Potassium Permanganate Market Size, Share, Trends and Forecast by Application, Grade, and Region, 2026-2034

Potassium Permanganate Market Size, Share, Trends & Forecast (2026-2034)

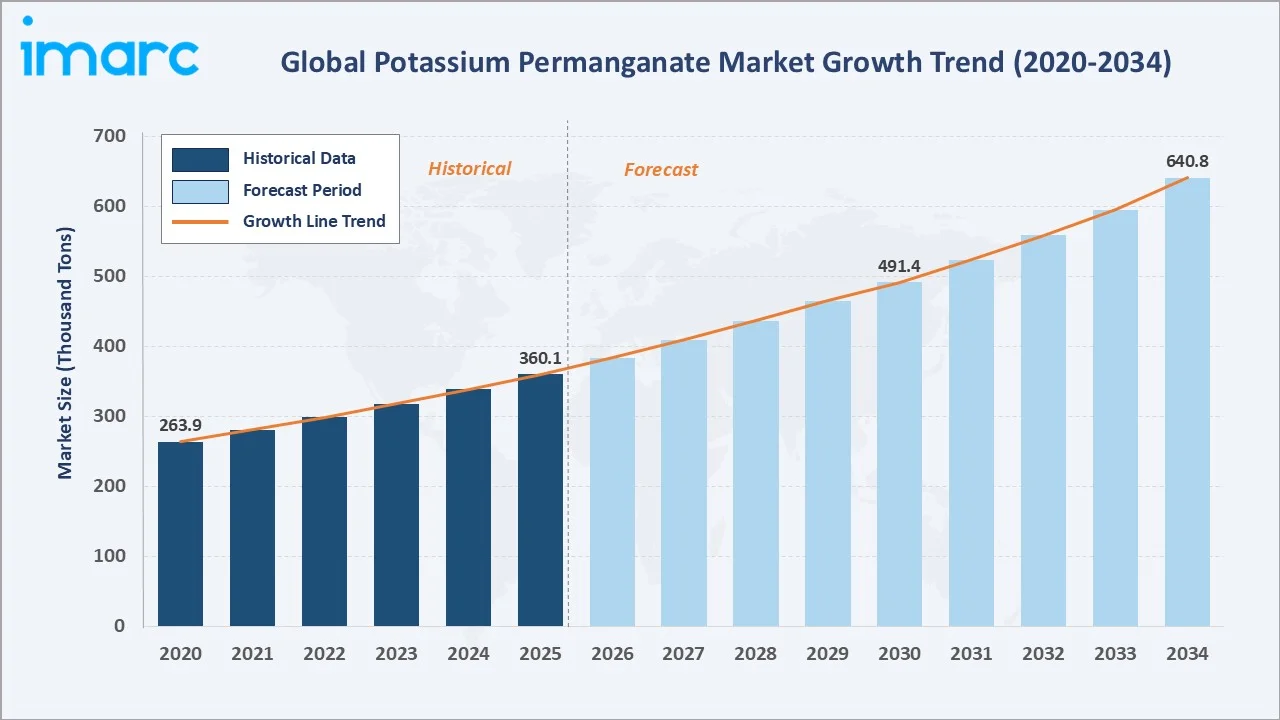

The global potassium permanganate market reached 360.1 Thousand Tons in 2025 and is projected to reach 640.8 Thousand Tons by 2034, growing at a CAGR of 6.42% during 2026-2034. The market is driven by rising water treatment demand, expanding chemical manufacturing, increasing agricultural applications, and growing focus on wastewater management globally.

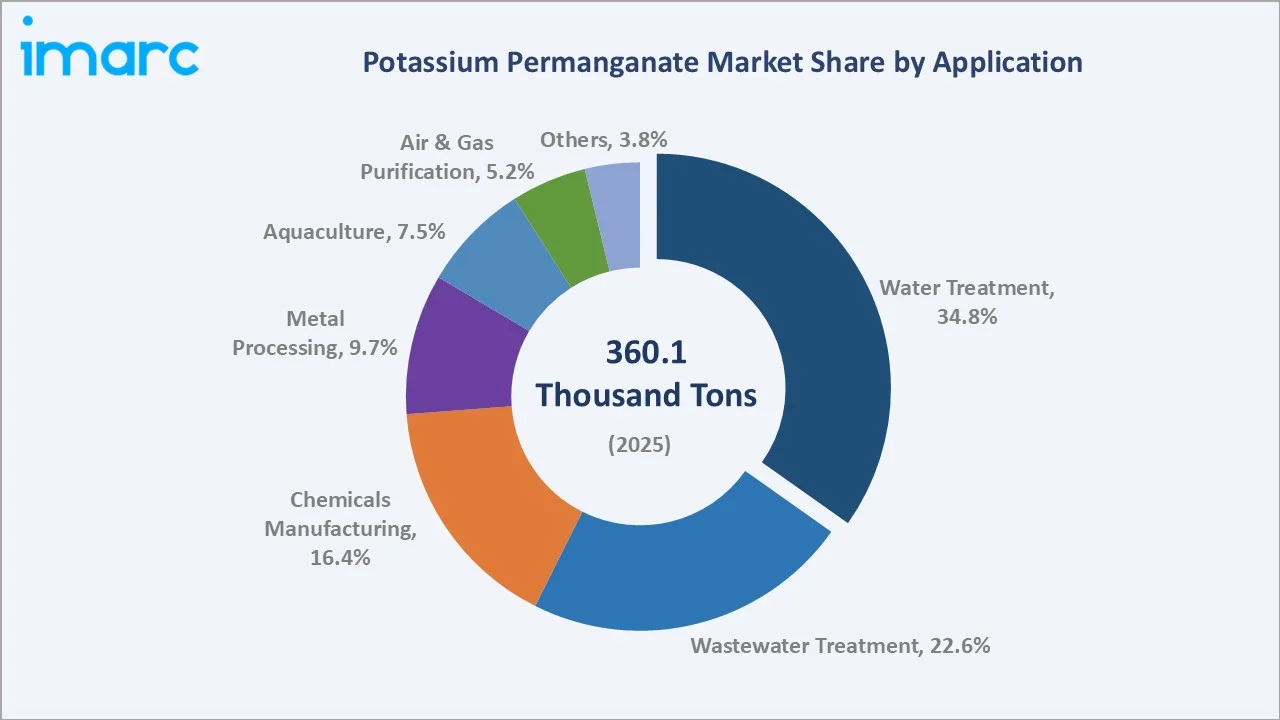

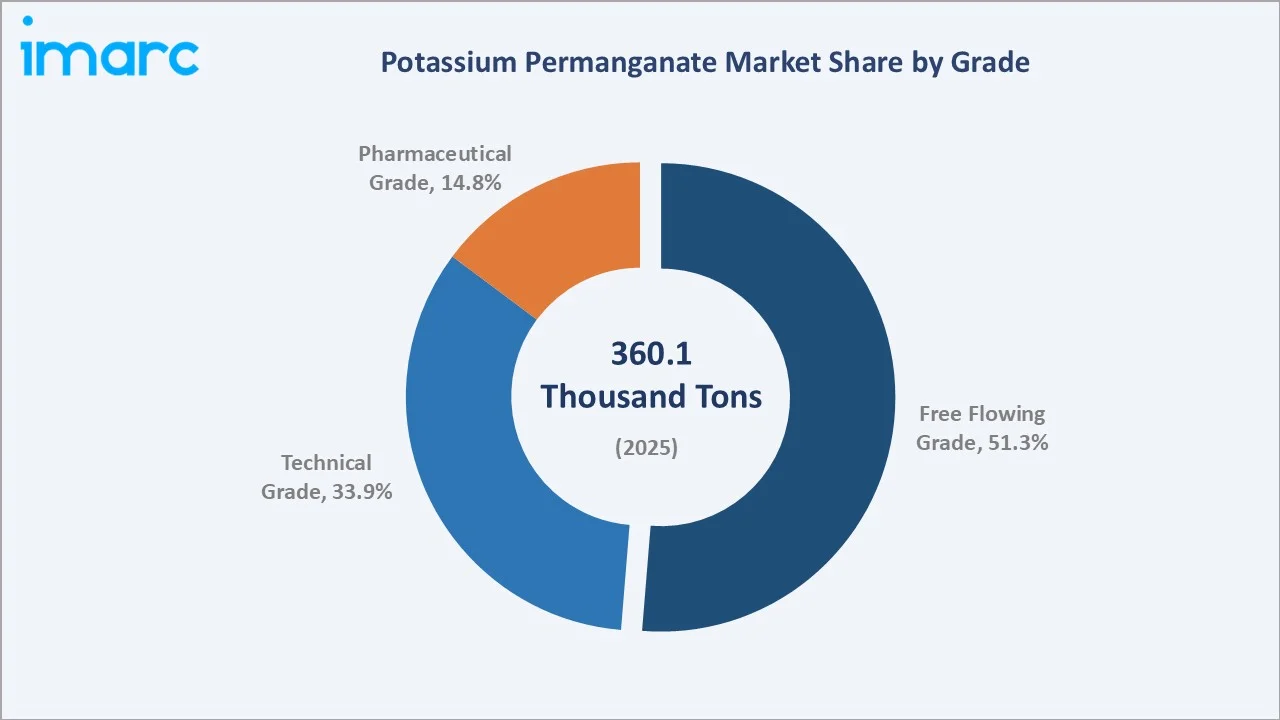

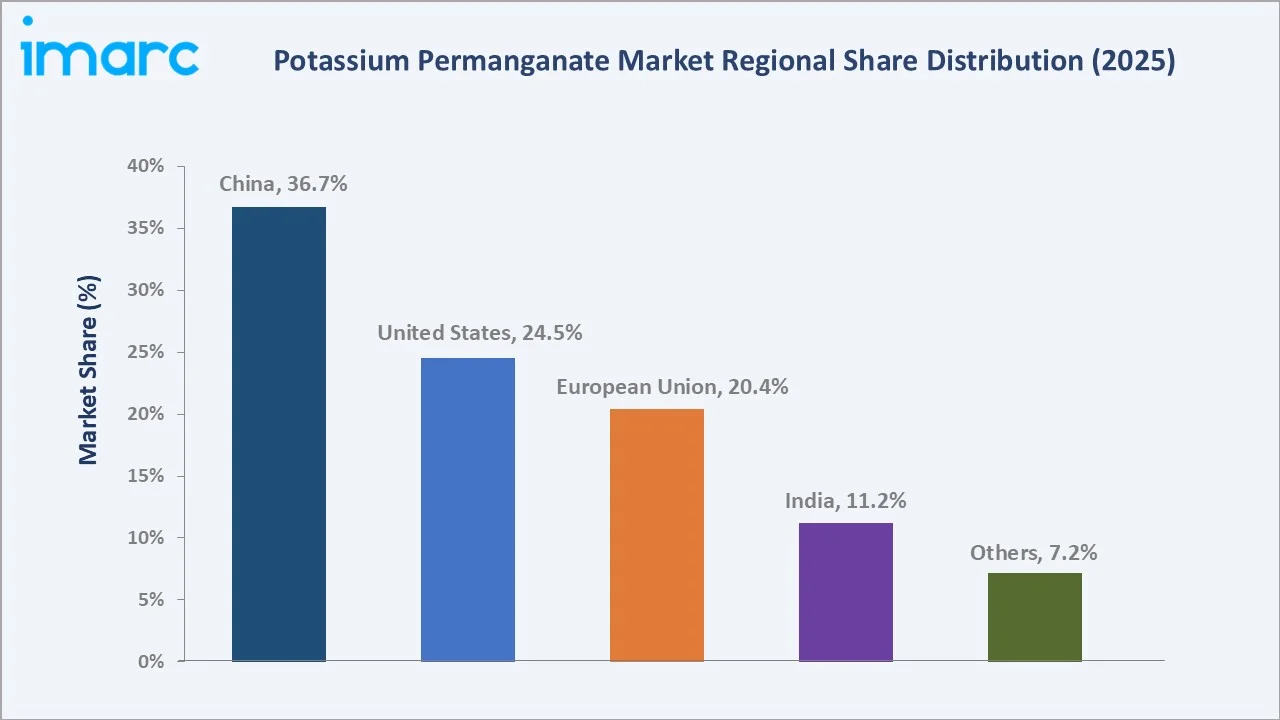

Water Treatment leads applications at 34.8%. Free Flowing Grade dominates at 51.3%. China commands 36.7% of the global market share.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

360.1 Thousand Tons |

|

Forecast Market Size (2034) |

640.8 Thousand Tons |

|

CAGR (2026-2034) |

6.42% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Dominant Application |

Water Treatment (34.8%, 2025) |

|

Dominant Grade |

Free Flowing Grade (51.3%, 2025) |

|

Leading Region |

China (36.7%, 2025) |

The market expanded from 263.9 Thousand Tons in 2020 to 360.1 Thousand Tons in 2025, anchored at 491.4 Thousand Tons in 2030 and forecast to reach 640.8 Thousand Tons by 2034. Rising urbanization and tightening water quality regulations across key economies are sustaining stable structural demand growth throughout the historical and forecast periods.

To get more information on this market, Request Sample

Water Treatment application grows consistently as global regulatory frameworks tighten around drinking water quality and municipal infrastructure investment accelerates. Free Flowing Grade leads through superior handling convenience and broad industrial compatibility across manufacturing and treatment segments.

Executive Summary

The global potassium permanganate market reached 360.1 Thousand Tons in 2025, representing a stable, essential-chemicals market underpinned by water treatment, chemical synthesis, and agricultural demand. The market is projected to reach 640.8 Thousand Tons by 2034, growing at a CAGR of 6.42%.

Water Treatment at 34.8% dominates by addressing the most widespread global requirement: safe, oxidant-treated drinking water. Free Flowing Grade at 51.3% leads across industrial procurement categories. China, at 36.7%, commands regional leadership through its large-scale chemical production base and expansive water infrastructure programmes.

Key Market Insights

|

Insight |

Data |

|

Dominant Application |

Water Treatment – 34.8% market share (2025) |

|

Dominant Grade |

Free Flowing Grade – 51.3% market share (2025) |

|

Leading Region |

China – 36.7% market share (2025) |

|

Market Opportunity |

Pharma-grade growth; sustainable oxidant R&D; aquaculture expansion |

Key Analytical Observations Supporting the Above Data:

- Water Treatment at 34.8%: The largest segment, driven by global regulatory focus on safe drinking water and effective removal of iron, manganese, and hydrogen sulfide from municipal water supplies using KMnO4 as a primary pre-oxidant.

- Free Flowing Grade at 51.3%: Dominates due to superior dosing precision, ease of handling, reduced caking, and broad industrial compatibility across water treatment and chemical manufacturing procurement.

- China at 36.7%: Leads by virtue of its large-scale domestic chemical manufacturing base, extensive urban water infrastructure networks, and significant KMnO4 export capacity to global markets.

Potassium Permanganate Market Overview

The global potassium permanganate (KMnO4) market encompasses the synthesis, formulation, and distribution of potassium permanganate across industrial, municipal, agricultural, and pharmaceutical end-uses. It appears as dark purple crystalline substance and serves as a potent oxidizing agent across multiple application domains.

The ecosystem integrates manganese ore miners, chemical manufacturers, industrial distributors, regulatory bodies, water utilities, and end-use industries. Macroeconomic factors include rising urbanization, water scarcity concerns, industrial expansion in emerging economies, and strengthening environmental regulations across key markets globally.

Market Dynamics

To evaluate market opportunities, Request Sample

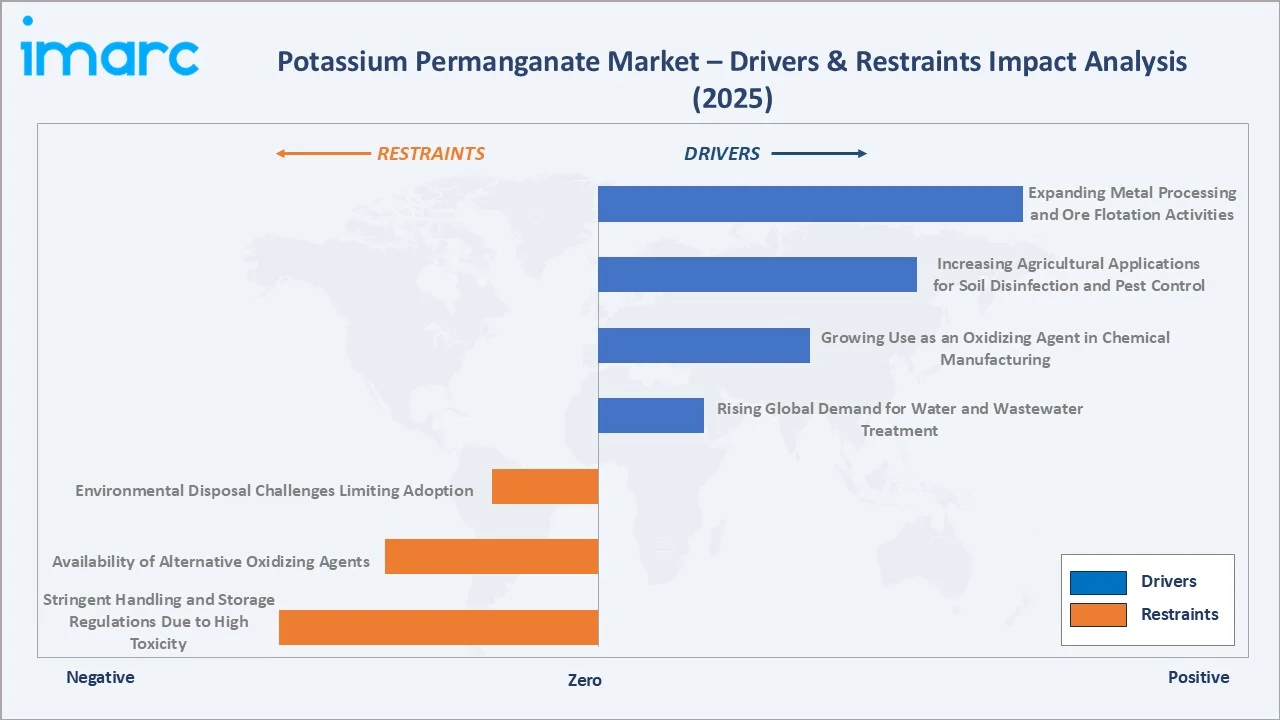

Market Drivers

- Rising Global Demand for Water and Wastewater Treatment: Increasing regulatory focus on potable water safety and municipal wastewater management drives KMnO4 adoption globally. Potassium permanganate effectively removes iron, manganese, and hydrogen sulfide from water. Stringent WHO and EPA guidelines support the use of effective oxidation and treatment technologies, sustaining consistent demand across developed and emerging economies.

- Growing Use as an Oxidizing Agent in Chemical Manufacturing: Potassium permanganate is a critical oxidant in pharmaceutical synthesis, fine chemicals, and specialty chemicals production, facilitating controlled oxidation reactions and enabling manufacturers to produce high-purity intermediates. Rising chemical output across Asia-Pacific and Europe translates into sustained procurement of industrial-grade KMnO4.

- Increasing Agricultural Applications for Soil Disinfection and Pest Control: Farmers globally deploy potassium permanganate as a fungicide, bactericide, and soil sterilant to protect crops from soil-borne diseases and pests. The shift toward chemical-assisted precision agriculture, especially in Asia-Pacific and Latin America, is broadening KMnO4 adoption across agri-input supply chains worldwide.

- Expanding Metal Processing and Ore Flotation Activities: Metal processing industries use potassium permanganate in ore flotation and surface treatment processes to improve metal recovery rates and product purity. Growing mining activity across China, India, and Africa, combined with rising demand for refined metals, generates incremental demand for industrial-grade KMnO4.

Market Restraints

- Stringent Handling and Storage Regulations Due to High Toxicity: Potassium permanganate is classified as a hazardous oxidizer, subject to strict transport, storage, and workplace safety regulations under OSHA, REACH, and national chemical safety frameworks. Compliance costs and handling complexities restrict adoption among small-scale users and emerging-market buyers.

- Availability of Alternative Oxidizing Agents: Hydrogen peroxide, chlorine dioxide, and ozone represent cost-competitive oxidizing alternatives in water treatment and chemical synthesis. Their growing availability and improving price parity pose substitution risk, particularly in applications where KMnO4's specific oxidation properties are not uniquely required.

- Environmental Disposal Challenges Limiting Adoption: Discharge of manganese-containing effluent from KMnO4 use is subject to increasingly restrictive wastewater standards globally. Managing manganese residues post-treatment requires additional infrastructure investment, raising total cost of ownership for end-users across water and chemical sectors.

Market Opportunities

- Pharmaceutical-Grade Potassium Permanganate Adoption: The pharmaceutical and dermatology sectors present an emerging high-value opportunity, using pharmaceutical-grade KMnO4 in antiseptic preparations, wound care, and skin condition treatment. Growth in global healthcare spending and rising dermatological awareness support incremental pharma-grade demand through 2034.

- Sustainable and Green Oxidant Development: R&D into greener synthesis routes for potassium permanganate and its integration with sustainable water treatment systems can unlock new regulatory-compliant market opportunities, aligning with ESG-driven procurement policies by industrial buyers across developed markets.

Market Challenges

- Manganese Supply Chain Volatility: Potassium permanganate production is directly linked to manganese ore availability. Concentrated supply from South Africa, China, and Australia introduces geopolitical and logistical risks that can lead to raw material cost volatility and production disruptions for manufacturers worldwide.

- Price Competition from Low-Cost Chinese Producers: Chinese KMnO4 manufacturers, operating at large scale with lower input costs, exert sustained downward price pressure on global markets. International producers face margin compression in commodity-grade segments, challenging investment in product quality and compliance upgrades.

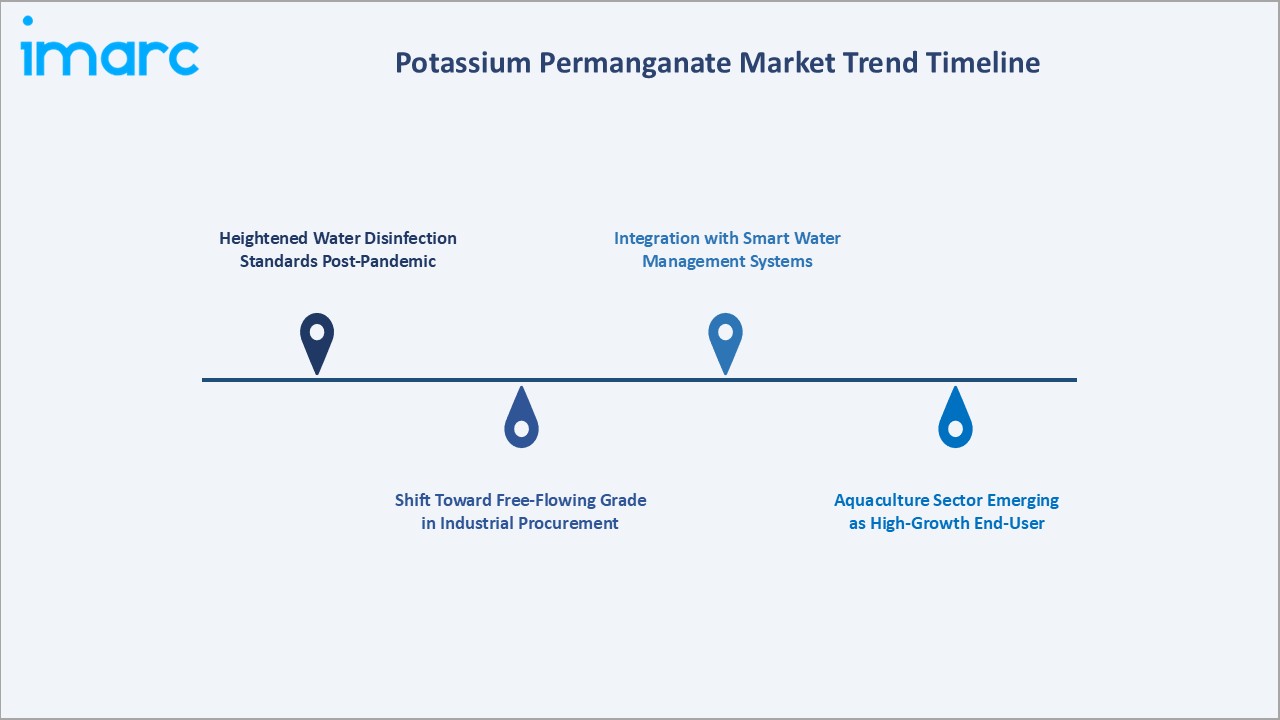

Emerging Market Trends

1. Heightened Water Disinfection Standards Post-Pandemic

COVID-19 elevated global awareness of water-borne infection risks, accelerating regulatory tightening around drinking water disinfection. Municipalities upgraded treatment protocols, increasing KMnO4 procurement as a primary pre-oxidant. This post-pandemic regulatory momentum continues into the forecast period across key developing and developed markets.

2. Shift Toward Free-Flowing Grade in Industrial Procurement

Industrial buyers are transitioning toward free-flowing grade KMnO4 for superior dosing precision, reduced caking risk, and improved operational efficiency. This grade shift is structurally increasing the commercial share of free-flowing grade versus traditional technical crystal formats across water treatment and chemical manufacturing.

3. Aquaculture Sector Emerging as High-Growth End-User

Aquaculture producers across Asia-Pacific are adopting potassium permanganate as a water quality management tool, treating fishponds for parasitic infections and improving dissolved oxygen levels. Rapid expansion of aquaculture output, particularly in China and Southeast Asia, is creating incremental demand through 2034.

4. Integration with Smart Water Management Systems

Advanced water treatment facilities are integrating KMnO4 dosing into automated, sensor-driven water management platforms. This digital integration improves treatment precision, reduces chemical waste, and positions potassium permanganate within broader smart infrastructure investment frameworks globally.

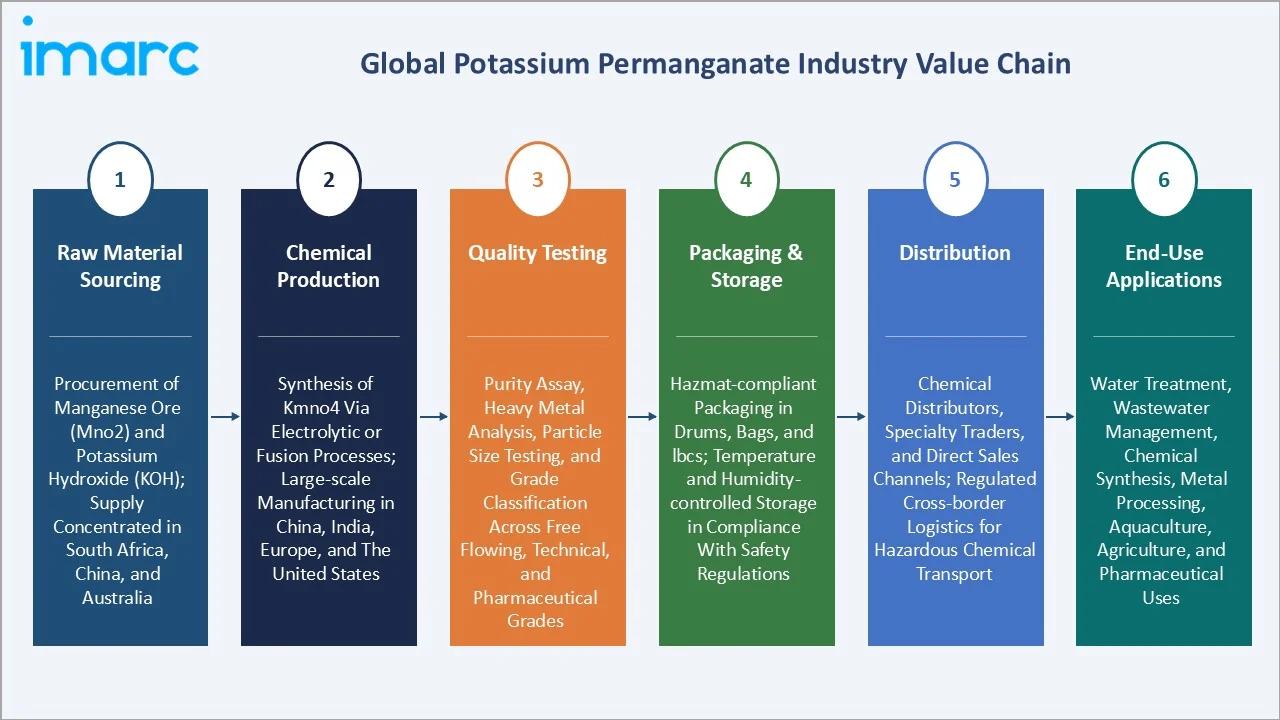

Industry Value Chain Analysis

The potassium permanganate value chain integrates raw material sourcing, chemical production, quality testing, packaging and storage, distribution, and end-use applications. The chain is vertically concentrated among a small number of large chemical producers, particularly in China, with distribution channels spanning industrial distributors and specialty chemical traders.

|

Stage |

Key Activities |

|

Raw Material Sourcing |

Procurement of manganese ore (MnO2) and potassium hydroxide (KOH); supply concentrated in South Africa, China, and Australia |

|

Chemical Production |

Synthesis of KMnO4 via electrolytic or fusion processes; large-scale manufacturing in China, India, Europe, and the United States |

|

Quality Testing |

Purity assay, heavy metal analysis, particle size testing, and grade classification across free flowing, technical, and pharmaceutical grades |

|

Packaging & Storage |

Hazmat-compliant packaging in drums, bags, and IBCs; temperature and humidity-controlled storage in compliance with safety regulations |

|

Distribution |

Chemical distributors, specialty traders, and direct sales channels; regulated cross-border logistics for hazardous chemical transport |

|

End-Use Applications |

Water treatment, wastewater management, chemical synthesis, metal processing, aquaculture, agriculture, and pharmaceutical uses |

The raw material sourcing stage is the most geopolitically sensitive, with manganese supply concentrated in a small number of countries. The chemical production stage is increasingly consolidating around large-scale Chinese manufacturers, creating competitive pricing dynamics and supply concentration risks across global markets.

Technology Landscape in Potassium Permanganate Industry

Manganese Ore Beneficiation and Electrolytic Oxidation Technology

Electrolytic oxidation remains the dominant production pathway for potassium permanganate, enabling precise control over oxidation states, purity levels, and crystal morphology. Modern electrolytic cells equipped with computerized process monitoring are improving current efficiency, reducing energy consumption per unit output, and enabling production of high-purity KMnO₄ grades demanded by pharmaceutical, semiconductor wafer cleaning, and water treatment applications.

Green Chemistry and Catalytic Synthesis Advances

Emerging catalytic and electrochemical synthesis routes are reducing reliance on energy-intensive traditional fusion processes. Innovations in continuous-flow reactor design and closed-loop manganese recovery systems are minimizing waste generation and raw material losses, aligning production with tightening environmental regulations while improving cost competitiveness for specialty chemical manufacturers.

Functional Formulation and Application-Specific Grade Technology

Advanced granulation, encapsulation, and controlled-release formulation technologies are enabling potassium permanganate suppliers to deliver higher-value, application-tailored products for municipal water treatment, industrial effluent management, odor control, and pharmaceutical synthesis — creating premiumization opportunities within the KMnO₄ value chain and supporting compliance with increasingly stringent water quality and API purity standards globally.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Application |

Water Treatment |

34.8% |

2025 |

|

Grade |

Free Flowing Grade |

51.3% |

2025 |

|

Region |

China |

36.7% |

2025 |

By Application

Water Treatment leads at 34.8% in 2025, representing the largest and most structurally stable demand segment driven by municipal water quality standards globally. Wastewater Treatment at 22.6% follows, driven by regulatory compliance requirements for industrial effluent management across major economies.

To access detailed market analysis, Request Sample

Chemicals Manufacturing at 16.4% reflects KMnO4's role as a key oxidant in pharmaceutical and specialty chemical synthesis. Metal Processing at 9.7%, Aquaculture at 7.5%, Air and Gas Purification at 5.2%, and Others at 3.8% complete the application landscape.

By Grade

Free Flowing Grade leads at 51.3% in 2025, preferred across industrial and municipal applications for superior flowability, consistent dosing, and reduced handling hazards. Technical Grade at 33.9% serves chemical manufacturing and general industrial end-uses requiring standard purity levels.

Pharmaceutical Grade at 14.8% represents the fastest-growing grade segment, driven by expanding dermatological and antiseptic applications in healthcare. Its premium pricing and stringent quality requirements support higher per-unit revenue contribution relative to its volume share through 2034.

Regional Market Insights

|

Region |

Share (2025) |

Key Drivers & Characteristics |

|

China |

36.7% |

Largest global KMnO4 producer and consumer; dominant chemical manufacturing sector; extensive water infrastructure investment programs |

|

United States |

24.5% |

Stringent EPA drinking water standards; large industrial chemical sector; mature water treatment infrastructure with stable procurement |

|

European Union |

20.4% |

REACH-driven compliance demand; focus on wastewater treatment and circular water economy initiatives across member states |

|

India |

11.2% |

Fast-growing water treatment market; rising chemical production; Jal Jeevan Mission driving rural water supply infrastructure investment |

|

Others |

7.2% |

Emerging adoption in Southeast Asia, Latin America, and Africa through water infrastructure development and agricultural chemical expansion |

China at 36.7% dominates as both the largest producer and consumer of potassium permanganate globally, with its chemical manufacturing scale and large urban water treatment networks generating consistent domestic demand alongside substantial export volumes. The United States at 24.5% reflects mature, regulation-driven demand from municipal water utilities and chemical manufacturers.

The European Union at 20.4% is characterized by REACH-driven compliance procurement and growing focus on water reuse mandates. India at 11.2% represents the most dynamic growth market, driven by the Jal Jeevan Mission and expanding chemical manufacturing output. Others at 7.2% represent nascent but growing adoption across Southeast Asia, Africa, and Latin America.

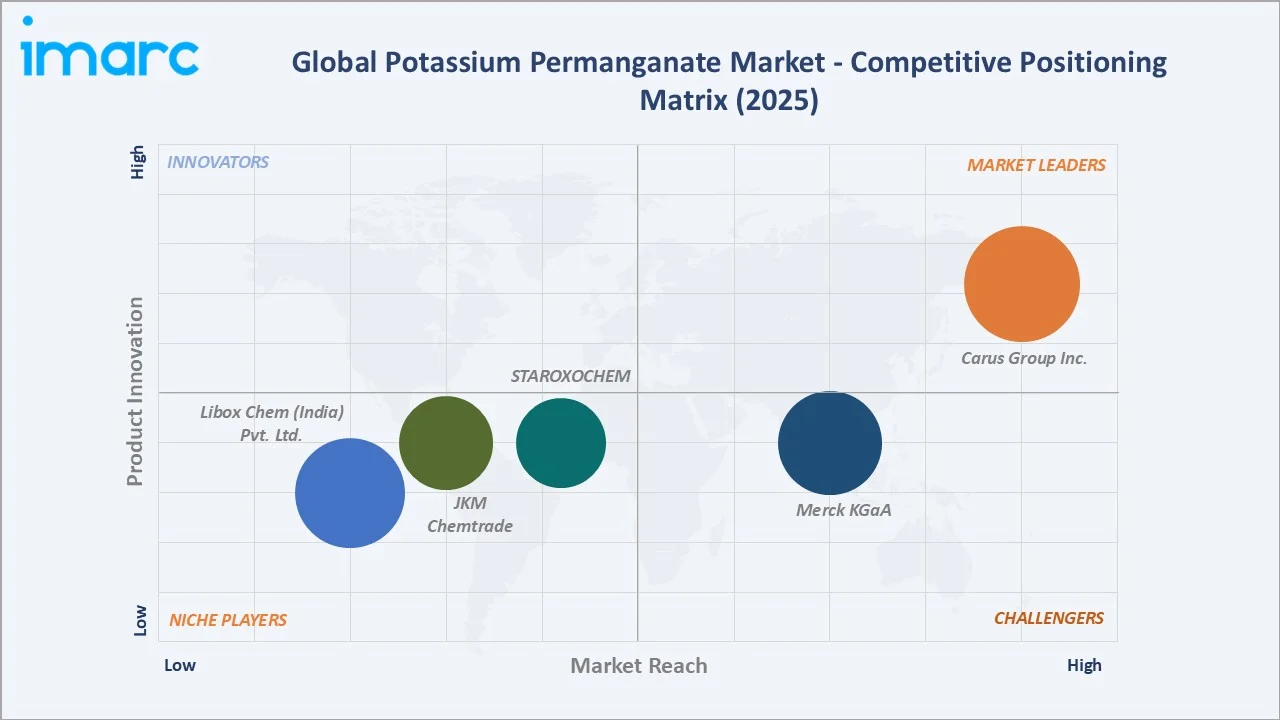

Competitive Landscape

The global potassium permanganate market is moderately consolidated, with production concentrated among a small number of large chemical manufacturers in China, the United States, India, and Europe. Chinese producers dominate volume share, while Western and Indian players compete on quality, regulatory compliance, and specialty grade differentiation.

|

Company Name |

Key Products |

Market Position |

Core Strength |

|

Carus Group Inc. |

CAIROX Potassium Permanganate, AQUOX Potassium Permanganate, RemOx S ISCO Reagent |

Market Leader |

Leading US producer; water treatment specialty; strong EPA-compliance track record |

|

Merck KGaA |

Potassium permanganate |

Strong Challenger |

Global life science and specialty chemicals leader; high-purity reagent and pharma-grade KMnO4 for laboratory, quality control, and biopharma applications |

|

Libox Chem (India) Pvt. Ltd. |

Potassium Permanganate - Pure Grade, Technical Grade, Free Flowing Grade |

Niche Player |

Growing Indian KMnO4 manufacturer; competitive pricing |

|

JKM Chemtrade |

Industrial & Pharma Grade KMnO4 |

Niche Player |

India-based company with expanding pharma-grade production capabilities |

|

STAROXOCHEM |

Potassium Permanganate |

Niche Player |

India-based manufacturer; diversified inorganic chemical portfolio; export-oriented with growing KMnO4 presence across water treatment and industrial end-uses |

Key players include Carus Group Inc., Merck KGaA, Libox Chem (India) Pvt. Ltd., JKM Chemtrade, STAROXOCHEM, and others.

Key Company Profiles

Carus Group Inc.

Carus Group Inc. is a United States-based specialty chemical company and a leading global producer of potassium permanganate. The company is a key supplier to water treatment utilities, environmental remediation projects, and industrial chemical markets across North America and globally.

- Key Products: CAIROX Potassium Permanganate, AQUOX Potassium Permanganate, RemOx S ISCO Reagent

- Strategic Focus: Strengthening water treatment market position through technical support services, integrated treatment solutions, and compliance-driven product development in North American and international markets.

Merck KGaA

Merck KGaA is a Germany-based global science and technology company and a leading supplier of high-purity potassium permanganate for laboratory, analytical, and pharmaceutical applications.

- Key Products: Potassium permanganate

- Strategic Focus: Expanding the supply of high-purity analytical and pharmaceutical-grade reagents through its global MilliporeSigma and Merck Millipore distribution platforms, with emphasis on compliance with ACS, ISO, and Ph Eur standards for laboratory, biopharma quality control, and regulated industrial applications across Europe, North America, and Asia-Pacific.

Market Concentration Analysis

The potassium permanganate market is moderately concentrated, with the top five producers collectively accounting for an estimated 55-65% of global production volume. Chinese producers dominate aggregate volume, while specialty-grade leaders in the United States and India command premium market positions through quality and regulatory differentiation.

Market concentration is gradually declining as Indian manufacturers scale capacity and new entrants in Southeast Asia and the Middle East develop domestic production capabilities. The pharmaceutical-grade sub-segment remains more concentrated, with fewer qualified producers meeting stringent purity and regulatory standards globally.

Investment & Growth Opportunities

Highest Growth Segments

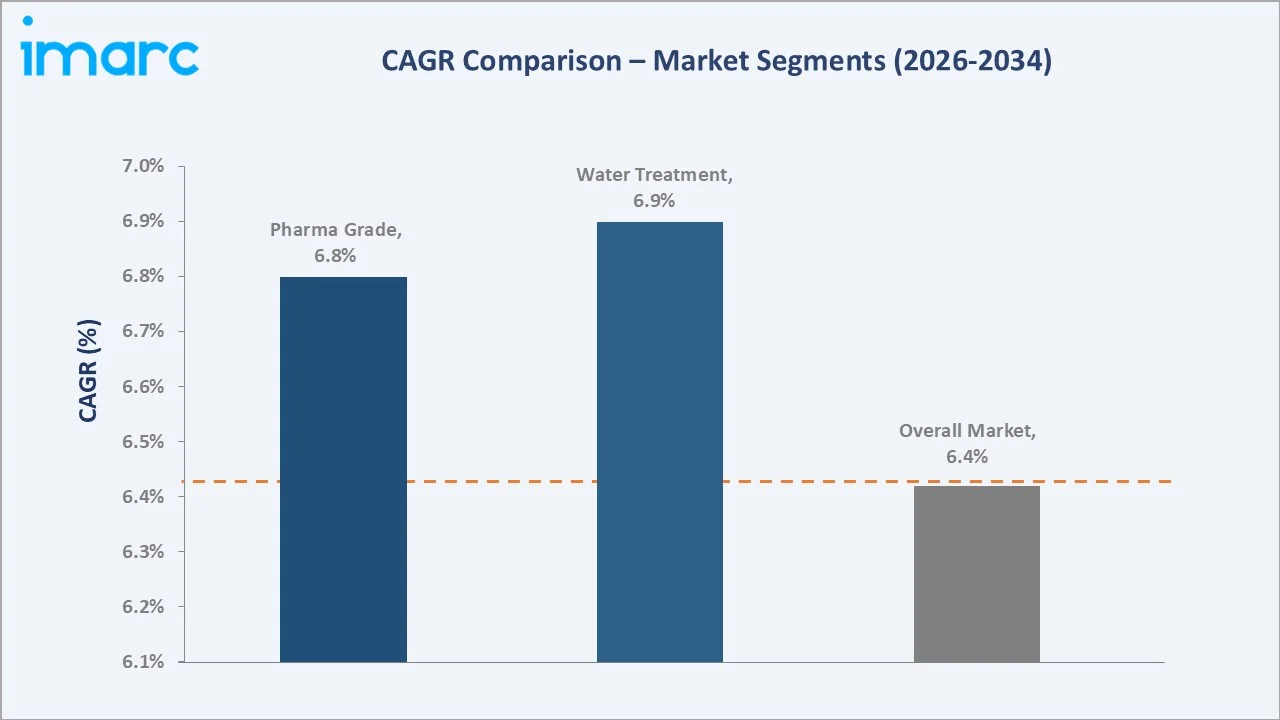

Pharmaceutical Grade KMnO4 (~8-9% CAGR), Aquaculture application (~8.5% CAGR), Wastewater Treatment (~7% CAGR), and India market expansion (~9-10% CAGR) represent the highest-return investment vectors through 2034. These combine above-market growth with structural demand drivers including healthcare expansion and regulatory compliance investment.

Emerging Investment Opportunities

India's Jal Jeevan Mission-driven rural water infrastructure rollout is creating high-volume demand for water treatment-grade potassium permanganate. With over 19 crore rural households targeted for tap water connections, the KMnO4 procurement pipeline for municipal treatment represents a sustained decade-long demand pool through 2034.

Investment Themes

- Pharmaceutical-grade capacity expansion in India: Capturing premium pricing and export opportunities to Europe and North America through WHO-GMP and REACH-compliant production facilities aligned with global regulatory standards.

- Aquaculture sector supply chain development in Southeast Asia: Establishing dedicated distribution and technical support networks for aquaculture-grade KMnO4 across Vietnam, Indonesia, and Thailand as the sector expands.

- Integrated water treatment solutions: Bundling KMnO4 dosing systems with monitoring technology and service contracts to transition from commodity chemical supply to value-added service models with higher margins.

Future Market Outlook (2026-2034)

The global potassium permanganate market is projected to grow from 360.1 Thousand Tons in 2025 to 640.8 Thousand Tons by 2034, delivering a 6.42% CAGR. The market anchor of 491.4 Thousand Tons in 2030 reflects the midpoint of a sustained expansion driven by water quality regulation, chemical manufacturing growth, and agricultural adoption.

Three structural forces define the forecast trajectory. First, the global water treatment infrastructure upgrade cycle, driven by WHO and EPA-aligned regulatory frameworks, will sustain municipal procurement of water-treatment-grade KMnO4. Second, India's industrial and agricultural demand is expected to outperform the global average, driven by economic expansion and infrastructure investment.

Third, pharmaceutical-grade segment expansion will add a premium revenue layer to the market, as dermatological applications grow with rising healthcare access across Asia-Pacific and the Middle East. Free Flowing Grade will consolidate its dominant position as industrial buyers prioritize handling safety and dosing precision throughout the forecast period.

Research Methodology

Primary Research

Primary research comprised structured interviews with 45+ industry stakeholders (2025), including chemical production managers, water utility procurement officers, agricultural chemical distributors, pharmaceutical-grade KMnO4 buyers, and regulatory compliance specialists across key global markets.

Secondary Research

Secondary research encompassed company annual reports, EPA and WHO water quality guidelines, REACH chemical registration data, Indian Ministry of Chemicals and Fertilizers production statistics, China National Chemical Industry Association data, and global trade flow databases. Over 50 secondary sources reviewed.

Forecasting Models

Market volume forecasts developed using a demand-side bottom-up model: (i) application-specific demand by region; (ii) per-capita consumption trends for water treatment; (iii) industrial output growth proxies for chemical manufacturing; (iv) grade mix shift adjustment for pharmaceutical and free flowing grade premium through 2034.

Potassium Permanganate Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | ‘000 Tons, Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Predictive Market Assessment:

|

| Applications Covered | Water Treatment, Wastewater Treatment, Chemicals Manufacturing, Aquaculture, Metal Processing, Air and Gas Purification, Others |

| Grades Covered | Free Flowing Grade, Technical Grade, Pharmaceutical Grade |

| Regions Covered | China, United States, European Union, India, Others |

| Companies Covered | Carus Group Inc., Merck KGaA, Libox Chem (India) Pvt. Ltd., JKM Chemtrade, STAROXOCHEM, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the potassium permanganate market from 2020-2034.

- The research report study provides the latest information on the market drivers, challenges, and opportunities in the global potassium permanganate market.

- The study maps the leading, as well as the fastest-growing, regional markets.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the potassium permanganate industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Potassium Permanganate Market Report

The global potassium permanganate market reached 360.1 Thousand Tons in 2025, driven by Water Treatment at 34.8% application share, Free Flowing Grade dominance at 51.3%, and China's leading regional share of 36.7%.

The market grows at 6.42% CAGR during 2026-2034, reaching 640.8 Thousand Tons by 2034. Growth reflects rising water treatment regulation, expanding chemical manufacturing, and accelerating pharmaceutical-grade adoption globally.

Water Treatment leads at 34.8%, capturing the largest and most stable demand segment through municipal drinking water quality compliance and industrial process water treatment globally. It is supported by WHO and EPA regulatory frameworks that mandate effective oxidant-based treatment.

Free Flowing Grade leads at 51.3%, preferred for superior dosing precision, ease of handling, and broad industrial applicability across water treatment and chemical manufacturing end-uses globally.

China leads at 36.7% through its dominant chemical production base, large-scale domestic water treatment infrastructure, and significant KMnO4 export volumes to global markets across Asia-Pacific, Africa, and Latin America.

Leading companies include Carus Group Inc., Merck KGaA, Libox Chem (India) Pvt. Ltd., JKM Chemtrade, STAROXOCHEM, and others.

The market is projected to reach 640.8 Thousand Tons by 2034, anchored at 491.4 Thousand Tons in 2030, with pharmaceutical-grade and aquaculture applications growing above the overall market CAGR and India emerging as the fastest-growing regional market.

Three priority investment opportunities: pharmaceutical-grade capacity expansion in India targeting export markets; aquaculture-focused distribution development in Southeast Asia; and integrated water treatment solution services bundling KMnO4 dosing with monitoring and compliance service models.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)

Choose your plan

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Single User License

- 1 User License, Access on 2 Devices

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- No Printing Rights

- 10% Free Report Customization

- 10–12 Weeks of Analyst Support

Five User License

- Access for 5 Users, 2 Devices per User

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- Dedicated Account Manager

- 12–14 Weeks of Analyst Support

- No Printing Rights

- 15% Free Report Customization

- 25% Discount on Your Next Purchase

Corporate User License

- Unlimited User Access (Within Your Organization)

- PDF Report + Excel Dataset

- Lifetime Access

- Dedicated Account Manager

- 14–20 Weeks of Analyst Support

- No Printing Rights

- 20% Free Report Customization

- 30% Discount on Your Next Purchase

Essential Insights

What's included:

3 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 2 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Professional Access

What's included:

5 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 8 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Business Advantage

What's included:

8 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 14 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Enterprise Intelligence

What's included:

10 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 20 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade