driven prepress workflows are improving efficiency by reducing manual intervention and job setup time. Print service providers in hubs like Tokyo and Osaka are increasingly integrating MIS, web-to-print, and end-to-end digital workflows.

5. Hybrid Digital-Offset Press Configurations

Hybrid presses combining digital inkjet heads with conventional offset units are gaining traction in Japan's label and folding carton segments. The configuration offers efficient hybrid economics, balancing variable data flexibility with high-volume throughput.

Industry Value Chain Analysis

Japan's digital printing value chain spans six stages from raw ink chemistry to end-customer print delivery. Each stage has distinct margin structures, with press OEMs and ink suppliers capturing premium economics relative to commoditized print service providers.

|

Stage |

Key Players / Examples |

|

Raw Materials & Ink Chemistry |

Suppliers produce pigments, resins, and specialty inks, including water-based and UV formulations, enabling consistent print quality, durability, and regulatory compliance |

|

Press & Equipment Manufacturing |

Manufacturers design and build digital presses and inkjet systems, focusing on speed, precision, scalability, and compatibility with substrates and applications |

|

Software & Workflow Solutions |

Software providers develop workflow solutions, including RIP, color management, and MIS tools, streamlining job processing, automation, integration, and production control |

|

Print Service Providers |

Print service providers operate presses to deliver customized, short-run, and on-demand printing services across commercial, packaging, publishing, and industrial segments |

|

Distribution & Converting |

Converters and distributors process materials into products, including packaging, labels, and textiles, ensuring logistics, finishing, and delivery to end users |

|

End Users / Consumers |

End users utilize outputs for communication, branding, packaging, and decoration, driving demand for customization, faster turnaround, and high-quality visual presentation |

Press OEMs and ink suppliers hold structural pricing power because of high R&D barriers and long product certification cycles. Print service providers compete on speed, colour quality, and customer service, with generally moderate and competitive margins.

Technology Landscape in the Japan Digital Printing Industry

Industrial Inkjet Print Head Innovation

Print head suppliers including Kyocera, Ricoh, and Konica Minolta are advancing single-pass and multi-pass piezo heads. Higher nozzle counts now deliver speeds above 150 meters per minute, enabling industrial-scale label and flexible packaging output.

Sustainable and Specialty Ink Development

Japanese ink majors Sakata INX and DIC Corporation are commercializing low-migration UV inks for food packaging, plus aqueous formulations meeting Japan's food contact compliance. New latex inks support outdoor signage and architectural applications.

Smart Connectivity and IoT Press Monitoring

Connected digital presses increasingly use IoT-based monitoring for performance tracking, ink usage, and maintenance alerts. Predictive maintenance helps reduce downtime and improve operational efficiency across industrial printing environments.

Workflow Automation and AI-Driven Color Management

AI-enabled colour management and automated workflows are streamlining prepress processes and improving consistency. Cloud-based platforms support continuous job submission and integration with web-to-print systems for commercial printing applications.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Type |

Inkjet |

72.6% |

2025 |

|

Ink Type |

🔒 |

🔒 |

2025 |

|

Application |

Paper/Books |

28.9% |

2025 |

|

Region |

Kanto Region |

38.7% |

2025 |

By Type

Inkjet technology dominates the Japan digital printing market with a 72.6% share in 2025, supported by its compatibility with diverse substrates and rising adoption across packaging, textile, and ceramic applications. Industrial inkjet investment by domestic OEMs continues to widen the technology lead.

To access detailed market analysis, Request Sample

Laser printing holds 27.4% in 2025, sustained by office, transactional, and short-text print runs where high speed and crisp monochrome output are valued. Toner-based digital systems remain entrenched in publishing book reprints and direct-mail marketing channels nationwide.

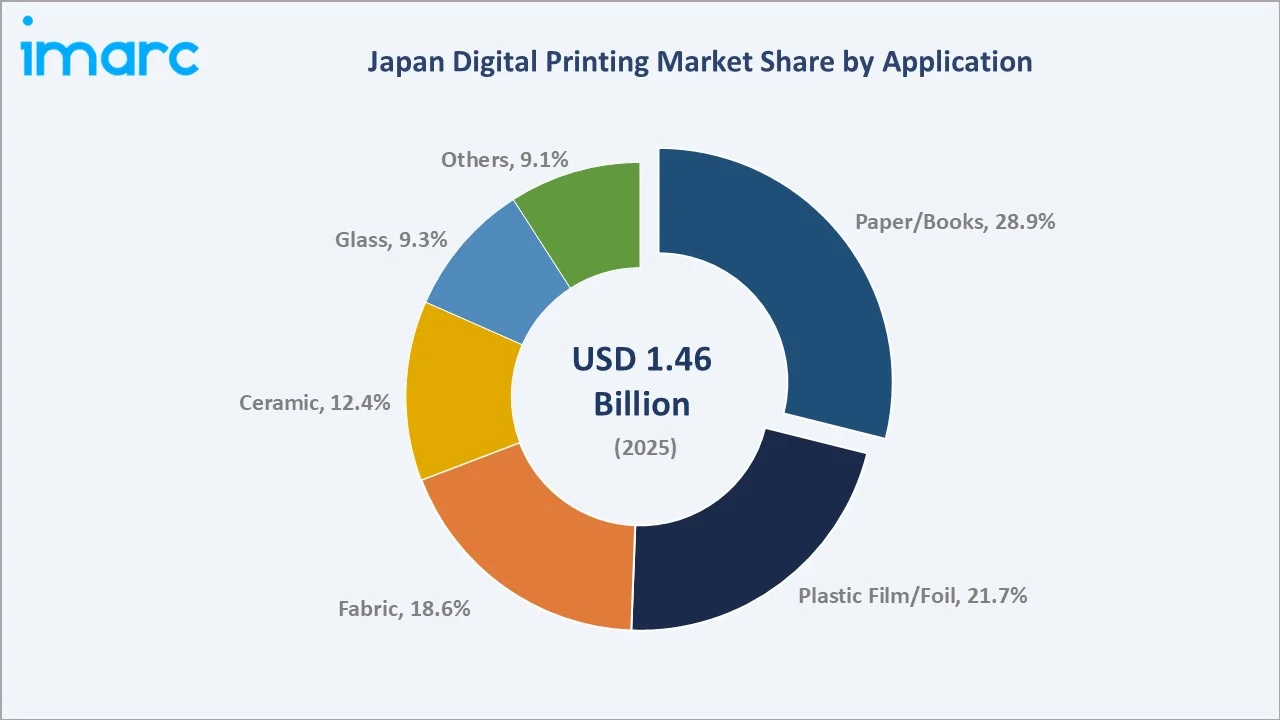

By Application

Paper and books represent the largest application segment in 2025, accounting for 28.9% of the Japan digital printing market. Short-print-run titles, academic textbook reprints, and self-publishing platforms continue to fuel sustained digital adoption among Japanese publishers.

Plastic film or foil, accounting for 21.7%, is driven by strong flexible packaging demand from food, cosmetics, and pharmaceutical sectors. Fabric holds 18.6%, supported by rising direct-to-textile printing adoption. Ceramic at 12.4% benefits from tile decoration and interior applications, while glass contributes 9.3% and other materials represent 9.1% of the market.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

|

Kanto Region |

38.7% |

Tokyo publishing, advertising, e-commerce packaging, electronics; high concentration of brand HQs |

|

Kansai/Kinki Region |

18.5% |

Osaka and Kyoto industrial textiles, ceramic tile decoration, traditional craft modernization |

|

Central/Chubu Region |

13.4% |

Nagoya automotive packaging, machinery labels, graphic and signage printing demand |

|

Kyushu-Okinawa Region |

8.6% |

Food and beverage packaging, regional FMCG production, semiconductor packaging printing |

|

Tohoku Region |

6.9% |

Industrial label printing, regional book publishing, government documentation printing |

|

Chugoku Region |

5.3% |

Hiroshima manufacturing labels, automotive parts marking, regional commercial printing |

|

Hokkaido Region |

4.8% |

Tourism marketing materials, agricultural product packaging, regional publishing demand |

|

Shikoku Region |

3.8% |

Paper industry adjacency, specialty packaging, niche industrial print job services |

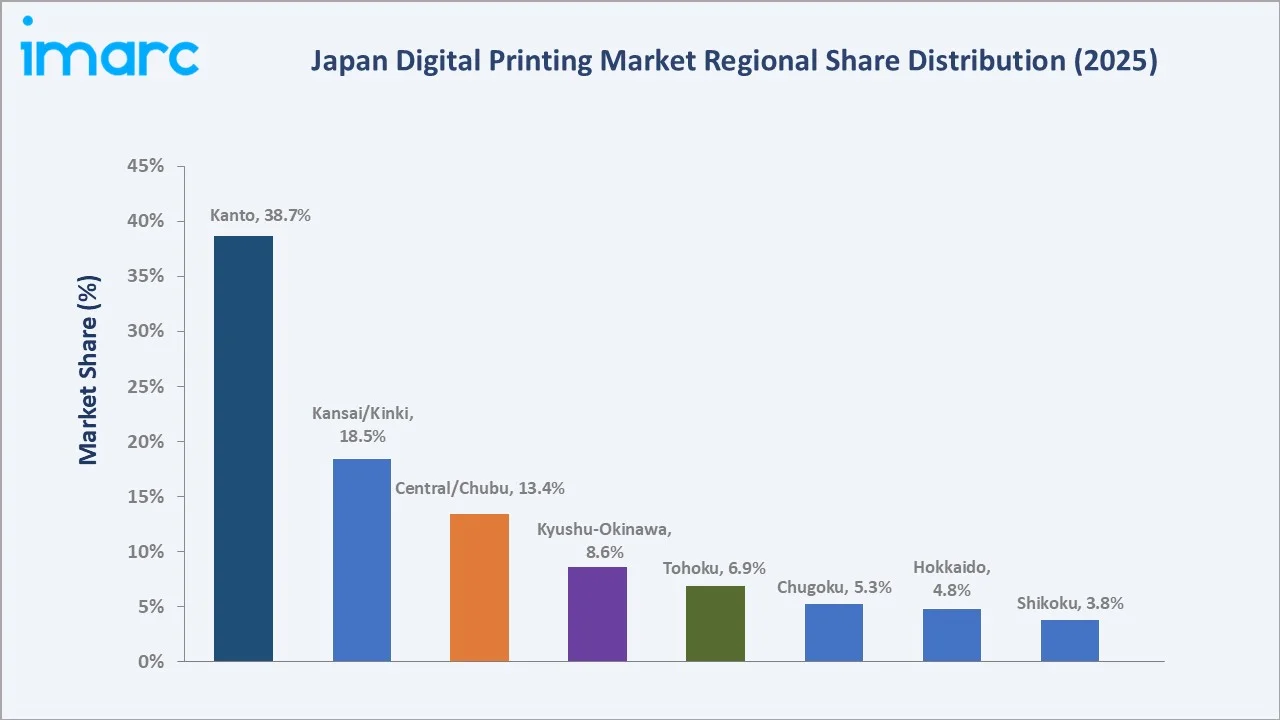

The Kanto Region leads Japan's digital printing market with a 38.7% revenue share in 2025, anchored by Tokyo's dense ecosystem of publishers, advertising agencies, e-commerce brands, and electronics packaging clusters. Saitama and Kanagawa industrial parks add converting and label production scale across the region.

The Kansai/Kinki Region holds 18.5% in 2025, driven by Osaka's packaging converters, Kyoto's traditional textile and ceramic industries, and Kobe's apparel and lifestyle brands. The Central/Chubu Region accounts for 13.4%, with Nagoya's automotive supply chain supporting industrial label and parts marking demand. Smaller regions including Kyushu-Okinawa (8.6%), Tohoku (6.9%), Chugoku (5.3%), Hokkaido (4.8%), and Shikoku (3.8%) collectively account for around 29.4% of the market, supported by regional FMCG packaging, agricultural product labeling, and local commercial print service providers.

Competitive Landscape

|

Company Name |

Brand / Platform |

Market Position |

Core Strength |

|

SCREEN Graphic Solutions Co., Ltd. |

Truepress Jet |

Leader |

Industrial inkjet for labels, packaging, ceramics |

|

Tokyo Kikai Seisakusho, Ltd. |

TKS Color Top / Jetleader / Colormaster / Economaster |

Leader |

Web-fed digital presses for newspapers and books |

|

CTC Japan, LTD. |

CTC Japan |

Challenger |

Digital print integration for industrial converters |

|

Kido Packaging |

Kido |

Challenger |

Flexible packaging and label digital printing |

The Japan digital printing market is moderately consolidated, with domestic equipment leaders including SCREEN Graphic Solutions Co., Ltd., Tokyo Kikai Seisakusho, Ltd., CTC Japan, LTD., and Kido Packaging dominating press supply, while a fragmented base of print service providers competes regionally on speed, colour quality, and customer service.

.webp)

Key Company Profiles

Screen Graphic Solutions Co., Ltd.

SCREEN Graphic Solutions, based in Kyoto, is a global leader in industrial inkjet printing, delivering high-speed digital presses for labels, packaging, and commercial applications. The company operates worldwide and plays a central role in advancing Japan’s industrial digital printing ecosystem.

- Product & Service Portfolio: Its portfolio includes Truepress Jet series (520HD/560HDX for commercial printing, LABEL 350UV SAI/UV+ for labels), inkjet solutions for flexible packaging and corrugated, and ceramic tile decoration systems, alongside workflow software and lifecycle support services.

- Recent Developments: In 2025, SCREEN Graphic Solutions Co., Ltd. enhanced its Truepress LABEL 350UV SAI S by introducing a digital primer option, significantly improving print quality, ink adhesion, and durability across diverse substrates, supporting advanced label and packaging applications. Additionally, the company showcased the press with new automation and UV ink capabilities at global exhibitions, reinforcing its role in high-productivity digital label printing.

- Strategic Focus: Screen Graphic Solutions focuses on industrial inkjet leadership, sustainability through low-migration ink platforms, ceramic decoration expansion, and partnerships with global label converters seeking high-throughput digital press capabilities.

Tokyo Kikai Seisakusho, Ltd.

Tokyo Kikai Seisakusho, headquartered in Tokyo and established in 1906, is a leading Japanese manufacturer of newspaper and commercial web offset presses, providing integrated printing systems and engineering services primarily to domestic publishers and newspaper companies.

- Product & Service Portfolio: The company provides newspaper offset presses, commercial web offset systems, press automation and control solutions, retrofitting/upgrade services, and engineering support, with limited exposure to digital printing mainly through hybrid workflow integration rather than proprietary digital presses.

- Recent Developments: Tokyo Kikai Seisakusho continued showcasing its engineering and automation capabilities at industry exhibitions in Japan, including logistics and industrial trade fairs, highlighting automation systems and workflow solutions alongside its core press technologies.

- Strategic Focus: Tokyo Kikai Seisakusho focuses on press modernization, digital-offset hybrid configurations, lifecycle service expansion, and supporting domestic publishing customers through technology upgrades that bridge legacy and digital workflows.

CTC Japan, LTD.

CTC Japan provides digital print integration, automation, and IT solutions to printing companies, packaging converters, and brand owners across Japan. The company serves as a key bridge between digital press OEMs and end users seeking complete workflow modernization solutions.

- Product & Service Portfolio: Digital press integration services, MIS and web-to-print platforms, color management consulting, and workflow automation solutions tailored for commercial and industrial Japanese print service providers.

- Recent Developments: CTC Japan offers eco-friendly inkjet printing systems for flexible packaging, such as the CSJ-N1000, using water-based pigment inks without VOCs, enabling high-mix, low-volume production and supporting sustainable packaging applications.

- Strategic Focus: CTC Japan focuses on digital workflow modernization, cloud platform adoption, automation consulting, and supporting Japan's mid-tier print service providers in scaling digital print volumes profitably.

Market Concentration Analysis

The Japan digital printing market shows moderate concentration on the equipment side and high fragmentation on the service-provider side. The top four press OEMs including SCREEN Graphic Solutions Co., Ltd., Tokyo Kikai Seisakusho, Ltd., CTC Japan, LTD., and Kido Packaging collectively hold over 60% of digital press shipments in 2025.

Print service provider fragmentation is much higher, with thousands of small and mid-sized printers across Kanto, Kansai, and Chubu serving regional publishers, packaging converters, and commercial clients. Consolidation pressure is gradually building as digital press investment requirements rise and ESG compliance costs scale. Acquisition activity has been moderate, with leading players like Toppan Holdings and Dai Nippon Printing absorbing smaller specialists in packaging and digital print niches to expand their service portfolios.

Investment & Growth Opportunities

Fastest-Growing Segments

Industrial fabric and textile printing is among the fastest-growing segments, driven by rising adoption of direct-to-fabric inkjet for apparel, home textiles, and on-demand production. Ceramic tile decoration also shows strong growth potential, supported by construction activity and demand for high-quality interior finishes.

Emerging Market Expansion

Regions beyond Kanto, particularly Kansai (Osaka, Kyoto) and Chubu (Nagoya), are emerging as key growth corridors. These areas benefit from industrial textile production, ceramics manufacturing, and automotive-related printing applications, creating expansion opportunities for digital press manufacturers and service providers.

Venture & Strategic Investment Trends

Capital is flowing into Japanese print-tech areas including AI-driven colour management software, cloud-based RIP platforms, sustainable ink chemistry startups, and workflow automation providers. Major players like Toppan Inc., Dai Nippon Printing, and Konica Minolta are actively expanding digital capabilities through partnerships and acquisitions.

Future Market Outlook (2026-2034)

The Japan digital printing market is projected to expand from USD 1.46 Billion in 2025 to USD 2.51 Billion by 2034 at a CAGR of 6.24%, representing more than USD 1 Billion of incremental value through the forecast period. Growth is anchored by inkjet technology leadership, packaging customization demand, and rising textile and ceramic application adoption.

Three transformational trends will reshape Japan's digital printing landscape through 2034. AI-driven colour management and cloud workflow platforms will compress prepress cycles. Sustainable ink chemistry will become the default standard for food and cosmetics packaging. Hybrid digital-offset press configurations will redefine economics across label and folding carton segments.

By 2034, digital printing in Japan is expected to mature into a connected, data-driven, and sustainability-aligned industry. Press OEMs investing in industrial inkjet leadership, ink suppliers commercializing low-migration formulations, and print service providers digitizing workflows will capture disproportionate share of the projected USD 2.51 Billion market opportunity.

Research Methodology

Primary Research

Primary research included structured interviews and surveys conducted in 2024 and 2025 with senior stakeholders across the Japan digital printing value chain including press OEM product managers, ink suppliers, packaging converters, commercial print service providers, brand owner procurement leaders, and industry consultants.

Secondary Research

Secondary sources include company annual reports (SCREEN Graphic Solutions Co., Ltd., Tokyo Kikai Seisakusho, Ltd., CTC Japan, LTD., and Kido Packaging), industry associations (Japan Printing Industry Federation, Japan Federation of Printing Industries), Japanese government statistics (METI, Statistics Bureau of Japan), and trade publications including Nikkei Print Industry News.

Forecasting Models

Market sizing combines top-down GDP and end-user industry mapping with bottom-up press shipment data, ink consumption patterns, and converter output analysis. Forecasts incorporate sustainability regulation timelines, e-commerce penetration projections, and substrate-specific adoption curves under base, optimistic, and conservative scenarios.

Japan Digital Printing Market Report Coverage

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical and Forecast Trends, Industry Catalysts and Challenges, Segment-Wise Historical and Predictive Market Assessment:

|

| Types Covered | Inkjet, Laser |

| Ink Types Covered | Aqueous Ink, UV-Cured Ink, Solvent Ink, Latex Ink, Dye Sublimation Ink |

| Applications Covered | Plastic Film or Foil, Fabric, Glass, Paper/Books, Ceramic, Others |

| Regions Covered | Kanto Region, Kansai/Kinki Region, Central/ Chubu Region, Kyushu-Okinawa Region, Tohoku Region, Chugoku Region, Hokkaido Region, Shikoku Region |

| Companies Covered | SCREEN Graphic Solutions Co., Ltd., Tokyo Kikai Seisakusho, Ltd., CTC Japan, LTD., Kido Packaging, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the Japan digital printing market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the Japan digital printing market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the Japan digital printing industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Japan Digital Printing Market Report

The Japan digital printing market reached USD 1.46 Billion in 2025, supported by short-run printing demand, e-commerce packaging customization, and rising fabric and ceramic application adoption.

The market is projected to reach USD 2.51 Billion by 2034, growing at a CAGR of 6.24% during 2026-2034, driven by inkjet technology adoption and sustainable ink migration.

Inkjet technology leads with a 72.6% share in 2025, supported by versatility across paper, fabric, plastic, ceramic, and glass substrates and ongoing investment by domestic Japanese OEMs.

Paper and books dominate at 28.9% in 2025, driven by short-run book publishing, on-demand textbook reprints, and self-publishing platform demand across Japan's mature publishing industry.

The Kanto Region leads with a 38.7% share in 2025, anchored by Tokyo's publishers, advertising agencies, e-commerce brand owners, and electronics packaging clusters across Saitama and Kanagawa.

Key drivers include short-run printing demand, e-commerce personalized packaging, sustainable ink migration, customization trends, and continuous innovation by domestic press OEMs in industrial inkjet platforms.

The Kansai/Kinki Region is among the fastest-growing, supported by Osaka packaging converters, Kyoto textile and ceramic industries, and Kobe-based apparel brands expanding into digital fabric printing.

Leading companies include SCREEN Graphic Solutions Co., Ltd., Tokyo Kikai Seisakusho, Ltd., CTC Japan, LTD., and Kido Packaging, alongside numerous regional print service providers.

Laser printing holds 27.4% in 2025, sustained by office documentation, transactional printing, and high-volume monochrome runs where speed and crisp text quality are valued by enterprise customers.

Direct-to-fabric inkjet adoption is rising due to apparel customization, short-run fashion, home textile demand, and reduced inventory risk needs among Japanese D2C brands and home textile producers.

AI-driven colour management, cloud-based RIP, IoT-enabled press monitoring, and hybrid digital-offset setups are improving productivity and turnaround times across print service providers. While efficiency gains are widely reported, specific improvements vary by application and are not consistently standardized across industry studies.

Plastic film and foil packaging at 21.7% leads packaging applications, with food, cosmetics, and pharmaceutical brand owners increasingly adopting digital printing for personalized SKUs and short-run promotions.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)