Motor Control Centers Market Size, Share, Trends, and Forecast by Type, Voltage, Component, End-Use Sector, and Region, 2026-2034

Motor Control Centers Market Size, Share, Trends & Forecast (2026-2034)

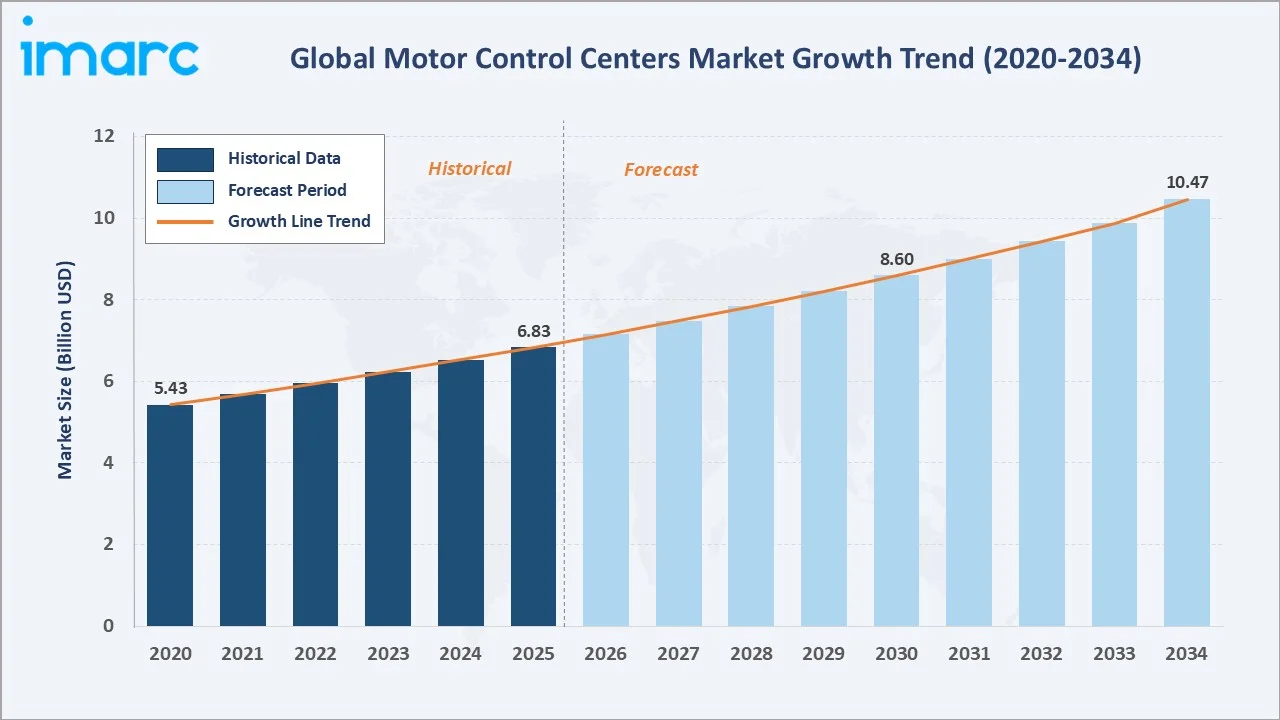

The global motor control centers market reached USD 6.83 Billion in 2025 and is projected to reach USD 10.47 Billion by 2034, growing at a CAGR of 4.71% during 2026-2034. Market growth is driven by accelerating industrial automation, rising demand for energy-efficient motor management systems, and expanding infrastructure investment across manufacturing, oil & gas, water treatment, and utilities sectors.

Market Snapshot

| Metric | Value |

|---|---|

| Market Size (2025) | USD 6.83 Billion |

| Forecast Market Size (2034) | USD 10.47 Billion |

| CAGR (2026-2034) | 4.71% |

| Base Year | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

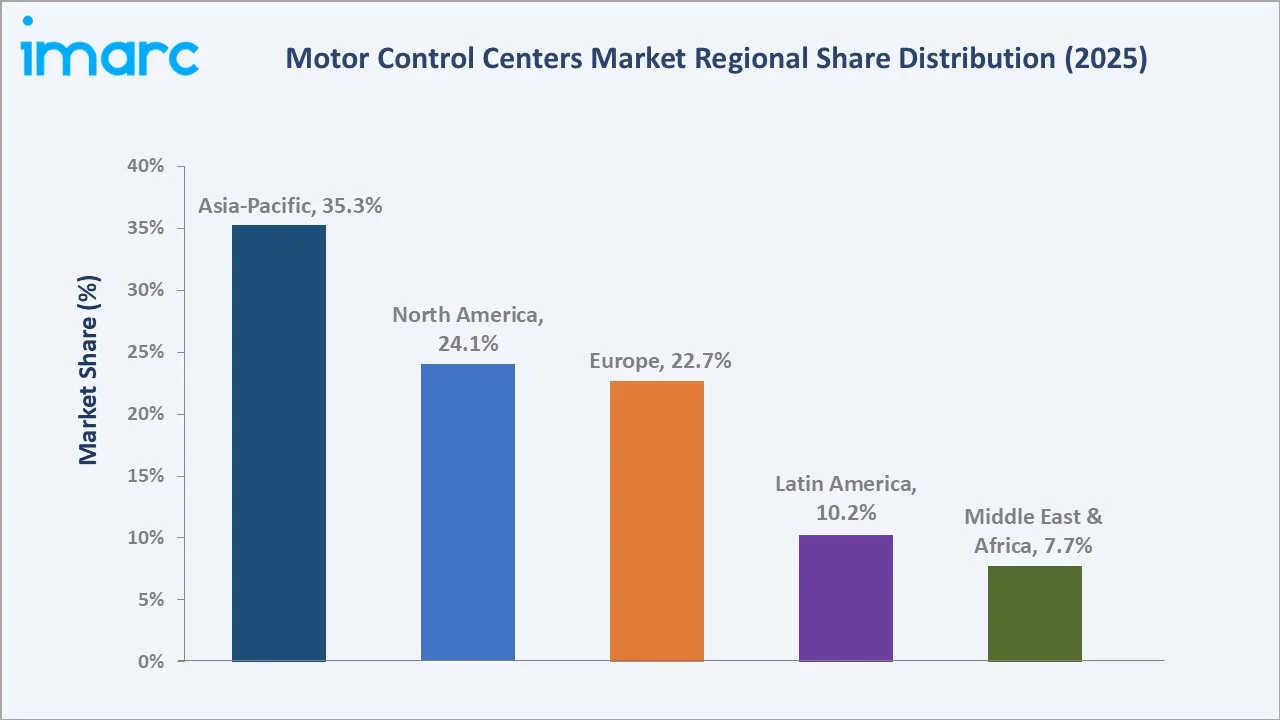

Asia-Pacific's market leadership is underpinned by China's large-scale manufacturing and infrastructure investment programs, India's rapidly expanding industrial and utilities base, and Southeast Asia's growing process industry capex. The conventional type’s 66.0% dominance reflects the large installed base of traditional motor control infrastructure in mature industrial markets, while the intelligent type is growing fastest as smart factory and Industry 4.0 adoption accelerates globally.

To get more information on this market, Request Sample

The market's 4.71% CAGR is supported by the structural tailwind of global industrial electrification, energy efficiency mandates, and the migration from standalone motor starters to centralized, intelligent motor control architectures that enable predictive maintenance, real-time diagnostics, and remote control across industrial plant operations.

Executive Summary

The global motor control centers market is on a steady growth trajectory supported by industrial automation demand, infrastructure expansion, and the technology transition from conventional to intelligent MCC platforms. From USD 6.83 Billion in 2025, the market is forecast to reach USD 10.47 Billion by 2034, creating incremental value of USD 3.64 Billion at a 4.71% CAGR.

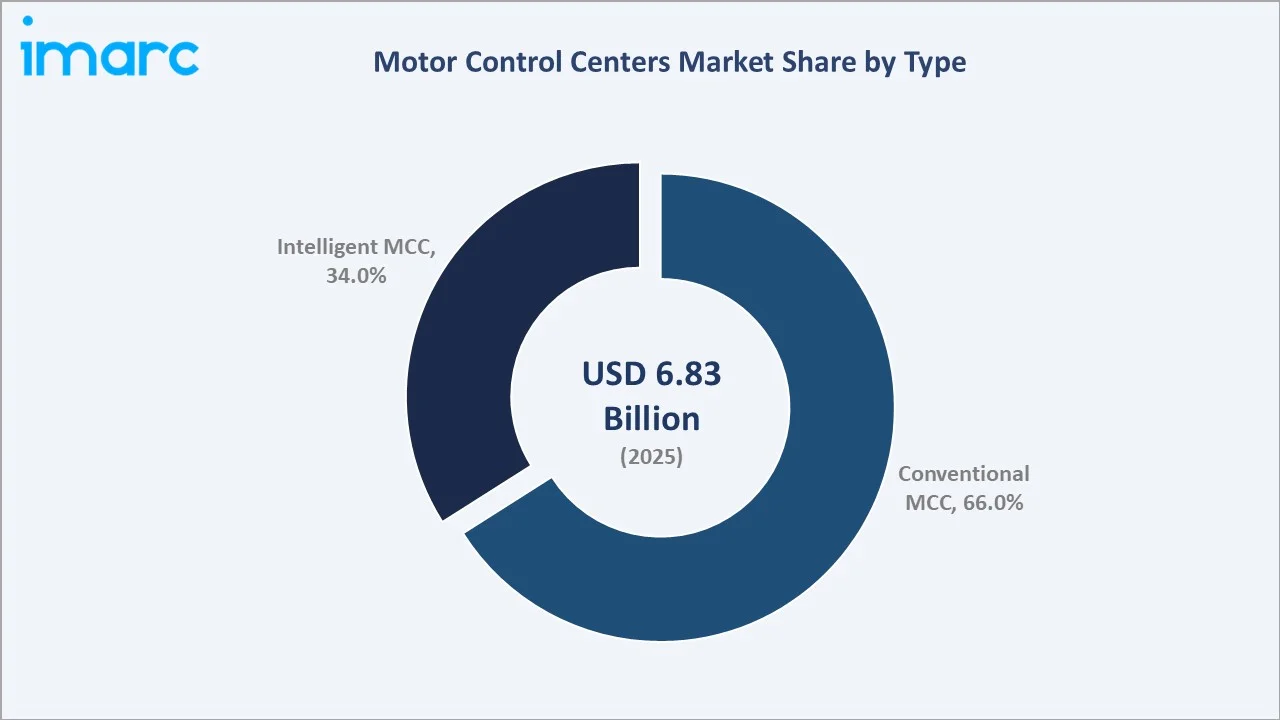

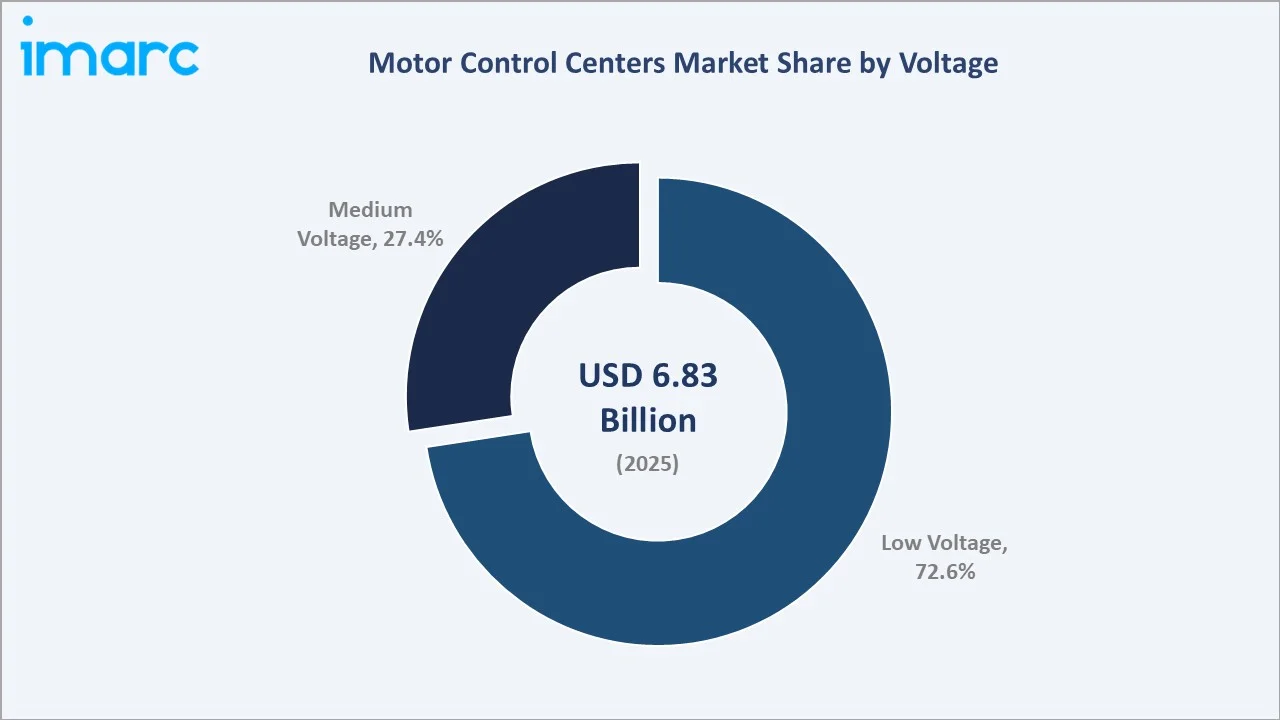

Conventional types hold a 66.0% share in 2025, anchored by the large global installed base of industrial motor control infrastructure and replacement demand in mature manufacturing markets. Intelligent types at 34.0% are growing at an estimated 6.80% CAGR, as IoT connectivity, predictive maintenance, and smart factory requirements drive technology upgrades. Low voltage MCCs dominate at 72.6%, while medium voltage MCCs at 27.4% serve high-power process industry applications.

Key players, including Siemens, ABB, Schneider Electric, Rockwell Automation, and Eaton, compete through product breadth, smart MCC technology platforms, industrial vertical expertise, and global EPC contractor relationships across the oil & gas, manufacturing, utilities, and water treatment end markets.

Key Market Insights

| Insight | Data |

|---|---|

| Largest Type | Conventional – 66.0% share (2025) |

| Fastest Growing Type | Intelligent MCC – ~6.80% CAGR (2026-2034) |

| Largest Voltage Segment | Low Voltage – 72.6% share (2025) |

| Fastest Growing Voltage | Medium Voltage – driven by process industry expansion |

| Leading Region | Asia-Pacific – 35.3% share (2025) |

| Top Companies | Siemens, ABB, Schneider Electric, Rockwell Automation, and Eaton |

Key Analytical Observations:

- Conventional types at 66.0% (2025) remain dominant due to the massive global installed base of industrial motor control infrastructure requiring replacement, retrofitting, and maintenance, particularly in mature industrial markets across North America and Europe.

- Intelligent types at 34.0% (2025) are the primary growth engine, with an estimated CAGR of 6.80%, nearly 50% higher than the overall market rate. Integration of PLCs, SCADA interfaces, Ethernet/IP communication, and IoT-enabled motor management modules transforms MCCs from passive switchgear enclosures into active, data-generating nodes within smart factory architectures.

- Low voltage MCCs at 72.6% (2025) reflect the dominant role of low-voltage (up to 1 kV) motor control in manufacturing, building automation, water treatment, and commercial facility applications. Their cost advantage, simpler installation requirements, and compatibility with standard 400V/480V power distribution infrastructure make them the default specification for the majority of global industrial projects.

- Asia-Pacific's 35.3% (2025) regional share is driven by China's capital-intensive industrial expansion, India's manufacturing sector growth under the Production Linked Incentive (PLI) scheme, and Southeast Asia's rapidly expanding chemical, food processing, and pharmaceutical industries.

Motor Control Centers Market Overview

A motor control center (MCC) is an assembly of one or more enclosed sections containing a common power bus and motor control units, each controlling one or more electric motors in an industrial or commercial facility.

MCCs centralize motor control, protection, and monitoring functions that would otherwise require individual starter units distributed across a plant, delivering advantages in space efficiency, operational safety, maintenance access, and electrical protection coordination.

The market is structured around two technology tiers: conventional MCCs (electromechanical starters, contactors, and overload relays in standardized enclosures) and intelligent MCCs (integrating variable frequency drives, smart motor controllers, fieldbus communication, and energy management software).

The transition to intelligent MCCs is the primary technology narrative of the 2025–2034 forecast period, driven by Industry 4.0 adoption and predictive maintenance mandates across process industries.

Market Dynamics

To evaluate market opportunities, Request Sample

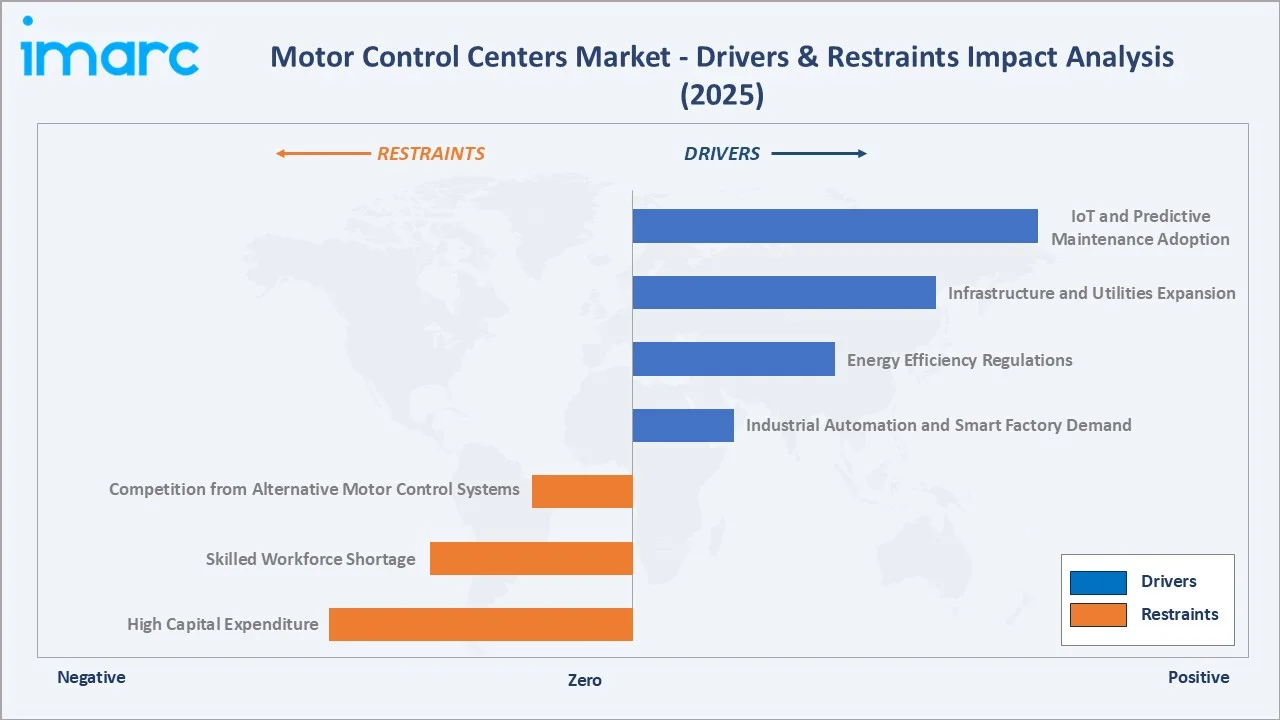

Market Drivers

- Industrial Automation and Smart Factory Demand: The global industrial automation services market is expected to grow at 6.84% through 2034, driven by labor cost pressures, quality consistency demands, and Industry 4.0 transformation initiatives. MCCs are a foundational infrastructure element of automated manufacturing plants, automated production lines, pumping stations, and conveyor systems.

- Energy Efficiency Regulations: IEC 60034-30-1 motor efficiency standards (IE3/IE4 premium efficiency requirements) and EU Ecodesign regulations are compelling industrial operators to replace aging motor systems with high-efficiency alternatives. Motor system upgrades typically include MCC replacement as part of drive optimization projects, creating a regulation-driven replacement demand cycle.

- Infrastructure and Utilities Expansion: Global infrastructure investment in water treatment, power generation, mining, and chemical processing is creating greenfield MCC demand. The global water and wastewater treatment market alone requires MCC installation across thousands of pump stations annually.

- IoT and Predictive Maintenance Adoption: Integration of smart sensors, wireless connectivity, and AI-driven analytics into MCC platforms enables predictive maintenance programs that reduce unplanned downtime by 30–50%. Industrial operators in high-availability process industries are upgrading to intelligent MCC.

Market Restraints

- High Capital Expenditure: A complete intelligent MCC installation for a medium-scale industrial plant costs USD 150,000–800,000 depending on the number of motor feeders and technology specification. This capital commitment creates budget approval cycles of 6–18 months in corporate capital planning processes, extending the sales cycle.

- Skilled Workforce Shortage: Intelligent MCC installation, commissioning, and maintenance require specialized expertise in industrial electrical systems, PLC programming, and fieldbus communication, skills that are in structural short supply globally.

- Competition from Alternative Motor Control Systems: Distributed motor control architectures using individual smart starters, intelligent electronic device (IED)-based systems, and decentralized variable frequency drives offer alternative motor control solutions that compete with centralized MCC configurations in certain application scenarios.

Market Opportunities

- Data Centre and Renewable Energy Infrastructure: The global data center construction boom and renewable energy installation programs are creating new MCC demand segments. Data centers require MCCs for cooling system motor control, while wind turbine nacelles and solar-plus-storage facilities require custom MCC configurations for generator control and battery management system integration.

- Emerging Market Industrialization: India, Indonesia, Vietnam, and Nigeria collectively represent a USD 1.5+ Billion incremental MCC opportunity by 2034, as manufacturing sector expansion under government industrial policy programs drives greenfield industrial facility construction requiring complete electrical infrastructure including MCCs.

Market Challenges

- Cybersecurity in Connected MCCs: As intelligent MCCs are integrated into industrial control networks with internet connectivity, they become potential attack surfaces for industrial control system (ICS) cyberattacks.

- Long Project Lead Times and Site-Specific Customization: MCCs are highly engineered, site-specific products requiring detailed engineering, factory acceptance testing, and on-site commissioning. Project lead times of 16–52 weeks create cash flow challenges for suppliers managing large order backlogs and create scheduling dependencies with broader plant construction programs that are difficult to accelerate.

Emerging Market Trends

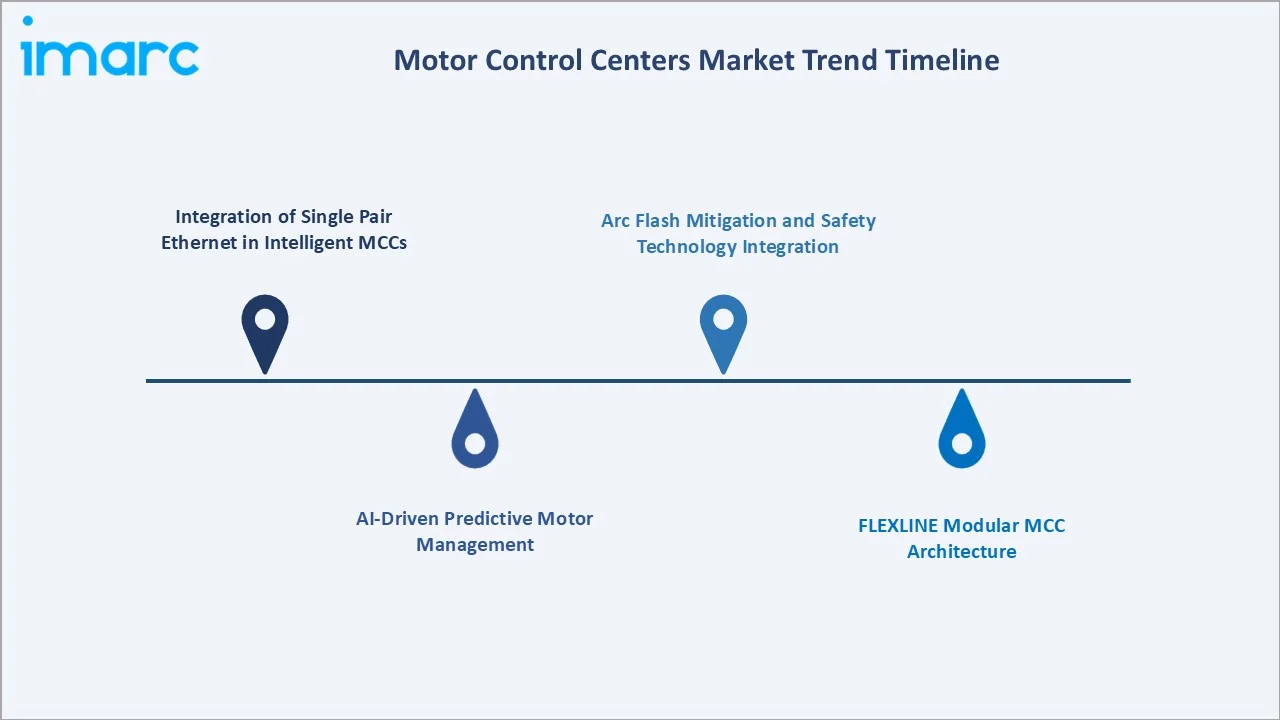

1. Integration of Single Pair Ethernet in Intelligent MCCs

Single Pair Ethernet (SPE), as implemented in Siemens' SIMOCODE M-CP launched in October 2024, enables digital communication over a single wire pair, dramatically reducing MCC panel wiring complexity and cost while enabling IP-level connectivity for every motor feeder unit. SPE integration makes each motor starter a smart network node, enabling granular energy monitoring, fault diagnostics, and remote control via standard industrial Ethernet infrastructure without requiring gateway devices or proprietary fieldbuses.

2. AI-Driven Predictive Motor Management

Machine learning algorithms applied to MCC-collected motor current, temperature, vibration, and voltage data are enabling predictive maintenance systems that identify incipient motor failures 2–6 weeks before breakdown. Rockwell Automation's FactoryTalk Analytics and ABB's Ability Smart Sensor platform exemplify this trend, delivering estimated 70% reductions in unplanned motor-related downtime for industrial operators in process industries.

3. FLEXLINE Modular MCC Architecture

Rockwell Automation's FLEXLINE 3500, unveiled at Hannover Messe in April 2024, represents the industry direction toward modular, IEC-standard MCC architectures with integrated smart variable frequency drives, real-time monitoring, and reduced power consumption. Modular MCC designs enable rapid reconfiguration for changing production layouts and reduce installation time by 20–35% compared to conventional fixed-configuration MCC assemblies.

4. Arc Flash Mitigation and Safety Technology Integration

Leading MCC suppliers are integrating arc flash detection systems, remotely operated racking mechanisms, and infrared monitoring ports into MCC enclosures as standard features. Eaton's arc-resistant MCC enclosures and Schneider Electric's ArcBlok technology represent the premium safety specification tier commanding 15–25% price premiums in regulated industrial markets.

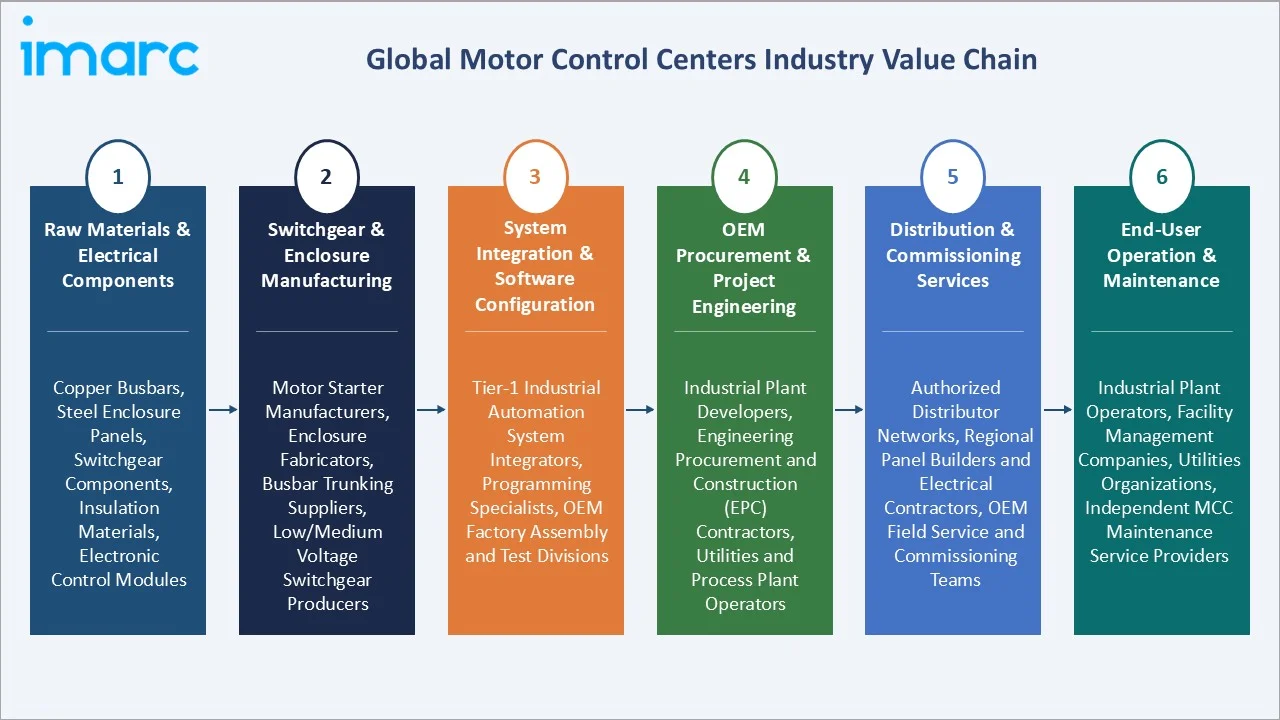

Industry Value Chain Analysis

The MCC value chain spans raw electrical component manufacturing through project-specific engineering, factory assembly, site commissioning, and long-term maintenance, with each stage requiring specialized capabilities in electrical engineering, industrial automation, and safety system integration.

| Stage | Key Players / Examples |

|---|---|

| Raw Materials & Electrical Components | Copper busbars, steel enclosure panels, switchgear components, insulation materials, electronic control modules |

| Switchgear & Enclosure Manufacturing | Motor starter manufacturers, enclosure fabricators, busbar trunking suppliers, low/medium voltage switchgear producers |

| System Integration & Software Configuration | Tier-1 industrial automation system integrators, programming specialists, OEM factory assembly and test divisions |

| OEM Procurement & Project Engineering | Industrial plant developers, engineering procurement and construction (EPC) contractors, utilities and process plant operators |

| Distribution & Commissioning Services | Authorized distributor networks, regional panel builders and electrical contractors, OEM field service and commissioning teams |

| End-User Operation & Maintenance | Industrial plant operators, facility management companies, utilities organizations, independent MCC maintenance service providers |

Technology Landscape in the Motor Control Centers Industry

Conventional MCC Technology

Conventional MCCs use electromechanical components, contactors, overload relays, fuses, and circuit breakers, assembled in standardized draw-out or fixed unit compartments within sheet steel enclosures. They remain the workhorses of global industrial motor control infrastructure, with proven reliability, simple maintenance requirements, and standardized components from all major suppliers.

Intelligent MCC Technology

Intelligent MCCs replace electromechanical starters with smart motor controllers or variable frequency drives (VFDs), integrated with fieldbus communication interfaces and energy metering capabilities. They communicate motor operating data, current, voltage, power factor, thermal status, and fault history to plant SCADA and MES systems in real time.

Medium Voltage MCC Technology

Medium voltage MCCs (1–15 kV) serve large motors in process industries, compressors, pumps, fans, and mills in oil & gas, mining, and power generation applications. They incorporate vacuum contactors, medium voltage VFDs, digital protection relays, and arc-resistant enclosure designs.

Market Segmentation Analysis

The report covers the following segments:

| Segment Category | Leading Segment | Market Share | Year |

|---|---|---|---|

| Type | Conventional | 66.0% | 2025 |

| Voltage | Low Voltage | 72.6% | 2025 |

| Component | 🔒 | 🔒 | 2025 |

| End-Use Sector | 🔒 | 🔒 | 2025 |

| Region | Asia-Pacific | 35.3% | 2025 |

By Type

Conventional MCCs lead with a 66.0% market share in 2025. Their dominance reflects the large global installed base of conventional motor control infrastructure requiring replacement and maintenance, combined with ongoing greenfield deployments in price-sensitive emerging market industrial projects where the cost premium of intelligent MCCs cannot be justified against project economics.

To access detailed market analysis, Request Sample

Intelligent MCCs represent 34.0% of the market in 2025 and are growing at an estimated 6.80% CAGR, the highest of any MCC segment. Smart factory investment, Industry 4.0 transformation programs, and predictive maintenance mandates from industrial operators in process industries are driving the migration from conventional to intelligent MCC platforms.

By Voltage

Low voltage MCCs dominate with a 72.6% share in 2025. Operating at voltages up to 1 kV, low voltage MCCs are specified for the vast majority of industrial motor control applications, from manufacturing assembly lines and HVAC systems to water treatment pumping stations and commercial building services.

Medium voltage MCCs at 27.4% serve the high-power process industry segment, controlling motors typically rated 200 kW to 10+ MW in oil & gas refineries, mining concentrators, power plants, and large water treatment facilities. Per-unit revenue for medium voltage MCCs is 5–15× higher than equivalent low voltage configurations, making this segment disproportionately valuable despite its smaller volume share.

Regional Market Insights

Asia-Pacific leads the global MCC market with a 35.3% share in 2025. The region's position reflects China's capital-intensive industrial expansion, India's rapidly growing manufacturing and infrastructure sectors, and Southeast Asia's expanding process industries requiring large-scale motor control infrastructure investment.

North America's 24.1% share reflects the region's large industrial installed base and active MCC replacement cycle, as well as significant oil & gas and manufacturing sector capital investment. Europe's 22.7% share is anchored by stringent energy efficiency regulations and Industry 4.0 transformation programs that are driving intelligent MCC specification across the region's automotive, chemical, and pharmaceutical manufacturing sectors.

| Region | Share (2025) | Key Growth Drivers |

|---|---|---|

| Asia-Pacific | 35.3% | China's large-scale manufacturing and infrastructure investment, India's industrial expansion under PLI schemes, and Southeast Asia's growing chemical, food processing, and utility sectors |

| North America | 24.1% | Large industrial replacement demand cycle, smart factory investment in automotive and food & beverage sectors, oil & gas infrastructure spending |

| Europe | 22.7% | IEC energy efficiency mandates driving motor system upgrades, Industry 4.0 manufacturing transformation, strong process industry base (chemicals, pharmaceuticals) |

| Latin America | 10.2% | Mining and oil & gas sector expansion in Brazil, Chile, and Mexico, growing utilities infrastructure investment, increasing industrial automation adoption |

| Middle East & Africa | 7.7% | Large oil & gas and petrochemical capital projects in GCC countries, growing power generation and water desalination infrastructure, expanding manufacturing investment in South Africa and the UAE |

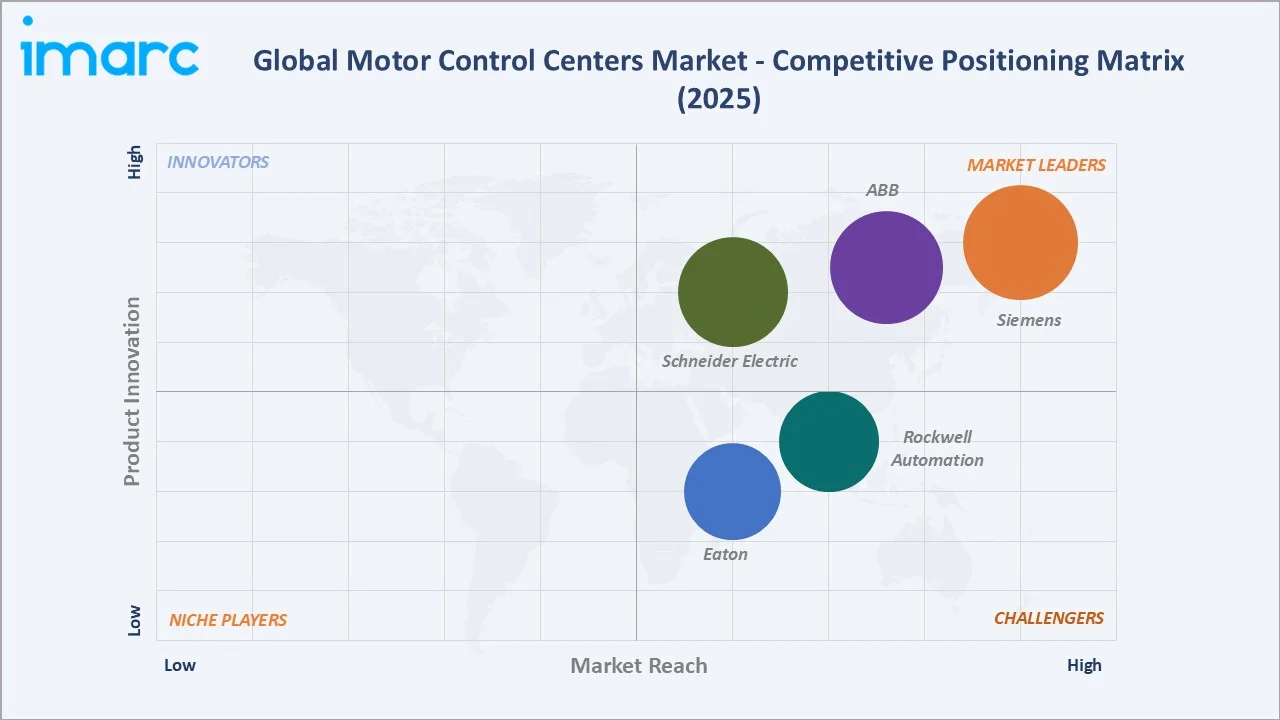

Competitive Landscape

The global motor control centers market is highly concentrated. Siemens, ABB, Schneider Electric, Rockwell Automation, and Eaton collectively account for an estimated 60–65% of global MCC revenues in 2025.

| Company Name | Brand Name | Market Position | Core Strength |

|---|---|---|---|

| Siemens | tiastar | Market Leader | Intelligent motor control and protection platforms, industrial Ethernet connectivity integration, broad global coverage across manufacturing and process industries |

| ABB | ABB | Market Leader | Modular MCC architecture, digital monitoring and analytics platform, strong presence in process-intensive industries including oil & gas and mining |

| Schneider Electric | Square D | Market Leader | Smart motor management and energy optimization solutions, integrated energy management ecosystem, dominant position in European manufacturing and OEM segments |

| Rockwell Automation | CENTERLINE, FLEXLINE | Strong Challenger | Scalable modular MCC design, advanced industrial analytics and software integration, strong foothold in North American automotive and food & beverage verticals |

| Eaton | Eaton | Strong Challenger | Arc-resistant and safety-focused MCC enclosures, IoT-enabled monitoring platform, established strength in data center infrastructure and utility applications |

The five players leverage deep industrial vertical expertise, global EPC contractor relationships, broad product portfolios spanning conventional and intelligent MCCs, and extensive installed base service networks to maintain their dominant market positions.

Key Company Profiles

Siemens

Siemens is one of the global market leaders in motor control center systems. Through its Smart Infrastructure and Digital Industries divisions, Siemens supplies conventional and intelligent MCCs to industrial, infrastructure, and commercial facility markets across all major global regions.

- Product Portfolio: Siemens tiastar standard motor control centers and SIMOCODE M-CP

- Recent Developments: In October 2024, Siemens launched the SIMOCODE M-CP, a next-generation motor management system featuring Single Pair Ethernet communication, compact design, and scalable licensable features, reducing installation costs and enhancing operational efficiency in MCC deployments.

- Strategic Focus: Single Pair Ethernet MCC integration, AI-driven predictive motor management, SIMOCODE ecosystem expansion, and intelligent MCC platform rollout across manufacturing, water treatment, and infrastructure markets globally.

ABB

ABB is also one of the world's largest MCC suppliers with a particularly strong presence in process industries including oil & gas, mining, pulp & paper, and power generation. ABB's MNS MCC system is the industry benchmark for intelligent MCC specifications in process industry applications globally.

- Product Portfolio: MNS low voltage intelligent MCC, ACS/ACH/ACQ series, and ABB Ability Smart Sensor for motor condition monitoring.

- Recent Developments: In January 2026, ABB announced that it will supply advanced motor control and electrification equipment, including 80+ medium-voltage drives, motors, generators, switchgear and eHouses, for Fervo Energy’s Cape Station geothermal project in Utah.

- Strategic Focus: Process industry intelligent MCC leadership, ABB Ability IoT platform integration, mining and oil & gas sector smart MCC deployment, and medium voltage MCC digital upgrade programs.

Market Concentration Analysis

The MCC market is highly concentrated at the top tier, with Siemens, ABB, and Schneider Electric alone accounting for an estimated 45–50% of global revenues. The top players hold approximately 60–65%. Below the global tier, a fragmented mid-market includes 50+ regional panel builders, local electrical switchgear manufacturers, and niche intelligent MCC specialists serving specific geographic markets or industrial verticals.

M&A consolidation is ongoing. Eaton's acquisition of Exertherm's thermal monitoring technology in 2024 strengthens its intelligent MCC safety monitoring capabilities. Regional consolidation in Asia-Pacific, where Chinese domestic manufacturers including Chint and Delixi are expanding internationally, is creating competitive pricing pressure in the conventional MCC segment that is constraining margin expansion for global tier-1 suppliers.

Investment & Growth Opportunities

Fastest Growing Segments

Intelligent MCCs (~6.80% CAGR), medium voltage MCCs for process industries, data center motor control applications, and MCC retrofits with IoT sensor overlays represent the highest-growth investment vectors through 2034. Together, these sub-segments address a combined incremental addressable market of approximately USD 2.0 Billion by 2034.

Emerging Market Expansion

India, Indonesia, Vietnam, and Saudi Arabia collectively represent a USD 1.5+ Billion incremental MCC opportunity by 2034. India's PLI-driven manufacturing expansion, Indonesia's downstream minerals processing investment (nickel smelting, aluminum refining), and Saudi Arabia's Vision 2030 industrial diversification program are creating large-scale greenfield industrial facility demand for MCC systems across all voltage tiers.

Venture and Institutional Investment Trends

- Global data center capital expenditure exceeding USD 250 Billion annually is creating a rapidly growing MCC demand segment for cooling system motor control, generating multi-year supply agreements for leading MCC vendors.

- Renewable energy infrastructure (wind farm electrical balance of plant, solar generation station switchgear) represents an incremental USD 400+ Million MCC opportunity by 2030 as global wind and solar installed capacity doubles through the forecast period.

- Industrial IoT platform investments by Siemens, ABB, and Schneider are creating digital service revenue streams from MCC-connected motor assets, supplementing hardware revenues with subscription-based analytics and monitoring contracts.

Future Market Outlook (2026-2034)

The motor control centers market is positioned for consistent, broad-based growth through 2034. From USD 6.83 Billion in 2025, the market will reach USD 10.47 Billion by 2034, representing total incremental value creation of USD 3.64 Billion at a 4.71% CAGR. Growth will be anchored by industrial automation investment, infrastructure expansion across emerging markets, and the continuing technology migration from conventional to intelligent MCC platforms.

The intelligent MCC segment will grow its share from 34.0% in 2025 to an estimated 42–45% by 2034, driven by smart factory adoption, energy efficiency mandates, and the declining cost of smart motor management technology. Asia-Pacific will maintain regional leadership, with India overtaking Japan as the second-largest Asia-Pacific MCC market by 2030 as its manufacturing and infrastructure investment cycle matures.

Research Methodology

Primary Research

Primary research comprised structured interviews with over 90 industry participants in 2024–2025, including MCC product managers, industrial electrical engineers, EPC project managers, industrial plant operators, and institutional investors across Asia-Pacific, Europe, and North America. Expert input validated market sizing, technology adoption timelines, and end-use sector demand drivers.

Secondary Research

Secondary research encompassed supplier annual reports, IEC and NEMA MCC standards documentation, IEA energy efficiency reports, industrial automation market publications, EPC project award databases, and trade publications including Plant Engineering, Electrical Contractor, and Control Engineering.

Forecasting Models

Market size estimations used top-down and bottom-up forecasting incorporating global industrial capex volumes, MCC market penetration rates by end-use sector, average system selling price trajectories, replacement cycle assumptions, and intelligent MCC upgrade program timelines. A base-case CAGR of 4.71% reflects consensus validated against OEM backlog disclosures and industrial capex forecasts.

Motor Control Centers Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical and Forecast Trends, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Types Covered | Conventional, Intelligent |

| Voltages Covered | Low Voltage, Medium Voltage |

| Components Covered | Overload Relays, Circuit Breakers & Fuses, Soft Starter, Busbars, Variable Speed Drives, Others |

| End-Use Sectors Covered | Industrial Sector, Commercial Sector |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico, Argentina, Colombia, Chile, Peru, Turkey, Saudi Arabia, Iran, United Arab Emirates |

| Companies Covered | Siemens, ABB, Schneider Electric, Rockwell Automation, Eaton, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the motor control centers market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the global motor control centers market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's five forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyse the level of competition within the motor control centers industry and its attractiveness.

- The competitive landscape allows stakeholders to understand their competitive environment and provides insight into the current positions of key players in the market.

Frequently Asked Questions About the Motor Control Centers Market Size Report

The market reached USD 6.83 Billion in 2025 and is projected to grow to USD 10.47 Billion by 2034 at a 4.71% CAGR.

Asia-Pacific leads with a 35.3% share in 2025, driven by China's industrial expansion, India's manufacturing growth, and Southeast Asia's process industry capex.

Conventional MCCs use electromechanical starters in standard enclosures, while intelligent MCCs integrate smart motor controllers, VFDs, fieldbus communication, and IoT connectivity for predictive maintenance and remote monitoring.

Conventional types lead with a 66.0% share in 2025, anchored by replacement demand and greenfield deployment in price-sensitive markets.

Siemens, ABB, Schneider Electric, Rockwell Automation, and Eaton, are some of the key players.

Low voltage MCCs lead with 72.6% of the voltage segment in 2025, with medium voltage MCCs at 27.4%.

Intelligent MCCs are the fastest growing segment at approximately 6.80% CAGR, driven by smart factory and Industry 4.0 adoption.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)