Pyrolysis Oil Price Increases 2.5% in Canada, 2.2% in USA — Q1 2026 Update

10-Feb-2026

Summary:

Q1 2026 delivered a clean reversal for tracked pyrolysis oil markets, with all five regions posting quarter-on-quarter gains. Tightening circular economy regulations, firming chemical recycling offtake, and more efficient waste plastic collection systems all converged to tighten supply-demand balances through the period. Driven by these forces, pyrolysis oil prices advanced between 1.4% and 2.5% QoQ across the five tracked geographies. The broader energy picture grew more uncertain as the conflict escalated. Brent crude surged as much as 13% in early trading on March 2, 2026, a development that adds feedstock cost pressure to producers already contending with tighter operating margins.

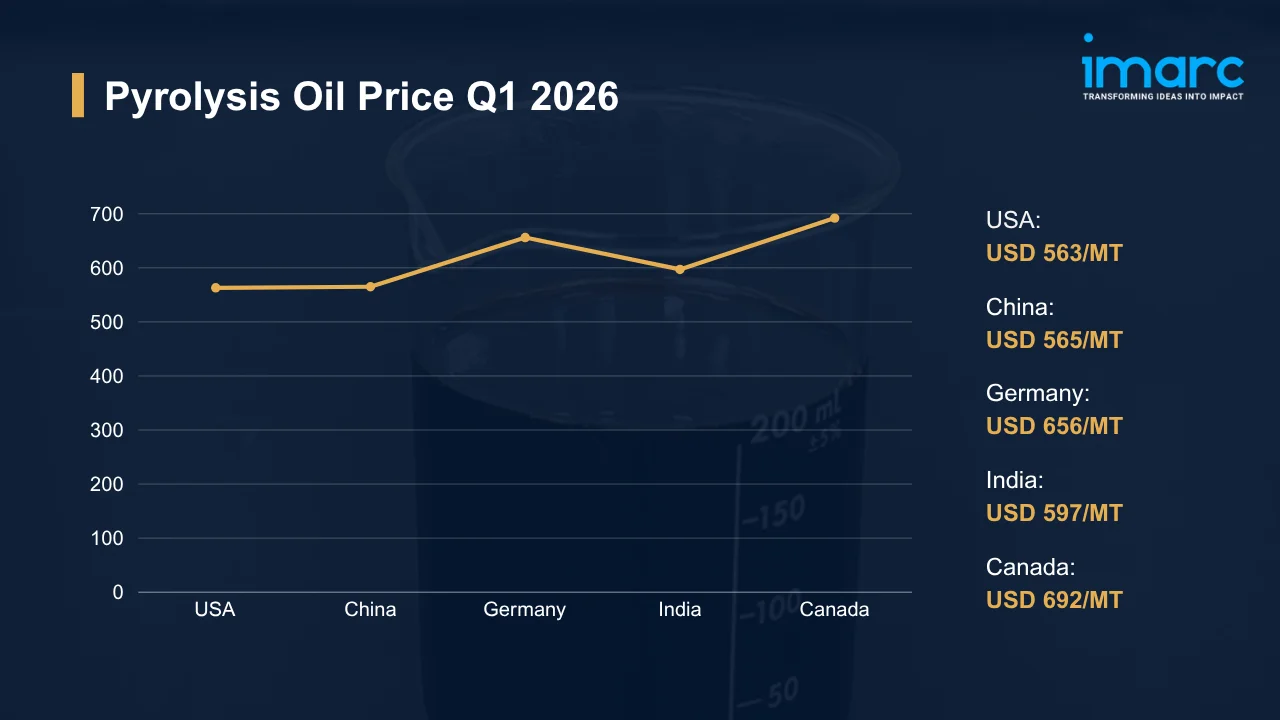

Pyrolysis Oil Price Q1 2026:

Regional prices (USD per MT) and QoQ changes Q1 2026 vs Q4 2025:

| Region | Price (USD/MT) | QoQ Change | Direction |

|---|---|---|---|

| USA | 563 | +2.2% | ↑ Growth |

| China | 565 | +2.0% | ↑ Growth |

| Germany | 656 | +1.4% | ↑ Growth |

| India | 597 | +1.5% | ↑ Growth |

| Canada | 692 | +2.5% | ↑ Growth |

To access real-time prices Request Sample

Kindly note: IMARC’s pricing database tracks pyrolysis oil price movements across major global markets.

What Moved Prices:

USA:

- In Q1 2026, pyrolysis oil prices in the USA reached USD 563/MT, a 2.2% QoQ recovery built on two converging forces. Driving the rebound was renewed offtake from Gulf Coast refiners blending pyrolysis oil as an alternative feedstock alongside conventional crude-derived inputs, with chemical recycling operators also expanding contracted volumes as environmental compliance mandates tightened further. Spot availability tightened as a result, giving sellers the leverage to push offer levels higher through the quarter.

- The pyrolysis oil price chart through Q1 showed a steady climb from January through March, driven by stable domestic waste plastic collection networks that kept feedstock costs predictable and Midwest logistics corridors operating without major disruption. Buyers who had stayed cautious in Q4 returned with firmer order books once supply adequacy proved reliable across the quarter.

China:

- During Q1 2026, pyrolysis oil prices in China climbed to USD 565/MT, marking a 2.0% QoQ gain from the USD 554/MT recorded in Q4 2025, as post-holiday industrial restocking and recovering fuel blending demand from petrochemical processors tightened available spot volumes. Government backing for chemical recycling drove capacity expansion. Export interest from overseas buyers also returned, absorbing incremental production output that would otherwise have weighed on domestic pricing.

- Supported by efficient feedstock collection systems, pyrolysis units operated at stable throughput rates throughout the period, limiting any risk of supply overhang building in the domestic market. Stable domestic freight conditions kept logistical cost escalation in check, while the QoQ improvement in domestic selling prices gave Chinese producers a modest margin cushion that had been absent during the softer Q4 2025 trading environment.

Germany:

- In the fourth quarter of 2025, German pyrolysis oil eased to USD 647/MT before recovering to USD 656/MT by Q1 2026, a 1.4% QoQ gain shaped by the structural pull of Europe’s circular economy mandates on alternative fuel consumption. Industrial heating and energy recovery operators maintained consistent offtake through the quarter, providing a reliable demand floor that prevented offer levels from softening. High operating costs constrained rapid capacity additions. Supply remained tight as a result.

- Across Germany’s well-organized waste-sorting infrastructure, feedstock availability held steady through Q1, with collection networks operating without significant disruption for the second consecutive quarter. Steady import flows supplemented domestic pyrolysis output, while European circular economy policy continued pulling converter procurement toward pyrolysis-derived materials over conventional fossil-fuel alternatives. Energy-intensive processing costs remain a structural brake on margin recovery even as selling prices firm.

India:

- In Q1 2026, pyrolysis oil prices in India rose to USD 597/MT, a 1.5% QoQ gain from USD 588/MT, as the seasonal industrial slowdowns that had weighed on Q4 demand gave way to recovering activity from brick kilns, small-scale boilers, and waste-to-fuel blending operations. Government initiatives supporting waste-to-energy conversion contributed positive sentiment throughout the period, encouraging more active procurement from industrial end users who had sat on the sidelines in Q4.

- Improved waste collection networks across key producing states enhanced feedstock availability, enabling domestic pyrolysis units to sustain production without major raw material shortages through the quarter. CIF import volumes held steady as overseas sellers maintained competitive offer levels, which limited any sharp tightening of domestic supply balances. Intermittent demand variability from smaller industrial operators persisted. Pricing held its upward bias regardless.

Canada:

- During Q1 2026, pyrolysis oil prices in Canada climbed to USD 692/MT, the strongest QoQ gain at 2.5% among all tracked markets, as industrial buyers accelerated procurement of sustainable fuel alternatives under regulatory frameworks mandating low-emission energy adoption. Efficient waste management systems ensured feedstock consistency throughout the period, supporting reliable production throughput even as energy and processing costs remained structurally elevated relative to Q4 2025.

- Turning more active after a cautious Q4, buyers competed for available spot volumes as industrial heating demand recovered in January and February, pushing FOB prices from domestic producers steadily higher through the quarter. Higher energy-linked production costs compressed margins to some degree, though the QoQ price recovery was sufficient to offset the headwind for most participants. Supply-demand balances remained firm through March with no significant inventory overhang.

Pyrolysis Oil Price Outlook After the Israel–Iran–USA Conflict:

Rising Energy Costs and Feedstock Availability Pressure for Pyrolysis Oil: Crude oil benchmark movements feed directly into pyrolysis oil production cost structures, making the Strait of Hormuz disruption an immediate operational concern for producers in all five tracked markets. The benchmark freight rate for Very Large Crude Carriers (VLCCs) hit an all-time record of USD 423,736 per day on March 2, 2026 as tanker traffic through the strait collapsed. Waste plastic feedstock collection and thermal conversion operations might absorb substantially higher fuel costs as the energy shock propagates through the supply chain.

Regional Price Volatility and Demand Uncertainty for Pyrolysis Oil: Geopolitical uncertainty is reshaping procurement planning across industrial segments that rely on pyrolysis oil as an alternative fuel or chemical feedstock, with buyers in Europe and Asia reluctant to lock in large forward volumes while energy price direction remains unclear. Producers in India and Germany face the steepest exposure, as crude oil import pricing transmits most directly into their cost-price spreads. QoQ price volatility might widen if the conflict extends beyond the near term.

Immediate Market Reaction:

Pyrolysis oil markets are repricing risk across all major buying regions as crude and feedstock cost volatility accelerates. The pyrolysis oil price index faces upward pressure in Germany and India, where Brent-correlated production costs feed most directly into local offer levels, and buyers in Canada are factoring conflict-driven energy risk premiums into Q2 contract negotiations. Gulf-adjacent trade corridors carrying waste plastic feedstock and pyrolysis-derived fuel products face near-term interruption risk. Producers in Europe and Asia-Pacific reliant on imported energy inputs might see margin compression widen before stabilizing, depending on how quickly shipping lanes normalize.

Impact on Pyrolysis Oil Prices:

The conflict might trigger several key changes in the pyrolysis oil market:

- Feedstock Cost Escalation: Thermal conversion processes at pyrolysis facilities are energy-intensive, and crude oil benchmark surges translate directly into higher fuel costs for both collection logistics and on-site processing operations. At USD 563/MT to USD 692/MT across tracked markets, pyrolysis oil offers little pricing cushion. Producers will push selling prices higher to defend margins, and buyers in markets without domestic feedstock alternatives will have limited leverage to resist those increases.

- Trade Route Disruptions for Feedstock and Products: Shipments of waste plastic feedstock and pyrolysis oil products routed through Gulf-adjacent corridors face mounting congestion risk as shipping lines divert vessels to Cape of Good Hope alternatives. Re-routing adds two to three weeks of transit time, inflating CIF landed costs for import-dependent producers. Contract renegotiations might accelerate across key trade lanes as buyers and sellers attempt to share the additional freight burden before it fully hits spot pricing.

- Demand Repricing Across Industrial Segments: Industrial buyers including fuel blenders, chemical producers, and district heating operators might suspend new spot commitments while energy price direction remains uncertain, compressing near-term transaction volumes. Tightening conventional fuel supply under the same conflict conditions will, however, simultaneously improve pyrolysis oil’s relative cost competitiveness for buyers seeking alternatives. Procurement desks will balance those opposing pressures on a week-by-week basis through the conflict period.

Taken together, the cost-side and demand-side forces will pull pyrolysis oil pricing in opposing directions through the conflict period, with cost escalation likely the stronger near-term driver. Energy input pressures might dominate through H1 2026. Producers with established feedstock inventory positions and inland logistics networks will weather the disruption more effectively than those dependent on maritime routes.

Supply Chain Disruptions:

Pyrolysis oil supply chains carry direct exposure to Strait of Hormuz disruption through two transmission channels: the maritime freight costs embedded in waste plastic feedstock imports and the energy-input pricing that governs on-site production economics. Vessel transits through the strait have collapsed, with UNCTAD reporting a 95% drop from approximately 129 daily crossings in February 2026 to just 6 per day in March, generating immediate lead-time extensions and sharply higher landed costs for energy inputs across key pyrolysis processing facilities in Germany, India, and China.

Cape of Good Hope re-routing is emerging as the primary contingency for affected shipping operators, though each diverted voyage adds roughly two to three weeks of additional transit time and compounds bunker fuel cost exposure at elevated oil prices. Domestic feedstock procurement will likely gain share over import-dependent sourcing as CIF differentials widen. Inventory buffers at Canadian and German facilities might be drawn down faster than planned, while Chinese producers supplying Asian export markets absorb war-risk shipping surcharges that compress QoQ margin gains.

Global Market Overview:

Globally, the pyrolysis oil industry was valued at USD 621.08 Million in 2025. Market projections indicate steady growth, with the industry expected to reach USD 1,073.61 Million by 2034, with a compound annual growth rate (CAGR) of 6.27% during 2026-2034. Waste-to-energy policy frameworks and tightening plastic recycling mandates are expanding the addressable demand base across industrial heating, chemical feedstock, and fuel blending end uses. Technological improvements in pyrolysis conversion efficiency are reducing production costs and broadening commercial viability, reinforcing the positive pyrolysis oil price trend expected to continue through the forecast horizon.

Recent Highlights & Strategic Developments:

Recent strategic moves within the industry further illustrate evolving dynamics:

- In January 2026, French officials officially designated pyrolysis oil produced from waste tires, known as tire pyrolysis oil, as a raw material for the chemical sector. This choice represented a significant move in promoting circular material utilization from used tires, as the new classification improved its incorporation into chemical value chains while offering more clarity and stability for upcoming procurement strategies and collaborative relationships.

- In September 2025, Coolbrook, a prominent innovator in technology and engineering, revealed a major breakthrough in the production of circular plastics and sustainable materials. The firm effectively converted 100% of plastic waste into pyrolysis oil using its unique RotoDynamic Reactor (RDR) technology at a large-scale pilot plant in the Netherlands.

Pyrolysis Oil Price Forecast (2026):

Near-term pyrolysis oil prices will stay sensitive to conflict-driven energy cost movements, with procurement caution likely to persist among European and Asian industrial buyers through mid-2026. North American markets benefit from more insulated domestic feedstock sourcing networks and low-emission fuel mandates that sustain baseline demand, providing a degree of price support that import-dependent markets in Germany and India might not fully share.

Should geopolitical hostilities intensify, pyrolysis oil prices will face renewed upward pressure as energy benchmarks climb and freight surcharges widen across key trade routes; producers in conflict-exposed import-dependent markets might curtail output as feedstock costs approach unviable levels, tightening global spot availability. A negotiated de-escalation, by contrast, might ease Brent benchmarks and restore normal Hormuz transit, allowing cost structures to normalize and prices to stabilize across all tracked geographies by late 2026, as outlined in the pyrolysis oil price forecast.

Strategic Takeaways:

Looking ahead, the pyrolysis oil market is expected to sustain its upward price trajectory through 2026, anchored by tightening environmental mandates, expanding chemical recycling capacity, and growing institutional demand for waste-derived fuel alternatives. Feedstock availability improvements and regulatory tailwinds across Germany, India, Canada, and China will underpin steady appreciation across all five tracked markets.

To navigate this complex landscape, stakeholders should:

- Monitor Geopolitical Risk Exposure: Track escalation dynamics in the current conflict and assess how shifts in hostility levels might affect pyrolysis oil pricing, feedstock availability, and logistics costs. Establish internal alert thresholds that trigger procurement or hedging action when key energy benchmarks breach defined levels.

- Diversify Supply Chain Routes: Evaluate alternative sourcing geographies and shipping corridors to reduce dependence on conflict-exposed trade lanes. Secondary supplier agreements and contingency freight arrangements will provide critical resilience if primary routes face prolonged disruption or escalating war-risk surcharges.

- Adjust Procurement Strategy for Conflict Conditions: Adopt flexible contract structures with price reopener clauses and force majeure provisions to protect against geopolitical price spikes. Precautionary inventory buffers might reduce exposure if feedstock supply tightens abruptly across key sourcing markets during the conflict period.

- Track Regional Price Differentials: Monitor quarterly movements in pyrolysis oil price per MT across all five tracked markets to identify cost-saving procurement windows. Benchmark landed costs against prevailing contract rates to capture regional arbitrage and optimize sourcing decisions on a rolling basis.

- Monitor Upstream Feedstock Costs: Track waste plastic and biomass feedstock pricing alongside crude oil and natural gas benchmarks, as these inputs directly shape pyrolysis oil production economics. QoQ cost trend analysis will help anticipate selling price movements before they fully materialize in offer lists.

- Evaluate Regulatory and Circular Economy Developments: Monitor policy frameworks in Germany, France, India, and Canada governing pyrolysis oil classification, sustainability certification, and fuel blending mandates. Regulatory shifts will reshape both demand trajectories and feedstock cost structures, requiring proactive adjustment of sourcing and contracting strategies.

Subscription Plans & Customization:

IMARC offers flexible subscription models to suit varying needs:

- Monthly Updates — 12 deliverables/year

- Quarterly Updates — 4 deliverables/year

- Biannual Updates — 2 deliverables/year

Each includes detailed datasets (Excel + PDF) and post-report analyst support.

.webp)

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)