OSS & BSS Market Size, Share, Trends and Forecast by Component, OSS & BSS Solution Type, Deployment Mode, Organization Size, Industry Vertical, and Region 2026-2034

Global OSS & BSS Market Size, Share, Trends & Forecast (2026-2034)

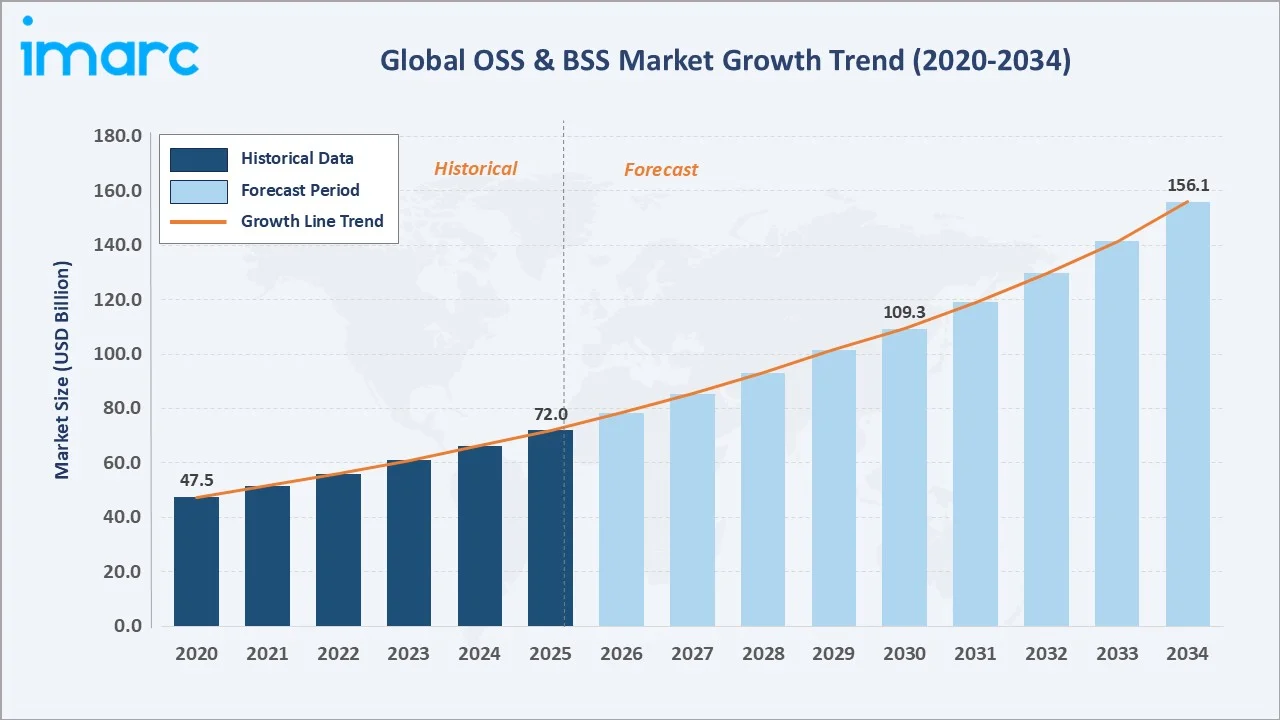

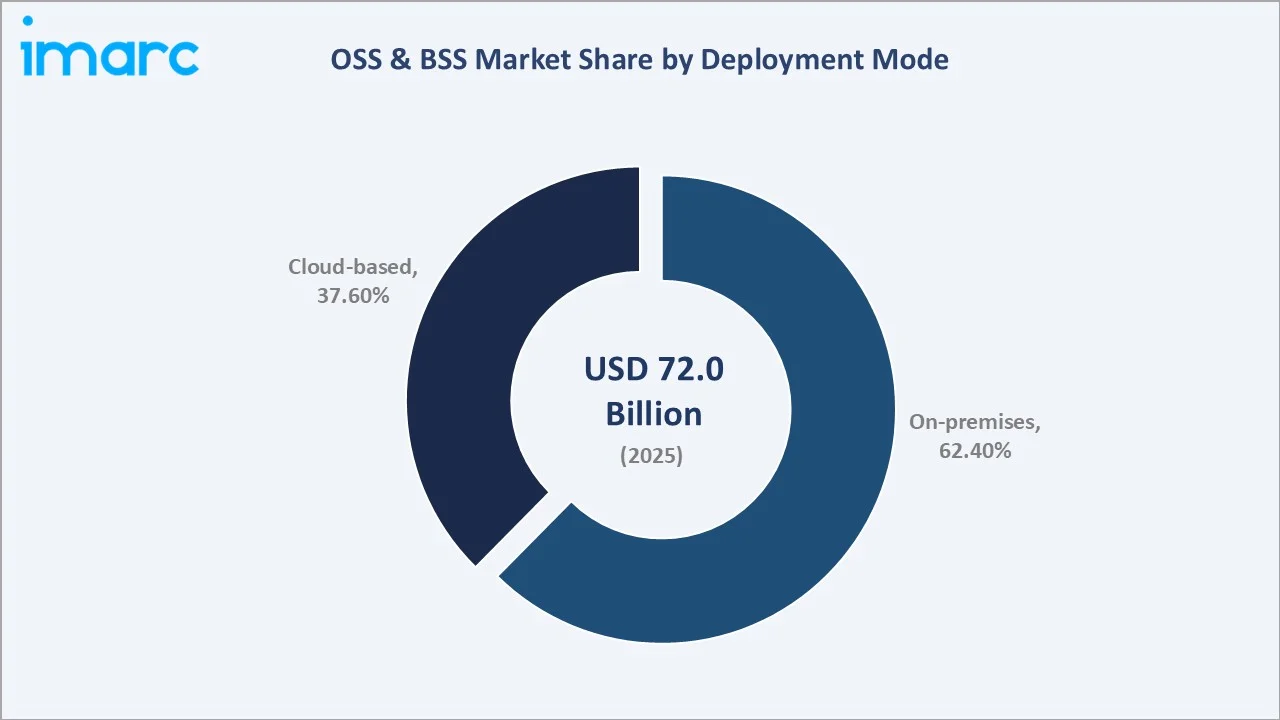

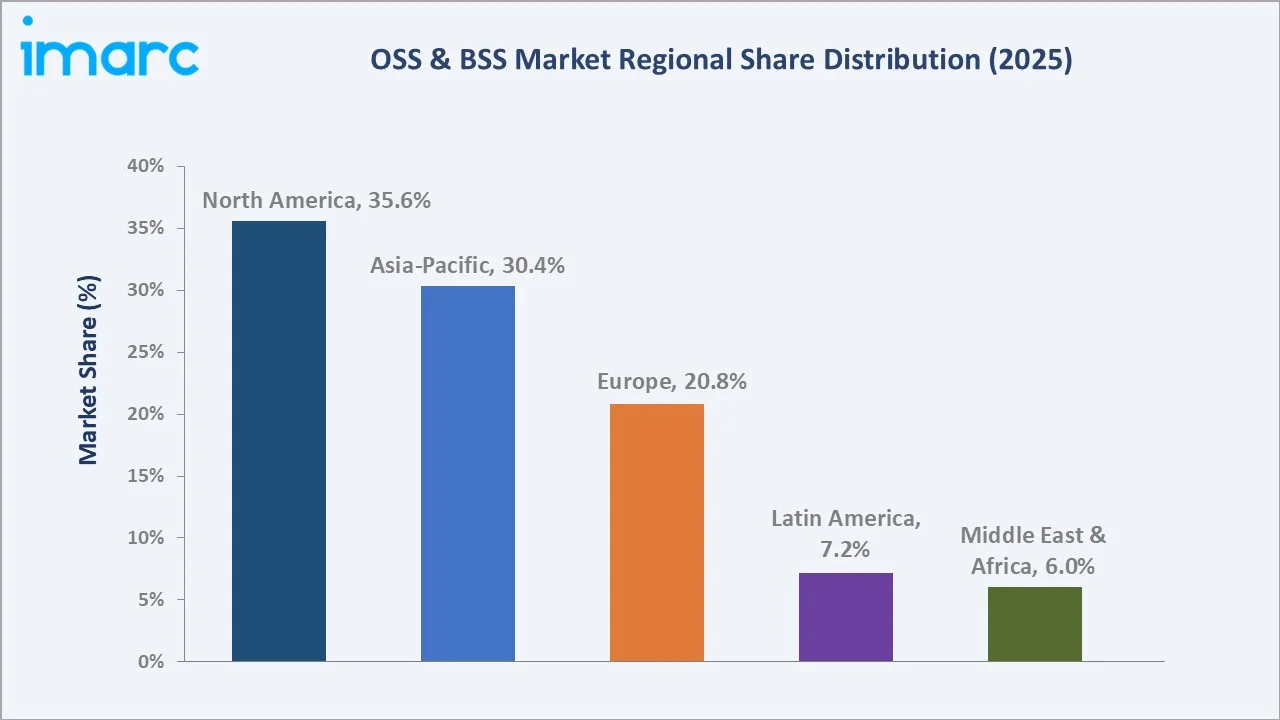

The global OSS & BSS market was valued at USD 72.0 Billion in 2025 and is projected to reach USD 156.1 Billion by 2034, expanding at a CAGR of 8.70% during the forecast period (2026-2034). The market is propelled by accelerating 5G network connections, with 2.7 Billion by 2025, rising cloud migration among telecom operators, and the growing need for AI-driven revenue assurance and network automation. On-premises deployment leads with 62.4% market share (2025), while large enterprises account for 62.4% of demand by organization size. North America dominates with 35.6% revenue share.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 72.0 Billion |

|

Forecast Market Size (2034) |

USD 156.1 Billion |

|

CAGR (2026-2034) |

8.70% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

North America (35.6%, 2025) |

|

Fastest Growing Region |

Asia-Pacific (CAGR ~10.8%, 2026-2034) |

The OSS & BSS market from 2020 through 2034 expanded from USD 47.45 Billion in 2020 to USD 72.0 Billion in 2025, anchored at USD 109.31 Billion in 2030 before reaching USD 156.1 Billion by 2034.

To get more information on this market, Request Sample

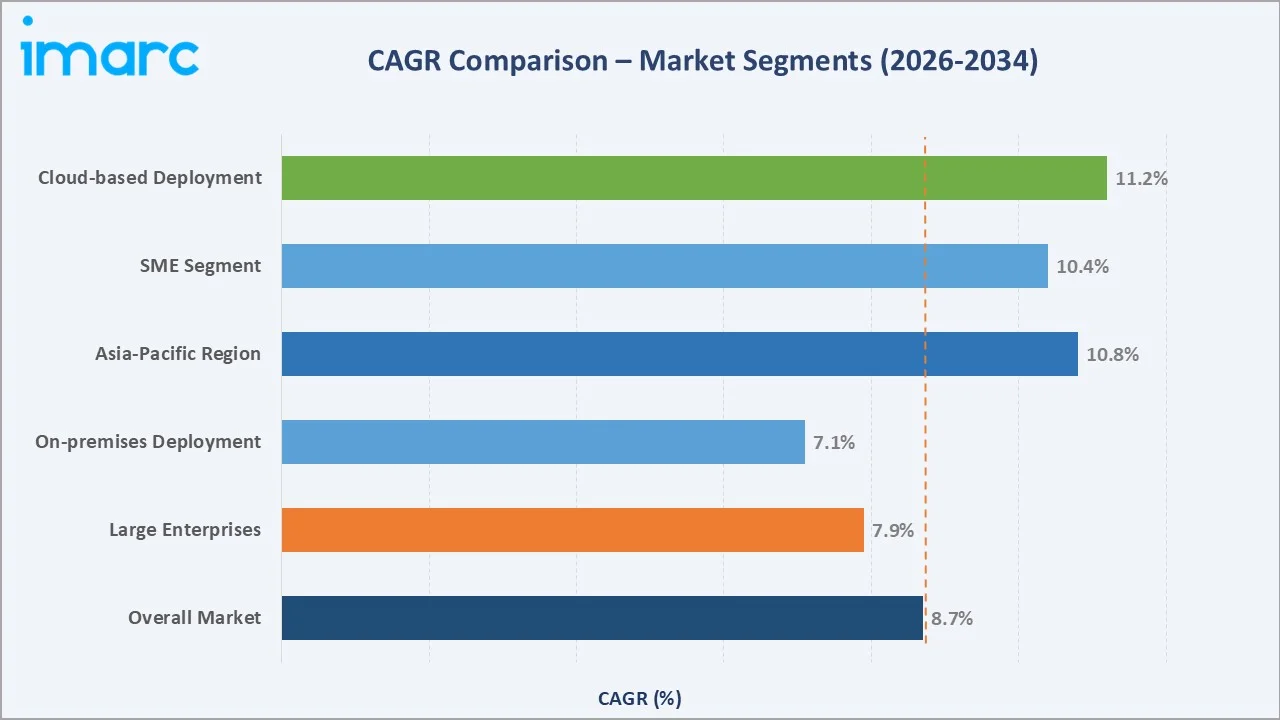

The overall market CAGR is 8.7%, the cloud-based deployment segment is growing at a CAGR of 11.2%, the small and medium-sized enterprises segment is growing at a CAGR of 10.4%, and the Latin America region is growing at 10.8% CAGR.

Executive Summary

The global OSS & BSS market is experiencing accelerated growth driven by the telecommunications industry's most significant structural transformation in two decades. Valued at USD 72.0 Billion in 2025, the market is forecast to reach USD 156.1 Billion by 2034, representing a CAGR of 8.70%. The rollout of 5G connections, with 2,7 billion globally by 2025 (GSMA), demands next-generation OSS/BSS platforms capable of managing network slicing, ultra-low latency service assurance, and real-time revenue monetization at unprecedented scale.

On-premises deployment retains the largest market share at 62.4% (2025), reflecting the preference of large tier-1 carriers for controlling mission-critical billing and network management data. However, cloud-based OSS/BSS is the fastest growing deployment mode at approximately 11.2% CAGR through 2034, as CSPs increasingly adopt SaaS-based billing, API-driven service catalogs, and containerized OSS platforms to reduce total cost of ownership and accelerate time-to-market for new digital services. Large enterprises lead organizational demand at 62.4% (2025), while SME adoption is growing rapidly through purpose-built SaaS BSS platforms from Optiva, Comarch, and Amdocs digital.

North America leads with a 35.6% market share (2025), anchored by AT&T, Verizon, and T-Mobile's massive 5G OSS/BSS transformation programs. Asia-Pacific follows at 30.4%, driven by China's state-led 5G expansion, India's Digital India telecom modernization, and South Korea's next-generation network automation investments. Europe holds 20.8%, with EU Digital Decade Policy driving operator OSS consolidation and open API mandates reshaping incumbent vendor relationships.

Key Market Insights

|

Insight |

Data |

|

Largest Deployment Mode |

On-premises – 62.4% share (2025) |

|

Largest Organization Size |

Large Enterprises – 62.4% share (2025) |

|

Leading Region |

North America – 35.6% revenue share (2025) |

|

Fastest Growing Region |

Asia-Pacific (CAGR ~10.8%, 2026-2034) |

Key Analytical Observations Supporting The Above Data:

- On-premises OSS/BSS dominates with 62.4% share (2025), as tier-1 carriers including AT&T, Vodafone, and China Mobile maintain strict data sovereignty requirements for billing systems, making full cloud migration a multi-year phased undertaking.

- Large enterprises command 62.4% of OSS/BSS spending (2025), reflecting the platform cost and complexity requirements of tier-1 carriers.

- North America leads with 35.6% market share (2025), driven by the U.S.'s dense 5G deployment pace and the consequent urgent need for 5G-capable OSS/BSS platforms that support network slicing monetization, private 5G management, and API-based service exposure.

- Asia-Pacific is the fastest growing region at ~10.8% CAGR. China's three state-owned carriers (China Mobile, China Unicom, China Telecom) are deploying AI-driven OSS platforms covering 1.7 billion mobile subscribers.

Global OSS & BSS Market Overview

Operations Support Systems (OSS) and Business Support Systems (BSS) form the foundational software infrastructure enabling telecommunications operators and digital service providers to deliver, manage, and monetize communications services. OSS encompasses network-facing functions, network inventory, service provisioning, fault management, performance monitoring, and configuration management. BSS covers customer-facing operations such as billing, revenue management, customer relationship management, product catalog management, and order management. Together, OSS/BSS constitute the operational backbone of every CSP (communications service provider) globally.

The global OSS/BSS ecosystem serves telecom operators, cable companies, MVNOs (mobile virtual network operators), internet service providers, and increasingly enterprise verticals, including BFSI, media and entertainment, and retail e-commerce that require carrier-grade service management. Macroeconomic drivers are compelling, with the global telecommunications market growth, with OSS/BSS playing a critical role in total telecom revenues as mandatory operational infrastructure investment.

Market Dynamics

To evaluate market opportunities, Request Sample

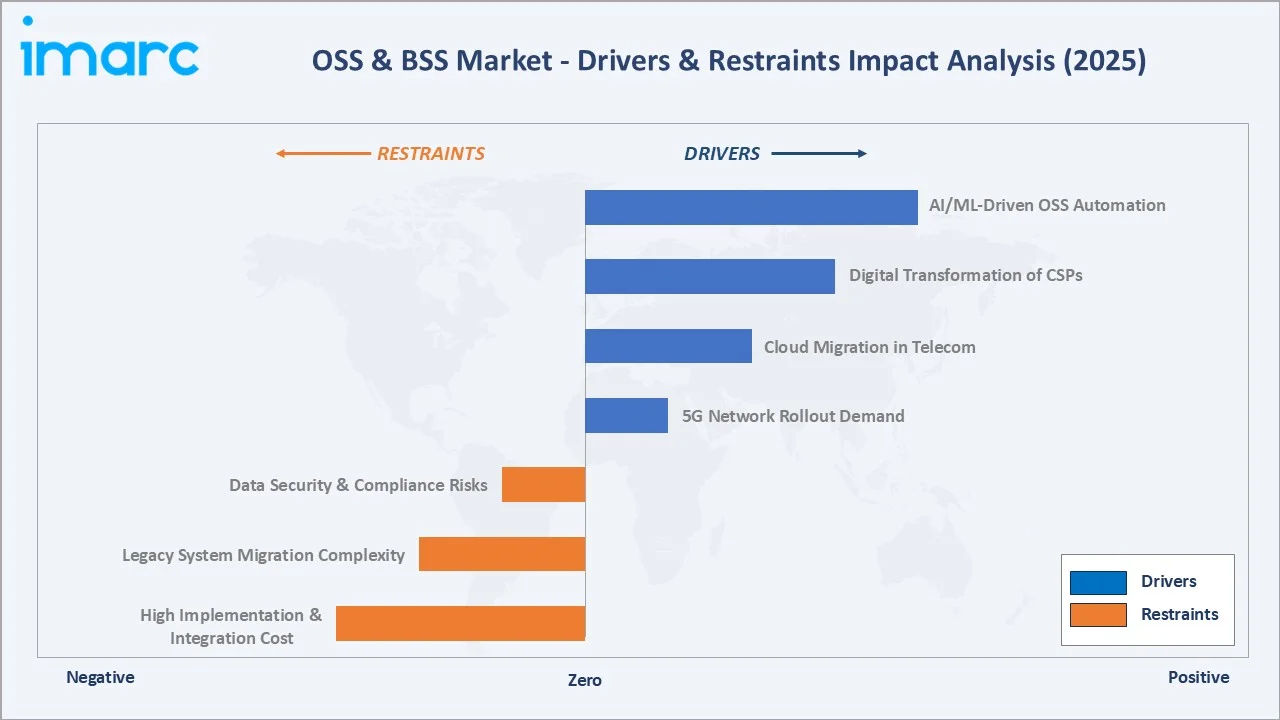

Market Drivers

- 5G Network Rollout Driving OSS/BSS Modernization: Global 5G connections reached 2.7 billion in 2025 (GSMA), 40 service providers have deployed or launched 5G standalone in public networks, with 5G network management requiring fundamentally new OSS capabilities for managing network slicing, edge computing nodes, and ultra-dense small cell deployments.

- Digital Transformation and New Revenue Streams: CSPs are launching IoT connectivity management, private 5G-as-a-service, and API-based network monetization products that require agile BSS platforms with real-time charging and flexible product catalogs.

- AI and Automation in Network Operations: AI-powered predictive fault detection reduces network outage resolution time. Nokia's AVA platform and Ericsson's OSS with AI capabilities are deployed in carrier networks globally, with AI-driven OSS reducing NOC (network operations center) headcount requirements.

Market Restraints

- High Implementation and Integration Costs: Budget overruns affect large-scale BSS transformation projects, creating risk aversion among CSP CIOs considering platform replacement decisions.

- Data Security and Regulatory Compliance: BSS platforms process highly sensitive subscriber PII, billing data, and communication records subject to GDPR (EU), CCPA (California), TRAI (India), and ANATEL (Brazil) regulations. Gartner predicts that by 2025, 45% of the global organizations will have faced attacks on their software supply chains.

Market Opportunities

- Open RAN and TM Forum Open API Adoption: The O-RAN Alliance's open interface mandates are driving OSS disaggregation. This creates an opportunity for independent OSS vendors to supply network management platforms without being tied to RAN vendor ecosystems.

- SME and MVNO Market Digitalization: Over 2,100 active MVNOs globally represent an underserved OSS/BSS market.

- IoT and Private 5G Service Management: The global IoT connectivity market growth, with each IoT service requiring OSS/BSS platforms capable of managing billions of low-ARPU device connections, real-time MVNO billing, and SLA assurance across heterogeneous networks.

Market Challenges

- Vendor Lock-in and Proprietary Architecture: Leading OSS/BSS vendors have historically maintained proprietary data models and API interfaces that lock CSPs into 10–15-year replacement cycles.

- Talent Shortage in Telecom IT: The global shortage of engineers proficient in both telecom domain knowledge and modern cloud/DevOps practices is hampering the market growth. This limits the pace at which CSPs can execute OSS/BSS transformation programs.

Emerging Market Trends

1. Cloud-Native, Microservices-Based OSS/BSS Architecture

The telco industry is transitioning from monolithic to microservices-based OSS/BSS architecture aligned with TM Forum Open Digital Architecture (ODA) standards.

2. AI-Powered Autonomous Network Management

Intent-based networking and AI-driven self-healing OSS are progressing from proof-of-concept to production deployment. AI-driven OSS deployed automatically resolves network faults without human intervention, reducing MTTR. TM Forum's George Glass stated that, "You can't reach autonomous network level 4 if you haven't embedded AI into your design and operations processes".

3. Revenue Assurance and Fraud Management Innovation

AI-driven revenue assurance platforms are identifying and recovering CSP revenues previously lost to billing errors, interconnect fraud, and SIM-swap attacks.

4. 5G Network Slicing Monetization Through BSS

Network slicing, virtualizing a single 5G network into multiple isolated logical networks with distinct SLA parameters, requires BSS platforms capable of real-time slice-based charging and guarantee tracking.

5. Generative AI for Customer Experience and BSS Self-Service

Generative AI is being integrated into BSS customer management layers to automate bill dispute resolution, personalized plan recommendation, and contract renewal negotiation. In February 2024, Amdocs launched the amAIz Suite, a comprehensive, modular, and plug-and-play solution designed to eliminate data silos, anticipate customer needs, and enable proactive, autonomous actions. The offering aims to redefine Generative AI (GenAI) for communications service providers (CSPs), regardless of their stage in the data maturity journey.

Industry Value Chain Analysis

The OSS/BSS industry value chain extends from foundational telecom infrastructure through software development, system integration, cloud deployment, and professional services to the communications service provider end users managing billions of subscriber relationships and network assets.

|

Stage |

Key Players / Examples |

|

Telecom Infrastructure & HW |

Ericsson, Nokia, Huawei, Cisco, network equipment and connectivity |

|

OSS/BSS Software Development |

Amdocs, CSG Systems – billing, network management |

|

Professional Services |

Implementation, testing, training, and managed services providers |

|

Operations & Maintenance |

24/7 managed service, SLA management, upgrade and patch support |

|

End Users (CSPs & Enterprises) |

Telecom operators, MVNOs, BFSI, media, retail e-commerce firms |

The OSS/BSS software development stage captures the highest margin in the value chain, with Amdocs, Ericsson, and Nokia generating gross margins of 55–68% on platform license and subscription revenues. System integration services, typically representing 2–3 times the software license value in total project cost, are captured by Infosys, TCS, and Netcracker, generating EBIT margins of 18–26% on multi-year managed service contracts.

Technology Landscape in the OSS & BSS Industry

Cloud-Native OSS/BSS Architecture

TM Forum Open Digital Architecture (ODA) defines the reference architecture for cloud-native OSS/BSS, decomposing traditional monolithic platforms into standard software components that can be independently deployed, upgraded, and replaced.

AI and Machine Learning Integration

Machine learning is embedded across OSS/BSS functions: anomaly detection in network performance data, predictive churn models identifying at-risk subscribers 90 days in advance, fraud detection in real time, and generative AI automating customer interaction workflows.

Real-Time Charging and Revenue Management

5G standalone networks require online charging systems (OCS) capable of processing millions of charging events per second with sub-5ms latency. The shift from offline to online real-time charging is the single most significant BSS infrastructure investment cycle among tier-1 carriers globally.

Market Segmentation Analysis

The report covers the following segments:

| Segment Category | Leading Segment | Market Share | Year |

|---|---|---|---|

| Component | Solution | 62.4% | 2025 |

| Solution Type | Network Planning and Design | 19.3% | 2025 |

| Deployment Mode | On-premises | 62.4% | 2025 |

| Organization Size | Large Enterprises | 62.4% | 2025 |

| Industry Vertical | IT and Telecom | 61.8% | 2025 |

| Region | North America | 35.6% | 2025 |

By Deployment Mode

On-premises deployment dominates with a 62.4% market share in 2025. This deployment model is preferred by tier-1 carriers (AT&T, Vodafone, China Mobile) that process billions of CDRs daily and maintain strict regulatory data residency requirements. On-premises OSS/BSS investments also reflect massive sunk costs in existing infrastructure.

To access detailed market analysis, Request Sample

Cloud-based OSS/BSS holds 37.6% market share (2025) and is growing at ~11.2% CAGR through 2034. MVNOs, tier-2 operators, and digital-native service providers are bypassing on-premises deployment entirely. Optiva's manage over 250 million subscriber relationships.

By Organization Size

Large enterprises dominate OSS/BSS demand with a 62.4% market share (2025). This segment encompasses tier-1 and tier-2 carriers, large cable operators, and major enterprise verticals (BFSI, media) deploying carrier-grade OSS/BSS. AT&T’s Amdocs platform contract, Vodafone’s Nokia deal, and Deutsche Telekom’s Ericsson OSS program each represent OSS/BSS investments, anchoring the large enterprise segment's revenue dominance.

SMEs hold 37.6% market share (2025) and represent the higher-growth segment at ~10.4% CAGR through 2034. The SME segment includes MVNOs, ISPs, IoT connectivity providers, and enterprise IT teams requiring OSS/BSS-like service management platforms.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

|

North America |

35.6% |

5G monetization by AT&T/Verizon, cloud BSS adoption, digital telco transformation |

|

Asia-Pacific |

30.4% |

China 5G scale, India Digital India telecom push, APAC MVNO proliferation, South Korea network upgrades |

|

Europe |

20.8% |

EU Digital Decade policy, telco consolidation, network slicing monetization, IoT service management |

|

Latin America |

7.2% |

Brazil telecom modernization, Claro/Telefonica BSS upgrades, eSIM adoption in Mexico |

|

Middle East & Africa |

6.0% |

Saudi Vision 2030 digital infra, UAE 5G BSS upgrade, Africa mobile money OSS integration |

North America's 35.6% market share (2025) represents the most mature and highest-spending OSS/BSS geography globally. The U.S. market is dominated by three carriers, AT&T, Verizon, and T-Mobile, each executing OSS/BSS transformation programs.

Asia-Pacific's 30.4% share (2025) is forecast to grow at ~10.8% CAGR. China's three state-owned carriers are deploying AI-native OSS platforms for managing 1.7 billion mobile subscribers. India’s Reliance Jio, serving 480 million subscribers, is executing a cloud-first BSS transformation.

Europe's 20.8% share (2025) reflects the market's regulatory complexity and operator consolidation dynamics. The EU Digital Decade Policy mandates digital connectivity targets that are driving network investment, while BEREC open API regulations are forcing incumbent vendors to open interfaces, reducing switching costs and intensifying competition among OSS/BSS suppliers.

Competitive Landscape

The global OSS/BSS market is moderately concentrated, with Amdocs, Ericsson, and Nokia collectively accounting for approximately 38–42% of global OSS/BSS software revenues. The market's service and implementation layer is more fragmented, with hundreds of regional system integrators competing for implementation mandates on major platform programs.

|

Company Name |

Brand / Platform |

Market Position |

Core Strength |

|

Amdocs |

Intelligent Networking Suite |

Market Leader |

End-to-end telco BSS/OSS stack, AI-native billing and customer management |

|

Telefonaktiebolaget LM Ericsson |

Ericsson Intelligent IT Suite |

Market Leader |

Largest telco infrastructure vendor, OSS tightly integrated with 5G RAN/Core |

|

Nokia Corporation |

Nokia Operations Support System (OSS) |

Strong Challenger |

Full-stack 5G OSS/BSS suite, AI-driven network analytics |

|

NEC Corporation |

Netcracker |

Strong Challenger |

Billing and revenue management specialist, cloud-native Ascendon platform |

|

Infosys Limited |

Next Generation OSS |

Specialist Leader |

Large-scale OSS implementation and digital transformation |

|

Mavenir |

Mavenir’s Digital Enablement (MDE) BSS |

Emerging |

Cloud-native, open-source-first BSS for 5G service providers |

|

Comarch SA |

Comarch OSS/BSS Suite |

Established |

Comprehensive telecom IT stack, managed services and SaaS delivery models |

|

Optiva, Inc. (a Qvantel company) |

Optiva BSS Platform |

Niche Specialist |

Cloud-native, microservices-based BSS for Tier 2/3 operators and MVNOs; real-time charging engine specialist |

Competitive differentiation is driven by AI capability, cloud-native architecture, TM Forum certification compliance, and the breadth of telecom domain vertical coverage.

Key Company Profiles

Amdocs

Amdocs is the global market leader in OSS/BSS software and services, serving communications and media companies.

- Product Portfolio: Intelligent Networking Suite

- Recent Developments: In July 2023, Amdocs completed its acquisition of TEOCO’s service assurance business.

- Strategic Focus: Generative AI integration across BSS customer engagement; cloud-native OSS/BSS migration leadership; 5G network slicing monetization platform; expansion into enterprise 5G private network management beyond traditional CSP customer base.

Telefonaktiebolaget LM Ericsson

Ericsson is one of the world's largest telecommunications equipment vendors and a major OSS/BSS software provider, with OSS solutions.

- Product Portfolio: Ericsson Intelligent IT Suite.

- Recent Developments: In June 2025, Ericsson announced the availability of a wide range of AI-powered enhancements to its evolved Business and Operations Support Systems (OSS/BSS) portfolio, and launched new collaborative initiatives in AI with close partners.

- Strategic Focus: AI-driven autonomous network management, 5G standalone OSS as a competitive differentiator; cloud-native open RAN management, enterprise private 5G OSS expansion beyond traditional telco customers.

NEC Corporation

NEC Corporation acquired CSG Systems, a specialist BSS vendor, globally recognized for its billing and revenue management expertise.

- Product Portfolio: CSG Singleview

- Recent Developments: In October 2025, NEC Corporation and CSG Systems International, Inc. announced a definitive agreement under which NEC will acquire CSG for $80.70 per share in cash, valuing the transaction at approximately $2.9 billion, including debt.

- Strategic Focus: Cloud-native SaaS BSS market leadership, 5G monetization through real-time slice billing; expansion into convergent digital services billing across media, utilities, and fintech; partner ecosystem API monetization.

Infosys Limited

Infosys is one of the world's largest IT services and consulting firms, with a specialized telecom practice delivering OSS/BSS transformation programs.

- Product Portfolio: Next Generation OSS.

- Recent Developments: In April 2023, Infosys announced its collaboration with ServiceNow to launch the Infosys Live Operations platform.

- Strategic Focus: Large-scale OSS/BSS transformation delivery, AI-native network operations automation, telecom-specific generative AI tools for BSS customer interaction automation.

Market Concentration Analysis

The global OSS/BSS market exhibits moderate concentration at the software platform tier and higher fragmentation at the services layer. Amdocs, Ericsson, Nokia, NEC, Infosys collectively account for approximately 50–55% of global OSS/BSS software revenues. This concentration is highest in the network management OSS subsegment, where Ericsson and Nokia together hold approximately 52% of the deployed network management platform market, and lower in the BSS tier.

Open-source OSS/BSS adoption is introducing structural fragmentation pressure. Projects including ONAP (Open Network Automation Platform), OpenBSS, and ONOS (Open Networking Operating System) are gaining traction as carrier-grade open-source alternatives, particularly for OSS functions like network inventory and configuration management.

Consolidation is accelerating across the OSS/BSS landscape. Notable recent transactions include Amdocs’ acquisition of MYCOM OSI and Nokia’s acquisition of Fenix Systems. Private equity interest in mid-market OSS/BSS vendors, particularly those with cloud-native and AI-enhanced capabilities, remains high, with significant M&A transactions recorded in the OSS/BSS sector.

Investment & Growth Opportunities

Fastest Growing Segments

Cloud-based OSS/BSS (CAGR ~11.2%), AI-native network operations platforms (CAGR ~22%), and 5G network slicing monetization BSS (CAGR ~18%) represent the three highest-growth investment vectors through 2034. The AI OSS subsegment growth making it the single most valuable technology investment category within the broader OSS/BSS market.

Emerging Market Expansion

India's telecom market, three major operators, and a government-mandated 5G rollout, represents the single largest emerging OSS/BSS growth opportunity globally. Jio and Airtel together are investing in OSS/BSS modernization. Saudi Arabia's STC and Mobily, backed by Vision 2030 technology investment mandates, represent the Middle East's highest-priority OSS/BSS expansion market for international vendors.

Venture Investment Trends

Key themes include open-source BSS commercialization, AI-driven revenue assurance, and API monetization platforms.

- Key growth bets: AI-native autonomous OSS platforms, cloud-native SaaS BSS for MVNOs, 5G network slicing monetization engines, and API marketplace management platforms.

- ESG-aligned investors are targeting OSS/BSS vendors whose platforms demonstrably reduce carrier energy consumption through AI-driven network sleep mode optimization, a capability that can reduce RAN energy costs.

- Strategic PE focus remains on mid-market OSS/BSS consolidation, particularly vendors with strong recurring managed service revenues, cloud-native architecture, and domain expertise in 5G standalone and private network management segments.

Future Market Outlook (2026-2034)

The global OSS/BSS market is positioned for sustained high-growth expansion through 2034. From USD 72.0 Billion in 2025, the market is forecast to reach USD 156.1 Billion by 2034, an absolute value addition of USD 84.1 Billion over nine years. This growth trajectory is structurally secured by the telecommunications industry’s non-discretionary investment requirement in OSS/BSS for managing 5G network complexity and monetizing new digital service revenue streams. Unlike many enterprise software categories, OSS/BSS has no viable alternative – every CSP on the planet must maintain operational and billing systems regardless of economic conditions.

Between 2026 and 2030, the dominant transformation will be the mass migration from on-premises to cloud-native OSS/BSS, enabled by confidential computing breakthroughs resolving data sovereignty barriers. The OSS/BSS market will also expand beyond its traditional telecom client base, BFSI institutions managing complex network infrastructure, utilities operating smart grid communications, and enterprise IT teams managing private 5G deployments.

Research Methodology

Primary Research

Primary research for this report included structured interviews with over 150 industry stakeholders in 2025, comprising OSS/BSS vendor executives, telecom CIO and CTO officers, network operations leadership, BSS procurement specialists, and financial analysts covering the telecom software sector. Geographies covered included North America, Europe, Asia Pacific, Latin America, and the Middle East. Primary insights validated market size, deployment mode shares, and identified AI adoption acceleration patterns not visible in vendor disclosures.

Secondary Research

Secondary research encompassed a comprehensive review of company annual reports, earnings calls, TM Forum industry reports, GSMA Intelligence data, Heavy Reading and Dell'Oro Group analyst research, regulatory filings, telecom industry conference proceedings, and government spectrum and network licensing documents across 40+ countries. Over 280 secondary sources were synthesized.

Forecasting Models

Market size estimations were derived using a hybrid bottom-up and top-down methodology. Key input variables include 5G network deployment pace, cloud adoption rate curves for telecom IT, operator IT budget as percentage of revenue, and AI OSS platform premium pricing trajectories.

OSS & BSS Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical and Forecast Trends, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Components Covered | Solution, Services |

| OSS & BSS Solution Types Covered | Network Planning and Design, Service Delivery, Service Fulfillment, Service Assurance, Billing and Revenue Management, Network Performance Management, Customer and Product Management, Others |

| Deployment Modes Covered | On-premises, Cloud-based |

| Organization Sizes Covered | Small and Medium-sized Enterprises, Large Enterprises |

| Industry Verticals Covered | IT and Telecom, BFSI, Media and Entertainment, Retail and E-Commerce, Others |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | Amdocs, Telefonaktiebolaget LM Ericsson, Nokia Corporation, NEC Corporation, Infosys Limited, Mavenir, Comarch SA, Optiva Inc.(a Qvantel company), etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the OSS & BSS market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the global OSS & BSS market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's Five Forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyse the level of competition within the OSS & BSS industry and its attractiveness.

- The competitive landscape allows stakeholders to understand their competitive environment and provides insight into the current positions of key players in the market.

Frequently Asked Questions About the OSS & BSS Market Report

The global OSS & BSS market was valued at USD 72.0 Billion in 2025 and is projected to reach USD 156.1 Billion by 2034, expanding at a CAGR of 8.70%.

North America dominates with a 35.6% revenue share (2026-2034), anchored by massive 5G BSS transformation programs at AT&T, Verizon, and T-Mobile investments.

Asia-Pacific is the fastest growing region at ~10.8% CAGR, driven by India's Jio/Airtel OSS/BSS investment and China's state-carrier AI-native OSS deployments.

Key drivers include 5G network rollout demanding new OSS/BSS capabilities, cloud migration reducing TCO by 30–40%, AI automation, and digital service monetization requirements globally.

On-premises deployment dominates with 62.4% share (2025), preferred by tier-1 carriers with strict data sovereignty requirements processing billions of CDRs daily.

Large enterprises lead with 62.4% market share (2025), driven by tier-1 carrier platform investments.

The leading companies include Amdocs, Telefonaktiebolaget LM Ericsson, Nokia Corporation, NEC Corporation, Infosys Limited, Mavenir, Comarch SA, and Optiva, Inc. (a Qvantel company).

Key trends include cloud-native microservices OSS/BSS architecture, AI autonomous network management, 5G network slicing BSS monetization, open RAN OSS, and generative AI BSS integration.

High-growth opportunities include AI-native autonomous OSS platforms, cloud SaaS BSS for MVNOs, 5G slice monetization engines, India/Saudi Arabia market expansion, and API marketplace BSS.

Key challenges include high implementation costs, legacy migration complexity, data sovereignty barriers to cloud adoption, and talent shortages in telecom IT.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)