Medical Cannabis Market Size, Share, Trends and Forecast by Species, Derivatives, Application, End-Use, Route of Administration, and Region 2026-2034

Global Medical Cannabis Market Size, Share, Trends & Forecast (2026-2034)

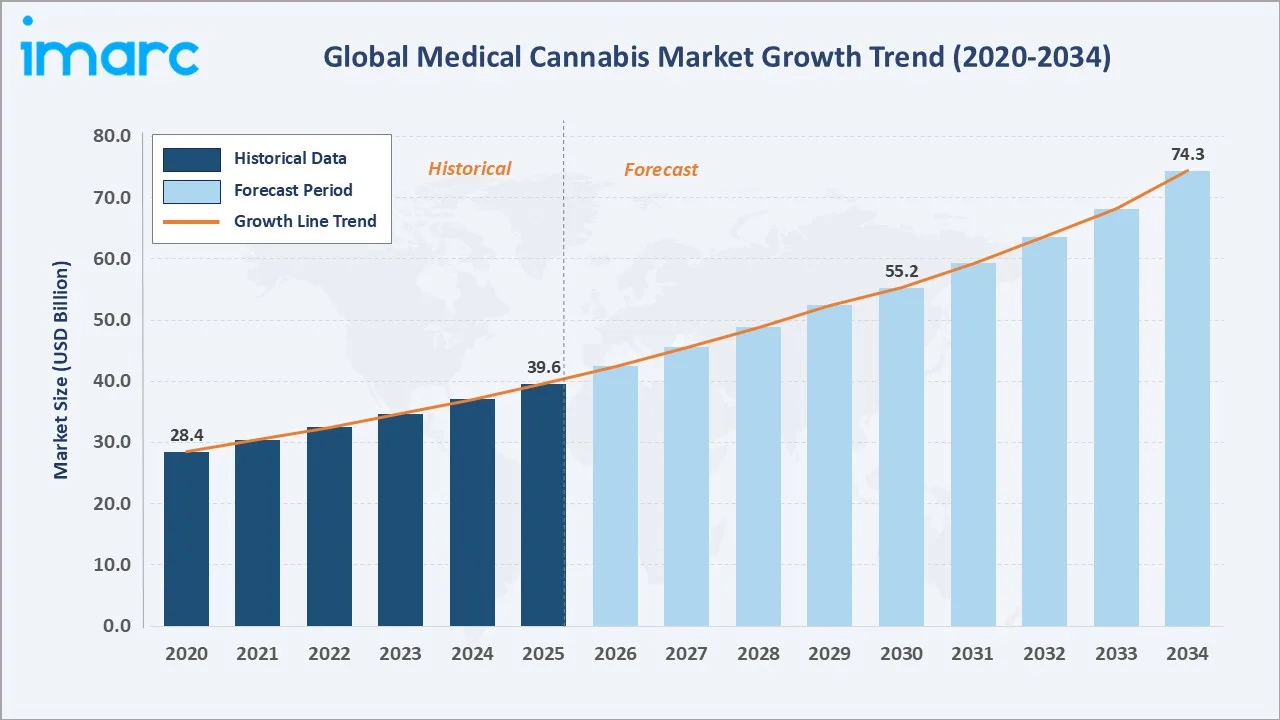

The global medical cannabis market was valued at USD 39.6 Billion in 2025 and is projected to reach USD 74.3 Billion by 2034, expanding at a CAGR of 6.9% during 2026-2034. The market is driven by accelerating global legalization, rising prevalence of chronic diseases, growing acceptance among healthcare providers, and rapid pharmaceutical-grade innovation.

Market Snapshot

|

Metric |

Value |

|

Market Size 2025 |

USD 39.6 Billion |

|

Forecast Market Size 2034 |

USD 74.3 Billion |

|

CAGR 2026-2034 |

6.9% |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

North America (48.6% share, 2025) |

|

Fastest Growing Segment |

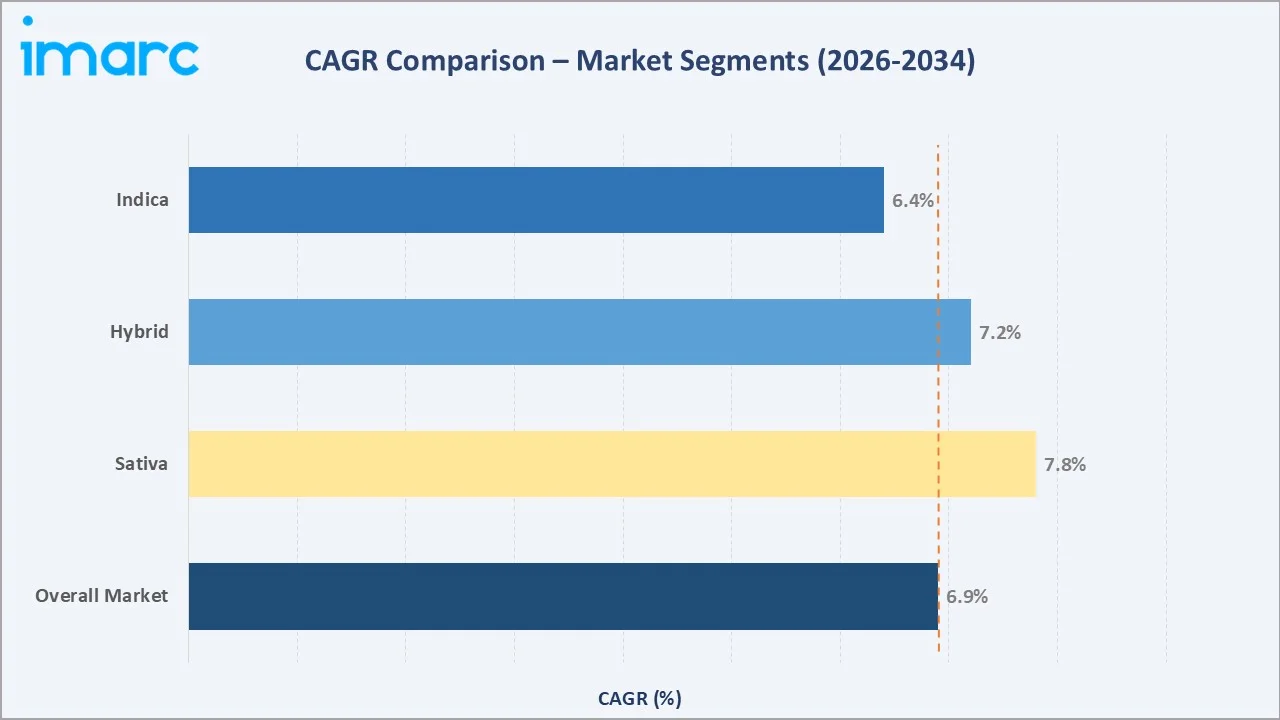

Sativa (est. CAGR ~7.8%, 2026-2034) |

To get more information on this market, Request Sample

As more countries and states legalize cannabis for medicinal use, the market has expanded rapidly, with patients seeking alternative treatments for conditions that may not respond well to traditional pharmaceuticals. The growing body of research supporting the efficacy of cannabis-based treatments, coupled with the development of new delivery methods such as oils, capsules, and topicals, has contributed to this upward trend.

Executive Summary

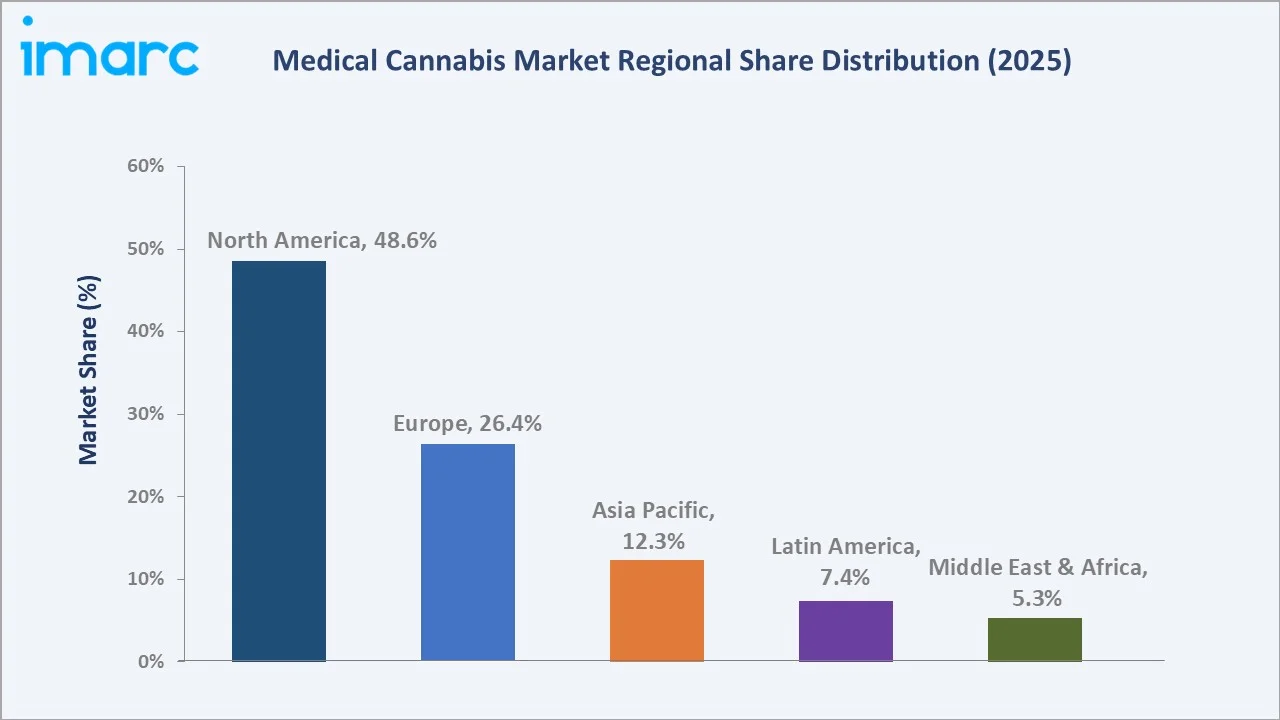

The global medical cannabis market is undergoing a transformative expansion phase, driven by a convergence of regulatory liberalization, clinical evidence maturation, and growing patient acceptance of cannabis-based therapies. Valued at USD 39.6 Billion in 2025, the market is projected to reach USD 74.3 Billion by 2034 at a CAGR of 6.9%. The U.S. and Canada collectively anchor North America's 48.6% regional dominance, while Europe emerges as the fastest-growing major region, supported by Germany's landmark cannabis reform.

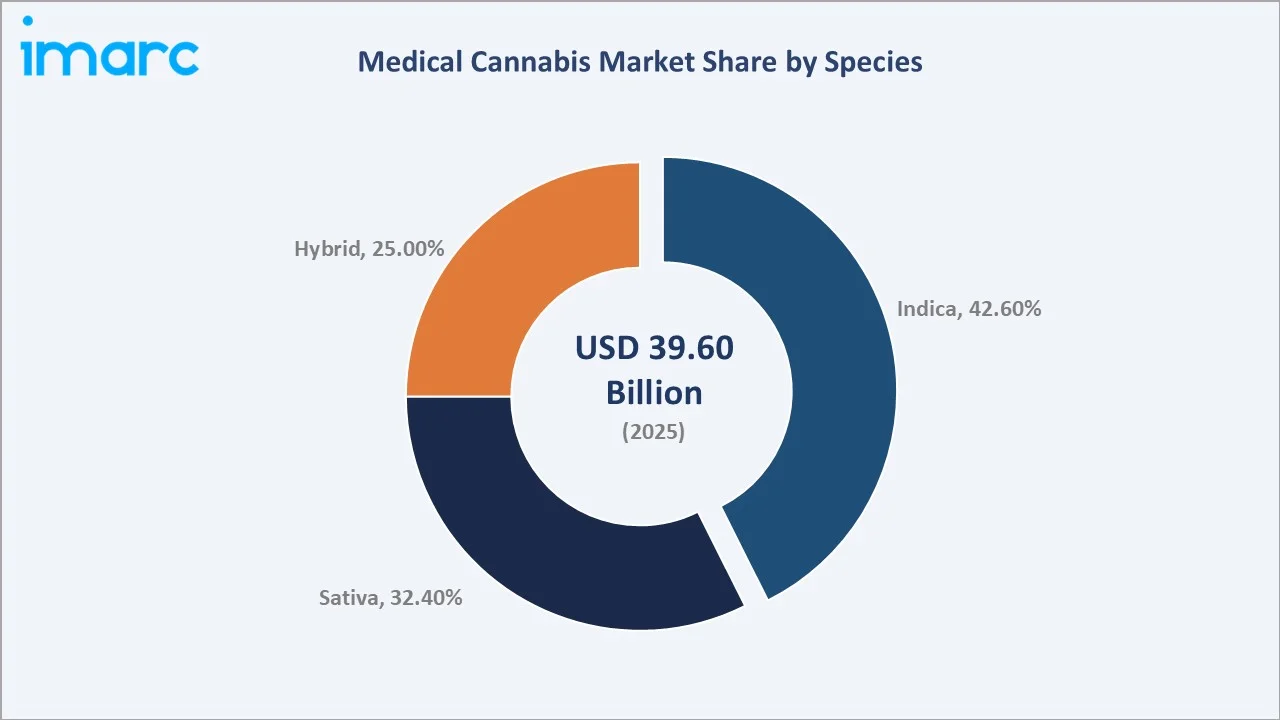

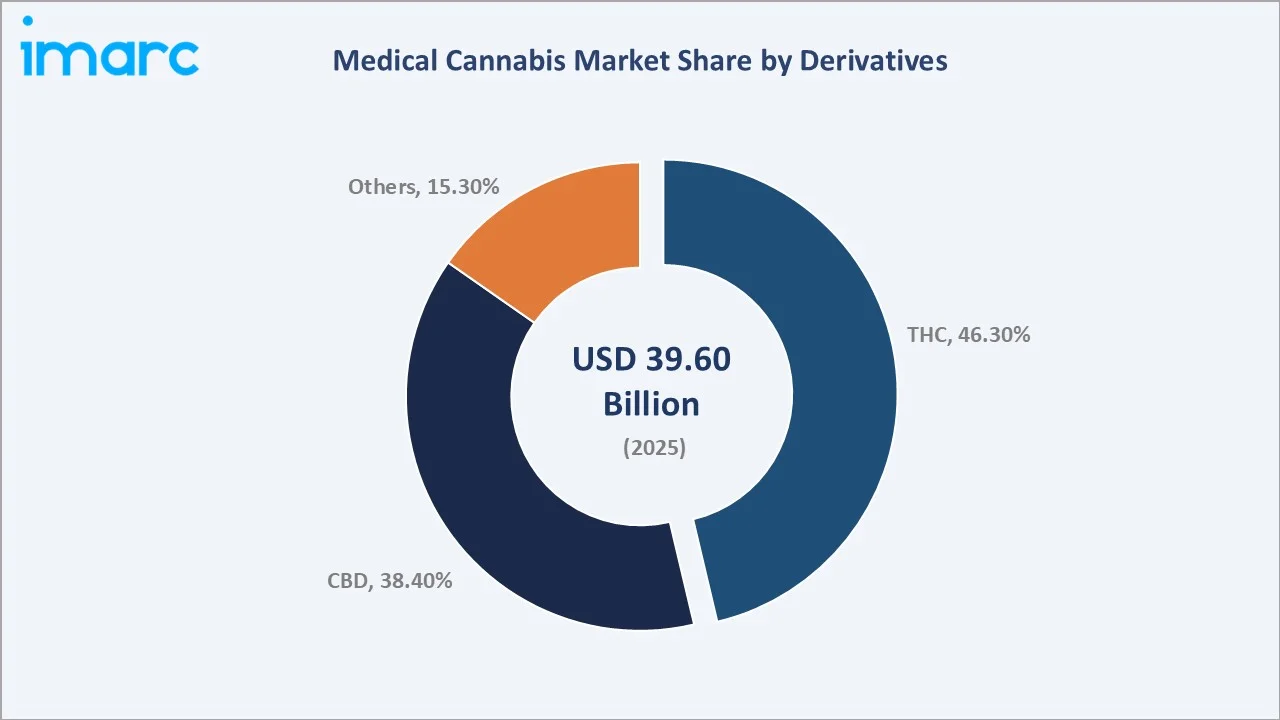

Among species, indica commands a 42.6% share, favored for its high-potency therapeutic properties, particularly in chronic pain, anxiety, and sleep disorders. THC dominates the derivatives segment at 46.3%, driven by established pharmaceutical approvals including GW Pharmaceuticals' Sativex. CBD follows at 38.4%, experiencing rapid growth in epilepsy, anxiety, and inflammatory conditions following FDA approval of Epidiolex.

The competitive landscape is led by Canopy Growth Corporation, Tilray Brands, Aurora Cannabis, and GW Pharmaceuticals (Jazz Pharmaceuticals), which are investing heavily in clinical trials, pharmaceutical formulations, and international expansion. The medical cannabis market outlook through 2034 is characterized by increasing integration into mainstream healthcare and broadening insurance reimbursement frameworks across key markets.

Key Market Insights

|

Insight |

Data |

|

Largest Species |

Indica - 42.6% share (2025) |

|

Dominant Derivative |

THC - 46.3% share (2025) |

|

Fastest Growing Derivative |

CBD - est. CAGR ~7.5% (2026-2034) |

|

Leading Region |

North America - 48.6% revenue share (2025) |

|

Top Companies |

Canopy Growth Corp., Tilray Brands Inc., Aurora Cannabis Inc., GW Pharmaceuticals (Jazz), Cronos Group Inc., and Curaleaf Holdings |

|

Market Opportunity |

Over 70 countries legalized medical cannabis by 2025; Germany market alone accounts for ~38% of European revenue. |

Key Analytical Observations Supporting The Above Data:

- Indica dominates with a 42.6% species share 2025, attributed to its higher cannabinoid potency, shorter flowering cycles, and wider therapeutic applications in pain management, sleep disorders, and anxiety treatment compared to other species.

- THC commands a 46.3% derivatives share 2025, supported by FDA/EMA-approved products including Sativex, and growing clinical evidence for cancer-related pain, multiple sclerosis spasticity, and appetite stimulation in HIV/AIDS patients.

- North America generates 48.6% of global revenues 2025, with the US pharmaceutical-grade cannabis segment alone representing over 62% of the total market in the region, driven by state-level medical programs and DEA research scheduling reforms.

- Europe is the fastest-growing major region, with Germany's medical cannabis market accounting for approximately 38% of European revenues in 2025 following its landmark legalization reforms and expanding pharmacy distribution networks.

- GW Pharmaceuticals' Epidiolex (FDA-approved CBD treatment for epilepsy) and Sativex (approved in 29 countries for MS-related spasticity) represent the most commercially successful pharmaceutical-grade cannabis products globally.

Global Medical Cannabis Market Overview

Medical cannabis refers to the use of Cannabis sativa, Cannabis indica, or Cannabis ruderalis and their derivatives, primarily tetrahydrocannabinol (THC) and cannabidiol (CBD), for therapeutic purposes under medical supervision.

The industry encompasses cultivation, extraction, pharmaceutical manufacturing, distribution, and clinical application across a diverse spectrum of conditions, including chronic pain, epilepsy, multiple sclerosis, cancer-related symptoms, PTSD, and inflammatory disorders. The global ecosystem spans licensed cultivators, pharmaceutical manufacturers, regulatory bodies, healthcare providers, testing laboratories, and patients.

Macroeconomic and demographic drivers, including the global rise in chronic disease burden, an aging population seeking alternatives to opioids, and accelerating healthcare digitization, are structurally expanding the addressable market. Approximately 228 million people aged 15 to 64 have reported using cannabis, raising the prevalence from an estimated 3.5% in 2000 to 4.4% in 2024 (UNODC).

Market Dynamics

To evaluate market opportunities, Request Sample

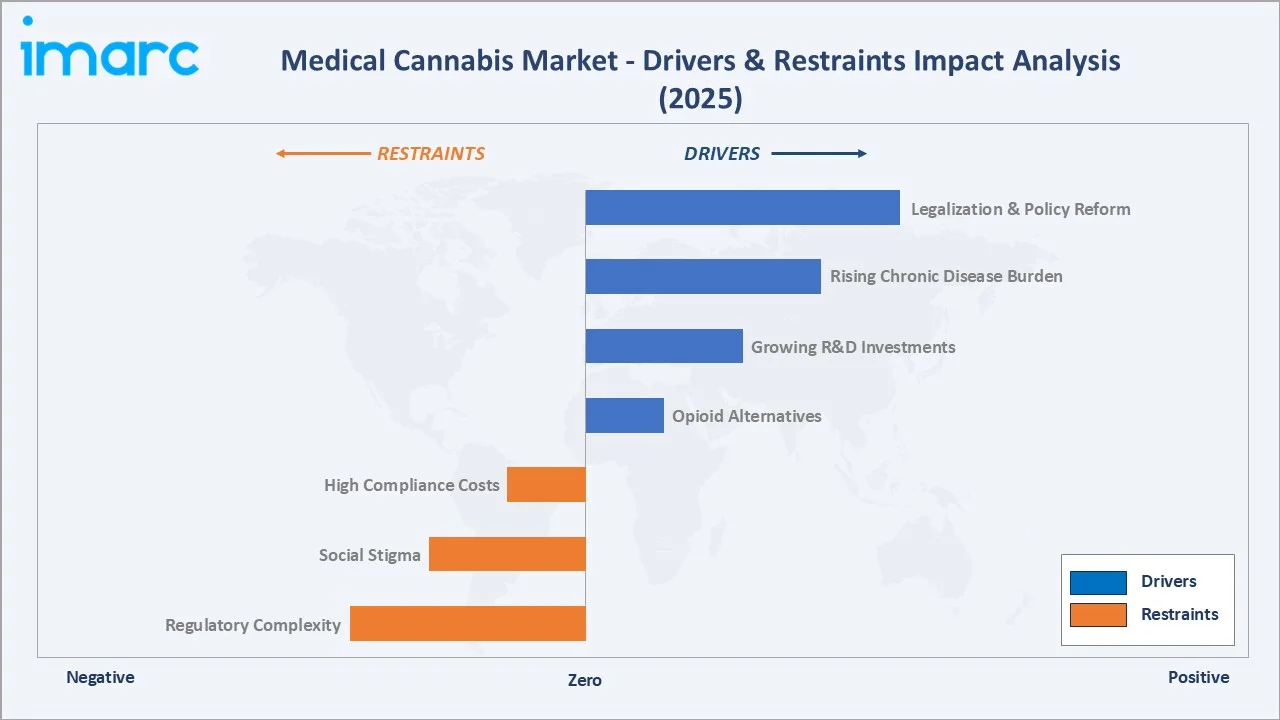

Market Drivers

- Expanding Global Legalization and Policy Reform: Germany's landmark reform, the UK's broadening prescription programs, Australia's therapeutic goods approval pathway, and Thailand's medical cannabis framework represent the vanguard of this regulatory liberalization wave.

- Rising Prevalence of Chronic Pain and Treatable Conditions: Around 1.71 billion people globally are affected by musculoskeletal conditions, while neurological disorders affecting over one billion people represent a major unmet therapeutic need. The opioid crisis, with over 80,000 opioid-related deaths annually in the U.S. alone, has intensified demand for cannabis-based alternatives for chronic pain management.

- Accelerating R&D Investment and Pharmaceutical-Grade Innovation: Aurora Cannabis has launched Daily Special, a new medical cannabis brand in Germany designed to deliver high‑quality, affordable product options to patients in one of its fastest‑growing markets.

- Growing Acceptance Among Healthcare Providers: The proportion of physicians open to prescribing medical cannabis has risen substantially, supported by mounting clinical evidence from FDA and EMA-approved products, peer-reviewed studies, and structured medical education programs.

These drivers collectively reinforce a self-reinforcing cycle. Legalization enables clinical research, which generates physician confidence, which drives prescription volumes, which attracts pharmaceutical investment, anchoring the medical cannabis market outlook through 2034.

Market Restraints

- Regulatory Complexity and Inconsistency: Varying rules on THC limits, cultivation licenses, product formulations, advertising, and cross-border trade create operational complexity and increase time-to-market for new products.

- Persistent Social Stigma: In many markets, including large parts of Asia, the Middle East, and Latin America, social and cultural stigma surrounding cannabis, even for medical use, limits patient willingness to seek prescriptions and physician willingness to prescribe, suppressing demand below the addressable potential.

- High Compliance and Quality Control Costs: Achieving pharmaceutical-grade GMP certification, third-party testing, standardized formulation, and regulatory documentation requires significant capital investment, particularly for smaller operators, limiting market participation and raising product prices for end patients.

Market Opportunities

- Emerging Applications in Mental Health: Growing clinical evidence supporting cannabis-based interventions for PTSD, anxiety disorders, and depression. An estimated 3.9% of the global population has experienced post-traumatic stress disorder (PTSD) at some point in their lives .

- Expansion into Asia Pacific and Emerging Markets: Australia, Thailand, South Korea, and the Philippines are establishing regulated medical cannabis frameworks. Australia's market is growing rapidly, attracting investments from Canopy Growth (7ACRES brand launch, August 2025) and Curaleaf International (May 2025 partnership with Canngea ).

- Biosynthetic Cannabinoids and Precision Medicine: Advances in biosynthetic production of rare cannabinoids, including THCV, CBG, and CBN, via yeast fermentation and synthetic biology are enabling high-purity therapeutic compounds at lower cost, potentially unlocking targeted treatments for conditions currently underserved by plant-derived extracts.

Market Challenges

- Reimbursement Gaps: In most markets, medical cannabis is not reimbursed by public or private health insurance, limiting patient access to those with sufficient disposable income. While Germany has made progress on reimbursement inclusion, the majority of global markets still require out-of-pocket expenditure.

- Banking and Financial Services Restrictions: Particularly in the U.S., cannabis companies continue to face limited access to traditional banking, insurance, and financial services due to federal Schedule I classification, constraining capital deployment and operational efficiency despite state-level legalization.

- Competition from Illicit Market: In markets with high product taxes or limited dispensary access, the illicit market continues to undercut regulated operators on price, creating ongoing challenges for market share capture and public health outcomes in key geographies.

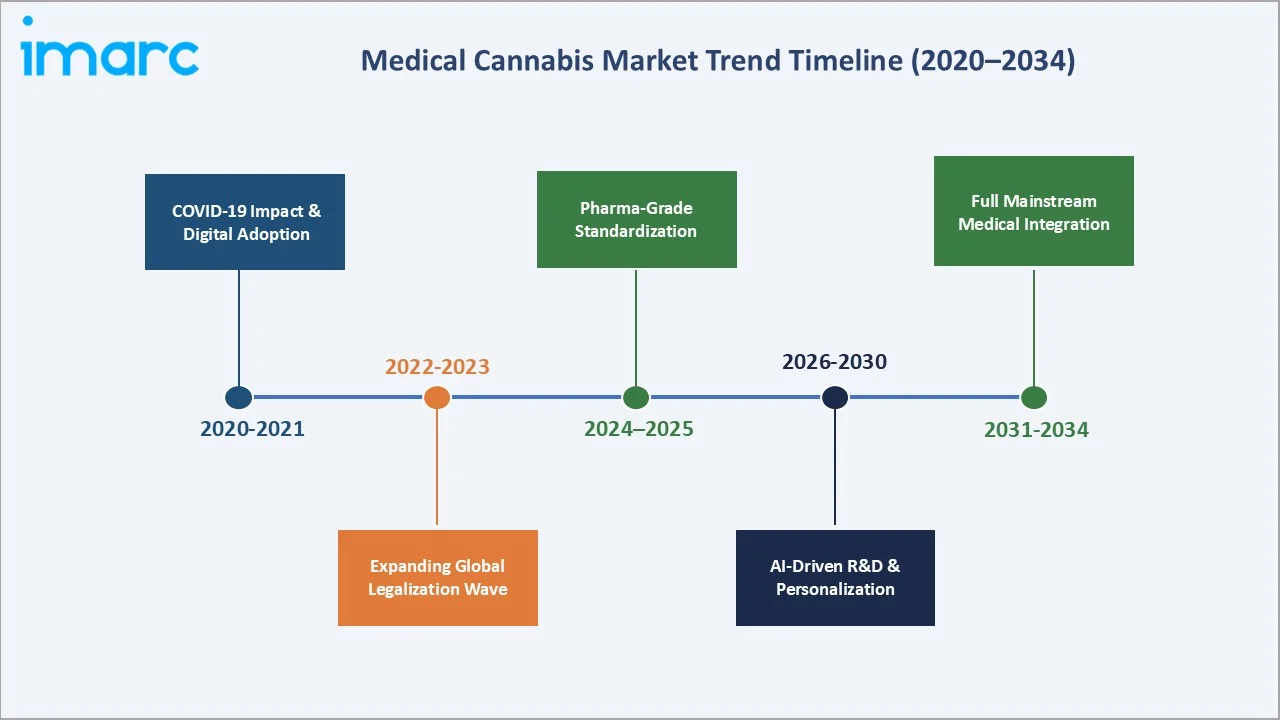

Emerging Market Trends

1. Rapid Advancement of Pharmaceutical-Grade Cannabis Standardization

GW Pharmaceuticals' success with Epidiolex has established a regulatory blueprint that pharmaceutical companies globally are following. In January 2025, Aurora Cannabis launched IndiMed, its first domestic German-grown medical cannabis brand, from its EU-GMP certified facility in Leuna, signaling the acceleration of local pharmaceutical-grade production across key markets.

2. AI-Driven Strain Development and Precision Cultivation

AI-driven strain development enables cultivators to engineer plant chemotypes with precise THC: CBD ratios and specific terpene profiles matched to target clinical indications. These innovations are increasing crop yeilds15-20% compared to traditional cultivation while improving cannabinoid consistency—a critical requirement for pharmaceutical certification and clinical trial use.

3. Expanding Legalization and Global Market Access

In September 2025, Aurora Cannabis is investing in a five‑year upgrade program at its EU‑GMP manufacturing facility in Leuna, Germany, to increase flower growth capacity, improve product quality, and enhance cost efficiency. Thailand became Asia's first country to decriminalize cannabis in 2022, and Australia's therapeutic goods pathway has made it one of the fastest-growing Asia Pacific markets.

4. Growth of CBD-Based Products and Wellness Integration

CBD-based medical cannabis products are experiencing accelerating growth, driven by Epidiolex's FDA approval for epilepsy and patient preferences for non-psychoactive therapeutic options. The CBD derivatives segment is projected to grow at an estimated CAGR of ~7.5% through 2034, as regulatory clarity improves and insurance reimbursement for CBD-based formulations expands in Germany, the UK, and Canada.

5. Digital Health Integration and Telemedicine Prescribing

The digitalization of medical cannabis prescribing is lowering access barriers and expanding the patient funnel, particularly in rural and underserved areas. Product-specific telehealth consultations for prescribing medicinal cannabis have also seen an increase. Blockchain-based supply chain tracking is also gaining traction, ensuring product traceability from seed to sale and supporting regulatory compliance across multi-jurisdictional operations.

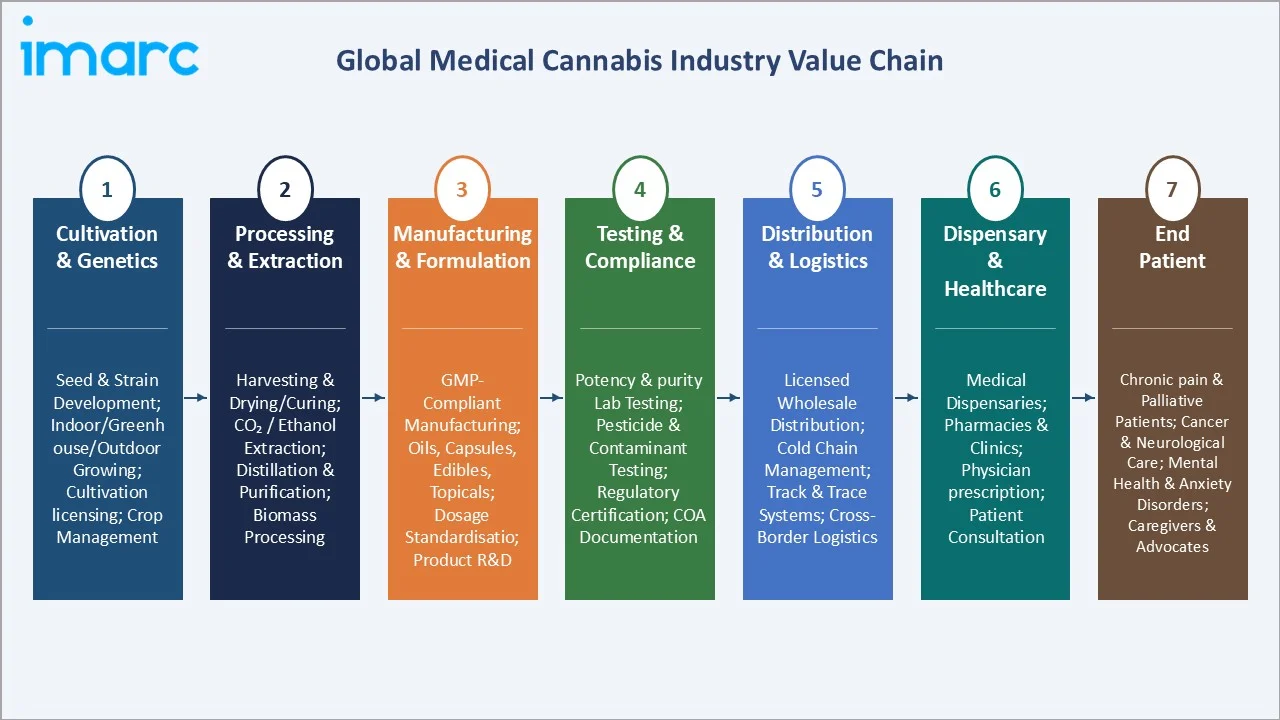

Industry Value Chain Analysis

The medical cannabis value chain spans from seed genetics through patient delivery, encompassing specialized stages that require distinct expertise and regulatory compliance. Each stage is governed by strict licensing requirements and quality standards that collectively ensure product safety and therapeutic consistency.

|

Stage |

Key Players / Examples |

|

Genetics & Seed Supply |

Specialized genetics firms, in-house R&D programs |

|

Licensed Cultivation |

Canopy Growth Corp., Aurora Cannabis Inc., Tilray Brands Inc., local licensed producers |

|

Extraction & Processing |

MediPharm Labs, licensed extraction facilities |

|

Pharmaceutical Manufacturing |

GW Pharmaceuticals (Jazz), Canopy Growth Corp., Tilray Brands Inc., Aurora Cannabis Inc., BOL Pharma |

|

Quality Testing & Standards |

Government laboratories, ISO/GMP-certified labs |

|

Distribution & Dispensing |

Curaleaf Holdings, Trulieve, national pharmacy networks, licensed dispensaries |

|

End Users & Patients |

Chronic pain patients, epilepsy patients, cancer patients, and MS patients |

Technology Landscape in the Medical Cannabis Industry

Precision Cultivation & Controlled Environment Agriculture (CEA)

Aurora Cannabis operates one of Europe's most advanced CEA facilities at its EU-GMP certified site in Leuna, Germany, one of only three licensed cannabis cultivation facilities in Germany as of 2025. Canopy Growth's 7ACRES brand leverages precision indoor cultivation to consistently deliver high-THC sativa strains for medical markets, including Australia, where 7ACRES was launched in August 2025.y.

Advanced Genetics & Strain Development

Proprietary genetics programs represent a critical source of competitive advantage and intellectual property in the medical cannabis sector. Companies are increasingly deploying marker-assisted selection (MAS), genomic sequencing, and CRISPR-based gene editing to develop strains with targeted therapeutic profiles. Cronos Group has engaged Ginkgo Bioworks for fermentation-based biosynthesis of rare cannabinoids, potentially enabling yeast-derived production of CBDV, CBG, and THCV at pharmaceutical scale.

Extraction & Processing Technology

Ethanol extraction is favored for high-volume throughput in broad-spectrum products, while CO2 extraction is preferred for premium, terpene-preserved full-spectrum medical formulations. Winterization, decarboxylation, and chromatographic purification are standard post-extraction steps for pharmaceutical-grade cannabinoid isolation (THC API, CBD API).

Pharmaceutical Drug Delivery Innovation

GW Pharmaceuticals (Jazz) pioneered the application of pharmaceutical drug delivery science to cannabis-derived compounds, developing Sativex as the world's first botanical cannabis medicine with full regulatory approval (2010, UK) and Epidiolex as the world's first FDA-approved cannabis-derived drug.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Species |

Indica |

42.6% |

2025 |

|

Derivatives |

Tetrahydrocannabinol (THC) |

46.3% |

2025 |

|

Application |

Cancer |

🔒 |

2025 |

|

End-Use |

Pharmaceutical Industry |

🔒 |

2025 |

| Route of Administration | Oral Solution and Capsules | 🔒 | 2025 |

|

Region |

North America |

48.6% |

2025 |

By Species

Indica is the dominant species segment with a 42.6% share of the global medical cannabis market in 2025. Cannabis indica is characterized by higher concentrations of CBD and certain terpenes, producing sedating and analgesic effects that are particularly effective for chronic pain management, anxiety disorders, insomnia, and muscle spasms.

To access detailed market analysis, Request Sample

Sativa holds a 32.4% share, favored for its uplifting, cerebral effects and higher THC content, widely prescribed for depression, fatigue, and appetite stimulation in cancer and HIV/AIDS patients. In August 2025, Canopy Growth expanded its Sativa portfolio in Australia with the 7ACRES brand, demonstrating growing clinical interest in THC-rich Sativa formulations.

By Derivatives

THC dominates the derivatives segment with a 46.3% share, reflecting its foundational role in the most established pharmaceutical cannabis products globally. THC-based medications, including Sativex (nabiximols, GW Pharmaceuticals, approved in 29 countries), and Cesamet (nabilone), represent decades of clinical validation and regulatory acceptance.

CBD follows at 38.4%, experiencing robust growth driven by Epidiolex's expansion into new epilepsy indications and growing clinical evidence for anxiety, inflammatory conditions, and neurodegenerative diseases.

Regional Market Insights

North America is the dominant regional market, commanding 48.6% of global medical cannabis revenues in 2025. In the US, over 42 states and the District of Columbia have established medical cannabis programs, and the recreational or adult-use of cannabis has been legalized in the District of Columbia and 24 states.

|

Region |

Share (2025) |

Key Drivers |

Regulatory Impact |

Major Companies |

|

North America |

48.6% |

Opioid crisis, state programs, insurance reform |

FDA approvals, DEA scheduling reform, and state laws |

Canopy Growth Corp., Tilray Brands Inc., Curaleaf Holdings |

|

Europe |

26.4% |

Germany reform, UK prescriptions, EU clinical trials |

EU GMP mandates, national reimbursement schemes |

Tilray Brands Inc. (EU), Aurora Cannabis Inc. |

|

Asia Pacific |

12.3% |

South Korea has limited medical access to Epidiolex, Cesamet, and Sativex |

TGA pathway (AU), national frameworks |

Curaleaf International, Canopy Growth Corp., and local producers |

|

Latin America |

7.4% |

Colombia exports, Brazil domestic market growth |

INVIMA (Colombia), ANVISA (Brazil) |

Khiron Life, Clever Leaves |

|

Middle East & Africa |

5.3% |

Israel R&D leadership, South Africa reform |

IMC-GMP (Israel), emerging national frameworks |

BOL Pharma, InterCure (Israel) |

Asia Pacific represents 12.3% of global revenues and is emerging as a high-growth region as government-backed medical frameworks expand. Australia's therapeutic goods approval pathway is the most developed, attracting major international operators, Curaleaf International (May 2025, via Canngea partnership) and Canopy Growth Corp. (7ACRES launch, August 2025).

Competitive Landscape

|

Company Name |

Brand Name |

Market Position |

Core Strength |

|

Canopy Growth Corp. |

7ACRES, Tweed |

Global Leader |

Premium medical portfolio; Australia 7ACRES launch (Aug 2025); R&D partnerships |

|

Tilray Brands Inc. |

Tilray, Broken Coast |

Global Leader |

Post-Aphria merger scale; North America + Europe; Broken Coast BC Selects (Sep 2025) |

|

Aurora Cannabis Inc. |

Aurora, IndiMed |

Global Leader |

EU-GMP Leuna facility; IndiMed Germany launch (Jan 2025); 5-country operations |

|

GW Pharmaceuticals (Jazz) |

Epidiolex |

Pharma Leader |

Epidiolex (FDA-approved CBD for epilepsy); Sativex (approved in 29 countries for MS) |

|

Cronos Group Inc. |

Spinach |

Challenger |

adult-use cannabis in Canada and internationally; Altria strategic partnership; R&D investment |

|

Curaleaf Holdings |

Curaleaf, Select |

Challenger |

Australia entry (May 2025, Canngea); approximately 147 dispensaries in ~17 states per recent filings; International expansion |

The global medical cannabis market is characterized by moderate consolidation at the top tier, with a mix of large vertically-integrated cannabis corporations and specialized pharmaceutical companies. Canopy Growth Corp., Tilray Brands Inc., Curaleaf Holdings, Aurora Cannabis Inc., GW Pharmaceuticals (Jazz), and Cronos Group Inc., dominate through large-scale cultivation, pharmaceutical-grade manufacturing, and multinational distribution.

In March 2023, Canopy Growth divested its retail operations to concentrate on premium medical cannabis products, while Tilray's merger with Aphria created one of the largest cannabis companies globally by revenue. The report provides a comprehensive analysis of the competitive landscape in the medical cannabis market with detailed profiles of all major companies.

Key Company Profiles

Canopy Growth Corporation

Canopy Growth Corporation, headquartered in Smiths Falls, Ontario, Canada, is one of Canada's most established publicly traded cannabis companies by market capitalization. The company operates across medical and adult-use cannabis segments, with principal operations in Canada, Germany, and Australia.

- Product Portfolio: Premium dried flower (7ACRES, Tweed), Spectrum Therapeutics cannabis oils (Red, Yellow, White, Blue formulations), softgel capsules, oral sprays, vaporizers (Storz & Bickel).

- Recent Developments: Launched 7ACRES brand in Australia (August 5, 2025), adding Ultra Jack and Jack Frost high-THC sativa strains to the Australian medical market.

- Strategic Focus: Building a scalable global medical cannabis platform with international distribution anchored by established brands. Canopy Growth is leveraging its Storz & Bickel vaporizer technology, premium genetics, and Canopy USA ecosystem.

Tilray Brands Inc.

Tilray Brands Inc., headquartered in New York, is a leading global lifestyle and consumer packaged goods company operating at the intersection of cannabis, beverages, wellness, and entertainment.

- Product Portfolio: EU-GMP certified medical cannabis flower, oils, capsules, and oral solutions. Broken Coast premium craft cannabis (indoor, hand-trimmed, slow-cured).

- Recent Developments: Received Italy's first authorization from the Ministry of Health for Tilray Medical flower distribution (June 2025). Won the Luxembourg government tender for medical cannabis flower (2025).

- Strategic Focus: Establishing Tilray Medical as the defining global brand in pharmaceutical-grade medical cannabis, with a unified EU-GMP supply platform across Europe, Canada, and Australia.

Aurora Cannabis Inc.

Aurora Cannabis Inc., headquartered in Edmonton, Alberta, Canada, is a pioneer in global medical cannabis with a strategic focus on high-margin, pharmaceutical-grade international medical markets.

- Product Portfolio: Pharmaceutical-grade dried cannabis flower, oils, and extracts for medical patients. IndiMed is Aurora's Germany-specific, domestically grown brand.

- Recent Developments: Launched IndiMed brand in 0047ermany, the first domestically cultivated German medical cannabis product from the EU-GMP Leuna facility, as one of only three licensed German cultivators.

- Strategic Focus: Cementing leadership in the premium international medical cannabis segment by leveraging its EU-GMP manufacturing network, proprietary genetics library, and deep pharmaceutical channel relationships.

Cronos Group Inc.

Cronos Group Inc., headquartered in Toronto, Ontario, Canada, is an innovative global cannabinoid company focused on adult-use cannabis in Canada and international medical cannabis.

- Product Portfolio: Spinach (Canada's #1 cannabis brand in 2024): dried flower, pre-rolls, vapes, SOURZ gummies, and infused products. Lord Jones: premium live resin fusions, edibles, and flower.

- Recent Developments: Spinach ended 2024 as the cannabis brand in Canada by market share. PEACE NATURALS maintained its position as the medical cannabis brand in Israel with record revenues in H1 2025.

-

Strategic Focus: Leveraging its unparalleled financial strength (USD 800M+ cash, zero debt) to execute a disciplined 'borderless brand' expansion strategy, scaling Spinach, Lord Jones, and PEACE NATURALS across new international markets as cannabis regulation evolves.

Market Concentration Analysis

The global medical cannabis market exhibits moderate concentration, with the top five operators collectively accounting for approximately 35–40% of global revenues in 2025. The market's dual structure, a concentrated pharmaceutical-grade tier led by GW Pharmaceuticals, Aurora, and Canopy Growth, alongside a highly fragmented licensed producer base in domestic markets, reflects the industry's parallel evolution across pharmaceutical and consumer health channels.

The pharmaceutical-grade segment exhibits a higher concentration due to GMP certification barriers and clinical trial requirements. M&A activity is reshaping the competitive structure, with Tilray's Aphria merger and Jazz Pharmaceuticals' GW Pharmaceuticals acquisition being landmark transactions that have strengthened the leading operators' scale and capabilities.

Investment & Growth Opportunities

Fastest Growing Segments

CBD derivatives (est. CAGR ~7.5%), Sativa species (est. CAGR ~7.8%), and minor cannabinoid formulations represent the highest-growth investment vectors through 2034. Neurological disorder applications, particularly treatment-resistant epilepsy and MS, are the fastest-growing therapeutic category, driven by Epidiolex's expanding indications and growing clinical pipeline for rare conditions.

Emerging Market Expansion

Germany, Australia, South Korea, and Colombia represent the most compelling geographic investment opportunities. Germany's reformed market has attracted Aurora, Tilray, and Canopy Growth with multi-hundred-million-dollar production and distribution commitments. Colombia's favorable regulatory and agricultural environment positions it as a global production hub for cost-competitive cultivation and export.

Technology Investment Themes

Biosynthetic cannabinoid production, AI-powered strain development, pharmaceutical-grade delivery system innovation (transdermal, inhalation, nano-emulsification), and digital health prescribing platforms are the four highest-return innovation themes through 2034, offering superior performance versus plant-extract approaches while reducing regulatory compliance complexity.

Future Market Outlook (2026-2034)

The global medical cannabis market is positioned for robust, sustained expansion through 2034, anchored by structural drivers of accelerating legalization, chronic disease prevalence, and pharmaceutical-grade innovation. From a 2025 base of USD 39.6 Billion, the market is forecast to reach USD 74.3 Billion by 2034, representing an absolute incremental value of USD 34.7 Billion over the forecast horizon at a CAGR of 6.9%.

By 2034, the industry is expected to be firmly integrated into mainstream healthcare in North America, Europe, and the Asia Pacific. Biosynthetic cannabinoids, precision-dosed delivery systems, and AI-driven patient matching will progressively transform the market from predominantly plant-derived products toward a sophisticated pharmaceutical category with well-characterized efficacy profiles.

Research Methodology

Primary Research

Primary research included structured interviews with over 200 industry participants in 2024–2025, comprising cannabis company executives, clinical pharmacologists, healthcare providers, regulatory affairs specialists, patients, and investment analysts across North America, Europe, Asia Pacific, Latin America, and the Middle East.

Secondary Research

Secondary research encompassed a comprehensive review of company annual reports, FDA and EMA regulatory filings, peer-reviewed clinical publications, government policy documents, WHO health databases, and publicly available market data. Over 300 secondary sources were reviewed and cross-validated to ensure accuracy.

Forecasting Models

Market size projections were derived using bottom-up and top-down approaches, incorporating patient population data, prescribing rate trends, regulatory approval timelines, price per course of therapy benchmarks, and macroeconomic indicators. Scenario analysis was conducted to account for regulatory timing uncertainty.

Medical Cannabis Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical and Forecast Trends, Industry Catalysts and Challenges, Segment-Wise Historical and Predictive Market Assessment:

|

| Species Covered | Indica, Sativa, Hybrid |

| Derivatives Covered | Cannabidiol (CBD), Tetrahydrocannabinol (THC), Others |

| Applications Covered | Cancer, Arthritis, Migraine, Epilepsy, Others |

| End-Uses Covered | Pharmaceutical Industry, Research and Development Centres, Others |

| Route of Administrations Covered | Oral Solutions and Capsules, Vaporizers, Topicals, Others |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, Netherlands, Italy, Spain |

| Companies Covered | Canopy Growth Corp., Tilray Brands Inc., Aurora Cannabis Inc., GW Pharmaceuticals (Jazz), Cronos Group Inc., Curaleaf Holdings, Inc, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the medical cannabis market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the global medical cannabis market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's five forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the medical cannabis industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Medical Cannabis Market Report

The global medical cannabis market was valued at USD 39.6 Billion in 2025, driven by expanding legalization, rising chronic disease prevalence, and growing pharmaceutical-grade innovation across North America, Europe, and the Asia Pacific.

The market is projected to reach USD 74.3 Billion by 2034, exhibiting a CAGR of 6.9% during 2026-2034, supported by continued policy reform, pharmaceutical integration, and expanding insurance reimbursement.

Key drivers include expanding global legalization (45+ countries by 2025), rising opioid crisis demand for safer pain alternatives, FDA/EMA pharmaceutical approvals, growing chronic disease burden, and increasing physician acceptance of cannabis-based therapies.

North America dominates with a 48.6% share (2025), driven by U.S. and Canadian pharmaceutical-grade production, extensive state-level medical programs, and growing insurance reimbursement for cannabis-based medications.

Indica leads with a 42.6% share in 2025, valued for its higher potency, broader therapeutic applications in chronic pain and sleep disorders, and suitability for pharmaceutical-grade production at scale.

THC holds the largest derivatives share at 46.3% (2025), supported by established pharmaceutical products including Sativex (approved in 29 countries), with growing applications in pain management, MS spasticity, and antiemetic therapy

Key trends include pharmaceutical-grade standardization under GMP, AI-driven strain development, Germany's landmark legalization reform, CBD product expansion following Epidiolex's success, and digital health integration enabling telemedicine prescribing.

Major players include Canopy Growth Corp., Tilray Brands Inc., Curaleaf Holdings, Aurora Cannabis Inc., GW Pharmaceuticals (Jazz), and Cronos Group Inc., among others.

CBD demand is driven by FDA-approved Epidiolex for epilepsy, growing clinical evidence for anxiety and inflammatory conditions, non-psychoactive patient preference, and improving insurance reimbursement in Germany, the UK, and Canada.

High-growth opportunities include CBD pharmaceutical formulations, biosynthetic rare cannabinoid production, European market entry post-German reform, Asia Pacific licensed producer partnerships, and AI-driven precision cultivation technology platforms.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)