Low Voltage DC Circuit Breaker Market Size, Share, Trends and Forecast by Type, Application, End User, and Region, 2026-2034

Global Low Voltage DC Circuit Breaker Market Size, Share, Trends & Forecast (2026-2034)

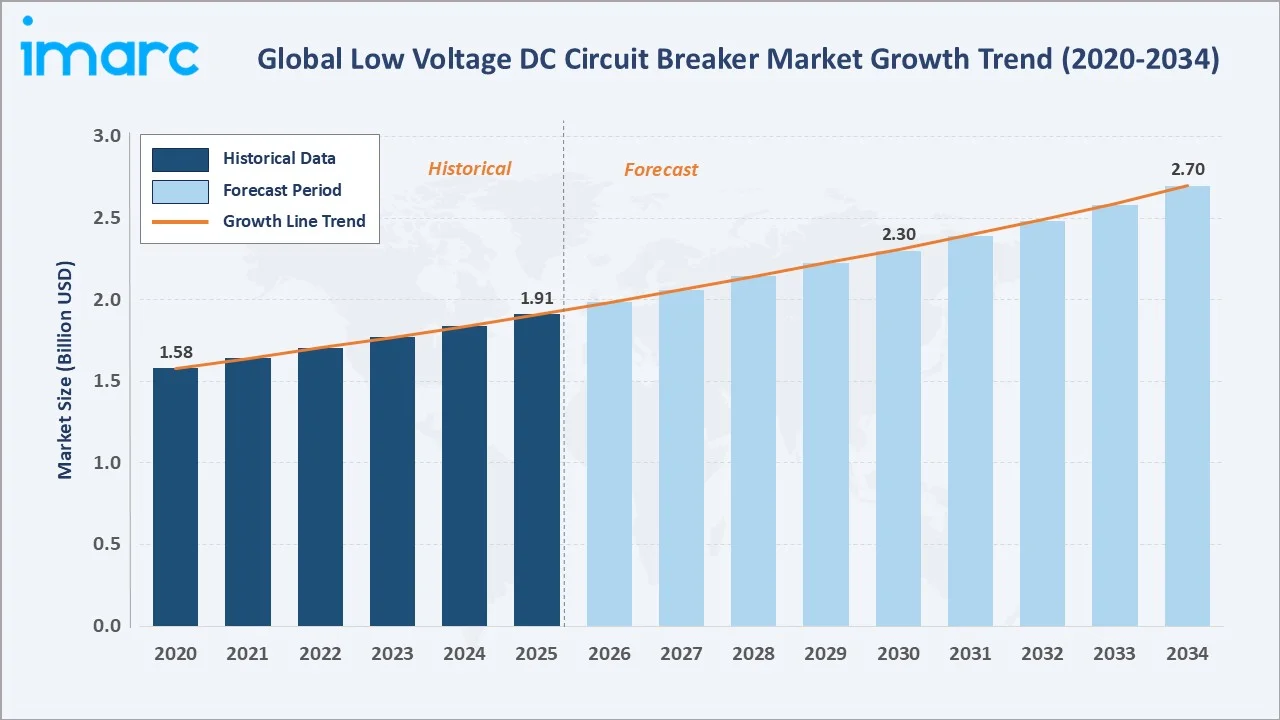

The global low voltage DC circuit breaker market reached USD 1.91 Billion in 2025 and is projected to reach USD 2.70 Billion by 2034, growing at a CAGR of 3.81% during 2026-2034. Rapid expansion of renewable energy installations, surging demand from data centers and EV battery infrastructure, and accelerating grid modernization are the primary catalysts.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 1.91 Billion |

|

Forecast Market Size (2034) |

USD 2.70 Billion |

|

CAGR (2026-2034) |

3.81% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

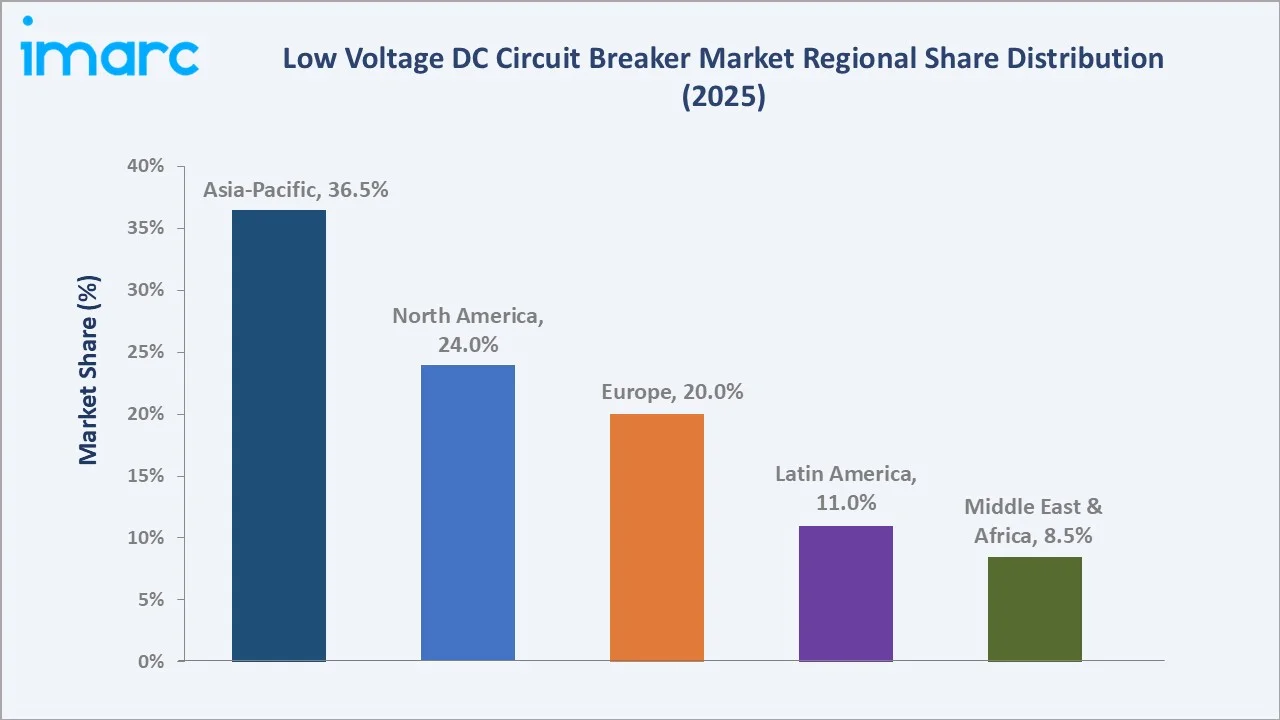

Asia-Pacific (36.5% share, 2025) |

|

Fastest Growing Region |

Asia-Pacific |

Asia-Pacific leads globally with a 36.5% revenue share in 2025, driven by large-scale solar and EV deployments across China, India, and South Korea.

To get more information on this market, Request Sample

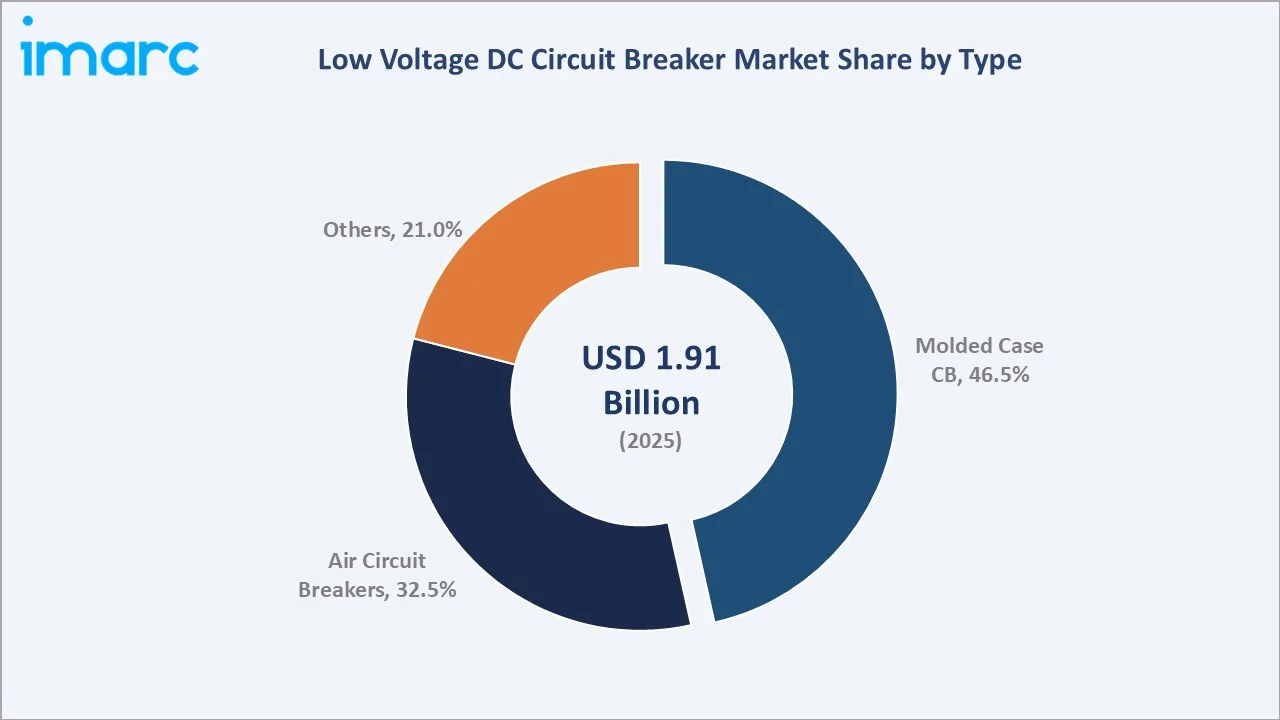

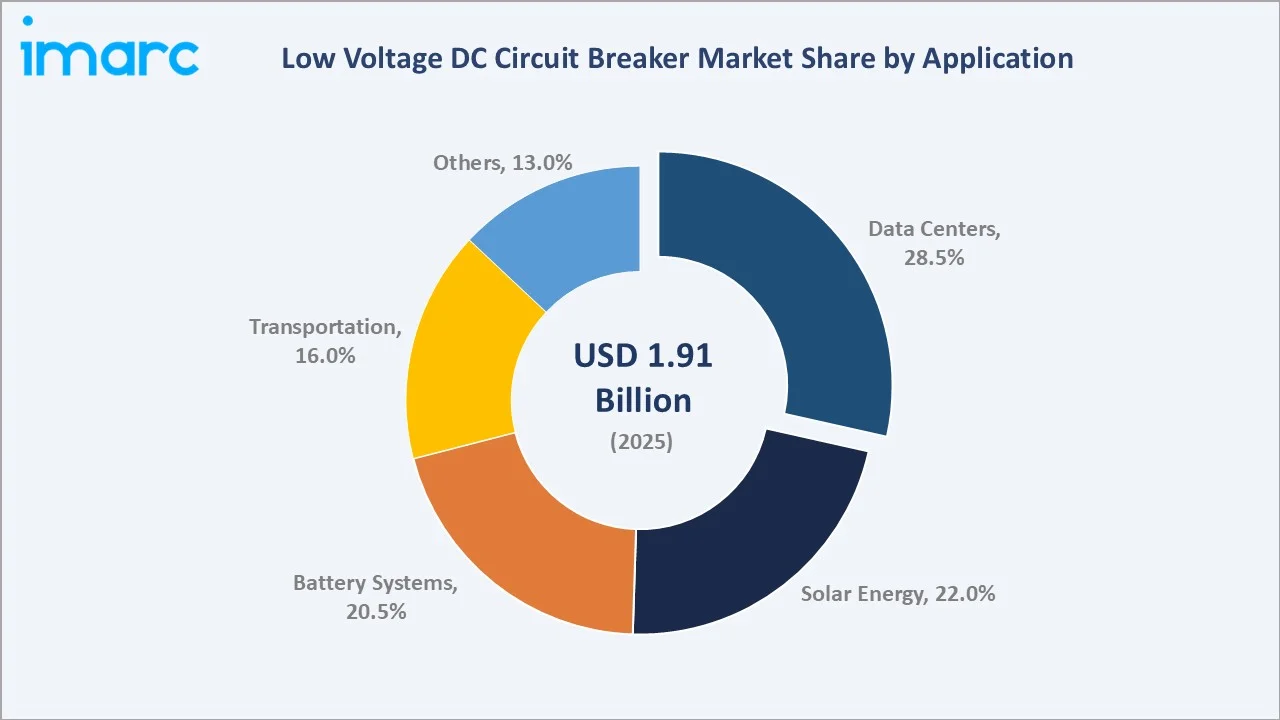

Molded Case Circuit Breakers (MCCBs) dominate the type segment with a 46.5% share in 2025. Data centers represent the largest application at 28.5%. The shift towards DC power distribution in hyperscale facilities and utility-scale solar plants is reshaping product demand and driving innovation toward higher voltage ratings and solid-state switching.

Executive Summary

The global low voltage DC circuit breaker market is on a consistent growth trajectory, underpinned by the global energy transition, the proliferation of DC-native infrastructure, and tightening electrical safety regulations. The market reached USD 1.91 Billion in 2025 and is forecast to surpass USD 2.70 Billion by 2034, reflecting a CAGR of 3.81%.

Asia-Pacific commands 36.5% of the market in 2025, with China and India deploying large-scale solar and battery storage systems that require DC-rated protection. North America (24.0%) is driven by hyperscale data center investment and EV fast-charging infrastructure. Europe (20.0%) remains a mature but steady market with strong regulatory compliance demand under IEC 60947 and EN 50604 standards.

Leading global manufacturers, including ABB, Siemens, Schneider Electric, Eaton, Legrand SA, and Mitsubishi Electric Corporation, continue to invest in smart, communicating circuit breakers and solid-state CB technology to address the growing complexity of DC power systems.

Key Market Insights

|

Insight |

Data |

|

Largest Segment (Type) |

Molded Case Circuit Breaker – 46.5% share (2025) |

|

Largest Segment (Application) |

Data Centers – 28.5% share (2025) |

|

Leading Region |

Asia-Pacific – 36.5% revenue share (2025) |

|

Fastest Growing Application |

Solar Energy (CAGR 5.8%, 2026-2034) |

|

Top Companies |

ABB, Siemens, Schneider Electric, Eaton, Legrand SA, and Mitsubishi Electric Corporation |

|

Market Opportunity |

Solid-state DC circuit breakers projected to exceed USD 400 Million by 2034 |

Key Analytical Observations Supporting the Above Data:

- Molded Case Circuit Breakers – 46.5% share (2025): MCCBs dominate due to their compact design, adjustable trip ratings (up to 1,600 A), and suitability for solar combiner boxes, battery racks, and EV charging infrastructure.

- Data Centers – 28.5% application share (2025): The hyperscale data center construction boom, with global investment surpassing USD 340 Billion in 2024, is driving demand for high-reliability DC protection.

- Asia-Pacific – 36.5% regional share (2025): China's 250 GW annual solar installation target through 2025 and India's 500 GW renewable energy target by 2030 collectively require hundreds of millions of DC circuit breakers for PV string, combiner, and inverter-level protection.

- Solar Energy – fastest-growing application (CAGR 5.8%): Each MW of utility-scale solar PV requires approximately 1,500–2,000 DC circuit breakers. Global solar capacity additions exceeding 400 GW per year through 2034 will sustain this growth trajectory.

- Solid-state DC CBs – emerging high-value opportunity: Solid-state circuit breakers eliminate arc interruption challenges, enabling sub-millisecond fault clearing. Pilot deployments in railway traction and naval microgrids are expanding into commercial data center and EV applications.

Global Low Voltage DC Circuit Breaker Market Overview

Low-voltage DC circuit breakers are electrical protection devices designed to interrupt fault currents in DC circuits operating up to 1,500 V. Unlike AC circuit breakers, DC variants must overcome the absence of a natural current zero crossing, requiring specialized arc extinction chambers, magnetic blowout coils, or solid-state switching elements to safely interrupt fault currents.

Applications span solar PV systems, battery energy storage, EV charging infrastructure, data centers, railway traction, and marine/offshore installations. The IEC 60947-2 and UL 489B standards govern product certification, with increasingly stringent requirements driving R&D investment in higher-performance DC interruption technologies.

Market Dynamics

To evaluate market opportunities, Request Sample

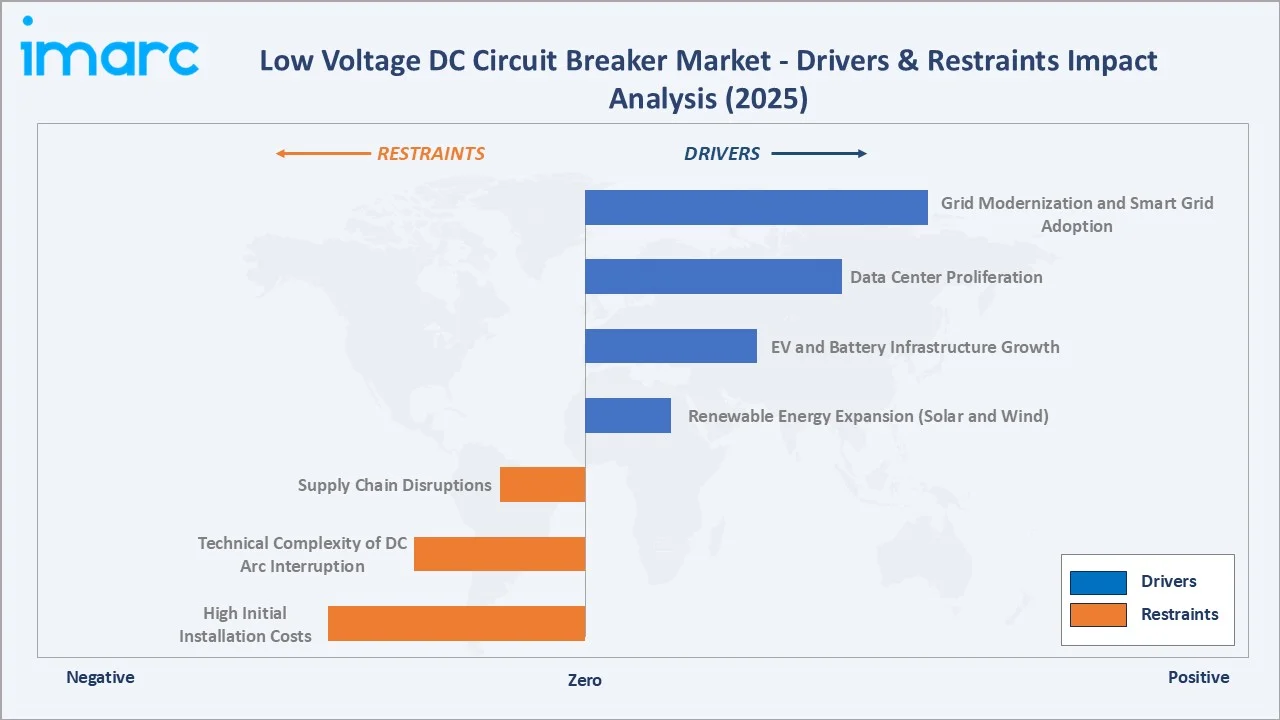

Market Drivers

- Renewable Energy Expansion (Solar and Wind): By the end of 2024, global solar PV capacity reached 2,247 GW, nearly double the total installed in 2022 and more than three times the capacity installed before 2020.

- EV and Battery Infrastructure Growth: Global EV sales reached 17 million units in 2024, requiring DC protection at battery management system, pack, and fast-charger levels. In 2024, over 1.3 million public charging points were added globally, marking a 30%+ increase compared to the previous year, each requiring certified DC circuit protection.

- Data Center Proliferation: Hyperscale data center investment exceeded USD 340 Billion globally in 2024. Migration to 380 V DC power distribution architecture reduces conversion losses compared to 480 V AC systems and increases demand for DC-rated overcurrent protection devices at every distribution tier.

- Grid Modernization and Smart Grid Adoption: Utilities globally are investing in DC microgrids and HVDC interconnections, requiring low-voltage DC protection at the local distribution level. U.S. Department of Energy allocated USD 3.5 billion to support 58 projects in 44 states under the Grid Resilience and Innovation Partnerships program.

Market Restraints

- High Initial Installation Costs: DC circuit breakers carry a 25–40% cost premium over equivalent AC units due to more complex arc extinction mechanisms. For cost-sensitive small-scale solar and battery installations in emerging markets, this represents a barrier to premium-specification procurement.

- Technical Complexity of DC Arc Interruption: DC arc interruption requires specialized engineering knowledge. The absence of a natural current zero creates longer, more energetic arcs than AC equivalents. Incorrectly specified or installed DC CBs can fail to interrupt faults, representing a safety and liability risk for installers.

- Supply Chain Disruptions: Copper (primary conductor material) experienced 22% price volatility between 2022 and 2025. Arc chamber component shortages affected lead times across the industry, with average delivery windows extending from 4 weeks to 14 weeks for some product lines in 2022–2023.

Market Opportunities

- Solid-State DC Circuit Breaker Technology: Solid-state CBs using IGBT or GaN power semiconductors can interrupt DC faults in under 1 millisecond, 1,000 times faster than mechanical equivalents. ABB and Eaton have demonstrated prototypes; commercial scale-up will address railway, data center, and naval microgrid applications with a total addressable market exceeding USD 400 Million by 2034.

- Emerging Market Solar Expansion: India is targeting 450 GW of additional renewable capacity by 2030. Local content requirements and cost-sensitive procurement in these markets create manufacturing and partnership opportunities for international CB producers establishing regional production.

- Building Integration and Microgrids: The U.S. Department of Energy (DOE) Office of Electricity has announced over USD 8 million in funding selections for projects aimed at accelerating microgrid innovation through the Community Microgrid Assistance Partnership (C-MAP) program.

Market Challenges

- Standardization Fragmentation: Diverging certification requirements between IEC 60947-2 (Europe), UL 489B (North America), and GB/T standards (China) increase per-product compliance costs by up to 18% for manufacturers targeting multiple geographies, slowing international expansion strategies.

- Competition from Fuse-Based Protection: High-speed DC fuses remain a lower-cost alternative for many solar string and battery rack protection applications. Fuses offer faster interrupt times for some fault profiles and remain preferred in cost-sensitive utility-scale deployments where reset-ability is not a priority.

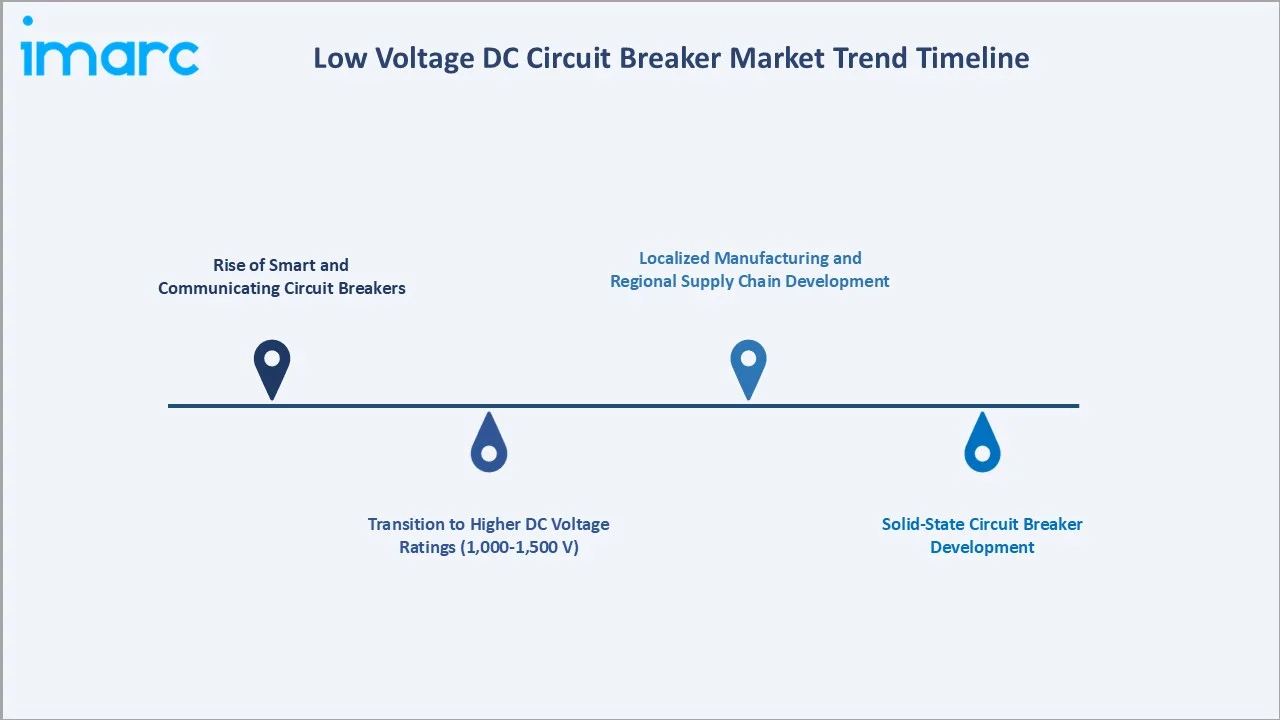

Emerging Market Trends

1. Rise of Smart and Communicating Circuit Breakers

ABB's SACE Emax 2 and Schneider Electric's MasterPact MTZ series offer integrated power metering and SCADA connectivity. Communicating circuit breaker installations grew 38% in 2024 versus 2023, with the segment projected to represent 22% of total DC CB sales by 2030.

2. Transition to Higher DC Voltage Ratings (1,000–1,500 V)

Utility-scale solar PV systems are migrating from 1,000 V to 1,500 V DC string configurations, reducing copper cabling costs by 25–30% and improving inverter efficiency. This voltage migration requires upgraded DC circuit breakers with 1,500 V DC ratings, creating a significant retrofit and new-installation demand wave. IEC 60947-2 Edition 5 (2022) incorporated 1,500 V DC testing requirements, accelerating product certification timelines.

3. Solid-State Circuit Breaker Development

Siemens' SION 3VA DC and GE's research into GaN-based DC CBs represent the industry frontier. Commercial deployment in railway traction and data center applications is projected between 2027 and 2029, with broader market penetration by 2034.

4. Localized Manufacturing and Regional Supply Chain Development

In 2023, Schneider Electric laid the foundation for a new state‑of‑the‑art manufacturing factory in Kolkata for manufacturing energy-efficient products and electrical distribution systems. ABB expanded its circuit breaker manufacturing capacity in China, and the U.S. Regional production reduces lead times from 12+ weeks to 3–4 weeks for key Asian and North American markets, improving competitive positioning versus import-dependent suppliers.

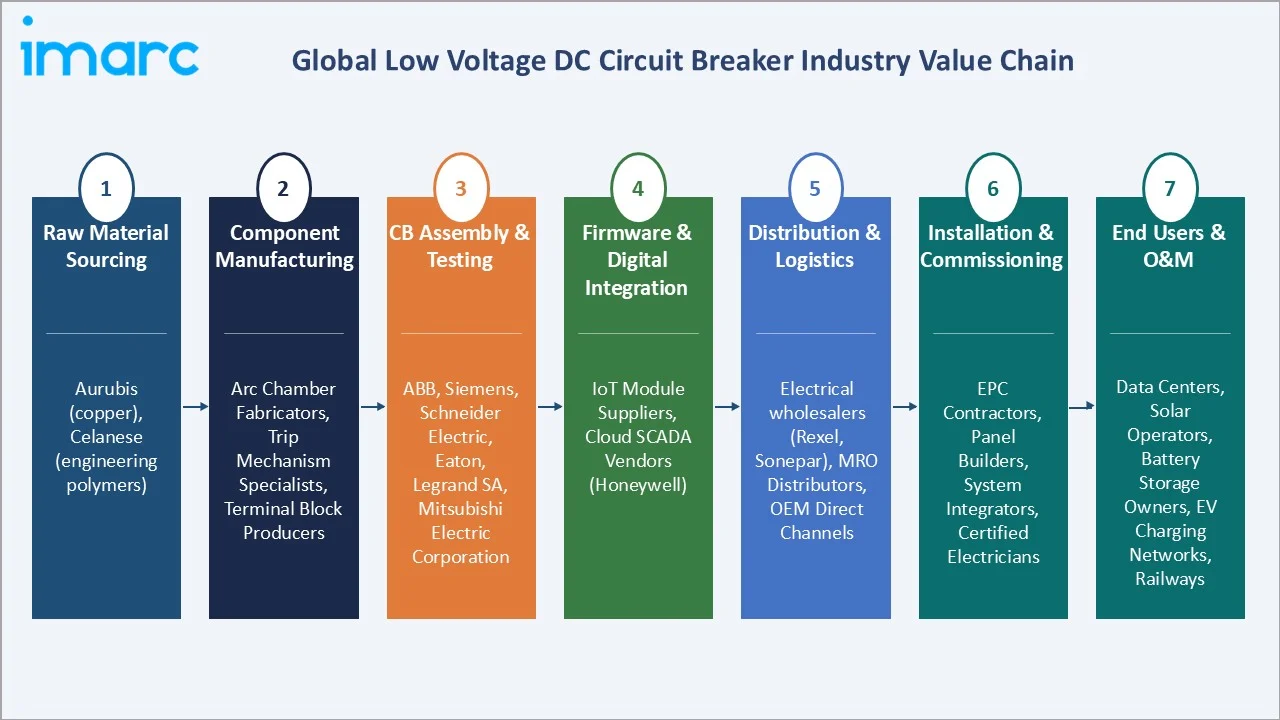

Industry Value Chain Analysis

The low-voltage DC circuit breaker value chain spans specialized raw material inputs through precision electromechanical manufacturing, firmware integration, and application-specific installation by trained contractors. Each stage requires specialized technical expertise.

|

Stage |

Key Players / Examples |

|

Raw Material Sourcing |

Aurubis (copper), Celanese (engineering polymers) |

|

Component Manufacturing |

Arc chamber fabricators, trip mechanism specialists, terminal block producers |

|

CB Assembly & Testing |

ABB, Siemens, Schneider Electric, Eaton, Legrand SA, and Mitsubishi Electric Corporation |

|

Firmware & Digital Integration |

IoT module suppliers, cloud SCADA vendors (Honeywell) |

|

Distribution & Logistics |

Electrical wholesalers (Rexel, Sonepar), MRO distributors, OEM direct channels |

|

Installation & Commissioning |

EPC contractors, panel builders, system integrators, certified electricians |

|

End Users & O&M |

Data centers, solar operators, battery storage owners, EV charging networks, and railways |

Technology Landscape in the Low Voltage DC Circuit Breaker Industry

Advanced Arc Extinction Technologies

Modern DC circuit breakers employ multiple arc extinction strategies, including magnetic blowout (de-ion grid chambers), series resistance insertion, and permanent magnet-assisted arc elongation. Eaton's NZM series uses a patented double-break contact system, achieving 100 kA DC interrupting capacity.

Electronic Trip Unit Technology

Microprocessor-based electronic trip units (ETUs) replace traditional thermal-magnetic bimetals, enabling precise, programmable trip characteristics including long-time delay, short-time delay, and instantaneous thresholds. Schneider Electric's Micrologic family and ABB's Ekip Trip Units offer onboard power quality measurement, harmonic analysis, and energy monitoring – transforming the circuit breaker from a passive protection device into an active power management node.

Solid-State and Hybrid Switching

Hybrid DC circuit breakers combine mechanical pre-charge contacts with solid-state semiconductor switches. The mechanical path carries normal load current (low conduction losses), while the semiconductor path clears faults at near-infinite speed. This architecture, pioneered by ABB for HVDC applications, is being scaled down for low-voltage DC applications. Hybrid designs achieve fault clearing in under 2 milliseconds at 1,000 V DC with interrupting ratings up to 50 kA.

Market Segmentation Analysis

The report covers the following segments:

| Segment Category | Leading Segment | Market Share | Year |

|---|---|---|---|

| Type | Molded Case Circuit Breaker | 46.5% | 2025 |

| Application | Data Centers | 28.5% | 2025 |

| End User | 🔒 | 🔒 | 2025 |

| Region | Asia-Pacific | 36.5% | 2025 |

By Type

Molded case circuit breakers dominate the type segment with a 46.5% share in 2025. MCCBs offer compact, cost-effective protection for currents up to 1,600 A and are the standard choice for solar combiner boxes, battery management systems, and EV charger main disconnects. Their molded thermoplastic housing, integrated thermal-magnetic or electronic trip units, and field-adjustable settings drive broad adoption.

To access detailed market analysis, Request Sample

Air circuit breakers hold a 32.5% share, primarily serving high-current applications (1,000–6,300 A) in utility-scale solar inverter rooms, large battery energy storage system (BESS) installations, and data center main distribution boards.

By Application

Data centers represent the largest application segment at 28.5% in 2025. It is projected that 56% of new global data center capacity between 2023 and 2035 will be sourced from renewable energy. The migration to 380 V DC bus architectures reduces energy conversion stages, making DC distribution the preferred architecture for Tier III and Tier IV facilities.

Solar energy holds 22.0% of the application mix, the fastest-growing segment at a CAGR of 5.8% through 2034. Battery systems represent 20.5%, driven by utility-scale BESS deployments and behind-the-meter residential storage. Transportation accounts for 16.0%, covering EV charging infrastructure, railway traction power, and marine DC distribution.

Regional Market Insights

Asia-Pacific's market leadership (36.5%, 2025) is driven by China's annual solar installation rate of 250+ GW, India's Renewable Energy by 2030 programme, and South Korea's large-scale BESS deployments. China alone accounts for approximately 22% of the global market, with domestic manufacturers competing strongly at the mid-market tier alongside global OEMs.

|

Region |

Share (2025) |

Key Growth Drivers |

Regulatory Impact |

|

Asia-Pacific |

36.5% |

Solar PV, BESS, EV infrastructure, data centers |

IEC 60947-2, GB/T standards, local content rules |

|

North America |

24.0% |

Hyperscale data centers, EV charging, and grid modernisation |

UL 489B, NEC 2023, DOE grid investment programs |

|

Europe |

20.0% |

Offshore wind, EV expansion, industrial automation |

IEC 60947-2, CE marking, EU Green Deal compliance |

|

Latin America |

11.0% |

Solar expansion (Brazil, Chile), mining, oil & gas |

ABNT NBR standards, ANEEL renewable mandates |

|

Middle East & Africa |

8.5% |

Utility-scale solar (NEOM, DEWA), data centers |

IEC standards, GCC grid codes, Aramco specs |

North America (24.0%) is the second-largest market, with the U.S. hyperscale data center investment pipeline exceeding USD 500 Billion through 2030. The Inflation Reduction Act (IRA) has accelerated domestic solar and battery storage investments, expanding the DC protection addressable market.

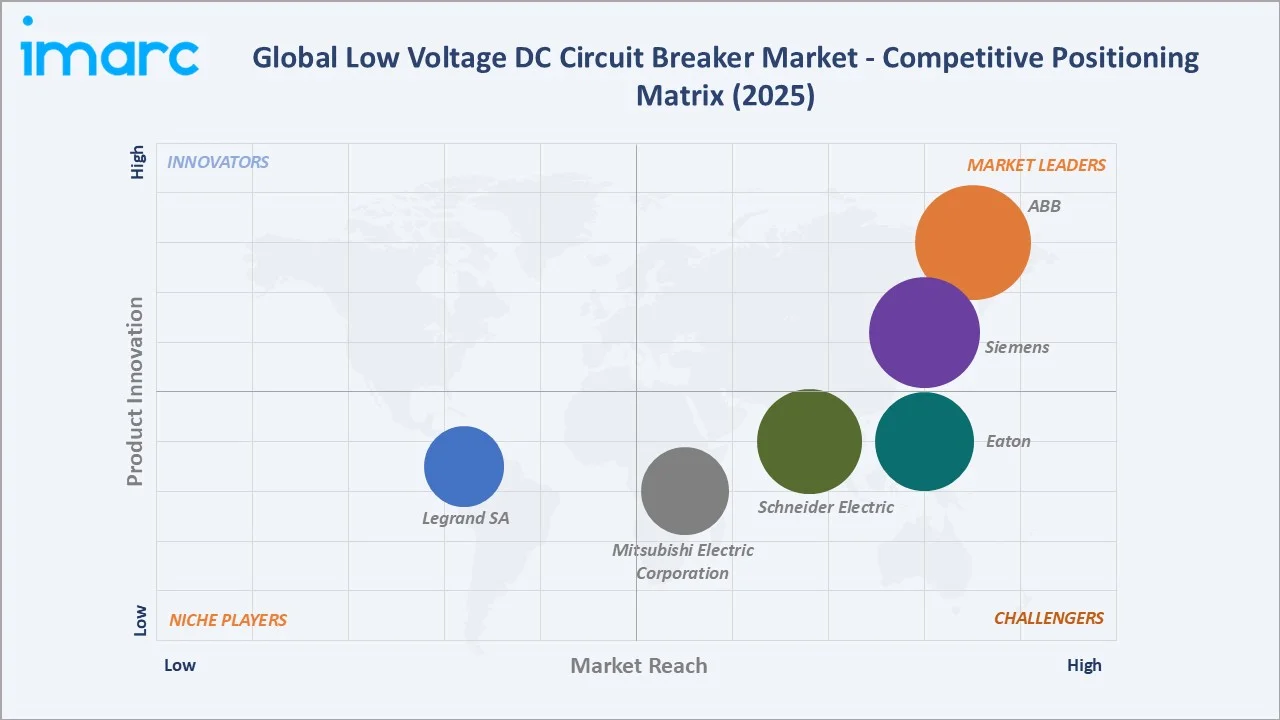

Competitive Landscape

The global low voltage DC circuit breaker market exhibits moderate concentration. The top five manufacturers, ABB, Siemens, Schneider Electric, Eaton, and Legrand SA, collectively account for approximately 55–60% of global revenue in 2025.

|

Company Name |

Brand / Product Line |

Market Position |

Core Strength |

|

ABB |

SACE Emax2, Tmax, System pro M, SACE Infinitus |

Market Leader |

Broadest DC CB product portfolio; 1,500 V DC rating; solid-state CB R&D leadership |

|

Siemens |

SENTRON 3VA, 3WL |

Market Leader |

IEC/UL dual-certified products; digital grid solutions; strong data center presence |

|

Schneider Electric |

Masterpact NW DC, Compact NSX DC |

Strong Challenger |

EcoDesign sustainable CBs; IoT-enabled Micrologic trip units; solar-optimised variants |

|

Eaton |

NZM, Power Defense |

Strong Challenger |

DC-rated series for solar and BESS; solid-state CB development; UL 489B leadership |

|

Legrand SA |

DX3 |

Niche Player |

European residential and commercial focus; strong installer channel distribution |

|

Mitsubishi Electric Corporation |

NF-CV, NF-S Series |

Challenger |

Asia-Pacific strength; railway and industrial OEM specification experience |

Regional manufacturers in China and India account for a significant share of volume in cost-sensitive residential and small commercial solar applications.

Key Company Profiles

ABB

ABB, headquartered in Zurich, Switzerland, is the global market leader in low-voltage DC circuit breakers with the most comprehensive product portfolio spanning MCCBs, ACBs, and miniature circuit breakers rated up to 1,500 V DC.

- Product Portfolio: SACE Emax 2 (ACB, up to 1,500 V DC), SACE Tmax XT (MCCB), System pro M Compact (MCB) – all with optional Ekip smart trip units.

- Recent Developments: In October 2025, ABB unveiled its next‑generation low‑voltage power distribution solution for AI‑ready data centers, featuring the advanced SACE Emax 3 air circuit breaker integrated into its MNS switchgear.

- Strategic Focus: Solid-state CB commercialization; digital connectivity via ABB Ability platform; expansion in Asia-Pacific solar and BESS markets.

Siemens AG

Siemens, headquartered in Munich, Germany, is a leading global supplier of low-voltage switchgear. Its Smart Infrastructure division includes circuit breakers for industrial, commercial, and renewable energy applications.

- Product Portfolio: SENTRON 3VA MCCB (DC-rated), SENTRON 3WL ACB, SENTRON 3QD2 semiconductor circuit breaker (SCCB)

- Recent Developments: Siemens’s new Low‑Voltage DC circuit breaker (SENTRON 3QD2) delivers ultrafast semiconductor‑based interruption in microseconds for enhanced protection and system availability in DC grids.

- Strategic Focus: Digital grid integration; DC power architecture for data centers; solid-state CB development for railway and industrial microgrids.

Schneider Electric SE

Schneider Electric, headquartered in Rueil-Malmaison, France, focuses on energy management and automation. Its Low Voltage Products division supplies circuit breakers to data center, industrial, and renewable energy sectors globally.

- Product Portfolio: MasterPact MTZ (ACB, DC-rated), ComPact NSX (MCCB), Multi 9 C60H-DC (MCB for solar).

- Recent Developments: Schneider Electric has signed a long‑term framework agreement with E.ON to supply its SF₆‑free medium‑voltage switchgear, accelerating the deployment of sustainable, digital‑ready grid infrastructure across E.ON’s network ahead of upcoming EU regulations.

- Strategic Focus: EcoDesign and circular economy product development; energy efficiency in data centers; growth in solar and BESS protection segments.

Market Concentration Analysis

The low voltage DC circuit breaker market exhibits moderate concentration at the top tier, with ABB, Siemens, Schneider Electric, Eaton, Legrand SA, collectively holding approximately 55–60% of global revenue in 2025. Below this tier, a substantial mid-market exists populated by Mitsubishi Electric, Fuji Electric, CHINT Group, Delixi Electric, and regional specialists across Asia, Latin America, and the Middle East.

Consolidation activity is accelerating, driven by the technical complexity of DC interruption (creating barriers for smaller manufacturers), IEC/UL certification costs, and the increasing importance of digital communication protocols that require software development investment.

Investment & Growth Opportunities

Fastest Growing Segments

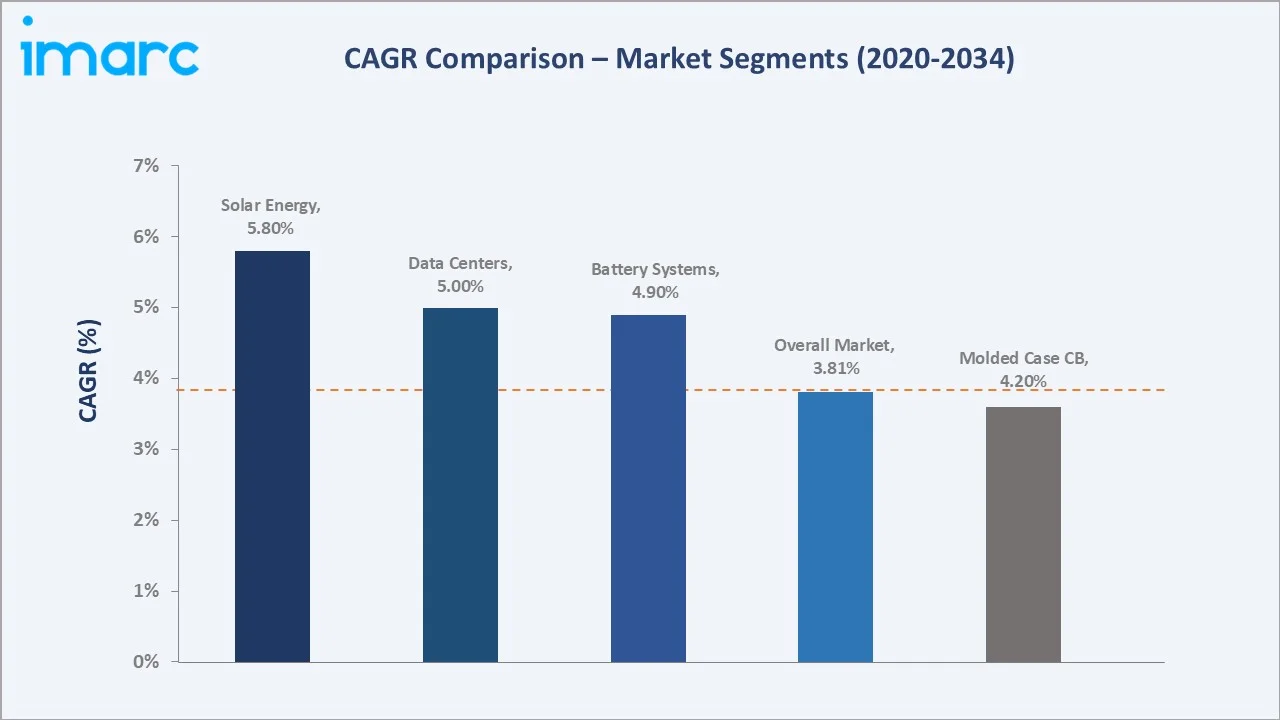

Solar energy applications (CAGR 5.8%), battery system protection (CAGR 4.9%), and data center DC infrastructure (CAGR 5.0%) represent the three highest-growth investment vectors through 2034. Together, these segments address an incremental demand of approximately USD 550 Million beyond the base 2025 market over the forecast decade.

Solid-State Circuit Breaker Technology

The development and commercialization of solid-state DC circuit breakers represents the highest-value R&D opportunity in the sector. The addressable market for solid-state DC CBs is estimated at USD 80–120 Million by 2030, growing to over USD 400 Million by 2034. Key investment themes include power semiconductor device development, hybrid mechanical-electronic architectures, and application-specific firmware for renewable energy and EV charging platforms.

Venture and Institutional Investment Trends

- Manufacturing Localization: IRA incentives in the US and PLI incentives in India are attracting USD 2+ Billion in electrical equipment manufacturing investment. Local circuit breaker production reduces logistics costs by 12–18% and improves delivery lead times for the fastest-growing regional markets.

- Digital Twin and Predictive Maintenance: Software overlays that provide circuit breaker health monitoring, remaining useful life prediction, and remote configuration are commanding premium pricing of 15–25% over base hardware.

- Emerging Market Solar Partnerships: JV structures with local manufacturers in India (partnering with Havells, L&T) and Brazil (WEG) provide international OEMs with certified local content credentials required for government-funded renewable tenders.

Future Market Outlook (2026-2034)

The global low voltage DC circuit breaker market is positioned for sustained, broad-based growth through 2034. From a base of USD 1.91 Billion in 2025, the market is projected to reach USD 2.70 Billion by 2034, representing total incremental value creation of approximately USD 790 Million over the forecast decade.

Technology evolution, particularly the commercialization of solid-state circuit breakers, the adoption of 1,500 V DC system architectures, and the integration of digital communication into protection devices, will reshape competitive dynamics. Manufacturers that achieve multi-geography certification, digital product portfolios, and strong positions in solar, BESS, and data center segments by 2027 will capture a disproportionate share of the projected growth.

Long-term, the market's trajectory is tied to three structural macro-themes: the global energy transition (requiring DC protection at every stage of the solar-to-storage-to-consumption chain), the digitalization of power infrastructure (creating demand for intelligent protection devices), and the electrification of transportation (expanding the EV charging and railway traction DC protection installed base).

Research Methodology

Primary Research

Primary research for this report comprised structured interviews and surveys with over 140 industry participants in 2024–2025, including circuit breaker manufacturers, electrical wholesalers, EPC contractors, solar project developers, data center operators, and procurement engineers across Asia-Pacific, Europe, and North America.

Secondary Research

Secondary research encompassed a systematic review of company annual reports, IEC and UL standards documentation, IEA energy statistics, BloombergNEF solar and storage forecasts, patent filings (USPTO, EPO), and industry publications. Over 260 secondary sources were reviewed and triangulated for data consistency.

Forecasting Models

Market size estimations were derived using top-down and bottom-up forecasting approaches, incorporating renewable energy capacity addition projections, data center investment pipelines, EV market forecasts, and historical manufacturer revenue growth rates. The base-case CAGR of 3.81% reflects consensus analyst estimates validated against reported OEM revenue trajectories.

Low Voltage DC Circuit Breaker Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Types Covered | Air Circuit Breaker, Molded Case Circuit Breaker, Others |

| Applications Covered | Battery System, Data Centers, Solar Energy, Transportation, Others |

| End Users Covered | Industrial, Commercial, Others |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | ABB, Siemens, Schneider Electric, Eaton, Legrand SA, Mitsubishi Electric Corporation., etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the low voltage DC circuit breaker market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the global low voltage DC circuit breaker market.

- The study maps the leading as well as the fastest growing regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the low voltage DC circuit breaker industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Low Voltage DC Circuit Breaker Market Report

The global low voltage DC circuit breaker market reached USD 1.91 Billion in 2025 and is projected to reach USD 2.70 Billion by 2034.

The market is expected to grow at a CAGR of 3.81% during 2026-2034, driven by renewable energy expansion, EV infrastructure growth, and data center proliferation.

Asia-Pacific leads the market with a 36.5% revenue share in 2025, driven by China's solar installations, India's renewable energy programme, and South Korea's BESS deployments.

Molded Case Circuit Breakers (MCCBs) dominate with a 46.5% share in 2025. Their cost-effectiveness, compact design, and adjustable trip ratings make them the standard choice for solar, battery, and EV charging applications.

Data centers hold the largest application share at 28.5% in 2025 (approx. USD 0.54 Billion), driven by hyperscale facility construction and the migration to 380 V DC power distribution architectures.

Key players include ABB, Siemens, Schneider Electric, Eaton, Legrand SA, and Mitsubishi Electric Corporation.

Solar Energy is the fastest-growing application at a CAGR of 5.8%, driven by annual global solar capacity additions exceeding 400 GW and the requirement for DC circuit protection at string, combiner, and inverter levels in every installation.

Key investment opportunities include solid-state DC circuit breaker commercialization (projected to exceed USD 400 Million by 2034), manufacturing localization under IRA and PLI incentive programs, and digital twin/predictive maintenance software overlays commanding 15–25% pricing premiums over base hardware.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)