North America Automotive Market Size, Share, Trends, and Forecast by Type, Application, and Country, 2026-2034

North America Automotive Market Size, Share, Trends & Forecast (2026-2034)

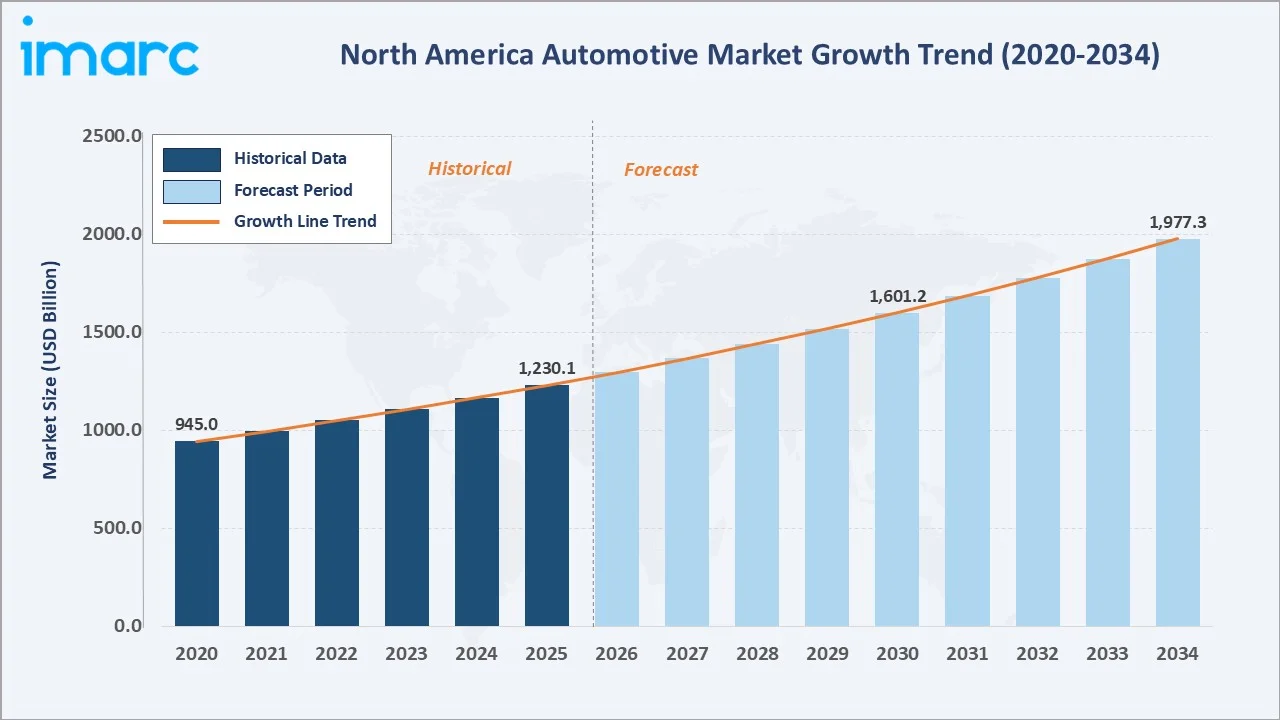

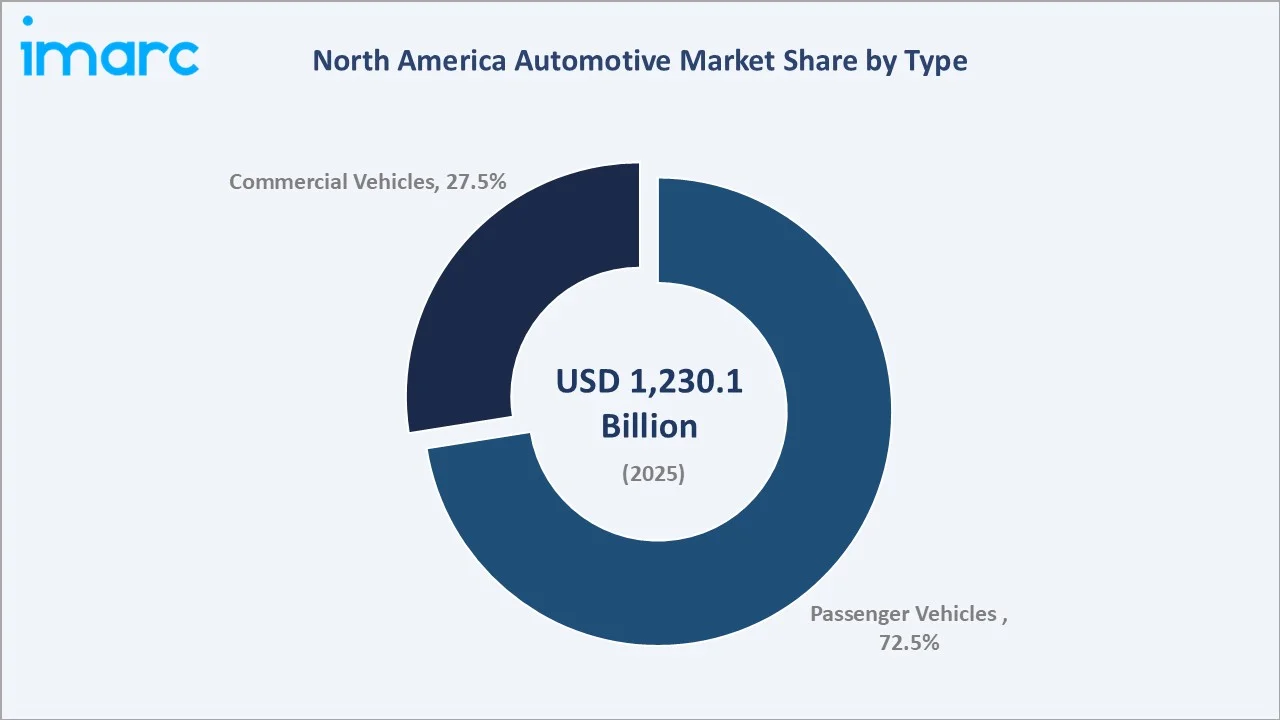

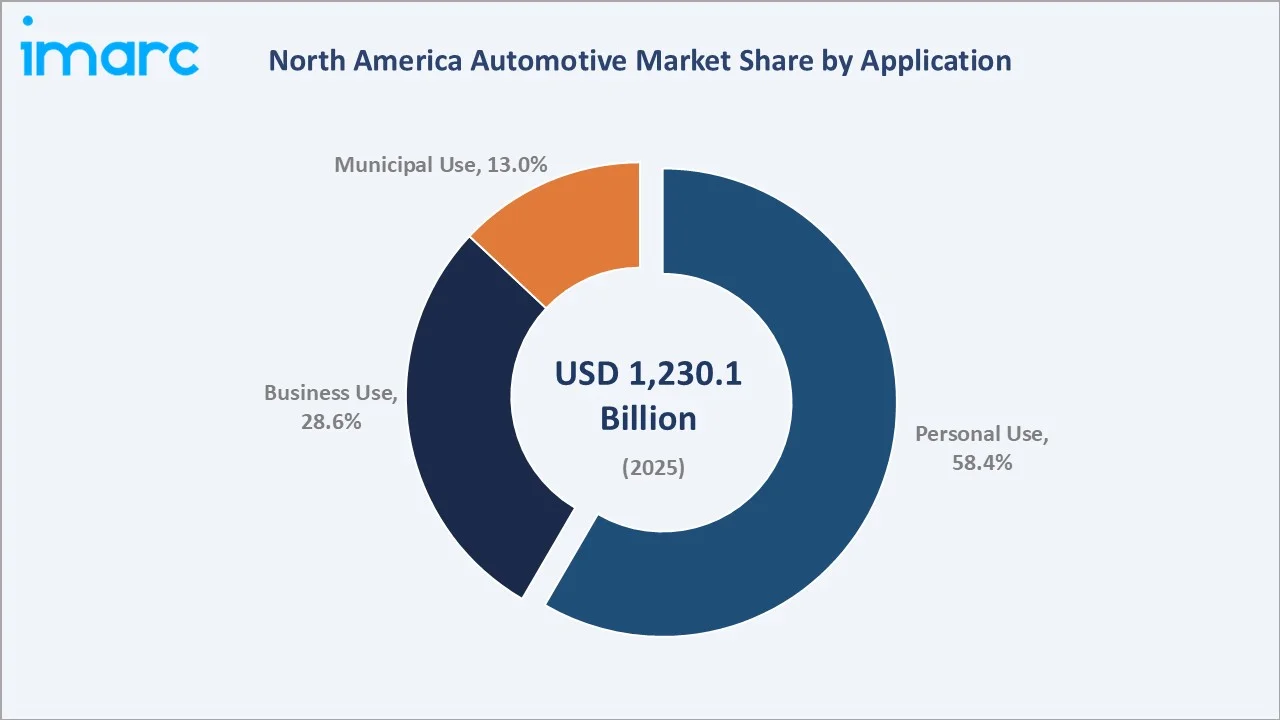

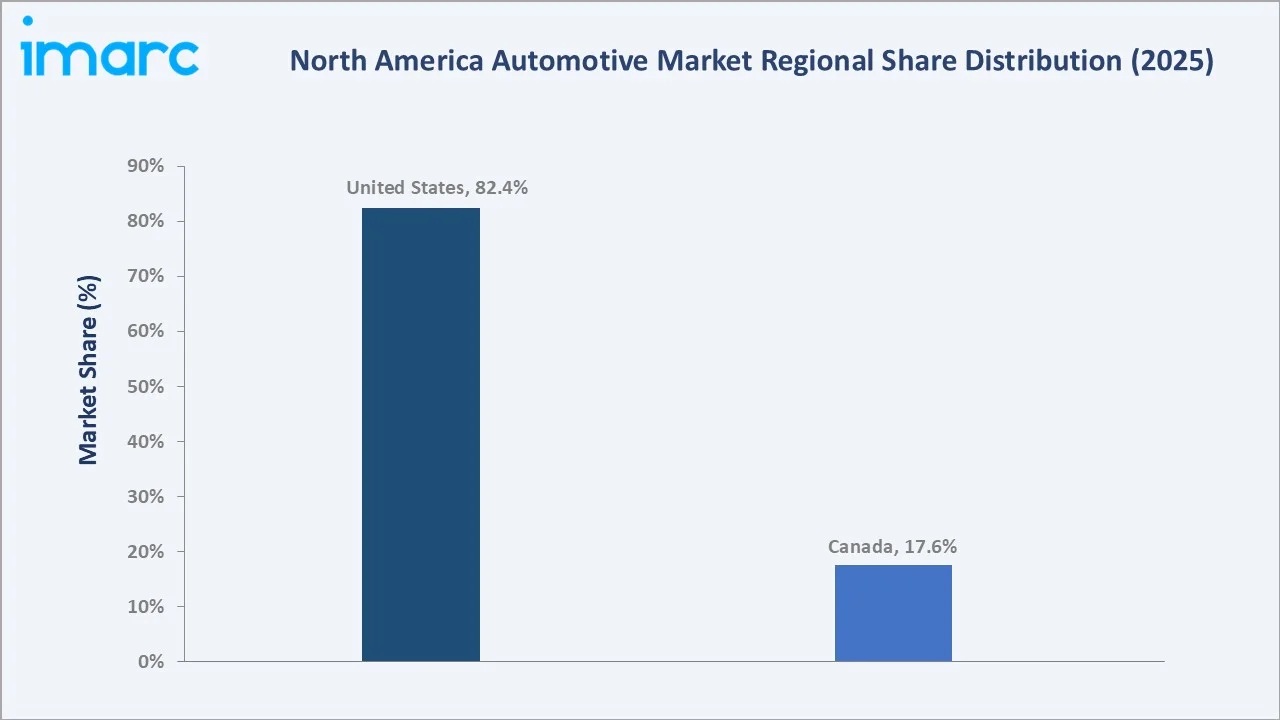

The North America automotive market size was valued at USD 1,230.1 Billion in 2025 and is projected to reach USD 1,977.3 Billion by 2034, exhibiting a CAGR of 5.42% during the forecast period 2026-2034. Surging consumer demand for personal mobility, accelerating federal EV incentive programmes under the Inflation Reduction Act, expanding fleet electrification commitments, and the rapid proliferation of software-defined vehicles are driving the North America automotive market growth. Passenger vehicles lead vehicle type at 72.5% in 2025, while Personal Use dominates the application segment at 58.4%. The United States accounts for 82.4% of North America's automotive revenue in 2025, the region's dominant country market.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 1,230.1 Billion |

|

Forecast Market Size (2034) |

USD 1,977.3 Billion |

|

CAGR (2026-2034) |

5.42% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Country |

United States (82.4% share, 2025) |

|

Fastest Growing Country |

Canada (accelerated EV manufacturing investment) |

|

Leading Type |

Passenger Vehicles (72.5%, 2025) |

|

Leading Application |

Personal Use (58.4%, 2025) |

To get more information on this market, Request Sample

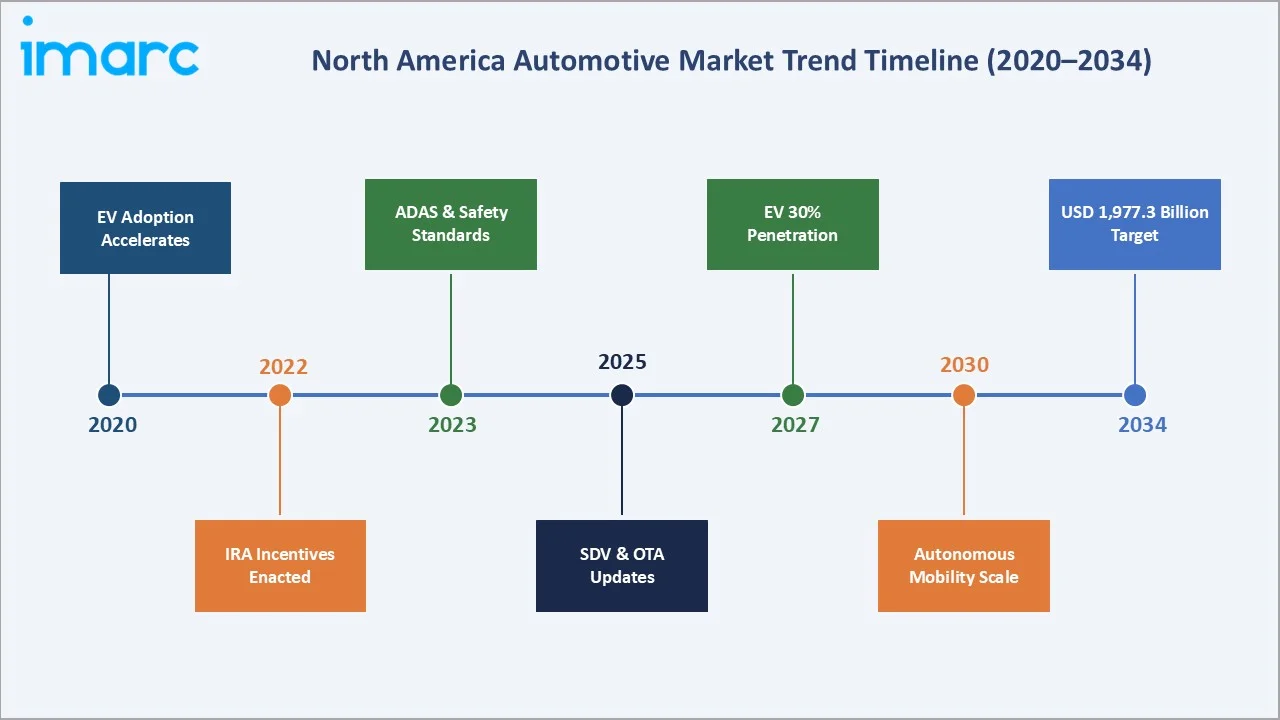

The North America automotive market growth trajectory from 2020 through 2034, contrasting a consistent historical expansion base against a sustained forecast curve powered by EV adoption, fleet electrification, and software-defined vehicle platform investment.

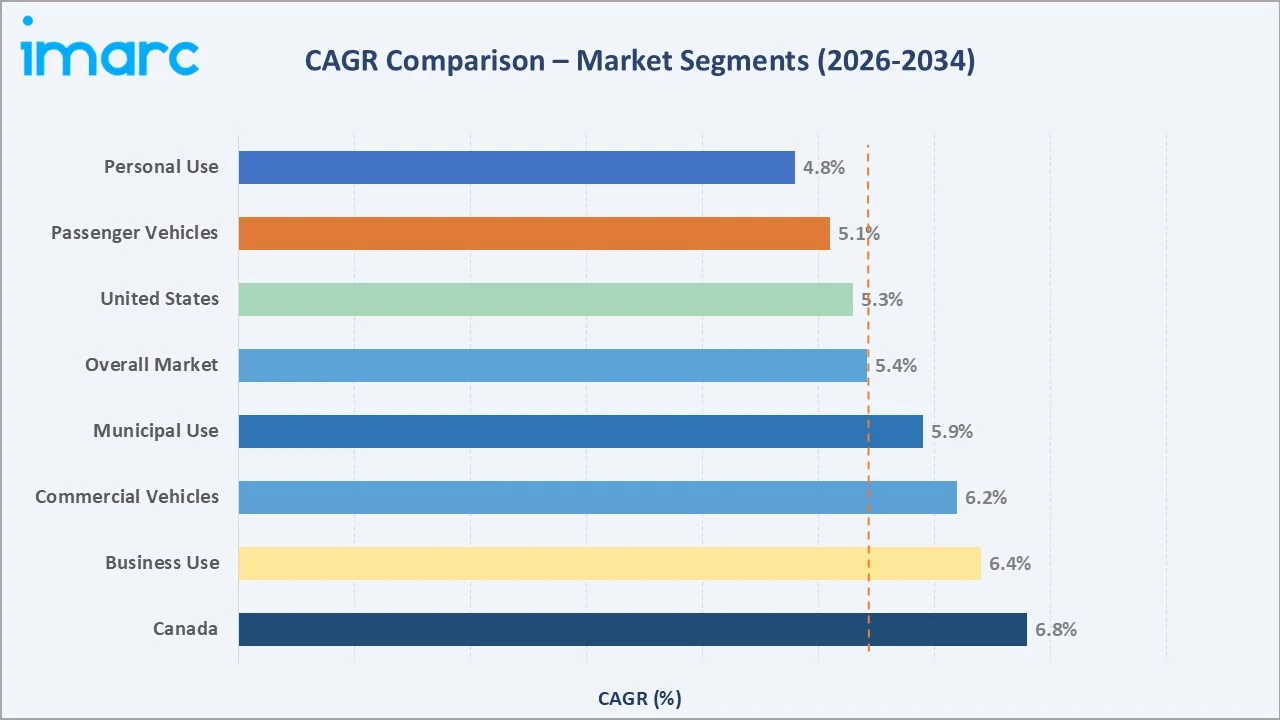

Segment-level CAGR comparisons highlighting commercial vehicles and business-use application as the fastest-growing sub-categories within the North America automotive market through 2034, with Canada emerging as the highest-growth country market.

Executive Summary

The North America automotive market is undergoing a fundamental structural transformation driven by the convergence of electrification, fleet modernisation, and digital vehicle technology. Valued at USD 1,230.1 Billion in 2025, the market is forecast to reach USD 1,977.3 Billion by 2034 at a CAGR of 5.42%.

Passenger vehicles command a 72.5% market share in 2025, anchored by sustained consumer demand for SUVs and crossovers. Commercial vehicles at 27.5% are experiencing accelerating electrification, driven by e-commerce last-mile delivery fleet commitments from Amazon, FedEx, and UPS. Personal use leads the application segment at 58.4%, reflecting North America's high per-capita vehicle ownership, averaging 1.9 vehicles per US household, while business use at 28.6% captures fleet, rental, and ride-hailing demand.

The United States dominates North America with 82.4% of regional revenue in 2025, supported by a deep OEM base and a national dealer network servicing registered vehicles.

Key Market Insights

|

Insight |

Data |

|

Largest Vehicle Type |

Passenger Vehicles – 72.5% share (2025) |

|

Leading Application |

Personal Use – 58.4% share (2025) |

|

Leading Country |

United States – 82.4% revenue share (2025) |

|

Fastest Growing Sub-segment |

Commercial EVs (~28% CAGR through 2034) |

|

Top Companies |

General Motors, Ford Motor Company, Stellantis NV, Tesla, Toyota Motor Corporation, Honda Motor Co., Ltd., Hyundai Motor Group |

Key Analytical Observations Supporting the Above Data:

- Passenger vehicles' 72.5% dominance in 2025 reflects the US and Canada's high-ownership vehicle culture.

- Commercial EV electrification is the highest-growth sub-segment, expanding at approximately 28% CAGR through 2034. Rivian's exclusive Amazon delivery van programme, Ford's E-Transit fleet, and Tesla's Semi truck entry are redefining commercial fleet purchasing standards across North America.

- Personal use's 58.4% application share reflects North America's suburban land-use patterns and limited public transit penetration outside major metropolitan areas.

- The United States' 82.4% country share reflects both consumer demand volume and production scale.

- Canada's 17.6% share is poised for rapid expansion.

North America Automotive Market Overview

The North America automotive industry encompasses the full lifecycle of passenger cars, light trucks, and commercial vehicles — from raw material sourcing, component manufacturing, and OEM assembly through to franchised dealership distribution, aftermarket services, and an expanding EV charging infrastructure sector. The region's automotive ecosystem spans two countries, with the United States as the dominant demand and production hub and Canada as an increasingly significant EV manufacturing centre.

Applications span personal transportation, corporate and government fleet procurement, municipal operations including public transit buses and emergency vehicles, and emerging autonomous mobility platforms. Macroeconomic enablers include consumer credit availability, sustained GDP per capita growth, demographic demand from Millennial and Gen-Z first-time buyers, and transformative policy frameworks.

Market Dynamics

To evaluate market opportunities, Request Sample

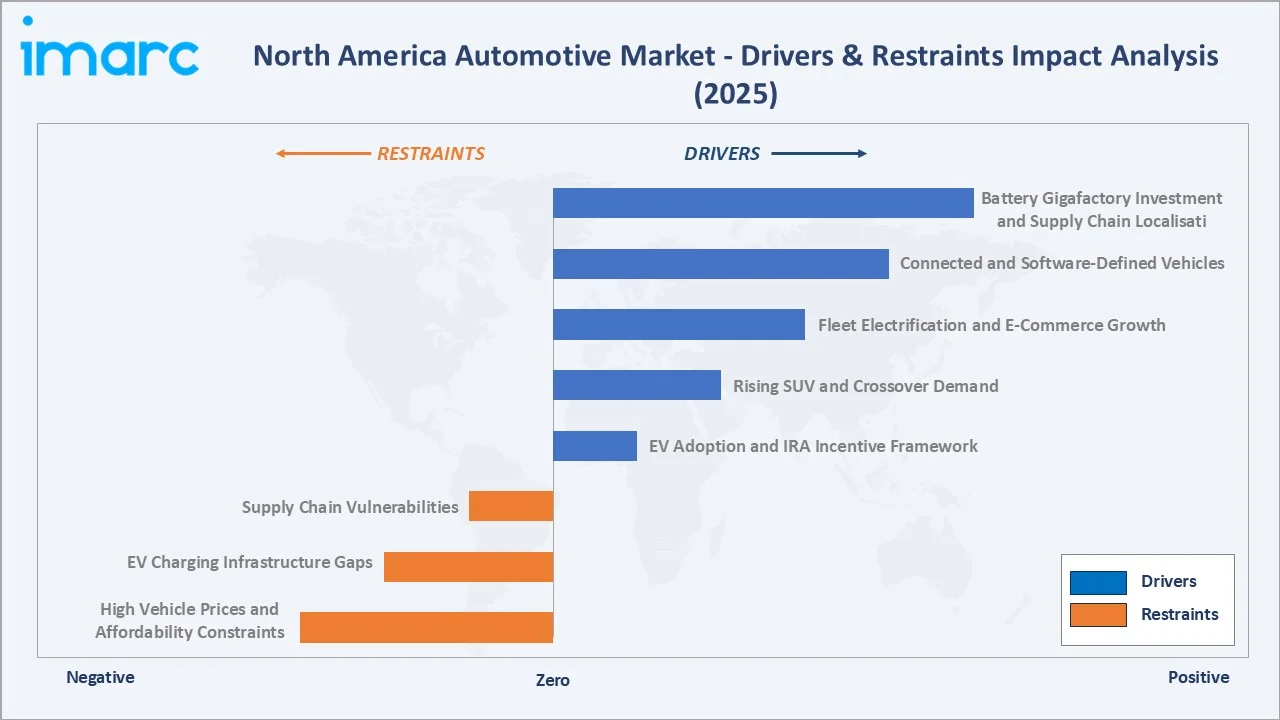

Market Drivers

- EV Adoption and IRA Incentive Framework: North American EV adoption continues to scale, supported by strong policy incentives. EVs accounted for ~9% of new U.S. vehicle sales in early 2024, reflecting steady year-on-year growth.

- Rising SUV and Crossover Demand: Light trucks (SUVs, pickups, crossovers) dominate U.S. vehicle demand, accounting for the majority of new vehicle sales and driving higher average selling prices. This shift toward premium and utility vehicles has structurally increased industry revenue per unit.

- Fleet Electrification and E-Commerce Growth: Commercial fleet electrification is accelerating, driven by logistics and last-mile delivery demand. Large-scale commitments (e.g., Amazon, UPS, FedEx) are catalyzing sustained EV demand in the commercial vehicle segment, reinforcing long-term volume visibility.

- Connected and Software-Defined Vehicles: Connected vehicle adoption is expanding rapidly, enabling recurring revenue streams. Automakers are increasingly monetizing software—e.g., subscription-based fleet and vehicle services, with Ford reporting ~630,000 paid software subscriptions in 2024.

Market Restraints

- High Vehicle Prices and Affordability Constraints: Elevated vehicle prices are constraining mass-market demand, with affordability increasingly dependent on long-duration financing. This disproportionately impacts entry-level segments and slows volume growth despite strong premium demand.

- EV Charging Infrastructure Gaps: Charging infrastructure expansion remains a bottleneck. Industry data indicates charging deployment is lagging EV growth, with roughly 1 public charger added per ~48 EVs in the U.S. This imbalance creates adoption friction, particularly outside urban areas.

- Supply Chain Vulnerabilities: The industry continues to face exposure to semiconductor shortages and battery raw material volatility. OEM investment announcements highlight ongoing efforts to localize supply chains, but cost instability remains a structural risk.

Market Opportunities

- Battery Gigafactory Investment and Supply Chain Localisation: Automakers and partners have announced >$100 billion in North American EV and battery investments, aimed at building localized supply chains and qualifying for IRA incentives. This shift reduces dependency on global supply chains and strengthens regional manufacturing ecosystems.

- Software-Defined Vehicle Revenue Models: The transition toward software-enabled vehicles is unlocking recurring revenue streams via OTA updates, Subscription features, and Fleet management platforms. OEMs are increasingly positioning software as a long-term profit pool beyond vehicle sales.

- Autonomous Mobility Commercialisation: Autonomous vehicle deployments (e.g., robotaxi pilots) are advancing in select U.S. cities, positioning North America as a leader in early commercialization and creating a new long-term mobility revenue category.

Market Challenges

- Regulatory Complexity Across Jurisdictions: Diverging federal and state-level regulations—particularly zero-emission mandates—create compliance complexity for OEMs operating across multiple markets.

- Workforce Transition from ICE to EV Manufacturing: The shift from internal combustion engine to EV manufacturing requires retraining over 100,000 workers in battery manufacturing and EV assembly skills. OEMs managing dual-platform ICE-to-EV production transitions face concurrent labour cost and productivity risks that constrain near-term margin expansion.

Emerging Market Trends

1. Software-Defined Vehicle (SDV) Architecture Redefining the Automotive Model

North American OEMs are shifting to centralized, software-defined architectures that replace legacy ECUs with high-performance compute platforms. Ford Motor Company (E3), General Motors (VIP), and Tesla (integrated stack) are leading this transition, enabling over-the-air updates and feature-on-demand models. This marks a structural shift toward lifecycle monetization through software, data, and connected services.

2. Electric Vehicle Ecosystem and Charging Infrastructure Expansion

EV adoption in the U.S. is scaling steadily, supported by federal funding under the Bipartisan Infrastructure Law led by the U.S. Department of Transportation. Charging infrastructure expansion by ChargePoint, EVgo, and Tesla is improving accessibility, though deployment remains uneven geographically. The combined push of policy support and network growth is critical to enabling mass-market EV adoption.

3. Advanced Driver Assistance Systems (ADAS) Mainstream Proliferation

ADAS features are rapidly becoming standard across North American vehicles, driven by regulatory mandates and safety demands. The National Highway Traffic Safety Administration requirement for Automatic Emergency Braking by 2029 is accelerating adoption across price segments. This is structurally increasing demand for sensing technologies such as radar and cameras, with selective LiDAR integration in higher-end systems.

4. Subscription-Based Mobility and Connected Services Revenue

OEMs are scaling subscription-based connected services to generate recurring revenue beyond vehicle sales. Platforms like General Motors’ OnStar, along with offerings from Ford Motor Company and Stellantis, provide features such as remote access, in-vehicle connectivity, and navigation upgrades. This model is redefining automotive revenue streams toward continuous customer engagement.

5. Reshoring and North American Supply Chain Localisation

Policy frameworks such as the CHIPS and Science Act and the Inflation Reduction Act are accelerating the localisation of semiconductor and battery supply chains. OEMs and suppliers are investing in domestic manufacturing to meet regulatory requirements and reduce geopolitical risk. This transition is strengthening regional self-sufficiency while supporting long-term EV ecosystem growth.

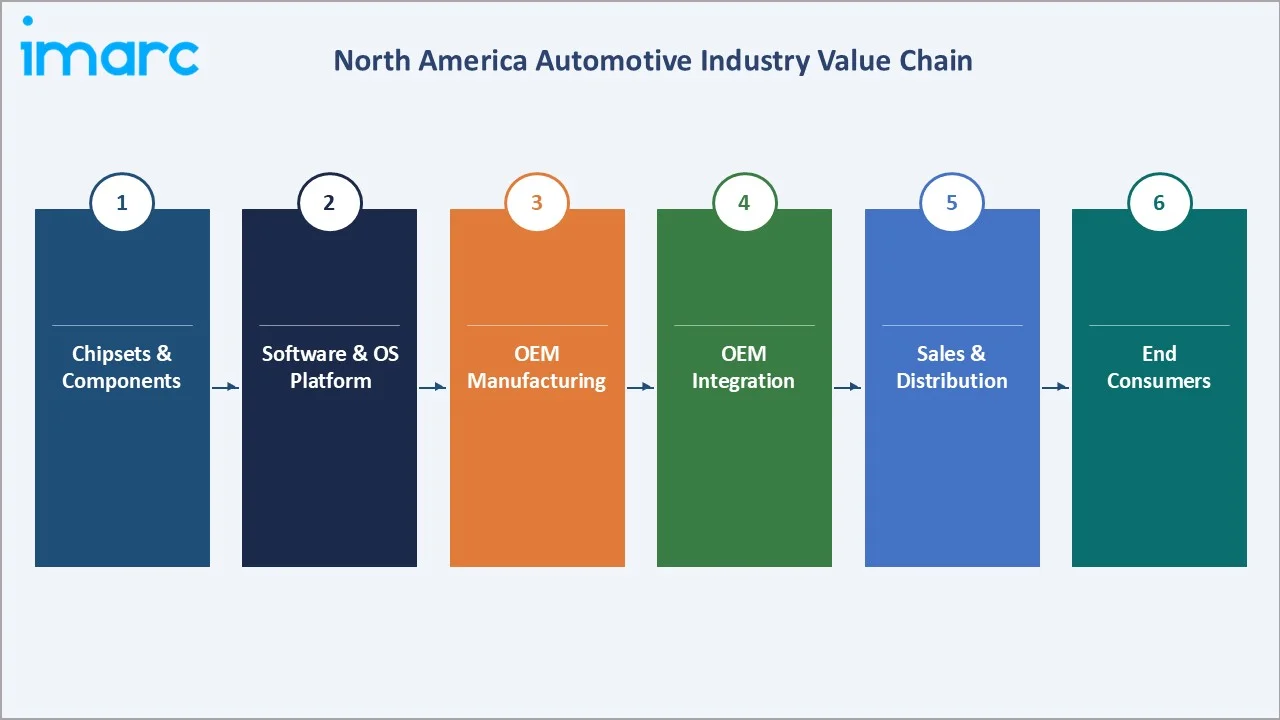

Industry Value Chain Analysis

The North America automotive value chain spans six integrated stages from raw material extraction through end-user vehicle ownership and aftermarket servicing. Each stage is undergoing varying degrees of transformation driven by electrification, digitalisation, and supply chain localisation.

|

Stage |

Key Players / Examples |

|

Chipsets & Components |

Specialized raw material extractors and processors (lithium, steel, aluminium), alongside advanced battery cell and semiconductor manufacturers supplying the foundational inputs for EV and connected vehicle systems. |

|

Software & OS Platform |

Semiconductor and SoC designers, GPU/AI chip developers, and automotive-grade OS and infotainment platform providers enabling vehicle compute, connectivity, and in-cabin digital experiences. |

|

OEM Manufacturing |

Established legacy automakers and pure-play EV manufacturers are responsible for full vehicle design, engineering, assembly, and brand ownership across combustion, hybrid, and electric powertrains. |

|

OEM Integration |

OEM-owned EV-specific sub-brands and dedicated manufacturing platforms that consolidate electrification R&D, battery integration, and regional production within parent OEM structures. |

|

Sales & Distribution |

Large franchise dealership groups and independent auto retailers, alongside direct-to-consumer EV sales models that bypass traditional dealer networks for streamlined purchasing experiences. |

|

End Consumers |

Private individual buyers, large e-commerce and logistics fleet operators, and public sector transit authorities are driving demand across personal mobility, last-mile delivery, and mass transit segments. |

OEM manufacturers occupy the highest strategic value position in the North America automotive value chain, integrating platforms, powertrains, software, and connectivity hardware into complete vehicle solutions. This structural position is under challenge from battery and software companies seeking greater direct OEM engagement, and from OEMs internalising battery manufacturing and software development to capture a larger share of EV lifecycle value.

Technology Landscape in the North America Automotive Industry

Electric Powertrain and Battery Technology

Lithium-ion battery technology continues to advance, with next-generation cells approaching higher energy densities that enable extended EV range and improved performance. General Motors’ Ultium platform, developed with LG Energy Solution, supports a broad EV lineup, while Toyota and QuantumScape are progressing toward commercializing solid-state batteries later this decade.

Autonomous Vehicle and ADAS Technology

North America leads in autonomous driving development, with Waymo accumulating tens of millions of real-world autonomous miles and expanding robotaxi operations. Concurrently, advancements from Qualcomm, Mobileye, and NVIDIA are enabling scalable Level 2+ ADAS features through high-performance, centralized compute platforms.

Connected Vehicle, V2X, and 5G Connectivity

Connected vehicle adoption is accelerating with the expansion of 5G integration and V2X pilot deployments supported by the U.S. Department of Transportation. Automakers are embedding connectivity and OTA capabilities as standard features, while projections from GSMA indicate strong growth in connected vehicles, enabling data-driven services and new monetization opportunities.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Type |

Passenger |

72.5% |

2025 |

|

Application |

Personal Use |

58.4% |

2025 |

|

Country |

United States |

82.4% |

2025 |

By Type

To access detailed market analysis, Request Sample

Passenger vehicles command a 72.5% majority share in 2025, reflecting the entrenched consumer preference for personal vehicle ownership across the United States and Canada. The passenger segment is benefiting from the industry-wide shift toward SUVs, crossovers, and electric sedans, collectively accounting for approximately 80% of regional battery electric passenger vehicle volume.

Commercial vehicles at 27.5% in 2025 are experiencing an accelerating electrification transition. The segment encompasses light commercial vans, medium-duty trucks, and heavy-duty freight vehicles. Electric light commercial vehicles by Rivian (Amazon's exclusive delivery partner), Ford's E-Transit programme, and Mercedes-Benz eSprinter are redefining last-mile logistics fleet standards. Heavy-duty electric trucks from Tesla (Semi) and Kenworth's T680E are entering fleet testing phases, with volume ramp anticipated through 2027-2028.

By Application

Personal use leads at 58.4% in 2025, driven by North America's suburban land-use patterns, an average US household vehicle ownership of 1.9 vehicles, and cultural preference for private mobility over public transit across non-metropolitan geographies. EV adoption within the personal use segment is most advanced in California, where ZEV penetration exceeded 25% of new personal vehicle registrations in 2024, serving as a leading indicator for national personal EV adoption trajectories.

Business use at 28.6% encompasses corporate fleet purchases, logistics operators, rental car companies, and ride-hailing platforms. Municipal use at 13.0% covers police vehicles, public transit buses, ambulances, and infrastructure fleets.

Regional Market Insights

|

Country |

Share (2025) |

Key Growth Drivers |

|

United States |

82.4% |

IRA EV incentives, consumer SUV demand, Tesla SDV model, ADAS mandates, fleet electrification |

|

Canada |

17.6% |

EV gigafactory investments (VW, Honda, Stellantis), ZEV mandate, CUSMA export platform, fleet modernisation |

The United States commands an 82.4% share of the North America automotive market revenue in 2025, underpinned by light vehicle sales and the country's deep OEM infrastructure encompassing General Motors, Ford Motor Company, Stellantis NV, and Tesla, alongside transplant production from Toyota, Honda, Hyundai, and BMW.

Canada holds 17.6% of North American automotive revenue in 2025 and is undergoing its most significant structural transformation in decades. Ontario is emerging as the continent's most active EV manufacturing investment destination, with Volkswagen's PowerCo battery gigafactory in St. Thomas.

Competitive Landscape

|

Company Name |

Key Platform / Brand |

Market Position |

Core Strength |

|

General Motors |

Chevrolet, GMC, Cadillac, Buick |

Leader |

Ultium EV platform, OnStar connected services, US volume scale |

|

Ford Motor Company |

Ford, Lincoln |

Leader |

F-150 Lightning, E-Transit commercial EV, BlueOval SDV platform |

|

Stellantis NV |

Jeep, Ram, Dodge, Chrysler |

Challenger |

Multi-brand portfolio, Windsor/Brampton EV manufacturing |

|

Tesla |

Tesla |

Emerging |

BEV share >50%, Full Self-Driving platform, NACS network |

|

Toyota Motor Corporation |

Lexus, Toyota |

Leader |

Hybrid leadership, bZ4X BEV, solid-state battery pipeline |

|

Honda Motor Co., Ltd. |

Honda, Acura |

Challenger |

Alliston EV investment, Honda Prologue BEV, North American base |

|

Hyundai Motor Group |

Kia,Hyundai |

Challenger |

Ioniq 5/6/9, Metaplant Georgia factory, aggressive EV pricing |

|

Volkswagen Group |

Audi, Porsche, Volkswagen |

Challenger |

ID.4 Chattanooga production, PowerCo Canada battery plant |

The North America automotive competitive landscape is characterised by a small number of legacy OEM volume leaders commanding deep dealer networks and fleet relationships, alongside Tesla's disruptive direct-to-consumer, software-first model and an increasingly competitive set of Asian transplant manufacturers. The EV transition is the primary competitive battleground, with traditional Detroit-Three market share under structural pressure from Tesla in passenger BEV and from Hyundai-Kia in mainstream EV price segments.

Key Company Profiles

General Motors

General Motors operates assembly facilities across Michigan, Indiana, Kansas, Tennessee, and Ontario and manages the Chevrolet, GMC, Cadillac, and Buick brand portfolio.

- Product & Platform Portfolio: Ultium EV platform (Chevrolet Equinox EV, Silverado EV, Blazer EV, GMC Sierra EV, Cadillac LYRIQ/CELESTIQ); OnStar connected services (15 million active subscribers); Super Cruise hands-free driving system.

- Recent Developments: In June 2025, General Motors announced plans to invest about $4 billion over the next two years in its domestic manufacturing plants to increase U.S. production of both gas and electric vehicles.

- Strategic Focus: GM's strategy centres on Ultium platform scalability targeting 400,000+ EV units annually, expansion of OnStar software subscription revenue, and maintaining commercial dominance in the light truck segment with the electrified Silverado and Sierra pickup lines through the forecast period.

Tesla

Tesla is the undisputed leader in North American battery electric vehicles. Tesla's vertically integrated model, encompassing battery cell manufacturing, vehicle assembly, direct-to-consumer sales, and a proprietary Supercharger network, creates structural competitive advantages that legacy OEMs are working to replicate over multi-year investment horizons.

- Product & Platform Portfolio: Model 3, Model Y (best-selling BEV globally in 2023), Model S/X, Cybertruck, Tesla Semi; Full Self-Driving (FSD) software subscription; Supercharger network (25,000+ US NACS connectors adopted industry-wide).

- Recent Developments: In September 2024, Eaton announced a planned collaboration with Tesla designed to boost the functionality and adoption of home energy storage and solar installations in North America.

- Strategic Focus: Tesla's strategy is anchored in Full Self-Driving software monetisation targeting a commercial robotaxi service launch, energy storage expansion through Megapack and Powerwall, and a next-generation USD 25,000 affordable EV platform planned for volume production from 2025-2026.

Stellantis NV

Stellantis manages one of North America's broadest OEM brand portfolios across Jeep, Ram, Dodge, Chrysler, Fiat, and Alfa Romeo. North American operations include assembly facilities in Michigan, Indiana, Illinois, and Ontario, with the Windsor battery plant developed with LG Energy Solution operational from 2024.

- Product & Platform Portfolio: Ram ProMaster EV commercial van, Jeep Wrangler 4xe PHEV, Jeep Recon BEV, Dodge Charger Daytona EV; STLA Large, Medium, and Frame EV platforms across the brand portfolio.

- Recent Developments: In October 2025, Stellantis announced its plans to invest $13 billion over the next four years to grow its business in the critical United States market and to increase its domestic manufacturing footprint.

- Strategic Focus: Stellantis N.V.centres on a multi-energy "freedom of choice" approach — balancing ICE, hybrid, and BEV offerings — while prioritising Jeep and Ram brand recovery across North America.

Market Concentration Analysis

The North America automotive market exhibits high concentration at the OEM level. The top six manufacturers – General Motors, Ford Motor Company, Stellantis NV, Toyota Motor Corporation, Honda Motor Co., Ltd., and Hyundai Motor Group– collectively account for approximately 73% of light vehicle sales in the US in 2024. Tesla, despite its BEV segment dominance at 50%+ of US BEV sales, holds approximately 4% of total US light vehicle sales, reflecting the still-emerging overall EV penetration level of 8.5%.

Consolidation pressures are intensifying among Tier-1 automotive suppliers, where EV platform complexity and software-defined vehicle R&D requirements demand investment levels that mid-size suppliers cannot sustain independently. Strategic alliances, including Aptiv's Motional autonomous driving JV with Hyundai, Bosch-Qualcomm's Snapdragon Ride Flex collaboration, and the Stellantis-Samsung SDI battery manufacturing partnership, are reshaping the supplier competitive landscape through 2034.

Investment & Growth Opportunities

Fastest-Growing Segments

Commercial EV electrification is emerging as one of the fastest-growing segments, driven by last-mile logistics and fleet decarbonization. Rivian’s electric delivery van partnership with Amazon, along with Ford Motor Company’s E-Transit and Mercedes-Benz eSprinter programs, highlight strong fleet adoption momentum. In parallel, software-enabled services are scaling rapidly, with Ford Motor Company and General Motors reporting over USD 1 billion annual revenue from connected and digital services, validating recurring revenue models.

Emerging Market Expansion

Canada is rapidly positioning itself as a key EV manufacturing hub, particularly in Ontario. Investments from Volkswagen, Honda, and Stellantis—spanning battery plants and EV assembly—are supported by significant federal and provincial incentives. Trade alignment under CUSMA further strengthens Canada’s role as a supply base for the U.S. market.

Venture & Private Investment Trends

Investment in automotive technology remains concentrated in electrification, autonomy, and charging infrastructure. Waymo raised USD 5.6 billion in 2024 to scale autonomous driving, while companies such as QuantumScape and Solid Power continue to attract funding for next-generation batteries. Charging networks, including ChargePoint and EVgo, are also expanding with institutional capital.

Future Market Outlook (2026-2034)

The North America automotive market forecast projects sustained value expansion from USD 1,230.1 Billion in 2025 to USD 1,977.3 Billion by 2034 at a CAGR of 5.42%, a near-60% value growth over nine years underpinned by EV penetration scaling, rising average transaction prices, and the emergence of software subscription and autonomous mobility revenue layers above traditional vehicle hardware economics.

The North American automotive market is undergoing a structural transformation driven by electrification, software centralization, and autonomous mobility. EV adoption is expected to rise significantly under policy support from the Inflation Reduction Act and regulatory pressure from the Environmental Protection Agency, reshaping the powertrain and supplier ecosystem. At the same time, software-defined vehicle architectures led by OEMs such as General Motors, Ford Motor Company, and Tesla—alongside platform providers like Qualcomm and NVIDIA—are shifting industry value toward integrated compute and recurring software revenue. Concurrently, autonomous mobility led by Waymo is moving toward early commercialization, while Canada is emerging as a critical EV manufacturing hub under CUSMA, reinforcing a more localized and software-driven automotive ecosystem.

Research Methodology

Primary Research

Primary research encompassed structured interviews conducted in 2024-2025 with North American automotive industry stakeholders, including product strategy directors at major US and Canadian OEMs, fleet procurement managers at logistics and municipal operators, EV charging infrastructure executives, battery manufacturing programme leaders, and institutional investors in automotive technology. Primary insights validated market sizing, segmentation estimates, EV adoption timelines, and competitive positioning assessments across both the US and Canadian markets.

Secondary Research

Secondary sources include US Bureau of Economic Analysis automotive sector data, NHTSA vehicle production and registration statistics, Natural Resources Canada transportation data, IEA Global EV Outlook 2024, WardsAuto vehicle sales data, J.D. Power purchase intention and satisfaction surveys, BloombergNEF EV market outlook, US DOE Alternative Fuels Data Center, company annual reports and investor presentations, and trade publications including Automotive News, Car and Driver, and SAE International.

Forecasting Models

Market size estimations and growth projections were derived using a combination of top-down and bottom-up forecasting models, incorporating US and Canadian GDP growth trajectories, consumer credit and spending patterns, EV adoption S-curve projections, fleet electrification mandate timelines, and historical automotive market evolution patterns. Scenario analysis encompassing base, optimistic, and conservative cases was conducted to account for macroeconomic uncertainty, policy evolution risk, and EV adoption pace variability.

North America Automotive Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Types Covered | Passenger, Commercial Vehicles |

| Applications Covered | Personal Use, Municipal Use, Business Use |

| Countries Covered | United States, Canada |

| Companies Covered | General Motors, Ford Motor Company, Stellantis NV, Tesla, Toyota Motor Corporation, Honda Motor Co., Ltd., Hyundai Motor Group, Volkswagen Group, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the North America automotive market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the North America automotive market.

- Porter's Five Forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the North America automotive industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the North America Automotive Market Report

The North America automotive market was valued at USD 1,230.1 Billion in 2025.

The market is projected to reach USD 1,977.3 Billion by 2034, growing at a CAGR of 5.42% during 2026-2034.

Passenger vehicles lead with a 72.5% share in 2025.

The United States dominates with an 82.4% share in 2025, backed by 15.9 million light vehicle sales in 2024.

Key drivers include IRA EV tax credits, rising SUV demand, commercial fleet electrification mandates, connected vehicle software revenue expansion, and EV manufacturing investments across the region.

Electric commercial vehicles are the fastest-growing sub-segment at approximately 28% CAGR through 2034.

Leading companies include General Motors, Ford Motor Company, Stellantis NV, Tesla, Toyota Motor Corporation, Honda Motor Co., Ltd., Hyundai Motor Group, and Volkswagen Group.

Personal use accounts for 58.4% of the North America automotive market in 2025.

Canada holds 17.6% of North American revenue in 2025.

Commercial vehicles at 27.5% in 2025 will be reshaped by electrification.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)