Pigeon Pea Market Size, Share, Trends and Forecast by Region 2026-2034

Pigeon Pea Market Size, Share, Trends & Forecast (2026-2034)

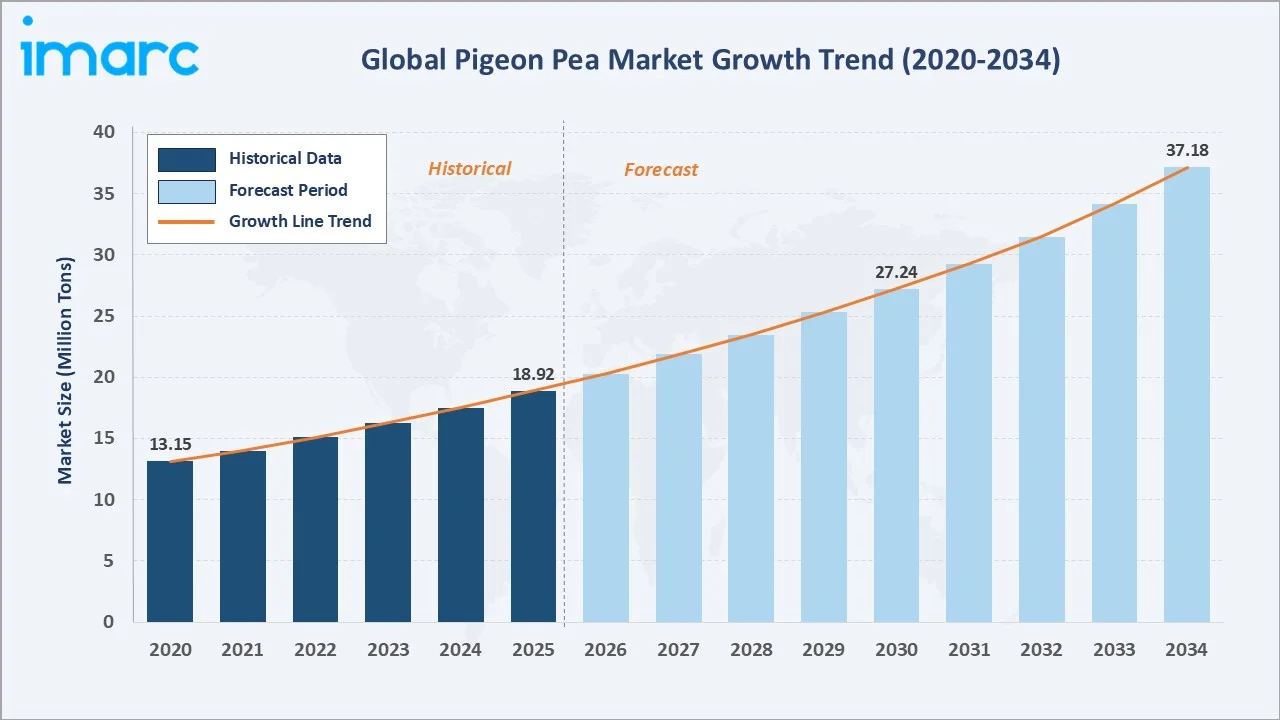

The pigeon pea market reached a volume of 18.92 Million Tons in 2025 and is projected to reach 37.18 Million Tons by 2034, exhibiting a CAGR of 7.56% during 2026-2034. Rising global demand for plant-based protein, robust government support through minimum support price (MSP) mechanisms, and the crop's natural climate resilience are the primary drivers shaping market growth.

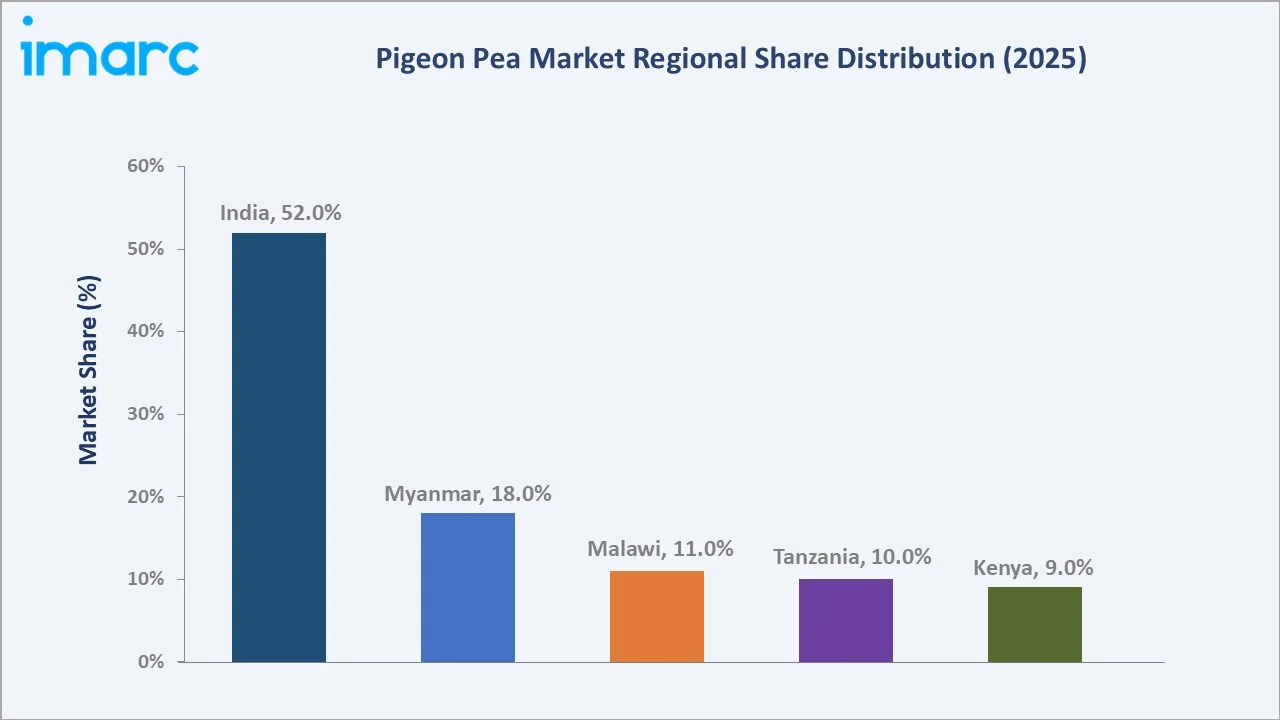

India dominates the market with a 52.0% share in 2025, driven by its large-scale cultivation base, strong domestic consumption, and supportive government policies promoting pulse production.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

18.92 Million Tons |

|

Forecast Market Size (2034) |

37.18 Million Tons |

|

CAGR (2026-2034) |

7.56% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

India (52.0%, 2025) |

|

Second Largest Region |

Myanmar (18.0%, 2025) |

The pigeon pea market expanded from 13.15 Million Tons in 2020 to 18.92 Million Tons in 2025, supported by expanding cultivation in India and emerging African markets. Anchored at 27.24 Million Tons in 2030, the forecast trajectory toward 37.18 Million Tons by 2034 reflects a structurally growing market driven by rising nutrition awareness and expanding export channels across Sub-Saharan Africa and South Asia.

To get more information on this market, Request Sample

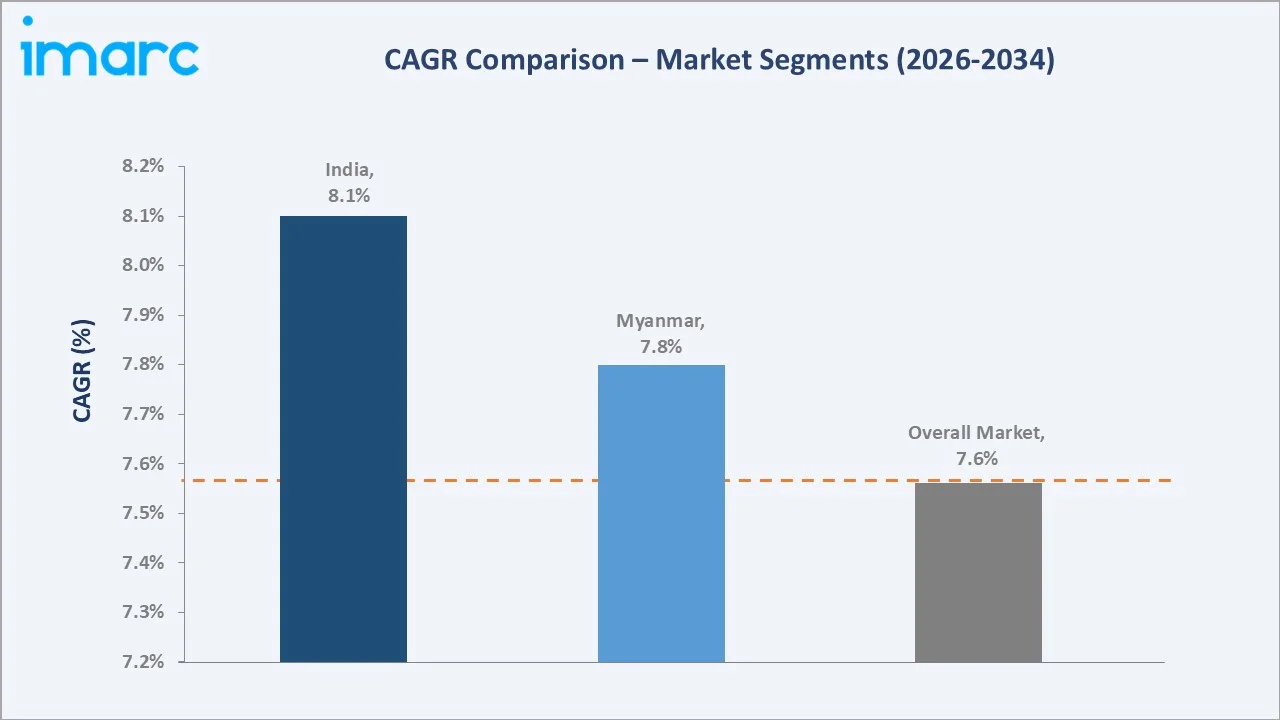

CAGR trajectories across regional sub-segments show India and Myanmar expanding faster than the overall 7.56% market CAGR, driven by government procurement programs, improved seed varieties, and growing dal processing capacity.

Executive Summary

The pigeon pea market is on a sustained growth path from 13.15 Million Tons in 2020 to a projected 37.18 Million Tons by 2034. Production has shifted toward improved hybrid varieties as smallholder farmers in India, Myanmar, and East Africa adopt higher-yielding cultivars. Rising livestock feed demand and growing plant-based protein consumption in developed markets are further expanding the end-use profile of pigeon peas beyond traditional dal consumption.

India leads the market at 52.0% in 2025, driven by domestic consumption of tur dal and strong government support through MSP and procurement programs. In October 2025, the Medical Education Minister of Karnataka, Sharan Prakash Patil, announced that the state government would distribute 2 kg of tur dal to each family living below the poverty line (BPL) statewide via the public distribution system.

Key Market Insights

|

Insight |

Data |

|

Leading Region |

India – 52.0% share (2025) |

|

Second Largest Region |

Myanmar – 18.0% share (2025) |

|

Top Companies |

ITC, Olam Agri Holdings Pte Ltd., AGT Food and Ingredients Inc. |

Key Analytical Observations Expanding On The Data Above:

- India at 52.0% dominates global pigeon pea production and consumption. Tur dal remains a dietary staple across the country, with domestic per capita consumption consistently among the highest globally. In India, tur production in 2024-2025 was projected to be 35.02 LMT, reflecting a 2.5% increase compared to 2023-2024’s output of 34.17 LMT. Government MSP support continues to incentivize cultivation and ensure price stability for farmers.

- Myanmar at 18.0% serves as a critical export hub, supplying pigeon pea primarily to India and regional markets. Smallholder-driven production, combined with growing port infrastructure, supports Myanmar's position as the second-largest contributor to global supply.

Pigeon Pea Market Overview

Pigeon pea is a perennial leguminous crop grown primarily in tropical and subtropical regions. It is a key source of plant-based protein, micronutrients, and dietary fiber, consumed widely as split pigeon pea (tur dal) in South Asia and as whole grain in Sub-Saharan Africa.

The ecosystem integrates seed suppliers, smallholder and commercial farmers, post-harvest processors, dal mills, domestic traders, export houses, and end use buyers including household consumers, food industry players, and livestock feed manufacturers. The market is supported by government procurement agencies, international commodity traders, and a growing network of agri-fintech and extension services.

Market Dynamics

To evaluate market opportunities, Request Sample

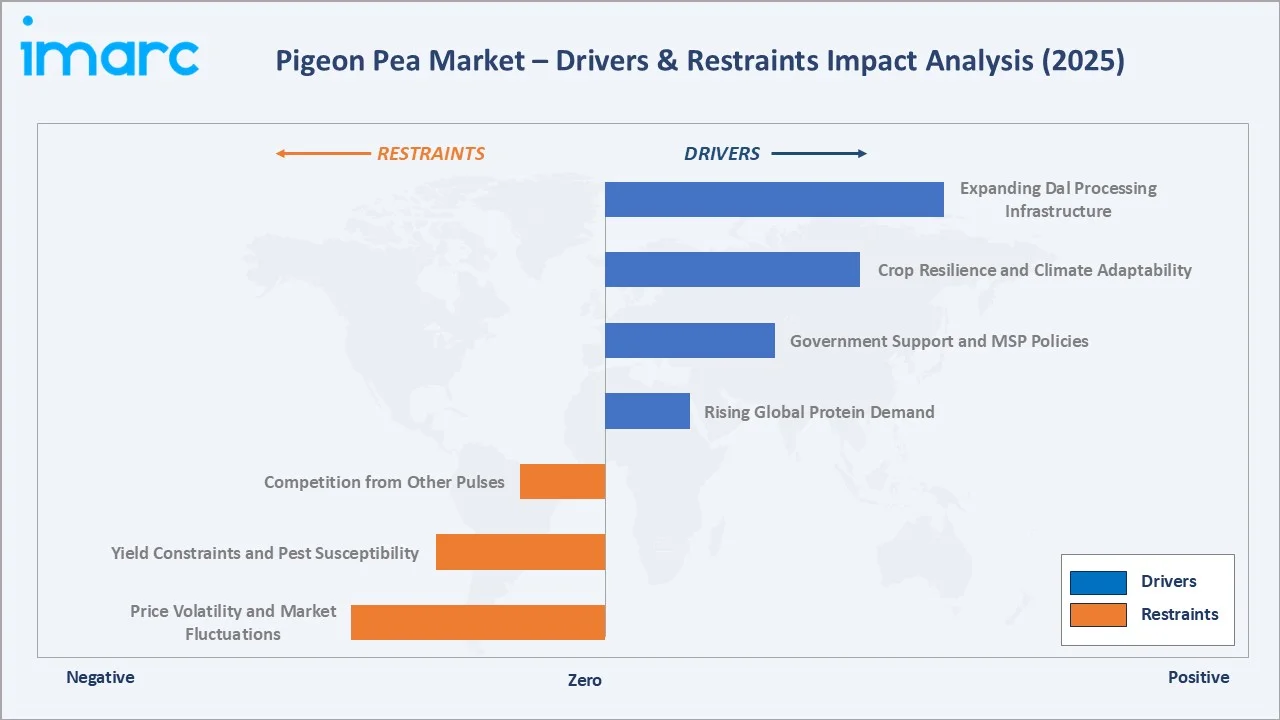

Market Drivers

- Rising Global Protein Demand: Accelerating demand for affordable plant-based protein, particularly across South Asia and Sub-Saharan Africa, is driving sustained pigeon pea consumption. Growing vegan and flexitarian dietary trends in developed economies are further broadening the demand base. As per IMARC Group, the India vegan food market size was valued at USD 1,621.30 Million in 2025.

- Government Support and MSP Policies: India's MSP mechanism provides crucial income stability for pigeon pea farmers, incentivizing cultivation and sustaining domestic supply. Regular MSP revisions and government procurement programs also help strengthen market confidence, encouraging farmers to maintain or expand pigeon pea acreage.

- Crop Resilience and Climate Adaptability: Pigeon pea's drought tolerance and nitrogen-fixing properties make it a preferred choice in rain-fed farming systems, particularly in semi-arid regions of India, East Africa, and Myanmar. Climate resilience enhances its appeal as a strategic crop under growing water stress scenarios.

- Expanding Dal Processing Infrastructure: New dal milling capacity additions in India, Malawi, and Myanmar are improving market access for smallholder producers and enabling better price realization. Vertical integration in processing supports supply chain efficiency and encourages larger farm investments.

Market Restraints

- Price Volatility and Market Fluctuations: Pigeon pea prices are highly sensitive to monsoon performance in India, government import-export policies, and global supply variability. Sharp price corrections discourage farmers from expanding cultivation acreage and create uncertainty across the value chain.

- Yield Constraints and Pest Susceptibility: Despite the crop's resilience, average yields remain relatively low due to limited adoption of improved varieties and vulnerability to wilt and sterility mosaic diseases. Low and stagnant yields constrain supply expansion even when demand is rising.

- Competition from Other Pulses: Chickpea, lentil, and black gram compete directly for farmland allocation, consumer spending, and trade flows. Shifting preferences among urban consumers create substitution pressure on pigeon pea consumption and pricing.

Market Opportunities

- East Africa and Southeast Asia Expansion: Rising agricultural investment in Tanzania, Malawi, and Myanmar is opening new frontiers for pigeon pea production. Regional food security programs and international development agency support are accelerating cultivation, processing, and export capacity.

- Functional Food and Nutraceutical Applications: Growing interest in high-protein, fiber-rich ingredients for the food processing, snack, and health supplement industries is creating new demand avenues beyond traditional dal consumption. Pigeon pea flour, protein isolates, and ready-to-eat snacks represent emerging product categories with strong premium pricing potential.

Market Challenges

- Fragmented Supply Chain and Post-Harvest Losses: Highly fragmented smallholder production and inadequate storage infrastructure result in significant post-harvest losses and income leakage.

- Limited Access to Finance and Technology: Many smallholder pigeon pea farmers in Sub-Saharan Africa and South Asia face limited access to formal credit, quality seeds, and extension services, constraining yield improvements and adoption of modern cultivation practices.

Emerging Market Trends

1. Adoption of High-Yielding Hybrid Varieties

Breeding programs led by ICRISAT and national agricultural research institutions are releasing improved pigeon pea cultivars with higher yield potential and disease resistance. Wider adoption of these varieties is reducing yield gaps and supporting supply expansion in key producing regions. In June 2025, ICRISAT introduced a new heat-tolerant pigeon pea cultivar (ICPV 25444) capable of withstanding high temperatures and shorter growing cycles, which is expected to promote year-round cultivation and enhance productivity.

2. Growth of Organic and Clean-Label Pigeon Pea Products

Consumer preferences for organic, non-GMO, and clean-label legume products are gaining traction across North America, Europe, and urban India. Certified organic pigeon pea commands a significant price premium and is attracting investment from specialty food processors and health-focused retailers.

3. Expansion of Pigeon Pea-Based Protein Ingredients

Food technology companies are increasingly incorporating pigeon pea protein isolates and concentrates into plant-based meat alternatives, protein bars, and dairy substitutes. This trend is broadening the market's addressable demand base well beyond traditional dal consumption.

4. Digital Agriculture and Traceability Platforms

Agri-tech platforms offering crop advisory, input procurement, and market linkages are being deployed at scale in India and East Africa, helping smallholder pigeon pea farmers improve productivity and access better prices. The integration of digital traceability systems is also enhancing supply chain transparency, enabling exporters and processors to meet evolving quality and sustainability requirements in international markets.

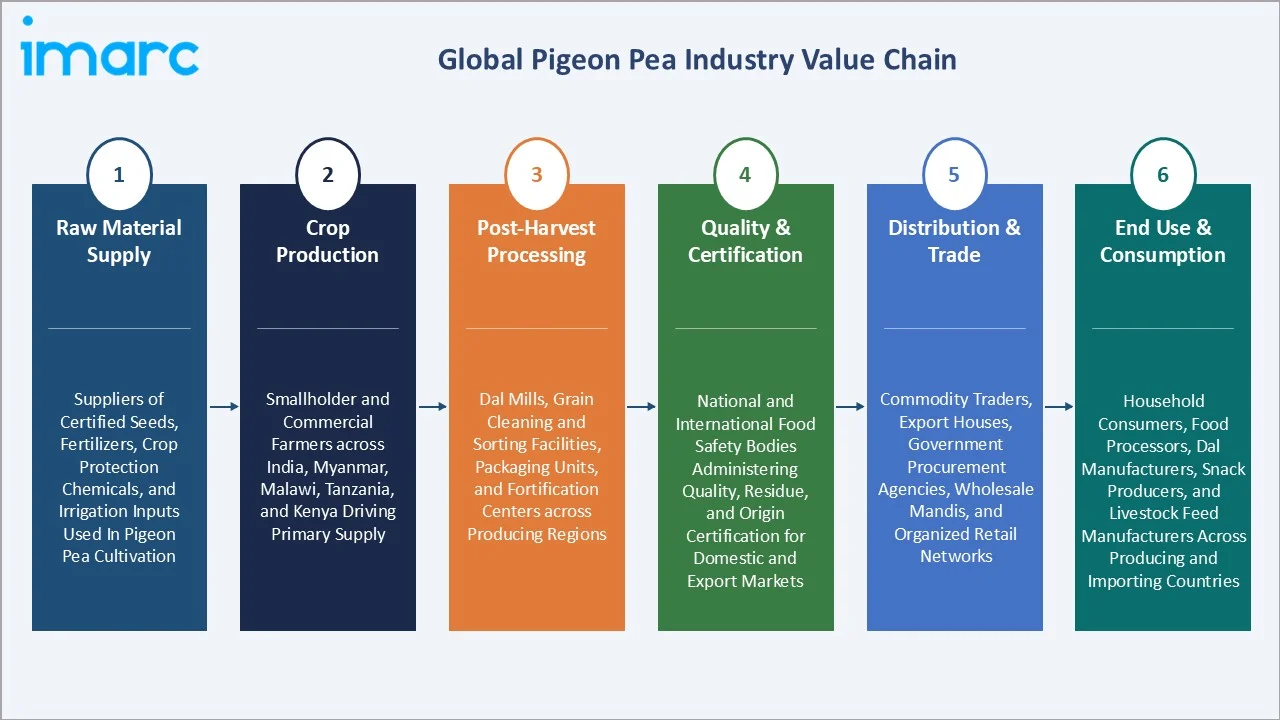

Industry Value Chain Analysis

The pigeon pea value chain spans six stages, from input supply through end use and lifecycle management. Post-harvest processing and distribution capture the highest value-add, while farm-level production and export trade determine market price dynamics.

|

Stage |

Key Players / Examples |

|

Raw Material Supply |

Suppliers of certified seeds, fertilizers, crop protection chemicals, and irrigation inputs used in pigeon pea cultivation |

|

Crop Production |

Smallholder and commercial farmers across India, Myanmar, Malawi, Tanzania, and Kenya driving primary supply |

|

Post-Harvest Processing |

Dal mills, grain cleaning and sorting facilities, packaging units, and fortification centers across producing regions |

|

Quality & Certification |

National and international food safety bodies administering quality, residue, and origin certification for domestic and export markets |

|

Distribution & Trade |

Commodity traders, export houses, government procurement agencies, wholesale mandis, and organized retail networks |

|

End Use & Consumption |

Household consumers, food processors, dal manufacturers, snack producers, and livestock feed manufacturers across producing and importing countries |

Vertically integrated players combining processing with direct procurement and export channels achieve stronger cost control and margin realization than smaller, fragmented intermediaries.

Technology Landscape in the Pigeon Pea Industry

Seed Biotechnology and Breeding Innovation

Advanced breeding techniques, including marker-assisted selection and genomic approaches, are being used to develop pigeon pea varieties with higher yields, early maturity, and tolerance to drought and disease. These innovations are directly shortening breeding cycles and accelerating cultivar release timelines.

Precision Agriculture and Digital Farming

Remote sensing, mobile-based crop advisory platforms, and soil health monitoring tools are being deployed across pigeon pea cultivation zones in India and East Africa. These technologies enable better input management, early pest detection, and yield forecasting, improving farm economics for smallholder producers.

Post-Harvest and Processing Technology

Modern dal milling equipment with improved dehusking efficiency, optical sorting, and dust-free packaging capabilities is reducing processing losses and improving product quality. Adoption of these technologies is expanding in India's organized milling sector and is beginning to penetrate East African markets.

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Region |

India |

52.0% |

2025 |

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

|

India |

52.0% |

Large domestic demand for tur dal, government MSP support, and expanding dal processing capacity |

|

Myanmar |

18.0% |

Strong export orientation to India, growing smallholder cultivation, and rising regional trade infrastructure |

|

Malawi |

11.0% |

Smallholder-led production expansion, international development program support, and growing export volumes |

|

Tanzania |

10.0% |

Rising domestic food security focus, expanding cultivation acreage, and government support for pulse production |

|

Kenya |

9.0% |

Growing urban demand for protein-rich legumes, improving market linkages, and regional export opportunity |

India at 52.0% in 2025 leads the market. The country is the world's leading producer, consumer, and importer of pigeon pea. The central role of tur dal in the Indian diet, combined with a robust procurement framework, makes India the defining market for global pigeon pea price and supply dynamics.

Myanmar at 18.0% is the most export-oriented major producer, with the bulk of its output directed to Indian demand. Growing trade relationships and improving post-harvest infrastructure are supporting its continued market share.

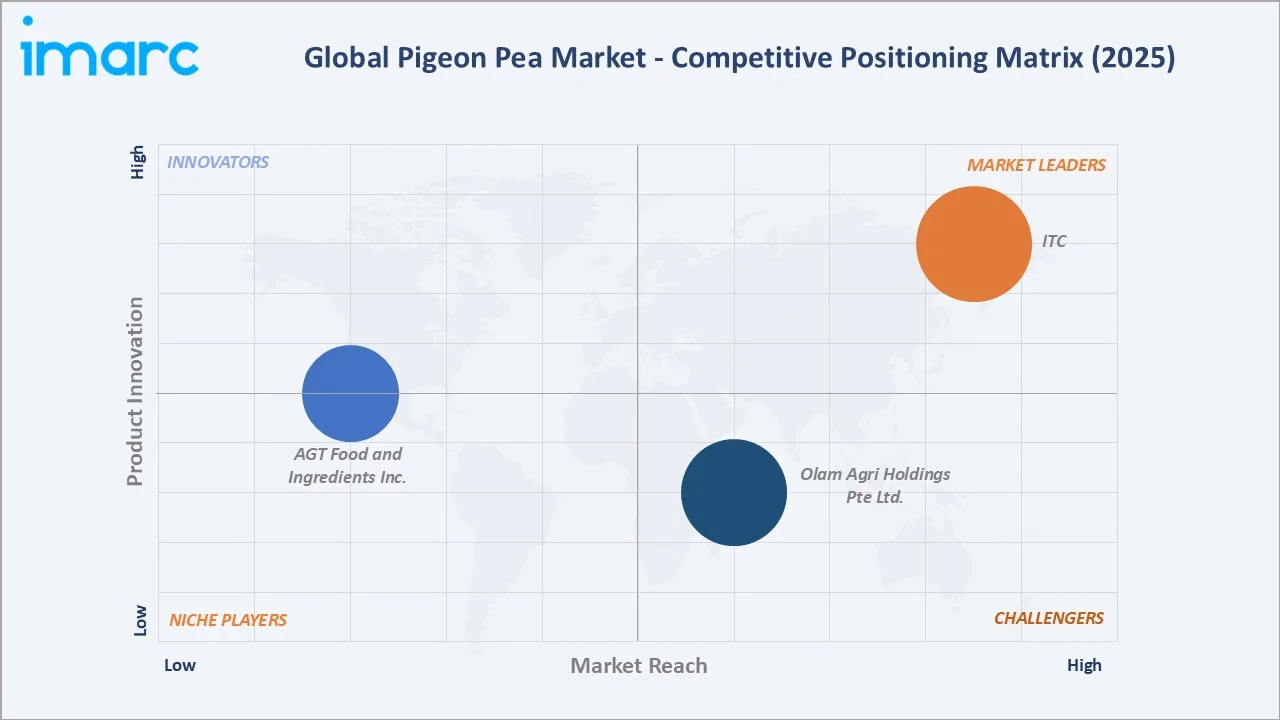

Competitive Landscape

The pigeon pea market is highly fragmented, with production largely driven by smallholder farmers across Asia and Africa. Competition is concentrated among processors, traders, exporters, and branded food companies that leverage sourcing networks, processing capabilities, and distribution reach. Market participants compete on product quality, procurement efficiency, supply reliability, and market access.

|

Company Name |

Brand / Key Product |

Position |

Strategic Focus |

|

ITC |

Aashirvaad, 24 Mantra Organic |

Leader |

Branded dal and organic staples portfolio, deep agri supply chain integration, and retail distribution |

|

Olam Agri Holdings Pte Ltd. |

NutriWaah |

Challenger |

Global commodity origination, risk management, and distribution across Africa and Asia |

|

AGT Food and Ingredients Inc. |

PulsePlus Ingredients |

Emerging |

Specialty pulse processing, plant-based protein ingredients, and global export supply |

Key players include ITC, Olam Agri Holdings Pte Ltd., and AGT Food and Ingredients Inc., among others.

Key Company Profiles

ITC

ITC is a diversified Indian conglomerate with operations spanning fast-moving consumer goods, agri-business, hospitality, paperboards, and information technology. Its foods business is among the largest in India, built on a portfolio of well-established consumer brands across staples, snacks, and beverages.

- Product Portfolio: ITC markets pigeon pea and other pulses under its Aashirvaad brand, which covers a broad range of branded staples including atta, rice, spices, and dals. The 24 Mantra Organic brand extends its reach into the certified organic pulses segment.

- Recent Development: ITC completed the 100% acquisition of Sresta Natural Bioproducts in June 2025 for INR 400 Crore, adding the 24 Mantra Organic brand to its foods portfolio.

- Strategic Focus: Expanding branded packaged staples and organic foods through a wide distribution network, leveraging agri-supply chain integration to strengthen sourcing, and deepening retail presence across urban and rural India.

Olam Agri Holdings Pte Ltd.

Olam Agri Holdings Pte Ltd. is a globally diversified food, feed, and fiber agri-business. The company operates across a broad range of agricultural commodities, with strong origination, processing, and distribution capabilities in key producing and consuming regions worldwide.

- Product Portfolio: The company engages in the origination, processing, and trading of pulses, including pigeon pea, alongside grains, oilseeds, rice, edible oils, cotton, and other agricultural commodities. In India, its NutriWaah brand markets a range of pulses sourced from select farming regions across India and Africa.

- Recent Development: The company has expanded its global agri-commodity origination footprint and strengthened its supply chain infrastructure in key markets across Africa, Asia, and the Middle East, maintaining active pulse sourcing operations in major producing regions.

- Strategic Focus: Global commodity origination and risk management, building processing and distribution capabilities across high-growth emerging markets, and connecting farming communities to international food and agri-trade flows.

AGT Food and Ingredients Inc.

AGT Food and Ingredients Inc. is a Saskatchewan-based global leader in the processing and distribution of pulses, staple foods, and plant-based protein ingredients. The company operates a vertically integrated model spanning origination, processing, and ingredient supply to food manufacturers across multiple continents.

- Product Portfolio: AGT Food and Ingredients Inc. processes pulses, including pigeon pea, into a range of value-added formats like split, whole, flour, protein concentrates, fibers, and starches, marketed through its PulsePlus Ingredients brand.

- Recent Development: The company continues to strengthen its global pulse sourcing and processing capabilities through ongoing investments in supply chain efficiency, value-added ingredient solutions, and expanded market reach across key food and ingredient applications.

- Strategic Focus: Leading in specialty pulse processing and ingredient innovation, growing the plant-based protein ingredients category, and expanding global export supply to food manufacturers seeking non-GMO, gluten-free, and sustainably sourced pulse-derived ingredients.

Market Concentration Analysis

The pigeon pea market exhibits a high degree of production-level fragmentation, with hundreds of millions of smallholder farmers spread across India, Myanmar, and East Africa contributing to global supply. Processing and distribution, however, are more concentrated, with ITC, Olam Agri Holdings Pte Ltd., and AGT Food and Ingredients Inc. holding meaningful shares of organized distribution and branded supply.

Barriers to entry in branded processing and distribution include brand trust, distribution reach, procurement scale, and food safety compliance infrastructure. These factors favor established players with existing farmer network relationships.

Consolidation at the processing level continues through capacity expansion and branding initiatives. State cooperatives and government procurement agencies maintain a significant counter-balancing role, ensuring competitive floor pricing and market access for smallholder producers.

Investment & Growth Opportunities

Fastest-Growing Regions

India and Myanmar are expected to grow faster than the overall 7.56% market CAGR through 2034, supported by expanding dal consumption and improved supply chain infrastructure. Malawi and Tanzania offer the highest absolute production growth potential as international development investment accelerates.

Emerging Markets

Malawi represents a promising growth market, supported by increasing adoption of improved pigeon pea varieties and export opportunities to major importing countries. Myanmar represents a key origination expansion opportunity as its agricultural infrastructure investment cycle deepens.

Venture & Investment Trends

Investment is concentrated in dal processing capacity, agri-tech platforms for smallholder productivity improvement, organic certification infrastructure, and plant-based protein ingredient extraction. Branded packaged dal and functional food ingredients are attracting the most consumer-facing investment interest.

Future Market Outlook (2026-2034)

The pigeon pea market is forecast to expand from 18.92 Million Tons in 2025 to 37.18 Million Tons by 2034 at a CAGR of 7.56%, adding approximately 18.26 Million Tons in incremental volume over the forecast period.

Four forces will shape the market through 2034: continued yield improvement from hybrid variety adoption, expanding East African production capacity, rising demand from plant-based food processors, and growing export flows to Europe and the Middle East.

By 2034, India is expected to remain the dominant market force, while Tanzania and Malawi's collective share is projected to increase meaningfully as mechanization and processing investment deepens.

Research Methodology

Primary Research

Primary research included consultations with pigeon pea farmers, dal millers, commodity traders, export houses, government procurement officers, and food industry professionals, validating market sizing, regional production dynamics, and competitive positioning across the forecast period.

Secondary Research

Secondary sources included FAO agricultural production statistics, national agricultural ministry reports, government MSP notifications, export-import trade data, company annual reports, industry association publications, and trade press covering pulse commodity markets.

Forecasting Models

Market forecasts combined top-down and bottom-up models using crop area and yield trend data, domestic consumption per capita trajectories, import-export balances, and price scenario analysis. Scenario modeling addressed monsoon variability, policy change risks, and competitive crop substitution effects.

Frequently Asked Questions About the Pigeon Pea Market Report

The market reached a volume of 18.92 Million Tons in 2025, driven by strong demand from India, growing East African production, and Myanmar's export-oriented supply base.

The market is projected to grow at a CAGR of 7.56% from 2026 to 2034, reaching 37.18 Million Tons, fueled by rising protein demand, yield improvements, and expanding processing infrastructure.

India dominates with a 52.0% market share in 2025, propelled by large domestic tur dal consumption, government procurement programs, and its role as the world's largest producer and consumer.

Myanmar holds an 18.0% share in 2025, driven by its strong export orientation to India and growing smallholder cultivation base across its tropical agricultural zones.

Leading players include ITC, Olam Agri Holdings Pte Ltd., and AGT Food and Ingredients Inc., among others.

Growth is driven by rising plant-based protein demand, government MSP policies, expanding dal milling capacity, crop climate resilience, and increasing export flows from India and Myanmar.

Key restraints include price volatility, yield stagnation due to limited adoption of improved varieties, pest susceptibility, fragmented post-harvest infrastructure, and import-export policy uncertainty.

Key opportunities include plant-based protein ingredient development, organic and clean-label product segments, and technology-driven post-harvest loss reduction.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)