Synthetic Rubber Price Update: Sustained Growth Across Key Markets in Q1 2026

26-Feb-2026

Synthesized from petroleum-derived monomers including butadiene, styrene, and isoprene, synthetic rubber is an elastomer engineered to outperform natural rubber in resistance to heat, ozone, oils, and chemical solvents. Across tire manufacturing, automotive components, industrial sealing systems, and construction adhesives, synthetic rubber prices reflect demand cycles spanning SBR, BR, and NBR grades. Feedstock cost exposure dominates the pricing structure.

Global Market Overview:

Globally, the synthetic rubber industry was valued at USD 33.9 Billion in 2025. Market projections indicate steady growth, with the industry expected to reach USD 45.0 Billion by 2034, with a compound annual growth rate (CAGR) of 3.20% during 2026-2034. Electric vehicle adoption is accelerating across markets. Tied to rising global automotive output, tire production expansions across Asia and the Americas sustain the synthetic rubber price trend, while specialty low-rolling-resistance compound requirements for electric vehicles and growing adhesive-grade demand in construction and packaging are diversifying end use consumption beyond traditional tire channels.

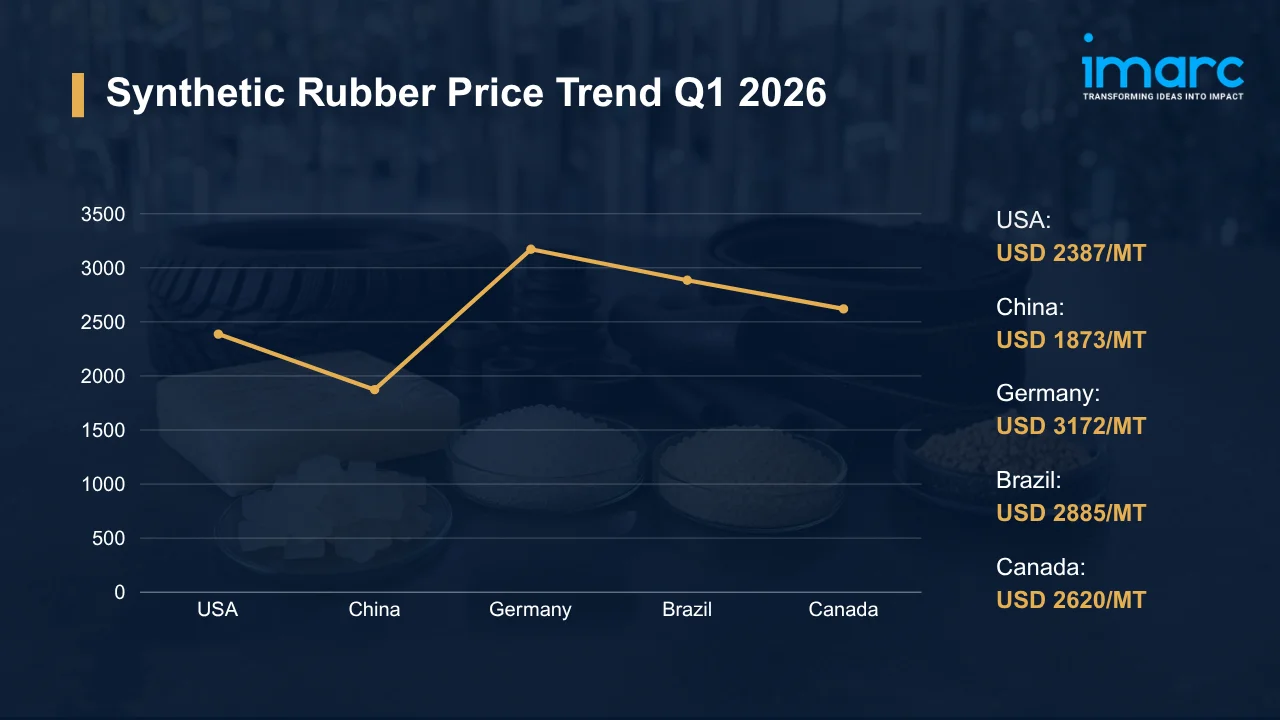

Synthetic Rubber Price Trend Q1 2026:

Regional prices (USD per MT) and QoQ changes Q1 2026 vs Q4 2025:

| Region | Price (USD/MT) | QoQ Change | Direction |

|---|---|---|---|

| USA | 2,387 | +2.23% | ↑ |

| China | 1,873 | +3.33% | ↑ |

| Germany | 3,172 | +1.46% | ↑ |

| Brazil | 2,885 | +2.11% | ↑ |

| Canada | 2,620 | +2.56% | ↑ |

To access real-time prices Request Sample

What Moved Prices:

USA:

- In Q1 2026, at USD 2,387/MT, synthetic rubber prices in the USA climbed 2.23% QoQ as automotive and tire manufacturers expanded procurement against recovering production schedules. Supported by steady feedstock flows from Gulf Coast petrochemical hubs, downstream processors maintained controlled operating rates throughout the quarter, containing supply-side disruptions.

- Replacement tire procurement volumes held firm. With cross-border logistics between Gulf Coast production centers and Midwest automotive belts operating reliably, industrial rubber goods and polymer-modification converters added incremental order activity without drawing down inventories aggressively. Constrained by cautious forward buying, spot transactions remained measured, keeping price gains gradual. The synthetic rubber price chart traced a steady upward path through March.

China:

- During Q1 2026, synthetic rubber prices in China advanced to USD 1,873/MT, driven by sustained procurement from tire producers and automotive OEMs. Regulated to prevent oversupply, domestic production kept availability balanced, while footwear manufacturers in coastal clusters absorbed incremental tonnage that might otherwise have weighed on domestic spot assessments.

- Pushed tighter by active export bookings to Southeast Asian markets, domestic availability tightened, lending upward support to quotations. At converter hubs in Guangzhou and Yiwu, cautious purchasing patterns capped speculative restocking as FMCG packaging demand and industrial applications sustained a consistent baseline.

Germany:

- In the first quarter of 2026, synthetic rubber prices in Germany reached USD 3,172/MT, reflecting firm feedstock costs and consistent demand from automotive engineering and high-performance rubber goods producers. Regional energy costs stayed persistently high. Elevated European natural gas pricing sustained production expenses across processing facilities, limiting any scope for downward price adjustment despite a relatively modest 1.46% QoQ increase.

- Across Rhine and Benelux industrial clusters, intra-EU logistics ensured reliable material distribution throughout the quarter. With replacement tire demand contributing steady baseline procurement, import volumes from Asian suppliers stayed controlled, preventing excess availability from pressuring prices. Adhering to routine replenishment schedules, buyers maintained sufficient inventory without accumulating surplus positions ahead of Q2.

Brazil:

- During Q1 2026, synthetic rubber prices in Brazil rose to USD 2,885/MT as tire producers and automotive sector converters expanded procurement against a backdrop of improving domestic demand. Against the backdrop of BRL exchange rate volatility, import parity economics shaped offshore sourcing decisions, with buyers from European and North American suppliers adjusting purchase timing to manage currency-driven cost exposure.

- Throughput at São Paulo-area terminals remained steady, enabling timely import arrivals and distribution to downstream manufacturing zones. Demand for industrial rubber compounds from the construction industry contributed additional volume. Expecting ongoing recovery in consumer demand, purchasers locked in forward contracts at increasing price points, boosting upward trends through March and finishing the quarter 2.11% higher than Q4 2025 evaluations.

Canada:

- In Q1 2026, synthetic rubber prices in Canada advanced to USD 2,620/MT, supported by stable demand from automotive and industrial component manufacturers. Underpinned by cross-border supply flows from US Gulf Coast petrochemical producers, feedstock-derived inputs remained consistently available, and domestic production volumes held steady without creating oversupply conditions in key buyer markets.

- Inbound material arrivals held market price. Rail and trucking networks across major manufacturing corridors delivered timely access to incoming shipments, and export activity to regional partners helped absorb any production surplus before it could pressure domestic quotations. Priced competitively below European-origin grades, US-sourced imports gave Canadian buyers cost flexibility, keeping landed cost exposure manageable through the quarter.

Drivers Influencing the Market:

Several factors continue to shape synthetic rubber pricing and market behavior:

- Automotive and Tire Sector Demand: Accounting for the largest share of global synthetic rubber consumption, tire manufacturing tracks automotive output and replacement tire cycles closely. According to the International Organization of Motor Vehicle Manufacturers (OICA), global vehicle production climbed to 96.4 Million units in 2025, a 3.9% year-on-year increase, with Asia-Pacific output alone rising 7.6% to roughly 59.2 Million vehicles. With expanding vehicle parc and replacement demand across emerging markets, procurement volumes sustain baseline demand.

- Upstream Feedstock Cost Dynamics: Within the synthetic rubber supply chain, butadiene and styrene are the principal inputs for SBR and BR production, and petrochemical price movements transmit directly to manufacturing costs. Shaped by steam cracker operating rates, naphtha feedstock availability, and scheduled refinery turnarounds, quarterly feedstock supply can swing tighter with very little notice. Tightening in mixed C4 streams, which serve as a butadiene source, or unexpected cracker outages compresses producer margins sharply. Once higher input costs crystallize, producers typically pass them through to buyers within one to two contract cycles.

- Energy Expenditure in Production: Consumed intensively during polymerization and downstream processing, natural gas and electricity rank as decisive cost inputs for synthetic rubber manufacturers across all major regions. Per the US Energy Information Administration (EIA), the 2025 annual average price of natural gas paid by industrial sector customers rose 21% compared with the 2024 average, driven by LNG export growth outpacing domestic production gains. Pushed higher by these energy cost shifts, production expenses shaped the synthetic rubber price index across European, North American, and Asian processing facilities throughout the year.

- Ocean Freight and Logistics Economics: Across trans-Pacific and Asia-Europe trade lanes, container shipping rates directly shape the landed cost of imported synthetic rubber grades. When freight tariffs rise, meaningful increments attach to CIF valuations, squeezing buyer margins on offshore-sourced material. Congestion at gateway terminals, such as Rotterdam, Los Angeles, and Ningbo, can disrupt scheduled arrivals and force costly spot procurement at premium rates. Tracked via FOB and CIF spread comparisons, prevailing freight conditions on each trade corridor are a key variable in sourcing strategy.

- Environmental and Regulatory Compliance: Covering synthetic rubber handling, storage, and waste-stream management, chemical safety regulations impose compliance expenditures on producers, importers, and distributors alike. Under REACH registration requirements in the EU and equivalent frameworks in North America, administrative and testing costs accumulate progressively and filter through to market pricing. Stricter VOC emissions standards at processing facilities require capital investment in abatement equipment, lifting fixed costs across the production base.

- Trade Policy and Currency Dynamics: Shaped by import tariff structures, antidumping measures, and trade agreement provisions, the competitive positioning of synthetic rubber grades from different origins shifts with each policy cycle. For Brazilian reais and Chinese yuan, exchange rate volatility influences export competitiveness and import parity pricing in buyer markets simultaneously. Through hedging strategies among large importers and export-oriented producers, transaction pricing adjusts across regions with floating-rate currency exposures, contributing to QoQ price variability.

Recent Highlights & Strategic Developments:

Recent strategic moves within the industry further illustrate evolving dynamics:

- In November 2025, Goodyear Tire and Rubber finalized the divestiture of its Polymer Chemical Business to private equity firm Gemspring Capital Management. The transaction transferred manufacturing operations in Houston and Beaumont, Texas, along with an R&D facility in Akron, Ohio, marking a significant corporate restructuring in the synthetic rubber sector.

Outlook & Strategic Takeaways:

Looking ahead, the synthetic rubber market is expected to sustain gradual expansion through 2034, supported by rising automotive output across emerging economies, growing EV-driven demand for specialty low-rolling-resistance compounds, and broadening industrial applications in adhesives, polymer modification, and construction sealing systems. Tracking upstream feedstock cost trajectories, particularly butadiene and styrene dynamics alongside energy pricing shifts, will remain the pivotal variable shaping the synthetic rubber price forecast across producing and consuming regions.

To navigate this complex landscape, stakeholders should:

- Monitor Regional Price Differentials: Track quarterly pricing variations across the USA, China, Germany, Brazil, and Canada to identify cost-saving procurement windows. Establish benchmarking protocols that compare landed costs against contract rates for optimal sourcing decisions.

- Assess Freight Market Developments: Monitor container shipping rate trends on trans-Pacific and Asia-Europe corridors to anticipate CIF cost movements on synthetic rubber imports. Negotiate logistics contracts with rate adjustment clauses tied to prevailing Baltic Exchange or Drewry WCI benchmark levels.

- Evaluate Downstream Demand Indicators: Track automotive production schedules and replacement tire order books across principal consumption markets as leading demand signals. Correlate sector output data with procurement planning cycles to optimize inventory positioning and avoid excess accumulation.

- Review Regulatory Compliance Expenditures: Audit current compliance costs associated with synthetic rubber handling, VOC emissions management, and chemical safety registration across operating jurisdictions. Identify operational efficiencies that reduce regulatory burden without compromising applicable chemical safety obligations.

- Strengthen Currency Exposure Management: Implement hedging strategies for procurement denominated in BRL, CNY, or EUR to stabilize landed cost projections against exchange rate volatility. Coordinate treasury and procurement functions to align foreign exchange coverage with anticipated import payment timelines, particularly for Brazil-origin material.

- Explore Emerging Application Segments: Investigate EV-grade synthetic rubber compound specifications and bio-based monomer developments with research partners to assess commercial viability. Benchmarking the synthetic rubber price per MT against specialty-grade contract rates will help procurement teams identify value-creation windows in higher-margin applications.

Subscription Plans & Customization:

IMARC offers flexible subscription models to suit varying needs:

- Monthly Updates — 12 deliverables/year

- Quarterly Updates — 4 deliverables/year

- Biannual Updates — 2 deliverables/year

Each includes detailed datasets (Excel + PDF) and post-report analyst support.

.webp)

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)