Japan E-Commerce Market Size, Share, Trends and Forecast by Type, Transaction, and Region 2026-2034

Japan E-Commerce Market Size & Forecast 2026-2034

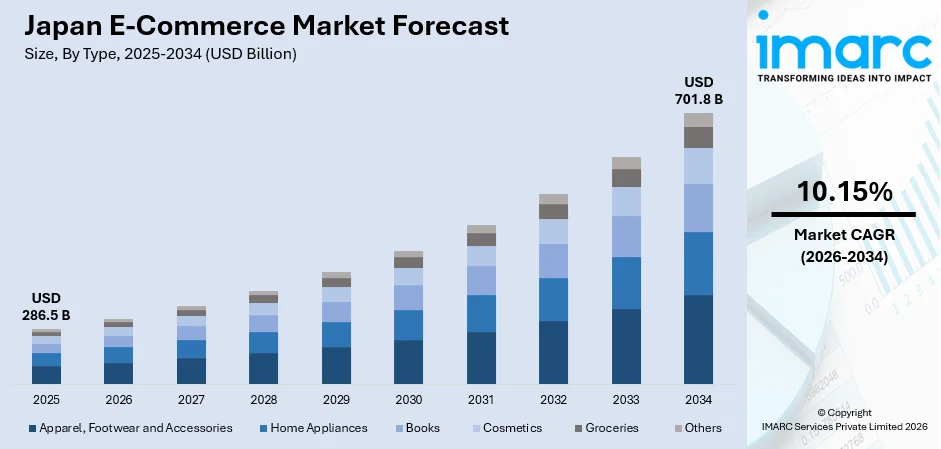

The Japan e-commerce market size, valued at USD 286.5 Billion in 2025, is projected to reach USD 701.8 Billion by 2034, growing at a CAGR of 10.15% from 2026-2034. The continuous investment in forefront logistical infrastructure, rising AI-based personalization adoption by key platforms, and growing international digital trade contributed to Japan's e-commerce market share. Additionally, the steady rise in domestic online sales points to long-term growth and wider adoption of digital retail in the country.

To get more information on this market Request Sample

Japan E-Commerce Industry Analysis - Key Insights

- Apparel, footwear and accessories command a 34.2% type share in 2025- Fashion and clothing contributed to the largest online product category in Japan, largely because younger and brand-conscious shoppers drive the major demand. Online platforms let people browse often, explore brands, and discover new styles.

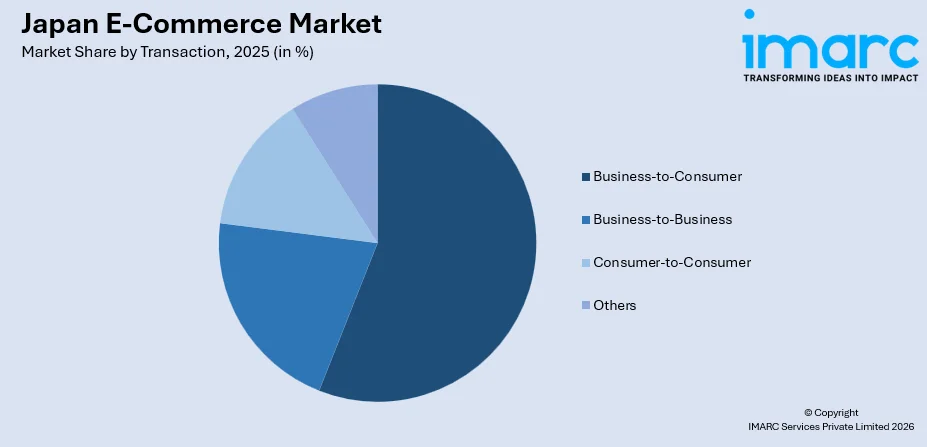

- Business-to-consumer leads transaction at 55.7% in 2025- Business-to-consumer (B2C) is the dominant e-commerce model in Japan, with popular platforms like Rakuten Ichiba leading the major market. Years of creating effective online shopping systems have made it easy for people to buy online, helping B2C to remain at the centre of the market.

- Kanto Region commands 40.3% of the Japan e-commerce market in 2025- Greater Tokyo is the headquarters of Japan's three largest e-commerce platforms namely, Rakuten, Amazon Japan, and LY Corporation. With a household internet penetration rate of 91.4% in 2024, as per Ministry of Internal Affairs and Communications, Kanto is not only Japan's largest consumer market but also the main hub of its digital retail economy.

Japan E-Commerce Market Trends and Dynamic 2026

Market Trends

Mobile Commerce Dominance Reshaping Japan's E-Commerce Architecture

Japan’s mobile commerce, which is valued at 6.7 trillion Yen in 2024, is majorly fuelled by high smartphone adoption, with 71% of consumers shopping via mobile. However, 41% of purchases still remained on Personal computer’s due to an aging population. Companies are making their apps better by adding features like one-click checkout, biometric authentication, and personalized engagement. These features are helping in the market growth

AI-Driven Personalization Elevating the Japanese Online Shopping Experience

Artificial intelligence and machine learning are changing how e-commerce market works in Japan by offering product recommendations based on what customers like and how they shop. Many companies are using AI shopping assistants that communicate with customers and give them real-time advice. These tools help buyers to find products more easily, stay interested, and simplify online shopping.

Cross-Border E-Commerce Expansion Connecting Japan to Global Marketplaces

Japan is quickly becoming a larger player in global cross-border e-commerce market. This growth comes from the popularity of Japanese brands, a weaker currency that makes prices more attractive to overseas buyers, and new investments in international shipping and local shopping options. Japan's Ministry of Economy, Trade and Industry (METI) revealed in its 2024 e-commerce industry survey that Chinese consumers made 2.6372 trillion yen in cross-border purchases from Japanese company operators in 2024, which is an 8.5% rise over the previous year.

- Loyalty Point Economy Deepening Platform Stickiness: Country’s e-commerce rewards schemes, such as Rakuten Super Points, PayPay points, and d-Point, rewards customers for repeat purchases as they keep using the same platforms. This strategy helps maintain high repeat transaction rates.

- Social Commerce and Live-Stream Shopping Emerging: Many platforms like 17Live, Mercari Shops, and TikTok Japan are attracting younger generations who use social media to find products before making a purchase in the same online space, combining entertainment with transactional commerce

- Subscription Commerce and Auto-Replenishment Growing: Rakuten Continuous Delivery and Amazon's Subscribe-and-Save features are gaining popularity for groceries, cosmetics, and household goods. These services are generating consistent recurring revenue streams for platform operators.

- Omnichannel Integration Accelerating: leading Japanese retailers like Aeon, Ito-Yokado, and Yodobashi Camera now offer click-and-collect, in-store pickup lockers, and micro-fulfilment services. Because of these changes, the difference between physical and digital retail channels is becoming less obvious.

.webp)

Growth Drivers

High Internet Penetration and Smartphone Adoption Creating Vast Online Consumer Base

The digital infrastructure and broad internet access in Japan are fuelling the market growth of e-commerce. This is because 117.3 million people (94.9% of the population), use the internet, and 90.6% of Japanese households own a smartphone. As a result, 58.7% of online purchases are made on mobile devices, making mobile commerce the norm and setting the stage for further e-commerce growth in Japan.

World-Class Logistics Infrastructure Enabling Fast, Reliable Fulfilment

Japan’s e-commerce market enjoys a well-developed logistics ecosystem, with reliable deliveries, urban fulfilment centres, and pick-up options at convenience store. Amazon Japan invested 1.2 trillion yen (USD 8 billion) in 2023. This investment enabled next- and same-day delivery, supporting USD 27.4 billion revenue in 2024, a 5.3% increase, highlighting logistics-driven consumer retention and sales growth.

Government-Backed Cashless and Digital Payment Expansion Lowering Transaction Friction

Japan’s government continues promoting cashless payments through incentives and supportive regulation, accelerating digital payment adoption. Integration of major payment apps into unified mobile wallets has reduced checkout friction for online shopping, while the expanding loyalty-points ecosystem further incentivizes digital transactions, strengthening long-term growth prospects for Japan’s e-commerce market.

- Rapidly Aging Population Embracing Online Convenience: As Japan's over-65 population is expected to account for 29.3% of the nation's population in 2024, they are increasingly embracing online shopping due to voice-assisted navigation, family-linked accounts, and same-day delivery windows that can accommodate schedules convenient for retiree.

- Rising Cross-Border Export Demand for Japanese Goods: Due to the declining value of the yen and the rising demand for country’s consumer electronics, fashion, food, and cosmetics worldwide, online platforms such as Mercari and Rakuten Ichiba are investing heavily in infrastructure for international sellers.

- Corporate Digital Transformation and B2B Procurement Digitalization: According to METI's FY2024 survey, B2B e-commerce sector in Japan increased by 10.6% reaching 514.4 trillion yen in 2024, due to an increase in mid-sized firms adoption of e-catalogue procurement directly into ERP workflows.

- New Platform Entrants Expanding Market Addressability: As SHEIN and Temu aggressively entered the market, underserved consumer segments that are price-conscious and entertainment-driven can now shop online, while TikTok's April 2025 e-commerce test in Japan has expanded online addressability.

Market Restraints

Last-Mile Logistics Complexity in Rural and Semi-Urban Japan: Geographical diversity and an aging population in Japan are causing costly last-mile delivery challenges in non-metropolitan areas. Driver shortages, low delivery densities, and geographical difficulties are resulting high cost for fulfilling orders in these regions. Additionally, cash-on-delivery is still being used in these regions, causing operational complexities.

Data Privacy and Cybersecurity Concerns Limiting Consumer Trust: Japanese consumers have high regard for data privacy and platform security. Thus, trust becomes a significant factor in e-commerce platform use. APPI compliance, especially in international data handling, adds complexity to business operations and may hinder platform development, whereas consumer sentiment towards data exchange may impact platform engagement.

Platform Dependency and High Commission Structures Constraining SME Participation: Japan’s e-commerce market is highly concentrated among major platforms, where commission fees, advertising costs, and algorithm-driven visibility create financial pressure for SME sellers. Regulatory requirements mandating greater transparency and compliance have increased operational costs for platforms and merchants, further tightening margins for smaller retailers operating within the digital marketplace ecosystem.

Japan E-Commerce Market Segmentation Analysis

| Segment Category | Leading Segment | Market Share | Year |

|---|---|---|---|

|

Type |

Apparel, Footwear and Accessories |

34.2% |

2025 |

|

Transaction |

Business-to-Consumer |

55.7% |

2025 |

|

Region |

Kanto Region |

40.3% |

2025 |

Type Insights

Apparel, Footwear and Accessories - 34.2% market share (2025) | Leading Type

Apparel, footwear, and accessories dominates the Japan’s e-commerce segment as online platforms enhance product discovery and convenience compared to physical retail. Fashion marketplaces aggregate extensive brand selections, while adoption of virtual try-on and digital visualization technologies reduces purchase uncertainty, encouraging consumers to shift clothing purchases from stores to online channels.

Segment BreakdownApparel, Footwear and Accessories (34.2%) · Home Appliances · Books · Cosmetics · Groceries · Others |

Transaction Insights

Access the comprehensive market breakdown Request Sample

Business-to-Consumer - 55.7% market share (2025) | Leading Transaction

Business-to-consumer leads Japan’s e-commerce market due to strong platform infrastructure, consumer trust, and advanced logistics networks. Major marketplaces continue expanding services beyond retail into healthcare and daily essentials, reinforcing consumer reliance on platform-based purchasing and supporting sustained dominance of the B2C model despite growth in alternative commerce formats.

Segment BreakdownBusiness-to-Consumer (55.7%) · Business-to-Business · Consumer-to-Consumer · Others |

Regional Insights

Kanto Region - 40.3% market share (2025) | Leading Region

Kanto leads Japan’s e-commerce market, serving as the biggest consumer region and the main hub for digital retail. Major platforms such as Amazon Japan, Rakuten Group, and LY Corporation (Yahoo! Shopping) make up 55–60% of 2025 consumer e-commerce gross merchandise. Their headquarters, engineering, and logistics centers are mostly located in the Greater Tokyo area.

|

Metric

|

Details

|

|---|---|

| Market Share in 2025 | 40.3% |

| Major Prefectures | Tokyo, Kanagawa, Saitama, Chiba, Ibaraki, Tochigi, Gunma |

| Key Growth Drivers | Headquarters of all three major e-commerce platforms, dense fulfilment infrastructure, highest household disposable income, 91.4% household internet penetration |

| Outlook | Sustained structural dominance through 2034 |

Regional BreakdownKanto Region (40.3%) · Kinki Region · Central/Chubu Region · Kyushu-Okinawa Region · Tohoku Region · Chugoku Region · Hokkaido Region · Shikoku Region |

Market Outlook (2026-2034)

What is the future outlook of the Japan e-commerce market?

The Japan e-commerce market is expected to sustain steady revenue growth through 2034.

Japan’s e-commerce market is expected to keep growing steadily through 2034. Key growth factors that are fuelling the market is retail digitalization, more mobile shopping, and greater use of AI for personalization. Other major drivers include cashless payments, cross-border trade, and new formats such as social commerce, quick commerce, and immersive digital shopping.

Japan E-Commerce Market - Leading Key Players

Japan's e-commerce competitive landscape is anchored by three dominant national platforms- Amazon Japan, Rakuten Ichiba, and LY Corporation's Yahoo! Shopping, that together control an estimated 55–60% of consumer gross merchandise value, alongside specialist vertical players including ZOZO for fashion and Mercari for C2C recommerce. Companies are working hard to stand out by using AI for personalisation, speeding up logistics, building loyalty programs, and expanding into international markets to protect and grow their market share.

| Company | Leading Brands/Products | Highlights |

|---|---|---|

|

ZOZO, Inc. |

ZOZOTOWN, ZOZOCOSME, WEAR |

The company specializes in clothing and lifestyle products and has built a domestic online fashion presence. Additionally, the company is expanding its global presence by acquiring Lyst, a UK-based fashion discovery platform, to expand cross-border digital fashion engagement. |

|

Mercari, Inc. |

Mercari, Merpay, Mercoin |

The top consumer-to-consumer (C2C) marketplace platform in Japan, which links buyers and sellers of used goods, maintains a sizable domestic user base while developing cross-border commerce capabilities through global platform initiatives. This allows customers from other countries to purchase Japanese resale goods and promotes the expansion of recommerce and circular economy transactions. |

|

DMM.com LLC |

DMM Shopping, DMM Books, DMM Games |

One of Japan's most popular e-commerce sites, this diverse platform has over 45 million members as of February 2024 and is strong in digital goods, video on demand, and specialized specialty retail. |

Some of the major players in the Japan e-commerce market include Rakuten Group Inc., Amazon Japan G.K., LY Corporation (Yahoo! Shopping), and others.

Latest Development & News

- In January 2026, Google Wallet has completed a phased rollout in Japan, enabling commuters to use their PayPay balances directly for transit payments and tap their smartphones at train and subway gates without requiring separate transport or card payment methods.

- In September 2025, Mercari has launched its Global App, letting consumers outside Japan to browse on Japan’s large second-hand goods marketplace. The app simplifies shopping and eliminates common problems such as language barrier, payment issues, and complex buying steps.

- In April 2025, ZOZO Inc. has purchased Lyst, a United Kingdom based fashion search and discovery platform, for USD 154 million. This exhibits the largest international purchase by a Japanese fashion e-commerce company in recent years. With this deal, ZOZO can now reach Lyst’s established customer base in Europe and North America.

Japan E-Commerce Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical and Forecast Trends, Industry Catalysts and Challenges, Segment-Wise Historical and Predictive Market Assessment:

|

| Types Covered | Home Appliances, Apparel, Footwear, and Accessories, Books, Cosmetics, Groceries, Others |

| Transactions Covered | Business-to-Consumer, Business-to-Business, Consumer-to-Consumer, Others |

| Regions Covered | Kanto Region, Kinki Region, Central/ Chubu Region, Kyushu-Okinawa Region, Tohoku Region, Chugoku Region, Hokkaido Region, Shikoku Region |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the Japan e-commerce market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the Japan e-commerce market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the Japan e-commerce industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Japan E-Commerce Market Report

The Japan e-commerce market reached a value of USD 286.5 Billion in 2025.

The market is projected to grow at a CAGR of 10.15% during 2026-2034, reaching USD 701.8 Billion by 2034.

Key growth drivers include widespread smartphone adoption, increasing internet penetration, advanced logistics, digital payment popularity, and changing consumer shopping behaviors.

The report covers segmentation by type, transaction, and region. Each segment includes detailed market size and forecast analysis.

Key trends include AI-driven personalization, mobile commerce expansion, social commerce growth, sustainable packaging, omnichannel integration, and cross-border online shopping.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)