Saudi Arabia Tire Market Size, Share, Trends and Forecast by Type, End-Use, Vehicle Type, Distribution Channel, and Region, 2026-2034

Saudi Arabia Tire Market Size, Share, Trends & Forecast (2026-2034)

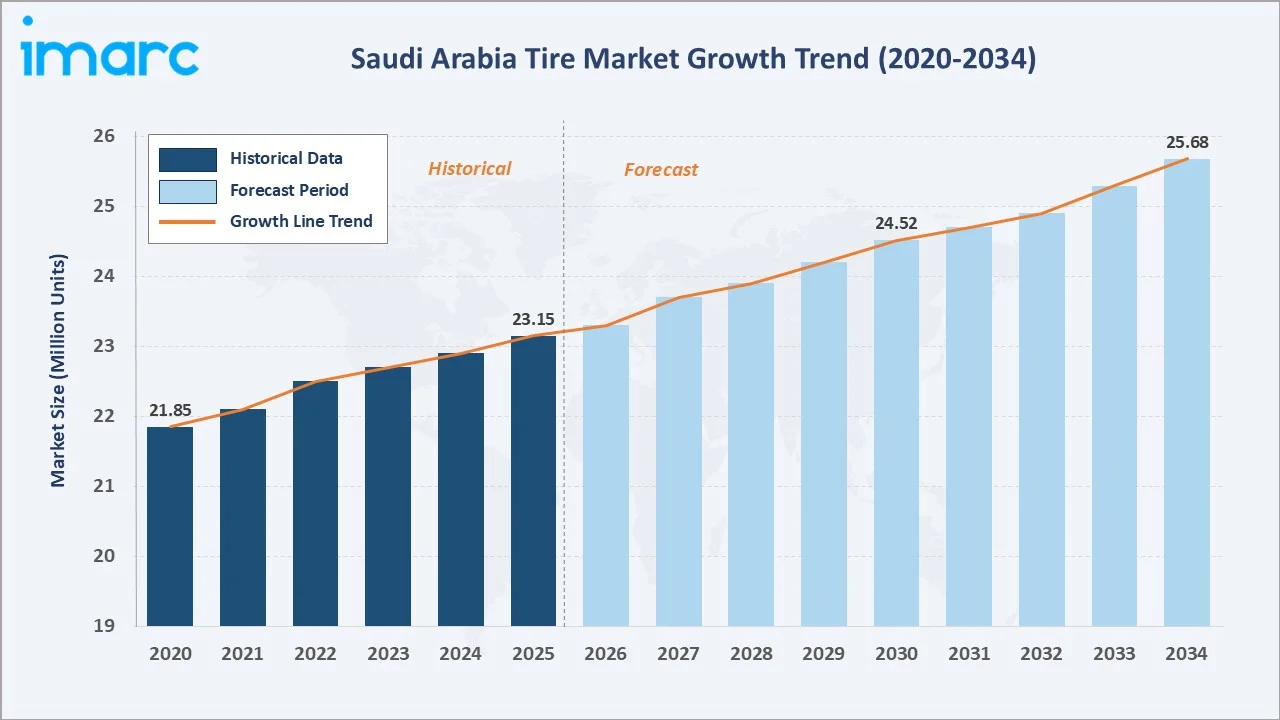

The Saudi Arabia tire market reached 23.15 Million Units in 2025 and is projected to reach 25.68 Million Units by 2034, growing at a CAGR of 1.16% during 2026-2034. Saudi Arabia’s tire market is driven by strong growth in the automotive fleet, supported by rising vehicle ownership and expanding transportation infrastructure under Vision 2030. The

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

23.15 Million Units |

|

Forecast Market Size (2034) |

25.68 Million Units |

|

CAGR (2026-2034) |

1.16% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

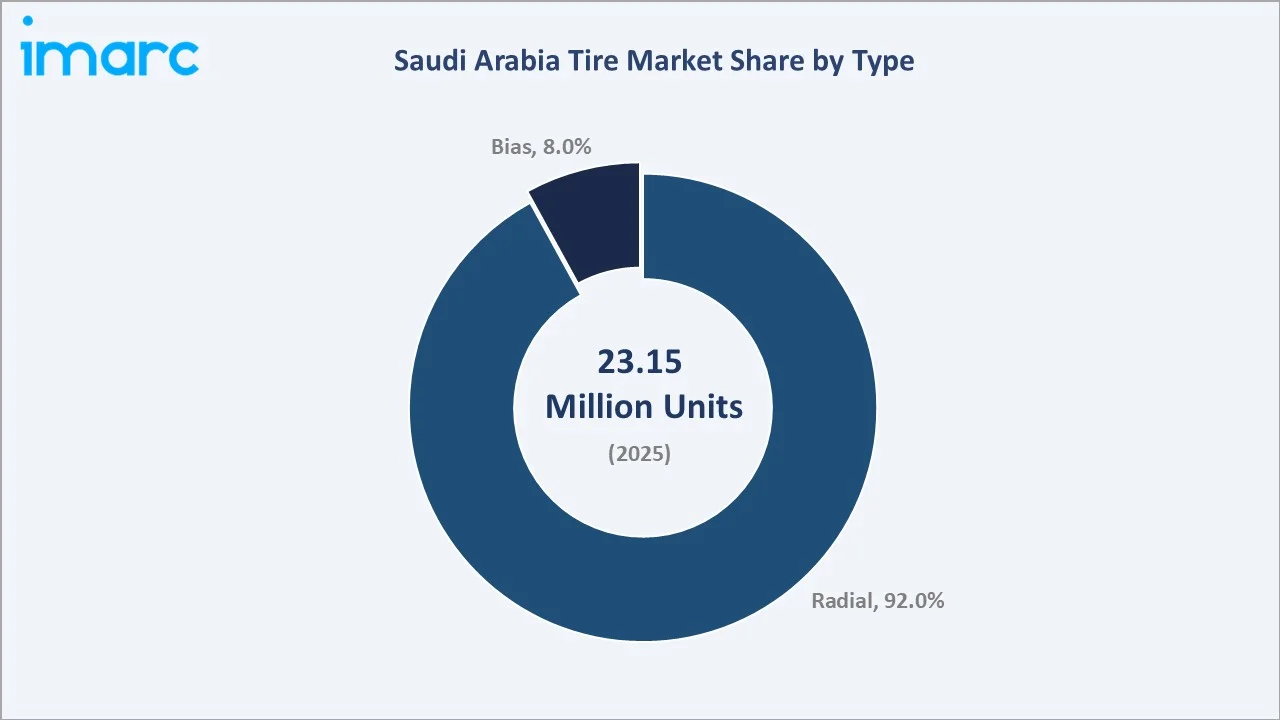

Largest Type |

Radial (92.0%, 2025) |

|

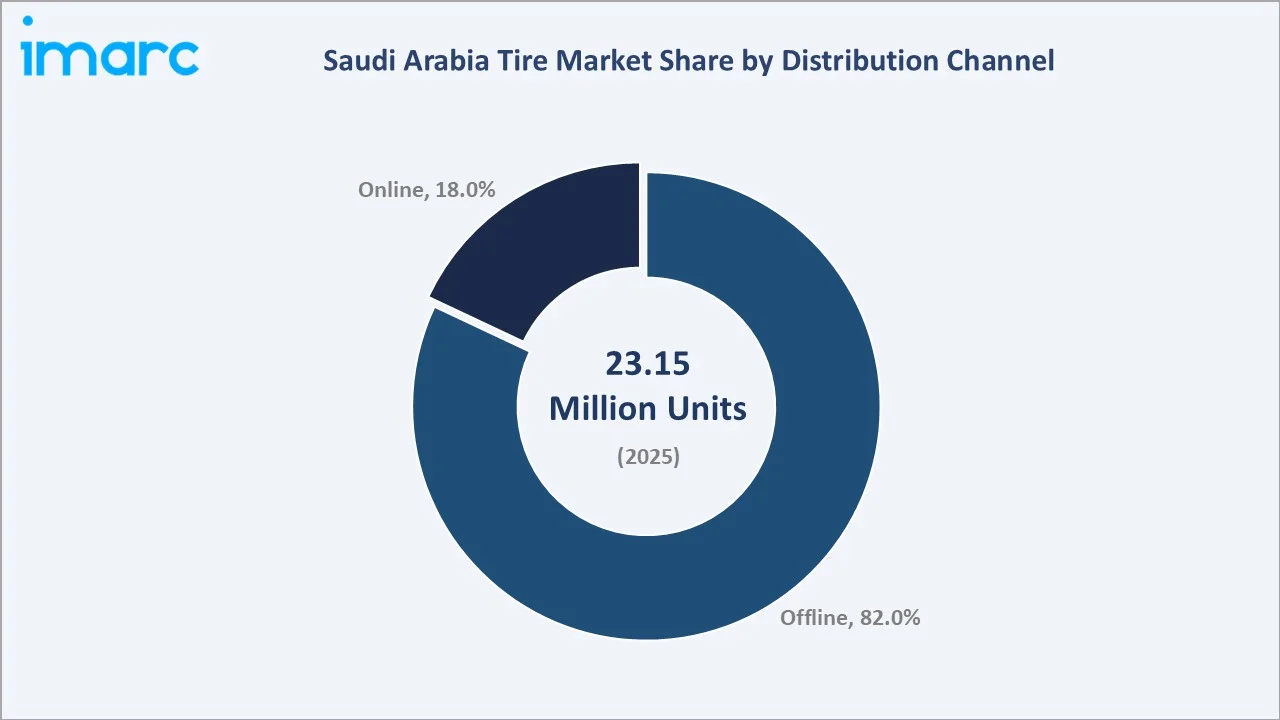

Largest Distribution Channel |

Offline (82.0%, 2025) |

|

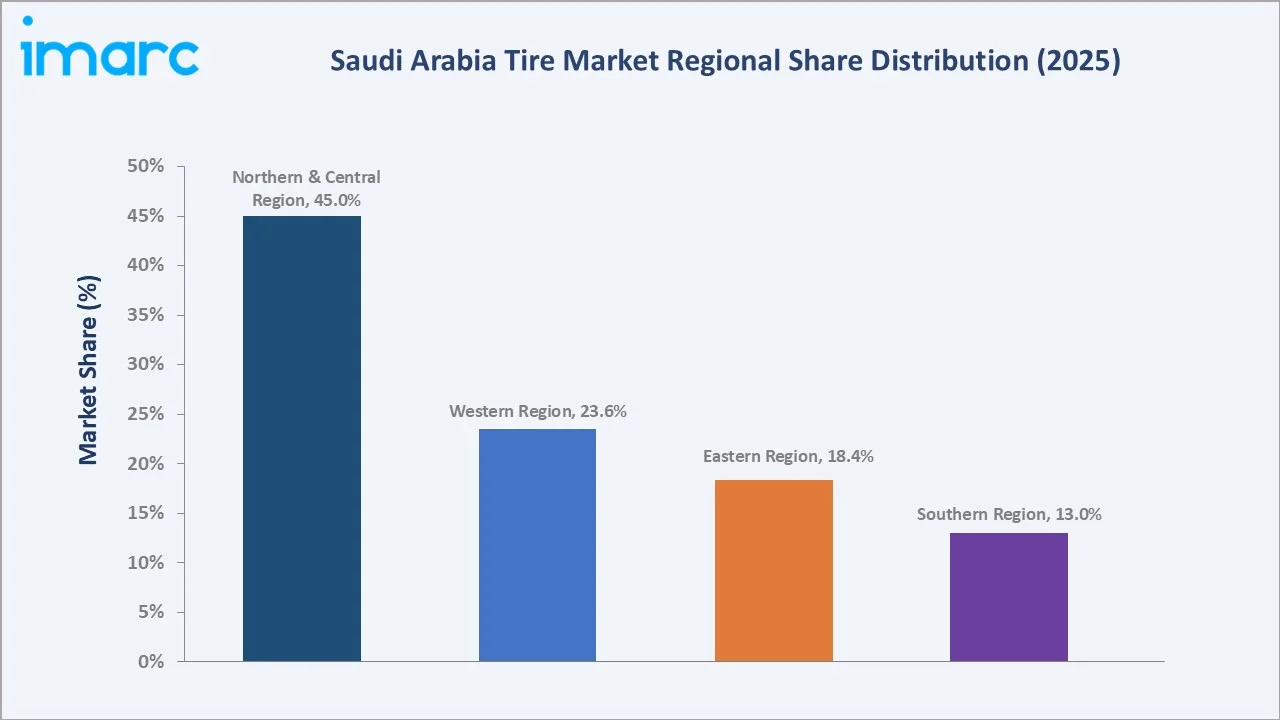

Dominant Region |

Northern & Central Region (45.0%, 2025) |

The market expanded from 21.85 Million Units in 2020 to 23.15 Million Units in 2025, anchored at 24.52 Million Units in 2030, and forecast to reach 25.68 Million Units by 2034. Growth is supported by Saudi Arabia's vehicle fleet expanding under Vision 2030 economic activity, rising tourism traffic, and construction vehicle demand from NEOM, The Line, Red Sea Global, and Qiddiya mega-projects.

To get more information on this market, Request Sample

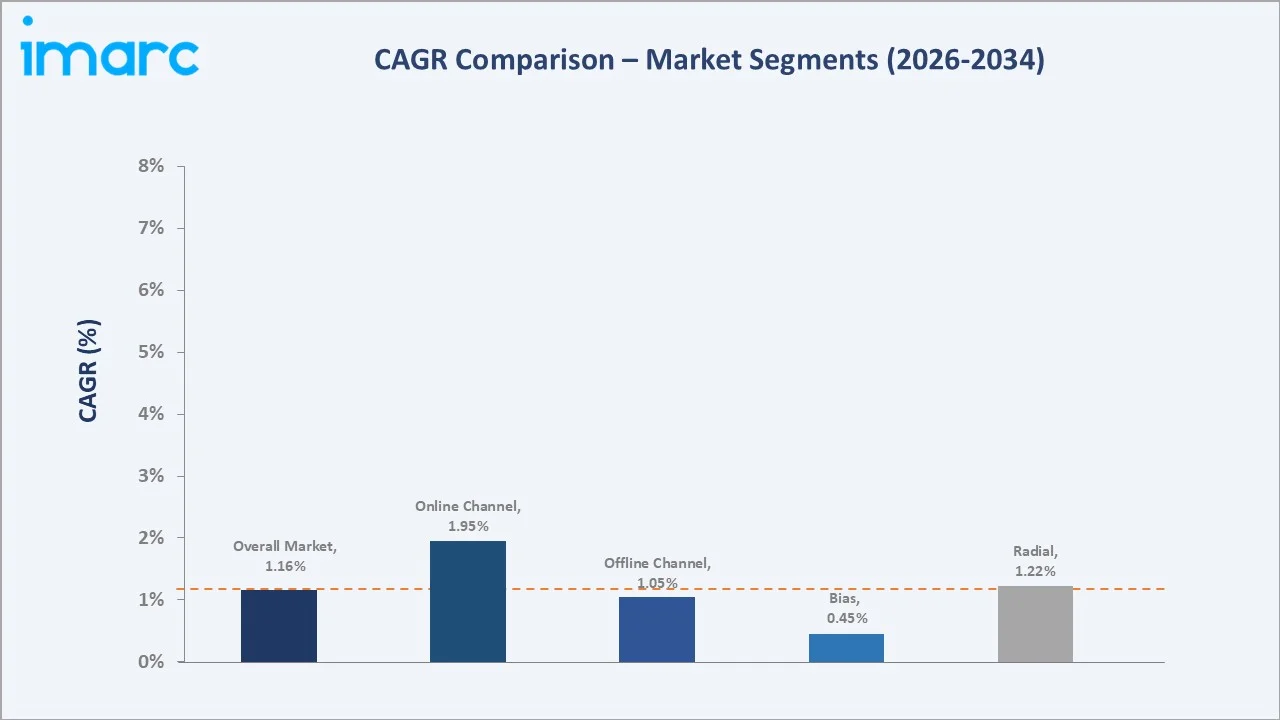

Online distribution grows fastest at ~1.95% CAGR (2026-2034), driven by e-commerce tire platforms expanding convenient tire-and-fit services. Radial tires maintain dominant growth at ~1.22% CAGR versus Bias at ~0.45%, reflecting the structural shift toward high-performance, heat-resistant radial construction for Saudi Arabia's high-speed highway and desert driving conditions.

Executive Summary

The Saudi Arabia tire market reached 23.15 Million Units in 2025, driven by one of the Middle East's largest vehicle fleets, extreme climate conditions that accelerate tire replacement cycles, and Vision 2030's sweeping infrastructure transformation. Saudi Arabia's record-breaking 1 million+ vehicle registrations in 2024 marked a historic milestone, creating structural demand across passenger car, SUV, and commercial vehicle tire segments. The market is projected to reach 25.68 Million Units by 2034 at a 1.16% CAGR, reflecting steady expansion driven by Vision 2030 economic activity, transportation infrastructure investment, EV fleet emergence, and growing tourism mobility.

Radial tires command 92.0% of the 2025 market, reflecting broad adoption across all vehicle categories due to their superior heat dissipation, reduced rolling resistance, and extended tread life - characteristics particularly valuable in Saudi Arabia's summer operating environment. Offline distribution channels retain 82.0% share, anchored by consumer preference for professional fitting services and established dealer networks. The Northern and Central Region dominates at 45.0%, anchored by Riyadh's vehicle concentration and industrial activity, while the Eastern Region benefits from Saudi Aramco's extensive industrial fleet operations.

Key Market Insights

|

Insight |

Data |

|

Largest Type |

Radial - 92.0% volume share (2025) |

|

Dominant Distribution Channel |

Offline - 82.0% share (2025) |

|

Dominant Region |

Northern & Central Region - 45.0% share (2025) |

Key Analytical Observations Supporting the Above Data:

- Radial tires at 92.0% share (2025) driven by heat resistance and longevity advantages: Saudi Arabia's road surface temperatures in summer create severe bias-ply tire degradation risks. Radial construction's steel belt system and flexible sidewalls dissipate heat more effectively, extending service life versus bias tires in Saudi conditions.

- Offline channels at 82.0% anchored by consumer demand for professional tire fitting: Saudi Arabia's tire retail market centers on specialty tire shops, automotive service centers, and hypermarket auto bays that offer mounting, balancing, alignment, and disposal services.

- Northern & central region is dominant with 45.0% share (2025): The region dominates due to the concentration of Riyadh and surrounding urban hubs, which host the highest vehicle density, industrial activity, and economic output in Saudi Arabia.

Saudi Arabia Tire Market Overview

Saudi Arabia's tire market encompasses all tire types sold for passenger vehicles, commercial vehicles, SUVs, motorcycles, and off-the-road equipment within the Kingdom. The market is predominantly import-driven, and Saudi Arabia has no established large-scale domestic tire manufacturing as of 2025, relying on global manufacturers to supply both OEM (original equipment manufacturer) vehicle assembly and the replacement aftermarket through licensed importers and regional distributors.

The market operates under Saudi Standards, Metrology and Quality Organization (SASO) regulatory standards, responsible for setting mandatory standards, quality systems, and conformity assessment procedures for goods and services. Macroeconomic influences include Saudi Arabia's Vision 2030 diversification, GDP growth in non-oil sectors, rising household incomes, and the Saudi government's infrastructure investment program, creating sustained commercial vehicle fleet expansion.

Market Dynamics

To evaluate market opportunities, Request Sample

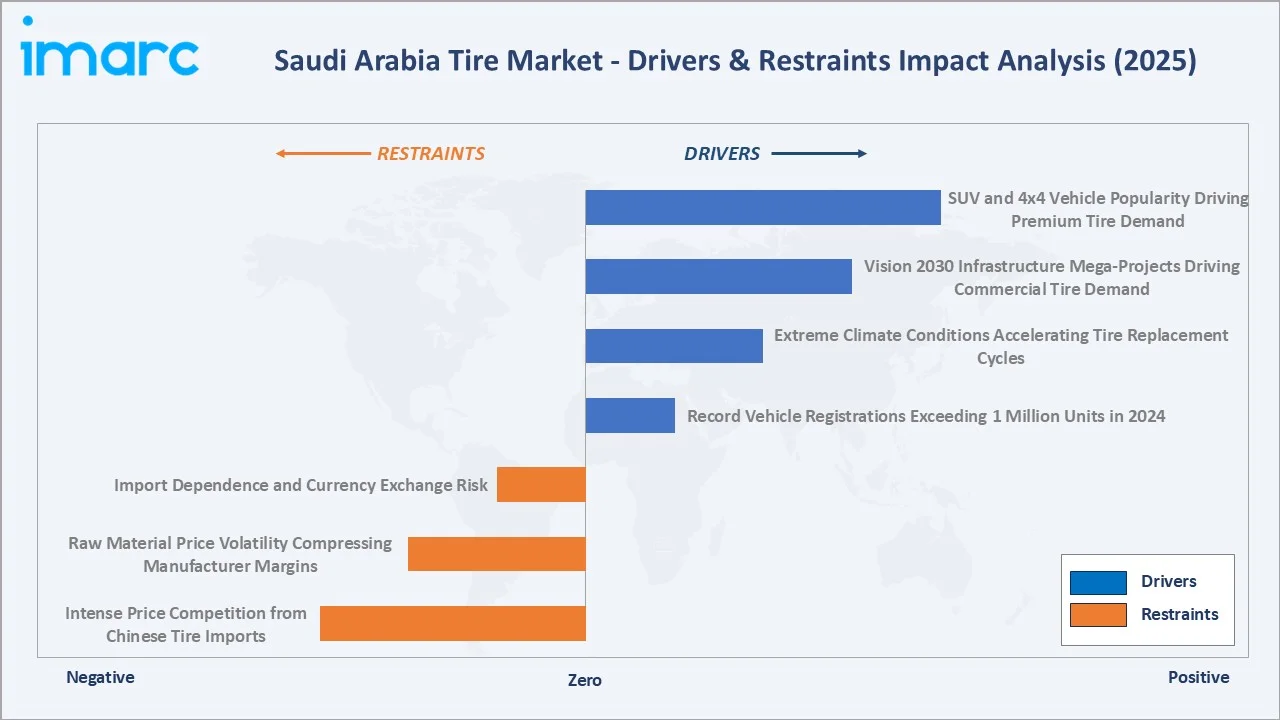

Market Drivers

- Record Vehicle Registrations: Saudi Arabia's vehicle registrations exceeded 1 million units for the first time in 2024, a historic milestone driven by Vision 2030's economic expansion, rising household incomes, growing female driver participation, and expanded automotive financing.

- Extreme Climate Conditions Accelerating Replacement Cycles: Saudi Arabia's summer temperatures and road surface temperatures create significantly accelerated tire degradation versus temperate climates.

- Vision 2030 Infrastructure Mega-Projects Driving Commercial Tire Demand: NEOM city construction, The Line's linear city project, Red Sea islands resort development, and Qiddiya entertainment city collectively require tens of thousands of construction vehicles, creating sustained OTR and commercial tire procurement.

- SUV and 4x4 Vehicle Popularity Driving Premium Tire Demand: Saudi consumers strongly prefer SUVs and pickup trucks, which collectively new vehicle sales. SUV tires command premium pricing versus standard passenger car tires, lifting average revenue per unit across the tire market. The growing popularity of desert off-roading as a recreational activity further amplifies premium all-terrain tire demand.

Market Restraints

- Import Dependence and Currency Exchange Risk: Saudi Arabia's near-total tire import dependency exposes the market to USD/SAR exchange rate fluctuations and international freight cost volatility.

- Raw Material Price Volatility Compressing Tire Manufacturer Margins: Natural rubber and synthetic rubber prices are subject to commodity cycle volatility. Carbon black prices, tied to oil feedstocks, add further input cost uncertainty. These raw material cycles periodically compress distributor margins and elevate consumer tire prices, temporarily dampening replacement demand in price-sensitive segments.

Market Opportunities

- Electric Vehicle Tire Specialization: Saudi Arabia's Vision 2030 includes EV adoption incentives and expanding charging infrastructure. In Saudi Arabia, in a high-growth scenario, EV adoption is projected to reach 14.8 million by 2050. Electric vehicles require specialized tires that command price premiums versus conventional tires.

- Domestic Tire Manufacturing Localization Under Vision 2030: Saudi Arabia's Vision 2030 industrial localization agenda creates incentives for foreign direct investment in domestic tire production. Joint ventures between global tire manufacturers and Saudi industrial companies could establish Saudi Arabia as a regional tire export hub serving GCC, East Africa, and South Asian markets.

Market Challenges

- Intense Price Competition from Chinese Tire Imports: Chinese tire brands are aggressively expanding in Saudi Arabia's budget and mid-segment through competitive pricing, typically 25-40% below equivalent Japanese and European brands. While quality perceptions have improved for Chinese brands among commercial vehicle operators, their pricing pressure compresses margins for premium brand distributors and challenges mid-tier Korean and Japanese brands competing on value.

- Limited Local Manufacturing Base Creating Supply Chain Fragility: Saudi Arabia's near-total import dependence creates supply chain vulnerability to geopolitical disruptions, shipping lane disruptions and port congestion.

Emerging Market Trends

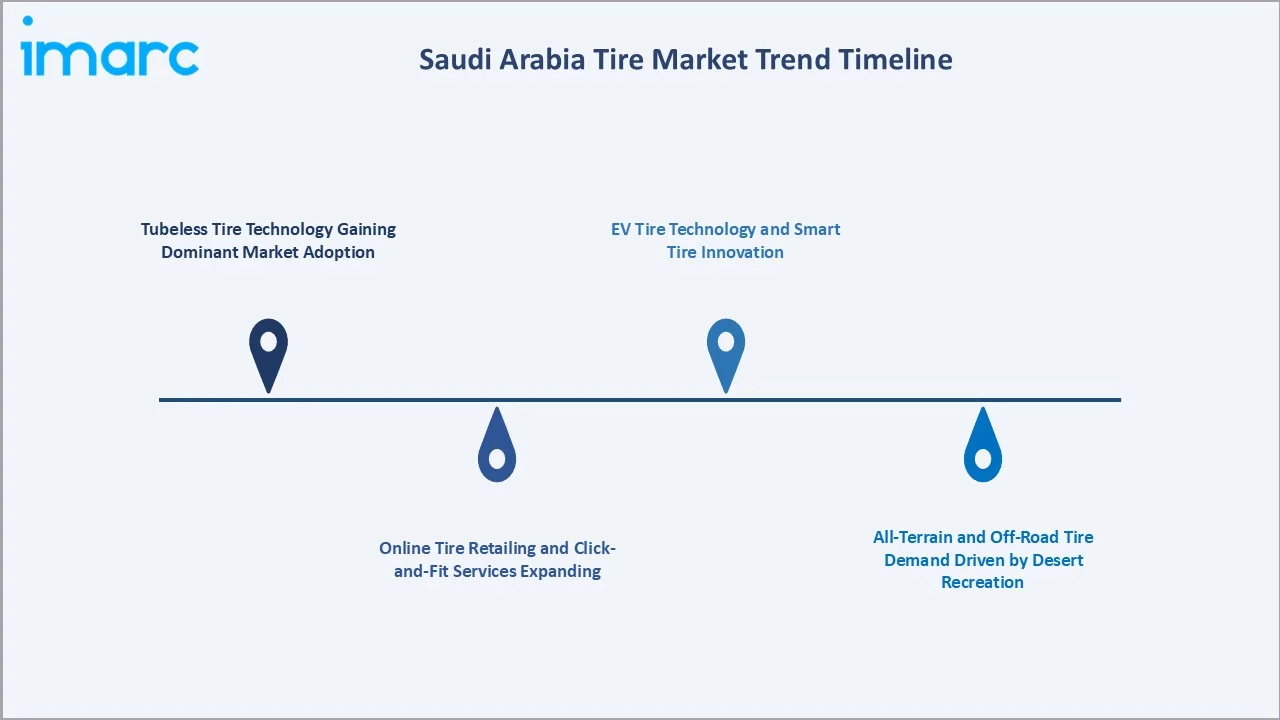

1. Tubeless Tire Technology Gaining Dominant Market Adoption

Tubeless tires are replacing tube-type alternatives across Saudi Arabia's passenger and commercial vehicle segments. Their slow air leakage profile significantly reduces sudden blowout risk at the 120-140 km/h highway speeds common on Saudi roads, while superior heat dissipation extends service life in 45°C+ temperatures.

2. Online Tire Retailing and Click-and-Fit Services Expanding

Saudi Arabia's tire e-commerce channel at 18.0% (2025) is growing as online platforms offer transparent pricing, home delivery, and affiliated workshop installation networks. Brand direct-to-consumer tire websites launched Saudi-specific portals, offering warranty-backed online purchase with authorized installer networks.

3. All-Terrain and Off-Road Tire Demand Driven by Desert Recreation

Saudi Arabia's growing off-road recreational culture, desert dune bashing, off-road overlanding, and 4x4 adventure activities are creating a distinct high-demand segment for all-terrain and mud-terrain tires. The Saudi off-road tire market is growing significantly above the overall market CAGR.

4. EV Tire Technology and Smart Tire Innovation

Saudi Arabia's Vision 2030 EV adoption push is stimulating demand for specialized electric vehicle tires. Smart tire technology, incorporating pressure sensors, temperature monitoring, and wear indicators connected to vehicle telematics systems, is expected to enter Saudi Arabia's fleet management market.

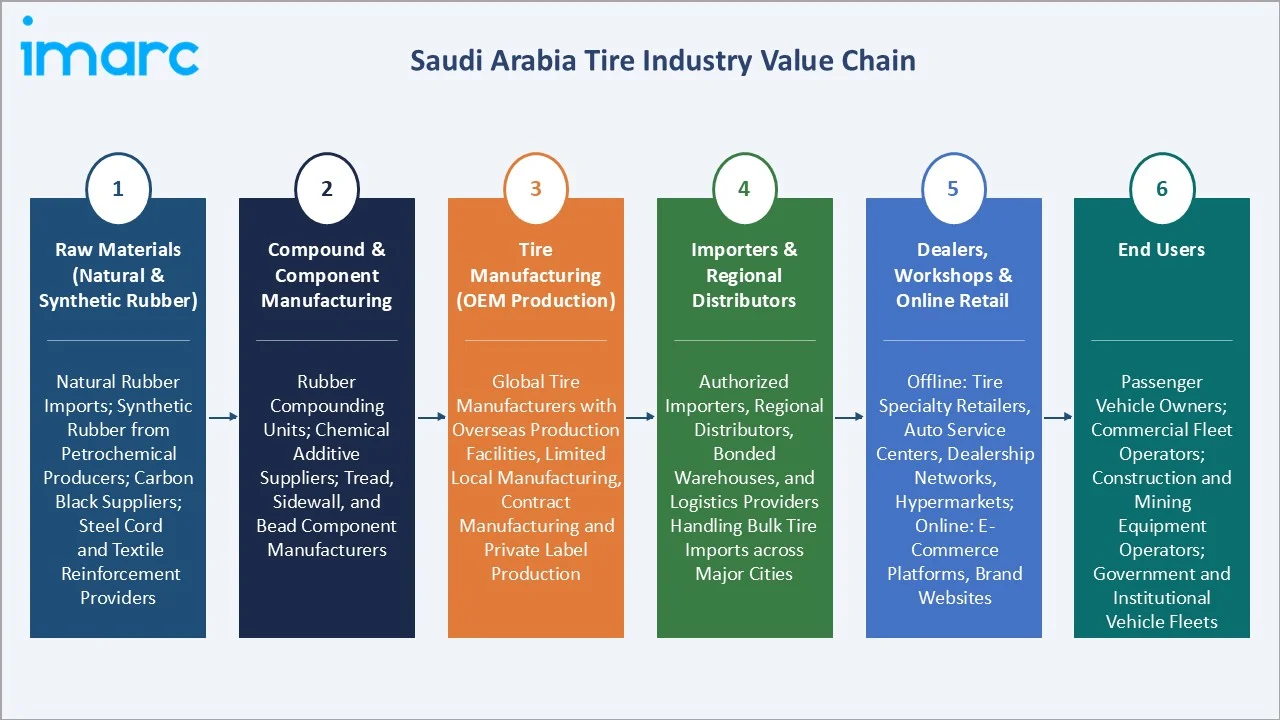

Industry Value Chain Analysis

Saudi Arabia's tire market value chain spans raw material sourcing from natural rubber-producing countries through global tire manufacturing operations, SASO regulatory compliance, multi-tier Saudi distribution networks, and end-consumer retail across offline dealer and online channels serving 23.15 Million Units of annual demand (2025).

|

Stage |

Key Participants |

|

Raw Materials (Natural & Synthetic Rubber) |

Natural rubber imports; synthetic rubber from petrochemical producers; carbon black suppliers; steel cord and textile reinforcement material providers |

|

Compound & Component Manufacturing |

Rubber compounding units; chemical additive suppliers; tread, sidewall, and bead component manufacturers |

|

Tire Manufacturing (OEM Production) |

Global tire manufacturers with overseas production facilities, limited local manufacturing, contract manufacturing and private label production |

|

Importers & Regional Distributors |

Authorized importers, regional distributors, bonded warehouses, and logistics providers handling bulk tire imports and inventory distribution across major cities |

|

Dealers, Workshops & Online Retail |

Offline: tire specialty retailers, auto service centers, dealership networks, hypermarkets with auto sections Online: e-commerce platforms, brand websites, digital marketplaces offering tire sales and installation booking |

|

End Users |

Passenger vehicle owners; commercial fleet operators (logistics, transport); construction and mining equipment operators; government and institutional vehicle fleets |

Saudi Arabia's tire distribution follows a two-tier model: global manufacturers sell to licensed Saudi importers/distributors, who in turn supply regional sub-distributors and retail tire shops. Importers earn 12-18% margins; retail tire shops earn 20-30% markup on tire unit pricing. The emergence of direct-to-consumer online channels is compressing traditional importer margins and creating pressure for supply chain restructuring.

Technology Landscape in the Saudi Arabia Tire Industry

Radial Tire Construction Technology

Radial tire construction, using steel cord belts running perpendicular to the direction of travel, dominates Saudi Arabia's market at 92.0% (2025) due to its superior performance in high-temperature environments. Modern radial tires incorporate multiple steel belt layers, silica-enhanced tread compounds for reduced rolling resistance in hot conditions, and optimized tread patterns for high-speed stability on Saudi Arabia's extensive highway network.

Smart Technology and Connected Monitoring

In December 2025, InDrive and AI Driver entered into a Memorandum of Understanding to initiate preparations for an autonomous ride-hailing pilot in Riyadh, Saudi Arabia. The project will operate on inDrive’s platform using WeRide’s technology, under the supervision of Saudi Arabia’s Transport General Authority (TGA). These advanced technologies further accelerating the market growth.

EV-Specific Tire Design and Acoustic Technology

Electric vehicle tires require specialized engineering to address three unique challenges: reinforced sidewall construction for battery weight support, low rolling resistance compounds for extended EV range, and acoustic foam technology to compensate for the absence of engine noise masking tire-road noise.

Market Segmentation Analysis

The report covers the following segments:

| Segment Category | Leading Segment | Market Share | Year |

|---|---|---|---|

| Type | Radial | 92.0% | 2025 |

| End-Use | Replacement | 61.0% | 2025 |

| Vehicle Type | Passenger Cars | 55.0% | 2025 |

| Size | Passenger Cars | 58.0% | 2025 |

| Distribution Channel | Offline | 82.0% | 2025 |

| Region | Northern and Central Region | 45.0% | 2025 |

By Type

Radial tires dominate at 92.0% market share (2025). Radial construction is universal across all vehicle segments in Saudi Arabia, passenger cars (100% radial), commercial trucks (95%+ radial), and SUVs (100% radial). Saudi Arabia's SASO tire standards effectively mandate radial construction for new vehicle tires through minimum performance requirements that bias-ply tires cannot consistently meet in the Kingdom's extreme climatic conditions.

To access detailed market analysis, Request Sample

Bias tires at 8.0% serve niche applications, including agricultural machinery, some construction equipment, and small motorcycle tires where radial construction is not technically required or economically justified. The bias tire segment declines at ~0.45% CAGR (2026-2034) as equipment modernization across agriculture and construction progressively adopts radial alternatives.

By Distribution Channel

Offline channels lead at 82.0% market share (2025). Saudi Arabia's offline tire retail ecosystem comprises specialty tire shops, integrated automotive service centers, hypermarket auto bays, and OEM dealership service departments. Professional mounting and balancing services, on-the-spot tire advice, and immediate availability reinforce offline dominance, particularly for commercial fleet operators with large-diameter truck tires requiring specialist equipment.

Online channels at 18.0% are growing at ~1.95% CAGR, the fastest segment through 2034. Saudi Arabia's rapid e-commerce adoption is driving tire digital commerce growth. Click-and-fit services, where consumers purchase tires online and schedule workshop installation, are normalizing online tire purchasing for urban consumers.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers & Characteristics |

|

Northern & Central Region |

45.0% |

Highest vehicle density and population concentration centered around Riyadh; strong industrial and commercial activity; major logistics hubs and extensive highway networks driving high tire replacement demand |

|

Western Region |

23.6% |

High tourism and religious travel are increasing vehicle usage; strong logistics demand around major port cities; growth in hospitality and transport fleets supporting tire consumption |

|

Eastern Region |

18.4% |

Presence of oil, gas, and petrochemical industries generating strong demand for commercial and industrial vehicle tires; high freight movement and supply chain logistics activity |

|

Southern Region |

13.0% |

Emerging infrastructure development and regional connectivity projects; increasing domestic tourism and cross-border logistics supporting gradual growth in tire demand |

The Northern and central region's 45.0% dominance reflects Riyadh's status as Saudi Arabia's economic capital, home to the highest vehicle registration density, largest government fleet procurement authority, and the greatest concentration of mega-project construction activity. Riyadh's population growth creates compounding passenger vehicle fleet expansion and replacement tire demand that sustains the region's outsized market share.

The Western region's 23.6% share is anchored by Jeddah's role as Saudi Arabia's largest commercial port. Makkah and Madinah's year-round Hajj and Umrah pilgrimage traffic creates sustained transportation vehicle demand, generating above-average tire replacement cycles. The Eastern region's 18.4% share reflects Saudi Aramco's industrial vehicle fleet and petrochemical complex logistics, creating intensive commercial tire demand in the industrial corridor.

Competitive Landscape

Saudi Arabia's tire market is moderately concentrated among premium international brands at the top, with intensifying competition from Korean mid-tier brands and expanding Chinese budget brands in the value segments. Michelin, Bridgestone, and Continental collectively hold an estimated 35-40% of Saudi Arabia's premium passenger and commercial tire market value (2025).

|

Company Name |

Brand / Product Line |

Market Position |

Core Strength |

|

Michelin |

PILOT SPORT A/S 4, PRIMACY XC, ENERGY SAVER A/S, PILOT SPORT S 5, 4X4 O/R XZL, ENERGY SAVER + |

Market Leader |

Global innovation leader; Michelin's presence in the Kingdom of Saudi Arabia through its representative office and local partners for more than 10 years. |

|

Bridgestone |

Turanza, Potenza, Dueler, Duravis |

Market Leader |

One of the world's largest tire manufacturers by revenue, operating in the Middle East and Africa |

|

Continental AG |

PremiumContact, EcoContact, SportContact, CrossContact, and UltraContact |

Strong Challenger |

Operates in Saudi Arabia with a focus on tires and industrial products. |

|

The Goodyear Tire & Rubber Company |

Eagle F1, Assurance, Wrangler |

Strong Challenger |

Goodyear Tire & Rubber Company operates in Saudi Arabia through official distributor Al Rashed Tires Co. |

|

Pirelli & C. S.p.A. |

P Zero, Cinturato, Scorpion |

Established Player |

In 2023, the Public Investment Fund (PIF) and Pirelli signed a joint venture (JV) agreement to build a tire manufacturing facility in Saudi Arabia. |

Saudi Arabia's tire competitive landscape is bifurcated: the premium OEM supply segment is dominated by Michelin, Bridgestone, Continental, and Goodyear through long-term supply agreements, while the replacement aftermarket is more fragmented with Korean and Chinese brands actively competing on price-performance value propositions targeting Saudi Arabia's rapidly expanding fleet of mid-range vehicles.

Key Company Profiles

Michelin

Michelin is one of Saudi Arabia's leading tire brands by value market share, commanding premium positioning across passenger car, SUV, and commercial vehicle segments. Michelin's presence in the Kingdom of Saudi Arabia through its representative office and local partners for more than 10 years.

- Product Portfolio: PILOT SPORT A/S 4, PRIMACY XC, ENERGY SAVER A/S, PRIMACY ALL SEASON, PILOT SPORT S 5, 4X4 O/R XZL, ENERGY SAVER +.

- Recent Developments: In July 2022, Michelin launched two more ranges of products for the Middle East and North African markets. MICHELIN Pilot Sport 5 and MICHELIN Pilot Sport EV will cater to a wide range of automotive and super car enthusiasts.

- Strategic Focus: Premium brand positioning anchored by performance tire innovation.

Bridgestone

Bridgestone is one of the world's largest tire manufacturers by revenue and maintains the highest combined volume share in Saudi Arabia across passenger, SUV, and commercial categories.

- Product Portfolio: Turanza, Potenza, Dueler, Duravis.

- Recent Developments: In March 2026, Bridgestone introduced its first motorhome-specific tire, the Duravis Camper All Season. Designed for year-round use, the tire combines all-season performance with enhanced load capacity and durability to meet the demands of motorhome applications.

- Strategic Focus: Commercial fleet tire management service platforms value-tier entry point for price-sensitive commercial segments.

Pirelli & C. S.p.A.

Pirelli occupies Saudi Arabia's ultra-premium tire niche, supplying exclusive OEM tire specifications to luxury and supercar brands with significant Saudi market presence.

- Product Portfolio: P Zero, Cinturato, Scorpion

- Recent Developments: In October 2023, the Public Investment Fund (PIF) and Pirelli signed a joint venture (JV) agreement to build a tire manufacturing facility in Saudi Arabia.

- Strategic Focus: Ultra-premium brand exclusivity through limited distribution; exclusive OEM tire supply to luxury vehicle brands with strong Saudi market positions.

Market Concentration Analysis

Saudi Arabia's tire market exhibits moderate concentration at the premium branded level and significant fragmentation in the mid-to-budget segments. Michelin, Bridgestone, Continental, and Goodyear collectively hold an estimated 35-42% of Saudi Arabia's passenger and light commercial tire market by value (2025), with their combined volume share lower due to premium pricing versus mid-tier competitors. No single brand exceeds 15% total market volume share in Saudi Arabia's competitive tire environment.

The market's structural fragmentation below the premium tier reflects Saudi Arabia's diverse consumer base - from price-sensitive expatriate workers seeking budget Asian brands to ultra-high-net-worth Saudi consumers purchasing exclusive performance tires. Korean brands hold collectively 20-25% of Saudi Arabia's mid-tier replacement market volume, while Chinese brands have grown to approximately 15-20% of the budget passenger car tire market.

Consolidation trends are limited at the importer level, with the large Saudi automotive conglomerates expanding their multi-brand tire distribution portfolios. Global tire manufacturers are increasingly pursuing direct Saudi distribution agreements to reduce importer margin layers, a trend that is compressing traditional distributor margins and reshaping the distribution landscape.

Investment & Growth Opportunities

Fastest Growing Segments

Online distribution channel (~1.95% CAGR), EV-specific tire segment (~25-30% CAGR from small base), ultra-high-performance tire segment (~3-5% CAGR), all-terrain and off-road tires (~4-5% CAGR), and commercial tire demand from Vision 2030 construction projects (~3-4% CAGR) represent Saudi Arabia's highest-growth investment vectors through 2034. EV tire specialization represents the highest per-unit revenue opportunity.

Emerging Market Opportunities

Saudi Arabia's financing for industrial localization creates a viable pathway for global tire manufacturers to establish Saudi-based tire production. A mid-scale tire manufacturing plant serving Saudi Arabia and the 6-nation GCC market would benefit from Vision 2030 industrial zone infrastructure, competitive energy costs, and government procurement preference for locally manufactured goods under the Saudi content program.

Investment Themes

- EV tire portfolio development: Saudi Arabia's government EV incentive program and Saudi fleet electrification commitment create first-mover advantage for tire brands establishing EV-specific Saudi distribution and technical expertise ahead of 2028-2030 EV fleet scaling.

- Digital tire retail platform investment: Saudi Arabia's e-commerce CAGR creates a compelling opportunity for online tire platforms integrating price comparison, purchase, and workshop fitting appointment booking.

- Commercial fleet tire management services: Saudi Arabia's expanding logistics sector creates demand for fleet tire management subscription services combining tire monitoring sensors, predictive replacement analytics, and performance dashboards.

Future Market Outlook (2026-2034)

The Saudi Arabia tire market is projected to grow from 23.15 Million Units in 2025 to 25.68 Million Units by 2034, at a 1.16% CAGR, reflecting steady, structurally supported growth in one of the Middle East's most significant automotive markets. Saudi Arabia's 24.52 Million Unit market in 2030 will be shaped by Vision 2030's economic transformation, with commercial vehicle tire demand from mega-project construction and logistics fleet expansion serving as the primary volume growth drivers above baseline passenger car replacement demand.

Three structural forces anchor Saudi Arabia's tire market growth trajectory through 2034 with high certainty: Vision 2030's irreversible infrastructure transformation creating permanent commercial vehicle fleet expansion; Saudi Arabia's demographic dividend sustaining passenger vehicle ownership growth; and the Kingdom's climate reality that extreme heat will continue to compress tire replacement cycles to 2-3 years versus 4-6 years in temperate markets, creating double the replacement demand per vehicle in the fleet.

Research Methodology

Primary Research

Primary research comprised structured interviews with 70+ industry stakeholders (2025), including regional tire distributors and importers, tire retail chain managers from Riyadh and Jeddah, commercial fleet procurement managers from Saudi logistics, transport division, and major Saudi logistics operators, SASO regulatory officials for tire standards, and import data specialists.

Secondary Research

Secondary research encompassed Saudi Customs Authority tire import statistics 2024-2025, SASO tire regulation database, General Authority for Statistics (GaStat) vehicle registration data 2024, Saudi Vision 2030 infrastructure project investment documentation, Saudi logistics market reports, Saudi e-commerce market data, and company annual reports for major tire brands operating in Saudi Arabia. Saudi Arabia Monetary Authority (SAMA) automotive financing statistics and CITC (Communications and Information Technology Commission) e-commerce market data were key secondary inputs. Over 120 secondary sources were reviewed.

Forecasting Models

Market volume forecasts were developed using bottom-up vehicle fleet size x average tire replacement frequency models, segmented by vehicle type (passenger car, SUV, commercial, construction) and type (radial, bias), validated against Saudi Customs Authority import data and SASO registration statistics. Key inputs include GaStat vehicle fleet growth projections, Vision 2030 mega-project construction vehicle estimates, Saudi climate-adjusted tire replacement frequency coefficients, EV fleet adoption S-curve modeling, and online channel adoption projections from Saudi e-commerce growth rates.

Saudi Arabia Tire Market Report Coverage

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million Units |

| Scopr of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Types Covered | Radial, Bias |

| End-Uses Covered | OEM, Replacement |

| Vehicle Types Covered | Passenger Cars, Light Commercial Vehicles, Medium and Heavy Commercial Vehicles, Two Wheelers, Off-The-Road (OTR) |

| Distribution Channels Covered | Offline, Online |

| Region Covered | Northern and Central Region, Western Region, Eastern Region, Southern Region |

| Companies Covered | Michelin, Bridgestone, Continental AG, The Goodyear Tire & Rubber Company, Pirelli & C. S.p.A., etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the Saudi Arabia Tire Market Report

The Saudi Arabia tire market reached 23.15 Million Units in 2025, driven by record vehicle registrations exceeding 1 Million units in 2024, Vision 2030 mega-project commercial vehicle demand, and climate-driven replacement cycles.

The Saudi Arabia tire market is projected to grow at a CAGR of 1.16% during 2026-2034, reaching 25.68 Million Units by 2034, supported by Vision 2030 economic expansion, EV fleet emergence, and sustained replacement demand.

Radial tires lead at 92.0% volume share (2025), driven by their superior heat dissipation, fuel efficiency advantages, and extended tread life, critical performance characteristics for Saudi Arabia's summer operating environment.

Offline channels hold the largest share at 82.0% (2025), anchored by consumer preference for professional mounting and balancing services, in-person product inspection, and established dealer networks across Saudi Arabia's major cities.

Online channels grow fastest at ~1.95% CAGR (2026-2034), driven by click-and-fit service models, tire category expansion, and Saudi Arabia's e-commerce growth.

The northern and central region leads with 45.0% market share (2025), anchored by Riyadh's highest vehicle registration density, mega-project construction activity, and government fleet procurement concentration.

Leading companies include Michelin, Bridgestone, Continental AG, The Goodyear Tire & Rubber Company, Pirelli & C. S.p.A., among others.

Vision 2030 creates mega-project construction vehicle demand (NEOM, Red Sea Global, Qiddiya), logistics fleet expansion, tourist arrivals, and EV adoption incentives, driving specialized tire demand.

Saudi Arabia's tire market is projected to reach approximately 24.52 Million Units by 2030, supported by EV fleet emergence, NEOM and mega-project peak construction activity, and high online channel share.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)