Latin America Automotive Electric Actuators Market Size, Share, Trends and Forecast by Product, Vehicle Type, and Country, 2026-2034

Latin America Automotive Electric Actuators Market Size, Share, Trends & Forecast (2026-2034)

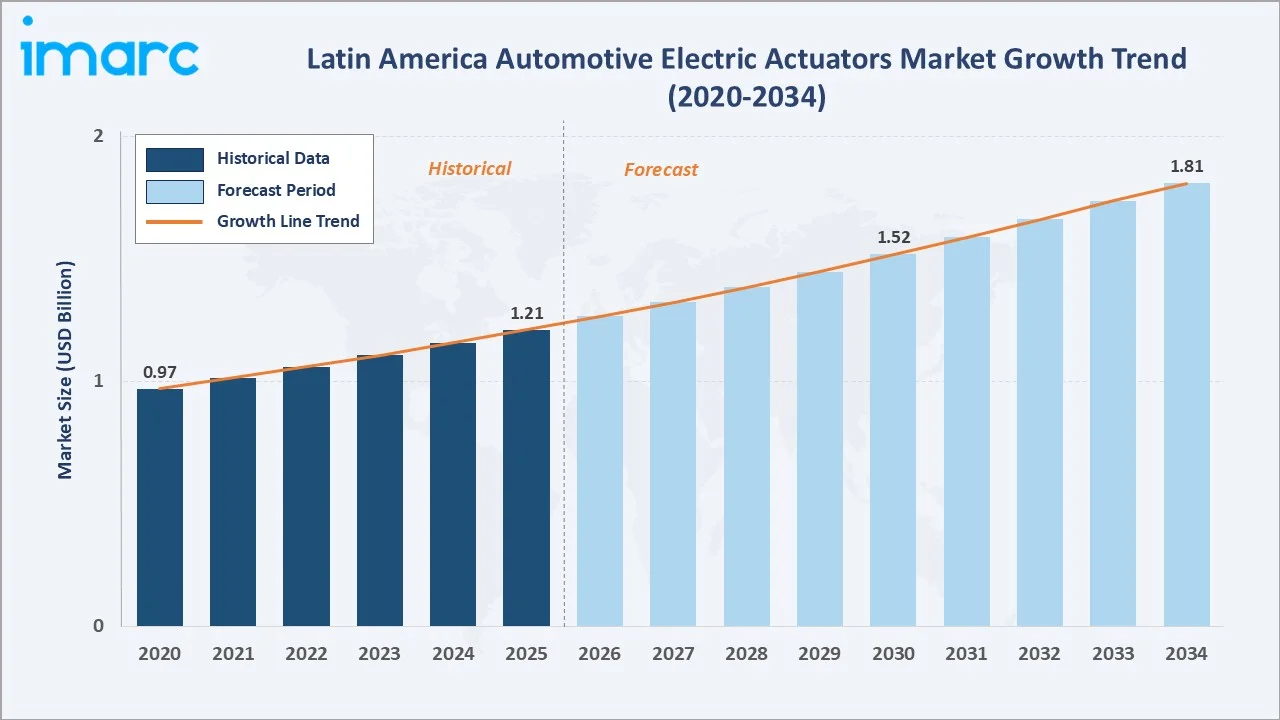

The Latin America automotive electric actuators market reached USD 1.21 Billion in 2025 and is projected to reach USD 1.81 Billion by 2034, growing at a CAGR of 4.56% during 2026-2034. The market is driven by rising vehicle electrification, stricter emission regulations, growing ADAS adoption, and automaker investments in advanced powertrain technologies across the region.

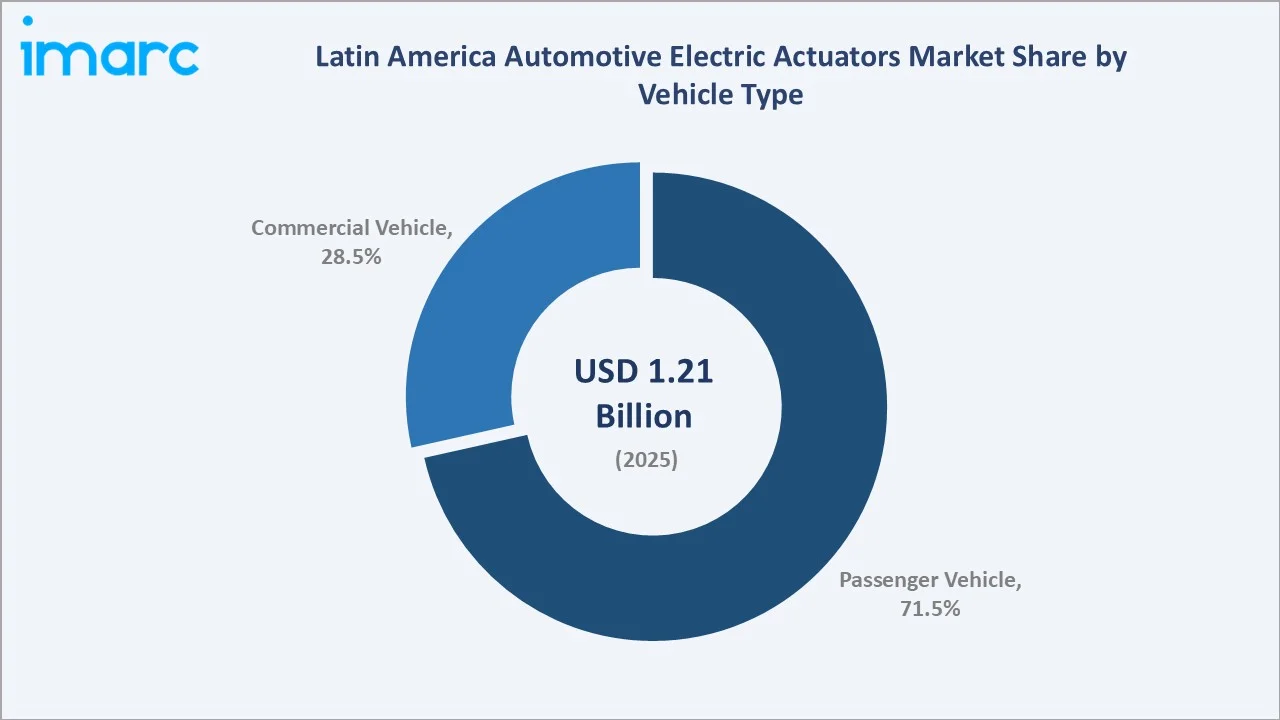

Brazil's EV sales surged 90% in 2024 to 177,360 units, accelerating actuator demand across throttle, brake, seat, and closure subsystems. Throttle Actuator dominates at 27.4%, Passenger Vehicles lead at 71.5%, and Brazil commands 38.9% of regional share in 2025.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 1.21 Billion |

|

Forecast Market Size (2034) |

USD 1.81 Billion |

|

CAGR (2026-2034) |

4.56% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Dominant Product |

Throttle Actuator (27.4%, 2025) |

|

Dominant Vehicle Type |

Passenger Vehicle (71.5%, 2025) |

|

Leading Country |

Brazil (38.9%, 2025) |

The market expanded from USD 0.97 Billion in 2020 to USD 1.21 Billion in 2025, anchored at approximately USD 1.52 Billion in 2030, and forecast to reach USD 1.81 Billion by 2034. Regulatory compliance requirements and OEM electrification transitions sustained steady growth through the historical period.

To get more information on this market, Request Sample

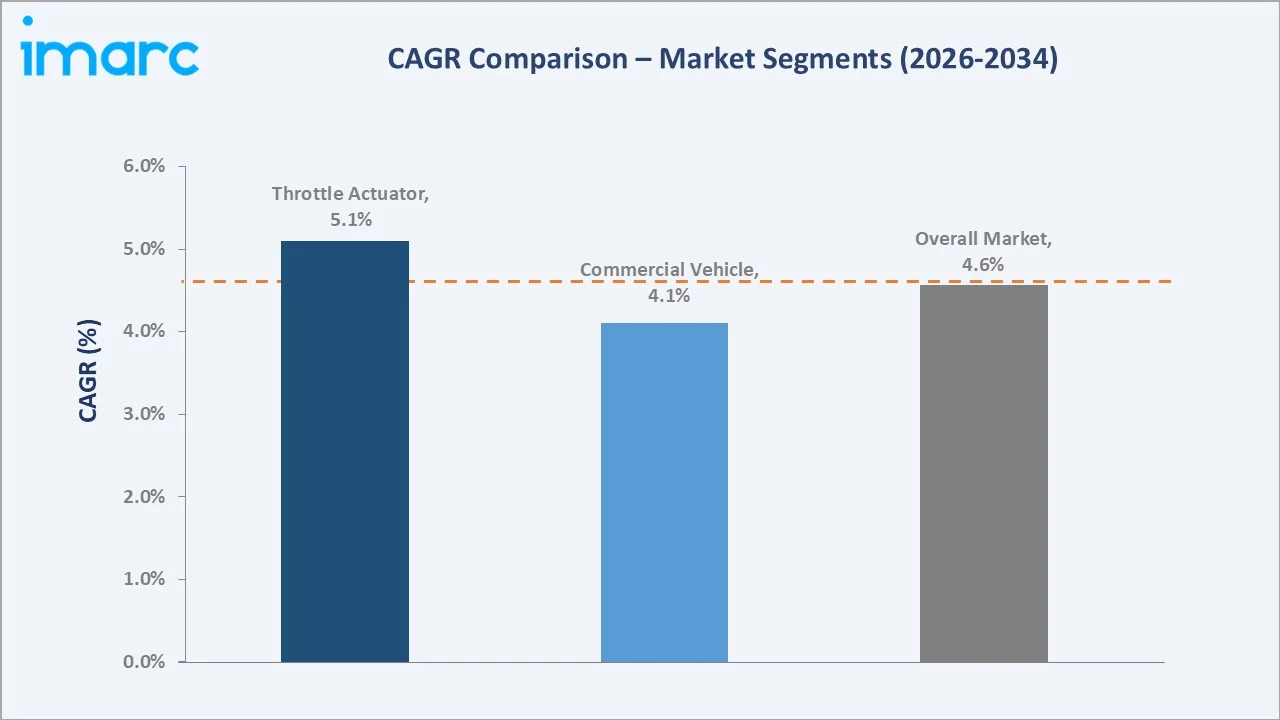

Throttle Actuator grows at ~5.1% CAGR as emission-compliant engine management upgrades accelerate adoption across ICE and hybrid platforms. Passenger Vehicle at ~4.9% CAGR reflects OEM electrification investment. The overall market CAGR of 4.56% during 2026–2034 reflects sustained structural growth across all segments.

Executive Summary

The Latin America automotive electric actuators market reached USD 1.21 Billion in 2025, representing a high-growth segment within the region's expanding automotive electronics ecosystem. Electric actuators replace conventional hydraulic and pneumatic systems, offering superior precision, energy efficiency, and integration with digital vehicle control architectures for ADAS and emission-compliant powertrains.

The market is projected to reach USD 1.81 Billion by 2034. Throttle Actuator leads at 27.4%, Passenger Vehicle at 71.5%, and Brazil at 38.9%.

Key Market Insights

|

Insight |

Data |

|

Dominant Product |

Throttle Actuator – 27.4% share (2025) |

|

Dominant Vehicle Type |

Passenger Vehicle – 71.5% market share (2025) |

|

Leading Country |

Brazil – 38.9% market share (2025) |

|

Market Opportunity |

EV fleet growth; ADAS integration; smart closure systems; fleet electrification programs |

Key Analytical Observations Supporting The Above Data:

- Throttle Actuator at 27.4%: Dominates as precision throttle control is mandatory for ADAS-equipped and emission-compliant powertrains. High integration across ICE, hybrid, and electric platforms sustains leading share.

- Passenger Vehicle at 71.5%: Leads through high-volume light vehicle production in Brazil and Mexico, driven by OEM standardization of electronic safety, comfort, and closure actuator systems in modern passenger cars.

- Brazil at 38.9%: Commands regional leadership via its large-scale automotive manufacturing ecosystem and compliance-driven actuator adoption under PROCONVE emission regulations.

Latin America Automotive Electric Actuators Market Overview

The Latin America automotive electric actuators market encompasses the design, manufacture, and supply of electrically operated actuator devices used in throttle control, braking, seat adjustment, and closure systems across all vehicle categories. The ecosystem integrates Tier-1 actuator manufacturers, OEM vehicle integrators, semiconductor suppliers, and regulatory bodies enforcing emission and safety standards.

Macroeconomic factors include rising fuel prices, government electrification mandates, urbanization, expanding middle-class vehicle ownership, and investments in automotive production capacity. Brazil and Mexico serve as the primary manufacturing and demand hubs, contributing over 59% of regional market revenue in 2025.

Market Dynamics

To evaluate market opportunities, Request Sample

Market Drivers

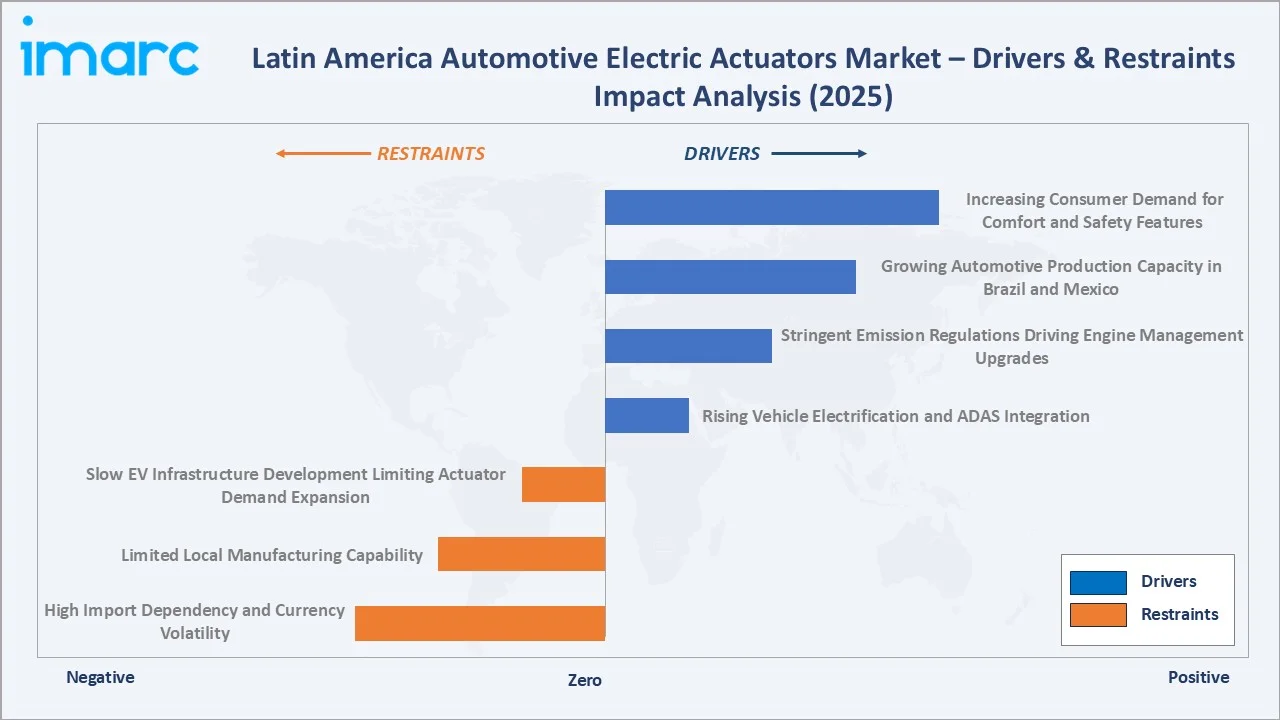

- Rising Vehicle Electrification and ADAS Integration: Growing EV and hybrid vehicle adoption is accelerating demand for electric actuators as EV architectures replace hydraulic systems. Brazil's EV sales surged 90% in 2024 to 177,360 units, creating significant actuator procurement growth. Every EV subsystem, braking, throttle, and closure, requires dedicated electric actuation.

- Stringent Emission Regulations Driving Engine Management Upgrades: Brazil's PROCONVE Phase L7 and Mexico's NOM-044 emission standards compel OEMs to integrate precision throttle and EGR actuators to achieve regulatory compliance. Mandates for fuel efficiency and CO₂ reduction are directly expanding the market for high-precision electric actuators across ICE, hybrid, and EV powertrains.

- Growing Automotive Production Capacity in Brazil and Mexico: Mexico's export-oriented manufacturing under USMCA creates demand for advanced actuator specifications. New OEM assembly plant investments are increasing actuator procurement volumes across the region.

- Increasing Consumer Demand for Comfort and Safety Features: Rising consumer preference for power seat adjustment, automated closure systems, and electronic parking brake is boosting actuator adoption. OEMs are standardizing these features in mid-range vehicle segments across Brazil, Mexico, and Argentina, expanding per-vehicle actuator content and creating sustained demand growth.

Market Restraints

- High Import Dependency and Currency Volatility: A significant portion of electric actuator components is imported from Asia and Europe, exposing regional OEMs to currency depreciation risk. Brazilian Real and Mexican Peso volatility increases actuator procurement costs, compressing OEM margins and slowing technology upgrade cycles for mid-range vehicle models.

- Limited Local Manufacturing Capability: Latin America lacks deep local actuator manufacturing capacity, with most precision components sourced externally. High tooling investment requirements, limited precision engineering workforce, and restricted rare-earth material access constrain local production, limiting supply chain flexibility and elevating lead ti: Inadequate EV charging infrastructure across secondary Latin America markets limits full electric vehicle adoption, moderating EV-specific actuator demand growth. Slower BEV fleet expansion in Argentina, Colombia, and Peru constrains the market uplift expected from full actuator electrification of powertrain systems.

Market Opportunities

- Fleet Electrification Programs: Government commercial vehicle fleet renewal mandates in Brazil and Mexico create large-scale procurement opportunities for electric brake, throttle, and closure actuators in electric buses and delivery trucks, generating high per-unit actuator revenue.

- ADAS-Integrated Actuator Modules: Rising ADAS penetration in mid-range passenger vehicles is creating demand for integrated actuator-sensor modules, enabling premium system-level procurement contracts for Tier-1 suppliers across the region.

Market Challenges

- Supply Chain Fragmentation: Dependence on multi-tier imported components creates vulnerability to global logistics disruptions, affecting production schedules and OEM delivery commitments for actuator programs across Latin America.

- Cost Pressure from Mechanical Actuator Competition: Conventional hydraulic and pneumatic actuators remain cost-competitive in lower-specification commercial vehicles, limiting electric actuator penetration in cost-sensitive fleet segments across secondary Latin America markets.

Emerging Market Trends

1. ADAS Integration Driving Multi-Function Actuator Adoption

Advanced driver-assistance systems are accelerating adoption of integrated multi-function actuators combining throttle, braking, and stability control into unified electronic modules. This integration trend increases per-vehicle actuator content and average selling price, expanding market revenue beyond simple unit volume growth across Brazil and Mexico.

2. EV Fleet Growth Creating Dedicated Electric Actuator Demand

Growing EV production across Latin America is creating structured demand for fully electric actuator architectures replacing all hydraulic subsystems. Chile's EV adoption leadership and Brazil's electric bus fleet expansion are creating early-stage but growing demand for EV-specific brake, closure, and throttle actuator systems.

3. Smart Closure System Integration in Premium and Semi-Premium Segments

OEM standardization of smart closure actuators for automated tailgates, powered doors, and electronic door handles is expanding across premium and semi-premium vehicle segments. This trend adds new actuator content to vehicle categories previously relying on mechanical closure systems, creating incremental addressable market growth.

4. Commercial Vehicle Electrification Creating Scale Actuator Volume

Fleet electrification initiatives in Brazil and Mexico for public transport and logistics vehicles are creating large-scale actuator procurement opportunities. Electric buses and delivery trucks require fully electric brake, throttle, and auxiliary actuator systems, generating high per-unit actuator revenue and establishing a growing commercial vehicle actuator segment.

Industry Value Chain Analysis

The automotive electric actuator value chain integrates raw material and component sourcing, actuator core manufacturing, assembly and testing, electronics integration, OEM vehicle integration, and after-sales maintenance. The commercial architecture has progressively consolidated toward an integrated actuator-electronics module supply as the primary format for Tier-1 OEM delivery.

|

Stage |

Key Participants |

|

Raw Material & Component Sourcing |

Procurement of copper, electrical steel, rare-earth magnets, aluminum, and polymer components from global and regional suppliers |

|

Actuator Core & Component Manufacturing |

Actuator motor winding, gear mechanism machining, valve body manufacturing, and housing component production by specialized manufacturers |

|

Actuator Assembly & Testing |

Full actuator assembly, performance calibration, endurance testing, and quality validation to OEM specifications at Tier-1 facilities |

|

Electronics & Control System Integration |

Electronic control unit programming, sensor integration, CAN-bus communication module assembly, and ADAS compatibility validation |

|

OEM Vehicle Integration |

Electric actuator installation and integration into vehicle throttle, braking, seating, and closure systems at OEM assembly plants |

|

Aftersales & Maintenance |

Actuator servicing, diagnostics, replacement part supply, and predictive maintenance solutions for fleet operators and workshops |

The raw material and component sourcing tier is the most commercially sensitive stage, exposed to rare-earth price volatility and logistics disruption. The electronics and control system integration tier is experiencing the most rapid technology transition as OEMs migrate from standalone actuators to fully integrated ADAS-compatible actuator-ECU modules.

Technology Landscape in the Latin America Automotive Electric Actuators Industry

Electric Motor-Driven Actuator Technology

Electric motor-driven actuator technology offers high precision, low maintenance, rapid response, and integration with vehicle electronic control systems. Brushless DC and stepper motor-based actuators are progressively replacing hydraulic and pneumatic alternatives across throttle, seating, and closure applications, enabling superior position control and energy efficiency for modern vehicle platforms.

Electrohydraulic Actuator Technology

Electrohydraulic actuator technology combines electric control precision with hydraulic force output, making it suitable for high force braking and steering applications. Electrohydraulic systems are commonly used in selected braking and heavy-duty applications across Latin America truck and bus OEM programs, bridging the transition to fully electric architectures.

Integrated Smart Actuator Technology

Integrated smart actuator technology embeds position sensing, temperature monitoring, and ECU communication within the actuator unit, enabling real-time feedback control and predictive maintenance. In 2025, leading Tier-1 suppliers introduced CAN-FD and LIN bus-compatible smart actuator modules aligned to ADAS integration requirements in next-generation Latin America OEM platforms.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Product |

Throttle Actuator |

27.4% |

2025 |

|

Vehicle Type |

Passenger Vehicle |

71.5% |

2025 |

|

Region |

Brazil |

38.9% |

2025 |

By Product

Throttle Actuator leads at 27.4% in 2025, capturing the highest share through mandatory integration in emission-compliant ICE, hybrid, and electric powertrains. Throttle actuators are universally required across all vehicle categories and powertrain types, sustaining segment leadership through the forecast period.

To access detailed market analysis, Request Sample

Brake Actuator at 22.6% reflects growing ESC and electronic parking brake adoption. Seat Adjustment Actuator at 19.8% represents comfort feature standardization in mid-range vehicles. Closure Actuator at 17.3% captures smart door and tailgate system demand. Others at 12.9% covers HVAC, lighting, and auxiliary actuator applications in premium segments.

By Vehicle Type

Passenger vehicles lead at 71.5% in 2025, driven by the highest per-vehicle actuator content in modern sedans and SUVs, OEM standardization of electronic safety systems, and Brazil's dominance in regional passenger car production volumes.

Commercial vehicles at 28.5% are witnessing above-average growth as fleet electrification and logistics sector expansion drive brake, throttle, and closure actuator demand in trucks and buses. Government fleet renewal programs and emission mandates are accelerating commercial vehicle actuator upgrade cycles across Brazil and Mexico.

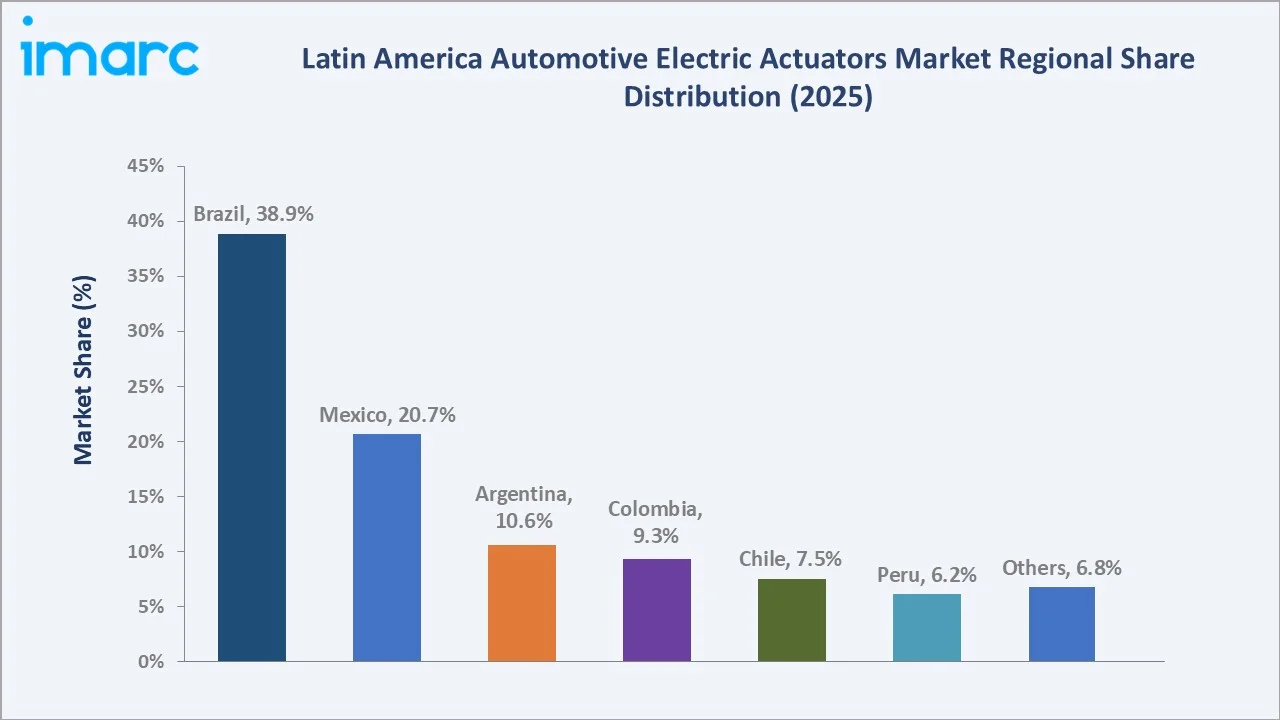

Regional Market Insights

|

Country |

Share (2025) |

Key Market Drivers & Characteristics |

|

Brazil |

38.9% |

Largest automotive producer in Latin America; PROCONVE emission mandates drive throttle and brake actuator demand; strong OEM and Tier-1 manufacturing presence |

|

Mexico |

20.7% |

USMCA export manufacturing hub; North America OEM integration requires advanced actuator specifications; growing EV assembly programs |

|

Argentina |

10.6% |

Recovering automotive sector; growing consumer demand for comfort features in mid-range vehicles; government incentives supporting local vehicle assembly |

|

Colombia |

9.3% |

Expanding commercial vehicle fleet; logistics growth creating brake and throttle actuator demand; rising urban mobility investment programs |

|

Chile |

7.5% |

Highest EV penetration rate in Latin America; progressive adoption of fully electric actuator architectures; strong government electrification policy support |

|

Peru |

6.2% |

Growing vehicle import volumes driving actuator-equipped new vehicle sales; urban mobility expansion creating incremental actuator demand |

|

Others |

6.8% |

Includes Ecuador, Venezuela, Bolivia, and other markets; early-stage growth led by vehicle import expansion and regional fleet renewal programs |

Brazil at 38.9% leads through its established OEM ecosystem and emission-compliance mandate. Mexico at 20.7% reflects export-oriented manufacturing requiring OEM-specification actuator systems. Chile leads per-capita EV adoption in Latin America, progressively shifting demand toward fully electric actuator architectures across vehicle subsystems.

Argentina at 10.6% and Colombia at 9.3% represent emerging sub-markets with growing commercial vehicle and mid-range passenger car actuator demand. Chile at 7.5% and Peru at 6.2% together contribute 13.7% of regional revenue, with Chile driving above-average growth through accelerating EV adoption and progressive electrification policy.

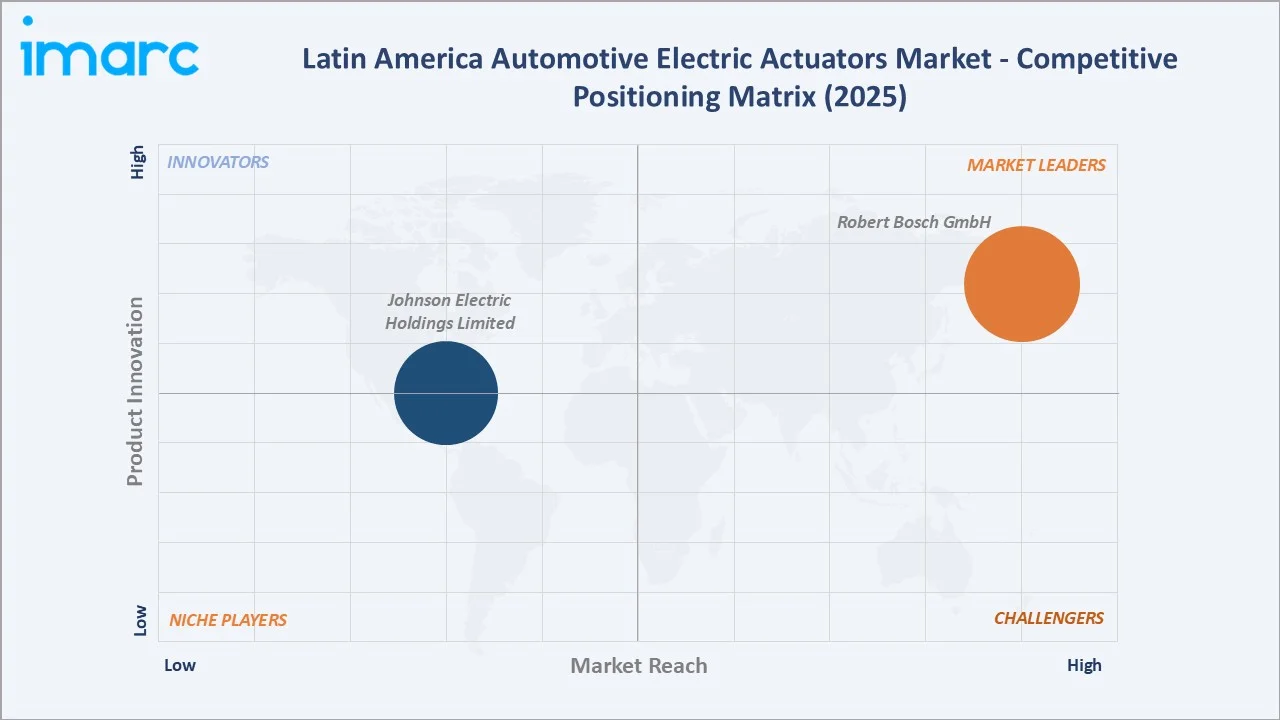

Competitive Landscape

The Latin America automotive electric actuators market is moderately concentrated, with global Tier-1 automotive suppliers dominating OEM supply relationships. The competitive landscape comprises global full-portfolio Tier-1s with regional manufacturing, specialized technology suppliers serving premium OEM programs, and local distributors serving aftermarket channels.

|

Company Name |

Key Products |

Market Position |

Core Strength |

|

Robert Bosch GmbH |

Actuators for powertrain, General-purpose actuator, Comfort actuators |

Market Leader |

Broadest actuator portfolio with deep integration into Latin America OEM supply chains and regional manufacturing presence in Brazil |

|

Johnson Electric Holdings Limited |

Coolant & Refrigerant Valve Actuators, Headlamp Actuators, HVAC Actuators, Grill Shutter Actuators |

Established Player |

Broad comfort and closure actuator range serving Latin America OEMs with competitive pricing and application breadth |

Key players include Robert Bosch GmbH, Johnson Electric Holdings Limited, and others.

Key Company Profiles

Robert Bosch GmbH

Robert Bosch GmbH is a Germany-based multinational engineering and technology company and the world's largest automotive supplier, with a strong presence in the Latin America automotive electric actuators market through its comprehensive powertrain and chassis actuation portfolio across all major OEM programs in Brazil and Mexico.

- Key Products: Actuators for powertrain, General-purpose actuator, Comfort actuators.

- Strategic Focus: Expanding integrated actuator and sensor modules for hybrid and EV platforms while deepening Brazil and Mexico OEM supply relationships through localized manufacturing and engineering support.

Johnson Electric Holdings Limited

Johnson Electric Holdings Limited is a Hong Kong-based global leader in electric motors, actuators, and motion subsystems, with an active manufacturing and supply presence in Latin America, serving regional automotive OEM programs across comfort, thermal, and closure actuator applications.

- Key Products: Coolant & Refrigerant Valve Actuators, Headlamp Actuators, HVAC Actuators, Grill Shutter Actuators.

- Recent Developments: In April 2025, Johnson Electric launched its new EV Locking Actuator, designed for safe EV charging port locking applications, reinforcing its expanding portfolio for electric vehicle platforms supplied to OEMs operating in Latin America assembly programs.

- Strategic Focus: Expanding EV thermal management actuators, chassis, and body actuator content, and e-powertrain auxiliary systems for OEM EV programs, with localized production capacity in Mexico supporting reduced lead times for Latin America automotive customers.

Market Concentration Analysis

The Latin America automotive electric actuators market is moderately concentrated at the Tier-1 OEM supply level, with the top 3-4 key players collectively accounting for an estimated 45–55% of regional actuator revenue. Global Tier-1 suppliers hold structural advantages through OEM qualification programs, regional manufacturing investment, and integrated product portfolios.

Market concentration is gradually declining as specialized actuator suppliers gain OEM qualification for niche applications. The commercial vehicle segment is attracting additional competitor entry as fleet electrification mandates create large-scale procurement opportunities distinct from the passenger car actuator market structure.

Investment & Growth Opportunities

Highest Growth Segments

Throttle Actuator electrification for hybrid platforms (~5.1% CAGR), electric brake actuator adoption in safety-mandated vehicles (~4.8% CAGR), seat adjustment actuators for mid-range vehicle standardization (~4.9% CAGR), smart closure systems (~4.3% CAGR), and commercial vehicle fleet electrification programs represent the highest-growth investment vectors through 2034.

Emerging Investment Opportunities

Brazil's fleet electrification programs for public transport and commercial vehicles represent the market's highest per-unit-value emerging opportunity. Electric bus and commercial truck actuator systems generate 2–3x the per-unit revenue of passenger car actuators. Government fleet renewal contracts in Brazil and Mexico create structurally growing demand through 2034.

Investment Themes

- Local manufacturing capacity in Brazil or Mexico: Reducing import dependency, leveraging USMCA and Mercosur trade benefits, and achieving cost advantages for OEM supply programs through regional actuator production.

- EV-ready integrated actuator module development: Investing in combined electric actuator modules for BEV architectures to capture the growing EV-specific actuator market in Chile and Brazil as regional EV adoption accelerates.

- ADAS-integrated smart actuator system supply: Developing actuator systems with embedded ECU and sensor communication capability aligned to ADAS adoption growth across premium and semi-premium passenger vehicle OEM programs.

Future Market Outlook (2026-2034)

The Latin America automotive electric actuators market is projected to grow from USD 1.21 Billion in 2025 to USD 1.81 Billion by 2034, delivering a 4.56% CAGR. Brazil's emission regulation tightening, Mexico's export-oriented OEM electrification, and Chile's accelerating EV adoption collectively define the structural demand trajectory through 2034.

Three structural forces define market growth through 2034: regulatory-driven actuator technology upgrades across ICE and hybrid vehicle fleets; OEM electrification investment creating EV-specific actuator demand; and consumer preference shifts toward feature-rich vehicles standardizing comfort and safety actuators in mid-range segments across all major Latin America markets.

The market's anchor value of approximately USD 1.52 Billion in 2030 represents the actuator industry's key commercial inflection, when EV-specific actuator architectures will achieve mainstream OEM adoption alongside continued ICE and hybrid platform actuator volume growth.

Research Methodology

Primary Research

Primary research comprised structured interviews with 40+ industry stakeholders (2025), including OEM procurement directors, Tier-1 actuator sales leads, automotive association representatives, and EV program engineers across Brazil, Mexico, Argentina, and Chile.

Secondary Research

Secondary research encompassed company annual reports, ANFAVEA Brazilian vehicle production statistics, AMIA Mexican automotive industry data, Latin America EV adoption reports, government emission regulation publications, IMARC Group market databases, and regional OEM investor presentations. Over 50 secondary sources reviewed.

Forecasting Models

Market revenue forecasts developed using bottom-up vehicle production model: (i) regional vehicle production forecast by country and vehicle type; (ii) average actuator content per vehicle by segment; (iii) average actuator revenue per vehicle by product type; (iv) regulatory compliance adjustment for emission-driven actuator technology upgrade cycles.

Latin America Automotive Electric Actuators Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Products Covered | Throttle Actuator, Seat Adjustment Actuator, Brake Actuator, Closure Actuator, Others |

| Vehicle Types Covered | Passenger Vehicle, Commercial Vehicle |

| Countries Covered | Brazil, Mexico, Argentina, Colombia, Chile, Peru, Others |

| Companies Covered | Robert Bosch GmbH, Johnson Electric Holdings Limited, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the Latin America automotive electric actuators market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the Latin America automotive electric actuators market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the Latin America automotive electric actuators industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Latin America Automotive Electric Actuators Market Report

The market reached USD 1.21 Billion in 2025, with Brazil leading at 38.9% regional share, Throttle Actuator dominating at 27.4%, and Passenger Vehicles contributing 71.5% of demand.

The market grows at 4.56% CAGR during 2026-2034, reaching USD 1.81 Billion by 2034, driven by vehicle electrification, emission regulations, ADAS integration, and OEM feature standardization.

Throttle Actuator leads at 27.4% in 2025, capturing the highest share through mandatory integration in emission-compliant and electrified powertrain systems across all vehicle categories and powertrain types.

Passenger vehicles lead at 71.5% through high per-vehicle actuator content and OEM standardization of electronic safety and comfort systems. Commercial vehicles at 28.5% are the fastest-growing sub-segment.

Brazil leads at 38.9% through its established OEM manufacturing ecosystem, emission compliance mandates under PROCONVE, and the region's largest vehicle production and sales volumes.

Leading companies include Robert Bosch GmbH, Johnson Electric Holdings Limited, and others.

The market is projected to reach approximately USD 1.52 Billion by 2030, driven by ADAS integration growth, commercial vehicle fleet electrification, and smart closure system standardization.

Key opportunities include local actuator manufacturing in Brazil or Mexico, EV-ready integrated actuator module development, ADAS-compatible smart actuator systems, and commercial fleet electrification programs.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)