Mexico Fashion and Apparel Market Size, Share, Trends, and Forecast by Type, Distribution Channel, End User, and Region, 2026-2034

Mexico Fashion and Apparel Market Size, Share, Trends & Forecast (2026-2034)

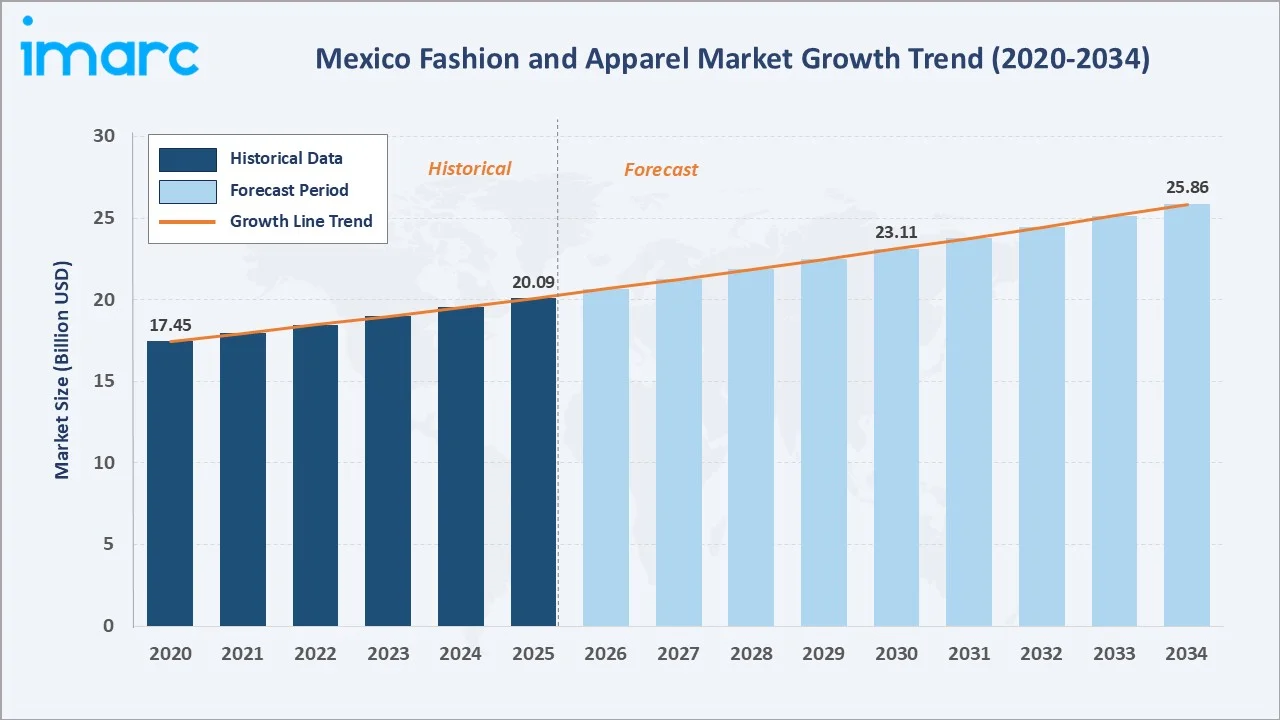

The Mexico fashion and apparel market reached USD 20.09 Billion in 2025 and is projected to reach USD 25.86 Billion by 2034, growing at a CAGR of 2.85% during 2026-2034. The market is driven by rising disposable incomes, growing social media influence, and expanding retail channels.

Casual wear leads at 42.6% in 2025. Offline distribution dominates at 68.1%, while online retail accelerates rapidly. Central Mexico commands 43.4% of the national market.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 20.09 Billion |

|

Forecast Market Size (2034) |

USD 25.86 Billion |

|

CAGR (2026-2034) |

2.85% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Dominant Type |

Casual Wear (42.6%, 2025) |

|

Dominant Distribution Channel |

Offline (68.1%, 2025) |

|

Leading Region |

Central Mexico (43.4%, 2025) |

The market expanded from USD 17.45 Billion in 2020 to USD 20.09 Billion in 2025, reflecting steady demand through post-pandemic recovery and rising consumer confidence. It is forecast to reach USD 23.11 Billion by 2030 and USD 25.86 Billion by 2034, driven by e-commerce adoption and brand diversification.

To get more information on this market, Request Sample

Casual wear accounts for 42.6% of market revenue in 2025, driven by lifestyle shifts and remote-work adoption. Sports wear at 22.4% is the fastest-growing sub-segment, powered by rising fitness awareness and athleisure trends among younger demographics in urban Mexico.

Executive Summary

The Mexico fashion and apparel market reached USD 20.09 Billion in 2025, underpinned by Mexico's expanding middle class and urban population. The market is forecast to reach USD 25.86 Billion by 2034, growing at a CAGR of 2.85%.

Casual wear at 42.6% and sports wear at 22.4% together account for nearly two-thirds of market revenue. Formal wear at 18.3%, safety wear at 9.7%, and others at 7.0% complete the type segmentation landscape.

Central Mexico leads regional markets at 43.4%, followed by Northern Mexico at 29.8% and Southern Mexico at 19.1%. Offline channels dominate at 68.1%, while online channels at 31.9% are growing at a faster pace.

Key Market Insights

|

Insight |

Data |

|

Dominant Type |

Casual Wear – 42.6% share (2025) |

|

Dominant Distribution Channel |

Offline – 68.1% market share (2025) |

|

Leading Region |

Central Mexico – 43.4% market share (2025) |

|

Market Opportunity |

E-commerce growth, sustainable fashion, artisanal textile integration |

Key Analytical Observations Supporting The Above Data:

- Casual Wear at 42.6%: Casual wear dominates as Mexican consumers increasingly prioritize comfortable, versatile clothing for both home and social settings, supported by growing global fashion influence through social media.

- Offline Channels at 68.1%: Physical retail remains dominant as Mexican consumers prefer in-store experiences, fit-testing, and immediate purchase gratification across department stores and specialty chains.

- Central Mexico at 43.4%: Central Mexico leads due to Mexico City's status as the country's primary fashion hub, highest population density, and concentration of flagship brand stores.

Mexico Fashion and Apparel Market Overview

The Mexico fashion and apparel market encompasses the design, manufacture, and retail of all garment categories for men, women, and children, spanning casual wear, formal wear, sports wear, safety wear, and other apparel types.

The ecosystem integrates domestic textile manufacturers, international brand licensees, retail chains, department stores, fast fashion importers, e-commerce platforms, and independent boutiques. Macroeconomic factors include consumer spending, peso exchange rate dynamics, trade agreements, and demographic trends.

Market Dynamics

To evaluate market opportunities, Request Sample

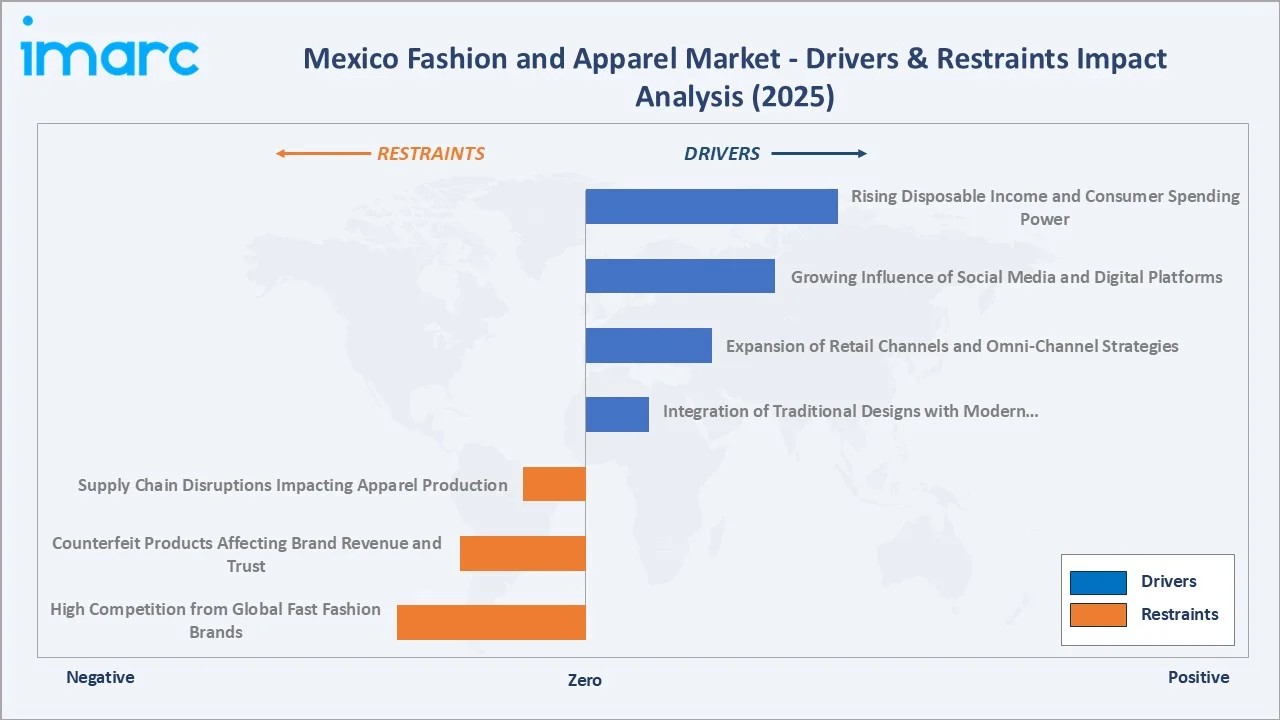

Market Drivers

- Rising Disposable Income and Consumer Spending Power: Mexico's expanding middle class and increasing per-capita income are enabling consumers to allocate greater spending to fashion, including international brands and premium segments. The growing purchasing power is translating directly into higher average transaction values across casual, sports, and formal wear categories.

- Growing Influence of Social Media and Digital Platforms: With over 90 million social media users, Mexican consumers are increasingly influenced by global trends via Instagram, TikTok, and YouTube, accelerating demand for trend-responsive apparel. Fashion influencers and brand collaborations on social platforms are shortening the trend adoption cycle, compelling retailers to refresh collections more frequently. The rapid rise of social commerce features enabling in-app purchases is further blurring the boundary between content consumption and fashion purchasing, creating new direct-to-consumer revenue streams for both established and emerging brands.

- Expansion of Retail Channels and Omni-Channel Strategies: Both domestic and international retailers are expanding physical and digital footprints simultaneously, improving product accessibility across income segments. Online fashion purchases in Mexico occur approximately 6.1 times per year per buyer. Major retailers are investing in click-and-collect infrastructure, same-day delivery logistics, and AI-driven personalisation to elevate the omni-channel shopping experience. The integration of loyalty programmes across online and offline touchpoints is improving customer retention rates and driving higher lifetime value, giving established players with diversified channel presence a significant competitive edge over pure-play operators.

- Integration of Traditional Designs with Modern Styles: Mexican fashion brands and artisans are gaining recognition for blending indigenous textile traditions with contemporary design, attracting domestic consumers and international buyers seeking culturally distinctive fashion. This fusion of heritage craftsmanship with modern aesthetics is enabling premium pricing and differentiation from mass-market fast fashion competitors.

Market Restraints

- High Competition from Global Fast Fashion Brands: The dominance of international fast fashion brands exerts sustained pricing pressure on domestic manufacturers, limiting local brand growth and margin expansion across mid-market segments. Global fast fashion players leverage massive economies of scale, ultra-rapid product development cycles, and highly optimised global supply chains that domestic Mexican brands cannot easily replicate. This competitive imbalance is forcing local apparel companies to either differentiate aggressively through quality, cultural positioning, or sustainability credentials, or to compete primarily on price in lower-margin segments where informal market operators also present significant pressure.

- Counterfeit Products Affecting Brand Revenue and Trust: Widespread circulation of counterfeit and pirated apparel through informal markets reduces brand revenues, undermines consumer trust, and creates significant losses across premium and mid-market apparel categories. The proliferation of counterfeit luxury and mid-market fashion goods through street markets, informal online channels, and social commerce platforms weakens brand equity and makes it harder for authentic brands to justify premium pricing to price-sensitive consumer segments.

- Supply Chain Disruptions Impacting Apparel Production: Global and domestic supply chain vulnerabilities, including raw material cost volatility, logistics delays, and energy cost fluctuations, periodically disrupt apparel manufacturing timelines and increase operating costs. Mexico's apparel industry relies on both domestic cotton and synthetic fibre production and significant imports of fabrics, trims, and components, making it susceptible to global commodity price cycles and shipping disruptions. These supply chain vulnerabilities increase inventory planning complexity, create lead time unpredictability, and compress margins for manufacturers and brands that lack the scale or financial reserves to absorb cost shocks and maintain consistent product availability through disruption periods.

Market Opportunities

- E-Commerce and Digital Retail Expansion: Online fashion sales in Mexico are growing rapidly. Investments in digital logistics and payment infrastructure will further accelerate the online channel, which already represents 31.9% of total distribution. The continued expansion of digital payment solutions, including buy-now-pay-later services and mobile wallets, is lowering purchase barriers for a broader consumer base and enabling higher-value transactions online. As last-mile delivery infrastructure improves across secondary cities and rural areas, the addressable market for online fashion retail will expand significantly, creating growth opportunities for brands that invest early in digital distribution capabilities and consumer experience.

- Sustainable Fashion and Circular Economy Development: Growing environmental awareness among younger Mexican consumers is creating demand for sustainably produced and ethically sourced apparel, presenting new positioning opportunities for eco-conscious brands. The rise of pre-owned and resale fashion platforms in Mexico is extending product lifecycles and creating new revenue streams for brands that participate in circular economy business models.

Market Challenges

- Informal Market Competition Creating Pricing Pressure on Formal Retailers: Mexico's large informal retail economy provides low-cost apparel alternatives that create sustained competition for formal sector brands, particularly in lower-income consumer segments. Informal vendors operating in tianguis markets, street stalls, and unregistered online channels offer apparel at prices that formal retailers cannot match while maintaining quality standards and regulatory compliance costs. This dual-market structure compresses pricing power for formal players and makes it difficult to expand market share in price-sensitive demographic segments, requiring formal retailers to emphasise value-added services, brand trust, quality assurance, and after-sales support as differentiators that informal competitors cannot replicate.

- Currency Volatility Affecting Import Costs and Consumer Pricing: Peso fluctuations directly affect the cost of imported apparel and raw materials, creating pricing unpredictability for retailers dependent on international sourcing strategies. Significant portions of Mexico's premium and mid-market apparel are either imported finished goods or manufactured using imported fabrics and components priced in US dollars or euros, making domestic retail pricing highly sensitive to currency movements. Sharp peso depreciation events force brands to choose between absorbing margin compression or passing cost increases to price-sensitive consumers, both of which negatively impact profitability or volume, requiring sophisticated currency hedging strategies and supplier diversification to manage foreign exchange exposure effectively.

Emerging Market Trends

1. Athleisure and Sports-Casual Crossover Driving Sports Wear Premiumisation

The convergence of athletic and casual wear aesthetics is reshaping Mexico's apparel market. Sportswear at 22.4% in 2025 is the fastest-growing type segment, driven by rising health consciousness, gym membership growth, and flexible work environments enabling casual dress codes across urban workplaces.

2. Accelerating E-Commerce Adoption and Social Commerce Integration

E-commerce platforms are increasingly integrating social media shopping features, enabling direct purchase from Instagram and TikTok feeds. Mexico's online fashion segment is growing significantly faster than offline channels, with digital-first brands and marketplace sellers gaining substantial market share through 2034.

3. Resurgence of Traditional Mexican Textiles and Artisanal Fashion

Contemporary Mexican designers are incorporating traditional indigenous textile techniques, embroidery, and regional craft traditions into modern fashion lines, creating distinct market positioning. This trend is attracting premium domestic consumers and international buyers seeking culturally distinctive fashion products.

4. Omni-Channel Retailing Becoming the Industry Standard for Major Players

Leading Mexican retailers are investing in unified commerce infrastructure enabling seamless shopping experiences across physical stores, branded websites, and marketplace platforms. In-store digital integration, click-and-collect services, and loyalty programme unification are defining competitive advantage for established chains.

Industry Value Chain Analysis

The Mexico fashion and apparel value chain integrates raw material sourcing, textile manufacturing, apparel design and production, quality control, distribution through multiple retail channels, and end-consumer engagement. The architecture is evolving toward omni-channel integration as the dominant commercial format.

|

Stage |

Key Activities |

|

Raw Material & Fabric Sourcing |

Procurement of natural and synthetic fibres, fabrics, dyes, and trims from domestic and international suppliers |

|

Textile Manufacturing & Dyeing |

Fabric weaving, knitting, dyeing, printing, and finishing processes for downstream garment production |

|

Apparel Design & Production |

Pattern making, cutting, sewing, embroidery, embellishment, and assembly by brands and manufacturers |

|

Quality Control & Packaging |

Garment inspection, labelling, tagging, pressing, folding, and packaging for retail or wholesale distribution |

|

Distribution & Retail Channels |

Logistics, warehousing, and delivery through offline stores, department chains, and online platforms |

|

End Consumer & After-Sales Service |

Consumer purchase, use, alteration, resale, and recycling of apparel products |

Raw material and fabric sourcing is the most cost-sensitive stage, influenced by global cotton prices, currency exchange rates, and USMCA trade provisions. The distribution and retail stage is experiencing the most rapid transformation as e-commerce reshapes the traditional offline-dominant model.

Technology Landscape in the Mexico Fashion and Apparel Industry

E-Commerce and Digital Retail Technology

E-commerce platforms powered by advanced recommendation engines, AI-driven personalisation, and seamless mobile payment integration are transforming how Mexican consumers discover and purchase fashion. Platforms integrating social commerce functionalities directly into social media feeds are enabling frictionless purchase journeys that significantly reduce conversion steps for fashion buyers.

Artificial Intelligence and Data Analytics in Fashion

AI-driven demand forecasting and trend analytics are enabling Mexican fashion brands and retailers to optimise inventory management, reduce overstock risks, and align product assortments with rapidly evolving consumer preferences. Machine learning algorithms analyse social media signals, search data, and purchase behaviour patterns to guide product development and merchandising decisions, improving sell-through rates and margin performance.

Sustainable Textile and Manufacturing Technology

Advances in sustainable textile production technology, including waterless dyeing processes, recycled fibre integration, and bio-based material innovation, are enabling Mexican apparel manufacturers to reduce environmental footprint while meeting growing consumer demand for sustainably produced garments. Certifications and traceability technologies are increasingly used by brands to substantiate sustainability claims and build consumer trust in eco-conscious product lines.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Type |

Casual Wear |

42.6% |

2025 |

|

Distribution Channel |

Offline |

68.1% |

2025 |

|

End User |

🔒 |

🔒 |

2025 |

|

Region |

Central Mexico |

43.4% |

2025 |

By Type

Casual wear leads the Mexico fashion and apparel market at 42.6% in 2025, encompassing everyday garments such as jeans, t-shirts, casual dresses, and leisurewear that serve as the core of Mexican consumer wardrobes across all income segments.

To access detailed market analysis, Request Sample

Sports wear at 22.4% captures growing fitness culture and athleisure adoption, while formal wear at 18.3% serves professional and occasion-wear demand. Safety wear at 9.7% reflects occupational protective clothing demand across manufacturing, construction, and industrial sectors.

By Distribution Channel

Offline channels lead at 68.1% in 2025, encompassing department stores, specialty fashion retailers, brand-owned stores, and informal market stalls that serve as primary purchase points for most Mexican consumers across income levels.

Online channels at 31.9% are growing significantly faster than offline, driven by expanding internet penetration, growing consumer comfort with digital payments, and aggressive pricing by e-commerce marketplaces and direct-to-consumer fashion brands.

Regional Market Insights

|

Region |

Share (2025) |

Key Fashion Market Drivers & Characteristics |

|

Central Mexico |

43.4% |

Driven by Mexico City's fashion retail concentration, high consumer spending power, and density of flagship domestic and international brand stores |

|

Northern Mexico |

29.8% |

Supported by proximity to the United States, strong industrial and maquiladora workforce demand, and growing middle-class brand adoption |

|

Southern Mexico |

19.1% |

Rising adoption of affordable fashion supported by increasing internet penetration, tourism-related spending, and growing informal retail activity |

|

Others |

7.7% |

Driven by regional retail expansion, tourist zone apparel demand, and growing e-commerce accessibility across smaller cities and towns |

Central Mexico at 43.4% leads through Mexico City's fashion retail concentration, highest disposable income levels, and widest availability of international and domestic fashion brands. Northern Mexico at 29.8% reflects strong border commerce, industrial workforce demand for workwear, and rising premium brand adoption in Monterrey and Guadalajara.

Northern Mexico at 29.8% benefits from its geographical proximity to the United States, driving cross-border fashion influence and strong demand for international brands. The region's manufacturing sector creates consistent demand for workwear and safety wear alongside growing premium fashion consumption in major cities.

Southern Mexico at 19.1% is the fastest-growing regional market, powered by rising internet penetration, increasing e-commerce adoption, and growing tourism-related apparel demand in Oaxaca, Cancún, and Mérida.

Competitive Landscape

The Mexico fashion and apparel market features a mix of global fast fashion giants, domestic department store chains, premium international brands, and local off-price retailers. The market is moderately fragmented, with leading players competing across price segments, retail formats, and digital channels.

|

Company Name |

Key Products |

Market Position |

Core Strength |

|

Grupo Axo |

Urban Store, Hollister, TAF, Old Navy |

Strong Challenger |

Mexico's leading multi-brand retailer with off-price and premium brand distribution capabilities |

|

H&M Group |

H&M |

Strong Challenger |

Fast fashion at accessible price points with growing store footprint in urban Mexican markets |

|

PVH Corp. |

Calvin Klein, Tommy Hilfiger |

Niche Player |

Global premium brand presence targeting upper-middle and premium consumer segments in Mexico |

|

Mutuo |

Unisex casual wear, outerwear, jackets, dresses, leather bags, wallets, shoes |

Niche Player |

Mexico City-based slow fashion brand with sustainable, direct-to-consumer boutique model |

|

Solei Store |

Handcrafted dresses, tops, ponchos, shawls, guayaberas, shoes, jewellery; Ethnic artisanal line |

Niche Player |

Proudly Mexican artisanal brand sourcing from indigenous women cooperatives |

Key players include Grupo Axo, H&M Group, PVH Corp., Mutuo, Solei Store, and others.

Key Company Profiles

Grupo Axo

Grupo Axo is Mexico's largest multi-brand apparel and fashion accessories retailer, operating off-price banners alongside premium international brand distribution across Mexico.

- Key Products: Promoda, Reduced, and Urban Store off-price banners; distribution of international premium brands; footwear and accessories retail across Mexico.

- Strategic Focus: Expanding off-price retail footprint and leveraging the TJX partnership to enhance inventory sourcing capabilities and bring the proven US off-price retail model to Mexican consumers.

Mutuo

Mutuo is a Mexico City-based slow fashion brand producing timeless, sustainably made garments and accessories through a premium direct-to-consumer boutique model, with worldwide shipping capabilities.

- Key Products: Unisex casual wear, outerwear, coats, jackets, shirts, pants, dresses, jumpsuits; leather bags, wallets, and shoes. All garments are produced using natural fibre fabrics including cotton, linen, and hemp.

- Strategic Focus: Deepening the direct-to-consumer boutique model across Mexico City's premium fashion districts while expanding wholesale distribution through curated cultural and concept store partners; leveraging worldwide shipping to grow international demand for sustainably produced Mexican contemporary fashion.

Market Concentration Analysis

The Mexico fashion and apparel market is moderately fragmented at the retail level, with international fast fashion giants, domestic department store chains, and informal market operators collectively serving a highly diverse consumer base across income segments and geographies.

Informal market operators continue to account for a substantial portion of total apparel sales, particularly in lower-income segments, creating a dual-market structure that is a defining characteristic of Mexico's fashion economy.

Investment & Growth Opportunities

Highest Growth Segments

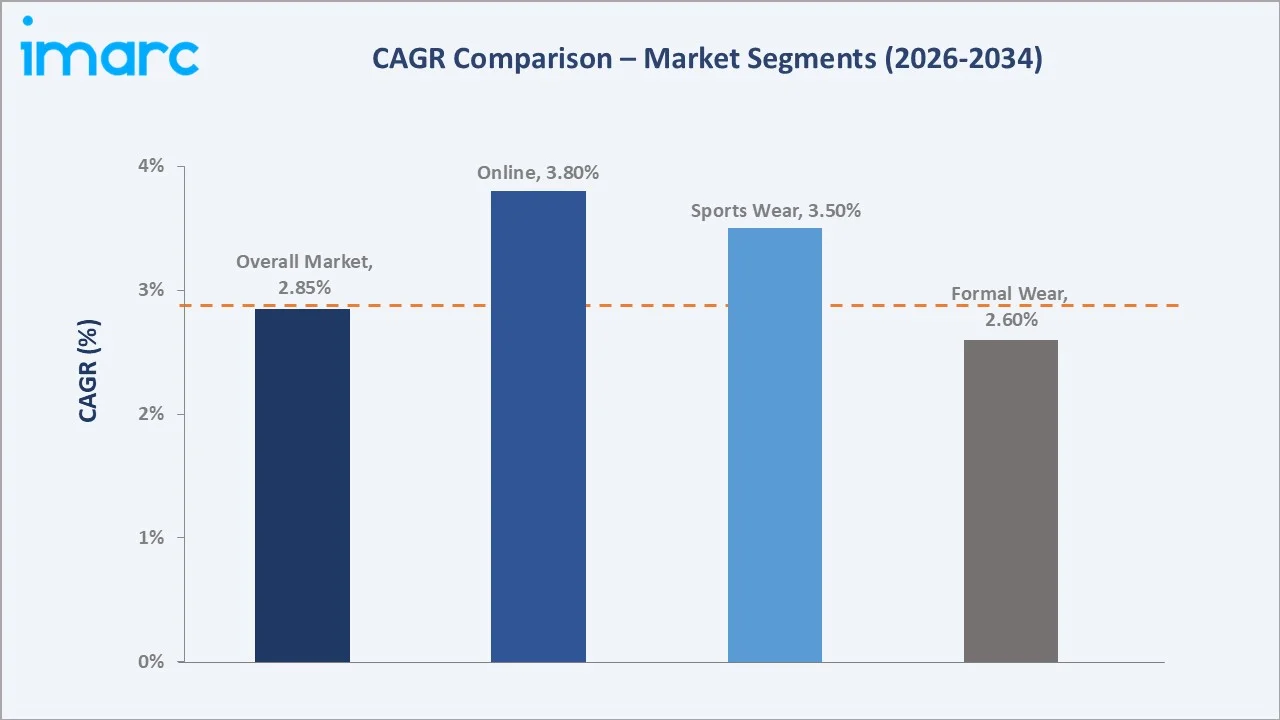

Sports wear (~3.50% CAGR), online distribution channel (~3.80% CAGR), Southern Mexico (fastest-growing regional market), sustainable fashion, and artisanal fashion lines represent the highest-growth investment vectors through 2034.

Emerging Investment Opportunities

E-commerce and social commerce infrastructure for direct-to-consumer fashion brands represents the most significant near-term emerging opportunity. Platform investments enabling seamless payment, logistics, and returns management will differentiate winners in Mexico's rapidly growing online fashion market.

Investment Themes

- Omni-channel retail technology investment: Unified commerce platforms enabling seamless cross-channel consumer experiences represent a critical differentiator as Mexico's fashion retail landscape evolves beyond offline dominance.

- Sustainable and ethically sourced fashion lines: Capitalising on growing eco-consciousness among younger Mexican demographics by launching or certifying sustainable fashion collections with transparent supply chain credentials.

Future Market Outlook (2026-2034)

The Mexico fashion and apparel market is projected to grow from USD 20.09 Billion in 2025 to USD 25.86 Billion by 2034, delivering a 2.85% CAGR. The market will reach USD 23.11 Billion by 2030, reflecting steady mid-period progression supported by Mexico's favourable demographics, expanding middle class, and accelerating digital retail adoption.

Three structural forces will define market growth through 2034: the continued premiumisation of casual and sports wear; the progressive shift of purchase occasions from offline to online channels; and the growing integration of traditional Mexican textile heritage into commercially viable fashion products targeting domestic and international consumers.

Research Methodology

Primary Research

Primary research comprised structured interviews with 50+ industry stakeholders including retail chain executives, fashion brand managers, textile manufacturers, e-commerce platform managers, and fashion trend analysts operating in Mexico.

Secondary Research

Secondary research encompassed company annual reports; INEGI consumer spending statistics; Mexico retail industry association data; fashion industry publications; e-commerce market data; trade association reports covering textile and apparel manufacturing; and government trade data under USMCA provisions.

Forecasting Models

Market revenue forecasts developed using consumption-based bottom-up model: (i) Mexico consumer spending on apparel by income segment; (ii) category penetration rates by type and channel; (iii) brand market share allocation by segment; (iv) e-commerce adoption rate adjustment for online channel forecast acceleration through 2034.

Mexico Fashion and Apparel Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Types Covered | Formal Wear, Casual Wear, Sports Wear, Safety Wear, Others |

| Distribution Channels Covered | Online, Offline |

| End Users Covered | Men, Women, Kids |

| Regions Covered | Northern Mexico, Central Mexico, Southern Mexico, Others |

| Companies Covered | Grupo Axo, H&M Group, PVH Corp., Mutuo, Solei Store, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the Mexico fashion and apparel market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the Mexico fashion and apparel market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the Mexico fashion and apparel industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Mexico Fashion and Apparel Market Report

The Mexico fashion and apparel market reached USD 20.09 Billion in 2025, driven by casual wear dominance at 42.6%, offline channel leadership at 68.1%, and Central Mexico commanding 43.4% of the national market share. Rising disposable incomes, growing social media influence, and expanding retail channels are the primary growth drivers.

The Mexico fashion and apparel market grows at a CAGR of 2.85% during 2026-2034, reaching USD 25.86 Billion by 2034. This growth reflects steady middle-class expansion, accelerating e-commerce adoption, omni-channel retail maturation, and growing consumer preference for branded and premium fashion products.

Casual wear leads at 42.6% in 2025, capturing the dominant everyday clothing category driven by lifestyle normalisation of relaxed dressing, growing remote-work culture, and strong fast fashion retailer presence. Sports wear at 22.4% is the fastest-growing type segment through the forecast period.

Offline channels dominate at 68.1% through department stores, specialty fashion retailers, brand-owned stores, and informal market stalls. However, online channels at 31.9% are growing at a significantly faster rate, driven by increasing internet penetration and growing digital payment adoption across Mexico.

Central Mexico leads at 43.4% through Mexico City's fashion retail concentration, highest consumer spending power, and the widest availability of both international and domestic fashion brands. Northern Mexico at 29.8% and Southern Mexico at 19.1% are the next largest regional markets.

Leading companies include Grupo Axo, H&M Group, PVH Corp., Mutuo, Solei Store, and others.

The Mexico fashion and apparel market is projected to reach approximately USD 23.11 Billion by 2030, with online retail growing its share, casual and sports wear continuing to dominate, and Central Mexico maintaining regional leadership while Southern Mexico registers faster growth.

Three priority investment opportunities: e-commerce and social commerce platform infrastructure for direct-to-consumer fashion brands; sustainable fashion product development targeting eco-conscious younger Mexican consumers; and off-price retail expansion leveraging proven US off-price models in Mexico's growing middle-market consumer segment.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)