Japan Security Market Size, Share, Trends and Forecast by System, Service, End User, and Region, 2026-2034

Japan Security Market Size, Share, Trends & Forecast (2026-2034)

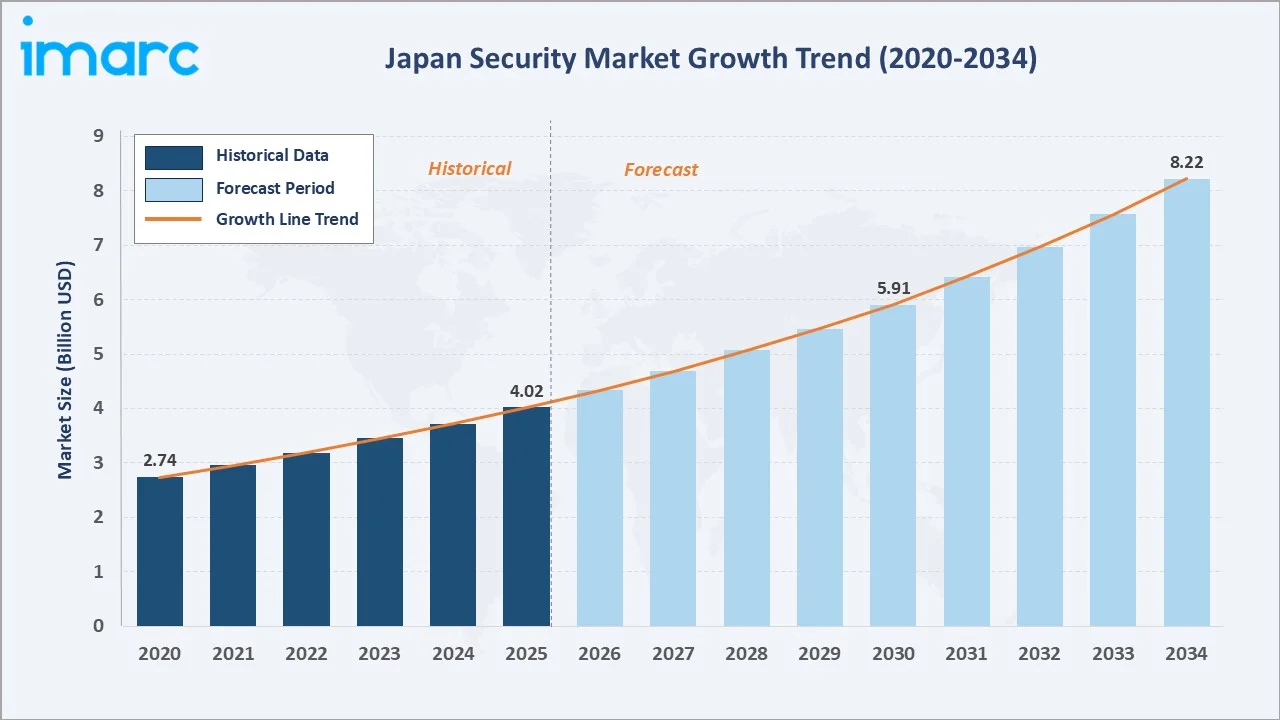

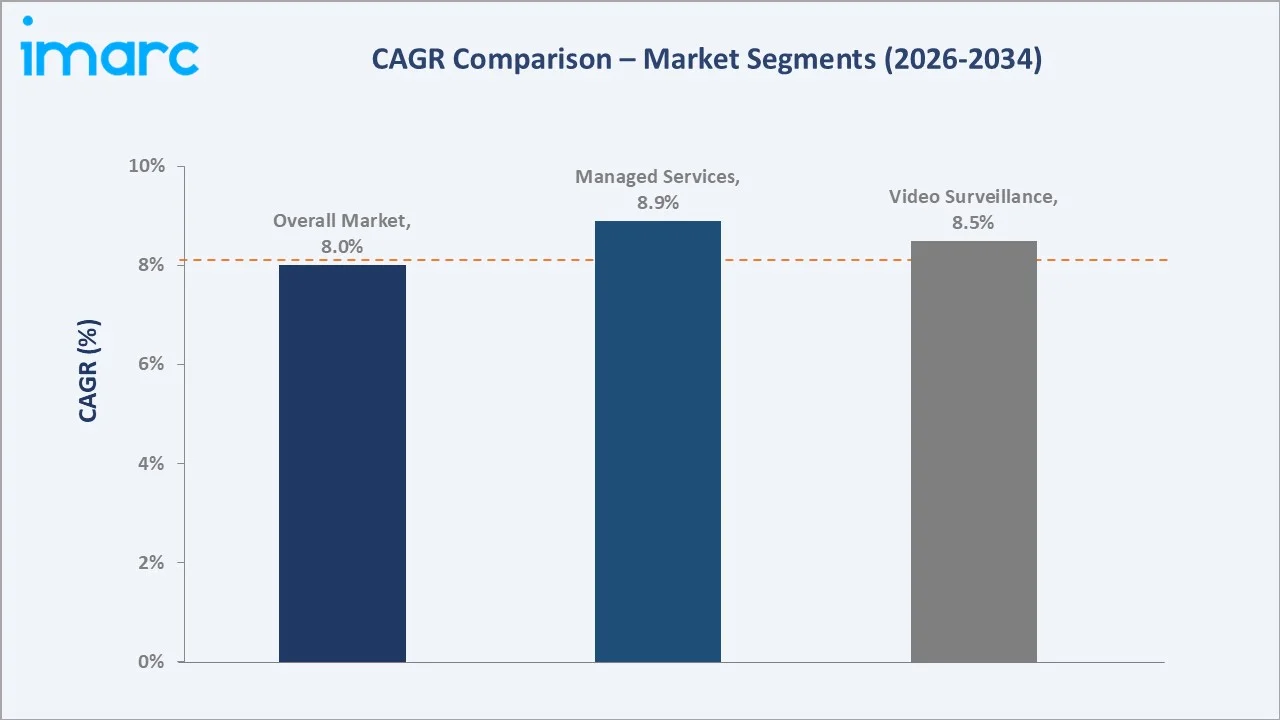

The Japan security market reached USD 4.02 Billion in 2025 and is projected to reach USD 8.22 Billion by 2034, growing at a CAGR of 8.02% during 2026-2034. The market is driven by rising public-safety spending, smart-city rollouts, and rapid adoption of AI-enabled video surveillance and cloud-based monitoring across enterprises, government facilities, and critical infrastructure. Video Surveillance Systems dominate the system segment at 29.8%. Managed Services lead services at 34.6%. The Government sector leads end users, and the Kanto Region commands 35.8% of the national market in 2025.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 4.02 Billion |

|

Forecast Market Size (2034) |

USD 8.22 Billion |

|

CAGR (2026-2034) |

8.02% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Dominant System |

Video Surveillance Systems (29.8%, 2025) |

|

Dominant Service |

Managed Services (34.6%, 2025) |

|

Leading Region |

Kanto Region (35.8%, 2025) |

The Japan security market expanded from USD 2.74 Billion in 2020 to USD 4.02 Billion in 2025, anchored at USD 5.91 Billion in 2030, and forecast to reach USD 8.22 Billion by 2034, supported by sustained investment in integrated, analytics-driven security infrastructure across public and private sectors.

To get more information on this market, Request Sample

Managed Services and Video Surveillance Systems are among the fastest-growing segments, while the Government end-user sector expands steadily as organizations consolidate fragmented tools into unified, AI-driven security platforms across the country.

Executive Summary

The Japan security market reached USD 4.02 Billion in 2025, representing a mature convergence of physical security, cybersecurity, and connected surveillance technology. The market spans hardware, software analytics, system integration, and recurring managed services delivered to enterprise, government, and infrastructure customers.

Video Surveillance Systems at 29.8% lead through dense urban camera deployment. Managed Services at 34.6% dominate services as organizations outsource monitoring. The Kanto Region, at 35.8%, leads through concentrated corporate, government, and transport infrastructure around Tokyo.

Key Market Insights

|

Insight |

Data |

|

Dominant System |

Video Surveillance Systems - 29.8% share (2025) |

|

Dominant Service |

Managed Services - 34.6% share (2025) |

|

Leading Region |

Kanto Region - 35.8% share (2025) |

|

Market Opportunity |

AI video analytics; smart-city surveillance; cloud-based access control; managed detection services; critical-infrastructure protection; disaster-resilient monitoring |

Key Analytical Observations Supporting The Above Data:

- Video Surveillance Systems at 29.8%: Video surveillance leads due to extensive urban camera deployment, transport-network coverage, and the shift toward high-resolution IP cameras with edge analytics for real-time threat detection and crowd management across Japanese cities.

- Managed Services at 34.6%: Managed services dominate as enterprises and public agencies outsource continuous monitoring and response, reducing in-house staffing pressures amid a shrinking, aging workforce and rising operational and compliance complexity.

- Kanto Region at 35.8%: Kanto leads on the concentration of corporate headquarters, government facilities, and dense transit infrastructure around Tokyo, driving sustained demand for integrated, high-specification security systems.

Japan Security Market Overview

The Japan security market encompasses the design, supply, integration, and operation of electronic and physical security systems protecting people, assets, and infrastructure. It spans surveillance, access control, intrusion detection, alarms, barriers, and associated professional and managed services.

Macro factors include heightened public-safety awareness, government smart-city and disaster-resilience programs, and an aging population increasing reliance on remote monitoring. Rapid digitalization and cyber-physical convergence further accelerate adoption of cloud-based, analytics-driven security solutions nationwide.

Market Dynamics

To evaluate market opportunities, Request Sample

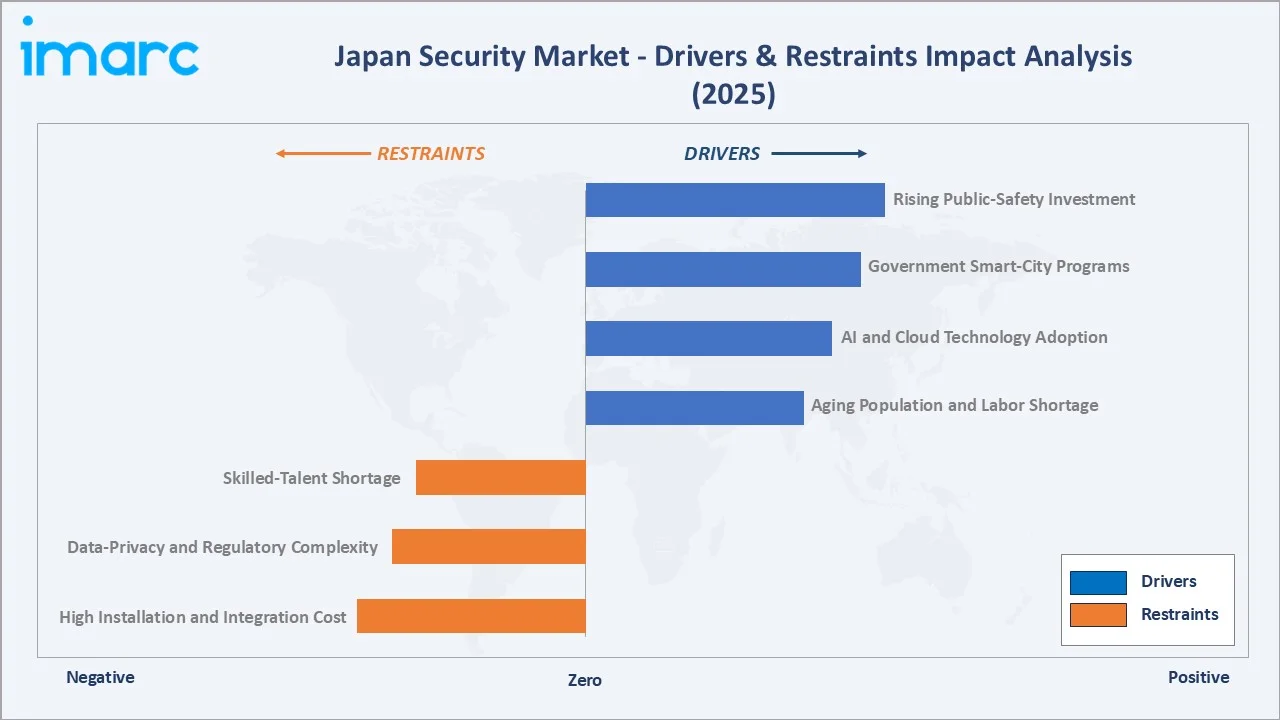

Market Drivers

- Rising Public-Safety Investment: Persistent public-safety priorities and urban crime prevention are increasing security budgets across municipalities, transport operators, and commercial property owners, driving broad deployment of surveillance and access-control systems throughout Japan's dense metropolitan areas.

- Government Smart-City Programs: National smart-city, Society 5.0, and critical-infrastructure protection initiatives are embedding connected security into public projects, expanding demand for integrated surveillance, sensor networks, and centralized command platforms across cities and utilities.

- AI and Cloud Technology Adoption: Growing adoption of AI video analytics, facial recognition, and cloud-based monitoring enables real-time detection, automation, and scalability, encouraging enterprises to modernize legacy analog systems into intelligent, data-driven security platforms.

- Aging Population and Labor Shortage: A shrinking, aging workforce is intensifying demand for remote monitoring and managed services that reduce dependence on on-site guarding, supporting sustained growth in automated and outsourced security operations.

Market Restraints

- High Installation and Integration Cost: Advanced integrated systems require significant upfront investment in hardware, software, and integration, discouraging adoption among small and medium enterprises and slowing modernization in cost-sensitive segments across regional markets.

- Data-Privacy and Regulatory Complexity: Strict data-privacy rules and evolving surveillance regulation increase compliance complexity, particularly for facial recognition and cloud storage, constraining deployment scope and lengthening procurement cycles for public and private operators.

- Skilled-Talent Shortage: A shortage of skilled cybersecurity and systems-integration professionals limits the pace of advanced deployments, raising project costs and creating delivery bottlenecks for complex, converged security implementations nationwide.

Market Opportunities

- Cloud Managed Security Services: Cloud-based, analytics-led managed detection and response services present strong recurring-revenue opportunities as organizations shift from hardware ownership to subscription models supporting continuous, scalable, and cost-efficient security monitoring.

- Converged Cyber-Physical Platforms: Integrated cyber-physical platforms unifying surveillance, access, and network security offer differentiation, addressing rising demand for converged protection across critical infrastructure, data centers, and connected industrial environments.

Market Challenges

- Legacy System Integration: Interoperability gaps between legacy analog equipment and modern IP-based platforms complicate upgrades, increasing integration effort and cost while slowing migration to unified, analytics-capable security architectures.

- Cybersecurity of Connected Devices: Expanding connectivity increases exposure to cyber threats, requiring continuous investment in securing surveillance networks, cloud platforms, and connected devices against intrusion, data breaches, and operational disruption.

Emerging Market Trends

1. Migration from Analog to Cloud-Native IP Surveillance

Japanese operators are replacing analog CCTV with cloud-native IP systems offering remote access, scalable storage, and centralized management. This shift reduces on-premises infrastructure, improves footage quality, and enables integration with analytics for faster, more reliable incident response across sites.

2. AI Video Analytics Enabling Proactive Security Operations

AI-driven analytics for object detection, behaviour recognition, and anomaly alerts are transforming surveillance from passive recording into proactive prevention. Automated detection reduces monitoring workload, improves accuracy, and supports real-time decision-making across transport, retail, and public-safety environments.

3. Convergence of Physical Security and Cybersecurity

Organizations are unifying physical and cyber defences as connected devices blur traditional boundaries. Converged platforms provide holistic visibility, coordinated response, and stronger protection for critical infrastructure, aligning with Japan's growing focus on resilient, integrated security governance.

4. Growth of Subscription-Based Managed Security Services

Subscription and as-a-service models are expanding as enterprises seek predictable costs and continuous monitoring without heavy capital outlay. Managed providers deliver scalable surveillance, access, and detection services, strengthening recurring-revenue economics across the Japanese security landscape.

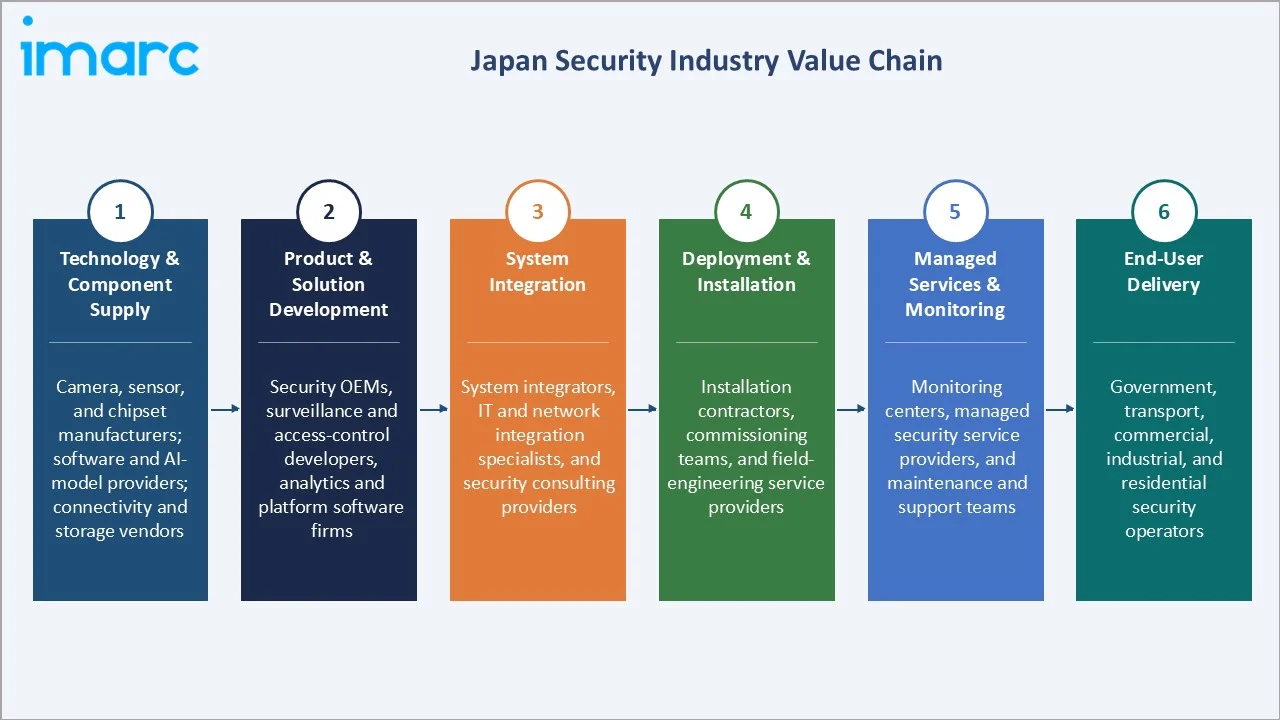

Industry Value Chain Analysis

The Japan security value chain integrates technology and component supply, product and solution development, system integration, deployment and installation, managed services and monitoring, and end-user delivery across enterprise, government, and infrastructure segments.

|

Stage |

Key Participants |

|

Technology & Component Supply |

Camera, sensor, and chipset manufacturers; software and AI-model providers; connectivity and storage vendors |

|

Product & Solution Development |

Security OEMs, surveillance and access-control developers, analytics and platform software firms |

|

System Integration |

System integrators, IT and network integration specialists, security consulting providers |

|

Deployment & Installation |

Installation contractors, commissioning teams, and field-engineering service providers |

|

Managed Services & Monitoring |

Monitoring centers, managed security service providers, maintenance and support teams |

|

End-User Delivery |

Government, transport, commercial, industrial, and residential security operators |

The system integration and managed-services stages are the value chain's most differentiated phases, where interoperability expertise, monitoring reliability, and analytics capability determine competitive advantage and customer retention across long-term service contracts.

Technology Landscape in the Japan Security Industry

AI-Powered Video Analytics

AI video analytics enables automated detection of objects, faces, and behaviours, transforming raw footage into actionable intelligence. It improves accuracy, reduces manual monitoring, and supports real-time alerts, becoming a core differentiator in modern Japanese surveillance deployments.

Cloud-Based Security Management

Cloud platforms centralize video, access, and alarm management with scalable storage and remote administration. They lower on-premises costs, enable multi-site oversight, and support subscription models, accelerating the transition toward flexible, analytics-ready security operations.

Integrated Access Control and IoT Sensors

Integrated access control combined with IoT sensors links entry management, environmental monitoring, and intrusion detection into unified systems. This convergence enhances situational awareness, automates responses, and strengthens protection across commercial, industrial, and critical-infrastructure facilities.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

System |

Video Surveillance Systems |

29.8% |

2025 |

|

Service |

Managed Services |

34.6% |

2025 |

|

End User |

🔒 |

🔒 |

2025 |

|

Region |

Kanto Region |

35.8% |

2025 |

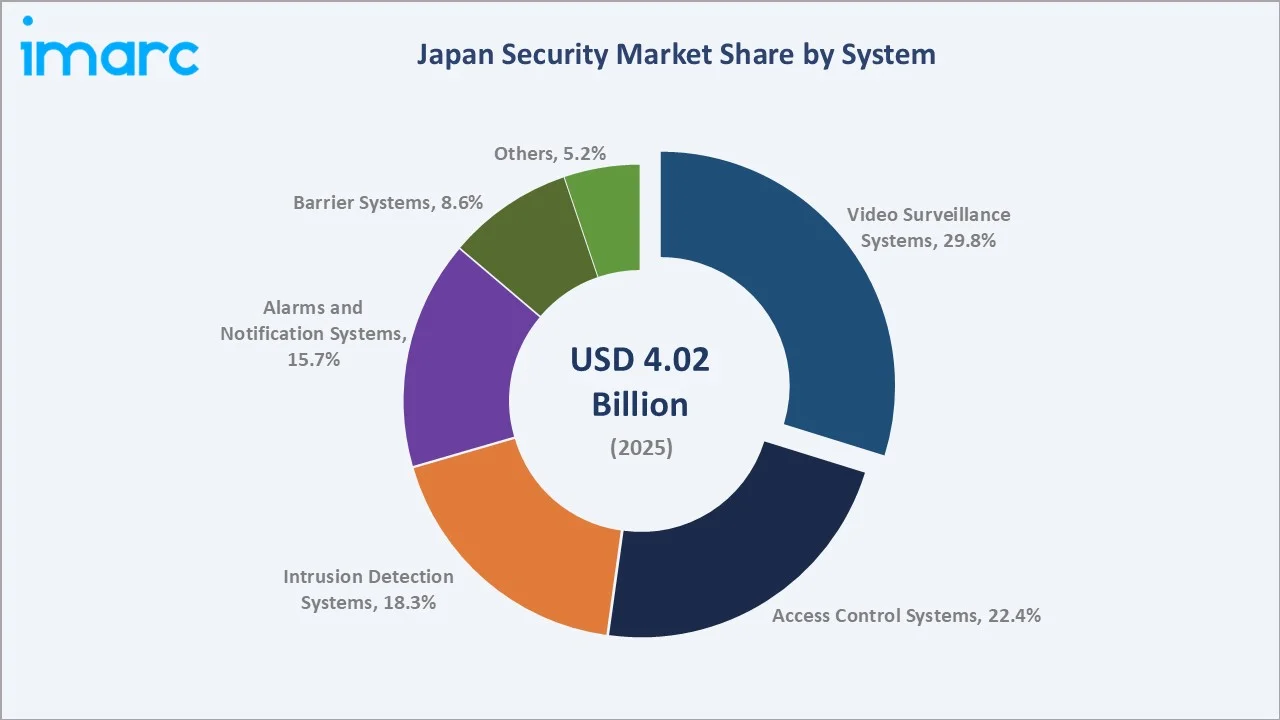

By System

Video Surveillance Systems lead at 29.8% (2025). The segment covers IP cameras, network video recorders, and edge-analytics devices deployed across transport, retail, public spaces, and enterprise facilities for real-time monitoring and incident response.

To access detailed market analysis, Request Sample

Access Control Systems at 22.4% follow, driven by demand for secure, contactless entry management. Intrusion Detection at 18.3% and Alarms and Notification Systems at 15.7% support layered protection, while Barrier Systems and Others complete the mix.

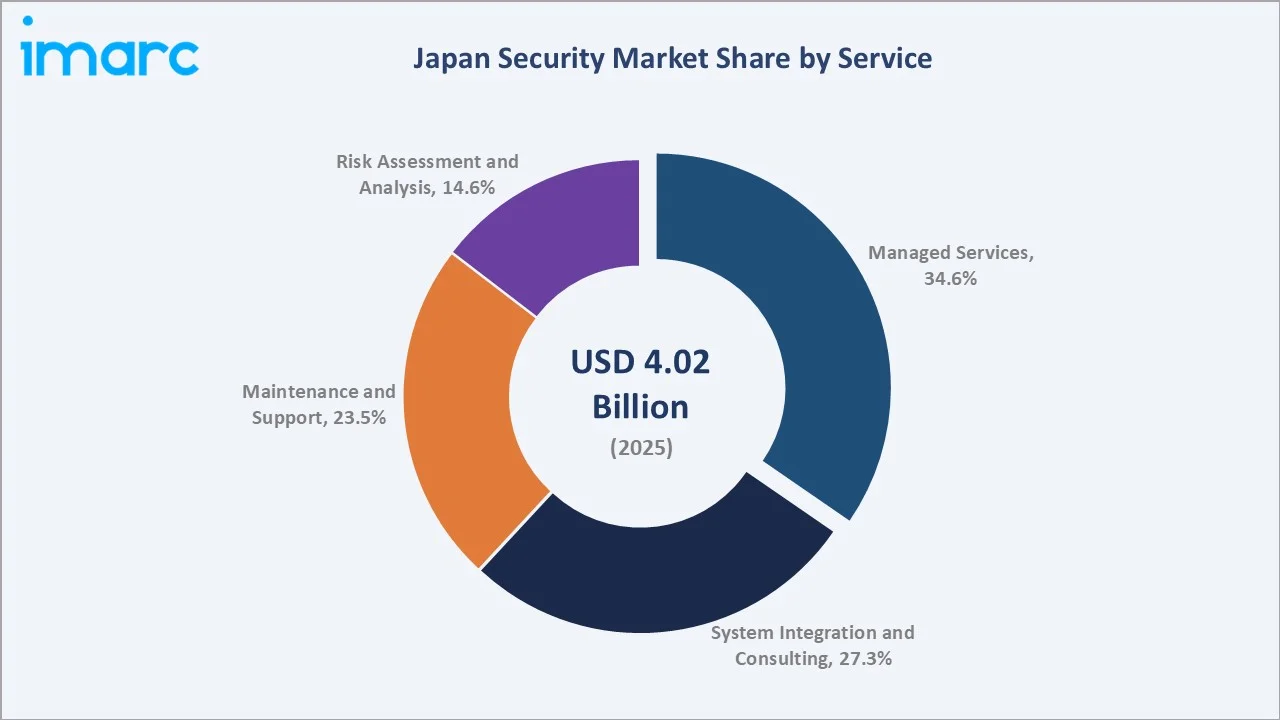

By Service

Managed Services lead at 34.6% (2025), reflecting strong outsourcing of continuous monitoring and response. Providers deliver scalable, subscription-based oversight that reduces staffing pressure and improves reliability for enterprise and public-sector clients.

System Integration and Consulting at 27.3% supports complex deployments, while Maintenance and Support at 23.5% ensures operational continuity. Risk Assessment and Analysis at 14.6% underpins proactive, compliance-aligned security planning across sectors.

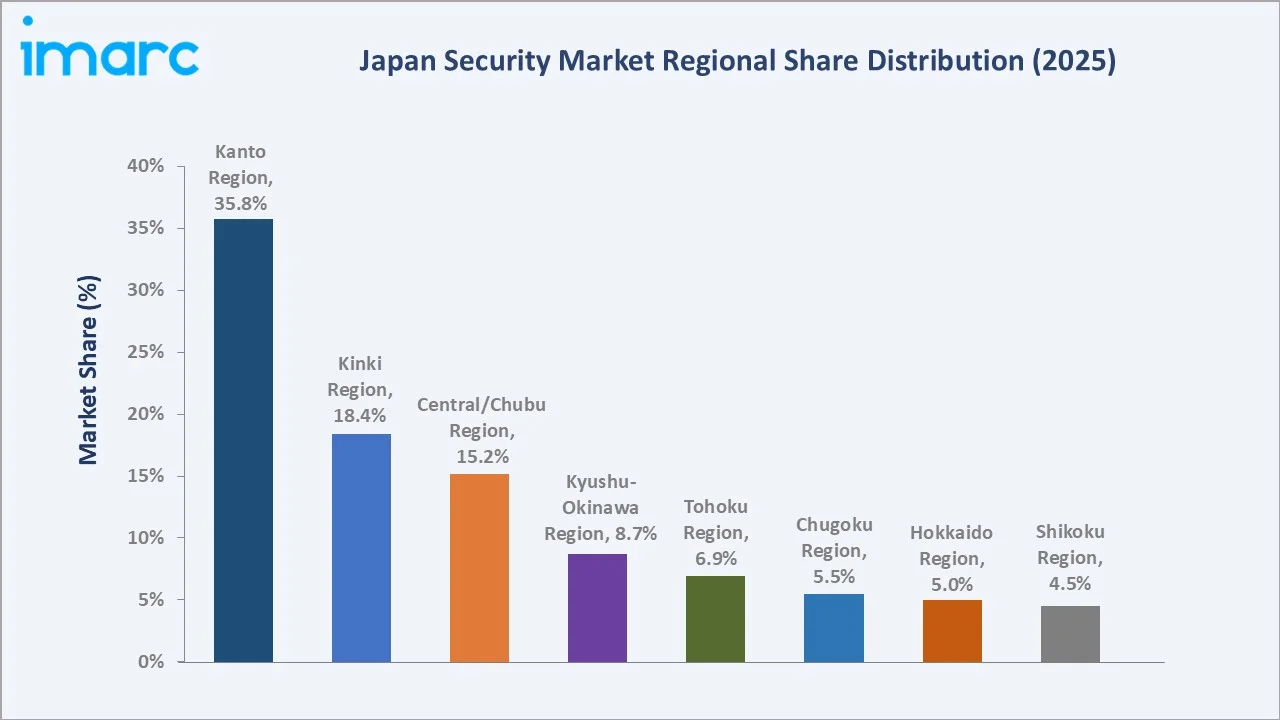

Regional Market Insights

|

Region |

Share (2025) |

Key Market Drivers & Characteristics |

|

Kanto Region |

35.8% |

Driven by concentrated corporate, government, and transport infrastructure around Tokyo requiring high-specification integrated security. |

|

Kinki Region |

18.4% |

Supported by Osaka-Kyoto commercial density, industrial facilities, and expanding smart-city surveillance initiatives. |

|

Central/Chubu Region |

15.2% |

Anchored by Nagoya's manufacturing base and automotive-industry demand for industrial and facility security. |

|

Kyushu-Okinawa Region |

8.7% |

Growing through logistics hubs, tourism infrastructure, and rising public-safety modernization investment. |

|

Tohoku Region |

6.9% |

Driven by disaster-resilience programs and reconstruction-linked infrastructure protection demand. |

|

Chugoku Region |

5.5% |

Supported by industrial ports and steady commercial security upgrades. |

|

Hokkaido Region |

5.0% |

Driven by tourism, agriculture, and remote-monitoring adoption across dispersed sites. |

|

Shikoku Region |

4.5% |

Growing through gradual modernization of commercial and public facility security. |

Kanto's 35.8% market leadership is anchored by Tokyo's dense concentration of enterprises, government facilities, and transit networks. Kinki and Central/Chubu follow through commercial density and industrial demand, forming Japan's core security investment corridor.

Secondary regions including Kyushu-Okinawa, Tohoku, and Hokkaido are advancing through disaster-resilience, logistics, and tourism-driven security modernization, gradually broadening national demand beyond the traditional metropolitan strongholds.

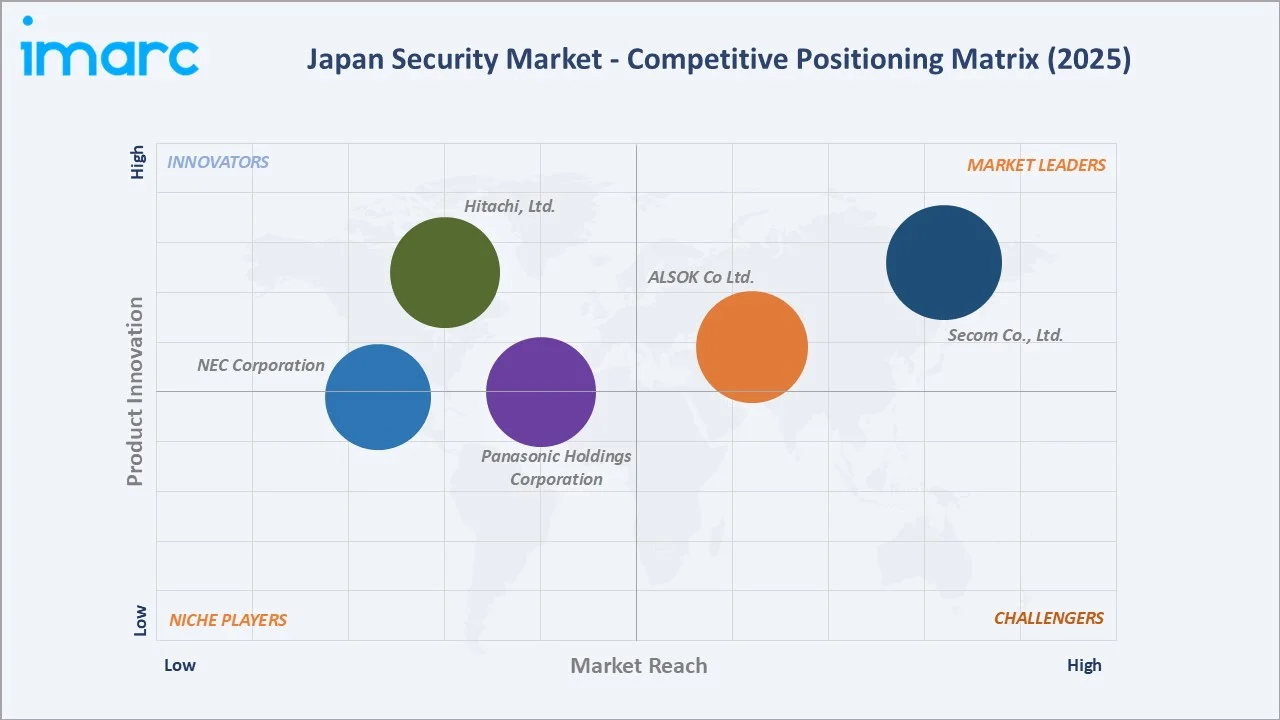

Competitive Landscape

The Japan security market competitive landscape spans integrated security service leaders, electronics and surveillance manufacturers, and IT-driven solution providers competing on technology depth, service reliability, and nationwide operational reach.

|

Company Name |

Key Products |

Market Position |

Core Strength |

|

Secom Co., Ltd. |

Home security |

Market Leader |

Nationwide monitoring network and managed security services |

|

ALSOK Co Ltd. |

Home Alsok Connect, Home Alsok Mimamori Support |

Market Leader |

Extensive guarding and integrated monitoring operations |

|

Panasonic Holdings Corporation |

Surveillance & access hardware |

Established Player |

Broad surveillance and access-control product portfolio |

|

Hitachi, Ltd. |

Digital Security portfolio |

Established Player |

AI, biometrics, and large-scale integration capability |

|

NEC Corporation |

Biometrics & analytics |

Established Player |

Facial recognition and public-safety solutions |

Market leadership is concentrated among integrated service providers Secom and ALSOK, whose nationwide monitoring infrastructure and long-term contracts create durable advantage. Electronics and IT players compete through technology differentiation and public-sector partnerships.

Key Company Profiles

Secom Co., Ltd.

Secom is Japan's leading integrated security provider, delivering electronic security, managed monitoring, and disaster-prevention services through an extensive nationwide response network serving enterprise, government, and residential customers.

- Key Focus: Electronic security systems, centralized monitoring, on-line security, and disaster-prevention services.

- Strategic Focus: Centered on cloud monitoring, AI-driven analytics, and integrated security-plus-cybersecurity solutions.

ALSOK Co Ltd

ALSOK is a major Japanese security company specializing in guarding, electronic security, and integrated monitoring, combining human resources with technology-driven surveillance and response across commercial, public, and event environments nationwide.

- Key Focus: Static and patrol guarding, electronic security, cash logistics, and integrated monitoring services.

- Recent Developments: In October 2025, ALSOK announced that it was selected as the Official Event Supporter (Security Services and Planning) for the World Athletics Championships Tokyo 2025. Under this partnership, the company will provide comprehensive security planning and operational security services to help ensure the safe and secure execution of the international sporting event, leveraging its expertise in integrated security systems, surveillance, and event security management.

- Strategic Focus: Centered on automation, robotics, and remote monitoring for scalable, technology-driven security operations.

Panasonic Holdings Corporation

Panasonic is a leading electronics manufacturer supplying surveillance cameras, access-control hardware, and integrated security solutions, leveraging imaging and sensing expertise to serve enterprise and infrastructure security applications across Japan.

- Key Focus: Network surveillance cameras, video management systems, and access-control hardware.

- Recent Developments: In April 2025, Panasonic Connect announced that it will deploy biometric authentication systems, AI sensing technologies, and integrated security solutions at Expo 2025 Osaka, Kansai, Japan. The technologies are designed to enhance secure access control, visitor management, operational efficiency, and safety across the Expo venue, construction sites, and surrounding infrastructure.

- Strategic Focus: Focused on AI imaging, edge analytics, and integrated platforms for smart-city and enterprise security.

Market Concentration Analysis

The Japan security market is moderately concentrated. Integrated service leaders Secom and ALSOK hold substantial share through nationwide monitoring networks and recurring contracts, while electronics and IT providers compete across hardware, analytics, and integration tiers. Concentration is highest in managed monitoring, where scale and response infrastructure create high barriers, while the technology and component tier remains more fragmented as competition intensifies through AI analytics and cloud-platform differentiation.

Investment & Growth Opportunities

Highest Growth Segments

Cloud-based deployment, AI video analytics, and managed detection services represent the highest-growth vectors through 2034, driven by subscription economics, scalability, and demand for continuous, intelligence-led monitoring across enterprise and public-sector clients.

Emerging Investment Opportunities

Smart-city surveillance, critical-infrastructure protection, and converged cyber-physical platforms offer strong near-term opportunities. Providers establishing early public-sector and infrastructure partnerships are positioned to capture above-market growth as government programs scale.

Investment Themes

- Recurring Managed Services: Cloud-native managed security platforms delivering subscription revenue create scalable, above-hardware-margin business models as organizations shift from ownership toward continuous, service-based security monitoring.

- AI and Biometrics Platforms: AI analytics and biometrics investment enables differentiated, high-value solutions addressing public-safety, transport, and enterprise demand for proactive, automated threat detection and response.

Future Market Outlook (2026-2034)

The Japan security market is projected to grow from USD 4.02 Billion in 2025 to USD 8.22 Billion by 2034, delivering an 8.02% CAGR. The USD 5.91 Billion 2030 anchor marks the mainstreaming of AI-driven, cloud-native security operations across enterprise and public-sector environments.

Three structural forces define growth: sustained public-safety and smart-city investment, accelerating adoption of AI analytics and converged cyber-physical platforms, and demographic-driven demand for managed, automated monitoring that offsets Japan's shrinking security workforce through 2034.

Research Methodology

Primary Research

Primary research comprised structured interviews with industry stakeholders including security service executives, systems integrators, technology vendors, and end-user security managers across Japanese enterprise, government, and infrastructure segments.

Secondary Research

Secondary research encompassed company reports, industry associations, government safety and infrastructure data, technology publications, and trade sources, with over 60 secondary sources reviewed to validate market sizing and segmentation.

Forecasting Models

Market forecasts were developed using a segment bottom-up model across system, service, and deployment components, triangulated with demand-side indicators and validated against historical performance and expert input.

Japan Security Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Systems Covered | Access Control Systems, Alarms and Notification Systems, Intrusion Detection Systems, Video Surveillance Systems, Barrier Systems, Others |

| Services Covered | System Integration and Consulting, Risk Assessment and Analysis, Managed Services, Maintenance and Support |

| End Users Covered | Government, Military and Defense, Transportation, Commercial, Industrial, Others |

| Regions Covered | Kanto Region, Kinki Region, Central/ Chubu Region, Kyushu-Okinawa Region, Tohoku Region, Chugoku Region, Hokkaido Region, Shikoku Region |

| Companies Covered | Secom Co., Ltd., ALSOK Co Ltd., Panasonic Holdings Corporation, Hitachi, Ltd., NEC Corporation, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the Japan security market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the Japan security market.

- Porter's Five Forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the Japan security industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Japan Security Market Report

The Japan security market reached USD 4.02 Billion in 2025, driven by rising public-safety investment, smart-city programs, and growing adoption of AI-enabled surveillance and cloud-based managed security services.

The market grows at 8.02% CAGR during 2026-2034, reaching USD 8.22 Billion by 2034, led by cloud deployment, AI analytics, and expanding managed-service adoption.

Video Surveillance Systems lead at 29.8%, driven by dense urban camera deployment, transport-network coverage, and the shift toward IP cameras with edge analytics for real-time detection.

Managed Services lead at 34.6%, as enterprises and public agencies outsource continuous monitoring to offset workforce constraints and improve reliability through scalable, subscription-based operations.

The Kanto Region leads at 35.8%, anchored by Tokyo's concentration of corporate headquarters, government facilities, and dense transport infrastructure requiring integrated, high-specification security systems.

Leading companies include Secom Co., Ltd., Alsok Co Ltd, Panasonic Holdings Corporation, Hitachi, Ltd, and NEC Corporation, among other electronics and IT-driven security solution providers.

The market is projected to reach approximately USD 5.91 Billion by 2030, with cloud-native surveillance, AI analytics, and converged cyber-physical platforms achieving mainstream commercial adoption.

The Government sector leads end-user demand, driven by national infrastructure protection, public-service facilities, and smart-city initiatives requiring integrated, high-specification security systems.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)