Kitchen Appliances Market Size, Share, Trends and Forecast by Product Type, Structure, Fuel Type, Application, Distribution Channel, and Region, 2026-2034

Kitchen Appliances Market Size and Share:

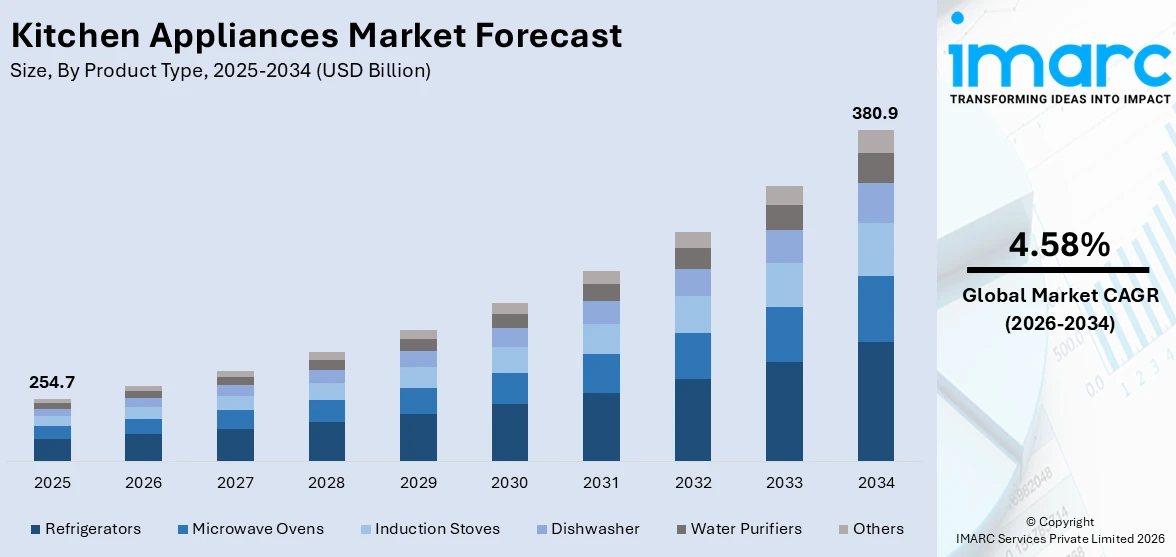

The global kitchen appliances market size was valued at USD 254.7 Billion in 2025. Looking forward, IMARC Group estimates the market to reach USD 380.9 Billion by 2034, exhibiting a CAGR of 4.58% from 2026-2034. North America currently dominates the market, holding a market share of 42.2% in 2025. The region benefits from high consumer spending on home improvement, widespread adoption of technologically advanced kitchen solutions, robust retail and e-commerce distribution networks, and a strong preference for energy-efficient and smart appliances that collectively drive the kitchen appliances market share.

The market for kitchen appliances is expanding at a steady pace owing to a number of factors. The rising rate of urbanization and the growing middle class in developed as well as developing nations are increasing the demand for modern kitchen solutions. For example, India’s TTK Prestige announced plans in 2025 to expand its physical store count by up to 30% over the next four years to capture greater household demand, underscoring how major appliance makers are scaling operations to meet consumption growth. The concept of smart homes has contributed largely to the growing demand for smart kitchen appliances. Changing dietary habits and the growing preference for home-cooked meals, influenced by health consciousness and evolving food cultures, are increasing household investments in high-performance cooking and food preservation equipment. Furthermore, ongoing kitchen renovation trends, particularly in mature housing markets, continue to support replacement and upgrade cycles for kitchen appliances market growth.

The United States has become a prominent region in the global kitchen appliances market due to a number of factors. It currently holds a share of 88.2%. The established housing market in the United States, as well as the regular home renovation activities, have been contributing to the steady demand for both fixed and standalone kitchen appliances. In August 2025, GE Appliances announced a historic $3 billion investment to expand and modernize its U.S. manufacturing operations, shifting production of refrigerators, gas ranges, and other appliances to facilities in Kentucky, Alabama, Georgia, Tennessee, and South Carolina to better serve American consumers and support local jobs. The consumer preference trend has been shifting towards smart kitchen appliances that are Wi-Fi enabled. Government-backed energy efficiency programs and rebate incentives encourage households to upgrade to newer, more sustainable models, accelerating replacement cycles. The increasing trend of dual-income families and busy lifestyles in urban areas are driving the demand for time-saving and multi-functional kitchen appliances like combination ovens, smart refrigerators, and high-performance dishwashers. In addition, the growing e-commerce market in the country is offering consumers easy access to products, competitive pricing, and convenient purchasing options, thereby supporting the kitchen appliances market outlook.

To get more information on this market Request Sample

Kitchen Appliances Market Trends:

Growing Adoption of Smart Kitchen Technology

The integration of artificial intelligence, Internet of Things connectivity, and advanced sensor technologies into kitchen appliances is fundamentally reshaping the consumer experience. At CES 2026, GE Appliances unveiled the GE Profile 27.9 cu ft Smart 4‑Door French‑Door Refrigerator with Kitchen Assistant, featuring a barcode scanner, AI meal planning, and remote inventory tracking. Contemporary refrigerators come equipped with in-built cameras, touch screens, and smart food management systems that assist consumers in inventory management, recipe suggestions, and reducing food waste. Smart ovens with AI-driven cooking options are capable of identifying the dish being cooked and adjusting the temperature and cooking time accordingly. Voice-control functionality through digital assistants is becoming a norm in the industry, allowing consumers to operate appliances without using their hands in a busy kitchen setting. Companies are also providing over-the-air software updates, adding new features to existing appliances.

Rising Demand for Energy-Efficient Appliances

Increasing environmental consciousness and rising energy costs are propelling consumer demand for kitchen appliances that prioritize energy efficiency and sustainability. In January 2026, India expanded mandatory energy‑efficiency star labeling to more appliances, including refrigerators and LPG stoves, under the Bureau of Energy Efficiency’s updated rules to promote low‑energy products. Regulatory frameworks in major markets, including updated energy labeling standards and ecodesign directives, are accelerating the replacement of older, less efficient models with newer alternatives that meet stringent performance benchmarks. Induction cookers, which have a much better energy transfer rate than conventional gas and electric cookers, are increasingly popular among environmentally conscious consumers. Energy-efficient refrigerators and dishwashers with advanced insulation, variable-speed compressors, and adaptive cycle control systems are cutting residential energy consumption without impairing kitchen appliances market forecast performance.

Increasing Preference for Multi-Functional Designs

The growing popularity of compact, space-efficient, and multi-purpose kitchen appliances reflects shifting consumer lifestyles and evolving living arrangements. As urban populations expand and average dwelling sizes shrink in major metropolitan areas, consumers are increasingly seeking versatile products that combine multiple cooking functions within a single unit. For example, in 2026, the launch of compact, multifunctional devices like the Ninja PossibleCooker Plus, which combines up to 12 cooking tools into one appliance, has highlighted how manufacturers are catering directly to consumers seeking space‑saving, all‑in‑one solutions. Combination microwave-convection ovens, air fryer-pressure cooker hybrids, and modular countertop appliances are experiencing robust demand, particularly among younger demographics and single-person households. This kitchen appliances market trends shift is further supported by the influence of social media platforms and culinary content creators who showcase innovative kitchen tools and cooking techniques, inspiring broader consumer experimentation.

Kitchen Appliances Industry Segmentation:

IMARC Group provides an analysis of the key trends in each segment of the global kitchen appliances market, along with forecast at the global, and regional, levels from 2026-2034. The market has been categorized based on product type, structure, fuel type, application, and distribution channel.

Analysis by Product Type:

- Refrigerators

- Microwave Ovens

- Induction Stoves

- Dishwasher

- Water Purifiers

- Others

Refrigerators have a market share of 35.0%. Refrigerators are the primary group of kitchen appliances, found in both residences and industry for the storage of food items. The segment is anticipated to retain its dominance over the cooling oil market over the forecast period owing to the universal need for temperature-controlled food storage, regular technological advancements in cooling systems, and increasing adoption of smart features such as internal camera, auto-inventory smart coolers and energy-optimizing compressor technologies, among others. Consumers are preferring larger models like French door and side-by-side models for better organization and convenience. The growing availability of built-in and counter-depth refrigerator designs is also fuelling demand for the premium and kitchen renovation segments. In addition, introduction of new labeling and rebates is pushing households to replace their old units with energy-efficient refrigeration models.

Analysis by Structure:

- Built-In

- Free Stand

Free stand leads the market with a share of 70.0%. Freestanding kitchen appliances maintain their leading position owing to their versatility, ease of installation, and broad affordability across diverse consumer segments. Unlike built-in alternatives that require custom cabinetry and professional installation, freestanding units offer straightforward placement flexibility, making them particularly suitable for rental properties, smaller kitchens, and households that value reconfigurable layouts. The segment benefits from a wide product range spanning refrigerators, stoves, dishwashers, and microwave ovens, available in multiple sizes, styles, and price points. Consumer preference is further supported by energy-efficient models, modern aesthetics, and smart technology integration, enhancing convenience, functionality, and long-term cost savings.

Analysis by Fuel Type:

- Cooking Gas

- Electricity

- Others

Cooking gas dominates the market, with a share of 48%. Gas-powered kitchen appliances continue to command a significant market position, driven by widespread consumer preference for the precise heat control and rapid temperature response that gas cooking provides. Professional and home cooks alike favor gas ranges and cooktops for their ability to deliver immediate flame adjustments, which is essential for diverse cooking techniques including searing, simmering, and flambeing. The extensive existing infrastructure for natural gas distribution in major markets, particularly across North America, Europe, and parts of Asia-Pacific, ensures continued accessibility and adoption of gas-fueled appliances. Additionally, gas appliances typically operate at lower running costs compared to electric alternatives in many regions, reinforcing their cost-effectiveness for daily household use.

Analysis by Application:

Access the comprehensive market breakdown Request Sample

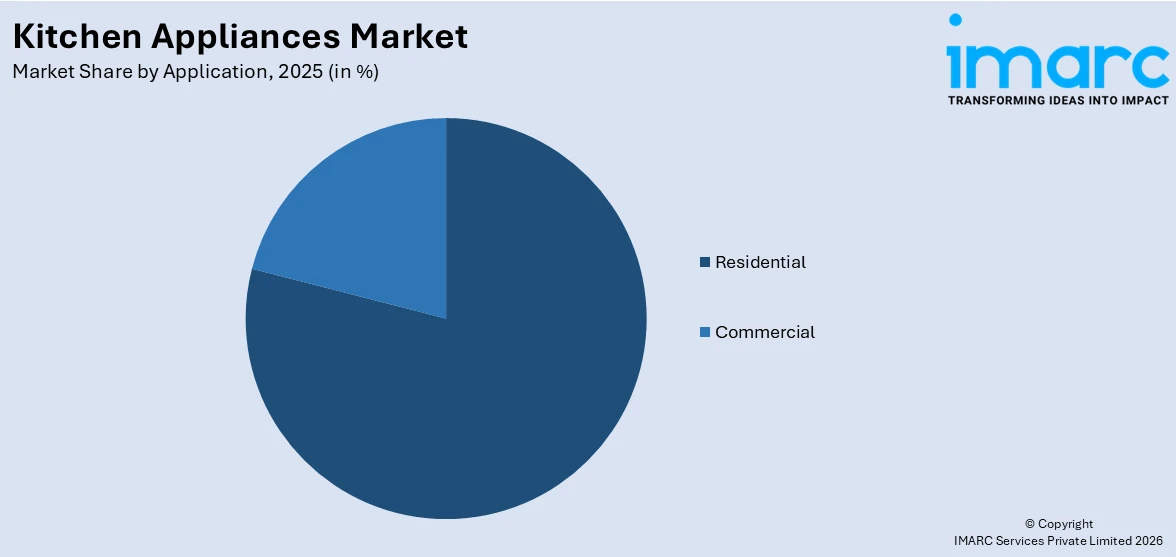

- Residential

- Commercial

Residential represents the leading segment, with a market share of 78.9%. The residential application segment maintains its dominant position, underpinned by the fundamental role of kitchen appliances in everyday household operations. Rising homeownership rates, particularly among millennial and Generation Z demographics, combined with the growing cultural emphasis on home cooking and kitchen-centric lifestyles, are sustaining robust demand for residential kitchen equipment. The home renovation and remodeling industry continues to prioritize kitchen upgrades, with consumers investing in premium appliance suites that offer enhanced functionality, improved aesthetics, and smart connectivity. The increasing influence of online platforms, home improvement content, and cooking shows further inspires household appliance purchases. Additionally, the growing number of dual-income families and single-person households drives demand for convenient, time-saving, and compact appliances tailored to modern residential living requirements.

Analysis by Distribution Channel:

- Supermarkets and Hypermarkets

- Specialty Stores

- Online Stores

- Departmental Stores

- Others

Specialty stores holds 34.2% of the market share. Specialty stores represent the leading distribution channel for kitchen appliances, offering consumers a focused shopping experience characterized by extensive product displays, expert guidance, and hands-on product demonstrations. These dedicated retail environments enable consumers to compare features, assess build quality, and receive personalized recommendations from trained staff, which is particularly valuable for high-involvement purchases such as major kitchen appliances. Specialty retailers typically maintain strong relationships with leading appliance manufacturers, ensuring access to the latest product launches, exclusive models, and competitive pricing. The in-store experience also supports after-sales services including installation coordination, warranty management, and maintenance support. While online retail continues to grow, specialty stores retain their competitive advantage through immersive showroom experiences and consultative selling approaches that help consumers make informed purchasing decisions.

Regional Analysis:

To get more information on the regional analysis of this market Request Sample

- Asia Pacific

- North America

- Europe

- Middle East and Africa

- Latin America

North America, accounting for 42.2% of the share, enjoys the leading position in the market. The region’s dominance is driven by high per capita consumer spending on household goods, a well-developed housing market that supports both new construction and renovation-driven appliance demand, and widespread adoption of technologically advanced kitchen solutions. The strong retail infrastructure, encompassing specialty appliance stores, home improvement chains, and a rapidly expanding e-commerce ecosystem, ensures broad product accessibility across urban and suburban markets. Consumer preferences in the region increasingly favor premium, energy-efficient, and connected kitchen appliances, supported by favorable financing options and government-backed energy incentive programs. The region also benefits from the presence of major global appliance manufacturers and their extensive distribution, service, and warranty networks that reinforce consumer confidence and support sustained market growth.

Key Regional Takeaways:

United States Kitchen Appliances Market Analysis

The United States represents a significant contributor to the North American kitchen appliances market, driven by a combination of strong consumer purchasing power, established home improvement culture, and rapid technological adoption. The country’s housing market, characterized by both new residential construction and a robust renovation sector, generates consistent demand for kitchen appliance upgrades and replacements. Consumer preferences are increasingly oriented toward smart, connected appliances that integrate with broader home automation ecosystems, including voice-controlled assistants and smartphone applications for remote monitoring and operation. The government’s continued support for energy-efficient appliances through programs and rebate structures encourages households to transition from older models to advanced, sustainable alternatives. The expanding online retail channel, complemented by traditional specialty stores and home improvement retailers, provides consumers with diverse purchasing options, competitive pricing, and convenient delivery services. Rising millennial homeownership and the growing influence of culinary media content further strengthen household investment in premium, aesthetically refined, and technologically sophisticated kitchen appliance solutions across the country.

Europe Kitchen Appliances Market Analysis

The European kitchen appliances market is characterized by strong consumer demand for premium, energy-efficient, and design-oriented products. Stringent regulatory frameworks, including updated energy labeling standards and ecodesign directives, are accelerating the replacement of older appliances with high-efficiency models across the continent. At IFA 2025 in Berlin, Samsung unveiled premium built‑in kitchen appliances for Europe, including an extractor induction hob and Bespoke AI Dishwasher, highlighting the focus on energy efficiency, modern design, and regional preferences. Germany, the United Kingdom, France, Italy, and Spain represent the largest contributors to the region’s appliance revenues. Urban renovation trends and the growing popularity of modular and integrated kitchen designs are supporting demand for built-in appliance solutions. Consumer interest in sustainable and environmentally responsible products continues to shape purchasing decisions, with induction cooktops, low-energy dishwashers, and advanced refrigeration units gaining significant market traction. The region’s well-established retail infrastructure, complemented by expanding e-commerce platforms, ensures broad product accessibility and competitive pricing across diverse consumer segments and income levels.

Asia Pacific Kitchen Appliances Market Analysis

The Asia-Pacific kitchen appliances market is experiencing rapid expansion, driven by accelerating urbanization, rising disposable incomes, and evolving consumer lifestyles across the region. The growing middle class in major economies is fueling demand for modern kitchen solutions that offer convenience, efficiency, and enhanced food preparation capabilities. Increasing household formation rates, driven by demographic shifts and urban migration patterns, are generating sustained demand for essential kitchen appliances. Government initiatives promoting energy efficiency and domestic manufacturing are further supporting market development. The region’s expanding e-commerce infrastructure is broadening product accessibility, particularly in semi-urban and rural areas, while the influence of digital media and cooking platforms continues to shape consumer preferences toward innovative kitchen technologies.

Latin America Kitchen Appliances Market Analysis

The Latin American kitchen appliances market is supported by rising consumer spending, expanding urbanization, and growing household formation across the region. Economic development in key markets is driving demand for modern kitchen solutions that offer improved functionality and convenience. The increasing penetration of organized retail and e-commerce platforms is broadening consumer access to a wider range of kitchen appliance products. Government housing programs and infrastructure development initiatives are contributing to market expansion, while the growing middle class is gradually shifting toward premium and energy-efficient appliance options that align with evolving lifestyle expectations.

Middle East and Africa Kitchen Appliances Market Analysis

The Middle East and Africa kitchen appliances market is witnessing steady growth, supported by rising disposable incomes, rapid urbanization, and increasing demand for modern household solutions. Infrastructure development and expanding residential construction across key markets are generating demand for contemporary kitchen equipment. The growing preference for energy-efficient and technologically advanced appliances is gaining momentum, driven by increasing consumer awareness and evolving regulatory frameworks. The expanding retail landscape, including the growth of specialty stores and online shopping platforms, is enhancing product accessibility and consumer choice across the region, supporting the overall development of the kitchen appliances market.

Competitive Landscape:

The global kitchen appliances market is characterized by intense competition among established multinational corporations that leverage extensive research and development capabilities, broad product portfolios, and expansive distribution networks. Leading players are increasingly investing in artificial intelligence integration, smart connectivity features, and energy-efficient technologies to differentiate their product offerings and capture premium market segments. Strategic initiatives including mergers, acquisitions, and partnerships are enabling companies to expand their geographic presence and strengthen their technological capabilities. Manufacturers are also focusing on direct-to-consumer models, subscription-based maintenance services, and enhanced after-sales support to improve customer lifetime value. The competitive landscape is further shaped by evolving regulatory requirements for energy efficiency and sustainability, compelling all market participants to continuously innovate and upgrade their product lines.

The report provides a comprehensive analysis of the competitive landscape in the kitchen appliances market with detailed profiles of all major companies, including:

- Whirlpool Corporation

- AB Electrolux

- Samsung Electronics Co. Ltd.

- LG Electronics

- Winia Daewoo Electronics

- Panasonic Corporation

- Haier Group Corporation

- BSH Hausgeräte GmbH

- Miele & Cie. KG

- Sub-Zero Group, Inc.

Latest News and Developments:

-

In February 2026, Midea unveiled its largest lineup of smart home appliances—including advanced kitchen tech, at the Kitchen & Bath Industry Show (KBIS) 2026 in Orlando, signaling its evolution into a full‑home solutions brand spanning kitchen, laundry, and climate comfort products.

- In February, 2026, JENNAIR Unveils Bold Kitchen Designs & Induction Focus at KBIS: JennAir showcased innovative kitchen concepts, including the “No Kitchen Kitchen,” at KBIS 2026, emphasizing design freedom and expanding its induction cooking solutions. The launch highlights the brand’s commitment to blending cutting‑edge technology with creative, high‑end kitchen design.

Kitchen Appliances Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Predictive Market Assessment:

|

| Product Types Covered | Refrigerators, Microwave Ovens, Induction Stoves, Dishwasher, Water Purifiers, Others |

| Structures Covered | Built-In, Free Stand |

| Fuel Types Covered | Cooking Gas, Electricity, Others |

| Applications Covered | Residential, Commercial |

| Distribution Channels Covered | Supermarkets And Hypermarkets, Specialty Stores, Online Stores, Departmental Stores, Others |

| Regions Covered | Asia Pacific, North America, Europe, Middle East and Africa, Latin America |

| Companies Covered | Whirlpool Corporation, AB Electrolux, Samsung Electronics Co. Ltd., LG Electronics, Winia Daewoo Electronics, Panasonic Corporation, Haier Group Corporation, BSH Hausgeräte GmbH, Miele & Cie. KG, Sub-Zero Group, Inc., etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the kitchen appliances market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the global kitchen appliances market.

- The study maps the leading, as well as the fastest-growing, regional markets.

- Porter's Five Forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the kitchen appliances industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Kitchen Appliances Market Report

The kitchen appliances market was valued at USD 254.7 Billion in 2025.

The kitchen appliances market is projected to exhibit a CAGR of 4.58% during 2026-2034, reaching a value of USD 380.9 Billion by 2034.

The kitchen appliances market is primarily driven by rising urbanization, increasing disposable incomes, growing adoption of smart and energy-efficient appliances, expanding home renovation activities, changing dietary preferences favoring home-cooked meals, and the proliferation of connected home technologies across both developed and emerging economies.

North America currently dominates the kitchen appliances market, accounting for a share of 42.2%. The region benefits from high consumer spending, advanced retail infrastructure, widespread smart technology adoption, and supportive government energy efficiency programs.

Some of the major players in the kitchen appliances market include Whirlpool Corporation, AB Electrolux, Samsung Electronics Co. Ltd., LG Electronics, Winia Daewoo Electronics, Panasonic Corporation, Haier Group Corporation, BSH Hausgeräte GmbH, Miele & Cie. KG, Sub-Zero Group, Inc., etc.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)