Saudi Arabia Cybersecurity Market Size, Share, Trends and Forecast by Offering, Deployment Mode, End User, and Region 2026-2034

Saudi Arabia Cybersecurity Market Size, Share, Trends & Forecast (2026-2034)

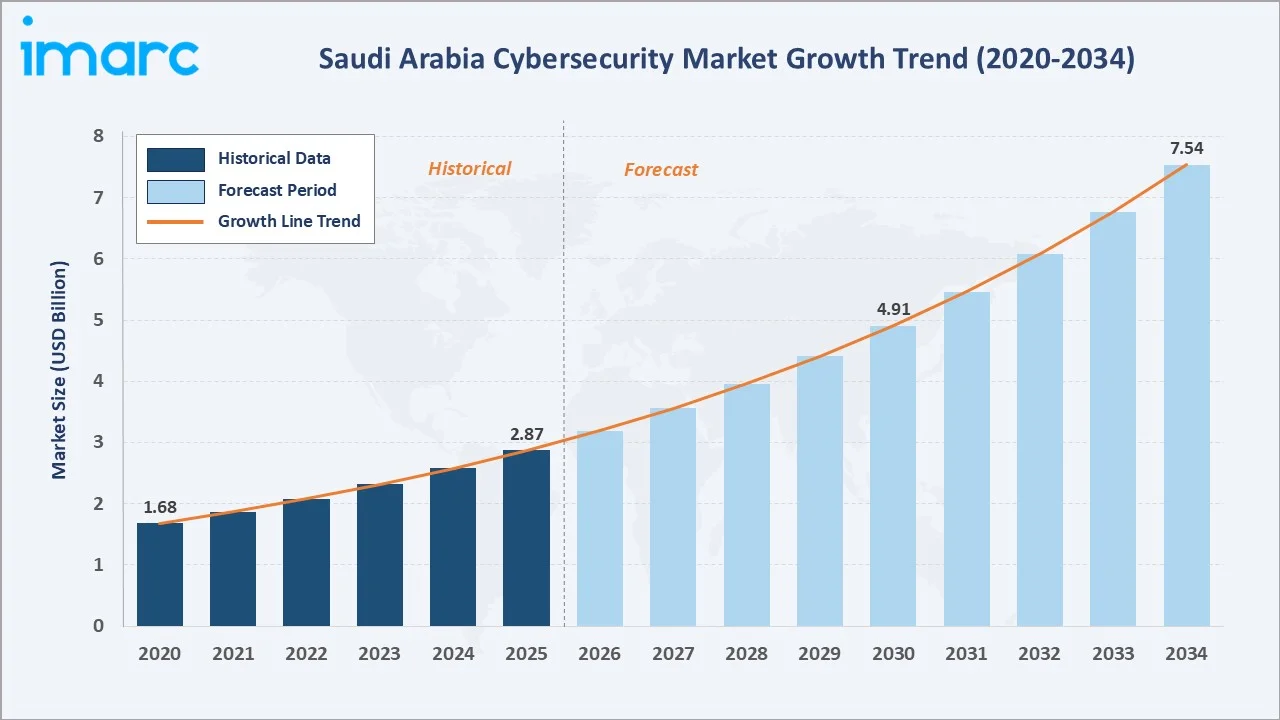

The Saudi Arabia cybersecurity market reached USD 2.87 Billion in 2025 and is projected to reach USD 7.54 Billion by 2034, growing at a CAGR of 11.32% during 2026-2034. Saudi Vision 2030, rising cyber threats targeting critical infrastructure, accelerated cloud adoption, and stringent National Cybersecurity Authority (NCA) regulations are the primary catalysts.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 2.87 Billion |

|

Forecast Market Size (2034) |

USD 7.54 Billion |

|

CAGR (2026-2034) |

11.32% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

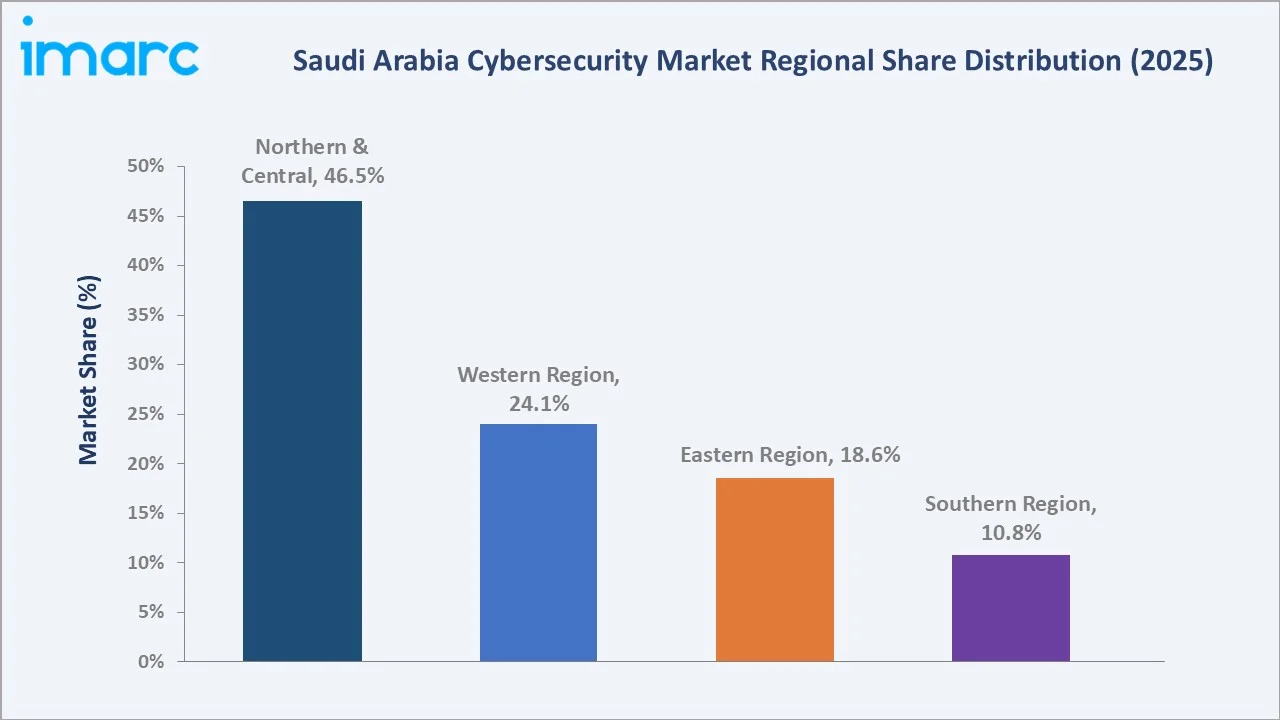

Largest Region |

Northern and Central Region (46.5%, 2025) |

|

Fastest Growing Region |

Western Region |

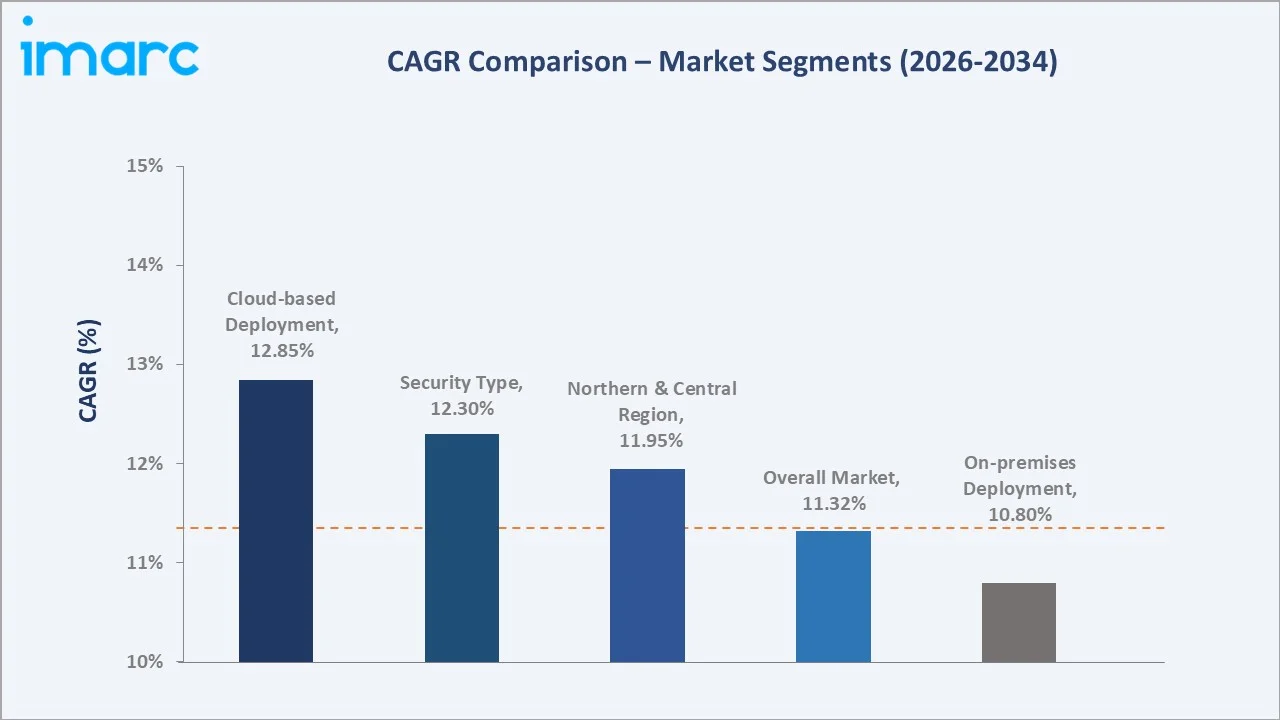

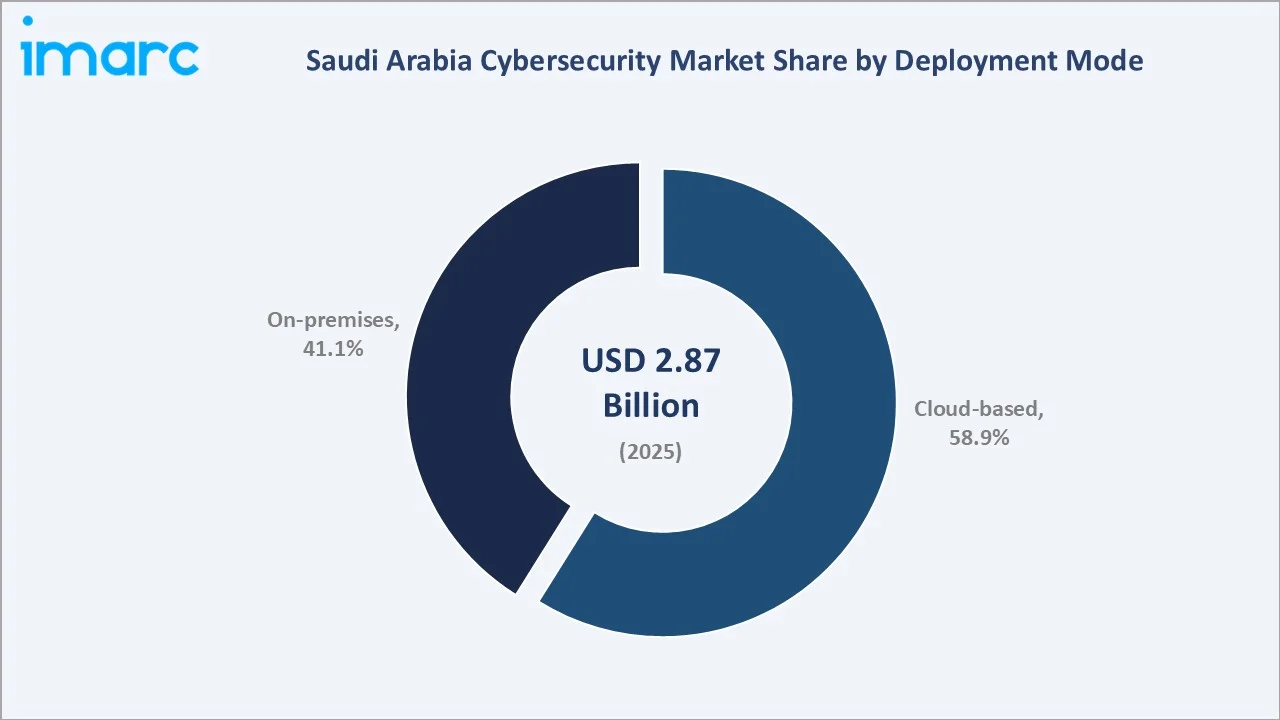

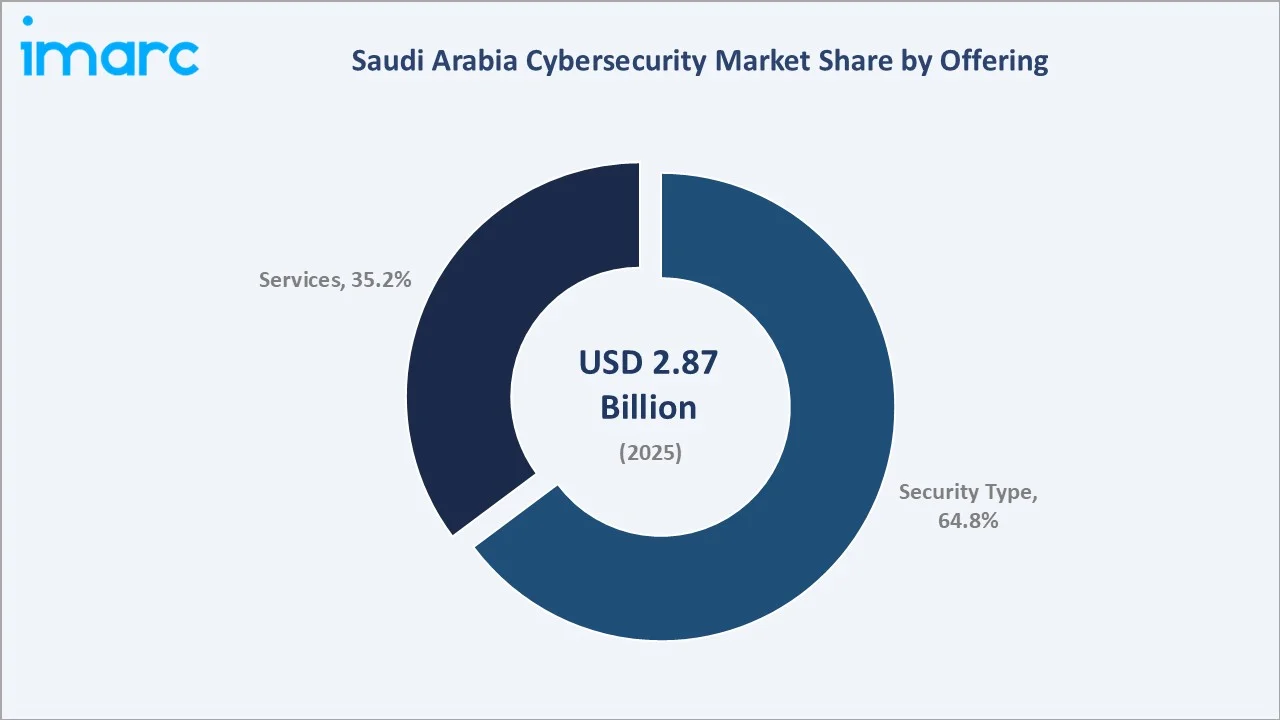

Cloud-based deployment commands a 58.9% market share in 2025, reflecting the enterprise shift to scalable security-as-a-service models. Security-type solutions dominate the offering segment at 64.8%, underpinned by demand for network security, endpoint protection, and identity and access management across BFSI, government, and energy sectors.

To get more information on this market, Request Sample

With applications spanning government and defense, BFSI, healthcare, oil and gas, manufacturing, and IT and telecommunications, the market is set for sustained double-digit expansion, supported by mandatory NCA compliance frameworks, multi-billion-dollar national cybersecurity investment programs, and increasing sophistication of state-sponsored and ransomware threat actors targeting the kingdom.

Executive Summary

The Saudi Arabia cybersecurity market is on an accelerated growth trajectory, underpinned by escalating digital threats, comprehensive regulatory mandates, and the kingdom’s USD 6.4 billion investment aimed at strengthening its digital economy, innovation ecosystem, and global tech leadership. The market grew from USD 1.68 Billion in 2020 to USD 2.87 Billion in 2025 and is forecast to reach USD 7.54 Billion by 2034 at a CAGR of 11.32%, establishing Saudi Arabia as the largest cybersecurity market in the Middle East.

The National Cybersecurity Authority (NCA), established in 2017, has emerged as one of the most active cybersecurity regulators globally, issuing 22 binding cybersecurity frameworks and controls including the Critical Systems Cybersecurity Controls (CCC) and Cloud Cybersecurity Controls (CCC-C). These frameworks mandate security architecture, vendor certification, and incident reporting standards across all government entities and critical infrastructure operators.

Cloud-based deployment (58.9%) is the dominant mode, reflecting the intersection of cloud adoption and shared-responsibility security models. Security type solutions lead the offering segment at 64.8%, driven by network security, endpoint detection and response (EDR), and zero-trust architecture investments. The Northern and Central Region anchors the market at 46.5%, concentrated in Riyadh’s financial and government district ecosystem.

Key Market Insights

|

Insight |

Data |

|

Largest Segment (Offering) |

Security Type – 64.8% share (2025) |

|

Largest Segment (Deployment) |

Cloud-based – 58.9% share (2025) |

|

Leading Region |

Northern and Central Region – 46.5% share (2025) |

|

Fastest Growing Region |

Western Region (Jeddah BFSI & smart city demand) |

|

Top Companies |

Cisco Systems, Inc., IBM Corporation, Palo Alto Networks, stc, and Fortinet, Inc. |

|

Market Opportunity |

AI-powered SOC and quantum-safe cryptography platforms |

Key Analytical Observations:

- Security type solutions command 64.8% of the market in 2025, driven by network security infrastructure upgrades, endpoint detection and response (EDR) deployments, and identity and access management (IAM) mandated under NCA’s Essential Cybersecurity Controls (ECC).

- Cloud-based security holds 58.9% of deployments in 2025, as enterprises leverage cloud-native SIEM, CASB, and SASE platforms that offer scalability, real-time threat intelligence, and reduced capital expenditure versus on-premises hardware.

- The Northern and Central Region commands 46.5%, concentrated in Riyadh’s government ministries, Saudi Aramco headquarters, and the dense BFSI cluster regulated by SAMA’s stringent cybersecurity framework.

- The Western Region is the fastest-growing market, driven by Jeddah’s financial services expansion, Vision 2030 mega-project cybersecurity requirements (NEOM, Red Sea Project), and the port logistics sector’s OT/ICS security needs.

- The Cisco AI Readiness Index indicates that 51% of organizations in Saudi Arabia have integrated AI into their security operations, while 60% report high awareness of AI-driven cyber risks as the technology becomes more embedded in their security frameworks.

Saudi Arabia Cybersecurity Market Overview

Saudi Arabia’s cybersecurity market encompasses the full spectrum of security solutions and services protecting digital assets, critical infrastructure, cloud environments, and data across government, enterprise, and critical infrastructure sectors. The market is structured around two primary segments: security type solutions (network security, endpoint security, cloud security, application security, identity and access management, data security, and others) and professional and managed security services.

The kingdom ranks among the world’s most targeted nations for cyberattacks. Saudi Arabia’s internet-connected critical infrastructure, including oil and gas facilities managed by Saudi Aramco and SABIC, financial systems regulated by SAMA, and government digital services, attracts persistent Advanced Persistent Threat (APT) actors, ransomware groups, and hacktivist campaigns. The 2012 Shamoon attack on Saudi Aramco, which wiped out 35,000 computers, remains a watershed event that permanently elevated cybersecurity to a national security priority.

Market Dynamics

To evaluate market opportunities, Request Sample

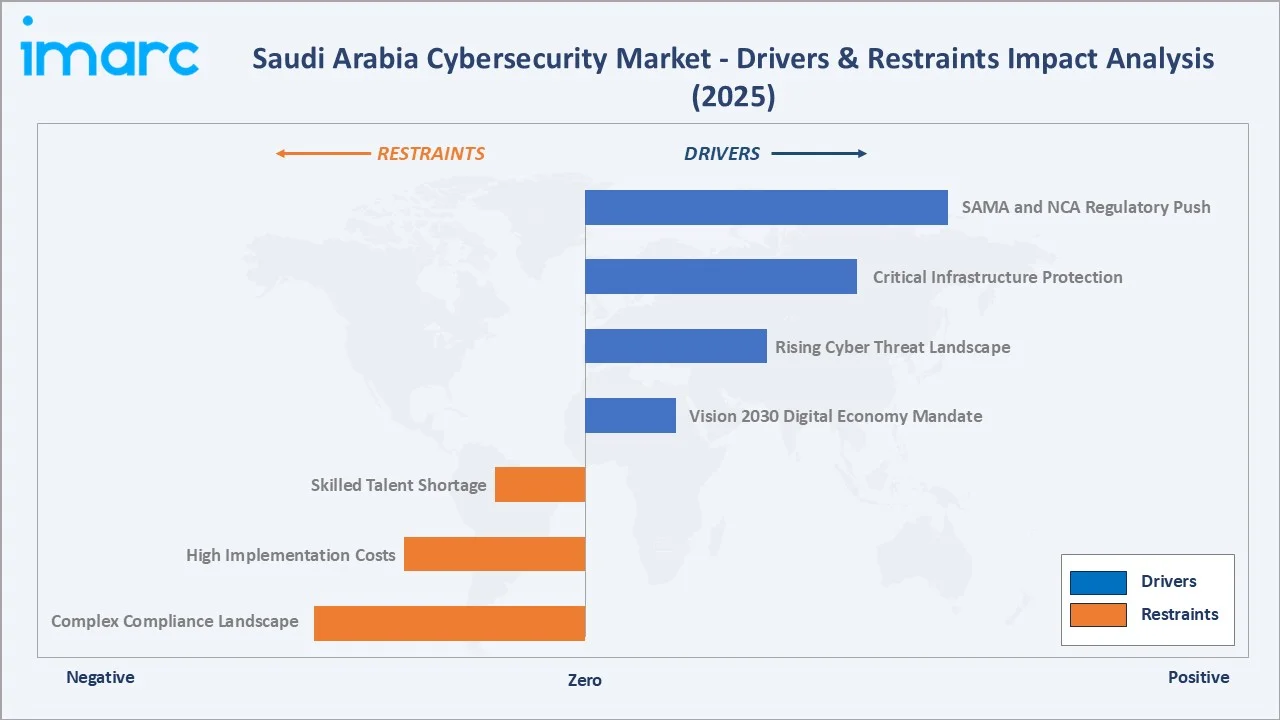

Market Drivers

- Vision 2030 Digital Economy Mandate: Key mandates include the Anti-Cyber Crime Law, the National Cybersecurity Authority (NCA) Essential Cybersecurity Controls (ECC), Cloud Cybersecurity Controls (CCC), and Critical Systems Cybersecurity Controls (CSCC), which require organizations to implement robust data protection, risk management, and incident response measures.

- Rising Cyber Threat Landscape: According to a 2024 IBM Security study, the average financial impact of a cyberattack on organizations in Saudi Arabia and the UAE reached USD 6.53 million. Saudi Arabia’s cybersecurity market expanded by 19% in 2024, contributing SAR 18.5 billion to the national economy and reinforcing the Kingdom’s position as a global cybersecurity leader.

- Critical Infrastructure Protection: Saudi Arabia’s oil and gas infrastructure, water treatment facilities, and power grid are classified as critical national assets. The NCA’s Critical Systems Cybersecurity Controls (CCC) framework mandates OT/ICS security standards, intrusion detection, and incident response capabilities for all operators, creating a large addressable market for industrial cybersecurity specialists.

- SAMA and NCA Regulatory Push: The SAMA Cybersecurity Framework provides a structured set of guidelines and controls to enhance cybersecurity maturity across financial institutions, ensuring protection of sensitive data and critical systems. NCA’s cloud cybersecurity controls require government agencies using public cloud services to implement data encryption, access management, and continuous monitoring, directly driving security product procurement.

Market Restraints

- Skilled Talent Shortage: Saudi Arabia faces a deficit of a 47% talent gap and over 35,000 unfilled cybersecurity roles. The NCA’s National Cybersecurity Workforce Development Program targets training specialists, but the near-term gap compels organizations to pay 40–60% salary premiums for qualified cybersecurity engineers and architects, inflating operating costs.

- High Implementation Costs: Enterprise-grade zero-trust architecture deployments cost USD 2–5 million for mid-sized organizations in Saudi Arabia, including infrastructure, software licensing, integration, and training. For SMEs and smaller government bodies, this represents a significant barrier, creating security coverage gaps that adversaries exploit.

- Complex Compliance Landscape: Organizations operating across multiple Saudi sectors must comply with overlapping frameworks: NCA ECC, SAMA Cybersecurity Framework, PDPL data protection requirements, and sector-specific controls for healthcare (MOH), energy (NEOM), and telecommunications (CITC). Managing multi-framework compliance simultaneously creates resource strain and vendor management complexity.

Market Opportunities

- AI-Powered Security Operations Centers (SOCs): Saudi Arabia’s National Cybersecurity Operations Center (NCOC) represents the government’s anchor investment in AI-driven threat intelligence. Commercial SOC-as-a-service platforms leveraging AI for automated threat detection, prioritization, and response represent a USD 900 million opportunity by 2030.

- OT/ICS Cybersecurity for Energy and Industrial Sectors: Saudi Arabia’s expanding industrial zones (Jubail, Yanbu, NEOM’s industrial city Oxagon) represent a concentrated OT/ICS security market. Purdue model segmentation, unidirectional security gateways, and OT-native threat detection platforms are mandatory under CCC, creating a USD 650 million specialty segment by 2030.

Market Challenges

- Evolving and Sophisticated Threat Actors: State-sponsored APT groups and ransomware-as-a-service (RaaS) operations increasingly target Saudi Arabia’s financial and energy sectors. IBM’s annual Cost of a Data Breach Report showed that the average cost of a data breach for businesses in the Middle East reached SAR 32.80 million in 2024, reflecting the high-value nature of targets and sophisticated attack methodologies deployed by threat actors.

- Third-Party and Supply Chain Risk: Saudi organizations rely heavily on international technology vendors for hardware, software, and managed services. Supply chain compromises (analogous to SolarWinds in 2020) expose the kingdom’s critical digital infrastructure to cascading risks. NCA’s vendor risk management requirements are expanding, but enforcement remains challenging across the extended supplier ecosystem.

Emerging Market Trends

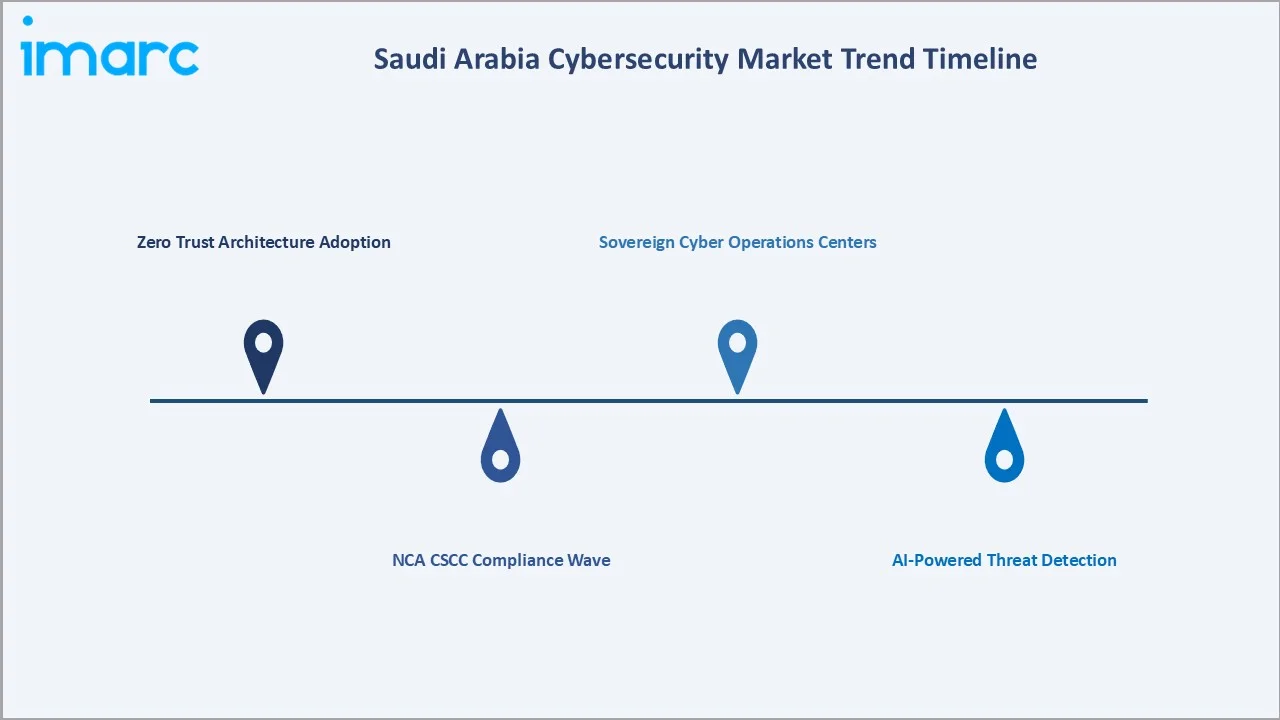

1. Zero Trust Architecture Adoption

Modern Zero Trust Network Access (ZTNA) solutions, especially when integrated with SASE frameworks, provide Saudi organizations with scalable security, centralized visibility, continuous monitoring, and simplified IT operations. Solutions like FortiGate ZTNA combine firewall, secure access, and zero-trust capabilities into a unified platform, enabling secure remote access without requiring major infrastructure changes.

2. NCA CSCC Compliance Wave

NCA’s Cloud Cybersecurity Controls (CSCC) and the Critical Systems Cybersecurity Controls (CCC), issued in 2022–2023, triggered a compliance-driven procurement cycle across all Saudi government entities and critical infrastructure operators. Spending on GRC (Governance, Risk and Compliance) platforms, vulnerability management tools, and security assessment services grew 41% between 2022 and 2024, representing over USD 280 million in incremental market value.

3. AI-Powered Threat Detection

Generative AI and machine learning are being integrated into SIEM, SOAR, and EDR platforms deployed in Saudi enterprises. Saudi Aramco’s digital security team deployed an AI-powered anomaly detection system in 2024 that reduced alert fatigue by 70% and improved threat hunting efficiency by 3x.

4. Sovereign Cyber Operations Centers

Saudi Arabia is building national sovereign cyber capabilities, including the National Cybersecurity Operations Center (NCOC), sector-specific SOCs for energy (Aramco), finance (SAMA), and healthcare, and NEOM Technology & Digital’s dedicated security operations infrastructure. Sovereign SOC investments total USD 1.2 billion in the 2025–2030 window, anchoring demand for SIEM, SOAR, threat intelligence, and incident response services.

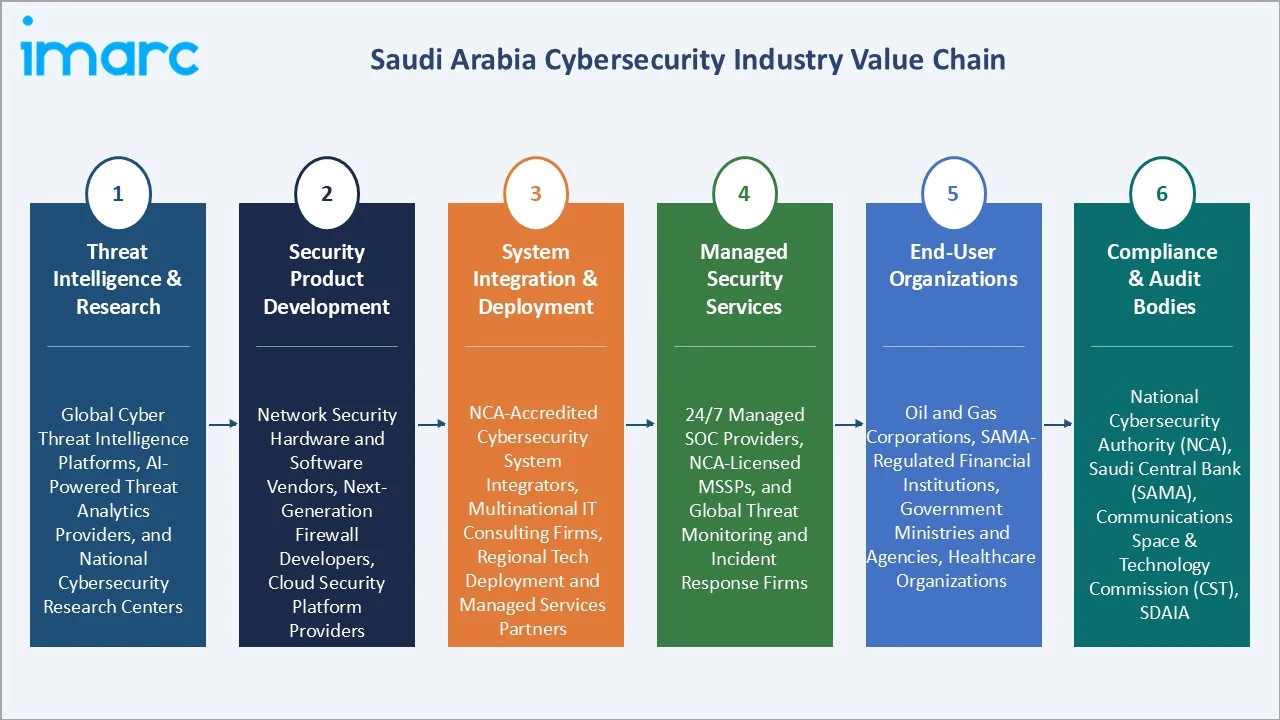

Industry Value Chain Analysis

The Saudi Arabia cybersecurity value chain spans threat intelligence research through end-user organizations and compliance oversight, with specialized operators at each stage whose performance directly influences the kingdom’s collective cyber resilience and regulatory compliance posture.

|

Stage |

Key Players / Examples |

|

Threat Intelligence & Research |

Global cyber threat intelligence platforms, AI-powered threat analytics providers, and national cybersecurity research centers |

|

Security Product Development |

Network security hardware and software vendors, next-generation firewall developers, cloud security platform providers |

|

System Integration & Deployment |

NCA-accredited cybersecurity system integrators, multinational IT consulting firms, regional technology deployment and managed services partners |

|

Managed Security Services |

24/7 managed SOC providers, NCA-licensed managed security service providers (MSSPs), and global threat monitoring and incident response firms |

|

End-User Organizations |

Oil and gas corporations, SAMA-regulated financial institutions, government ministries and agencies, healthcare organizations |

|

Compliance & Audit Bodies |

National Cybersecurity Authority (NCA), Saudi Central Bank (SAMA), Communications, Space and Technology Commission (CST), SDAIA |

Technology Landscape in the Saudi Arabia Cybersecurity Industry

Extended Detection and Response (XDR)

XDR platforms integrating endpoint, network, cloud, and email telemetry into unified detection and response workflows are gaining rapid adoption. Crux’s cybersecurity and AI governance services support XDR capabilities by enabling centralized risk management, continuous monitoring, and integrated visibility across enterprise systems, aligning with unified threat detection strategies.

Secure Access Service Edge (SASE) and Zero Trust Network Access

SASE convergence of networking and security functions is accelerating in Saudi Arabia’s distributed enterprise environments, particularly for Vision 2030 mega-projects spanning vast geographic areas. NEOM’s distributed city nodes, ROSHN’s smart residential communities, and PIF’s diversified portfolio companies have adopted SASE architectures from Zscaler, Cisco, and Fortinet, creating a USD 240 million SASE market in 2025.

OT/ICS Security for Critical Infrastructure

Operational technology security has emerged as a critical specialty following NCA’s CCC framework mandates. Claroty, Dragos, and Nozomi Networks have established Saudi partnerships with system integrators to address the unique security requirements of SCADA systems, distributed control systems (DCS), and safety instrumented systems (SIS) in oil and gas, water, and power sectors.

Market Segmentation Analysis

The report covers the following segments:

| Segment Category | Leading Segment | Market Share | Year |

|---|---|---|---|

| Offering | Security Type | 64.8% | 2025 |

| Deployment Mode | Cloud-based | 58.9% | 2025 |

| End User | 🔒 | 🔒 | 2025 |

| Region | Northern and Central Region | 46.5% | 2025 |

By Deployment Mode

Cloud-based deployment dominates the Saudi cybersecurity market with a 58.9% share in 2025. This reflects the broad enterprise migration to cloud infrastructure and the availability of cloud-native security platforms offering faster deployment, lower upfront capital costs, and continuous threat intelligence updates. NCA’s CSCC compliance requirements have accelerated cloud security investment, as organizations must implement CASB, CSPM, and CWPP controls for all cloud deployments.

To access detailed market analysis, Request Sample

On-premises deployment retains a 41.1% share, primarily in government entities and critical infrastructure operators where data sovereignty requirements and NCA mandates prohibit storing classified or sensitive data on external cloud platforms. SAMA-regulated financial institutions maintain on-premises data loss prevention (DLP), privileged access management (PAM), and HSM systems for compliance with financial data residency requirements.

By Offering

Security type solutions lead the offering segment with a 64.8% share in 2025. Network security represents the largest sub-segment, driven by firewall modernization, next-generation IPS, and SD-WAN security integration mandated under NCA’s ECC. Endpoint security has seen an 82% increase in deployment since 2022, accelerated by the shift to hybrid work and BYOD policies across Saudi enterprises.

Services account for 35.2% of the market, encompassing managed security services (MSS), security consulting and integration, and incident response and forensics. Managed SOC services are the fastest-growing service category, expanding at approximately 18% annually as organizations without in-house security expertise outsource threat monitoring to accredited MSPs.

Regional Market Insights

The Northern and Central Region commands a 46.5% share in 2025, driven by Riyadh’s concentration of government ministries, the Saudi Aramco headquarters, SAMA-regulated financial institutions, and the kingdom’s largest ICT and telecommunications companies. The NCA is headquartered in Riyadh, making the capital the operational hub for compliance advisory, audit services, and regulatory technology spending.

|

Region |

Share (2025) |

Key Growth Drivers |

|

Northern & Central |

46.5% |

Riyadh govt. cluster, Saudi Aramco, BFSI concentration |

|

Western Region |

24.1% |

Jeddah BFSI, NEOM security, port OT/ICS |

|

Eastern Region |

18.6% |

Oil & gas OT security, Aramco Dhahran, SABIC |

|

Southern Region |

10.8% |

NEOM southern nodes, Jizan industrial, edge security |

The Western Region (24.1%) is the fastest-growing, benefitting from Jeddah’s expanding financial hub, NEOM’s USD 500 billion smart city security infrastructure requirements, and the Red Sea Project’s hospitality IT security needs. The Eastern Region (18.6%) is dominated by OT/ICS cybersecurity spending from Saudi Aramco, SABIC, and SWCC, where production network security represents a mission-critical priority.

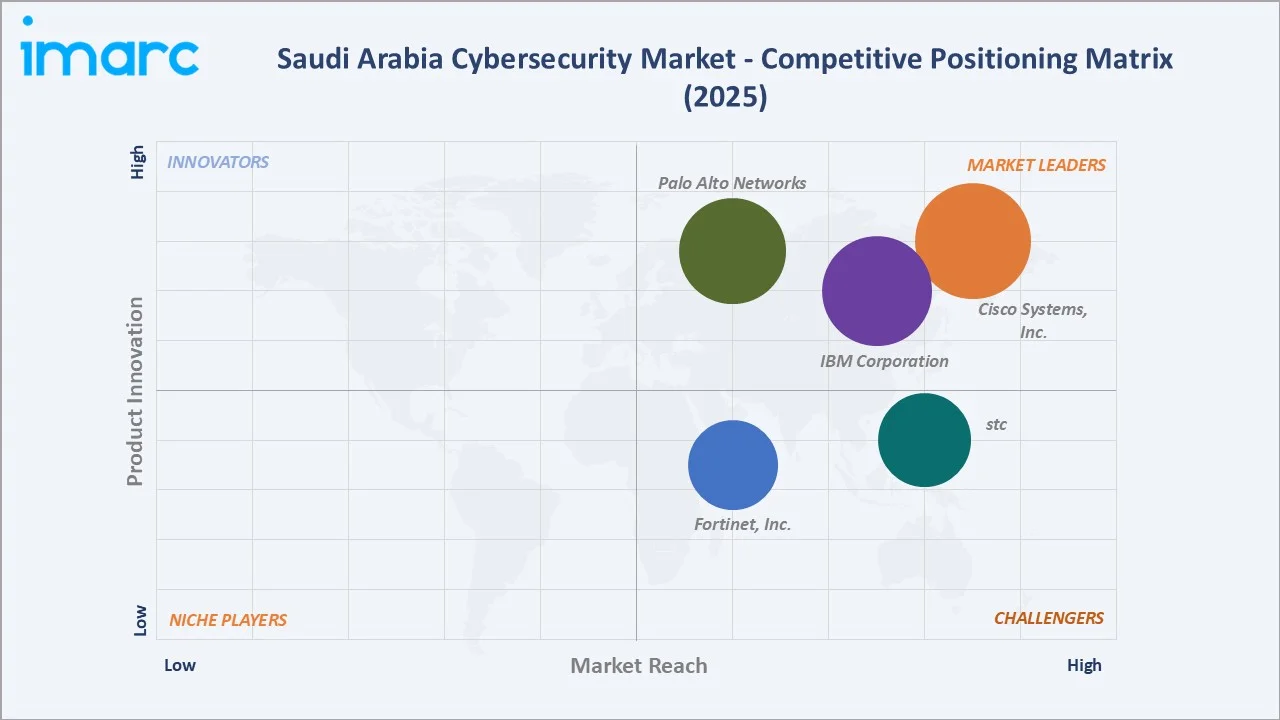

Competitive Landscape

The Saudi Arabia cybersecurity market exhibits moderate concentration at the solutions layer, with international technology vendors (Cisco Systems, Inc., IBM Corporation, Palo Alto Networks, and Fortinet, Inc.) holding an estimated 50–55% of combined solutions revenue in 2025.

|

Company |

Entity / Subsidiary |

Market Position |

Core Strength |

|

Cisco Systems, Inc. |

Cisco Saudi Arabia Limited |

Market Leader |

Largest network security portfolio; NCA-accredited vendor; Sec Ops integration |

|

IBM Corporation |

IBM Middle East and North Africa RHQ LLC |

Market Leader |

X-Force threat intelligence; government SOC partnerships |

|

Palo Alto Networks |

Palo Alto Networks Saudi Arabia Limited |

Market Leader |

Cortex XDR; Cortex Cloud; SASE leadership; NGFW dominance |

|

stc |

sirar by stc |

Strong Challenger |

Managed SOC; government framework compliance; Saudi national operator |

|

Fortinet, Inc. |

Fortinet Saudi Arabia |

Strong Challenger |

FortiGate NGFW; SD-WAN security; OT security integration |

The services layer is dominated by specialist integrators and managed security providers, where Help AG (an e& enterprise company) and stc collectively hold approximately 30–35% of managed and professional services revenue.

Key Company Profiles

Cisco Systems, Inc.

Cisco Systems, Inc. is the leading network security vendor in Saudi Arabia, operating through a dedicated Saudi Arabia entity and a network of authorized partners. Cisco is an NCA-accredited vendor for government procurement programs.

- Product Portfolio: Cisco Secure Firewall, Cisco Umbrella, Duo Security, Cisco XDR, Cisco Talos threat intelligence.

- Recent Developments: In May 2025, Cisco Systems, Inc. expanded its partnership with Saudi Arabia’s HUMAIN AI enterprise to build secure, scalable AI infrastructure, embedding advanced cybersecurity solutions into the Kingdom’s digital ecosystem.

- Strategic Focus: Government and critical infrastructure security; SASE leadership; AI-driven threat detection; NCA compliance acceleration.

stc

stc operates one of Saudi Arabia’s largest nationally owned cybersecurity services platforms via its subsidiary sirar by stc. Its deep integration with stc’s network infrastructure provides unique visibility into network-level threats across the kingdom.

- Product Portfolio: Managed SOC, DDoS protection, cloud security monitoring, identity and access management, cybersecurity training programs.

- Recent Developments: In December 2025, IBM and stc expanded their collaboration to advance quantum-safe cybersecurity solutions. The partnership focuses on strengthening data protection, mitigating cryptographic risks, and enhancing national cyber resilience in line with Saudi Arabia’s Vision 2030 digital transformation goals.

- Strategic Focus: Sovereign cybersecurity capability building; government digital services security; national-level threat intelligence sharing; Saudization of cybersecurity workforce.

Market Concentration Analysis

The Saudi Arabia cybersecurity market exhibits moderate concentration in the solutions layer, with the top five international vendors controlling an estimated 50–55% of solutions revenue in 2025. The services layer is more fragmented, with local system integrators and global consultancies competing with specialist MSSPs across a USD 1 billion annual addressable market.

Consolidation is emerging in the managed security services segment, driven by NCA’s MSSP licensing requirements that establish minimum capability thresholds (24×7 SOC, certified analysts, incident response SLAs), raising barriers to entry for smaller providers. Between 2022 and 2025, significant acquisitions reshaping the market included Etisalat’s complete acquisition of Help AG and stc’s majority stake in a regional cloud security platform.

Investment & Growth Opportunities

Fastest Growing Segments

AI-powered SOC platforms (estimated CAGR 22–25%), OT/ICS cybersecurity for energy and industrial sectors (18% CAGR), and cloud security posture management (CSPM) and SASE solutions (16% CAGR) represent the three highest-growth investment vectors through 2034. These segments collectively address a total addressable market exceeding USD 3.5 Billion within Saudi Arabia by 2034.

Emerging Market Expansion

NEOM’s smart city and industrial city infrastructure represents a USD 900 million cybersecurity opportunity by 2034. Entry modalities include NEOM Technology & Digital’s preferred vendor program, NCA’s approved product and service listings, and direct partnerships with Saudi system integrators (stc and Mobily) who hold established government and enterprise relationships across all four regions.

Venture and Institutional Investment Trends

- The Saudi Cyber Ventures Fund, announced by NCA in 2023 with SAR 600 million initial capital, targets investment in Saudi-developed cybersecurity technology companies, local talent incubation, and IP creation.

- PIF’s LEAP Tech Conference has attracted USD 4.2 billion in cybersecurity and ICT investment announcements between 2022 and 2025, with major hyperscalers embedding security investment commitments within broader data center and cloud region deals.

- Saudi Aramco Cybersecurity Investment Program provides seed and growth funding for cybersecurity startups addressing OT/ICS, threat intelligence, and industrial AI security requirements relevant to the energy sector.

Future Market Outlook (2026-2034)

The Saudi Arabia cybersecurity market is positioned for sustained, broad-based growth through 2034. From USD 2.87 Billion in 2025, the market will reach USD 4.91 Billion by 2030 and USD 7.54 Billion by 2034, delivering a total incremental market value of approximately USD 4.67 Billion over the forecast decade. The 11.32% CAGR reflects consensus among analysts who note that structural demand drivers, regulatory mandates, geopolitical threat environment, and digital transformation scale are compounding, not cyclical.

Three macro-themes define the market’s long-term trajectory: the regulatory ratchet effect (each successive NCA framework iteration raises baseline security investment requirements across all sectors); the AI threat amplification cycle (as adversaries leverage AI for attack automation, defenders must invest proportionally in AI-enhanced detection and response); and the critical infrastructure expansion wave (as NEOM, Red Sea, Qiddiya, and ROSHN projects digitize vast new assets, each requiring security architecture by design).

Vendors and investors that combine NCA regulatory expertise, Saudi-specific threat intelligence, and local Arabic-language support capability with globally competitive product platforms are positioned to disproportionately capture Saudi Arabia’s cybersecurity market growth through 2034.

Research Methodology

Primary Research

Primary research comprised structured interviews with over 130 industry participants in 2024–2025, including cybersecurity vendors, managed service providers, NCA-accredited consultants, CISO-level executives across banking, energy, and government sectors, and NCA regulatory advisors based in Riyadh and Jeddah.

Secondary Research

Secondary research encompassed NCA regulatory publications, SAMA cybersecurity circulars, IDC Middle East market data, Gartner Magic Quadrant assessments, IBM Cost of a Data Breach (Saudi Arabia annex), Fortinet Threat Landscape Reports, and company investor filings. Over 220 secondary sources were reviewed and triangulated.

Forecasting Models

Market size estimations used bottom-up segmentation modelling (by offering type, deployment mode, and end user) and top-down validation against reported vendor revenues, NCA procurement disclosures, and SAMA bank cybersecurity audit investment data. Base-case CAGR of 11.32% reflects analyst consensus validated against Vision 2030 program investment timelines.

Saudi Arabia Cybersecurity Market Report Coverage

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical and Forecast Trends, Industry Catalysts and Challenges, Segment-Wise Historical and Predictive Market Assessment:

|

| Offerings Covered |

|

| Deployment Modes Covered | Cloud-based, On-premises |

| End Users Covered | BFSI, Healthcare, Manufacturing, Government and Defense, IT and Telecommunication, Others |

| Regions Covered | Northern and Central Region, Western Region, Eastern Region, Southern Region |

| Companies Covered | Cisco Systems, Inc., IBM Corporation, Palo Alto Networks, stc, Fortinet, Inc., etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the Saudi Arabia cybersecurity market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the Saudi Arabia cybersecurity market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the Saudi Arabia cybersecurity industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Saudi Arabia Cybersecurity Market Report

The Saudi Arabia cybersecurity market reached USD 2.87 Billion in 2025, growing from USD 1.68 Billion in 2020. It is projected to reach USD 7.54 Billion by 2034 at a CAGR of 11.32%.

The market is projected to grow at a CAGR of 11.32% during 2026-2034, supported by Vision 2030 digital mandates, NCA regulatory frameworks, escalating cyber threats, and AI-driven security investments.

The Northern and Central Region leads with a 46.5% share in 2025, concentrated in Riyadh’s government ministries, BFSI cluster, Saudi Aramco headquarters, and the NCA’s operational base.

Cloud-based deployment holds 58.9% of the market in 2025, driven by enterprise cloud adoption, the availability of cloud-native SIEM/SASE platforms, and NCA’s CSCC compliance requirements for cloud security architecture.

Security type solutions command 64.8% of the market in 2025, led by network security, endpoint detection and response (EDR), and identity and access management (IAM) products mandated under NCA’s Essential Cybersecurity Controls.

Key players include Cisco Systems, Inc., IBM Corporation, Palo Alto Networks, stc, and Fortinet, Inc.

Key opportunities include AI-powered SOC platforms (CAGR 22–25%), OT/ICS security for energy and industrial sectors (18% CAGR), NEOM smart city security infrastructure, and Saudi Cyber Ventures Fund-backed domestic technology development, collectively representing a USD 3.5 Billion addressable opportunity by 2034.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)