Plant-based Seafood Market Size, Share, Trends and Forecast by Product Type, Distribution Channel, and Region, 2026-2034

Global Plant-based Seafood Market Size, Share, Trends & Forecast (2026-2034)

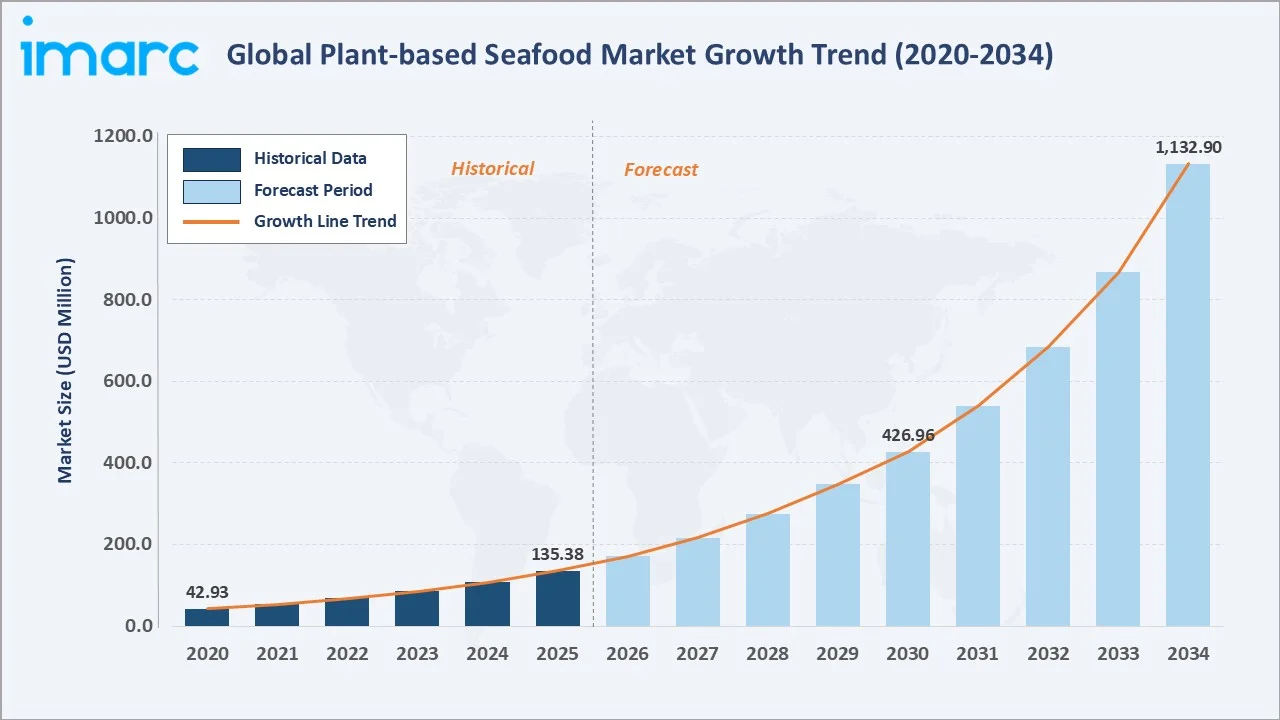

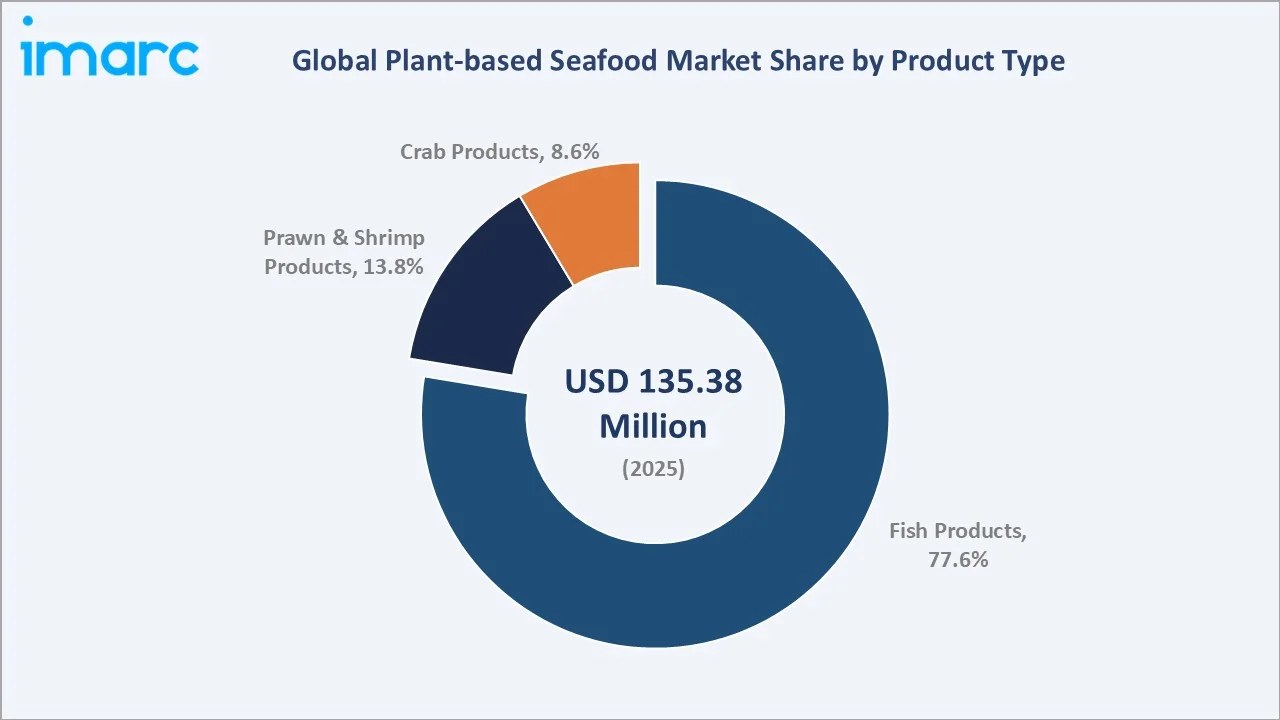

The global plant-based seafood market size was valued at USD 135.38 Million in 2025 and is projected to reach USD 1,132.90 Million by 2034, exhibiting a CAGR of 25.83% during the forecast period 2026-2034. The market's exceptional growth stems from rising veganism, flexitarian dietary shifts, and growing consumer concerns about overfishing and ocean sustainability.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 135.38 Million |

|

Forecast Market Size (2034) |

USD 1,132.90 Million |

|

CAGR (2026-2034) |

25.83% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

North America (38.4% share, 2025) |

|

Fastest Growing Region |

Asia Pacific |

|

Leading Product Type |

Fish Products (77.6%, 2025) |

|

Leading Distribution Channel |

Supermarkets and Hypermarkets (51.2%, 2025) |

The chart below illustrates the global plant-based seafood market growth trajectory from 2020 through 2034, contrasting historical expansion against a sustained forecast curve powered by shifting dietary habits, sustainability concerns, and continuous product innovation.

To get more information on this market, Request Sample

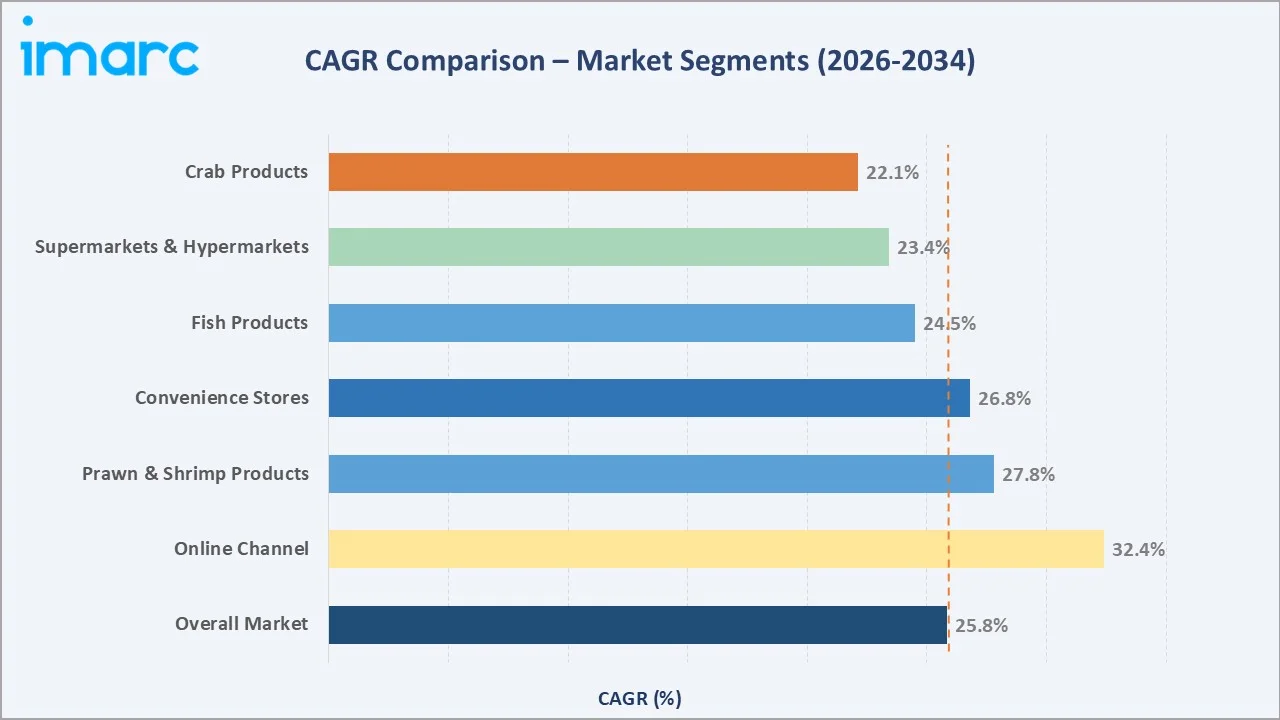

The segment-level CAGR chart below highlights the online channel and prawn & shrimp products as the fastest-growing sub-categories within the global plant-based seafood market forecast through 2034, both outpacing the overall market CAGR of 25.83%.

Executive Summary

The global plant-based seafood market is undergoing a transformative growth phase, driven by accelerating adoption of flexitarian and vegan lifestyles, mounting environmental concerns surrounding conventional fisheries, and significant product innovation across texture, flavor, and protein formulation. Valued at USD 135.38 Million in 2025 - up from USD 42.93 Million in 2020 - the market is forecast to reach USD 426.96 Million by 2030 and USD 1,132.90 Million by 2034, registering a robust CAGR of 25.83%.

Fish products command a dominant 77.6% share in 2025, backed by consumer familiarity with fish-based formats such as fillets, burgers, and fish sticks. The prawn and shrimp products segment, holding 13.8%, is projected to grow at an above-average pace as manufacturers improve textural replication using konjac, soy, and algae-based protein blends. Supermarkets and hypermarkets account for 51.2% of global distribution, while the online channel's 24.6% share is expanding rapidly as D2C brands and e-grocery platforms gain traction, growing at an estimated CAGR of 32.4% through 2034.

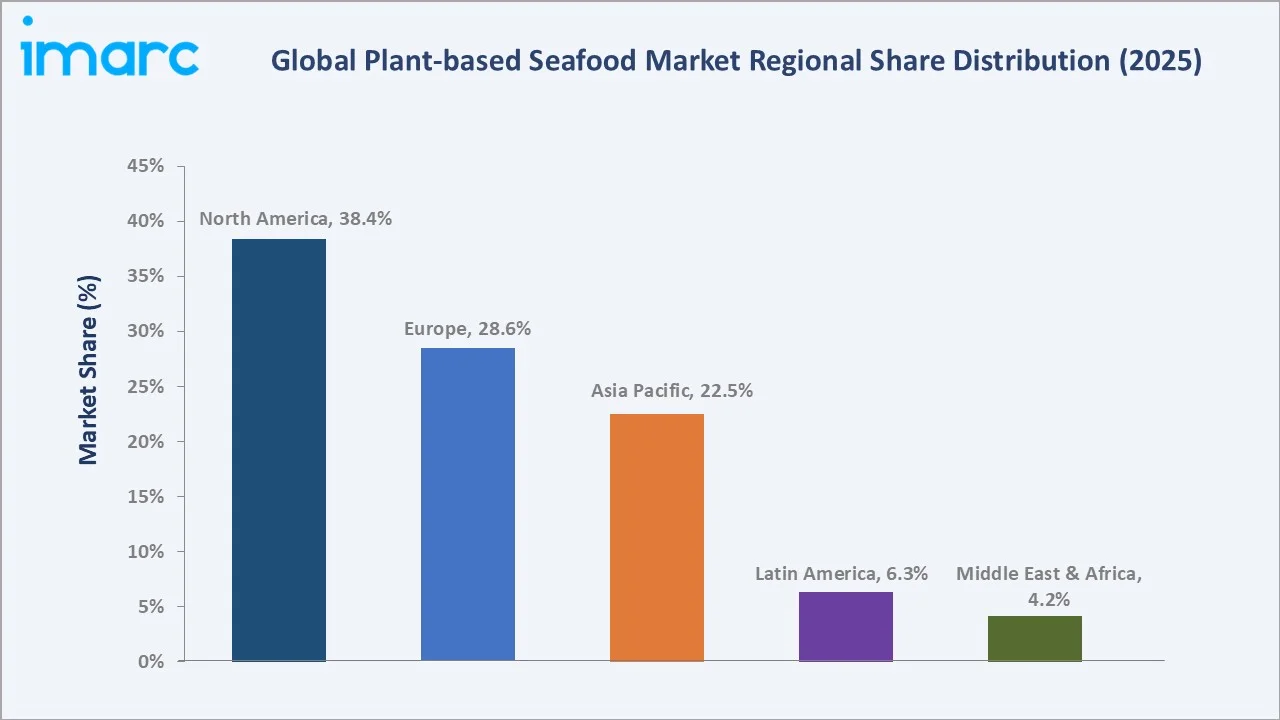

North America leads with 38.4% of global revenue in 2025, underpinned by established plant-based food retail, regulatory support for sustainable proteins, and high consumer willingness to pay premium pricing. Europe holds 28.6%, driven by EU Farm-to-Fork sustainability mandates and rising veganism. The market's outlook remains strongly positive as premiumization, mainstream retail adoption, and continuous R&D investment converge to drive long-term category expansion.

Key Market Insights

|

Insight |

Data |

|

Largest Product Type |

Fish Products – 77.6% share (2025) |

|

Fastest Growing Product Segment |

Prawn & Shrimp Products (~27.8% CAGR) |

|

Largest Distribution Channel |

Supermarkets and Hypermarkets – 51.2% (2025) |

|

Fastest Growing Distribution Channel |

Online – 32.4% CAGR (2026-2034) |

|

Leading Region |

North America – 38.4% revenue share (2025) |

|

Top Companies |

Conagra Brands, Inc., Monde Nissin, Ocean Hugger Foods, Inc, Century Pacific Food Inc., and SoFine Foods B.V. |

|

Market Opportunity |

Expanding vegan/flexitarian demographics and retail mainstreaming |

Key Analytical Observations Supporting The Above Data:

- Fish products' 77.6% dominance in 2025 reflects strong consumer recognition of fish-based formats and early-mover advantage by brands such as Gardein (Conagra Brands, Inc.), Quorn (Monde Nissin), and Ahimi (Ocean Hugger Foods.), which have developed best-in-class tuna, salmon, and fish cake alternatives using legume and algae proteins.

- Prawn and shrimp products (13.8% share, 2025) are the fastest-growing sub-segment at ~27.8% CAGR, benefiting from konjac and mycoprotein-based texturization advances. Sophie's Kitchen is leading innovation in commercially scaled plant-based shrimp formats, with expansion into premium foodservice channels.

- Supermarkets and hypermarkets account for 51.2% of distribution in 2025, reflecting successful mainstreaming beyond specialty health stores. Retailers such as Whole Foods ,and Tesco have dedicated plant-based sections prominently featuring seafood alternatives.

- The online channel holds 24.6% share in 2025, the fastest-growing channel at an estimated CAGR of 32.4% through 2034. Subscription-based delivery models, D2C brands, and integration with meal kit services are the primary growth levers.

- North America's 38.4% global dominance is supported by an estimated 9.7 million vegans in the U.S. in 2025, alongside high per-capita spending on premium and sustainable food products.

- Asia Pacific (22.5% share, 2025) represents the highest-potential emerging opportunity. Governments in Singapore, Japan, and China are actively funding alternative protein R&D, and the region's deep cultural affinity for seafood creates a natural conversion pathway for plant-based formats.

Global Plant-based Seafood Market Overview

Plant-based seafood refers to food products formulated from non-animal protein sources - including soy, pea protein, wheat gluten, algae, konjac, and mycoprotein - designed to replicate the texture, flavor, and appearance of conventional seafood. The product range includes alternatives to fish fillets, tuna, shrimp, crab, calamari, and scallops, served across retail grocery, food service, and direct-to-consumer channels.

The industry sits at the intersection of the broader alternative protein sector and the global seafood industry. Growth is supported by macroeconomic tailwinds including rising awareness of ocean depletion, increasing consumer health consciousness, and regulatory initiatives promoting sustainable food systems - notably the EU Farm-to-Fork Strategy and Singapore's "30 by 30" food security goal. Product innovation in protein sourcing, flavor science, and scalable manufacturing is structurally reshaping this high-growth category.

Market Dynamics

To access detailed market analysis, Request Sample

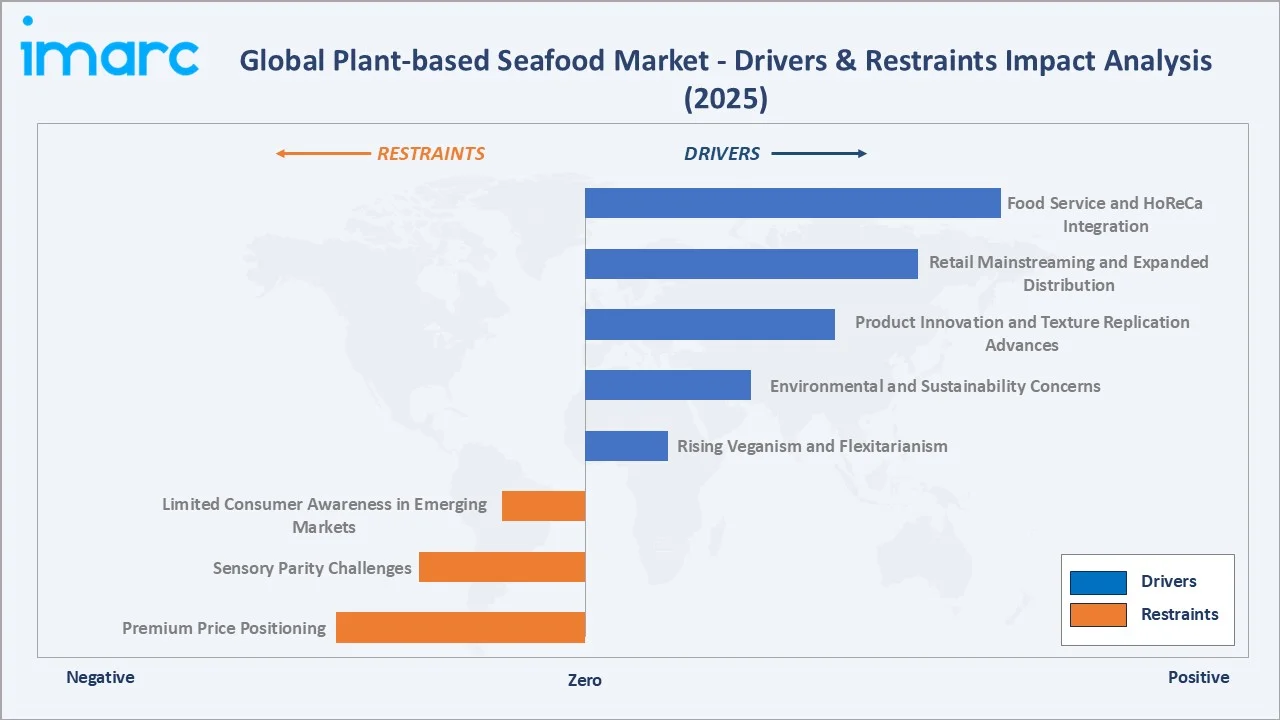

Market Drivers

- Rising Veganism and Flexitarianism: Around 1 % of the global population identified as vegan are actively seeking protein variety while reducing conventional meat and seafood consumption, creating a rapidly expanding demand base for plant-based seafood alternatives.

- Environmental and Sustainability Concerns: FAO data indicates over 35% of global fish stocks are overfished as of 2024. Consumer awareness of ocean ecosystem damage, plastic pollution in fisheries, and the carbon footprint of conventional aquaculture is creating strong pull toward sustainable, plant-derived seafood alternatives.

- Product Innovation and Texture Replication Advances: Significant R&D investment in protein texturization - including high-moisture extrusion technology, mycoprotein fermentation, and algae-based fatty acid incorporation - is closing the sensory gap between plant-based and conventional seafood. New launches in 2024-2025 include items achieving near-identical mouthfeel for tuna, shrimp, and scallops.

- Retail Mainstreaming and Expanded Distribution: Global supermarket chains now allocate permanent shelf space to plant-based seafood. The number of U.S. SKUs in the category has grown significantly in recent years, reflecting both expanding brand portfolios and increasing retailer confidence.

Market Restraints

- Premium Price Positioning: Plant-based seafood products typically command a significant price premium over conventional alternatives, limiting mass-market penetration, particularly in price-sensitive emerging markets where traditional seafood remains more affordable.

- Sensory Parity Challenges: Despite significant R&D advances, replicating the exact flakiness, umami depth, and cooking behavior of fish remains technically demanding. Consumer rejection rates remain higher for plant-based shrimp and whole-cut formats compared to processed fish formats.

- Limited Consumer Awareness in Emerging Markets: In Asia Pacific, Latin America, and Middle East & Africa, consumer familiarity with plant-based seafood remains low beyond urban centers, representing a significant category education cost burden for entering brands.

Market Opportunities

- Food Service and HoReCa Integration: Restaurant, hotel, and catering sectors represent a largely untapped revenue opportunity. Fine dining establishments globally are beginning to incorporate plant-based seafood as premium menu items, with dishes such as plant-based ceviche, shrimp tacos, and tomato-based tuna sushi rolls gaining traction.

- Asia Pacific Expansion: The region's deep culinary affinity for seafood, combined with rapid urbanization and government support for alternative proteins (e.g., Singapore's USD 144 Million Good Food Innovation Fund), creates a compelling growth corridor for established Western brands and local innovators alike.

- Private Label and Retailer Brand Development: Major chains including Lidl, Aldi, and Target are launching private-label plant-based seafood lines, reducing purchase barriers through lower price points and driving significant volume growth in mainstream grocery.

Market Challenges

- Supply Chain Scalability: Sourcing consistent, high-quality plant proteins, particularly specialty ingredients such as seaweed-derived alginates and pea protein isolates - at commercial scale remains a bottleneck for several mid-tier manufacturers.

- Regulatory Variability: Labeling regulations for plant-based seafood products differ significantly across markets. In the EU, restrictions on the use of terms like tuna or shrimp for non-animal products are under active debate, creating compliance complexity for brands seeking pan-regional distribution.

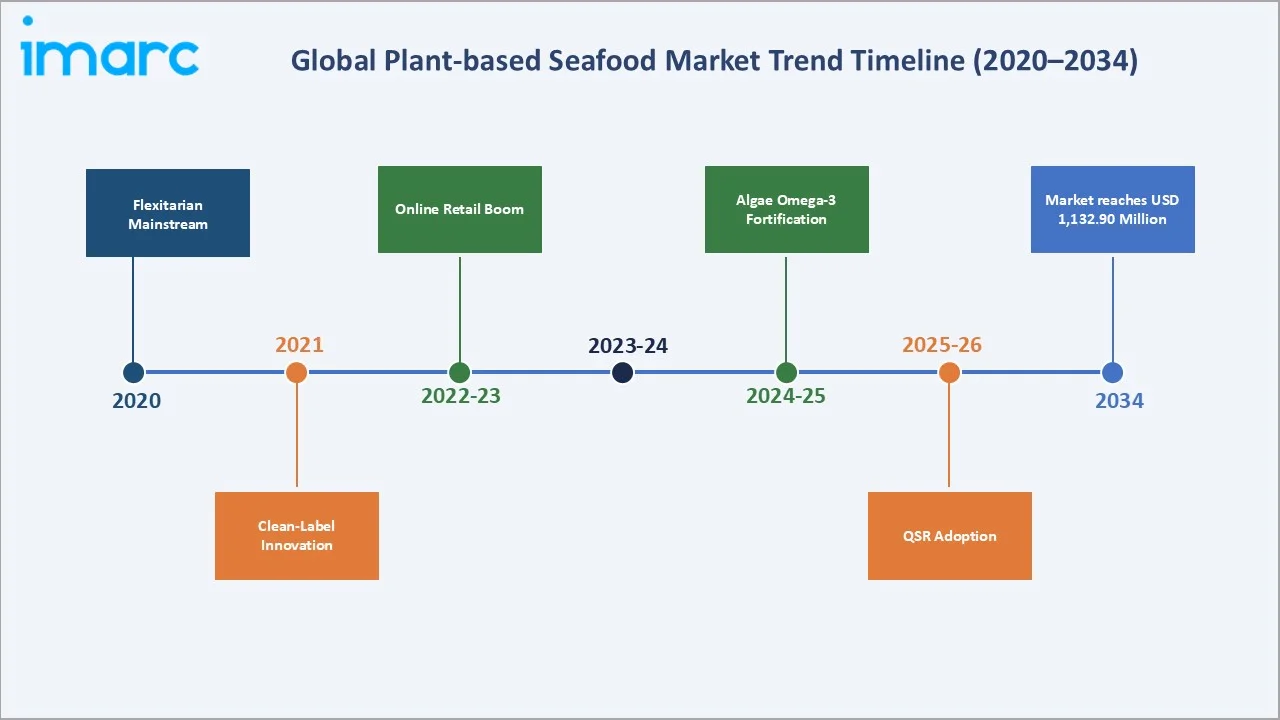

Emerging Market Trends

1. Whole-Cut Seafood Analogs

The industry is rapidly advancing beyond minced or processed formats toward whole-cut alternatives - including plant-based salmon fillets, whole shrimp, and crab legs. High-moisture extrusion technology has improved fiber alignment sufficiently for commercial launch.

2. Algae-Derived Omega-3 Fortification

Consumer demand for health-functional products is driving algae-based DHA and EPA omega-3 fortification of plant-based seafood. Products incorporating microalgae-derived fatty acids are increasingly featured in new product launches across North America and Europe, directly addressing the nutritional parity argument versus conventional fish.

3. Clean-Label and Allergen-Free Formulations

Soy and gluten-free plant-based seafood alternatives are gaining disproportionate share as formulation science advances. Brands using single-ingredient bases such as hearts of palm (for crab), jackfruit, and banana blossom are attracting consumers seeking minimally processed, transparent ingredient lists - a trend particularly prominent in European premium retail.

4. Online and Direct-to-Consumer Channel Growth

The direct-to-consumer model is reshaping category economics. Online platforms account for 24.6% of global plant-based seafood sales in 2025 and are growing at an estimated CAGR of 32.4% through 2034. Subscription-based seafood boxes are expanding customer lifetime value while generating proprietary first-party consumer data.

5. Foodservice and QSR Adoption

The quick service restaurant segment represents a high-volume emerging channel. In 2024-2025, major restaurant chains in North America and Europe piloted plant-based fish sandwiches, shrimp tacos, and sushi alternatives. Successful mainstreaming in QSR could significantly accelerate consumer trial and subsequent retail purchase behaviour.

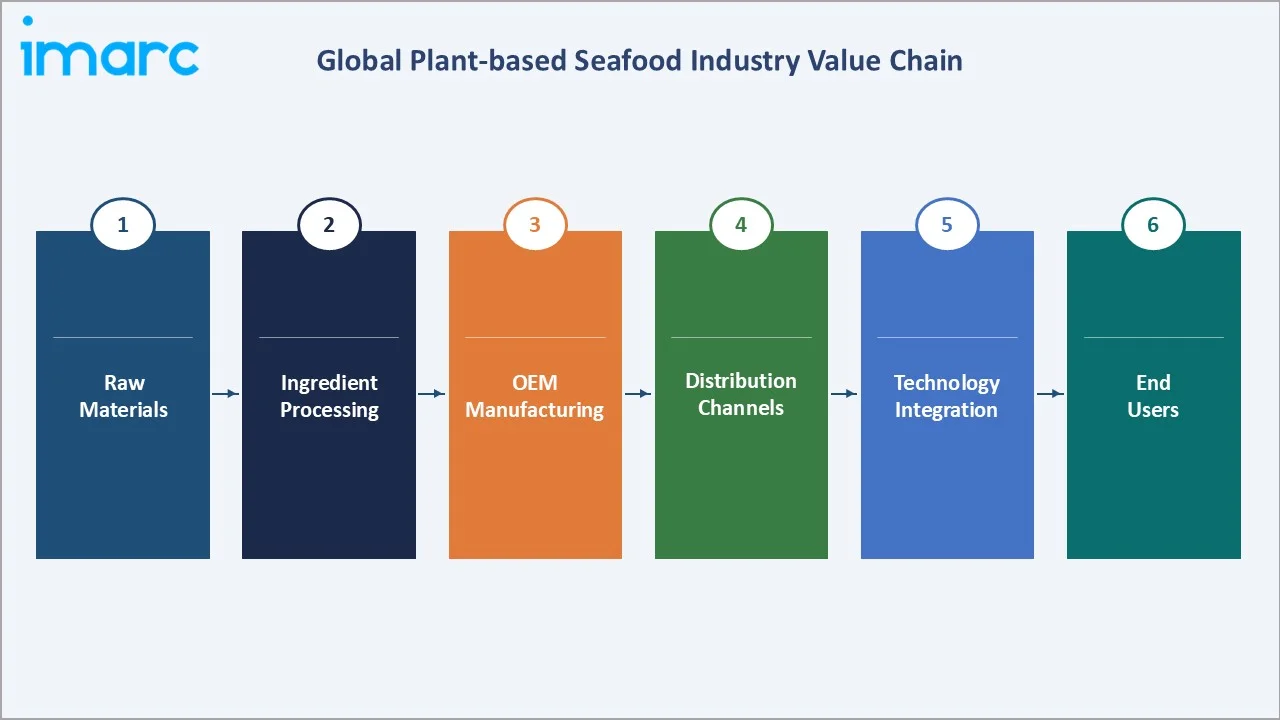

Industry Value Chain Analysis

The plant-based seafood value chain spans five key stages: raw material sourcing, ingredient processing, manufacturing, multi-channel distribution, and final consumption by retail and food service end users.

|

Stage |

Key Players / Examples |

|

Raw Materials |

Legume & Soy Suppliers, Algae Cultivators, Konjac Growers |

|

Ingredient Processing |

Protein Isolates, Flavour & Texture Ingredient Makers, Omega-3 Processors |

|

Manufacturing |

Conagra Brands, Inc., Monde Nissin, Ocean Hugger Foods, Inc |

|

Distribution |

Supermarket Chains, Online Retailers, Specialty Distributors |

|

End Users |

Retail Consumers, Food Service Operators, HoReCa Sector |

Key value chain observations: Raw material suppliers - particularly large soy and pea protein processors such as Roquette and Cargill - wield significant upstream bargaining power. Mid-chain manufacturers compete primarily on product innovation, sensory quality, and go-to-market speed. Distribution stage dynamics are shifting, with online and D2C gaining share from traditional retail. The end user segment is bifurcating between retail consumers and institutional food service buyers, each requiring different price points and product formats.

Technology Landscape in the Plant-based Seafood Industry

Protein Texturization Technologies

High-moisture extrusion (HME) technology is the most widely adopted manufacturing process for whole-cut plant-based seafood analogs. HME applies heat, moisture, and mechanical shear to plant proteins primarily soy and pea—generating aligned fibrous structures that mimic muscle tissue. Manufacturers investing in advanced twin-screw extruders report significant improvements in textural fidelity versus prior-generation equipment.

Fermentation and Mycoprotein Innovation

Mycoprotein fermentation - pioneered by Quorn (Monde Nissin) - offers a high-fiber, high-protein matrix with naturally fish-like flakiness. Precision fermentation is an emerging technology direction, enabling production of specific seafood-flavor compounds such as methylamines and aldehydes using engineered microorganisms, creating authentic flavor profiles without conventional seafood ingredients.

Algae and Marine-Ingredient Integration

Microalgae cultivation technology is enabling cost-effective production of omega-3-rich DHA and EPA oils, iodine, and taurine compounds—nutrients naturally associated with seafood that are critical for product health positioning. Integration of seaweed-based hydrocolloids (carrageenan, agar) improves gel texture in shrimp and scallop analogs. The global algae protein market is witnessing strong growth, driven by rising demand from the alternative protein sector.

Flavor Science and Umami Replication

Advanced flavor science is addressing one of the sector's critical barriers. Enzyme-modification of plant proteins generates glutamate-rich savory notes. Yeast extracts and fermented ingredients add umami depth. Seaweed-sourced compounds provide authentic oceanic aroma. Companies including Givaudan and IFF launched dedicated plant-based seafood flavor systems in 2024-2025, signaling rapid maturation of this technological sub-field.

Market Segmentation Analysis

The report covers the following segments:

| Segment Category | Leading Segment | Market Share | Year |

|---|---|---|---|

| Product Type | Fish Products | 77.6% | 2025 |

| Distribution Channel | Supermarkets and Hypermarkets | 51.2% | 2025 |

| Region | North America | 38.4% | 2025 |

By Product Type

The plant-based seafood market is segmented by product type into Fish Products, Prawn & Shrimp Products, and Crab Products. Fish products dominated the market in 2025 with a 77.6% share, followed by Prawn & Shrimp at 13.8% and Crab Products at 8.6%.

To access detailed market analysis, Request Sample

Fish products command the majority 77.6% share in 2025. This dominance reflects the strong consumer familiarity with fish-based food formats - including fish cakes, fish fingers, and fish burgers - that have an established purchase pattern in both retail and food service. The subcategory benefits from relative formulation simplicity compared to whole-cut shrimp or crab analogs, enabling a wider range of brands to compete effectively.

By Distribution Channel

The plant-based seafood market is distributed through Supermarkets and Hypermarkets, Online channels, Convenience Stores, and Others. Supermarkets and hypermarkets dominated in 2025 with a 51.2% share, followed by Online (24.6%), Convenience Stores (15.8%), and Others (8.4%).

Supermarkets and hypermarkets dominate at 51.2% in 2025. Major retail chains including Whole Foods Market, Tesco, Carrefour, and Kroger have dedicated plant-based sections providing significant visibility. The online channel, commanding 24.6% of global sales in 2025, is the fastest-growing channel at an estimated CAGR of 32.4% through 2034. D2C subscription models, meal kit integrations, and specialty health e-commerce platforms are driving this growth.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

|

North America |

38.4% |

Strong vegan/flexitarian adoption, retail mainstreaming, regulatory support for sustainable foods |

|

Europe |

28.6% |

EU Farm-to-Fork Strategy, rising veganism in UK/Germany/Netherlands, foodservice expansion |

|

Asia Pacific |

22.5% |

Deep seafood culture converting to plant-based, rapid urban growth, government food-tech funding |

|

Latin America |

6.3% |

Growing middle-class health awareness, expanding vegan-friendly retail |

|

Middle East & Africa |

4.2% |

Halal-certified plant-based launches, rising health consciousness, urbanization |

North America commands 38.4% of global plant-based seafood revenue in 2025, valued at approximately USD 51.99 Million. The United States is the single most important national market, supported by the world's largest flexitarian consumer base. The U.S. plant-based food retail sector grew 7% year-over-year. Moreover, Canada is a secondary growth market, with high urban consumer awareness and supportive regulatory frameworks for novel proteins.

Competitive Landscape

|

Company Name |

Brand Name |

Market Position |

Core Strength |

|

Conagra Brands, Inc. |

Gardein |

Leader |

Mass-market distribution, mainstream supermarket presence globally |

|

Monde Nissin |

Quorn |

Leader |

Mycoprotein-based seafood, strong European retail distribution |

|

Ocean Hugger Foods, Inc |

Ahimi |

Challenger |

Tomato-based raw tuna alternative; food service specialization |

|

Century Pacific Food Inc. |

Loma Linda |

Challenger |

Canned plant-based seafood; value positioning, wide availability |

|

SoFine Foods B.V. |

SoFine |

Emerging |

Dutch brand; premium plant-based seafood targeting European retail |

The global plant-based seafood market's competitive landscape is moderately fragmented, with a mix of specialized plant-based brands, diversified alternative protein companies, and conventional food conglomerates with emerging plant-based divisions.

Key Company Profiles

Conagra Brands, Inc.

Conagra Brands, Inc. is a leading North American consumer packaged goods (CPG) company engaged in the manufacturing and marketing of branded food products. Headquartered in Chicago, the company operates across retail, foodservice, and international channels, with a strong focus on frozen, snacks, and staple food categories.

- Product Portfolio: Gardein's (a brand of Conagra Brands, Inc.) plant-based seafood lineup includes F'sh Filets, Crabless Cakes, and crispy plant-based fish products available in frozen format across major U.S. and Canadian supermarket chains.

- Recent Developments: In 2024, Conagra Brands unveiled new product innovations at the Natural Products Expo West, including Evol’s first seafood entrée and a new plant-based fish offering under Gardein. The launch highlights Conagra’s focus on expanding its plant-based and frozen portfolio, with leadership emphasizing enhanced culinary experience and innovation as key growth drivers.

- Strategic Focus: The company leverages its national distribution infrastructure and marketing capabilities to maintain mass-market price accessibility while investing in flavor improvement R&D across its plant-based portfolio.

Monde Nissin

Monde Nissin Corporation is a leading Philippine-based multinational food and beverage company, with a diversified portfolio spanning packaged foods and alternative proteins. The company operates globally, with a strong presence in Asia-Pacific and a growing footprint in plant-based foods through its ownership of Quorn.

- Product Portfolio: Quorn's seafood-adjacent range includes fishless fingers, breaded fillets, and battered alternatives. Products are widely available across European supermarkets with growing U.S. and Asian market presence.

- Recent Developments: In 2025, Monde Nissin is intensifying its focus on the alternative protein segment, including plant-based seafood adjacencies, as part of its growth strategy. The company is leveraging its Quorn portfolio to expand innovation and marketing efforts, with increased emphasis on frozen product campaigns and nutritional positioning to drive demand in the evolving plant-based category.

- Strategic Focus: The company focuses on leveraging its proprietary mycoprotein fermentation platform to develop next-generation textured protein products while supporting the company’s expansion strategy in the Asia-Pacific region.

Ocean Hugger Foods

Ocean Hugger Foods is an innovative plant-based seafood company known for Ahimi, a tomato-based raw tuna alternative. Headquartered in New York, the company targets both foodservice and retail channels, particularly sushi and premium dining applications.

- Product Portfolio: Ocean Hugger Foods’ plant-based seafood portfolio includes Ahimi (a tomato-based raw tuna alternative), primarily designed for sushi, poke, and foodservice applications across restaurant and retail sushi channels.

- Recent Developments: In 2021, Ocean Hugger Foods relaunched the market through a partnership with Nove Foods to expand distribution of plant-based seafood analogs globally. The collaboration leverages Nove’s manufacturing scale and retail network to launch an expanded product portfolio across retail and foodservice channels, signaling renewed momentum in the plant-based seafood category.

- Strategic Focus: Ocean Hugger Foods pursues a food service-first strategy targeting premium sushi restaurants and upscale casual dining, using chef endorsements to build brand credibility and consumer awareness.

Market Concentration Analysis

The global plant-based seafood market is moderately fragmented, characterized by a mix of specialized startups, diversified plant-based brands, and conventional food company sub-brands. The top five players - Conagra Brands, Inc., Monde Nissin, Ocean Hugger Foods, Inc, Century Pacific Food Inc., SoFine Foods B.V.- are estimated to collectively account for approximately 45-55% of global revenues in 2025.

Consolidation trends are emerging. Conagra Brands Inc.’s' ownership of Gardein and Monde Nissin's ownership of Quorn demonstrate the strategic interest of large food conglomerates. Private equity and venture capital investment in specialist plant-based seafood companies is expected to drive further M&A activity as the market scales, supporting consolidation and accelerated growth through the forecast period.

Regional fragmentation is significant. European markets feature a distinct set of regional specialists that do not compete head-to-head with North American leaders. Asia Pacific's nascent market features local players alongside entering Western brands.

Investment & Growth Opportunities

Fastest-Growing Segments

Online distribution and prawn & shrimp products represent the highest-growth investment opportunities. Companies building scalable D2C platforms and brands with leading shrimp textural replication capabilities are well-positioned for outsized returns in the forecast period.

Emerging Markets with High Potential

Asia Pacific - particularly Singapore, Japan, South Korea, and coastal Chinese cities - offers the highest-potential emerging market opportunity given government funding support, seafood-centric food culture, and rapid growth in health-conscious urban consumers. Latin America's Brazil and Mexico are secondary targets with growing retail infrastructure.

Venture and Strategic Investment Trends

The Good Food Institute reported significant global investment in alternative seafood over recent years. Corporate venture arms of companies such as Unilever, Nestlé, and Anheuser-Busch InBev have made strategic investments in plant-based seafood startups. Meanwhile, food technology accelerators in Singapore, Israel, and Netherlands are fostering a strong pipeline of innovations supporting the sector’s growth.

Future Market Outlook (2026-2034)

The global plant-based seafood market is forecast to reach USD 1,132.90 Million by 2034, growing at a CAGR of 25.83% from a USD 135.38 Million base in 2025. An intermediate milestone of USD 426.96 Million is projected for 2030, representing 3.2x growth from the 2025 base in just five years.

Technological disruptions shaping the outlook include commercial launch of precision fermentation-derived seafood flavor compounds (projected 2026-2027); wide deployment of high-moisture extrusion lines capable of producing whole-cut fish and shrimp analogs at commercial scale; and Integration of AI-assisted protein formulation tools is significantly reducing R&D cycles, accelerating product development and innovation timelines in the sector.

Industry transformation will be driven by regulatory tailwinds including potential EU mandates for sustainable protein in public institution food procurement—alongside mainstream consumer normalization of plant-based diets. The market’s long-term potential remains substantial, with even modest penetration of the conventional seafood sector translating into a significant addressable opportunity.

Research Methodology

Primary Research

IMARC conducted over 200 primary interviews with market participants including plant-based seafood manufacturers, retail buyers, food service operators, ingredient suppliers, and industry experts across North America, Europe, and Asia Pacific. Primary data was used to validate market size estimates, competitive positioning, and segment-level insights.

Secondary Research

Secondary research sources included published reports from the Good Food Institute, FAO fisheries data, Euromonitor International, NielsenIQ retail panel data, company annual reports and investor presentations, trade publications such as Food Navigator and New Food Magazine, and government databases across all covered regions.

Forecasting Models

Market forecasts were developed using a combination of bottom-up and top-down modeling. The bottom-up approach estimated revenues at the product category and regional level using distribution channel penetration rates, average selling price trends, and consumer adoption curves. Statistical regression models incorporating macroeconomic indicators - including GDP per capita, urbanization rates, and sustainability index scores - were used to calibrate regional forecast paths.

Plant-based Seafood Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Product Types Covered | Fish Products, Prawn and Shrimp Products, Crab Products |

| Distribution Channels Covered | Supermarkets and Hypermarkets, Convenience Stores, Online, Others |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Netherlands, China, Japan, Singapore, Brazil, Mexico, South Africa, UAE |

| Companies Covered | Conagra Brands, Inc., Monde Nissin, Ocean Hugger Foods, Inc, Century Pacific Food Inc., SoFine Foods B.V., etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the plant-based seafood market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the global plant-based seafood market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's five forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the plant-based seafood industry and its attractiveness.

- The competitive landscape allows stakeholders to understand their competitive environment and provides insight into the current positions of key players in the market.

Frequently Asked Questions About the Plant-based Seafood Market Report

The global plant-based seafood market size was valued at USD 135.38 Million in 2025, growing significantly from USD 42.93 Million in 2020.

The market is projected to reach USD 1,132.90 Million by 2034, exhibiting a CAGR of 25.83% during the 2026-2034 forecast period.

Fish products lead the market with a 77.6% share in 2025, owing to strong consumer familiarity and wide retail availability across North America and Europe.

North America leads with 38.4% of global revenue in 2025, driven by established retail infrastructure, high flexitarian adoption, and consumer willingness to pay a premium.

The online channel is the fastest-growing, holding 24.6% share in 2025 and expanding at approximately 32.4% CAGR through 2034, driven by D2C brands and e-grocery platforms.

Leading companies include Conagra Brands, Inc., Monde Nissin, Ocean Hugger Foods, Inc, Century Pacific Food Inc., and SoFine Foods B.V.

Key drivers include rising veganism/flexitarianism globally, overfishing concerns, product innovation in texture replication, and mainstream retail distribution expansion across major markets.

Primary challenges include a significant price premium over conventional seafood, sensory parity gaps in whole-cut formats, limited consumer awareness in emerging markets, and fragmented global labeling regulations.

Asia Pacific accounted for 22.5% of global plant-based seafood revenues in 2025 and is the fastest-growing region, supported by government alternative protein funding and deep seafood-centric food culture.

High-moisture extrusion, mycoprotein fermentation, algae-based omega-3 fortification, precision fermentation for flavor compounds, and AI-assisted protein formulation are key technology trends reshaping the industry.

The global plant-based seafood market is projected to reach USD 426.96 Million in 2030, representing approximately 3.2x growth from the 2025 base of USD 135.38 Million.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)