Personal Hygiene Market Size, Share, Trends and Forecast by Product Type, Pricing, Usability, Distribution Channel, and Region, 2026-2034

Global Personal Hygiene Market Size, Share, Trends & Forecast (2026-2034)

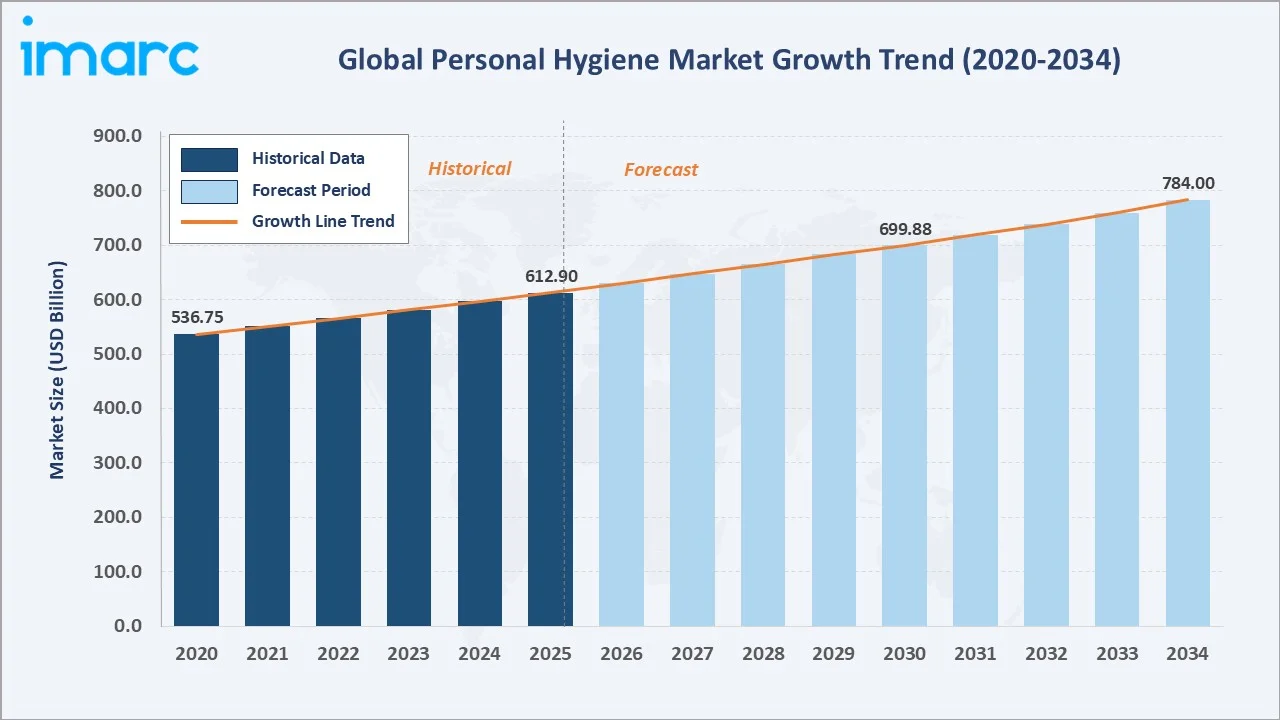

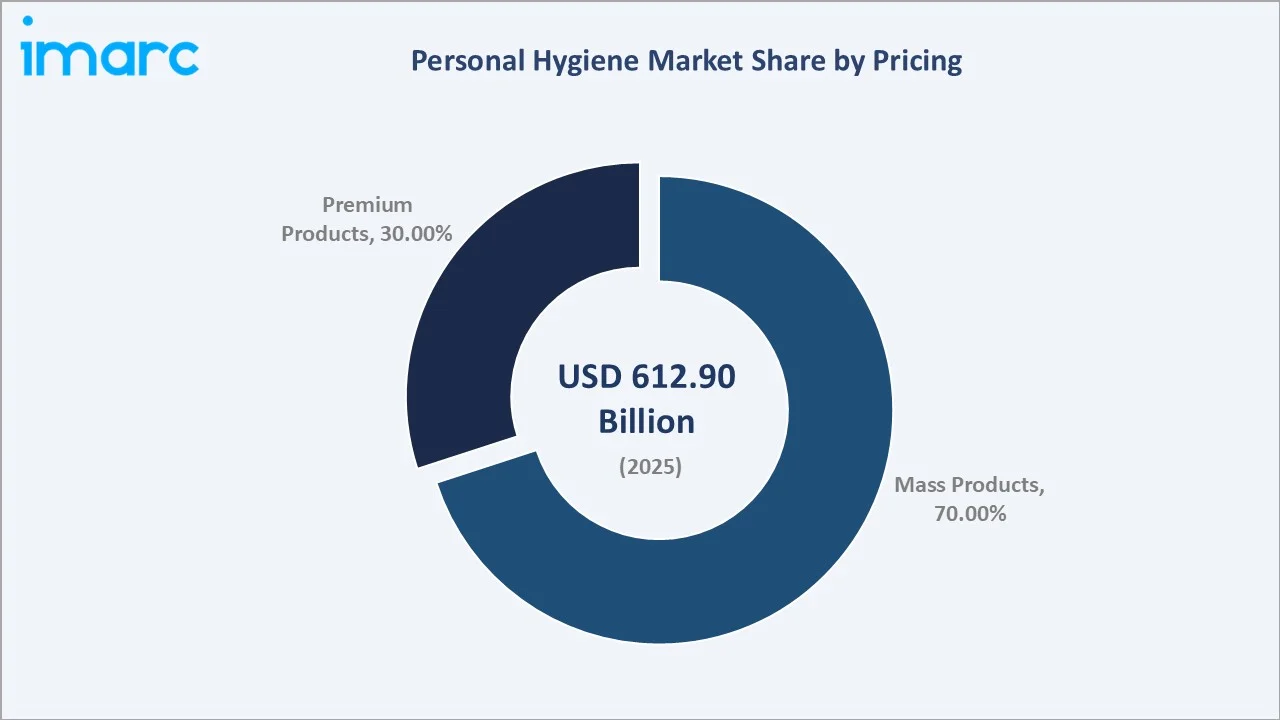

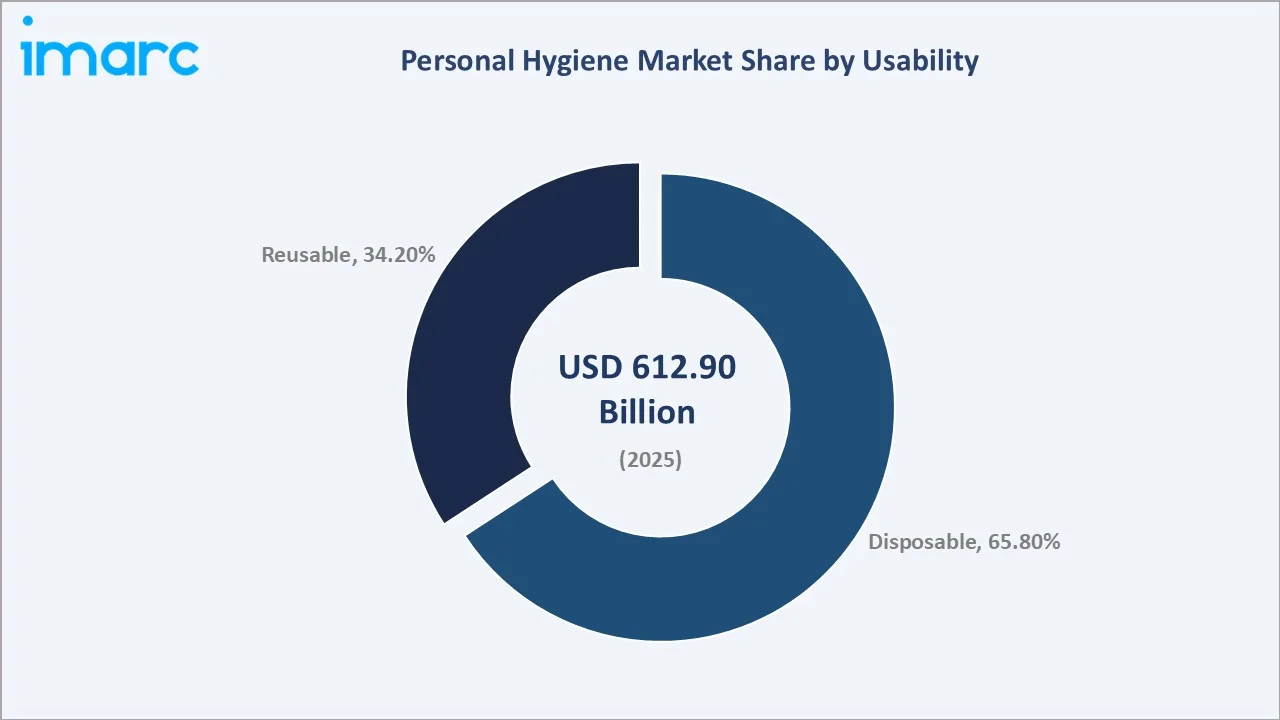

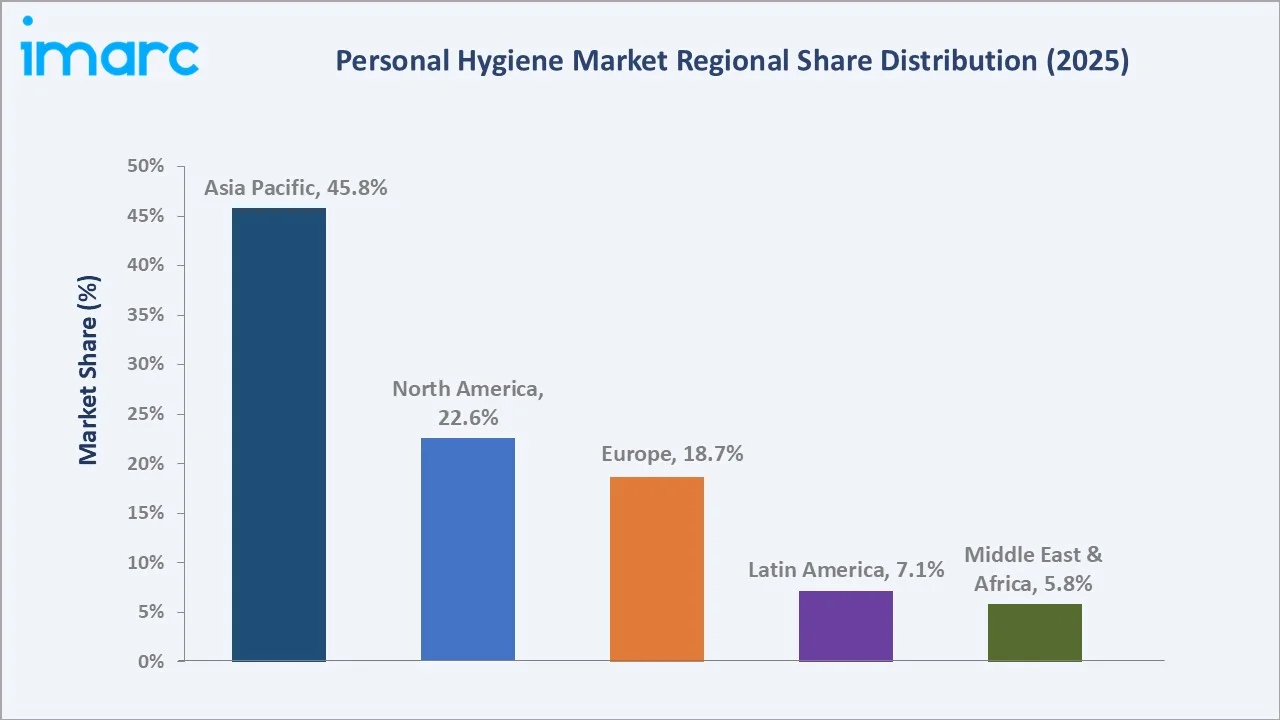

The global personal hygiene market was valued at USD 612.90 Billion in 2025 and is projected to reach USD 784.00 Billion by 2034, expanding at a CAGR of 2.69% during the forecast period (2026-2034). Market growth is driven by post-COVID hygiene habit elevation, rising urbanization and incomes in Asia Pacific, an aging global population with people aged 60 years and older will double (2.1 billion) by 2050, fuelling incontinence product demand, and accelerating consumer preference for premium and sustainable hygiene products. Mass products dominate at 70.0% market share (2025), while disposable products lead usability at 65.8%. Asia Pacific commands the largest regional share at 45.8%.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 612.90 Billion |

|

Forecast Market Size (2034) |

USD 784.00 Billion |

|

CAGR (2026-2034) |

2.69% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest and Fastest Growing Region |

Asia Pacific (45.8% in 2025, CAGR ~3.5%, 2026-2034) |

The global personal hygiene market expanded from USD 536.75 Billion in 2020 to USD 612.90 Billion in 2025, driven by pandemic-era hygiene consciousness, product category diversification, and expanding distribution in emerging markets. The market is forecast to cross USD 699.88 Billion by 2030 before reaching USD 784.00 Billion by 2034.

To get more information on this market, Request Sample

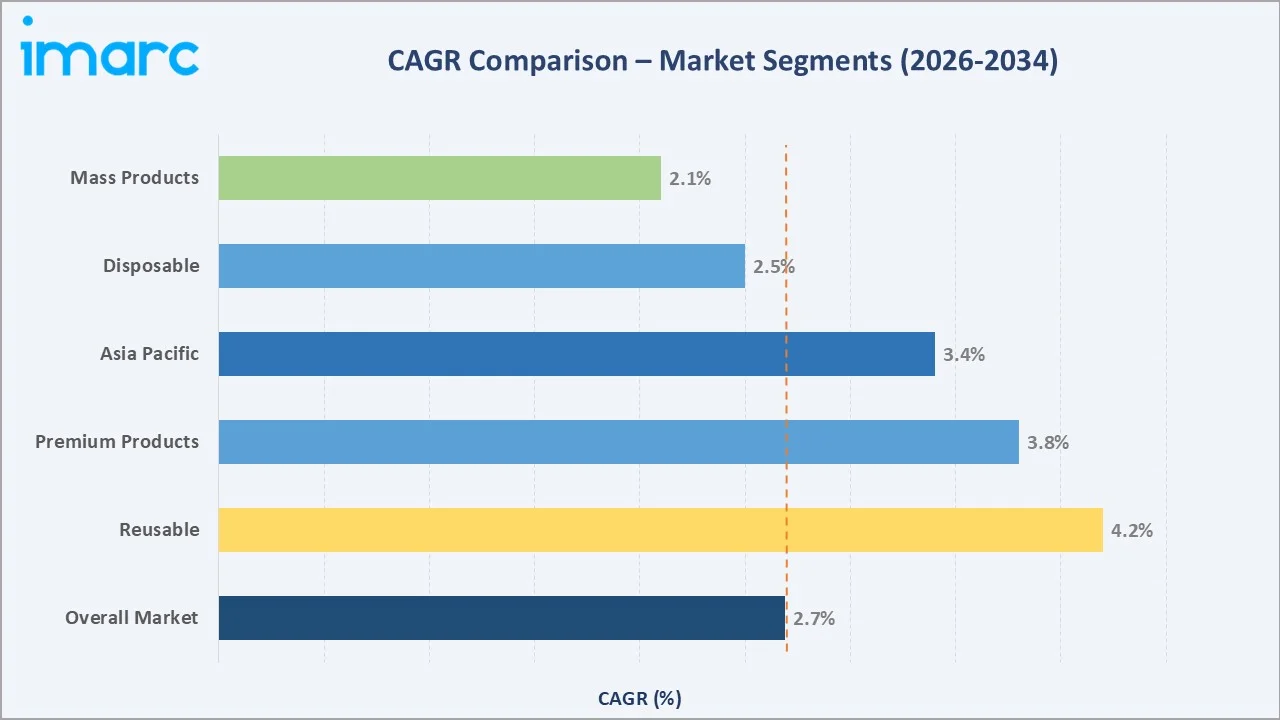

The CAGR across key pricing and usability segments, with reusable products lead at ~4.2% CAGR as sustainability consciousness drives shift from single-use formats. Premium products at ~3.8% CAGR outpace the overall market, reflecting consumers’ willingness to pay for natural, organic, and dermatologically tested formulations.

Executive Summary

The global personal hygiene market is one of the world’s most structurally stable and non-cyclical consumer goods categories, serving fundamental human health and cleanliness needs across all income levels, geographies, and demographics. From USD 536.75 Billion in 2020, the market reached USD 612.90 Billion in 2025, driven by the COVID-19 pandemic’s permanent elevation of hand hygiene, disinfection, and mask usage behaviors, combined with secular growth in feminine hygiene penetration across emerging markets and adult incontinence product adoption in ageing developed economies. The forecast trajectory to USD 784.00 Billion by 2034 reflects five compounding demand drivers: global population growth to 9.2 Billion by 2040; urbanization increasing retail channel access for hygiene products; rising disposable incomes in Asia and Africa driving premiumization; the ageing global demographic accelerating incontinence product volume; and the sustainability revolution expanding the reusable hygiene product category.

Mass products dominate at 70.0% of market revenue (2025). This segment encompasses the high-volume, accessible-price hygiene essentials consumed daily by billions of consumers globally. Premium products at 30.0% are the fastest-growing pricing tier at ~3.8% CAGR, as middle-class consumers in China, India, Brazil, and the Gulf transition from functional commodities toward branded, efficacy-differentiated, and sustainability-certified hygiene products.

Asia Pacific’s commanding 45.8% share (2025) reflects the region’s high population, combined with rapidly increasing per-capita hygiene product spend. The emergence of Japan’s Unicharm and Kao as global leaders in feminine and baby hygiene products alongside the established Western multinationals demonstrates Asia Pacific’s dual role as both the primary consumption market and an increasingly important production and innovation hub for the global personal hygiene industry.

Key Market Insights

|

Insight |

Data |

|

Dominant Pricing Segment |

Mass Products – 70.0% revenue share (2025) |

|

Dominant Usability |

Disposable – 65.8% revenue share (2025) |

|

Largest and Fastest Growing Region |

Asia Pacific (45.8% in 2025, CAGR ~3.5%, 2026-2034) |

Key Analytical Observations Supporting The Above Data:

- Mass products dominate at 70.0% (2025): The sheer scale of emerging market consumption, anchors mass product dominance. Hindustan Unilever’s Lifebuoy brand alone reached more than one Billion people with its handwashing with soap education programmes.

- Disposable leads at 65.8% (2025): Annual global disposable hygiene product consumption is staggering in scale, with sanitary pads, baby diapers, wipes, and surgical/consumer masks. In India, roughly 121 million women and girls use an average of eight disposable pads per month.

- Asia Pacific leads at 45.8% (2025): China’s personal hygiene market growth, India’s Swachh Bharat Mission and Beti Bachao Beti Padhao programs have driven feminine hygiene pad penetration, adding new feminine hygiene consumers over a decade.

Global Personal Hygiene Market Overview

The global personal hygiene market encompasses the manufacture, distribution, and retail of products designed to maintain human cleanliness, health, and wellbeing across body care, feminine care, baby and childcare, incontinence management, and surface disinfection categories. The ecosystem spans fast-moving consumer goods (FMCG) brands, pharmaceutical and healthcare companies, specialty personal care brands, and private label retailers, each targeting distinct consumer need states from daily preventative hygiene to specialized medical-grade disinfection.

Applications span feminine hygiene (sanitary pads, tampons, menstrual cups, period underwear), baby and childcare (diapers, wipes, baby wash), adult incontinence (protective underwear, adult diapers), surface and hand disinfection (hand sanitizers, antimicrobial wipes, disinfectant sprays), oral hygiene (toothpaste, mouthwash), and respiratory protection (masks, gloves). Macroeconomic drivers include global population growth, per-capita income growth in emerging economies, and the global sustainability transition reshaping packaging, formulation, and usability norms across the entire category.

Market Dynamics

To evaluate market opportunities, Request Sample

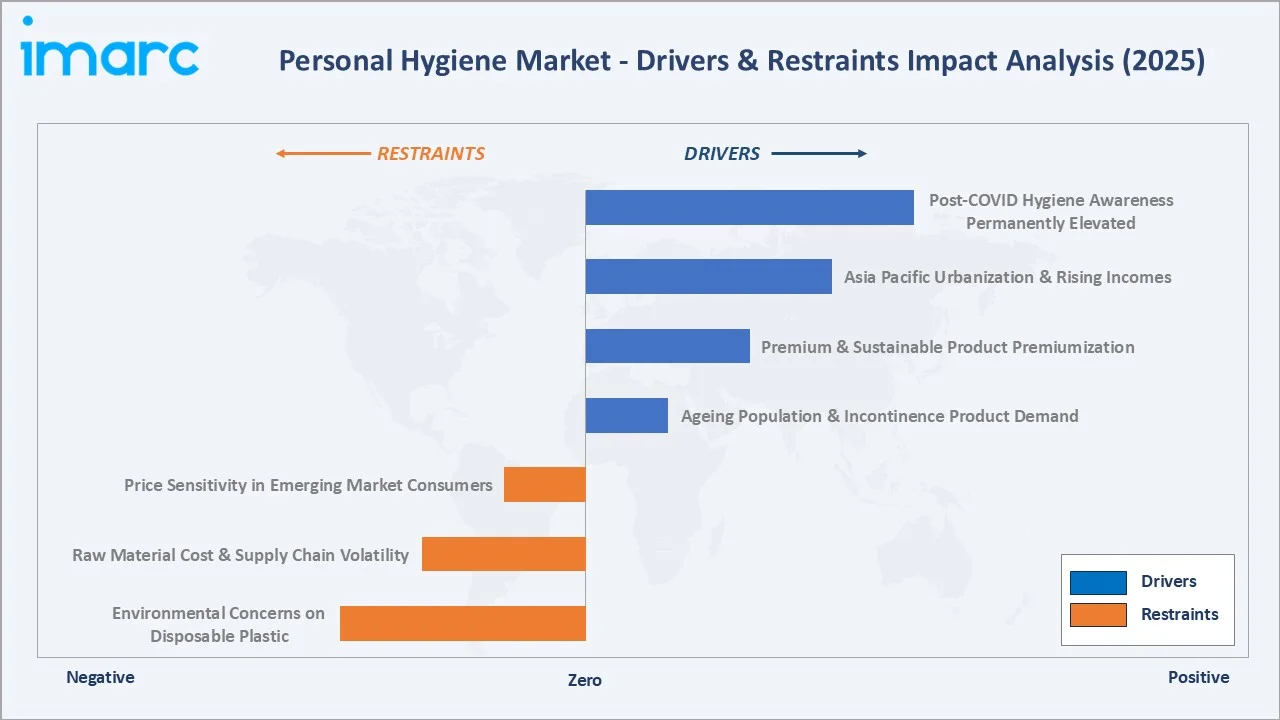

Market Drivers

- Post-COVID Elevated Hygiene Consciousness: The COVID-19 pandemic created the largest single-event behavioral shift in personal hygiene history. During the pandemic, it was observed that children used hand sanitizer up to 25 times a day, while adults used it more than 9 times daily.

- Asia Pacific Urbanization and Income Growth: By 2050, its urban population is projected to increase by 50% in Asia Pacific, with urban consumers spending 4–8× more on packaged personal hygiene products than rural counterparts.

- Premiumization and Wellness-Led Consumer Preferences: The global wellness economy, valued at USD 5.6 trillion in 2022, according to the Global Wellness Institute, is driving consumers toward premium personal hygiene products positioned at the intersection of hygiene, health, and self-care. Organic cotton sanitary products, probiotic feminine wash, microbiome-friendly deodorants, and activated charcoal dental hygiene products are growing.

- Ageing Global Population Driving Incontinence Demand: The global 65+ population will reach 2.2 Billion by 2070, with people experiencing some degree of urinary incontinence, driving the growth of the global adult incontinence product.

Market Restraints

- Environmental Concerns on Disposable Plastic Products: In India, approximately 121 million women and girls use an average of eight disposable, non-compostable pads each month, resulting in 1.021 Billion pads of waste per month, 12.3 Billion pads annually, and 113,000 metric tons of menstrual waste each year.

- Raw Material Cost and Supply Chain Volatility: Personal hygiene products rely on petrochemical-derived inputs that face acute cost volatility from oil price cycles. SAP, the key material in diapers and incontinence pads, saw price increases due to energy costs and supply disruptions.

- Price Sensitivity in Emerging Markets: In India, Sub-Saharan Africa, and rural Southeast Asia, price sensitivity remains the primary barrier to hygiene product adoption. This price-to-income ratio constrains premium product adoption and limits overall category penetration, forcing FMCG companies to offer ultra-low unit price formats that cannibalize profitability.

Market Opportunities

- Biodegradable and Sustainable Product Innovation: The sustainable personal hygiene product market, encompassing organic cotton pads, compostable wipes, bamboo toothbrushes, and refillable body wash systems, is projected to increase globally.

- Smart and Connected Hygiene Devices: The Oral-B iO electric toothbrush shows a significantly greater reduction in plaque and gingivitis versus the sonic brush. The convergence of personal hygiene with connected health technology, smart toothbrushes, AI-powered skin condition analysis apps paired with skincare regimens, and period tracking apps integrated with feminine hygiene product subscription services, is creating a new premium device + consumable revenue model.

Market Challenges

- Private Label Competition and Commoditization Pressure: Major retailers’ private label hygiene ranges are capturing increasing shelf space and consumer trust. This private label penetration compresses branded manufacturer margins and creates pricing pressure in mass market tiers, particularly for products where consumers perceive limited functional differentiation between brands.

- E-Commerce Channel Disruption of Traditional Brand Distribution: Direct-to-consumer digital brands have successfully disrupted established FMCG brands in specific hygiene subcategories by combining clean formulation positioning, subscription convenience, and premium packaging with social media-driven customer acquisition.

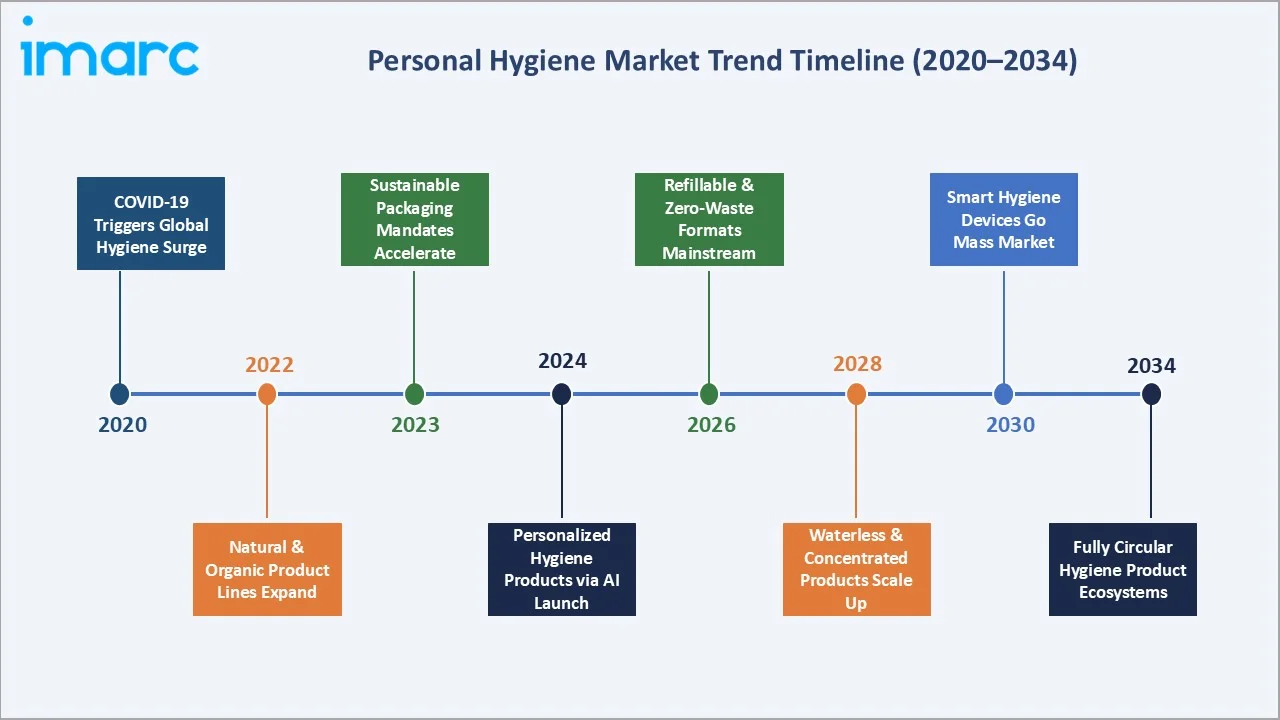

Emerging Market Trends

1. Menstrual Health and Period Equity Movement

According to the World Bank, at least 500 million women and girls globally lack adequate facilities for menstrual hygiene management, which is creating both social impact and commercial opportunity on an unprecedented scale. This political and social movement is both expanding the addressable market for feminine hygiene products and accelerating product innovation toward lower-cost, higher-accessibility formats.

2. Sustainable and Plastic-Free Product Formats

The personal hygiene industry is undergoing its most significant material transition in 70 years, moving from petroleum-derived polymers toward plant-based, biodegradable, and recycled materials. Bamboo-fibre flushable wipes are growing as regulatory pressure and consumer demand align.

3. Organic, Natural, and Certified-Clean Formulations

Consumers’ “clean beauty” preferences are extending into personal hygiene, with the natural and organic personal hygiene segment. The “toxin-free” positioning resonates particularly strongly among millennial and Gen-Z parents for baby hygiene products, driving to premium positioning that erodes conventional brand price competitiveness.

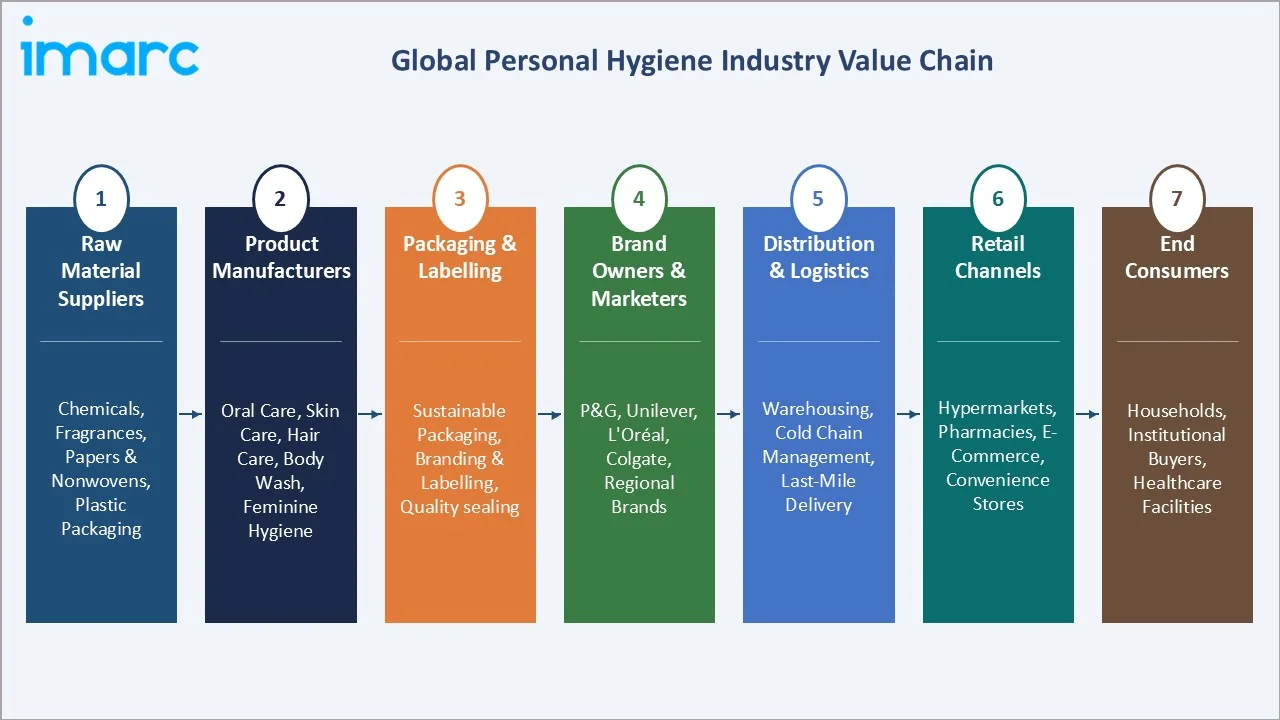

Industry Value Chain Analysis

The personal hygiene value chain spans upstream raw material production through manufacturing, brand development, multi-channel distribution, and consumer use. Each stage has distinct competitive dynamics, profitability profiles, and sustainability implications.

|

Stage |

Key Participants |

|

Raw Materials & Chemicals |

Surfactants, polymers, SAP, specialty cellulosic fibres; fragrance houses |

|

Component Manufacturing |

Nonwoven fabrics, fastening systems for diapers and incontinence products |

|

Packaging & Sustainability |

Sustainable flexible packaging; paper-based and compostable packaging innovation |

|

Distribution & Retail |

Supermarkets, online pharmacies, e-commerce platforms |

|

End Consumers |

Global population – infants/babies, women (feminine hygiene), elderly (incontinence), general consumers (sanitizers, wipes, masks) |

The brand ownership and manufacturing stage captures the highest absolute margins in the personal hygiene value chain, generating 50–60% gross margins on their branded hygiene portfolios. Retail distributors (Walmart, Amazon, Costco) operate at 25–35% gross margins but control the critical consumer touchpoint. Raw material suppliers, benefit from their oligopolistic market positions in niche hygiene material categories.

Technology Landscape in the Personal Hygiene Industry

Superabsorbent Polymer Innovation

Superabsorbent polymer (SAP), the material responsible for the absorbency of diapers, pads, and incontinence products, is undergoing its most significant innovation in 30 years. Plant-based SAP derived from starch is achieving comparable absorption performance to petroleum-derived SAP at a lower carbon footprint.

Nonwoven Fabric Technology for Skin Compatibility

Nonwoven technology blocks 99% of pathogens driving the market demand. The topsheet materials of feminine pads, baby diapers, and adult incontinence products, the layer in direct contact with skin, are transitioning from commodity polypropylene spunbond to premium cotton-feel, skin-neutral materials.

Smart Connectivity and IoT Hygiene Devices

IoT-connected hygiene products are emerging as a significant technology frontier. Oral-B’s iO Series toothbrush uses AI-powered pressure sensing, position detection, and app connectivity to achieve 100% plaque removal verification across all mouth zones. Smart baby monitors tracking diaper wetness and period tracking apps integrated with subscription feminine hygiene product delivery are creating connected hygiene ecosystems that generate recurring SaaS-like revenue alongside consumable product sales.

Market Segmentation Analysis

The report covers the following segments:

| Segment Category | Leading Segment | Market Share | Year |

|---|---|---|---|

| Product Type | Feminine Hygiene Products | 34.7% | 2025 |

| Pricing | Mass Products | 70.0% | 2025 |

| Usability | Disposable | 65.8% | 2025 |

| Distribution Channel | Supermarkets and Hypermarkets | 43.8% | 2025 |

| Region | Asia Pacific | 45.8% | 2025 |

By Pricing

To access detailed market analysis, Request Sample

Mass products dominate at 70.0% market share (2025). This segment comprises the high-volume everyday hygiene products that form the consumption backbone in both developed and emerging markets. Unilever’s Lifebuoy, P&G’s Pantene Aqua, and Colgate Cavity Protection represent category-entry products consumed by billions of consumers globally. The mass segment grows with population and income penetration in emerging markets, creating a reliable, albeit modest-growth, volume base for FMCG manufacturers.

Premium products at 30.0% are growing at ~3.8% CAGR, nearly 2× the overall market rate. This segment encompasses organic, natural, dermatologist-developed, and sustainably packaged hygiene products priced above category average. China’s premiumization story is the most powerful driver, with Chinese consumers trading up from Japanese-imported baby care products to domestic ultra-premium brands at an extraordinary pace.

By Usability

Disposable products dominate at 65.8% of market revenue (2025). The disposable category’s leadership reflects the embedded consumer value proposition of single-use hygiene products: guaranteed microbial safety, convenience of disposal, and absence of laundering effort. For the 2.3 Billion people globally did not have access to a handwashing facility with water and soap at home, making disposable products not merely a preference but a functional necessity.

Reusable products at 34.2% encompass a diverse range, including period underwear, menstrual cups, reusable cloth diapers, bamboo wipes, refillable soap dispensers, and reusable face masks. This category is driven by environmental consciousness, EU regulatory pressure, and the compelling lifetime cost economics of reusable products.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

|

Asia Pacific |

45.8% |

China and India’s population, rising middle-class disposable income, and increasing feminine hygiene awareness |

|

North America |

22.6% |

Premium product premiumization, post-COVID sustained hygiene habit elevation, ageing baby boomer incontinence product demand |

|

Europe |

18.7% |

EU sustainability regulations are driving reusable product adoption, and Germany and France premium organic hygiene demand |

|

Latin America |

7.1% |

Brazil and Mexico urbanisation and hygiene awareness programs, rising feminine hygiene awareness campaigns |

|

MEA |

5.8% |

GCC premium hygiene product demand, Sub-Saharan Africa feminine hygiene awareness programs |

Asia Pacific’s 45.8% market dominance (2025) is underpinned by the sheer scale of the region’s 4.5 Billion population and the extraordinary pace of per-capita hygiene spend growth. China’s personal hygiene market growth is driven by baby diapers, feminine hygiene, and oral care as the three largest subcategories. India’s market is propelled by government hygiene awareness programs (Swachh Bharat) and the world’s fastest-expanding middle class, adding new hygiene product consumers annually.

North America’s 22.6% share (2025) reflects a mature market driven by premiumization, product innovation, and the ageing boomer demographic’s expanding incontinence product requirements. Europe’s 18.7% share (2025) is being reshaped by the most ambitious sustainability regulation globally. The EU Single-Use Plastics Directive, the forthcoming EU Green Claims Directive (verified sustainability product claims), and national biodegradability standards in Germany and France are forcing the fastest material innovation cycle in European personal hygiene history.

Competitive Landscape

The global personal hygiene market is moderately concentrated at the brand tier, with P&G, Unilever, and Kimberly-Clark collectively accounting for approximately 35–40% of total market revenue.

|

Company Name |

Brand / Product Line |

Market Position |

Core Strength |

|

Procter & Gamble |

Pampers, Whisper, Oral-B |

Dominant Market Leader |

World’s #1 consumer goods company in personal hygiene, Pampers is the #1 baby diaper globally |

|

Unilever |

Lifebuoy, Closeup, Pepsodent, Vaseline |

Market Leader |

Personal care and hygiene brands sold in 190 countries, Lifebuoy handwash program |

|

Kimberly-Clark |

Huggies, GoodNites, DryNites, Poise, Plenitud, U by Kotex, Kotex, Intimus |

Market Leader |

Depend adult incontinence market leader in North America, Kotex feminine hygiene brand |

|

Kenvue |

Johnson’s Baby, Stayfree, Listerine, Carefree, Desitin |

Strong Challenger |

Healthcare and consumer hygiene convergence positioning; Listerine is world’s #1 mouthwash |

|

Colgate-Palmolive Company |

Colgate, Tom's of Maine, Hello, Elmex, Meridol, Sorriso, Palmolive, Softsoap, Protex |

Strong Challenger |

World’s #1 toothpaste and toothbrush brand (Colgate), Palmolive personal wash dominance |

|

Kao Corporation |

Laurier, Merries, Relief, Sanina, ClearClean, DeepClean, PureOra |

Established |

Japan’s largest hygiene and personal care company, Laurier #1 feminine hygiene brand in Japan and Southeast Asia |

The top five companies, capture approximately 50–55% of total market value. The remaining 45–50% is distributed across regional brands, specialist hygiene manufacturers, retail private label, and a long tail of direct-to-consumer digital brands.

Key Company Profiles

Procter & Gamble

Procter & Gamble is the world’s largest consumer goods company and the dominant force in global personal hygiene, with hygiene-related brands.

- Key Brands: Pampers, Whisper, Oral-B.

- Recent Developments: In March 2026, Procter & Gamble introduced Pampers AMORE, described as the most premium and absorbent diaper in the Pampers range.

- Strategic Focus: Superior product experience as brand differentiation vs. private label; sustainable packaging and formulation as regulatory compliance + consumer positioning; premium tier premiumization in China and India; connected device strategy through Oral-B iO and healthcare product digital integration.

Unilever

Unilever is the second-largest global personal hygiene company, with personal care brands. Unilever’s hygiene portfolio spans 35+ brands across 190 markets.

- Key Brands: Lifebuoy, Closeup, Pepsodent, Vaseline.

- Recent Developments: In April 2025, Unilever acquired the personal care brand Wild, marking another step in the optimisation of Unilever’s portfolio towards premium and high-growth spaces as part of the Growth Action Plan 2030.

- Strategic Focus: Science-led product superiority in skin hygiene; Lifebuoy’s social mission as emerging market expansion engine; premiumization through Dove Masterbrand; operational excellence and cost reduction following Nelson Peltz activist pressure; Beauty & Wellbeing separation as portfolio optimization strategy.

Kimberly-Clark

Kimberly-Clark is a global personal hygiene specialist and holds dominant positions in baby care, feminine hygiene, adult incontinence, and professional hygiene.

- Key Brands: Huggies, GoodNites, DryNites, Poise, Plenitud, U by Kotex, Kotex, Intimus.

- Recent Developments: In April 2024, Kimberly-Clark launched Kleenex Snap & Go in the United States, introducing a new portable tissue format aimed at enhancing convenience and hygiene in everyday, on-the-go situations.

- Strategic Focus: Powering Care growth strategy: premium tier leadership in developed markets; emerging market volume growth (China, India, Latin America) through Huggies and Kotex; Depend adult incontinence as highest-growth, highest-margin strategic priority; sustainable materials innovation reducing environmental footprint 50% by 2030.

Colgate-Palmolive Company

Colgate-Palmolive commands the world’s most dominant single-brand market share position in any personal hygiene category, Colgate toothpaste in global oral hygiene, and an extraordinary competitive position sustained across years of consistent brand investment.

- Key Brands: Colgate, Tom's of Maine, Hello, Elmex, Meridol, Sorriso, Palmolive, Softsoap, Protex.

- Recent Developments: In December 2024, Colgate-Palmolive (India) Limited unveiled a new sensorially captivating range of MaxFresh, that seamlessly blends its refreshing power with fun, flavour and aesthetics.

- Strategic Focus: Oral care category leadership defense and premiumization; naturals adjacency through Hello and Tom’s of Maine; personal care (Palmolive, Softsoap) share gain in North America; digital oral health through Colgate Connected Electric Toothbrush and AI app integration; emerging market volume growth in Africa and Southeast Asia.

Market Concentration Analysis

The global personal hygiene market exhibits moderate-to-high concentration at the branded goods tier and high fragmentation at the distribution and private label tier. P&G, Unilever, and Kimberly-Clark collectively generate approximately USD 90–95 Billion in hygiene-related revenue, representing 14–16% of the USD 612.90 Billion total market. The top five companies account for approximately 25–30% of total market value, reflecting the relatively low concentration for a category of this size and maturity.

The moderate concentration reflects the market’s breadth, spanning baby care, feminine hygiene, oral care, disinfection, and incontinence products in categories with distinct competitive dynamics, consumer preferences, and regional champions. Consolidation has been modest compared to other FMCG categories.

Investment & Growth Opportunities

Fastest Growing Segments

Premium products (CAGR ~3.8%), reusable hygiene (CAGR ~4.2%) represent the highest-growth investment vectors. Africa’s feminine hygiene market growth and the India personal hygiene market growth offer the highest volume growth opportunities in absolute terms.

Emerging Markets

Sub-Saharan Africa’s population and below-30% feminine hygiene penetration represent the largest underpenetrated personal hygiene market globally. India’s Northeast states, rural Bangladesh, and rural Indonesia represent secondary expansion frontiers where hygiene product access is increasing through mobile commerce and government distribution programs. The GCC premium hygiene market (UAE, Saudi Arabia, Qatar) is growing, supported by high-income demographics and Vision 2030’s expanding consumer class.

Venture Investment Trends

Personal care and hygiene attracted investments in global venture investment, with sustainable hygiene, smart oral care, and femtech hygiene leading subsegment investment.

- Key investment themes: Plant-based and biodegradable hygiene materials, period equity brands serving emerging markets, AI-powered personalized hygiene routines, connected oral care devices, and reusable feminine hygiene product brands.

- Government and development finance: World Bank’s Hygiene for Health Initiative, UNICEF WASH programs, and Gates Foundation Menstrual Health investments collectively deploy investments in hygiene market development across Sub-Saharan Africa and South Asia, creating commercial market infrastructure that benefits first-mover FMCG brands.

Future Market Outlook (2026-2034)

The global personal hygiene market is positioned for sustained, broad-based growth through 2034. From USD 612.90 Billion in 2025, the market is forecast to reach USD 784.00 Billion by 2034, at a 2.69% CAGR. This growth trajectory is among the most reliable in all of consumer goods, underpinned by three universally applicable structural drivers: population growth adding new global consumers; urbanization expanding retail access and consumer spending power; and post-COVID hygiene awareness sustaining elevated adoption of hand hygiene, disinfection, and antimicrobial products as permanent behavioral norms rather than temporary crisis responses.

Between 2026 and 2030, the most transformative developments will be the widespread adoption of sustainable product formats, biodegradable pads, reusable incontinence products, and plastic-free packaging, driven by the EU’s expanding Single-Use Plastics Directive and equivalent legislation in UK, Australia, and select U.S. states. The 2030–2034 period will be defined by the maturation of connected hygiene devices, smart toothbrushes, AI-guided incontinence management, period tracking-integrated feminine hygiene subscriptions, creating a personal hygiene market that generates recurring digital revenue alongside physical product consumption.

Research Methodology

Primary Research

Primary research for this report included structured interviews with 140+ industry stakeholders in 2025, including FMCG product managers, retail category buyers, supply chain directors, packaging sustainability managers, and women’s health specialists. Geographic coverage included North America, Europe, China, India, Japan, Brazil, and Sub-Saharan Africa. Primary insights validated segment-level market sizing, pricing tier dynamics, and sustainable product adoption timelines.

Secondary Research

Secondary research encompassed Euromonitor International personal care market data, Mintel hygiene product trends, IRI/Nielsen retail sales data, company annual reports and ESG disclosures, FDA and EMA regulatory databases, Ellen MacArthur Foundation plastics data, WHO and UNICEF WASH statistics, and patent filing databases for hygiene product innovation. Over 280 secondary sources were reviewed and synthesized.

Forecasting Models

Market size forecasts were developed using a bottom-up product category aggregation validated against top-down methodology. Key inputs include global population growth, urbanization rates, per-capita income projections, e-commerce penetration curves, and sustainability regulation implementation schedules.

Personal Hygiene Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Product Types Covered |

|

| Pricings Covered | Mass Products, Premium Products |

| Usabilities Covered | Disposable, Reusable |

| Distribution Channels Covered | Hospital Pharmacies, Supermarkets and Hypermarkets, Online Stores and Pharmacies, Convenience Stores and Retail Pharmacies, Others |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | Procter & Gamble, Unilever, Kimberly-Clark, Kenvue, Colgate-Palmolive Company, Kao Corporation, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the personal hygiene market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the global personal hygiene market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's Five Forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the personal hygiene industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Personal Hygiene Market Report

The global personal hygiene market was valued at USD 612.90 Billion in 2025 and is projected to reach USD 784.00 Billion by 2034, growing at a CAGR of 2.69%.

Asia Pacific leads with 45.8% revenue share (2025), driven by China and India’s growing population, rising middle class incomes, and expanding feminine hygiene product penetration.

Mass products dominate with 70.0% share (2025). Premium products at 30.0% are growing fastest at ~3.8% CAGR through 2034.

Reusable products are fastest growing, driven by EU Single-Use Plastics regulation, environmental consumer preferences, and the period underwear and menstrual cup markets.

Key market players include Procter & Gamble, Unilever, Kimberly-Clark, Kenvue, Colgate-Palmolive Company, and Kao Corporation.

Key drivers include post-COVID elevated hygiene consciousness, Asia Pacific urbanization, ageing population incontinence demand, premium product premiumization, and sustainable format innovation.

Key trends include sustainable/plastic-free product formats, menstrual health equity movement, personalized dermatologist-formulated products, subscription D2C models, and connected smart hygiene devices.

Premium products represented 30.0% of market revenue in 2025. Organic cotton pads, biodegradable wipes, and microbiome-friendly formulations lead premium growth.

Key challenges include environmental concerns on disposable plastics, raw material cost volatility, price sensitivity in emerging markets, private label competition, and regulatory compliance complexity across markets.

Top opportunities include Africa’s feminine hygiene expansion, biodegradable and organic product brands, adult incontinence in ageing demographics, connected smart hygiene devices, and Asia Pacific premium tier growth.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)