Japan Pharmacy Automation Market Size, Share, Trends and Forecast by Product Type, Application, End User, and Region, 2026-2034

Japan Pharmacy Automation Market Size, Share, Trends & Forecast (2026-2034)

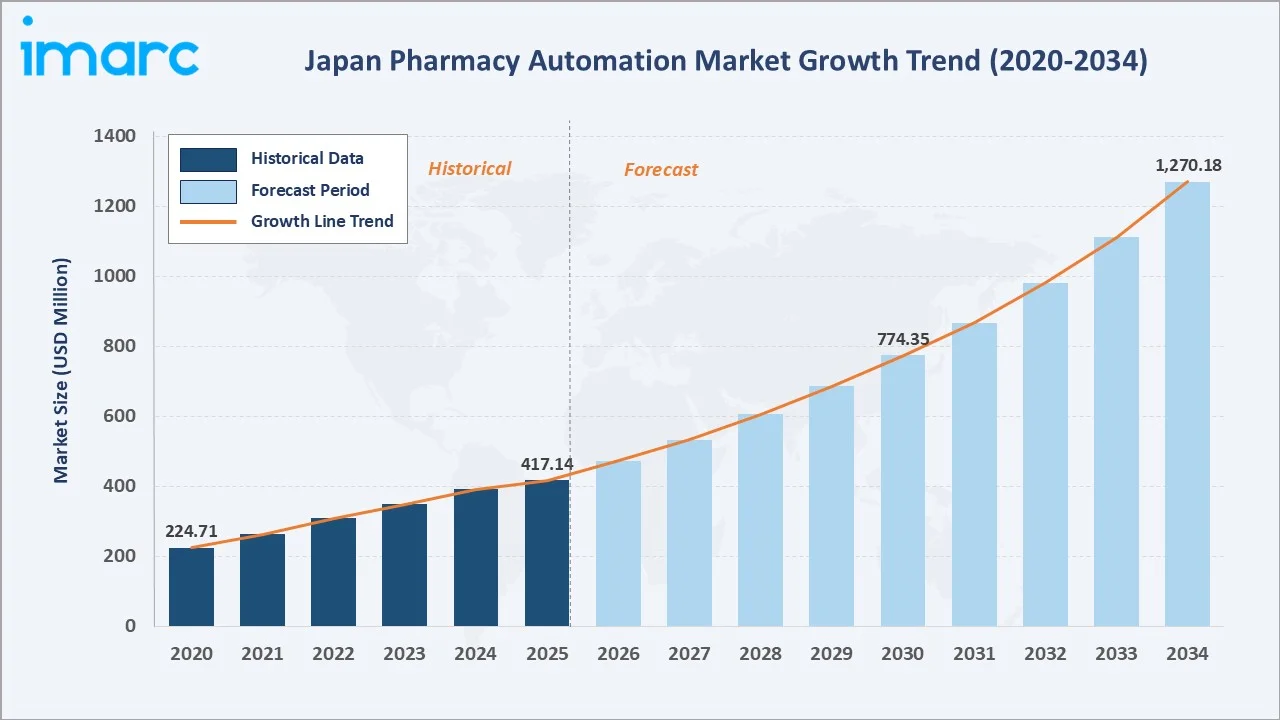

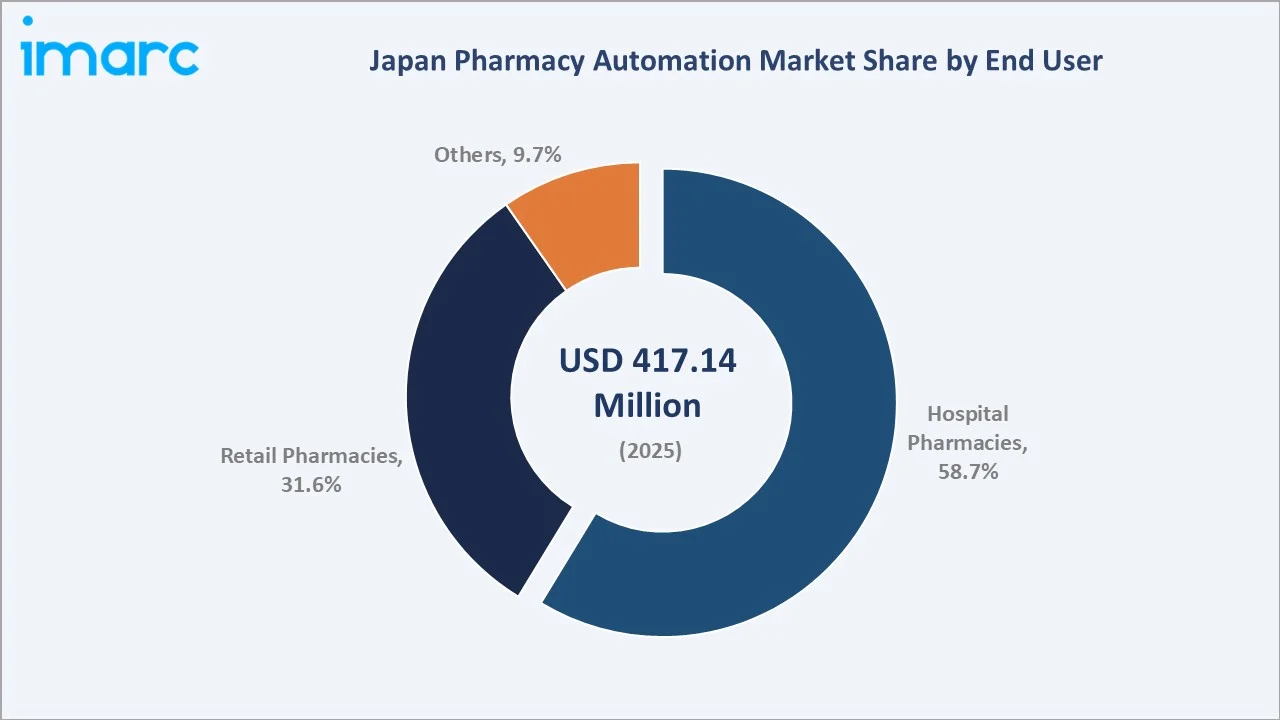

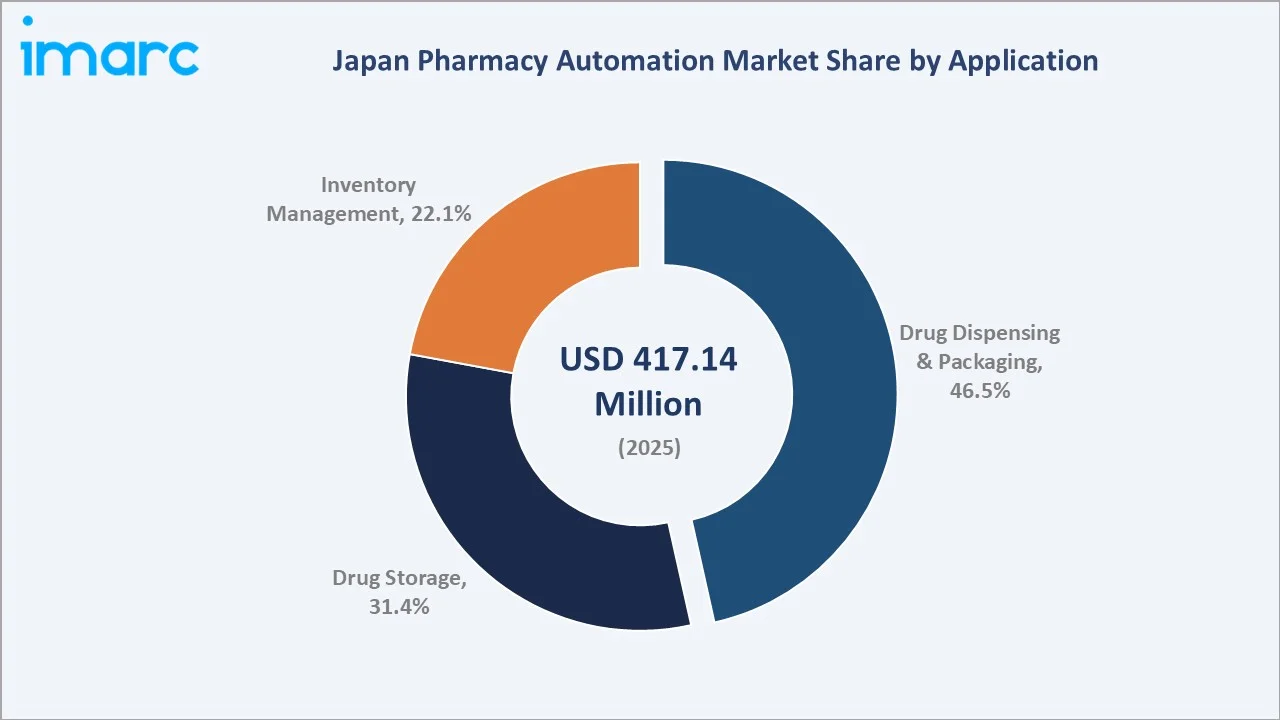

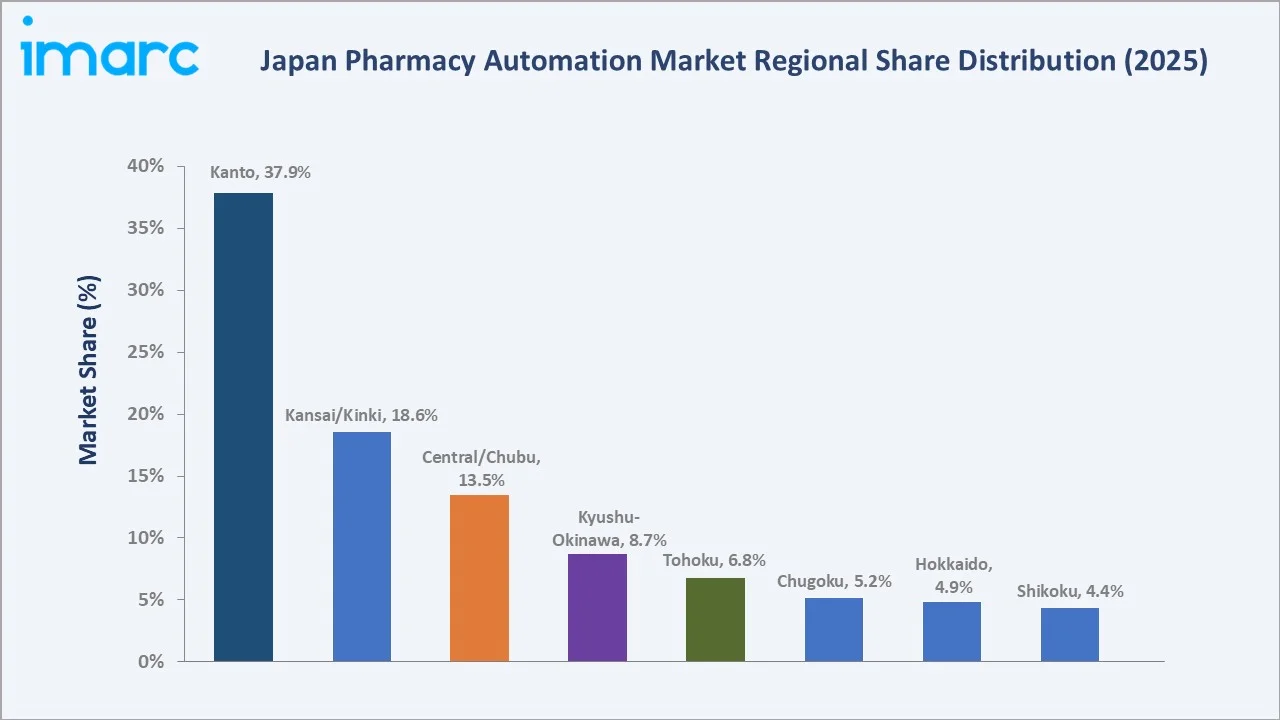

The Japan pharmacy automation market size was valued at USD 417.14 Million in 2025 and is projected to reach USD 1,270.18 Million by 2034, at a CAGR of 13.17% during 2026-2034. Rapid aging of the Japanese population, persistent hospital pharmacist shortages, government-led digital health reforms, and rising emphasis on medication safety are collectively driving Japan pharmacy automation market growth. Hospital Pharmacies dominate with a 58.7% share in 2025, while Drug Dispensing and Packaging accounts for 46.5% of the application mix. The Kanto Region leads with a 37.9% share in 2025.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 417.14 Million |

|

Forecast Market Size (2034) |

USD 1,270.18 Million |

|

CAGR (2026-2034) |

13.17% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

Kanto Region (37.9% share, 2025) |

|

Fastest Growing Region |

Kansai/Kinki Region |

|

Leading End User |

Hospital Pharmacies (58.7%, 2025) |

|

Leading Application |

Drug Dispensing & Packaging (46.5%, 2025) |

The chart below shows Japan pharmacy automation market growth from 2020–2034, supported by aging-population pressures, hospital labor shortages, and accelerating adoption of robotic dispensing systems through the forecast horizon.

To get more information on this market, Request Sample

CAGR analysis identifies Drug Dispensing and Packaging and Hospital Pharmacies as the fastest-growing segments in the Japan pharmacy automation market through 2034.

Executive Summary

The Japan pharmacy automation market is being reshaped by demographic strain, hospital workforce pressures, and the country's accelerating digital health agenda. Valued at USD 417.14 Million in 2025, the market is projected to reach USD 1,270.18 Million by 2034 at a 13.17% CAGR. Rising prescription volumes, an increasingly elderly patient base, and government incentives under Japan's Health and Medical Strategy are accelerating automation adoption across hospitals and retail pharmacy chains.

Hospital Pharmacies lead the market with a 58.7% share in 2025, supported by large prescription throughput at university and prefectural hospitals. Drug Dispensing and Packaging applications hold 46.5% of revenue, reflecting widespread deployment of automated tablet counters, sachet packagers, and robotic dispensing systems. Key trends include AI-enabled inventory analytics, cloud-based pharmacy management, and integrated closed-loop medication safety platforms.

The Kanto Region leads Japan's pharmacy automation market with a 37.9% share in 2025, anchored by Tokyo's dense hospital network and university medical centers. Kansai/Kinki follows with 18.6%, supported by Osaka-based equipment OEMs and a strong base of regional hospitals. Central/Chubu accounts for 13.5% and is gaining traction on the back of manufacturing-driven healthcare investment in Aichi prefecture.

Key Market Insights

|

Insight |

Data |

|

Largest End User Segment |

Hospital Pharmacies – 58.7% share (2025) |

|

Second End User Segment |

Retail Pharmacies – 31.6% share (2025) |

|

Leading Application |

Drug Dispensing & Packaging – 46.5% share (2025) |

|

Second Application |

Drug Storage – 31.4% share (2025) |

|

Leading Region |

Kanto Region – 37.9% (2025) |

|

Second Region |

Kansai/Kinki Region – 18.6% (2025) |

|

Top Companies |

Yuyama Co., Ltd., Tosho Inc., and Takazono Corporation |

|

Market Opportunity |

AI-enabled retail pharmacy automation in Tier-2 cities |

Key Analytical Observations Supporting the Above Data:

- Hospital Pharmacies' 58.7% dominance in 2025 reflects Japan's hospital-centric care model, with about 8,200 hospitals nationwide making automation essential for medication safety and pharmacist productivity.

- Retail Pharmacies at 31.6% in 2025 represent the fastest-expanding adoption frontier, as Welcia, Tsuruha, and Cosmos Pharmaceutical deploy tablet counters and robotic dispensing across thousands of stores.

- Drug Dispensing and Packaging at 46.5% in 2025 leads applications, driven by automated sachet packaging systems and tablet counters in hospital pharmacies to improve accuracy and workflow, with studies showing these technologies help reduce dispensing errors.

- Kanto Region's 37.9% lead in 2025 reflects concentration of university hospitals, advanced medical centers, and major pharmacy chain headquarters across Tokyo, Kanagawa, Saitama, and Chiba.

- Yuyama Co., Ltd. is a leading domestic supplier of pharmacy automation systems in Japan, with a long-standing presence in hospital dispensing since the 1960s.

Japan Pharmacy Automation Market Overview

Pharmacy automation refers to the deployment of robotic and software-driven systems that automate dispensing, packaging, storage, and inventory management within hospital and retail pharmacies. Solutions include automated medication dispensing systems, automated storage and retrieval systems, sachet packaging robots, and tabletop tablet counters. The Japanese ecosystem links domestic OEMs, software integrators, distributors, and end-user pharmacies under stringent PMDA and MHLW regulatory oversight.

Japan's pharmacy automation industry is shaped by demographic pressures, with 29.1% of the population aged 65 and above in 2024, the world's highest share. This drives prescription volumes upward and elevates the cost of medication errors. Government digitalization, telepharmacy expansion, and reimbursement-linked safety mandates are reinforcing structural demand.

Market Dynamics

To evaluate market opportunities, Request Sample

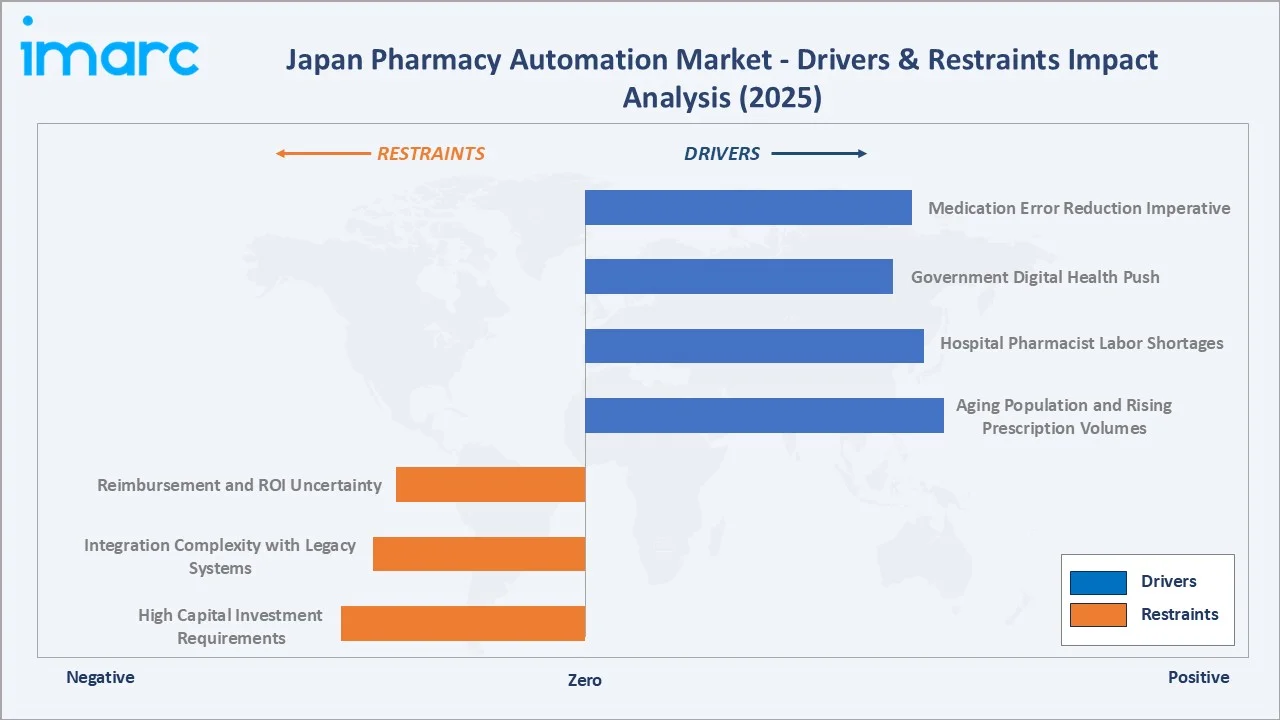

Market Drivers

- Aging Population and Rising Prescription Volumes: Japan's super-aged demographic, with around 36.2 million people above 65 in 2024, is sharply lifting prescription volumes. Polypharmacy among elderly patients intensifies pharmacy workload and automation demand.

- Hospital Pharmacist Labor Shortages: Pharmacist shortages, especially in rural Japan, are driving automation adoption to streamline dispensing workflows, reduce manual workload, and enable pharmacists to focus more on clinical and patient-care responsibilities.

- Government Digital Health Push: Japan's MHLW is advancing electronic prescriptions, hospital DX, and integrated medication records, making pharmacy automation a logical infrastructure investment aligned with national reforms.

- Medication Error Reduction Imperative: Reducing medication errors is a key driver, with automation improving dispensing accuracy and patient safety, encouraging adoption across hospitals and pharmacies despite limited Japan-specific quantification of error reduction rates.

Market Restraints

- High Capital Investment Requirements: High upfront investment in pharmacy automation systems limits adoption, particularly among small clinics and independent pharmacies, as capital-intensive solutions require significant financial commitment despite long-term efficiency benefits.

- Integration Complexity with Legacy Systems: Integration with legacy hospital IT systems is complex, requiring customization and slowing deployment timelines, which increases implementation challenges and discourages rapid adoption of pharmacy automation solutions.

- Reimbursement and ROI Uncertainty: Pharmacy automation lacks a dedicated reimbursement code under Japan's National Health Insurance, leaving hospitals to justify capex through indirect productivity benefits, slowing procurement decisions.

Market Opportunities

- AI-Enabled Inventory and Demand Forecasting: AI-driven inventory and demand forecasting solutions are gaining traction in hospital pharmacies, helping optimize stock management, reduce waste, and improve efficiency, creating new opportunities for automation vendors.

- Retail Chain Pharmacy Automation Rollouts: Large retail pharmacy chains with extensive store networks are expanding automation adoption, enabling scalable deployment of dispensing and verification systems across multiple locations, driving growth in the pharmacy automation market.

- Closed-Loop Medication Management Systems: Integrated platforms connecting prescribing, dispensing, and bedside administration with barcode verification represent a high-growth frontier as tertiary hospitals upgrade end-to-end medication safety.

Market Challenges

- Long Procurement Cycles: Hospital procurement in Japan involves multi-stage evaluations, approvals, and pilot testing, resulting in long decision cycles that delay adoption and revenue realization for pharmacy automation vendors.

- Aftermarket Service and Maintenance Demands: Vendors without nationwide service networks struggle to compete against incumbents with established prefectural support coverage critical for uptime-sensitive systems.

- Cybersecurity and Data Privacy Compliance: Pharmacy automation systems must comply with Japan’s strict data privacy laws and healthcare security guidelines, increasing compliance complexity and costs, particularly for cloud-based and connected solutions.

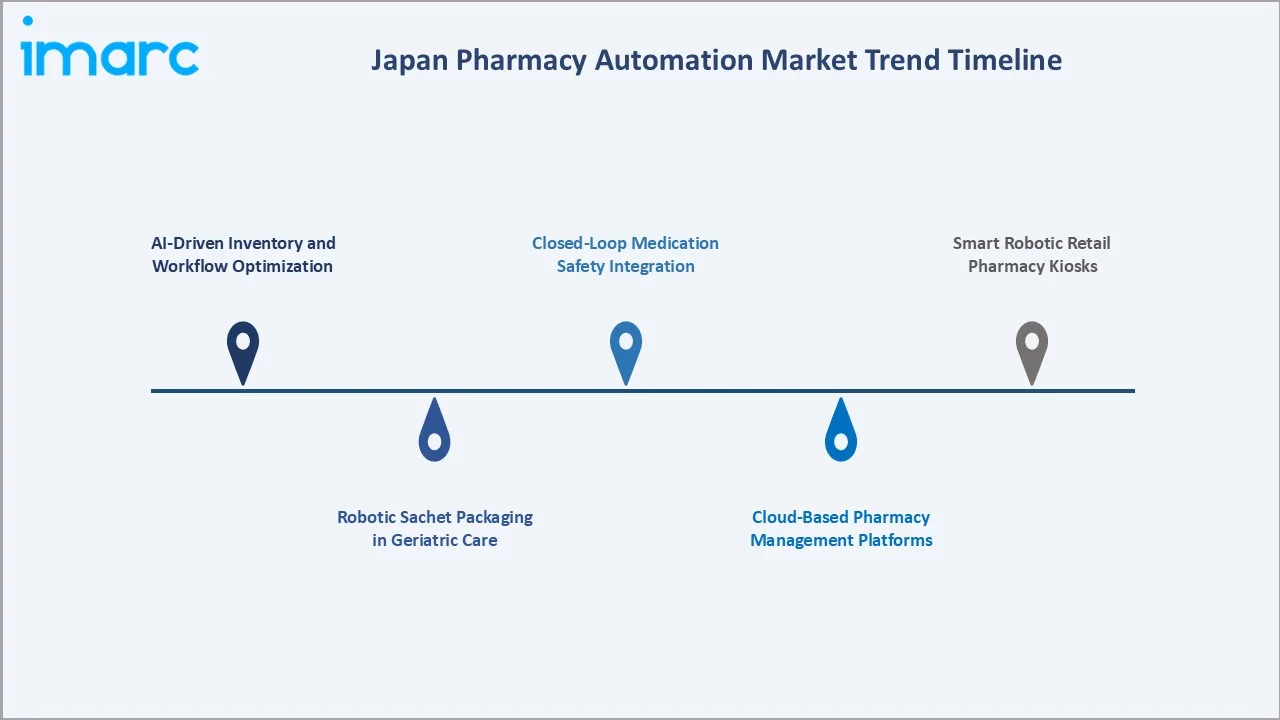

Emerging Market Trends

1. AI-Driven Inventory and Workflow Optimization

Japanese hospital pharmacies are deploying AI engines that analyze prescribing patterns, expiry risks, and demand variability. Vendors such as Yuyama and Tosho are embedding analytics into dispensing systems to reduce drug waste and improve replenishment cycles.

2. Robotic Sachet Packaging in Geriatric Care

Automated sachet packaging is widely used for elderly patients with multiple prescriptions, improving dosing accuracy and operational efficiency as Japan’s aging population increases demand for personalized medication dispensing.

3. Cloud-Based Pharmacy Management Platforms

Cloud-native platforms are gaining traction among multi-site retail chains, offering centralized inventory visibility, unified prescription analytics, and remote diagnostics. Adoption is accelerating in Tokyo and Osaka metro chains seeking nationwide standardization.

4. Closed-Loop Medication Safety Integration

Hospitals are adopting closed-loop medication systems integrating prescribing, dispensing, and barcode verification to enhance patient safety, reduce medication errors, and support broader healthcare digital transformation initiatives.

5. Smart Robotic Retail Pharmacy Kiosks

Self-service prescription kiosks integrating dispensing automation and remote pharmacist consultation are emerging in convenience-store-anchored pharmacies. Pilots across Tokyo and Yokohama are testing 24/7 prescription pickup models leveraging robotic dispensing technology.

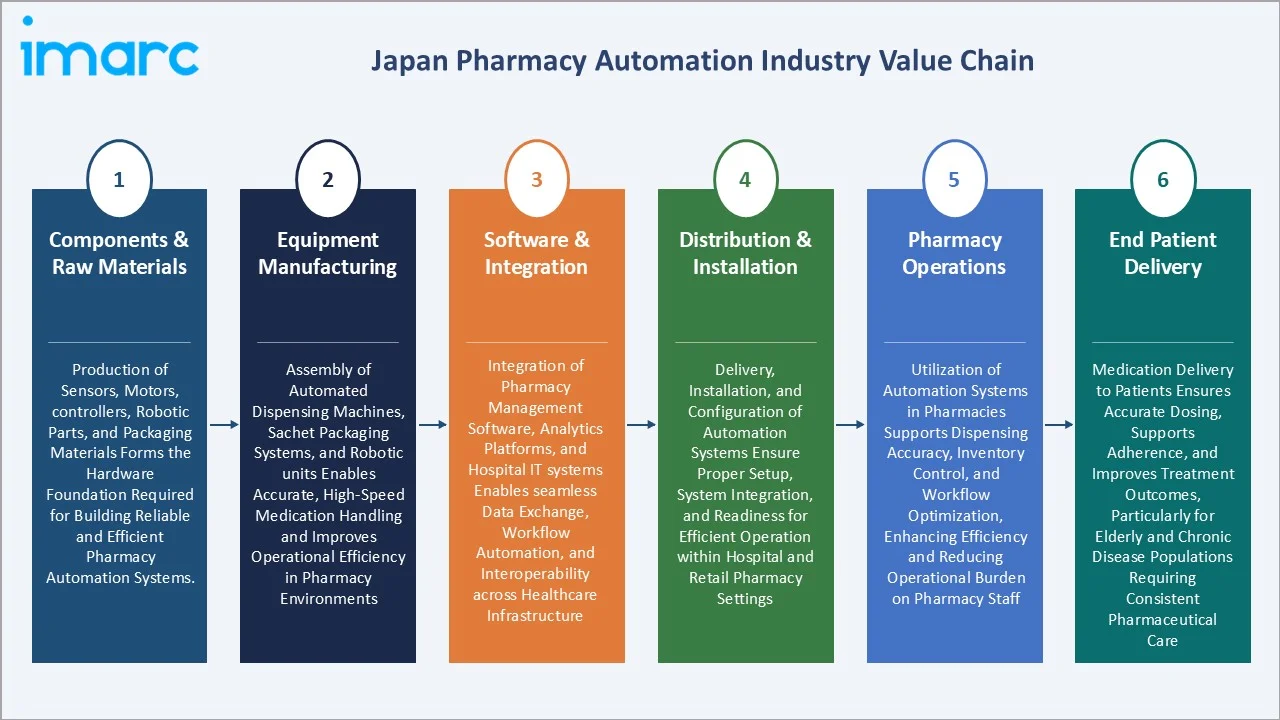

Industry Value Chain Analysis

The Japan pharmacy automation value chain spans six stages, from electronic and mechanical components through to medication delivery to patients, each with distinct cost structures, technological requirements, and competitive dynamics.

|

Stage |

Key Players / Examples |

|

Components & Raw Materials |

Production of sensors, motors, controllers, robotic parts, and packaging materials forms the hardware foundation required for building reliable and efficient pharmacy automation systems. |

|

Equipment Manufacturing |

Assembly of automated dispensing machines, sachet packaging systems, and robotic units enables accurate, high-speed medication handling and improves operational efficiency in pharmacy environments |

|

Software & Integration |

Integration of pharmacy management software, analytics platforms, and hospital IT systems enables seamless data exchange, workflow automation, and interoperability across healthcare infrastructure. |

|

Distribution & Installation |

Delivery, installation, and configuration of automation systems ensure proper setup, system integration, and readiness for efficient operation within hospital and retail pharmacy settings |

|

Pharmacy Operations |

Utilization of automation systems in pharmacies supports dispensing accuracy, inventory control, and workflow optimization, enhancing efficiency and reducing operational burden on pharmacy staff |

|

End Patient Delivery |

Medication delivery to patients ensures accurate dosing, supports adherence, and improves treatment outcomes, particularly for elderly and chronic disease populations requiring consistent pharmaceutical care. |

Japanese OEMs such as Yuyama and Tosho hold the highest value capture by integrating hardware design, proprietary packaging consumables, and aftermarket service. Their domestic service networks create barriers for global entrants attempting to compete on price alone.

Technology Landscape in the Pharmacy Automation Industry

Robotic Dispensing and Tablet Packaging

Robotic dispensing and tablet packaging systems automate counting, filling, and sachet preparation, improving accuracy and efficiency in pharmacies, though specific performance metrics vary across systems and healthcare settings.

AI and Machine Learning in Pharmacy Workflows

AI and machine learning are increasingly used to optimize inventory, detect prescription anomalies, and forecast demand, improving pharmacy efficiency, though quantified impact on waste reduction varies across implementations.

IoT-Connected Smart Storage and Retrieval

IoT-enabled automated storage and retrieval systems track temperature, humidity, and expiry in real time. Smart cabinets are increasingly standard in oncology and biologics-heavy hospital pharmacies across the Kanto and Kansai regions.

Cloud Platforms and Pharmacy Management Software

Cloud-based pharmacy management platforms enable multi-site analytics, centralized prescription auditing, and remote performance diagnostics. Major retail chains are migrating from on-premise to cloud architectures to support nationwide standardization.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Product Type |

🔒 |

🔒 |

2025 |

|

Application |

Drug Dispensing and Packaging |

46.5% |

2025 |

|

End User |

Hospital Pharmacies |

58.7% |

2025 |

|

Region |

Kanto Region |

37.9% |

2025 |

By End User

Hospital Pharmacies hold a 58.7% share in 2025, driven by large inpatient prescription volumes, complex polypharmacy regimens, and stringent medication safety mandates at university and prefectural hospitals. Tertiary care centers in Tokyo, Osaka, and Nagoya are leading adopters of integrated robotic dispensing platforms.

To access detailed market analysis, Request Sample

Retail Pharmacies account for 31.6% in 2025, with rapid expansion driven by chain consolidation among Welcia, Tsuruha, and Cosmos Pharmaceutical. Tabletop tablet counters and packaging automation are scaling across thousands of retail outlets nationally. Others, including long-term care, mail-order, and specialty pharmacies, hold 9.7% in 2025.

By Application

Drug Dispensing and Packaging holds 46.5% in 2025, leading the market, driven by high demand for automated dispensing, sachet packaging, and verification systems, with stronger adoption across large hospital pharmacy settings handling complex, high-volume workloads.

Drug Storage applications hold 31.4% in 2025, driven by automated storage and retrieval systems, refrigerated smart cabinets, and controlled substance vaults critical for biologics, oncology drugs, and narcotics. Inventory Management at 22.1% in 2025 is the fastest-evolving application, propelled by AI-driven analytics, expiry tracking, and demand forecasting.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

|

Kanto Region |

37.9% |

Tokyo's dense hospital network, university medical centers, headquarters of major pharmacy chains |

|

Kansai/Kinki Region |

18.6% |

Osaka-based OEMs (Yuyama, Takazono), strong hospital cluster, advanced retail pharmacy adoption |

|

Central/Chubu Region |

13.5% |

Aichi prefecture industrial healthcare investment, Nagoya tertiary hospitals, regional chain expansion |

|

Kyushu-Okinawa Region |

8.7% |

Fukuoka medical hub, growing hospital automation budgets, rural pharmacy modernization |

|

Tohoku Region |

6.8% |

Sendai academic medical center, post-2011 reconstruction-driven hospital infrastructure upgrades |

|

Chugoku Region |

5.2% |

Hiroshima and Okayama hospital adoption, mid-sized retail chain digitalization |

|

Hokkaido Region |

4.9% |

Sapporo hospital cluster, low-density geography supporting telepharmacy automation |

|

Shikoku Region |

4.4% |

Lower hospital density, rising adoption among prefectural hospitals and chain pharmacies |

The Kanto Region commands a 37.9% share in 2025, driven by Tokyo’s large hospital base and advanced healthcare infrastructure, with high prescription volumes and strong digital adoption supporting demand for pharmacy automation systems.

The Kansai/Kinki Region with 18.6% in 2025 is anchored by Osaka and Kyoto's hospital base, alongside the strategic presence of Yuyama and Takazono manufacturing operations, supporting strong domestic demand. The Central/Chubu Region at 13.5% in 2025 benefits from Aichi-led industrial healthcare investment and a growing tertiary hospital network around Nagoya.

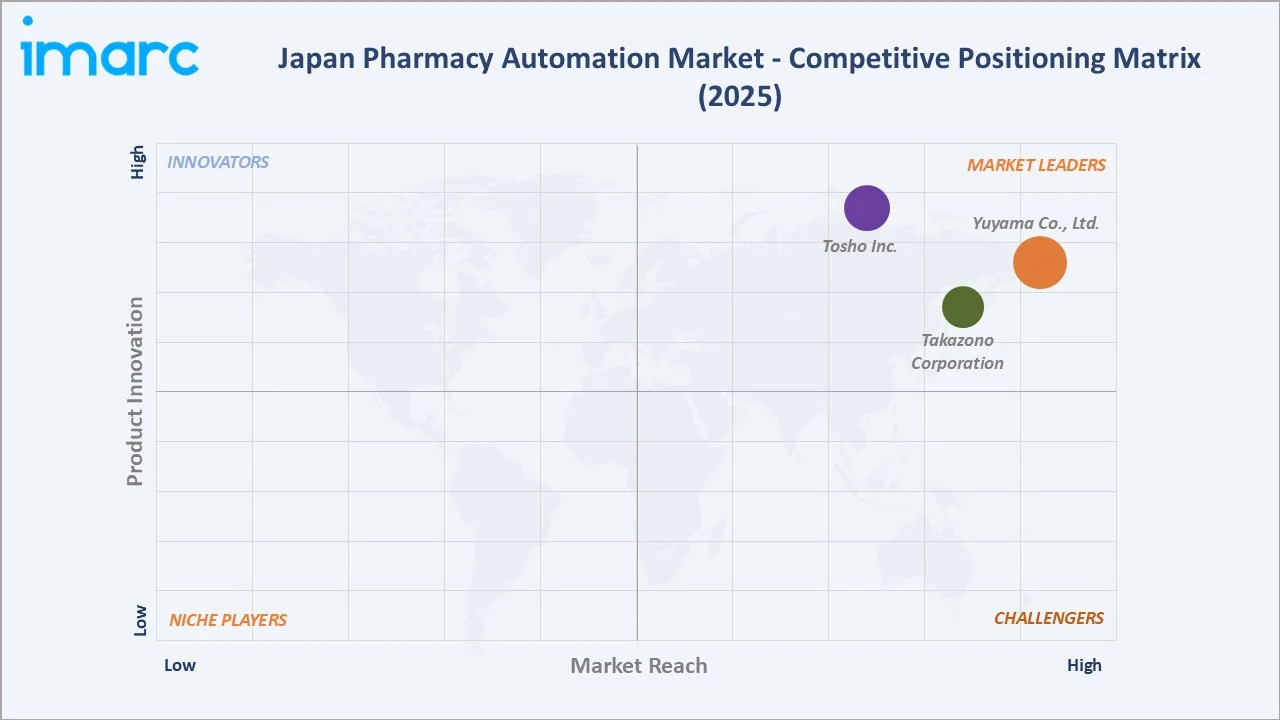

Competitive Landscape

|

Company Name |

Key Brand / Platform |

Market Position |

Core Strength |

|

Yuyama Co., Ltd. |

Yuyama |

Leader |

Domestic dominance, sachet packaging robotics, hospital integration |

|

Tosho Inc. |

Tosho / Xana |

Leader |

Hospital dispensing automation, retail pharmacy installations |

|

Takazono Corporation |

Takazono |

Leader |

Tablet packaging, hospital workflow systems |

The Japan pharmacy automation market is led by domestic OEMs Yuyama, Tosho, and Takazono, which collectively serve most Japanese hospital pharmacies. Yuyama Co. Ltd., the domestic leader, reported approximately Yen 480 billion in revenue in FY2024, supported by deep penetration in hospital pharmacy automation, decades of installed base, and a comprehensive prefectural service network across Japan.

Key Company Profiles

Yuyama Co., Ltd.

Yuyama Co., Ltd., headquartered in Toyonaka, Osaka, is a leading Japanese provider of pharmacy automation systems, specializing in dispensing and packaging technologies. The company serves hospitals and pharmacies domestically and internationally, with a strong presence across Asia and expanding global operations.

- Product & Service Portfolio: Yuyama offers automated tablet packaging machines (including ATC systems), sachet packaging systems (FastPack), automated dispensing systems, prescription filling support, and pharmacy workflow solutions integrated with hospital information and inventory management systems.

- Recent Developments: In December 2024, Yuyama Co., Ltd. launched the “Litrea-i” fully automatic compact tablet packaging machine with inspection support, featuring dual-side medication imaging, expanded cassette capacity, and compatibility with half-tablet cassettes to enhance accuracy and compact pharmacy workflows.

- Strategic Focus: Yuyama focuses on hospital and retail pharmacy automation expansion, AI-enabled workflow analytics, sachet packaging innovation, and global distribution scaling.

Tosho Inc.

TOSHO Inc., headquartered in Tokyo and part of the Toyota Tsusho Corporation group, is a leading provider of pharmacy automation systems in Japan, offering dispensing and packaging solutions for hospitals and retail pharmacies with strong nationwide service and installation capabilities.

- Product & Service Portfolio: TOSHO provides automated tablet packaging machines (Xana series), unit-dose dispensing systems, pharmacy automation equipment, and integrated workflow solutions designed for hospital and retail pharmacy operations.

- Recent Developments: In February 2025, TOSHO Inc. updated its Xana-100 tablet packaging system, highlighting its compact design for small pharmacy spaces while maintaining high-speed and reliable performance. The system features LED-guided semi-automatic conveyor filling, automatic cassette identification, and integration with the FILIA dispensing control system for improved workflow efficiency.

- Strategic Focus: TOSHO focuses on advancing pharmacy automation through high-efficiency dispensing and packaging systems, strengthening integration with healthcare workflows, and expanding adoption across hospitals and retail pharmacy networks in Japan.

Takazono Corporation

Takazono Corporation, headquartered in Osaka, is a Japanese manufacturer specializing in pharmacy automation systems, particularly tablet packaging machines. The company serves hospital and dispensing pharmacies in Japan and overseas, with a strong reputation for reliable, space-efficient automation solutions.

- Product & Service Portfolio: TPF tablet packaging robots, ATG automated dispensing machines, and pharmacy workflow systems addressing inpatient and outpatient hospital pharmacy operations.

- Recent Developments: In June 2023, Takazono Corporation advanced pharmacy automation by integrating IoT and imaging technologies to enhance medication identification, reduce human error, and improve patient safety. The company also emphasized digital transformation, compact packaging systems, and exploring new global opportunities in an evolving pharmaceutical distribution landscape.

- Strategic Focus: Takazono focuses on packaging robotics innovation, mid-sized hospital pharmacy adoption, and international expansion through distributor and OEM partnerships.

Market Concentration Analysis

The Japan pharmacy automation market is moderately concentrated at the top, with Yuyama Co., Ltd., Tosho Inc., Takazono Corporation collectively accounting for approximately 55–62% of total market revenue in 2025, driven by their entrenched hospital relationships, decades-long installed bases, and prefectural service networks unmatched by international entrants.

The market becomes more fragmented at the retail pharmacy and software-integration levels, with multiple regional integrators, IT system vendors, and emerging analytics specialists serving niche workflow segments. International players such as BD (Becton, Dickinson and Company), Omnicell, Inc., and Swisslog Healthcare are primarily focused on tertiary hospital automation and closed-loop medication management systems.

Consolidation trends are emerging through software acquisitions, with domestic OEMs increasingly partnering with AI and cloud analytics vendors to deepen digital differentiation. Strategic alliances between equipment manufacturers and pharmacy chains for nationwide rollouts are also accelerating, reinforcing the competitive moats of established Japanese players.

Investment & Growth Opportunities

Fastest-Growing Segments

Drug Dispensing and Packaging is projected to remain the fastest-growing application segment through 2034, supported by aging-driven prescription volume growth, retail chain pharmacy automation, and adoption of robotic sachet packaging. Hospital Pharmacies will continue to dominate end-user demand, with tertiary hospital upgrades unlocking sustained capital expenditure cycles.

Emerging Regional Markets

The Kyushu-Okinawa, Tohoku, and Hokkaido regions, together holding 20.4% of the market in 2025, represent the highest-growth opportunity zones, driven by hospital infrastructure upgrades, prefectural government healthcare investments, and underpenetrated retail pharmacy chains transitioning to automated dispensing.

Venture & Strategic Investment Trends

Investment activity in pharmacy automation software is intensifying, with venture capital flowing into AI-driven inventory analytics, cloud-based pharmacy management platforms, and retail kiosk automation startups. Strategic corporate investments by Toyota Tsusho, NEC, and Fujitsu Healthcare are reinforcing the domestic ecosystem's digital capabilities through 2030.

Future Market Outlook (2026-2034)

The Japan pharmacy automation market forecast projects sustained value expansion from USD 417.14 Million in 2025 to USD 1,270.18 Million by 2034 at a CAGR of 13.17%, representing a value increase of over USD 853 Million through the forecast period. Growth will be driven by aging-population demand, hospital labor shortages, MHLW digital health reforms, and expanding retail chain automation rollouts.

Three transformational shifts will reshape the market through 2034. First, AI-enabled pharmacy workflow optimization will become standard across tertiary hospitals. Second, closed-loop medication management integrating prescription, dispensing, and administration will accelerate among university hospitals. Third, cloud-based platforms will replace fragmented on-premises systems, enabling multi-site retail chains to standardize and scale automation efficiently.

By 2034, pharmacy automation in Japan is expected to evolve from standalone dispensing equipment into a fully integrated, AI-enabled, and cloud-orchestrated medication safety platform. Vendors investing in software, analytics, and end-to-end integration will capture disproportionate value, while traditional hardware-only suppliers face mounting pressure to digitalize their offerings.

Research Methodology

Primary Research

Primary research included structured interviews with hospital pharmacy directors at university and prefectural hospitals, retail pharmacy chain procurement leads at Welcia, Tsuruha, Cosmos Pharmaceutical, and Sundrug, equipment OEM executives at Yuyama, Tosho, and Takazono, and pharmacy IT integrators across Tokyo, Osaka, and Nagoya during 2024–2025.

Secondary Research

Secondary sources include MHLW (Ministry of Health, Labour and Welfare) publications, PMDA regulatory data, Japanese Society of Hospital Pharmacists reports, company annual reports of Yuyama, Tosho, BD, Omnicell, and Swisslog Healthcare, OECD healthcare statistics, and Japan Pharmaceutical Manufacturers Association industry briefs.

Forecasting Models

Market sizing and growth projections used a hybrid bottom-up and top-down approach, integrating hospital and retail pharmacy installation data, equipment ASP benchmarks, prescription volume trends, demographic projections, and macroeconomic indicators under base, optimistic, and conservative scenario analyses through 2034.

Japan Pharmacy Automation Market Report Coverage

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Scope of the Report | Exploration of Historical and Forecast Trends, Industry Catalysts and Challenges, Segment-Wise Historical and Predictive Market Assessment:

|

| Product Types Covered | Automated Medication Dispensing Systems, Automated Storage and Retrieval Systems, Automated Packaging and Labeling Systems, Tabletop Tablet Counters, Others |

| Applications Covered | Drug Dispensing and Packaging, Drug Storage, Inventory Management |

| End Users Covered | Hospital Pharmacies, Retail Pharmacies, Others |

| Regions Covered | Kanto Region, Kansai/Kinki Region, Central/ Chubu Region, Kyushu-Okinawa Region, Tohoku Region, Chugoku Region, Hokkaido Region, Shikoku Region |

| Companies Covered | Yuyama Co., Ltd., Tosho Inc., Takazono Corporation, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the Japan pharmacy automation market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the Japan pharmacy automation market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the Japan pharmacy automation industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Japan Pharmacy Automation Market Report

The Japan pharmacy automation market was valued at USD 417.14 Million in 2025, driven by aging demographics, hospital labor shortages, and rising prescription volumes.

The market is projected to reach USD 1,270.18 Million by 2034, growing at a CAGR of 13.17% during 2026-2034.

Hospital Pharmacies lead with a 58.7% share in 2025, supported by high inpatient prescription volumes and stringent medication safety mandates.

Drug Dispensing and Packaging holds 46.5% in 2025, reflecting widespread deployment of robotic sachet packagers, tablet counters, and dispensing systems.

The Kanto Region leads with a 37.9% share in 2025, anchored by Tokyo's hospital network and major pharmacy chain headquarters.

Key drivers include aging demographics, pharmacist shortages, MHLW digital health reforms, medication error reduction, and retail chain automation rollouts.

The Kansai/Kinki region is among the fastest-growing, supported by Osaka-based OEMs and accelerating retail pharmacy automation adoption.

Leading companies include Yuyama Co., Ltd., Tosho Inc., and Takazono Corporation, Among Others.

Retail Pharmacies hold 31.6% in 2025, driven by Welcia, Tsuruha, Cosmos Pharmaceutical, and Sundrug deploying tablet counting and dispensing automation.

Growth is driven by aging-related prescription volumes, polypharmacy management, robotic sachet packaging adoption, and medication safety regulations across hospitals.

Key challenges include high capital costs, legacy IT integration complexity, long procurement cycles, reimbursement uncertainty, and cybersecurity compliance.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)