Podcasting Market Size, Share, Trends and Forecast by Genre, Format, and Region 2026-2034

Podcasting Market Size, Share, Trends & Forecast (2026-2034)

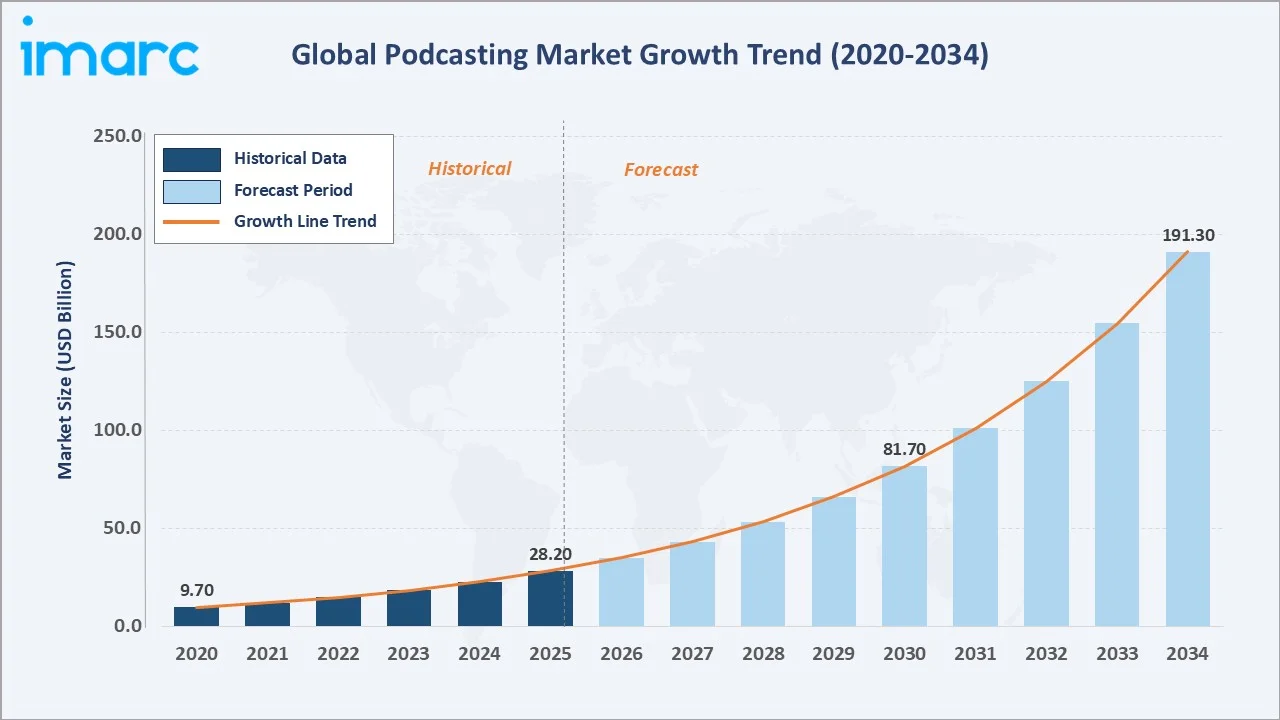

The global podcasting market was valued at USD 28.2 Billion in 2025 and is projected to reach USD 191.3 Billion by 2034, expanding at a CAGR of 23.71% during the forecast period (2026-2034). The podcasting market growth is driven by the proliferation of smartphones, widespread access to streaming platforms, the democratization of content creation, and the escalating availability of advertising opportunities.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 28.2 Billion |

|

Forecast Market Size (2034) |

USD 191.3 Billion |

|

CAGR (2026-2034) |

23.71% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region (2025) |

North America – 38.5% |

|

Fastest Growing Region |

Asia Pacific |

News and Politics leads genre segmentation with a 28.6% share in 2025, while Interviews commands the format segment at 34.8%. North America dominates regionally at 38.5%, with Asia Pacific emerging as the fastest-growing geography.

To get more information on this market, Request Sample

The market is fueled by rising advertising investments, subscription-based models, and exclusive content deals from major platforms, while advancements in streaming technology and AI-driven recommendations enhance user engagement. As brands increasingly leverage podcasts for targeted marketing and storytelling, the industry continues to evolve with new monetization strategies and global audience expansion.

Executive Summary

The global podcasting market continues to record exceptional expansion, cementing its position as one of the fastest-growing segments within the broader digital media landscape. Valued at USD 28.2 Billion in 2025, the market is forecast to reach USD 191.3 Billion by 2034, reflecting a remarkable CAGR of 23.71%.

The podcasting market forecast trajectory is underpinned by a global shift toward on-demand audio consumption, accelerating smartphone penetration in developing economies, and the rising sophistication of programmatic podcast advertising infrastructure. With an estimated 584 million monthly podcast listeners globally in 2025, the medium has transitioned from a niche format to a mainstream media channel.

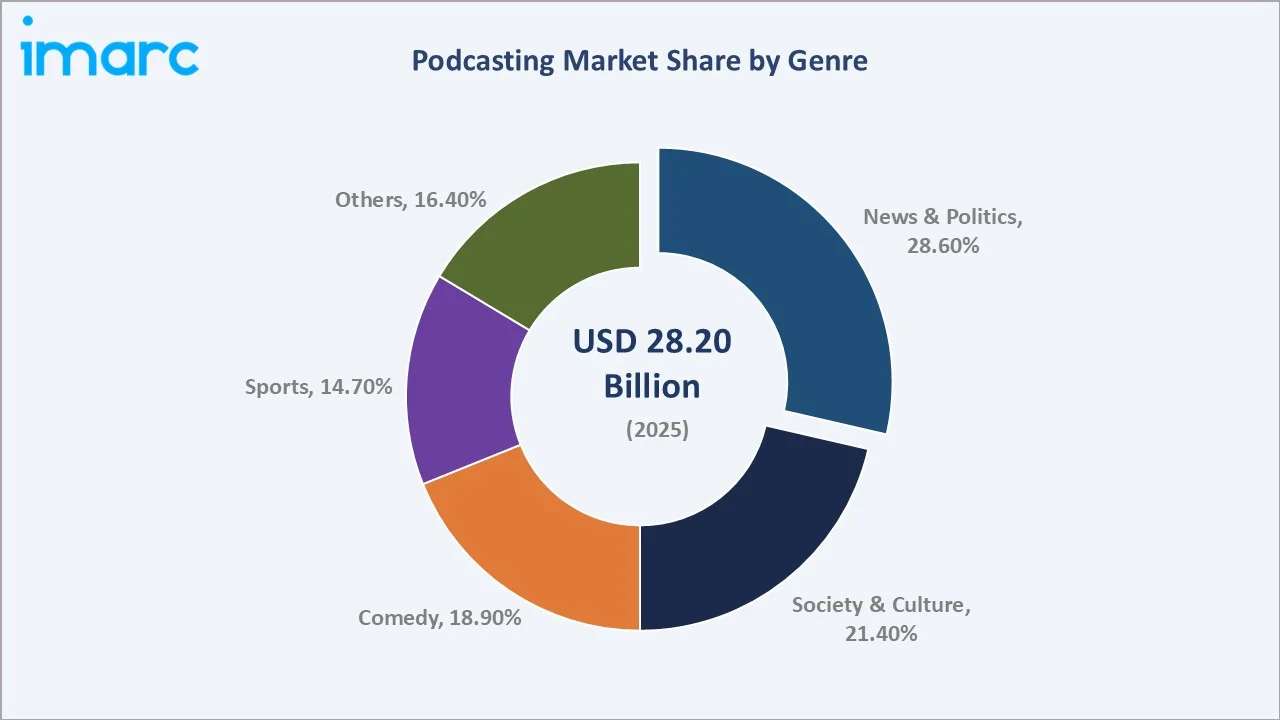

Content diversification is a defining characteristic of the current market environment. News and Politics, the dominant genre at 28.6% of the 2025 market share, is expanding in response to heightened civic engagement and independent journalism growth. Comedy, Society, and Culture genres are simultaneously attracting premium advertising spend due to their highly engaged, demographically attractive listener bases.

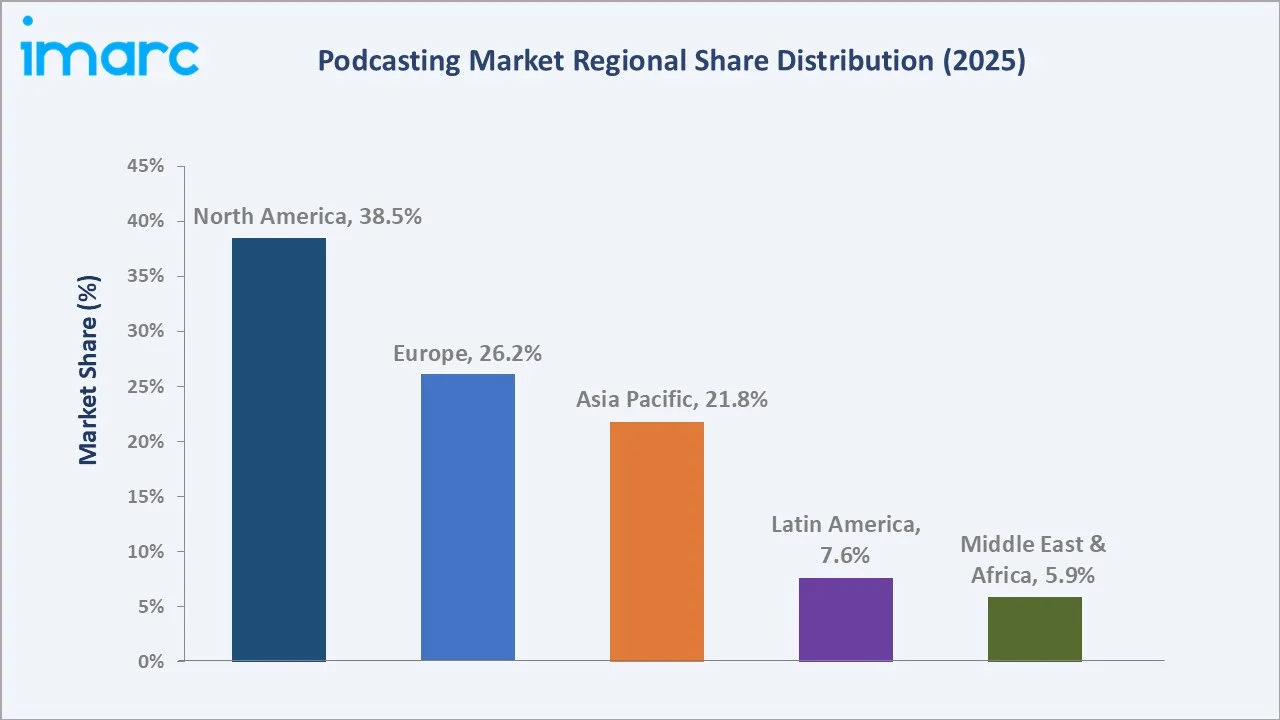

North America retains market leadership with a 38.5% share, anchored by a mature advertising ecosystem and high podcast listening rates. In the U.S. alone, over 55% of the population listens to podcasts monthly as of 2025. Asia Pacific - growing at the highest regional rate - represents the most compelling expansion frontier, as connectivity improvements and rising disposable incomes accelerate adoption across China, India, South Korea, and Southeast Asia.

Key Market Insights

|

Insight |

Data |

|

Largest Genre Segment |

News and Politics – 28.6% share (2025) |

|

Largest Format Segment |

Interviews – 34.8% share (2025) |

|

Leading Region |

North America – 38.5% share (2025) |

|

Fastest Growing Region |

Asia Pacific – highest CAGR (2026-2034) |

|

Global Monthly Listeners (2025) |

~584 million |

|

Top Companies |

Spotify, Apple, Amazon, iHeartMedia, Pandora, TuneIn |

|

Market Opportunity |

AI tools and video podcasting: transformational growth by 2034 |

Key Analytical Observations Supporting the Above Data:

- News and Politics leads genre segmentation with a 28.6% share (2025), fueled by global political engagement, the rise of independent journalism, and growing demand for real-time current affairs coverage through on-demand audio platforms.

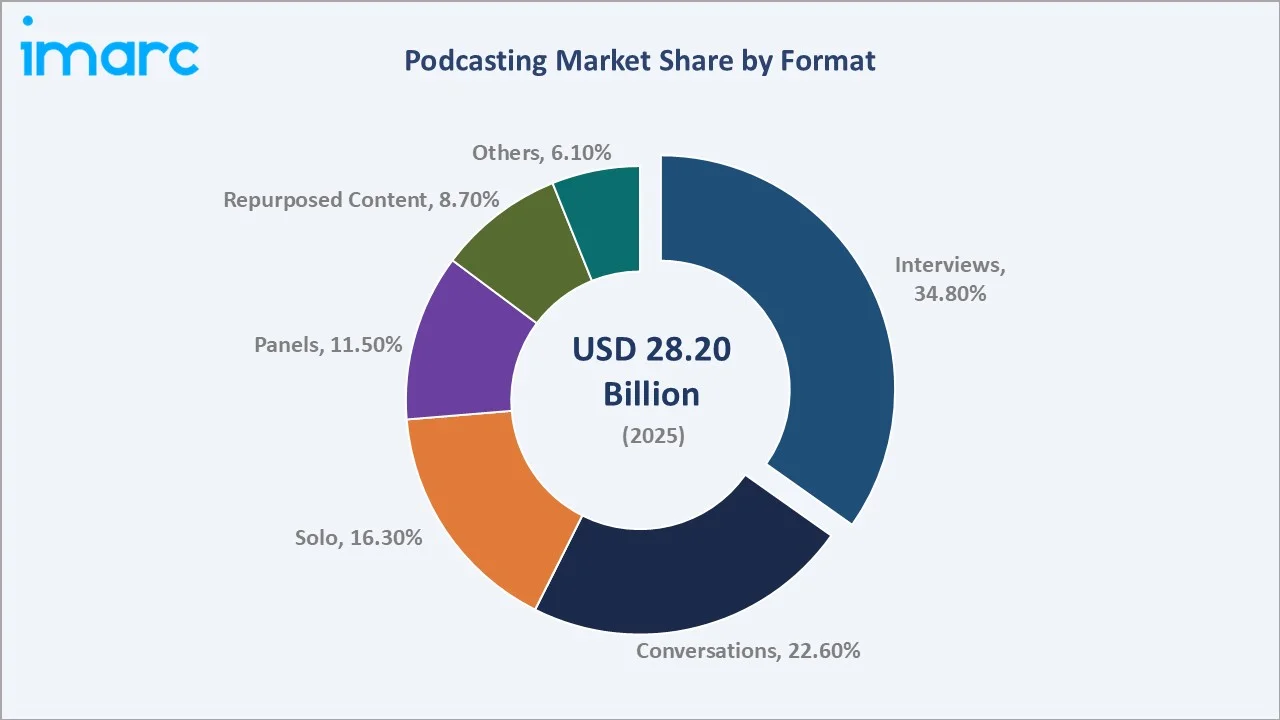

- Interview-format podcasts dominate with a 34.8% format share (2025), reflecting audience demand for authentic, conversation-driven, long-form content featuring credible guests and expert voices.

- North America commands 38.5% of global podcasting revenues (2025), bolstered by the world's most mature podcast advertising ecosystem and some of the highest per-capita listening rates globally.

- AI integration is reshaping production workflows, and real-time voice translation, automated transcription, and AI-driven episode personalization are expanding both creator capabilities and audience reach.

- Video podcasting is becoming a major monetization driver, with short-form video clips from podcast episodes generating millions of views on social platforms, attracting incremental advertising budgets.

- Premium subscriptions are emerging as a high-growth monetization layer, complementing advertising revenue and enabling creators to build sustainable direct audience relationships with exclusive content models.

Global Podcasting Market Overview

The global podcasting industry encompasses the creation, distribution, monetization, and consumption of digitally distributed audio and video episodic content across streaming platforms, podcast directories, dedicated apps, and smart devices. Podcasts span an expansive range of genres, from news and politics to comedy, sports, true crime, business, education, and niche interests, accessed by listeners on smartphones, smart speakers, tablets, computers, and connected vehicles.

The ecosystem encompasses independent creators, media companies, advertising networks, hosting platforms, analytics providers, and production tool vendors. Macroeconomic and demographic forces are structurally supportive. Rising global literacy and education levels are expanding audiences for educational and professional content. Urbanization and longer commuting patterns are creating sustained daily listening windows.

Declining data costs in emerging economies are democratizing access. The podcasting market trends through 2034 are shaped by these foundational shifts alongside technology cycles in AI, audio hardware, and platform economics, creating a uniquely robust multi-decade growth narrative.

Market Dynamics

To evaluate market opportunities, Request Sample

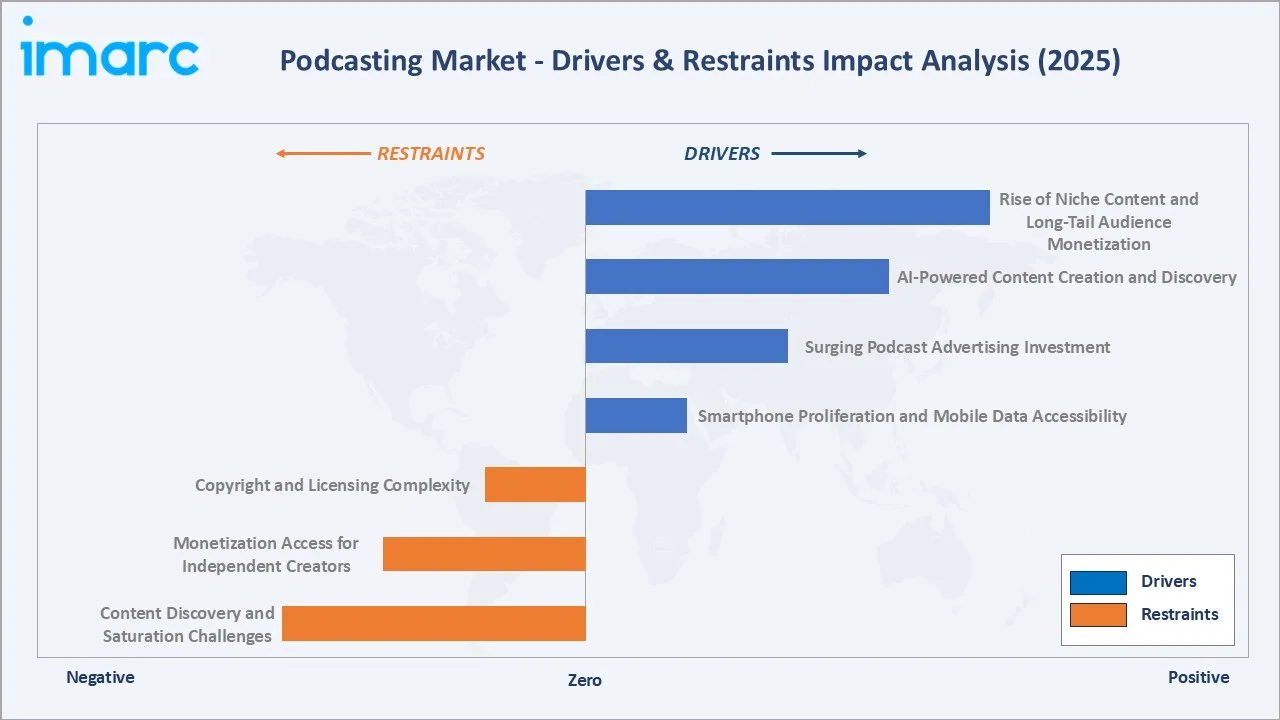

Market Drivers

- Smartphone Proliferation and Mobile Data Accessibility: Global smartphone users exceeded 6.8 billion in 2025, with mobile devices serving as the primary podcast consumption device globally. Declining mobile data costs in Asia Pacific, Latin America, and Africa are unlocking vast new listener populations.

- Surging Podcast Advertising Investment: Global podcast advertising revenue grew substantially year-over-year through 2025, with programmatic audio buying becoming a standard practice among major North American advertisers. iHeartMedia disclosed USD 140 million in Q4 2024 podcast revenue, exemplifying the scale of advertising monetization.

- AI-Powered Content Creation and Discovery: In 2025, Spotify introduced real-time voice translation for podcasts, enabling creators to reach global audiences without additional recordings, fundamentally expanding addressable listenership for any given show.

- Rise of Niche Content and Long-Tail Audience Monetization: There are approximately 4.5 to 4.6 million podcast shows available globally in 2025, and advertisers seeking precisely targeted demographics find podcasting uniquely effective. This long-tail content ecosystem drives platform engagement and overall market volume.

Market Restraints

- Content Discovery and Saturation Challenges: With millions of podcasts available, listener discovery has become a critical friction point. New creators face significant discoverability hurdles despite producing high-quality content, creating a concentration of listenership around established shows, and creating competitive barriers for emerging voices.

- Monetization Access for Independent Creators: While top podcasters generate substantial revenue, the vast majority of creators struggle to achieve sustainable monetization. Advertising rates favor shows with large, established audiences, creating an uneven revenue distribution that may limit the overall creator ecosystem's long-term growth if not addressed through better small-show monetization models.

- Copyright and Licensing Complexity: The growing use of third-party music, clips, and content in podcast productions raises significant copyright compliance challenges. The lack of standardized licensing frameworks across jurisdictions increases legal risk and compliance costs, particularly for globally distributed shows.

Market Opportunities

- Video Podcasting Expansion: The integration of video formats into podcasting is creating a dual-medium content category that attracts both audio and video advertising budgets. Studios adopting multicamera podcast production workflows in 2024-2025 reported significant increases in episode sponsorship revenue, signaling a major incremental monetization opportunity.

- Emerging Markets Audience Growth: Asia Pacific, Latin America, and Africa collectively represent hundreds of millions of prospective podcast listeners who have yet to adopt the medium. As connectivity expands and local-language content libraries grow, these markets represent the primary volume growth driver through 2034.

- B2B and Branded Podcast Expansion: Corporations are increasingly investing in branded podcasts as a content marketing and thought leadership channel. This corporate adoption is expanding the total addressable advertising budget and creating new revenue streams for production companies and distribution platforms.

Emerging Podcasting Market Trends

1. Video Podcasting Becomes a Primary Growth Engine

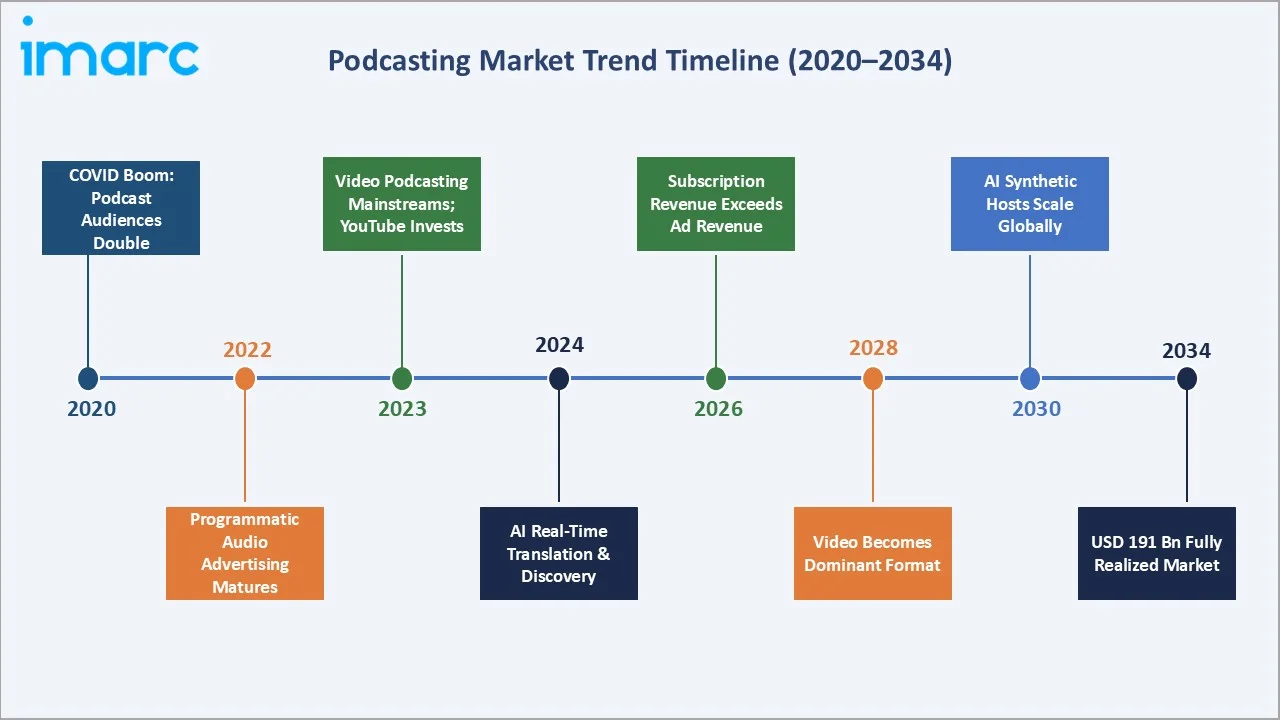

Leading platforms, including Spotify and YouTube, have rolled out dedicated video podcast features, enabling creators to publish full-length video episodes alongside traditional audio formats. In May 2025, Spotify introduced a redesigned podcast discovery feed with contextual recommendations, including video content integration, reflecting the platform's strategic commitment to dual-format content consumption.

2. AI Integration Transforms Production and Discovery

Spotify deployed real-time voice translation for podcasts, preserving the speaker's unique voice characteristics while translating content into multiple languages - a breakthrough that enables podcasters to reach global audiences without creating separate language-specific recordings. In March 2024, Apple introduced auto-generated transcripts for Apple Podcasts, enabling searchability and accessibility improvements that broaden podcast consumption among new audience segments, including hearing-impaired listeners.

3. Premium Subscriptions and Exclusive Content Monetization

In May 2025, PodX acquired Lemonada Media for USD 30 million, adding over 50 shows to expand its premium content library and subscriber base. This acquisition reflects increasing investor confidence in subscription-based podcast business models. Audiochuck secured USD 40 million from The Chernin Group in March 2025 to fund international true-crime productions - a genre that commands premium subscriber conversion rates globally.

Industry Value Chain Analysis

The global podcasting value chain spans multiple interconnected stages, from upstream content creation and audio production through platform distribution and algorithmic discovery to downstream listener engagement and advertiser monetization. Each stage involves specialized operators whose collective performance shapes content quality, audience reach, creator economics, and the ultimate commercial impact of the podcasting ecosystem.

|

Value Chain Stage |

Key Activities / Examples |

|

Content Creation |

Podcast recording, scripting, host talent, audio/video production |

|

Production & Editing |

Audio editing, sound design, transcript generation, video encoding |

|

Hosting & Distribution |

Podcast hosting platforms (Libsyn, Podbean, Buzzsprout, Megaphone) |

|

Discovery & Streaming Platforms |

Spotify, Apple Podcasts, Amazon Music, YouTube Music, TuneIn |

|

Advertising & Monetization |

Host-read ads, programmatic audio, subscriptions, listener donations |

|

Analytics & Data |

Listener analytics, download tracking, sentiment analysis (Spotify for Creators) |

|

End Listeners |

Global audience via smartphones, smart speakers, computers, connected vehicles |

Technology Landscape in the Podcasting Industry

AI-Powered Content Creation and Production

AI-powered transcription tools such as Whisper (OpenAI) and Descript’s AI editing platform have reduced post-production time by 60–70% for independent creators, enabling professional-quality audio output at minimal cost. In 2025, Spotify deployed real-time voice translation for podcasts that preserves the speaker’s unique vocal characteristics while delivering multilingual output.

Personalized Discovery and Algorithmic Recommendation

In March 2024, Apple introduced auto-generated transcripts for Apple Podcasts, making episodes fully searchable and significantly improving content discoverability for both new and established shows. These AI discovery layers are reducing the discoverability gap that has historically favored top-ranked shows, benefiting mid-tier and niche creators.

Video Podcast Production Technology

Studios adopting professional video podcast setups reported higher episode sponsorship rates even after absorbing increased production costs. YouTube’s dedicated podcast hub and Spotify’s video podcast feature set have created platform-level incentives for creators to invest in video capabilities, accelerating hardware and software adoption across the production ecosystem through 2034.

Programmatic Audio Advertising Technology

Programmatic advertising platforms specifically engineered for podcasting, including Spotify’s Streaming Ad Insertion (SAI), iHeartMedia’s SmartAudio, and independent platforms such as AdsWizz and Triton Digital, are enabling real-time audience targeting comparable to digital display and video advertising. IAB’s Podcast Measurement 2.1 standards, adopted by major platforms in 2024, provide unified attribution metrics that are attracting larger brand advertising budgets previously reluctant to invest without standardized measurement frameworks.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Genre |

News and Politics |

28.6% |

2025 |

|

Format |

Interviews |

34.8% |

2025 |

|

Region |

North America |

38.5% |

2025 |

By Genre

News and Politics is the dominant genre in the global podcasting market with a 28.6% share in 2025. This leadership position reflects the increasing demand for timely, accessible, and independent information in an era of fragmented traditional media trust.

To access detailed market analysis, Request Sample

Society and Culture holds 21.4%, encompassing true crime, storytelling, personal development, relationships, and lifestyle content - genres with high audience engagement and premium advertising appeal. Comedy accounts for 18.9%, attracting younger demographics and generating strong social media cross-promotion virality that drives organic audience growth. Sports holds 14.7%, buoyed by exclusive deals, live-event tie-ins, and celebrity athlete hosts.

By Format

Interview-format podcasts lead the global podcasting market by format with a commanding 34.8% share in 2025. The interview format's dominance stems from audience preference for authentic, guest-driven conversations that deliver unique insights from subject-matter experts, celebrities, executives, and public figures.

Conversational podcasts hold 22.6% of format share, reflecting sustained audience appetite for informal, multi-host discussions that simulate authentic dialogue. Solo formats at 16.3% are particularly prevalent in business, self-development, and educational niches where single expert voices deliver structured knowledge to dedicated listener communities.

Regional Market Insights

North America commands a 38.5% share of the global podcasting market in 2025, underpinned by the world's most mature podcast advertising infrastructure, the highest per-capita listening rates globally, and an unparalleled creator community. Over 55% of the U.S. population, approximately 158 million people, listen to podcasts monthly as of 2025. Canada contributes incrementally, particularly in technology, business, and lifestyle genres.

|

Region |

Share (2025) |

Key Growth Drivers |

Key Companies |

|

North America |

38.5% |

High listening rates, mature ad ecosystem, celebrity hosts |

Spotify, Apple, Amazon, iHeartMedia |

|

Europe |

26.2% |

Multilingual content, public broadcaster adoption, BBC/ARD |

Spotify, Apple, Acast, SoundCloud |

|

Asia Pacific |

21.8% |

Smartphone boom, regional language content, rising middle class |

Spotify, JioSaavn, Himalaya, Apple |

|

Latin America |

7.6% |

Portuguese/Spanish content growth, mobile-first audiences |

Spotify, Amazon |

|

Middle East & Africa |

5.9% |

Young demographics, rapid digitalization, Arabic content growth |

Spotify, Anghami |

Europe holds a 26.2% share of the global podcasting market in 2025. Sweden-based Acast reported a 30% increase in net sales in Q1 2025, driven by geographic diversification across European markets. EU digital media regulations and data privacy frameworks (GDPR) are shaping advertising targeting capabilities, creating a distinctly different advertising ecosystem from North America.

Competitive Landscape

The global podcasting market features a moderately concentrated competitive landscape at the platform level, with Spotify, Apple, and Amazon collectively commanding the majority of global podcast listening hours. Strategic acquisitions are a defining competitive tactic - Spotify's acquisition of Gimlet and Anchor (2019) established its end-to-end podcasting ecosystem leadership, while PodX's acquisition of Lemonada Media for USD 30 million in May 2025 reflects ongoing consolidation in premium content networks.

|

Company Name |

Brand / Platform |

Market Position |

Core Strength |

|

Spotify Technology S.A. |

Spotify Podcasts |

Market Leader |

AI recommendations, exclusive content, global scale |

|

Apple Inc. |

Apple Podcasts |

Market Leader |

Largest podcast directory, ecosystem integration |

|

Amazon.com Inc. |

Amazon Music |

Strong Challenger |

Voice-activated access via Alexa, Prime ecosystem |

|

iHeartMedia Inc. |

iHeartPodcasts |

Strong Challenger |

Broadcast-digital hybrid, largest ad sales network |

|

Pandora Media LLC (SiriusXM Holdings Inc.) |

Pandora |

Challenger |

Music-podcast hybrid, personalization algorithms |

|

TuneIn Inc. (a Stingray company) |

TuneIn |

Challenger |

Live radio + podcast integration, automotive |

|

SoundCloud |

SoundCloud |

Challenger |

Independent creator platform, audio community |

|

Podbean Tech LLC |

Podbean |

Specialist |

Creator hosting, monetization tools, community features |

|

Liberated Syndication Inc. |

Libsyn |

Specialist |

Podcast hosting infrastructure, distribution tech |

Key Company Profiles

Spotify Technology S.A.

Spotify Technology S.A., headquartered in Stockholm, Sweden, is the world’s largest music and podcast streaming platform with over 700 million monthly active users in 2025. Spotify dominates the podcast market with the largest global share of listening hours, driven by a combination of exclusive content deals,

- Product Portfolio: Spotify Podcasts; Spotify Open Access; Megaphone hosting and advertising platform; Spotify Audience Network.

- Recent Developments: In 2023, Spotify launched real-time podcast voice translation preserving speaker vocal characteristics, enabling multilingual audience reach. Redesigned podcast discovery feed introduced contextual recommendation notes.

- Strategic Focus: AI-driven personalization, video podcast expansion, premium subscriber growth, and creator monetization platform development to reduce creator dependency on third-party advertising networks.

Apple Inc.

Apple Inc., headquartered in Cupertino, California, operates the world’s largest podcast directory through Apple Podcasts, with over 2.9 million active shows available as of 2025. Apple Podcasts is the default podcast application across iPhone, iPad, Mac, Apple Watch, and Apple TV, providing unrivaled ecosystem reach across approximately 2.5 billion active devices globally.

- Product Portfolio: Apple Podcasts; Apple Podcasts Subscriptions; Apple Podcasts Connect for creators; Apple Podcasts Chapters; auto-generated transcripts (launched March 2024).

- Recent Developments: In March 2024, Apple introduced auto-generated transcripts for all Apple Podcasts episodes, enabling full-text searchability and improving accessibility for hearing-impaired audiences globally.

- Strategic Focus: Ecosystem lock-in through native device integration, creator tools expansion, subscription revenue development via Apple Podcasts Subscriptions, and accessibility improvements to expand total addressable listener demographics.

Amazon.com Inc.

Amazon.com Inc., headquartered in Seattle, Washington, participates in the podcasting market through Amazon Music, Audible, and Alexa-integrated voice-activated podcast access. Amazon’s acquisition of Wondery in 2020 for reportedly approximately USD 300 million established a premium podcast content library spanning business, true crime, science, and entertainment genres with strong listener engagement metrics.

- Product Portfolio: Amazon Music Podcasts; Audible Original Podcasts; Wondery premium podcast network; Alexa voice-activated podcast access across Echo device ecosystem.

- Recent Developments: Continued expansion of Wondery’s premium content library with original productions across multiple genres; integration of podcast listening into Amazon Prime ecosystem benefits.

- Strategic Focus: Leveraging Alexa’s smart speaker installed base for podcast discovery, deepening Prime ecosystem integration to drive podcast engagement among existing Amazon subscribers, and expanding Wondery’s original content pipeline.

iHeartMedia Inc.

iHeartMedia Inc., headquartered in San Antonio, Texas, is the largest podcast publisher in the United States by download volume, operating over 750 owned-and-operated podcasts across its iHeartPodcast Network. With direct access to over 250 million monthly listeners through its broadcast radio, digital, and podcasting platforms, iHeartMedia commands the largest podcast advertising sales network in North America.

- Product Portfolio: iHeartRadio (streaming + podcast); iHeartPodcast Network (750+ shows); SmartAudio programmatic advertising platform; live events and broadcast radio integration.

- Recent Developments: iHeartMedia disclosed USD 140 million in Q4 2024 podcast revenue, underscoring the scale of its advertising monetization. Continued expansion of the iHeartPodcast Network with new creator partnerships.

- Strategic Focus: Broadcast-to-digital audience migration, programmatic podcast advertising leadership through SmartAudio, and leveraging its unmatched advertiser relationships to drive podcast CPM premiums.

Market Concentration Analysis

The global podcasting market exhibits moderate concentration at the platform level, with Spotify, Apple, and Amazon collectively accounting for an estimated 65–70% of global podcast listening hours in 2025. Spotify alone commands approximately 30% of global listening share, having invested over USD 1 billion in podcast content acquisitions and technology development since 2019.

The hosting and distribution infrastructure segment exhibits higher fragmentation, with Libsyn, Podbean, Buzzsprout, and Megaphone (acquired by Spotify in 2020) competing for independent creator hosting revenue. Megaphone’s integration into Spotify’s Audience Network has created a vertically integrated competitive advantage, enabling Spotify to offer both hosting and programmatic advertising monetization within a single ecosystem.

The premium content network segment is consolidating around a small number of well-funded operators who can fund high-production-value original series, a dynamic comparable to the consolidation phase experienced in streaming video between 2018 and 2022. Entry barriers for new platform competitors remain high, given the capital intensity of content acquisition, technology development, and creator ecosystem building required to challenge established market leaders.

Investment & Growth Opportunities

Fastest Growing Segments

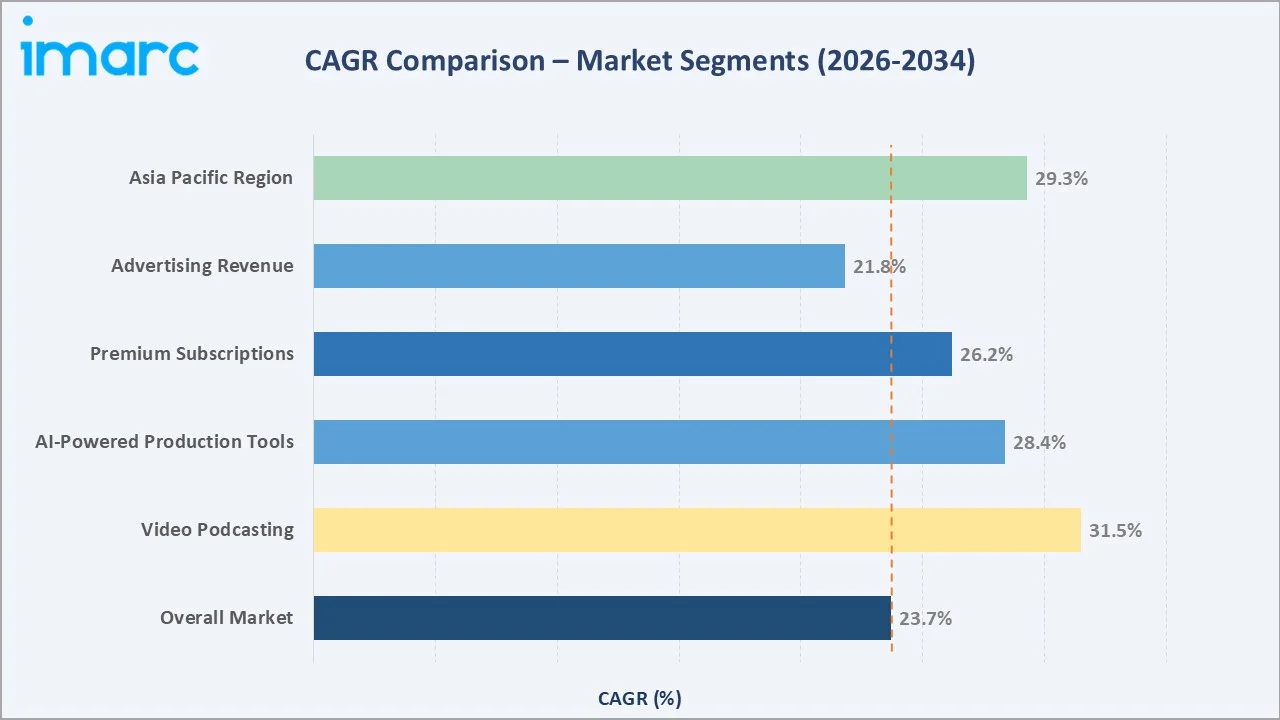

Video podcasting, premium subscription content, and AI-powered production tools represent the three highest-growth investment vectors in the global podcasting market through 2034. Video podcast advertising is attracting video-level CPMs while retaining the intimacy of host-read audio formats, creating premium monetization opportunities. Niche content verticals, including business, finance, health, and education, are attracting corporate advertising budgets that have traditionally been allocated to LinkedIn and industry media rather than podcasting.

Emerging Market Expansion

India, Southeast Asia, Brazil, and the MENA region collectively represent the largest untapped podcast audience potential globally. India's podcast market alone was valued at over USD 840 million in 2024, growing at a CAGR exceeding 28% through 2033.

Strategic Investment Trends

Venture and strategic capital continues flowing into the podcasting ecosystem. Audiochuck's USD 40 million funding round and PodX's USD 30 million Lemonada acquisition exemplify the M&A consolidation trend among premium content networks. Podcast advertising technology companies are attracting strategic interest from major digital advertising groups seeking to capture the growing shift of brand budgets toward audio.

Future Podcasting Market Outlook (2026-2034)

The global podcasting market is positioned for one of the most dramatic growth trajectories in the digital media landscape, rising from USD 28.2 Billion in 2025 to USD 191.3 Billion by 2034. This near seven-fold expansion over nine years reflects the fundamental reshaping of audio media consumption - from scheduled broadcast toward fully on-demand, personalized, multi-format experiences.

AI will be the most transformative technology force in this period, enabling real-time translation, synthetic content creation, and hyper-personalized discovery that will dramatically expand both the creator base and the global listener population beyond 2034 projections.

Video will emerge as the dominant podcast consumption format for younger demographics by the end of the forecast period, with platforms competing aggressively for creator exclusivity and viewer hours across both audio and visual interfaces. Subscription revenues will grow from a supplementary to a primary monetization channel for leading content creators and networks.

Research Methodology

Primary Research

Primary research included structured interviews with podcast platform executives, content creators, advertising agencies, and distribution technology providers across North America, Europe, and Asia Pacific. Voice of customer surveys and listener behavior studies supplemented industry expert consultations to validate market sizing and segment assumptions.

Secondary Research

Secondary research encompassed a comprehensive review of company annual reports, platform disclosures, industry associations (IAB Podcast Measurement Guidelines, Edison Research Infinite Dial reports), trade publications (Podnews, Hot Pod, Sounds Profitable), and verified listener statistics from major streaming platforms. Over 250 authoritative secondary sources were reviewed and triangulated to ensure data integrity.

Forecasting Models

Market size estimations utilized a combination of top-down approaches (total digital advertising market share allocation) and bottom-up models (per-listener monetization rates multiplied by projected audience sizes). Subscription revenue streams, live event income, and merchandise monetization were modeled separately and added to the advertising base projections.

Podcasting Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Genres Covered | News and Politics, Society and Culture, Comedy, Sports, Others |

| Formats Covered | Interviews, Panels, Solo, Repurposed Content, Conversational, Others |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | Spotify Technology S.A., Apple Inc., Amazon.com Inc., iHeartMedia Inc., Pandora Media LLC (SiriusXM Holdings Inc.), TuneIn Inc. (a Stingray company), SoundCloud, Podbean Tech LLC, Liberated Syndication Inc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the podcasting market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the global podcasting market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's five forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the podcasting industry and its attractiveness.

- The competitive landscape allows stakeholders to understand their competitive environment and provides insight into the current positions of key players in the market.

Frequently Asked Questions About the Podcasting Market Report

The global podcasting market was valued at USD 28.2 Billion in 2025.

The podcasting market is projected to reach USD 191.3 Billion by 2034, exhibiting a CAGR of 23.71% during 2026-2034.

Key drivers include smartphone proliferation, rising podcast advertising investment, AI-powered content tools, and growing demand for on-demand audio content globally.

North America dominates with a 38.5% share in 2025, driven by high listening rates, a mature advertising ecosystem, and major platform headquarters in the U.S.

News and Politics leads with a 28.6% market share in 2025, fueled by global political engagement and the rise of independent journalism in audio formats.

Interview-format podcasts dominate with a 34.8% share in 2025, reflecting audience preference for authentic, guest-driven long-form conversations.

Leading companies include Spotify Technology S.A., Apple Inc., Amazon.com Inc., iHeartMedia Inc., Pandora Media LLC (SiriusXM Holdings Inc.), TuneIn Inc (a Stingray company), SoundCloud, Podbean Tech LLC, Liberated Syndication Inc., etc.

Video podcasting adoption, AI content tools, and real-time translation, premium subscription expansion, and emerging market audience growth are the defining trends through 2034.

AI enables real-time voice translation, automated transcription, personalized content recommendations, and synthetic content creation, dramatically expanding creator reach and listener discovery.

Asia Pacific is the fastest-growing region, driven by smartphone penetration, rising disposable incomes, regional language content growth, and expanding digital infrastructure.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)