Mexico E-Commerce Market Size, Share, Trends and Forecast by Type, Transaction, and Region, 2026-2034

Mexico E-Commerce Market Size, Share, Trends & Forecast (2026-2034)

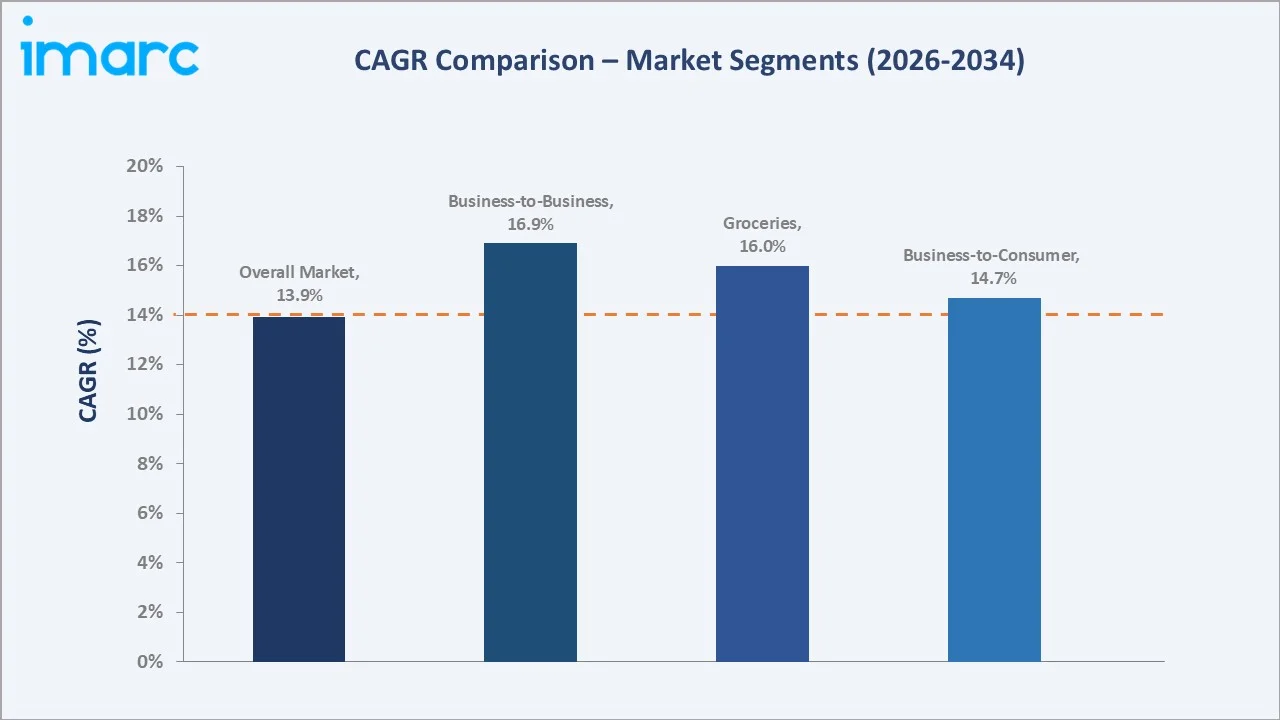

The Mexico e-commerce market reached USD 54.39 Billion in 2025 and is projected to reach USD 175.75 Billion by 2034, growing at a CAGR of 13.92% during 2026-2034. Growth is driven by rising internet and smartphone penetration, expanding digital payment adoption, improved logistics networks, and a growing middle class with higher disposable incomes.

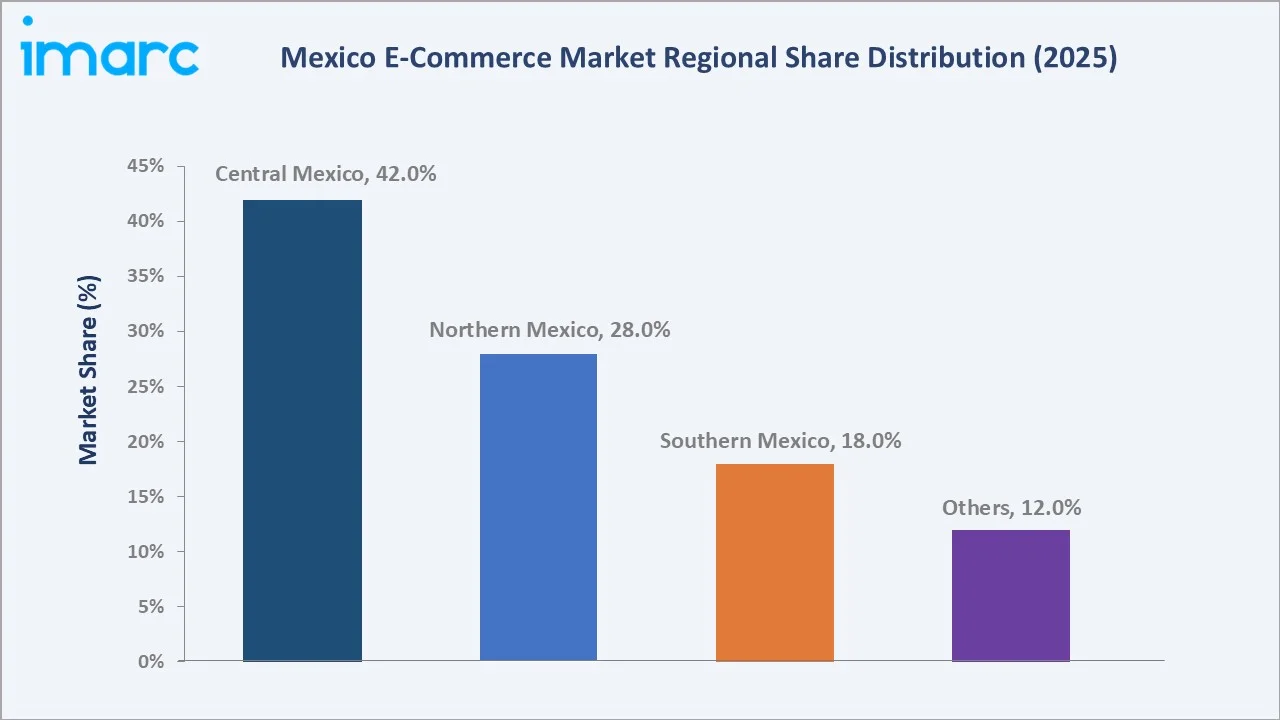

Apparel, Footwear and Accessories leads the type segment at 30.1% in 2025, while Business-to-Consumer dominates the transaction segment at 70.1%. Central Mexico commands the largest regional share at 42.0%, supported by Mexico City's dense urban population and advanced digital infrastructure.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 54.39 Billion |

|

Forecast Market Size (2034) |

USD 175.75 Billion |

|

CAGR (2026-2034) |

13.92% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Dominant Type |

Apparel, Footwear and Accessories (30.1%, 2025) |

|

Dominant Transaction |

Business-to-Consumer (70.1%, 2025) |

|

Leading Region |

Central Mexico (42.0%, 2025) |

The market expanded from USD 28.35 Billion in 2020 to USD 54.39 Billion in 2025, nearly doubling in five years, and is anchored at USD 104.35 Billion in 2030 before reaching USD 175.75 Billion by 2034. Growth has been propelled by accelerating internet penetration, rising consumer trust in digital payments, and continuous investment in logistics infrastructure across major Mexican retailers and marketplaces.

To get more information on this market, Request Sample

Business-to-Business transactions grow fastest at an estimated 16.9% CAGR as enterprise procurement platforms and cross-border digital trade expand. Among product types, Groceries grows at an estimated 16.0% CAGR, supported by quick-commerce adoption, while Apparel, Footwear and Accessories continues to scale on the back of mobile-first fashion retail.

Executive Summary

The Mexico e-commerce market reached USD 54.39 Billion in 2025, reflecting one of Latin America's fastest-growing digital retail economies, underpinned by rising internet penetration, expanding smartphone adoption, and a rapidly maturing digital payments ecosystem. The market is projected to reach USD 175.75 Billion by 2034.

Apparel, Footwear and Accessories leads the type segment at 30.1%, driven by fashion-conscious, mobile-first consumers and extensive product variety offered by marketplaces and Chinese fast-fashion entrants. Business-to-Consumer leads the transaction segment at 70.1% through the dominance of major marketplaces and omnichannel retailers. Central Mexico leads regionally at 42.0%, anchored by Mexico City's dense population, higher disposable incomes, and concentrated digital infrastructure.

Key Market Insights

|

Insight |

Data |

|

Dominant Type |

Apparel, Footwear and Accessories - 30.1% share (2025) |

|

Dominant Transaction |

Business-to-Consumer - 70.1% market share (2025) |

|

Leading Region |

Central Mexico - 42.0% market share (2025) |

|

Market Opportunity |

Rural and semi-urban market expansion; fintech-enabled payment adoption; AI-driven personalization; sustainable product categories; smart warehousing investment |

Key Analytical Observations Supporting the Above Data:

- Apparel, Footwear and Accessories at 30.1%: Apparel, Footwear and Accessories segment dominates as mobile-first consumers favor extensive product variety, easy return policies, and personalized fashion recommendations. Its widespread adoption across marketplaces such as Mercado Libre and Amazon, alongside fast-fashion entrants, further strengthens segment demand.

- Business-to-Consumer at 70.1%: The B2C segment dominates due to the high volume of consumers shopping directly through marketplaces and omnichannel retailers, supported by improving digital payment infrastructure and growing consumer trust. With over 107 million internet users in Mexico, B2C platforms generate substantial transaction volume across product categories.

- Central Mexico at 42.0%: Central Mexico dominates the e-commerce market due to its dense urban population, higher disposable incomes, and concentrated digital infrastructure. Mexico City's status as a major business hub, combined with strong logistics networks, generates substantial demand for online retail across all product types.

Mexico E-Commerce Market Overview

The Mexico e-commerce market encompasses the online sale of goods and services across all consumer and business categories, including apparel, groceries, home appliances, cosmetics, and books, transacted through business-to-consumer, business-to-business, and consumer-to-consumer channels. The market spans marketplace platforms, direct-to-consumer brand websites, and social commerce channels.

The ecosystem integrates online marketplaces, omnichannel retailers, digital payment providers, logistics and last-mile delivery operators, and regulatory bodies overseeing digital trade and taxation. Macroeconomic factors include rising internet and smartphone penetration, expanding middle-class disposable income, nearshoring-driven investment, and government digital transformation initiatives.

Market Dynamics

To evaluate market opportunities, Request Sample

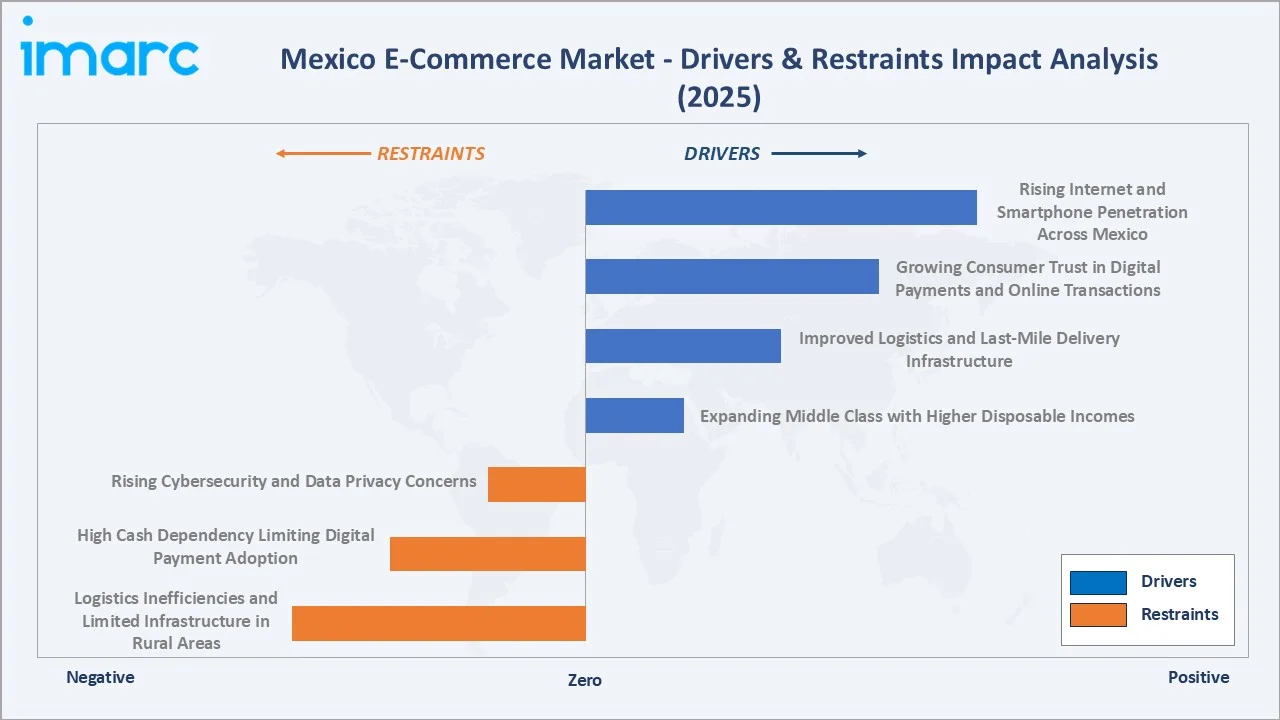

Market Drivers

- Rising Internet and Smartphone Penetration Across Mexico: Rising internet penetration and widespread smartphone adoption facilitate easy access to online shopping platforms. As of early 2024, Mexico had over 107 million internet users, with internet penetration standing at 83.2% and cellular mobile connections covering 97.3% of the population. This expanding digital base is directly fueling consumer engagement with e-commerce platforms across all product categories.

- Growing Consumer Trust in Digital Payments and Online Transactions: Increasing consumer confidence in digital payment systems and online transactions is supporting the expansion of e-commerce across Mexico. Continuous improvements in payment security, fraud prevention technologies, and user-friendly digital payment solutions are encouraging more consumers to shop online. The growing adoption of digital wallets, contactless payments, and flexible payment options is further enhancing transaction convenience and broadening the use of online retail platforms.

- Improved Logistics and Last-Mile Delivery Infrastructure: Ongoing investments in logistics infrastructure, warehousing, and last-mile delivery networks are improving order fulfillment efficiency and delivery reliability across Mexico. The expansion of distribution centers, enhanced transportation connectivity, and the adoption of advanced logistics technologies are enabling faster deliveries, reducing shipping times, and strengthening e-commerce supply chains, thereby improving customer satisfaction and supporting sustained market growth.

- Expanding Middle Class with Higher Disposable Incomes: The expanding middle class with higher disposable incomes is fueling greater spending power and increasing online purchase frequency. As incomes rise, consumers increasingly favor the convenience, variety, and competitive pricing offered by digital retail channels over traditional brick-and-mortar shopping, directly boosting e-commerce transaction volumes across both B2C and B2B channels.

Market Restraints

- Logistics Inefficiencies and Limited Infrastructure in Rural Areas: Logistics inefficiencies, including limited infrastructure in rural areas and high delivery costs, continue to restrict last-mile delivery reliability outside major urban centers. This limits consumer confidence and adoption in Southern Mexico and other less-developed regions, slowing the pace of nationwide e-commerce penetration.

- High Cash Dependency Limiting Digital Payment Adoption: Mexico's historically cash-dependent economy continues to constrain digital payment adoption, with a Bank of Mexico study revealing that 80% of retail transactions are still conducted in cash. This dependency limits the addressable consumer base for online platforms reliant on digital payment infrastructure.

- Rising Cybersecurity and Data Privacy Concerns: Rising cybercrime and data privacy concerns are increasing consumer hesitancy toward online transactions, particularly among older and less tech-savvy demographics. Platforms must continuously invest in fraud detection, secure payment gateways, and consumer education to maintain trust and sustain transaction growth.

Market Opportunities

- Expansion into Underserved Rural and Semi-Urban Markets: Expanding internet and smartphone penetration in semi-urban and rural areas presents a significant untapped consumer base. Platforms that invest early in localized logistics and payment solutions can capture first-mover advantages in these underserved markets.

- Increased Fintech Collaboration to Enhance Digital Payment Adoption: Deeper collaboration between e-commerce platforms and fintech providers can accelerate digital payment adoption among Mexico's large unbanked population, as innovations in real-time payments and digital wallets continue lowering barriers to online transactions.

Market Challenges

- Intense Price Competition Among Major Platforms: Intensifying competition from Chinese cross-border platforms is exerting sustained downward pricing pressure across fashion, electronics, and specialty categories, compressing margins for marketplace leaders and domestic retailers alike.

- Evolving Tariff and Customs Regulatory Environment: Newly implemented tariff and customs regulations targeting low-cost cross-border imports are reshaping cost structures for international platforms, requiring rapid adaptation of pricing and supply chain strategies.

Emerging Market Trends

1. Mobile-First Commerce and Social Shopping Integration

Mobile commerce continues to dominate consumer behavior, with smartphones powering most online purchases in Mexico. Social commerce integration through platforms is expanding rapidly, allowing sellers to reach younger, mobile-native consumers through direct social discovery and checkout.

2. Fintech-Driven Digital Payment Expansion

Expansion of real-time payment systems and digital wallets is steadily reducing Mexico's reliance on cash. Continued fintech innovation, including buy now, pay later services and instant bank transfers, is broadening the base of consumers able to transact securely online.

3. Cross-Border Platform Expansion and Regulatory Response

Chinese cross-border platforms have rapidly gained share across fashion and specialty categories, prompting new tariff and customs regulations aimed at leveling competitive conditions. This regulatory shift is reshaping sourcing and pricing strategies across the landscape.

4. AI-Driven Personalization and Logistics Optimization

Artificial intelligence is increasingly applied across recommendation engines, customer service chatbots, and demand forecasting. These technologies improve conversion rates while enabling more efficient inventory management and delivery routing across major platforms.

Industry Value Chain Analysis

The Mexico e-commerce value chain integrates sourcing and procurement, platform and marketplace operations, payment processing, order fulfillment and warehousing, logistics and last-mile delivery, and after-sales customer service. Leading platforms are increasingly vertically integrating fulfillment and logistics capabilities to improve delivery speed and customer experience.

|

Stage |

Key Participants |

|

Sourcing & Procurement |

Brand owners, domestic and international manufacturers, importers, and wholesale suppliers providing inventory to online sellers |

|

Platform & Marketplace Operations |

Online marketplaces, direct-to-consumer brand websites, and social commerce platforms enabling product discovery and transactions |

|

Payment Processing |

Digital payment providers, banks, mobile wallets, and buy now, pay later services facilitating secure online transactions |

|

Order Fulfillment & Warehousing |

Distribution centers, fulfillment service providers, and inventory management systems supporting order processing |

|

Logistics & Last-Mile Delivery |

Courier services, last-mile delivery operators, and transportation networks ensuring timely order delivery to consumers |

|

After-Sales & Customer Service |

Returns processing, customer support, and dispute resolution services maintaining consumer trust and satisfaction |

The logistics and last-mile delivery stage is the value chain's most infrastructure-sensitive segment, given Mexico's varied terrain and uneven regional connectivity. Payment processing is experiencing the most rapid transformation as fintech innovation progressively displaces cash-based transactions.

Technology Landscape in the Mexico E-Commerce Industry

Mobile Commerce Technology

Mobile commerce technology, including responsive platform design and native shopping apps, enables seamless purchasing across smartphones, which power most online transactions in Mexico. Continuous investment in checkout optimization supports rising conversion rates across major platforms.

Digital Payment Technology

Digital payment technology, spanning real-time payment rails, digital wallets, and buy now, pay later integration, is expanding the base of consumers able to transact securely online, addressing Mexico's historically cash-dependent economy with accessible payment alternatives.

AI-Driven Personalization and Logistics Technology

Artificial intelligence is increasingly embedded across recommendation engines, fraud detection systems, and delivery route optimization tools, improving both consumer experience and operational efficiency across leading e-commerce platforms.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Type |

Apparel, Footwear and Accessories |

30.1% |

2025 |

|

Transaction |

Business-to-Consumer |

70.1% |

2025 |

|

Region |

Central Mexico |

42.0% |

2025 |

By Type

Apparel, Footwear and Accessories leads the type segment at 30.1% in 2025, driven by fashion trends, extensive product variety, easy return policies, and personalized recommendations offered by marketplaces and fast-fashion platforms.

To access detailed market analysis, Request Sample

Groceries follows at 25.2%, propelled by the convenience of home delivery and the growing availability of fresh produce and household essentials through quick-commerce platforms. Home Appliances captures 18.3%, supported by competitive pricing and detailed product information, while Cosmetics at 12.4% benefits from diverse brand availability and online tutorials. Books at 8.5% and Others at 5.5% complete the segment, with Others including categories such as electronics accessories and specialty goods.

By Transaction

Business-to-Consumer leads the transaction segment at 70.1% in 2025, driven by consumer convenience, wide product selection, and personalized shopping experiences offered by major marketplaces such as Mercado Libre, Amazon, and Walmart de México.

Business-to-Business transactions account for 18.3%, fueled by streamlined procurement processes and improved supply chain transparency for enterprises. Consumer-to-Consumer transactions represent 8.4%, supported by the growth of peer-to-peer marketplaces, while Others at 3.2% includes emerging transaction formats such as government-to-consumer digital services.

Regional Market Insights

|

Region |

Share (2025) |

Key Mexico E-Commerce Market Drivers & Characteristics |

|

Central Mexico |

42.0% |

Driven by dense urban population, higher disposable incomes, concentrated digital infrastructure, and strong consumer demand for online retail |

|

Northern Mexico |

28.0% |

Supported by robust logistics networks, industrial economic activity, and a higher concentration of digitally engaged consumers |

|

Southern Mexico |

18.0% |

Driven by improving digital connectivity, expanding logistics infrastructure, and growing awareness of online shopping benefits |

|

Others |

12.0% |

Reflects emerging e-commerce activity across smaller metropolitan areas and rural regions benefiting from expanding logistics and payment infrastructure |

Central Mexico, at 42.0%, leads through its dense population, advanced digital infrastructure, and concentration of major retail and logistics hubs. Northern Mexico, at 28.0%, benefits from strong logistics connectivity and industrial income levels.

Southern Mexico, at 18.0%, represents a growing but still-developing market as digital connectivity and logistics infrastructure continue to expand into less-developed areas. The Others category, at 12.0%, captures emerging e-commerce activity across smaller cities and rural regions nationwide.

Competitive Landscape

The Mexico e-commerce market competitive landscape is highly competitive and moderately concentrated, dominated by global marketplace leaders, omnichannel retail chains, and fast-growing Chinese cross-border platforms competing for consumer wallet share.

|

Company Name |

Key Products |

Market Position |

Core Strength |

|

MercadoLibre, Inc. |

Online Marketplace, MercadoPago, Logistics Network |

Market Leader |

Mercado Libre is Latin America's leading e-commerce marketplace, anchoring customer loyalty through its integrated MercadoPago fintech ecosystem and extensive logistics footprint. |

|

Amazon |

Online Marketplace, Prime, AWS-backed Logistics |

Market Leader |

Amazon leverages its global marketplace scale, Prime membership benefits, and continuous logistics investment to maintain a leading position in Mexican online retail. |

|

Walmart |

Online Marketplace, Omnichannel Retail |

Strong Challenger |

Walmart combines its extensive supermarket footprint with a rapidly expanding online marketplace and seller network, driving strong digital revenue growth. |

|

Costco Wholesale Corporation |

Membership-Based Online and Warehouse Retail |

Niche Player |

Costco combines its membership warehouse model with a growing online retail presence, focused on bulk value purchasing for households and businesses. |

Key players include MercadoLibre, Inc., Amazon, Walmart, Costco Wholesale Corporation, and others.

Key Company Profiles

MercadoLibre, Inc.

MercadoLibre, Inc. is Latin America's leading e-commerce marketplace, with a strong presence in Mexico through its integrated marketplace, MercadoPago fintech platform, and proprietary logistics network.

- Key Products: Online Marketplace, MercadoPago Digital Payments, Mercado Envios Logistics.

- Recent Developments: In June 2026, Mercado Libre unveiled a USD 4.6 billion investment plan for Mexico aimed at expanding logistics infrastructure, technology capabilities, and fintech operations. The initiative is expected to support the country's digital transformation by driving greater adoption of online business processes and secure digital transaction solutions.

- Strategic Focus: Expanding logistics infrastructure and fintech integration through MercadoPago to anchor customer loyalty and strengthen its leadership position across Mexico's marketplace ecosystem.

Amazon

Amazon is a global e-commerce and technology company with a strong presence in the Mexico market through its online marketplace, Prime membership program, and expanding logistics network.

- Key Products: Online Marketplace, Amazon Prime, Amazon Business, AWS-backed Infrastructure.

- Strategic Focus: Strengthening logistics investment and Prime membership benefits while expanding its Business marketplace to capture growing B2B e-commerce demand across Mexico.

Market Concentration Analysis

The Mexico e-commerce market is moderately concentrated at the marketplace level, with the top 2 players together accounting for over 85% of vendor coverage and approximately 61% of shopper penetration, a concentration level that has drawn regulatory scrutiny.

Omnichannel retailers are investing significantly in digital and logistics infrastructure to expand their competitive position. Chinese cross-border platforms have collectively captured an estimated 40% share of online shoppers in select specialty categories, intensifying competitive pressure on both marketplace leaders and traditional retailers. Market concentration is expected to moderate over the forecast period as new tariff and customs regulations reshape competitive dynamics among cross-border and domestic players.

Investment & Growth Opportunities

Highest Growth Segments

Business-to-Business transactions (~16.9% CAGR), Groceries (~16.0% CAGR), Apparel, Footwear and Accessories (~15.2% CAGR), and Business-to-Consumer transactions (~14.7% CAGR) represent the highest-growth investment vectors through 2034, supported by enterprise procurement digitization and mobile-first retail expansion.

Emerging Investment Opportunities

Rural and semi-urban market expansion represents the highest-potential emerging opportunity, as improving connectivity and logistics infrastructure progressively unlock consumer segments currently underserved by major platforms, creating a structurally growing demand pool through 2034.

Investment Themes

- Fintech Collaboration for Digital Payment Infrastructure Expansion: Continued fintech partnership investment to expand digital wallet adoption and real-time payment integration represents a structural opportunity to convert Mexico's cash-dependent consumer base into active digital shoppers, expanding the addressable market across categories.

- Logistics and Fulfillment Infrastructure Investment in Underserved Regions: Investment in smart warehousing and last-mile delivery optimization in rural and semi-urban regions can capture the market's fastest-growing unserved consumer segments, a strategy already being pursued by leading marketplaces through distribution network expansion.

Future Market Outlook (2026-2034)

The Mexico e-commerce market is projected to grow from USD 54.39 Billion in 2025 to USD 175.75 Billion by 2034, delivering a 13.92% CAGR over the forecast period. The market's anchor value of USD 104.35 Billion in 2030 represents a critical mid-point in the country's digital retail transformation, as mobile commerce, fintech-enabled payments, and logistics modernization continue to mature in tandem.

Three structural forces define market growth through 2034. Continued internet and smartphone penetration growth will expand the addressable consumer base, particularly across Southern Mexico and rural regions currently underserved by digital infrastructure. The maturation of digital payment systems, including real-time payment platforms and growing fintech adoption, will progressively reduce Mexico's historical cash dependency. Finally, intensifying competition between established marketplaces, omnichannel retailers, and Chinese cross-border platforms will continue to expand product variety, improve pricing competitiveness, and accelerate last-mile delivery innovation nationwide.

Research Methodology

Primary Research

Primary research comprised structured interviews with industry stakeholders across Mexico's e-commerce ecosystem, including marketplace operations leads, omnichannel retail digital strategy executives, fintech payment specialists, and logistics and last-mile delivery programme leads.

Secondary Research

Secondary research encompassed company annual reports, Datareportal digital trend statistics, Bank of Mexico retail payment studies, INEGI national statistics on internet and smartphone penetration, industry association publications, and trade and customs regulatory filings. Over 50 secondary sources were reviewed.

Forecasting Models

Market revenue forecasts were developed using a consumption-based bottom-up model incorporating: (i) internet and smartphone penetration growth projections by region; (ii) average online spend per digital consumer by product type and transaction category; (iii) digital payment infrastructure maturation rates; and (iv) competitive share shift adjustments accounting for cross-border platform entry and tariff policy changes.

Mexico E-Commerce Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Types Covered | Home Appliances, Apparel, Footwear and Accessories, Books, Cosmetics, Groceries, Others |

| Transactions Covered | Business-to-Consumer, Business-to-Business, Consumer-to-Consumer, Others |

| Regions Covered | Northern Mexico, Central Mexico, Southern Mexico, Others |

| Companies Covered | MercadoLibre, Inc., Amazon, Walmart, Costco Wholesale Corporation, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the Mexico e-commerce market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the Mexico e-commerce market.

- Porter's five forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the Mexico e-commerce industry and its attractiveness.

- The competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Mexico E-Commerce Market Report

The Mexico e-commerce market reached USD 54.39 Billion in 2025, driven by the Apparel, Footwear and Accessories segment leading at 30.1%, Business-to-Consumer transactions dominant at 70.1%, and Central Mexico commanding 42.0% of regional market share through Mexico City's dense population and advanced digital infrastructure.

The market grows at a 13.92% CAGR during 2026-2034, reaching USD 175.75 Billion by 2034. This growth reflects rising internet and smartphone penetration, expanding digital payment adoption, improving logistics infrastructure, and a growing middle class with higher disposable incomes.

Apparel, Footwear and Accessories leads at 30.1%, driven by fashion-conscious, mobile-first consumers and extensive product variety offered by marketplaces and fast-fashion entrants.

Business-to-Consumer leads at 70.1% through the dominance of major marketplaces and omnichannel retailers, while Business-to-Business follows at 18.3% as enterprise procurement digitization accelerates.

Central Mexico leads at 42.0% through Mexico City's dense urban population, higher disposable incomes, and concentrated digital and logistics infrastructure.

Leading companies include MercadoLibre, Inc., Amazon, Walmart, Costco Wholesale Corporation, and others.

The market is projected to reach approximately USD 104.35 Billion by 2030, with continued fintech-enabled payment adoption, logistics modernization, and rural and semi-urban market expansion shaping market structure.

Priority opportunities include expansion into underserved rural and semi-urban markets, increased fintech collaboration to enhance digital payment adoption, and investment in smart warehousing and AI-driven personalization solutions.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)