RBD Palm Oil Price Update: Continued Decline Across Key Markets in Q1 2026

04-Sep-2025

Produced through a sequence of refining, bleaching, and deodorizing stages applied to crude palm oil, RBD palm oil emerges as a pale golden, semi-solid fat with strong oxidative stability and a high smoke point suited to intense heat applications. Bakeries, frying operations, margarine plants, confectionery manufacturers, soap producers, cosmetics formulators, and oleochemical processors all draw on it as a primary input. RBD palm oil prices respond to upstream CPO production costs in Malaysia and Indonesia, energy tariffs at refining facilities, ocean freight conditions on key Southeast Asian export lanes, biofuel blending policies, and procurement cycles across food and industrial end-use sectors.

Global Market Overview

Globally, the RBD palm oil industry was valued at USD 44.68 Billion in 2025. Market projections indicate steady growth, with the industry expected to reach USD 58.83 Billion by 2034, with a compound annual growth rate (CAGR) of 3.10% during 2026-2034. Backed by expanding urban food manufacturing across Asia and Sub-Saharan Africa, the RBD palm oil price trend continues to be anchored in structural consumption growth. Biofuel blending mandates in Indonesia and Malaysia divert sizable palm oil volumes into domestic energy programs, progressively eroding the surplus available for export. Deforestation-compliance requirements under EU regulatory frameworks layer additional certification costs onto supply chains, reshaping landed cost economics across importing regions.

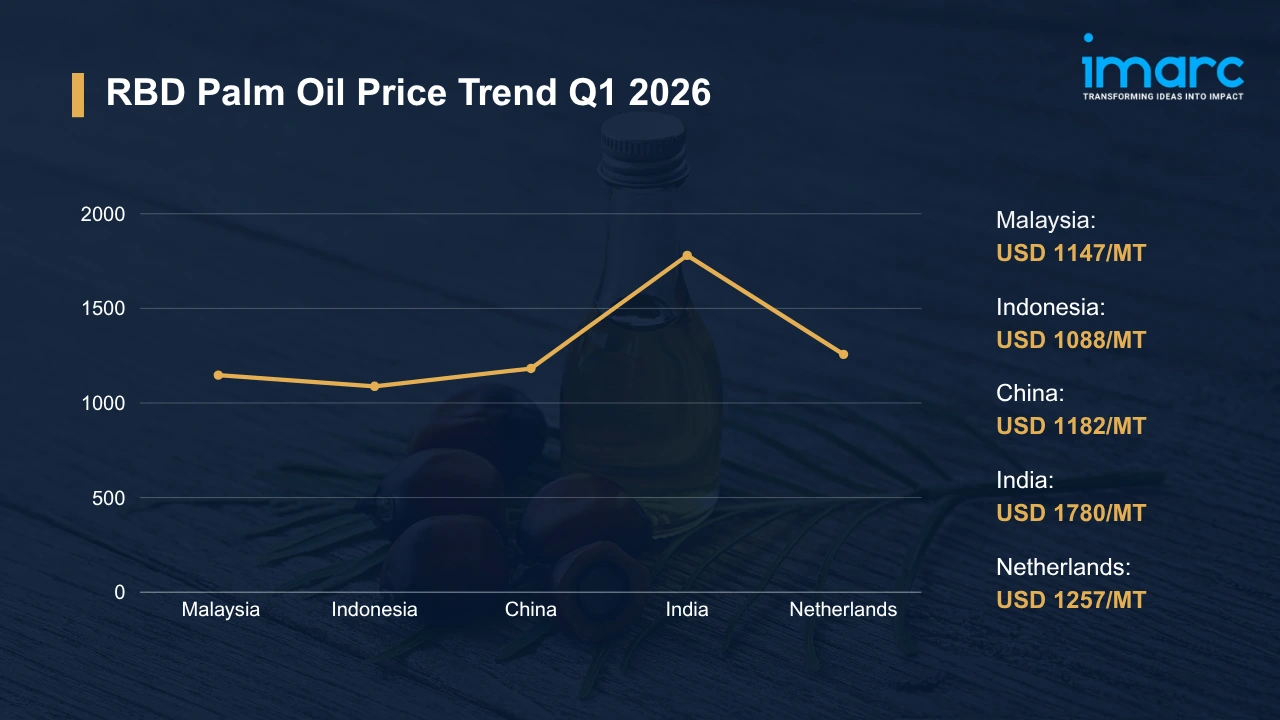

RBD Palm Oil Price Trend Q1 2026

Regional prices (USD per MT) and QoQ changes Q1 2026 vs Q4 2025:

| Region | Price (USD/MT) | QoQ Change | Direction |

|---|---|---|---|

| Malaysia | 1,147 | -2.48% | ↓ |

| Indonesia | 1,088 | -2.23% | ↓ |

| China | 1,182 | -1.32% | ↓ |

| India | 1,780 | -1.78% | ↓ |

| Netherlands | 1,257 | -2.10% | ↓ |

To access real-time prices Request Sample

What Moved Prices

Malaysia:

- At USD 1,147/MT in Q1 2026, Malaysian RBD palm oil prices recorded a 2.48% QoQ decline as bumper plantation output saturated near-term supply channels well ahead of export demand. Harvesting conditions proved favorable across key growing states. Downstream buyers in India, China, and Europe scaled back spot purchases, and the volume arriving at loading ports consistently exceeded committed shipment programs, keeping offer levels under pressure through March.

- Refinery throughput across Peninsular Malaysia stayed elevated, sustaining a steady flow of finished product into export positions. The RBD palm oil price chart traced a largely unbroken slide from January through quarter-end, with no meaningful demand catalyst emerging to interrupt the sequence. Subdued restocking interest from food processors in destination markets and cautious coverage by trading houses compounded the directional weakness established early in the quarter.

Indonesia:

- Prices in Indonesia softened to USD 1,088/MT across Q1 2026, with plantation output across Sumatra and Kalimantan holding at robust levels that kept origin supply ample throughout the period. Import demand from key buyers eased. Inventory accumulation at major refining facilities went largely unchecked, as export programs failed to draw down stocks at a pace that would have tightened near-term availability or shifted negotiating leverage toward sellers.

- Domestic absorption under the government's B40 biodiesel mandate diverted a portion of palm oil away from export channels, yet the overall supply overhang persisted. Ocean freight on Belawan-to-Rotterdam and Dumai-to-Mumbai corridors remained serviceable. Buyers favored short-dated spot parcels over forward cover, capping price floors and reinforcing the incremental QoQ decline observed in assessed export values.

China:

- In the first quarter of 2026, RBD palm oil prices in China eased to USD 1,182/MT as port inventories stayed well-supplied through uninterrupted import arrivals from Malaysia and Indonesia. Food processing demand was steady but flat. Confectionery producers, instant noodle manufacturers, and fats blenders drew on existing stocks rather than advancing procurement timelines, a pattern that kept spot inquiry thin and limited the scope for offer-price recovery through the quarter.

- Soybean and sunflower oil maintained competitive price spreads against palm oil across Shanghai and Guangzhou trading desks, reducing the urgency of substitution and giving downstream buyers flexibility to defer purchases. Port throughput and inland logistics operated without disruption. Contract renewal talks for Q2 2026 were consequently weighted toward buyers throughout the period.

India:

- During Q1 2026, RBD palm oil prices in India declined to USD 1,780/MT as import volumes through Kandla, Mundra, and Nhava Sheva arrived consistently, keeping edible oil distribution inventories at comfortable levels across the refining belt. Festive-season demand had cleared. Post-holiday procurement cycles among bulk buyers reset to conservative baseline schedules, reducing the restocking pressure that had briefly underpinned Q4 2025 values.

- Currency stability between the Indian rupee and US dollar kept landed cost movements narrow and predictable. Import duty adjustments introduced in the prior quarter had already been absorbed into market pricing, so no fresh tariff-driven volatility emerged. Refined palmolein distributors serviced day-to-day demand without building buffer stocks, which held the market in a steady, moderately softening trajectory through March 2026.

Netherlands:

- With import flows from Southeast Asia arriving without disruption across Rotterdam and Amsterdam terminals, RBD palm oil prices in the Netherlands settled at USD 1,257/MT in Q1 2026, down 2.10% from the prior quarter. Biofuel sector buying stayed restrained. Food manufacturers maintained lean procurement schedules calibrated to production runs rather than forward inventory targets, and no supply shortfall materialized to shift the market balance toward sellers.

- Unresolved compliance timelines under the EU Deforestation Regulation continued to cloud buying strategies for certified palm oil lots, as traders sought clarity on documentation requirements before committing to fresh forward positions. Competing vegetable oil supplies, particularly high-oleic sunflower oil, retained cost-competitiveness across the region. Logistics costs held steady throughout the quarter.

Drivers Influencing the Market

Several factors continue to shape RBD palm oil pricing and market behavior:

- Food Manufacturing and Edible Oil Sector Demand: Baseline procurement from bakeries, frying operations, margarine producers, and institutional food programs sustains a consistent demand floor for RBD palm oil across global markets. Urban population growth in Southeast Asia, South Asia, and Sub-Saharan Africa extends this floor year on year. Seasonal procurement surges linked to festive consumption cycles introduce periodic tightness into supply chains, creating short-window price support that can temporarily offset broader bearish fundamentals.

- Upstream CPO and Plantation Cost Dynamics: Labor availability, fertilizer application cycles, and fresh fruit bunch yields collectively determine CPO production economics, which feed directly into RBD palm oil refining margins. Per the USDA Foreign Agricultural Service, Indonesia's B40 mandate was projected to channel 14.5 Billion liters of biodiesel consumption in 2025, absorbing substantial CPO volumes into domestic energy use and compressing the share available for refined product export. That structural diversion shapes the RBD palm oil price index by tightening the effective supply base underpinning export price formation across major trade corridors.

- Energy Expenditure in Refining and Processing: Constrained by the energy intensity of bleaching and deodorizing stages, RBD palm oil production costs respond sharply to natural gas and electricity tariff movements at refining locations in Malaysia, Indonesia, and the Netherlands. Southeast Asian refiners benefit from subsidized industrial energy in certain producing regions. Cost gaps between origin refining hubs and European processing facilities influence trade flow patterns, shifting the competitive advantage in finished product supply and contributing to the periodic price divergence observed across regional assessments.

- Ocean Freight and Logistics Economics: Freight rate movements on Southeast Asia-to-Europe, Southeast Asia-to-India, and intra-Asia shipping corridors translate directly into landed cost variability for RBD palm oil at destination ports. Origin-pricing competitiveness narrows whenever freight surcharges widen, altering the delivered cost spread between Malaysian, Indonesian, and competing vegetable oil cargoes at key import terminals.

- Environmental and Regulatory Compliance: Across importing jurisdictions, traceability mandates, deforestation-risk due-diligence obligations, and RSPO certification requirements add measurable cost layers to palm oil supply chains. The EU Deforestation Regulation compels importers to document land-use compliance at origin, raising administrative and audit expenditures. Certified sustainable palm oil commands a structural price premium over non-certified grades, and that bifurcation influences contract pricing terms in regulated European and North American markets.

- Trade Policy and Currency Dynamics: Indonesia periodically revises export levy rates on crude and refined palm oil products, recalibrating the cost advantage held by origin refiners relative to destination-country processors. Malaysian ringgit and Indonesian rupiah movements introduce landed cost variability for buyers settling transactions in US dollars or euros. Import duty adjustments in India, the world's largest palm oil importer, alter purchase economics at the destination and ripple through origin offer pricing within weeks of policy announcements.

Recent Highlights & Strategic Developments

Recent strategic moves within the industry further illustrate evolving dynamics:

- In January 2026, Raj Oil Mills Limited introduced the PALMRAJ refined palmolein brand into the domestic Indian edible oil market. Disclosures were filed simultaneously with BSE and NSE under SEBI Regulation 30, with the company confirming the product line was designated for domestic sale only and fell outside the company's export programs.

- In September 2025, Agrinas Palma Nusantara, the Indonesian state-owned enterprise reclassified from a construction entity into a palm oil company earlier in 2025, unveiled a joint-venture strategy for managing its plantation portfolio. Assigned oversight of roughly 1.5 Million hectares at launch, the company has set a target of scaling that footprint to approximately 3 Million hectares by 2029.

Outlook & Strategic Takeaways

Looking ahead, the RBD palm oil market is expected to sustain measured growth through 2034, driven by expanding food manufacturing volumes in emerging economies, biodiesel mandate escalation in Southeast Asia, and broadening oleochemical applications in personal care and industrial segments. Anchored by upstream CPO yield trajectories and the evolving pace of EUDR implementation, the RBD palm oil price forecast will be shaped primarily by the interplay between origin supply availability, destination-market regulatory compliance costs, and freight rate cycles across key trade corridors.

To navigate this complex landscape, stakeholders should:

- Assess Freight Market Developments: Watch container rate movements on Southeast Asia-to-Europe and Southeast Asia-to-India corridors to anticipate shifts in landed cost structures. Negotiate logistics agreements that include rate adjustment provisions tied to published freight indices, reducing exposure to spot rate spikes.

- Evaluate Downstream Demand Indicators: Monitor food processing output volumes, edible oil consumption trends, and biofuel blending schedules across principal consuming markets. Align procurement planning cycles with observed demand signals to avoid over-stocking during low-demand phases and under-coverage during seasonal surges.

- Review Regulatory Compliance Expenditures: Audit costs tied to EUDR documentation, RSPO certification renewal, and import-market compliance obligations across all active distribution channels. Streamline audit workflows and supplier verification processes to reduce overhead without eroding sustainability credentials or market access.

- Strengthen Currency Exposure Management: Implement targeted hedging for palm oil procurement settled in Indonesian rupiah, Malaysian ringgit, or Indian rupee to stabilize projected landed costs. Synchronize treasury coverage windows with confirmed import payment schedules so foreign exchange positions align with actual transaction timing.

- Monitor Regional Price Differentials: Track quarterly pricing across Malaysia, Indonesia, India, and the Netherlands to identify cost-advantaged procurement windows by origin. Benchmark the RBD palm oil price per MT against prevailing contract rates at each import hub to sharpen sourcing decisions and reduce landed cost exposure.

- Explore Emerging Application Segments: Investigate commercial potential within specialty oleochemical derivatives, functional food ingredient markets, and industrial lubricant segments to broaden revenue exposure beyond conventional food and biofuel channels. Conduct feasibility assessments on novel palm-derived formulations that could capture addressable demand not served by existing product categories.

Subscription Plans & Customization

IMARC offers flexible subscription models to suit varying needs:

- Monthly Updates — 12 deliverables/year

- Quarterly Updates — 4 deliverables/year

- Biannual Updates — 2 deliverables/year

Each includes detailed datasets (Excel + PDF) and post-report analyst support.

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)