Oncology Molecular Diagnostics Market Size, Share, Trends and Forecast by Cancer Type, Product, Technology, End-User, and Region, 2026-2034

Oncology Molecular Diagnostics Market Size, Share, Trends & Forecast (2026-2034)

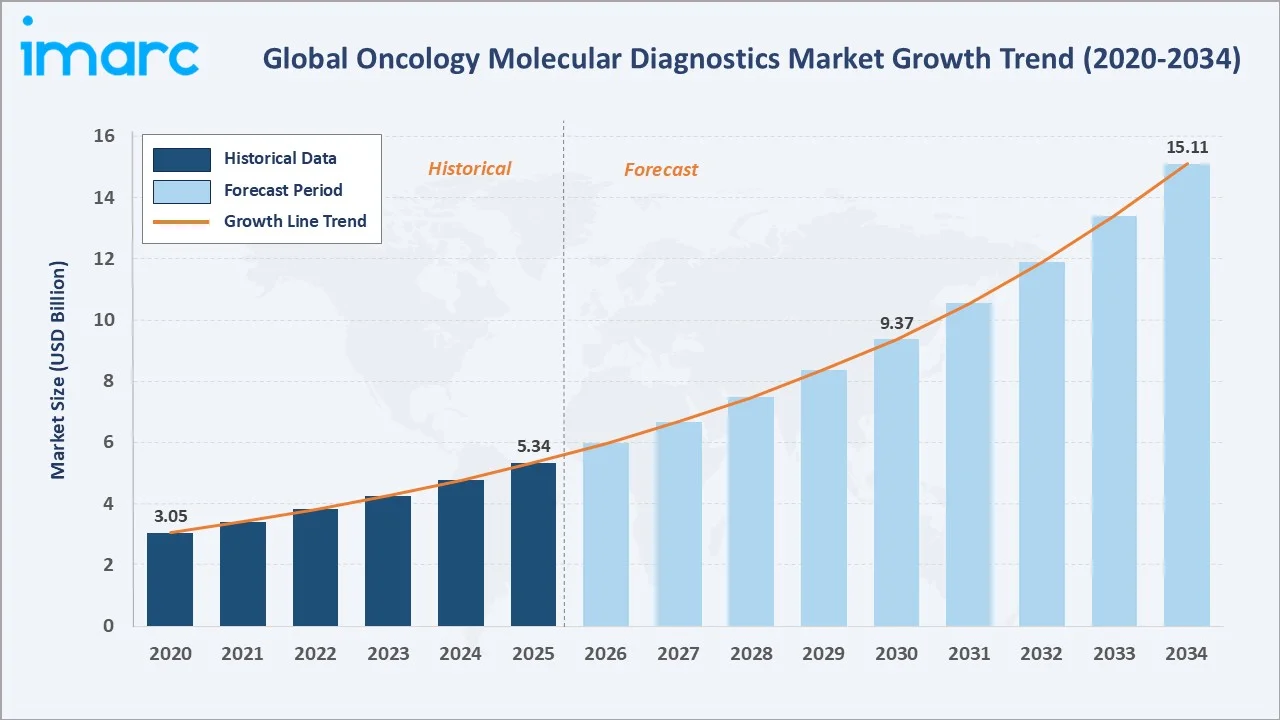

The global oncology molecular diagnostics market reached USD 5.34 Billion in 2025 and is projected to reach USD 15.11 Billion by 2034, exhibiting a CAGR of 11.87% during 2026-2034. Growth is anchored by the rising global cancer burden, expanding precision oncology and targeted therapy adoption, scaling liquid biopsy and multi-cancer early detection platforms, integration of AI-driven pathology, and supportive regulatory and reimbursement environments across major markets.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 5.34 Billion |

|

Market Forecast (2034) |

USD 15.11 Billion |

|

CAGR (2026-2034) |

11.87% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

Molecular diagnostics in oncology enable the detection of cancer-specific genetic mutations, biomarkers, and gene expression profiles, facilitating early diagnosis, personalized treatment strategies, and improved patient outcomes.

To get more information on this market, Request Sample

Innovations such as next-generation sequencing (NGS), liquid biopsies, and companion diagnostics are transforming cancer care by allowing clinicians to tailor therapies based on individual molecular profiles.

Executive Summary

The global oncology molecular diagnostics market accounted for USD 5.34 Billion in 2025 and is expected to reach USD 15.11 Billion by 2034. It is among the highest-growth precision-medicine categories in healthcare, expanding at an 11.87% CAGR through 2034. Growth is anchored by the rising global cancer burden, accelerating precision oncology and targeted therapy prescribing, scaling liquid biopsy and multi-cancer early detection platforms, and growing AI-driven pathology and bioinformatics integration.

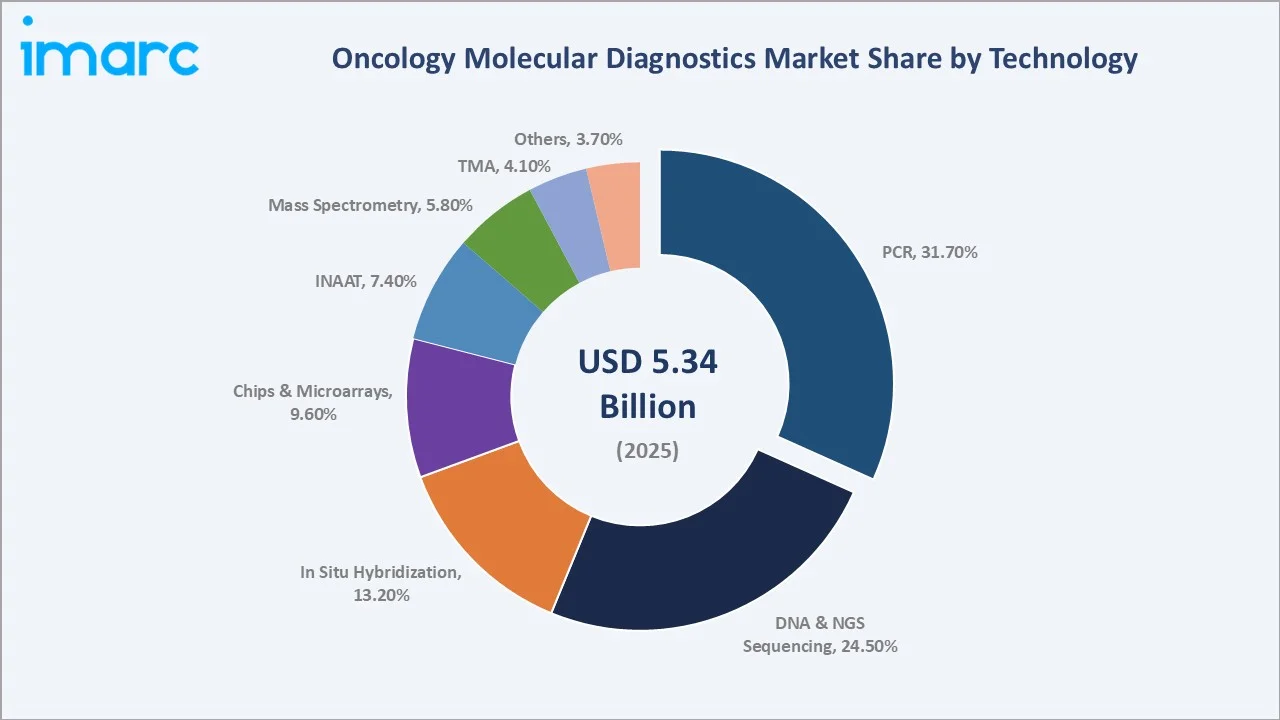

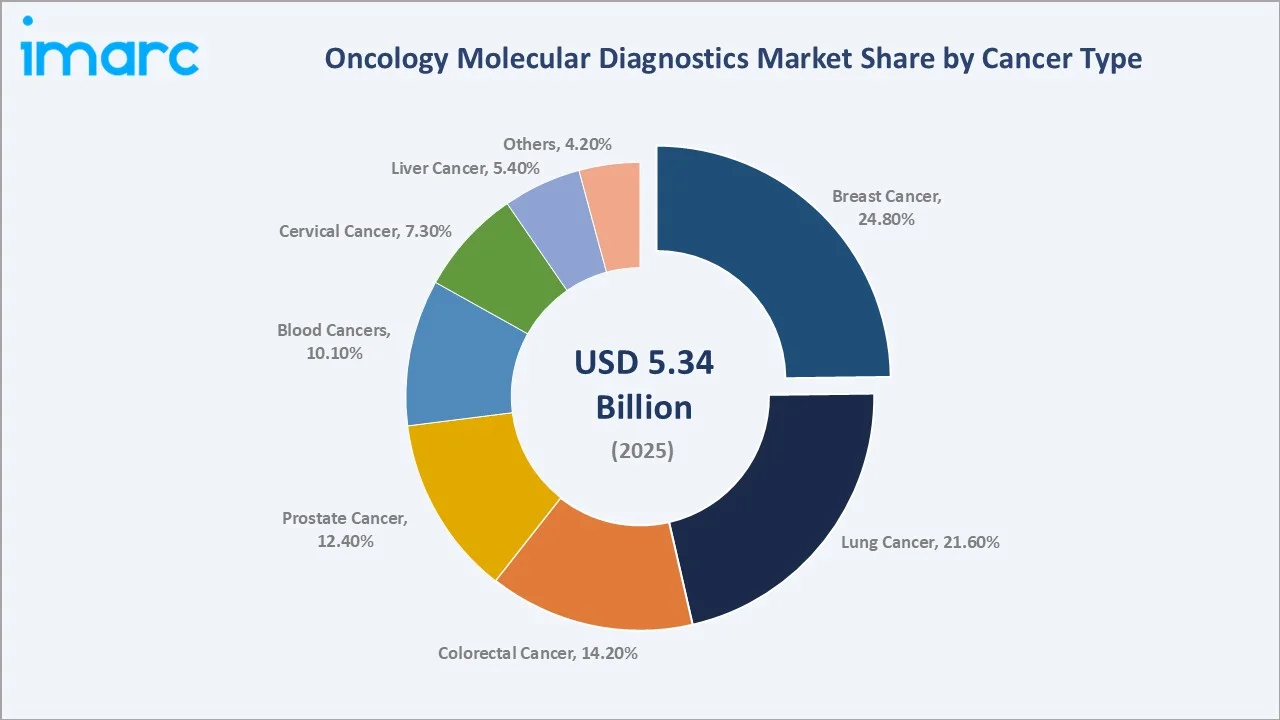

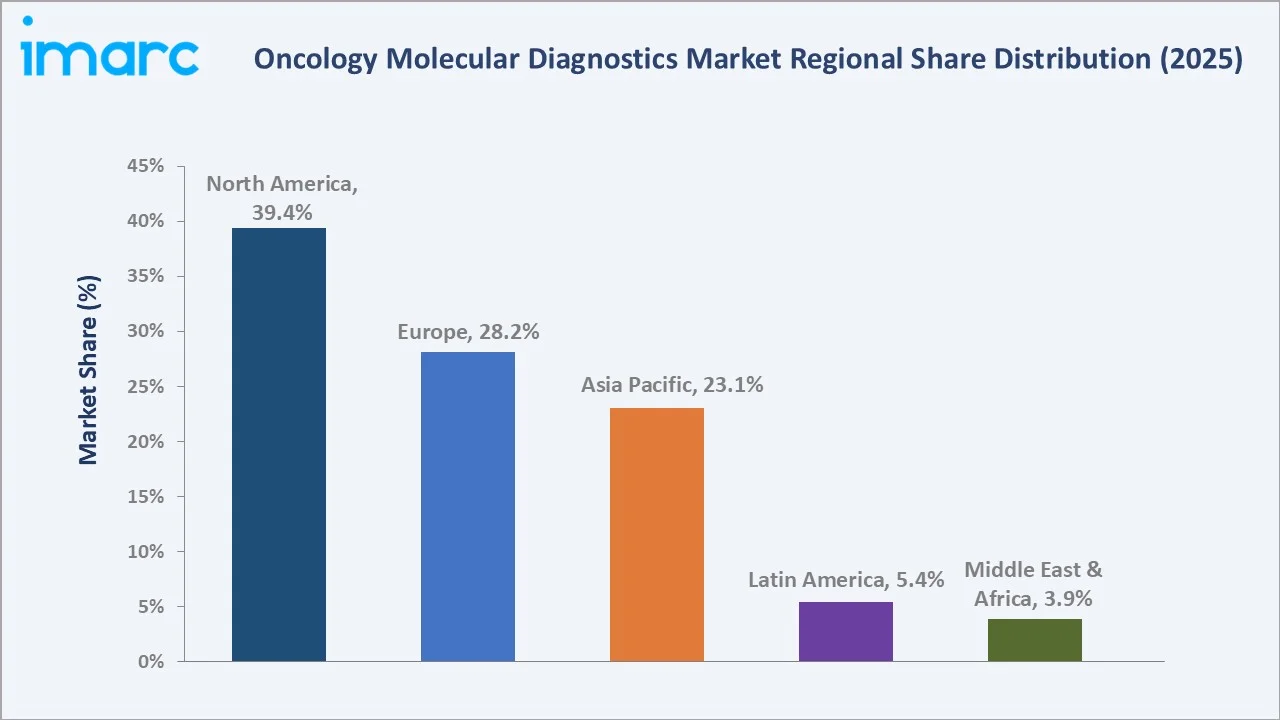

The market is moderately consolidated, with top players including F. Hoffmann-La Roche Ltd, Illumina, Inc., Thermo Fisher Scientific Inc., QIAGEN, and Hologic, Inc. collectively accounting for approximately 48% of revenue in 2025. Polymerase Chain Reaction (PCR) dominates the technology mix at 31.7%, breast cancer leads cancer-type segmentation at 24.8%, and North America anchors regional share at 39.4%.

Key milestones include QIAGEN's September 2024 launch of the QIAcuityDx Digital PCR System for clinical oncology testing, expanding its digital PCR portfolio into the North American and European Union clinical testing markets, and continued FDA and EMA approval expansion for companion diagnostics, NGS-based comprehensive genomic profiling, and minimal residual disease (MRD) testing assays.

Key Market Insights

|

Indicator |

Value (2025) |

|

Leading Technology |

Polymerase Chain Reaction (PCR) (31.7%) |

|

Leading Cancer Type |

Breast Cancer (24.8%) |

|

Fastest-Growing Technology |

DNA & NGS Sequencing (~14.5% CAGR) |

|

Largest Region |

North America (39.4%) |

|

Key Players (Top 5) |

F. Hoffmann-La Roche Ltd, Illumina, Inc., Thermo Fisher Scientific Inc., QIAGEN, Hologic, Inc. |

Key Analytical Observations Supporting the Above Data:

- Polymerase Chain Reaction (PCR) accounts for 31.7% of the oncology molecular diagnostics market in 2025, anchored by widespread clinical adoption of qPCR and digital PCR for mutation detection, gene expression profiling, MRD monitoring, and companion diagnostic testing across breast, lung, colorectal, and other solid tumor indications.

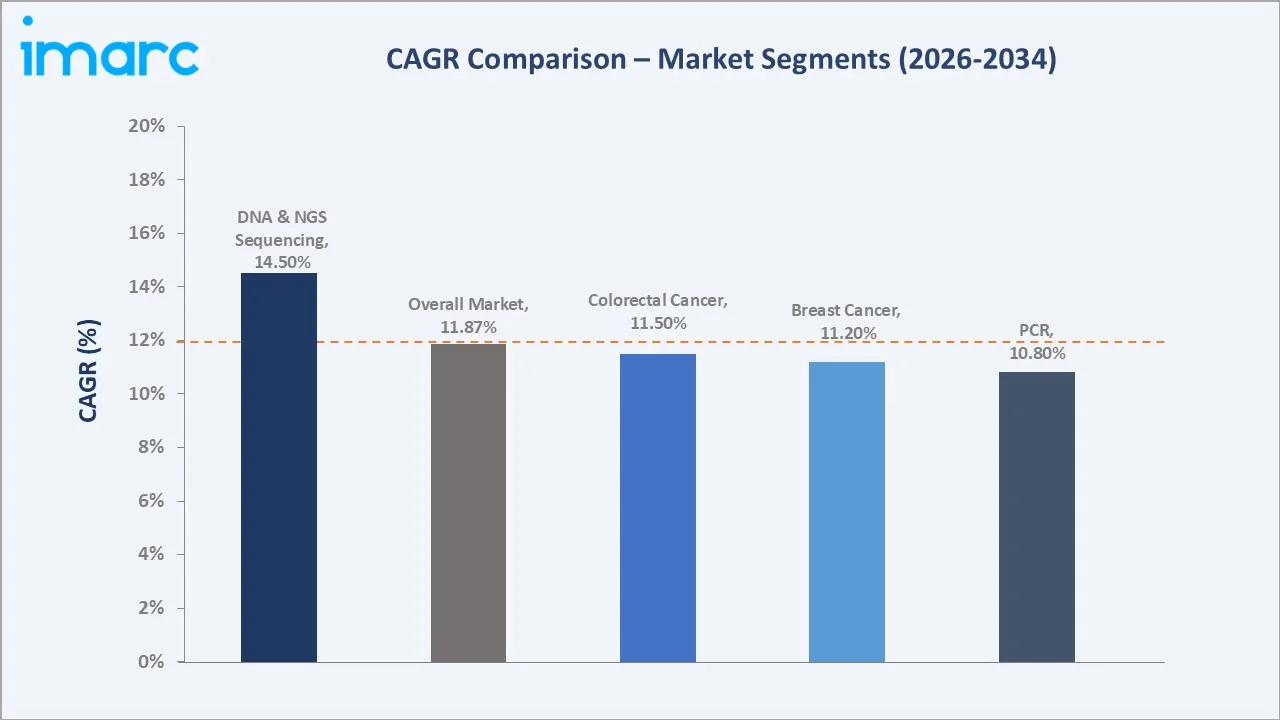

- DNA and NGS sequencing at 24.5% (2025) represents the fastest-growing technology segment, projected to grow at approximately 14.5% CAGR through 2034, supported by comprehensive genomic profiling for solid tumors, liquid biopsy applications, and multi-cancer early detection programs.

- Breast cancer leads cancer-type segmentation at 24.8% in 2025, supported by HER2/neu, BRCA1/2, Oncotype DX, and MammaPrint multi-gene assays anchoring treatment selection. Lung cancer at 21.6% reflects high comprehensive genomic profiling adoption for EGFR, ALK, KRAS, and PD-L1 biomarker testing.

- Colorectal cancer at 14.2% and prostate cancer at 12.4% leverage RAS, BRAF, MSI/MMR, and PCA3 biomarker assays. Blood cancers at 10.1% include comprehensive genomic profiling and MRD testing for AML, ALL, and lymphoma indications.

- North America's 39.4% regional share reflects the United States as the world's largest oncology molecular diagnostics market, supported by Medicare and commercial reimbursement, FDA companion diagnostic approvals, and the global concentration of leading market players including Roche, Illumina, Thermo Fisher, and Hologic.

Oncology Molecular Diagnostics Market Overview

Oncology molecular diagnostics refers to the laboratory testing of nucleic acids (DNA, RNA) and protein biomarkers to detect, characterize, and monitor cancer at the molecular level. The category spans companion diagnostics (CDx), tumor profiling assays, liquid biopsy circulating tumor DNA (ctDNA) tests, minimal residual disease (MRD) monitoring, Multi-Cancer Early Detection (MCED), pharmacogenomic-guided therapy selection, and hereditary cancer risk assessment.

The market is supported by the rising global cancer burden, with the global incidence of cancer projected to reach 35.3 million cases, representing a 76.6% increase from the estimated 20 million cases in 2022. Major pharmaceutical companies continue to pair targeted therapies with companion diagnostics. FDA, EMA, PMDA, and equivalent agencies oversee CDx approvals, NGS panel clearances, and laboratory-developed test (LDT) regulatory pathways.

Market Dynamics

To evaluate market opportunities, Request Sample

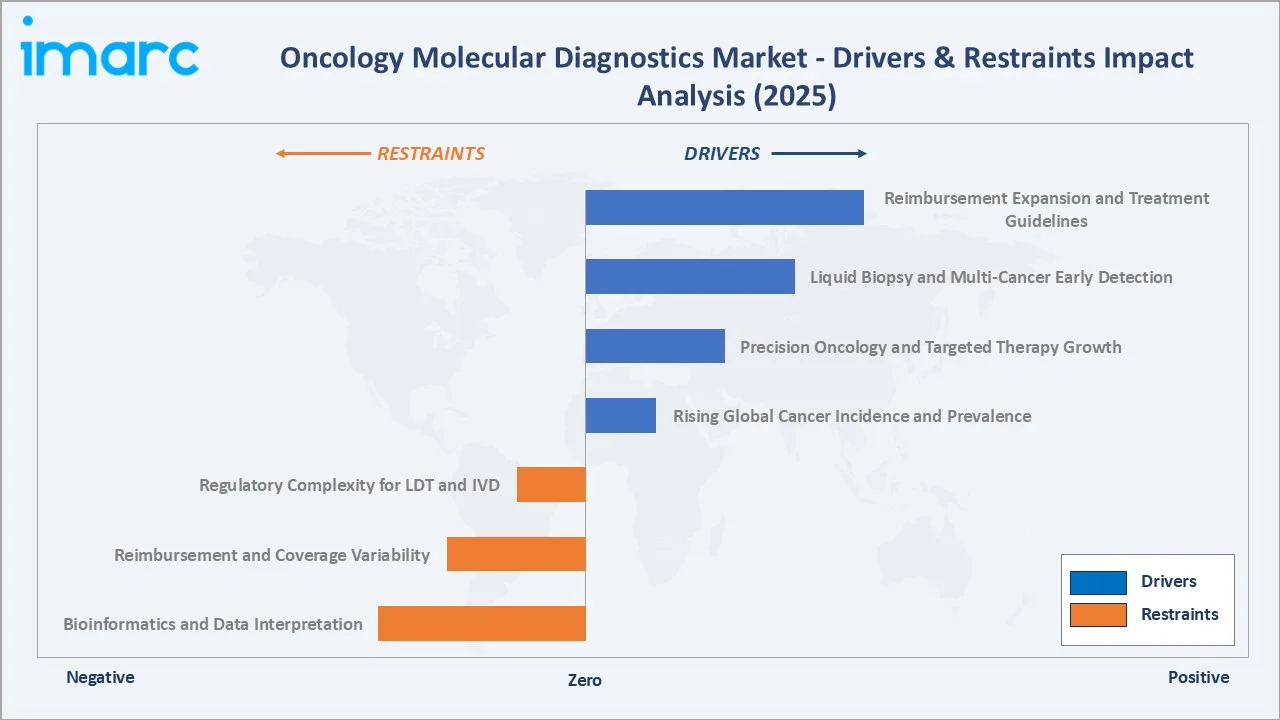

Market Drivers

- Rising Global Cancer Incidence and Prevalence: Global cancer cases are projected to surge from 20 million in 2022 to 35.3 million by 2050, marking a 76.6% increase. Rising cancer burden drives sustained demand for diagnostic testing across screening, treatment selection, and disease monitoring.

- Precision Oncology and Targeted Therapy Growth: The FDA has approved over 100 targeted oncology therapies paired with companion diagnostics, with biomarker-driven prescribing now standard of care across breast, lung, colorectal, and adjacent tumor types. Pharmaceutical-diagnostic codevelopment partnerships continue to expand the CDx pipeline.

- Liquid Biopsy and Multi-Cancer Early Detection: Liquid biopsies, blood or other fluid tests that detect cancer‑related molecular signals, are emerging as a promising tool to find many cancers earlier than current screening methods and potentially improve outcomes. Guardant Health, Natera, and Foundation Medicine continue to expand commercial ctDNA portfolios.

- Reimbursement Expansion and Treatment Guidelines: Medicare and commercial insurance coverage for comprehensive genomic profiling (CGP) tests, MRD monitoring, and companion diagnostics continues to expand. National Comprehensive Cancer Network (NCCN), ASCO, and ESMO treatment guidelines increasingly recommend molecular testing across solid tumor types.

Market Restraints

- High Cost: The cost of targeted gene panels typically ranges from USD 250 to USD 3,000, depending on the number of genes analyzed and the complexity of the assay, while WES falls between USD 1,000 and USD 3,000. This limits accessibility in resource-constrained settings and creates reimbursement complexity.

- Reimbursement and Coverage Variability: Reimbursement frameworks vary substantially across countries and US payers, with coverage policy fragmentation slowing speed-to-market for new oncology molecular diagnostics. Approval pathways for novel multi-cancer early detection and MRD assays remain complex.

- Regulatory Complexity for LDT and IVD: The FDA's laboratory-developed test (LDT) rule finalized in 2024 and EU IVDR enforcement are reshaping regulatory pathways. Compliance with new requirements requires substantial investment in quality systems, performance verification, and post-market surveillance.

Market Opportunities

- Multi-Cancer Early Detection (MCED): Multi-cancer early detection assays represent a substantial new growth opportunity. GRAIL leads the MCED market through the Galleri test, while Exact Sciences, Guardant Health, and Freenome continue MCED platform development with expanding clinical validation.

- Minimal Residual Disease (MRD) Monitoring: Tumor-informed MRD assays for solid tumors, including colorectal and breast cancer, are scaling rapidly. Natera's Signatera, Guardant Reveal, and emerging tissue-informed and tissue-free MRD platforms target multi-year monitoring revenue streams.

Market Challenges

- Bioinformatics and Data Interpretation: Comprehensive genomic profiling generates substantial bioinformatics challenges, including variant calling, clinical significance interpretation, and integration with electronic health records. Workforce shortages in molecular pathology and bioinformatics constrain laboratory throughput.

- Sample Collection and Pre-Analytical Variables: Liquid biopsy and tissue-based assay performance depends critically on sample collection, preservation, and pre-analytical handling. Pre-analytical variability remains a source of clinical performance variability and operational complexity.

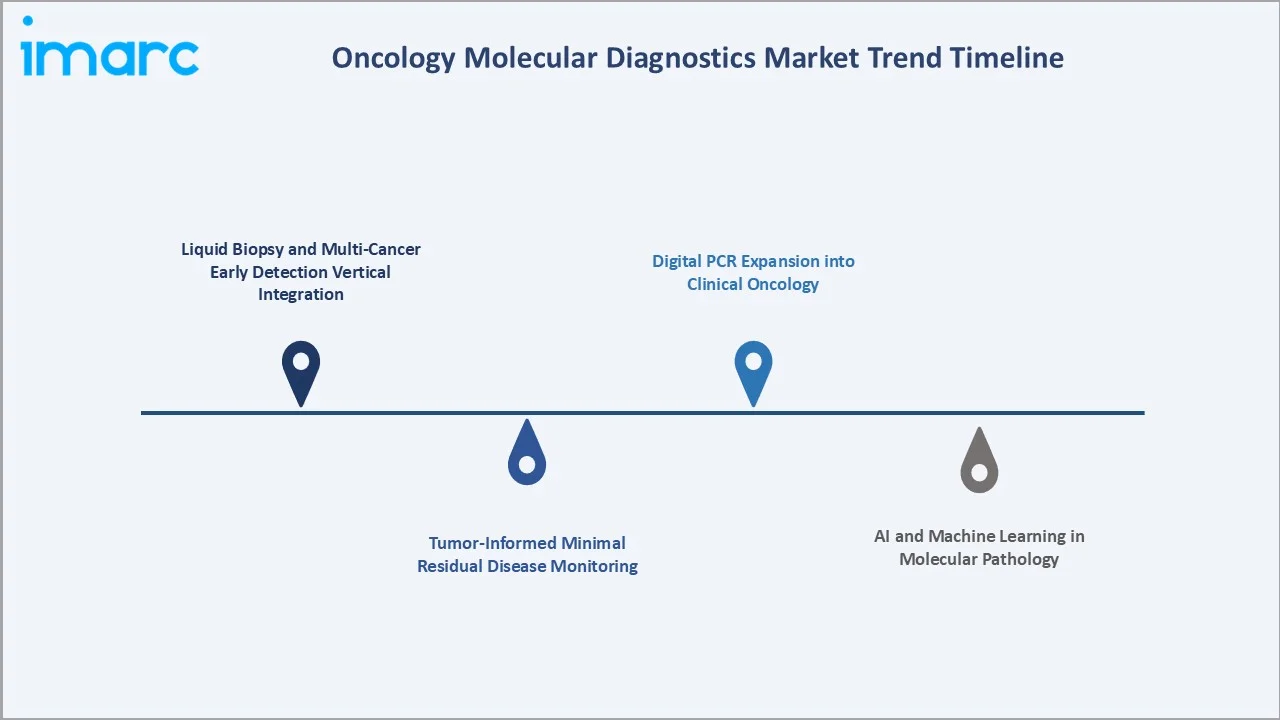

Emerging Market Trends

1. Liquid Biopsy and Multi-Cancer Early Detection Vertical Integration

Startups are advancing multi‑cancer early detection (MCED) tests that aim to identify various cancers at much earlier stages, often using blood‑based biomarkers and machine learning, addressing limitations of existing screening methods. Companies like UK‑based Xgenera are developing tests (miONCO) with high preliminary sensitivity and specificity, and are moving toward scaled clinical validation and potential commercial launch.

2. Digital PCR Expansion into Clinical Oncology

In September 2024, QIAGEN introduced the QIAcuityDx Digital PCR System for clinical oncology testing, expanding its digital PCR portfolio and entering the clinical testing industry in North America and the European Union. Digital PCR offers superior sensitivity and quantitative precision for ctDNA, MRD monitoring, and rare variant detection compared with conventional qPCR.

3. AI and Machine Learning in Molecular Pathology

AI-driven variant interpretation, digital pathology image analysis, and tumor board decision-support platforms are scaling rapidly. PathAI, Paige, Tempus, and major instrument vendors are integrating AI capabilities into NGS bioinformatics pipelines, supporting comprehensive genomic profiling at scale and accelerating turnaround times for clinical reporting.

4. Tumor-Informed Minimal Residual Disease Monitoring

Tumor-informed MRD assays for solid tumors including colorectal, breast, and lung cancer are scaling rapidly through commercial platforms such as Natera Signatera and Guardant Reveal. MRD monitoring represents a multi-year longitudinal testing opportunity that creates recurring revenue streams alongside upfront comprehensive genomic profiling.

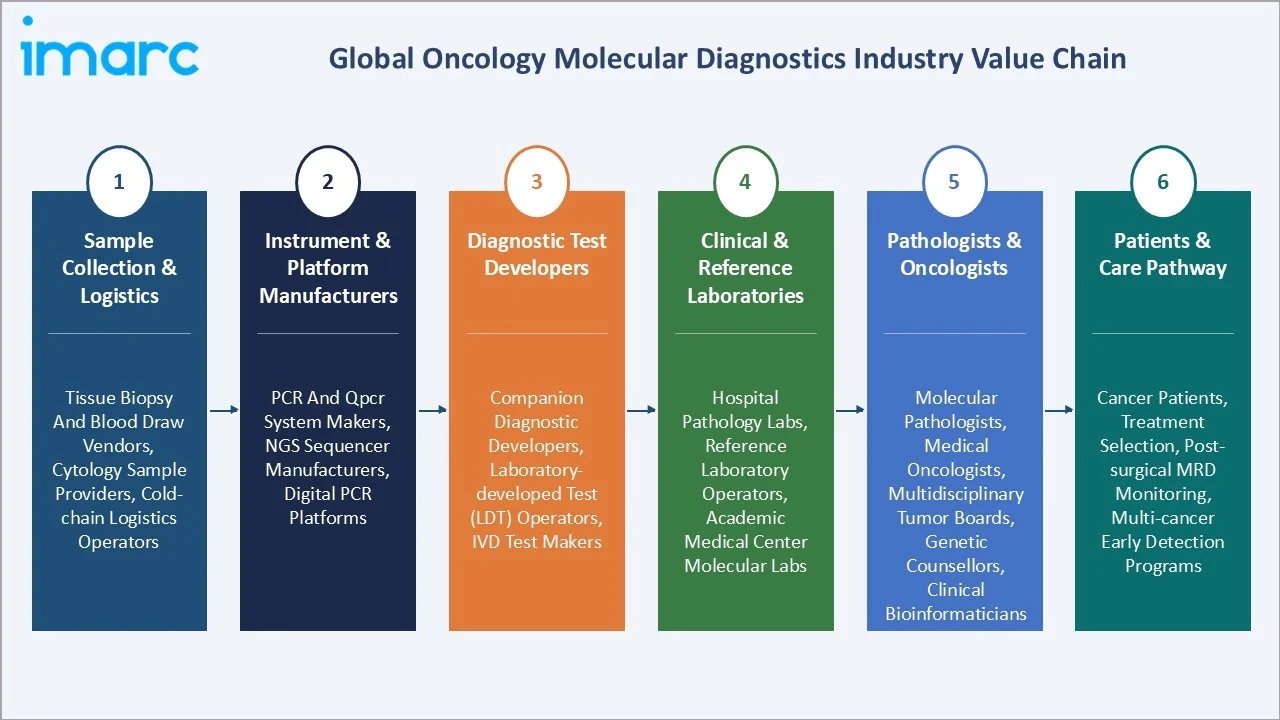

Industry Value Chain Analysis

|

Stage |

Key Players / Activities |

|

Sample Collection & Logistics |

Tissue biopsy and blood draw vendors, cytology sample providers, cold-chain logistics operators |

|

Instrument & Platform Manufacturers |

PCR and qPCR system makers, NGS sequencer manufacturers, digital PCR platforms |

|

Diagnostic Test Developers |

Companion diagnostic developers, laboratory-developed test (LDT) operators, IVD test makers |

|

Clinical & Reference Laboratories |

Hospital pathology labs, reference laboratory operators, academic medical center molecular labs |

|

Pathologists & Oncologists |

Molecular pathologists, medical oncologists, multidisciplinary tumor boards, genetic counsellors, clinical bioinformaticians |

|

Patients & Care Pathway |

Cancer patients, treatment selection, post-surgical MRD monitoring, multi-cancer early detection programs |

Technology Landscape in the Oncology Molecular Diagnostics Industry

PCR and Digital PCR

Polymerase chain reaction (PCR) remains the largest technology segment at 31.7% in 2025, encompassing qPCR for gene expression and mutation detection, and digital PCR for rare variant quantification, ctDNA monitoring, and MRD applications. QIAGEN's September 2024 QIAcuityDx Digital PCR launch and Bio-Rad's QX600 Droplet Digital PCR continue to expand clinical oncology PCR capability.

NGS and Comprehensive Genomic Profiling

DNA and next-generation sequencing technologies at 24.5% represent the fastest-growing segment. Illumina's NovaSeq and NextSeq platforms anchor sequencer infrastructure, supporting comprehensive genomic profiling, whole-exome and whole-genome sequencing, and liquid biopsy applications. Foundation Medicine, Tempus, Caris Life Sciences, and major academic medical centers operate clinical NGS pipelines.

In Situ Hybridization and Chromosomal Analysis

In situ hybridization (ISH) at 13.2% encompasses fluorescence ISH (FISH), bright-field ISH (BISH), and chromogenic ISH for HER2/neu, ALK, ROS1, and adjacent biomarker testing. ISH remains central to breast cancer (HER2/neu), lung cancer (ALK), and lymphoma diagnostic workflows.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Technology |

Polymerase Chain Reaction (PCR) |

31.7% |

2025 |

|

Cancer Type |

Breast Cancer |

24.8% |

2025 |

|

Product |

🔒 |

🔒 |

2025 |

|

End User |

🔒 |

🔒 |

2025 |

|

Region |

North America |

39.4% |

2025 |

By Technology

PCR dominates with a 31.7% share in 2025, anchored by widespread qPCR and digital PCR adoption across mutation detection, gene expression profiling, MRD monitoring, and companion diagnostic testing. PCR is supported by lower cost per test, faster turnaround, and broad clinical laboratory installed base relative to NGS platforms.

To access detailed market analysis, Request Sample

DNA and NGS sequencing at 24.5% is the fastest-growing technology segment (~14.5% CAGR), supported by comprehensive genomic profiling, multi-cancer early detection, and tumor-informed MRD applications. In situ hybridization at 13.2%, chips and microarrays at 9.6%, INAAT at 7.4%, mass spectrometry at 5.8%, and TMA at 4.1% serve adjacent diagnostic workflows.

By Cancer Type

Breast cancer leads with a 24.8% share in 2025, supported by HER2/neu, BRCA1/2 hereditary screening, Oncotype DX, MammaPrint multi-gene prognostic assays, and Prosigna ROR scoring. Lung cancer at 21.6% reflects high comprehensive genomic profiling adoption for EGFR, ALK, KRAS G12C, PD-L1, MET exon 14 skipping, and adjacent biomarkers central to targeted therapy selection.

Colorectal cancer at 14.2% leverages RAS, BRAF, MSI/MMR, and HER2 testing, while prostate cancer at 12.4% covers PCA3, Oncotype DX GPS, and BRCA hereditary screening. Blood cancers at 10.1% include AML, ALL, and lymphoma comprehensive genomic profiling. Cervical cancer at 7.3% incorporates HPV testing, and liver cancer at 5.4% includes AFP and emerging ctDNA approaches.

Regional Market Insights

North America leads at 39.4% in 2025, supported by the United States as the world's largest oncology molecular diagnostics market, comprehensive Medicare and commercial insurance reimbursement for CGP and companion diagnostics, and FDA leadership in CDx approvals.

Europe at 28.2% holds the second-largest share, anchored by EU IVDR enforcement, national cancer plans, and reference laboratory infrastructure depth across Germany, France, the UK, Italy, and the Nordics.

|

Region |

Share (2025) |

Key Growth Drivers |

|

North America |

39.4% |

US as world's largest market; Medicare and commercial CGP reimbursement; global player headquarters concentration |

|

Europe |

28.2% |

National cancer plans; aging population and cancer burden; reference lab infrastructure depth |

|

Asia Pacific |

23.1% |

Rapid adoption in China, Japan, India, Australia; expanding insurance coverage; large addressable cancer patient base; growing companion diagnostic uptake |

|

Latin America |

5.4% |

Growing oncology testing in Brazil, Mexico, Argentina; expanding private and public healthcare infrastructure; regional partnerships |

|

Middle East and Africa |

3.9% |

GCC oncology infrastructure expansion; rising cancer burden; emerging reference laboratory networks; growing CDx access |

Asia-Pacific at 23.1% reflects rapid growth across China, Japan, India, and Australia, supported by expanding insurance coverage and growing companion diagnostic adoption. Latin America (5.4%) and Middle East and Africa (3.9%) represent emerging-growth markets with rising oncology infrastructure investment.

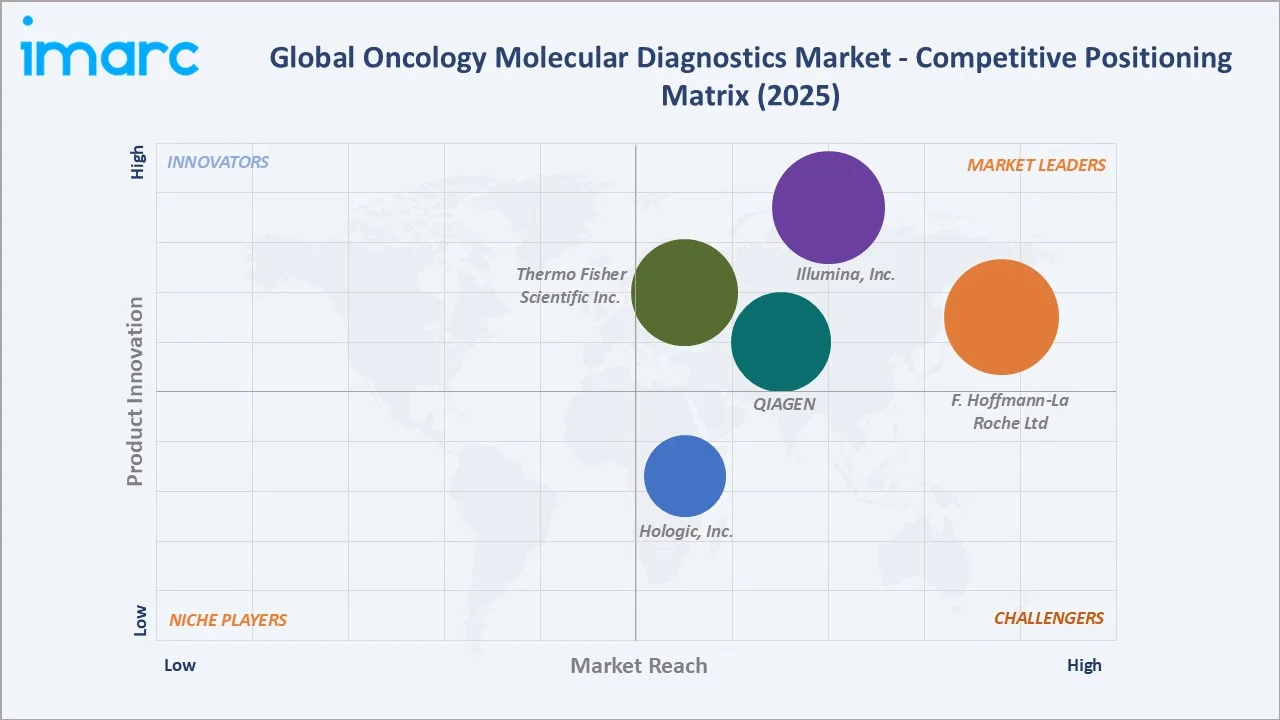

Competitive Landscape

The global oncology molecular diagnostics market is moderately consolidated, with the top five players, F. Hoffmann-La Roche Ltd, Illumina, Inc., Thermo Fisher Scientific Inc., QIAGEN, and Hologic, Inc., collectively accounting for approximately 48% of revenue in 2025.

|

Company Name |

Solutions |

Market Position |

Core Strength |

|

F. Hoffmann-La Roche Ltd |

cobas 4800 System, Foundation Medicine FoundationOne CDx and Liquid CDx assays, VENTANA, AVENIO ctDNA Surveillance Kit (RUO) |

Market Leader |

Foundation Medicine comprehensive genomic profiling; integrated tissue pathology, IHC, and ISH portfolio |

|

Illumina, Inc. |

NovaSeq, NextSeq, MiSeq; TruSight Oncology |

Market Leader |

NovaSeq and NextSeq platforms; global NGS sequencer install base leadership |

|

Thermo Fisher Scientific Inc. |

TrueMark MSI assay, OncoScan CNV and CNV Plus assays, TaqMan Liquid Biopsy dPCR assays, CytoScan HD Suite, Oncomine NGS oncology assays, Molecular oncology analysis and reporting solutions |

Market Leader |

Oncomine assays; CDx and comprehensive reagent/consumable portfolio across PCR and NGS |

|

QIAGEN |

QIAcuity and QIAcuityDx Digital PCR Systems, therascreen PDGFRA RGQ PCR Kit, ipsogen, AdnaTest series (RUO), QIAseq HRR Panel |

Market Leader |

QIAcuity Digital PCR; sample technology leadership; oncology PCR and NGS panel portfolio |

|

Hologic, Inc. |

CancerTYPE ID |

Challenger |

Women's cancer screening leadership; Panther integrated molecular testing platform |

Regional firms and laboratory-developed test specialists provide cost-effective alternatives across multiple geographies.

Key Company Profiles

F. Hoffmann-La Roche Ltd

F. Hoffmann-La Roche Ltd is the global leader in in-vitro diagnostics with a deeply integrated oncology molecular diagnostics portfolio spanning PCR, NGS, tissue pathology, IHC, and ISH platforms.

- Product Portfolio: cobas 4800 systems, Foundation Medicine FoundationOne CDx and Liquid CDx assays, VENTANA IHC and ISH systems, and AVENIO ctDNA Surveillance Kit (RUO).

- Recent Developments: In May 2026, F. Hoffmann-La Roche Ltd announced plans to present new clinical data at the 2026 ASCO Annual Meeting (May 29 – June 2, 2026), including subgroup analyses from the Phase III lidERA Breast Cancer trial, along with persevERA and evERA findings supporting giredestrant's potential to redefine standard of care in ER-positive, HER2-negative breast cancer.

- Strategic Focus: Integrated tissue-and-liquid biopsy leadership; companion diagnostic codevelopment with pharma pipeline; expansion across emerging cancer types and biomarkers; CGP portfolio depth.

Illumina, Inc.

Illumina, Inc. is the global leader in next-generation sequencing instruments and consumables. The company's NovaSeq and NextSeq platforms anchor global NGS sequencer infrastructure across clinical, research, and academic markets.

- Product Portfolio: NovaSeq, NextSeq, MiSeq, NextSeq 1000/2000 sequencing platforms; TruSight Oncology comprehensive genomic profiling panels.

- Recent Developments: In March 2026, Illumina, Inc. announced an expanded collaboration with Labcorp to broaden access to precision oncology testing by applying next‑generation sequencing (NGS) solutions more widely across health systems, promote equitable cancer biomarker testing, and develop new assays to meet unmet needs.

- Strategic Focus: NGS instrument leadership; comprehensive genomic profiling expansion via TruSight Oncology; integration with clinical bioinformatics partners.

Market Concentration Analysis

The global oncology molecular diagnostics market is moderately consolidated. The top players F. Hoffmann-La Roche Ltd, Illumina, Inc., Thermo Fisher Scientific Inc., QIAGEN, and Hologic, Inc. collectively account for approximately 48% of revenue in 2025, with regional firms providing cost-effective alternatives. Continued M&A activity across reference laboratory, CDx, and bioinformatics segments is expected to drive further consolidation.

Investment & Growth Opportunities

Fastest Growing Segments

- DNA and NGS sequencing is projected to grow at approximately 14.5% CAGR through 2034, the fastest among technology segments, supported by comprehensive genomic profiling, multi-cancer early detection, and tumor-informed MRD applications.

- Lung and breast cancer comprehensive genomic profiling continue to expand, with breast cancer maintaining the largest cancer-type share at 24.8% and lung cancer leveraging extensive biomarker testing for targeted therapy selection.

Emerging Market Expansion

- Multi-Cancer Early Detection (MCED) represents the highest-growth opportunity, with GRAIL Galleri anchoring the category and competing programs from Exact Sciences, Guardant Health, and Freenome expanding clinical validation.

- Tumor-informed MRD monitoring through commercial platforms including Natera Signatera and Guardant Reveal creates multi-year longitudinal testing opportunities with recurring revenue streams.

Venture and Institutional Investment Trends

- Liquid biopsy and MCED venture capital remains the most active investment theme globally, with multi-billion-dollar funding rounds flowing into Guardant Health, Natera, Exact Sciences, and emerging platforms targeting blood-based cancer detection.

- AI and bioinformatics platforms attached to molecular diagnostics represent a substantial software and services investment opportunity, with PathAI, Paige, Tempus and similar platforms commanding strategic valuations.

Future Market Outlook (2026-2034)

The global oncology molecular diagnostics market is positioned for sustained double-digit expansion through 2034. From USD 5.34 Billion in 2025, the market is projected to reach USD 15.11 Billion by 2034, representing incremental value of approximately USD 9.77 Billion at an 11.87% CAGR, increasingly composed of NGS-based comprehensive genomic profiling, liquid biopsy ctDNA testing, multi-cancer early detection, and tumor-informed MRD monitoring platforms.

DNA and NGS sequencing is expected to gain share toward 32% by 2034, while PCR retains category leadership at 28-30% through continued digital PCR clinical adoption. Breast and lung cancer will retain combined leadership above 45% of cancer-type share. North America will retain regional leadership, with Asia-Pacific closing the gap on rapid clinical adoption. Multi-cancer early detection and MRD monitoring will collectively define the structural growth frontier through 2034.

Research Methodology

Primary Research

Primary research included structured interviews with over 100 industry participants in 2024–2025, comprising molecular diagnostics executives, reference laboratory leaders, molecular pathologists, oncologists, payer organizations, and clinical key opinion leaders across North America, Europe, and Asia-Pacific, validating market sizing, segmentation, technology adoption, and pipeline trajectories.

Secondary Research

Secondary research covered WHO IARC publications, FDA and EMA companion diagnostic approval databases, NCCN, ASCO, and ESMO treatment guidelines, company annual reports and SEC filings, alongside government national cancer plan documents.

Forecasting Models

Market size estimations used combined top-down and bottom-up forecasting, incorporating country-level cancer incidence and prevalence, biomarker testing penetration rates, NGS adoption, MRD and MCED launch trajectories, and vendor revenue disclosures. The 11.87% CAGR reflects validation against announced product pipelines, regulatory approval timelines, and reimbursement expansion trajectories through 2034.

Oncology Molecular Diagnostics Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Cancer Types Covered | Breast Cancer, Prostate Cancer, Colorectal Cancer, Cervical Cancer, Liver Cancer, Lung Cancer, Blood Cancer, Others |

| Products Covered | Instruments, Reagents, Others |

| Technologies Covered | Polymerase Chain Reaction (PCR), In Situ Hybridization, Chips and Microarrays, Isothermal Nucleic Acid Amplification Technology (INAAT), Mass Spectrometry, DNA and NGS Sequencing, Transcription Mediated Amplification (TMA), Others |

| End-Users Covered | Hospitals and Clinics, Reference Laboratories, Others |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | F. Hoffmann-La Roche Ltd, Illumina, Inc., Thermo Fisher Scientific Inc., QIAGEN, Hologic, Inc., etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC's report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the oncology molecular diagnostics market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the global oncology molecular diagnostics market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's five forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the oncology molecular diagnostics industry and its attractiveness.

- The competitive landscape allows stakeholders to understand their competitive environment and provides insight into the current positions of key players in the market.

Frequently Asked Questions About the Oncology Molecular Diagnostics Market Report

The global oncology molecular diagnostics market reached USD 5.34 Billion in 2025 and is projected to reach USD 15.11 Billion by 2034.

The market is expected to grow at a CAGR of 11.87% during 2026-2034, driven by rising cancer burden, precision oncology growth, liquid biopsy and multi-cancer early detection expansion, and reimbursement and treatment-guideline support.

North America leads with a 39.4% share in 2025, supported by the United States as the world's largest single market and the global concentration of major industry players.

Polymerase Chain Reaction (PCR) dominates with a 31.7% share in 2025, anchored by widespread qPCR and digital PCR adoption across mutation detection, MRD monitoring, and companion diagnostic testing.

Breast cancer leads at 24.8%, supported by HER2/neu, BRCA1/2 hereditary screening, Oncotype DX, and MammaPrint multi-gene assays.

Key players include F. Hoffmann-La Roche Ltd, Illumina, Inc., Thermo Fisher Scientific Inc., QIAGEN, and Hologic, Inc.

DNA and NGS sequencing is growing at approximately 14.5% CAGR through 2034 due to comprehensive genomic profiling expansion, multi-cancer early detection adoption, and tumor-informed MRD applications.

Key challenges include high NGS testing costs, reimbursement and coverage variability, regulatory complexity for LDT and IVD pathways, bioinformatics and data interpretation, and pre-analytical sample handling.

Multi-cancer early detection, tumor-informed minimal residual disease monitoring, AI-powered pathology and bioinformatics, and Asia-Pacific clinical adoption expansion represent the highest-growth investment opportunities.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)