Secure Web Gateway Market Size, Share, Trends and Forecast by Component, Deployment Type, Organization Size, Vertical, and Region, 2026-2034

Secure Web Gateway Market Size, Share, Trends & Forecast (2026-2034)

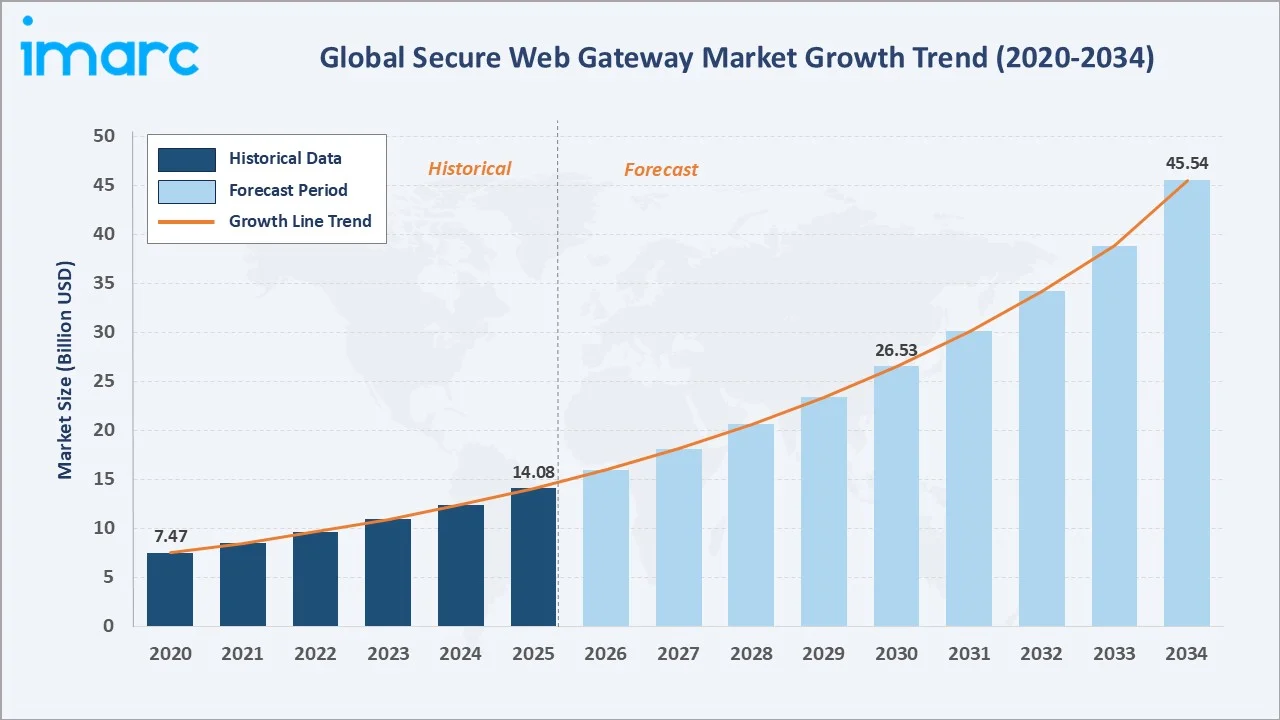

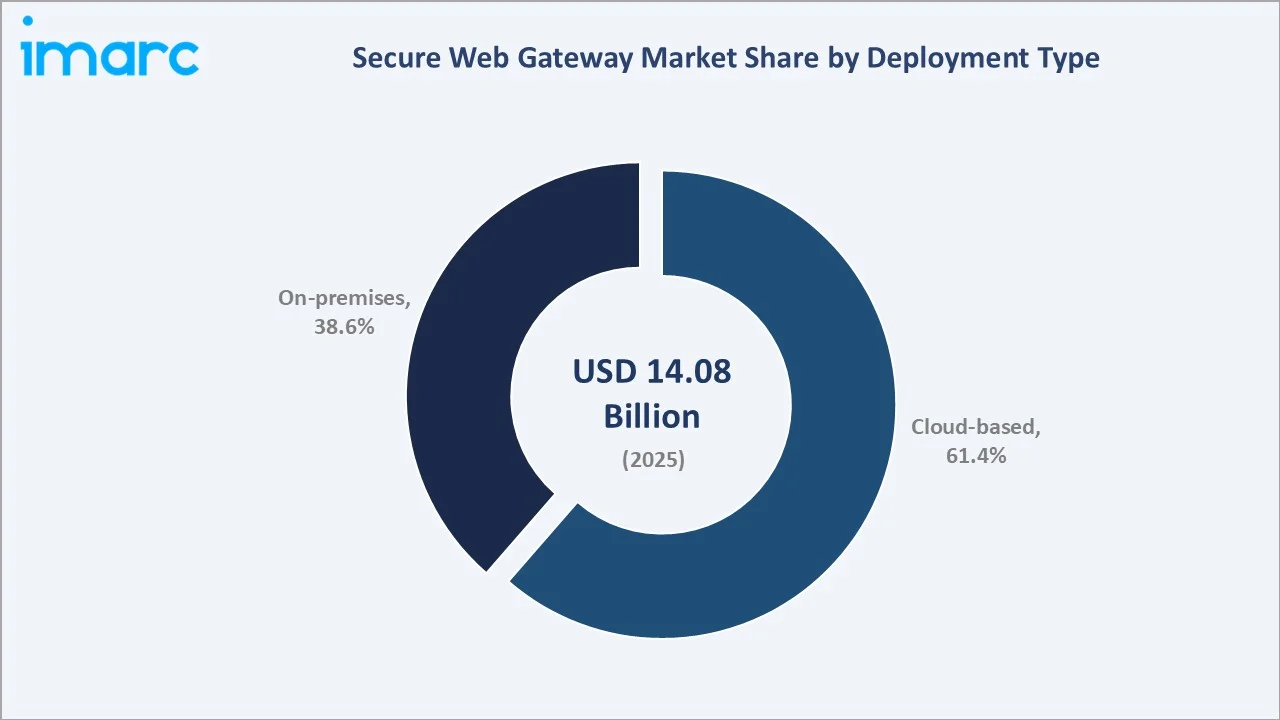

The secure web gateway market was valued at USD 14.08 Billion in 2025 and is projected to reach USD 45.54 Billion by 2034, exhibiting a CAGR of 13.52% during 2026-2034. Escalating frequency of cyberattacks, accelerating enterprise cloud adoption, and the rapid rise of remote and hybrid work models are the primary forces driving the market growth.

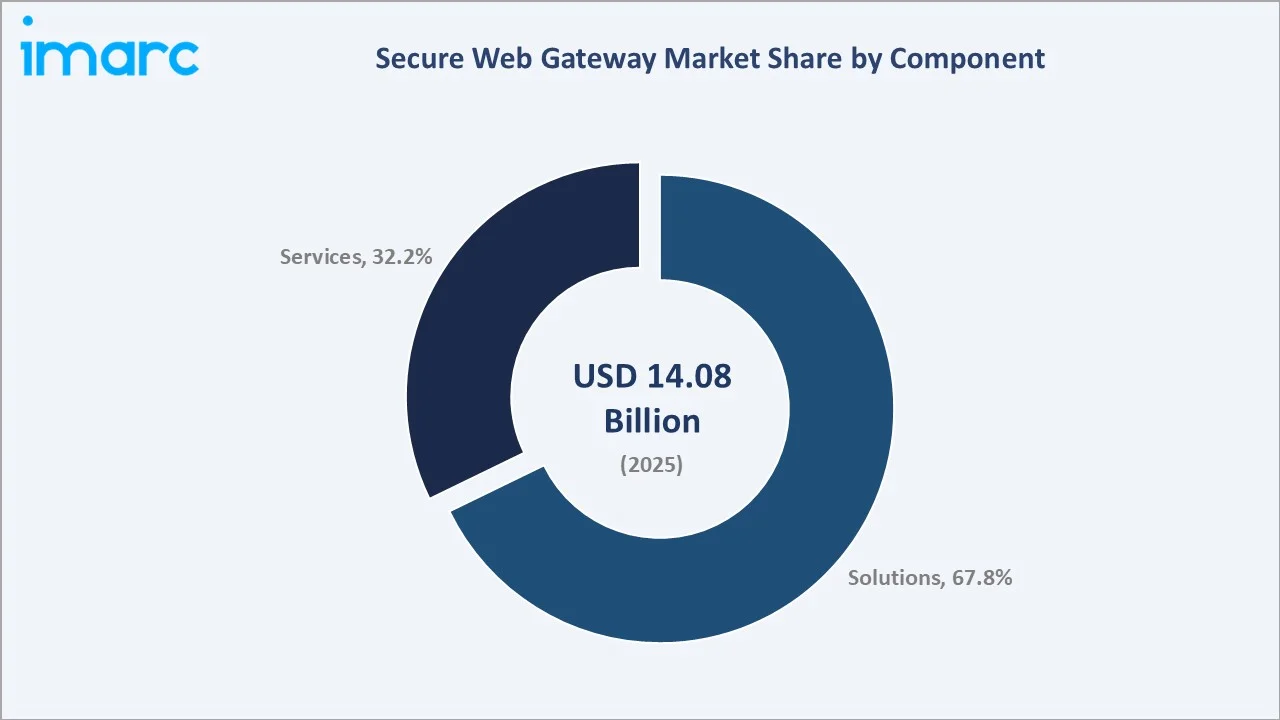

Solutions dominate the component segment at 67.8%, cloud-based leads the deployment type at 61.4%, and North America commands a 36.9% regional share.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 14.08 Billion |

|

Forecast Market Size (2034) |

USD 45.54 Billion |

|

CAGR (2026-2034) |

13.52% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

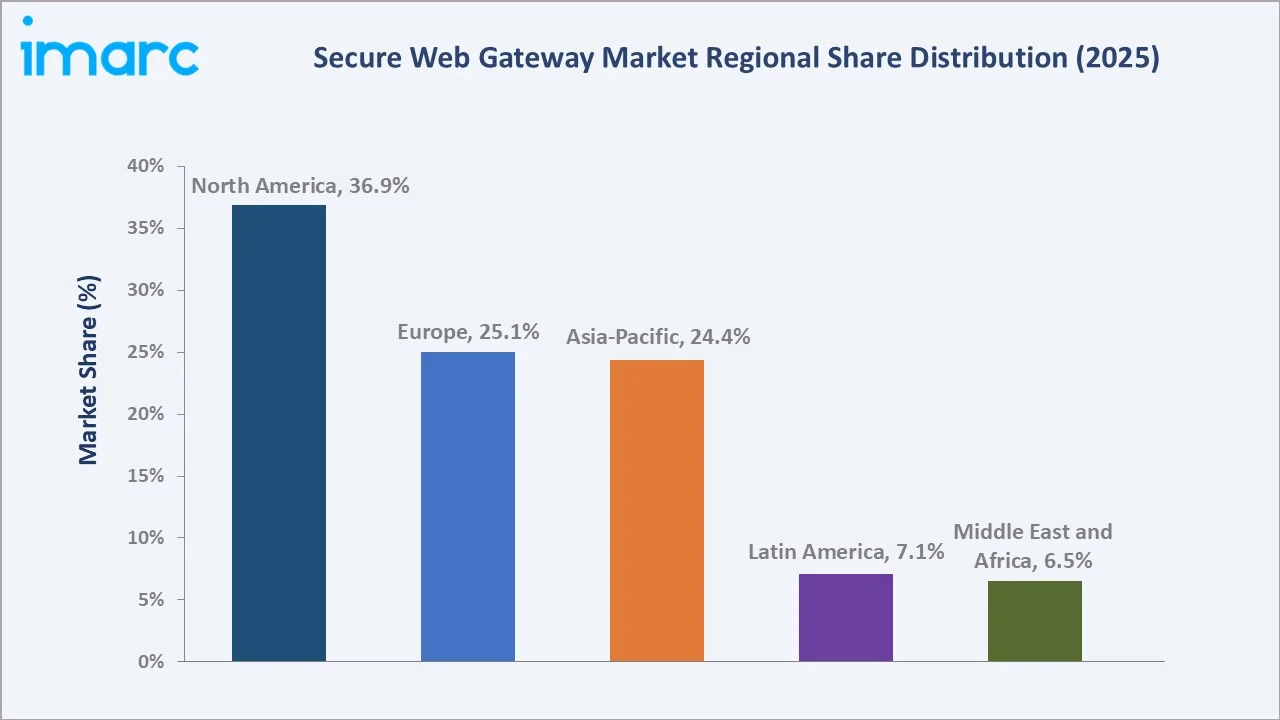

North America (36.9%, 2025) |

|

Second Largest Region |

Europe (25.1%, 2025) |

|

Leading Component |

Solutions (67.8%, 2025) |

|

Leading Deployment Type |

Cloud-based (61.4%, 2025) |

The secure web gateway market expanded from USD 7.47 Billion in 2020 to USD 14.08 Billion in 2025, reflecting rapid adoption of cloud-delivered security controls and widening threat surfaces driven by digital transformation. Anchored at USD 26.53 Billion in 2030, the forecast to USD 45.54 Billion by 2034 is supported by accelerating zero-trust security adoption, growing remote and hybrid work environments, and stricter regulatory requirements for data protection and web security across enterprises.

To get more information on this market, Request Sample

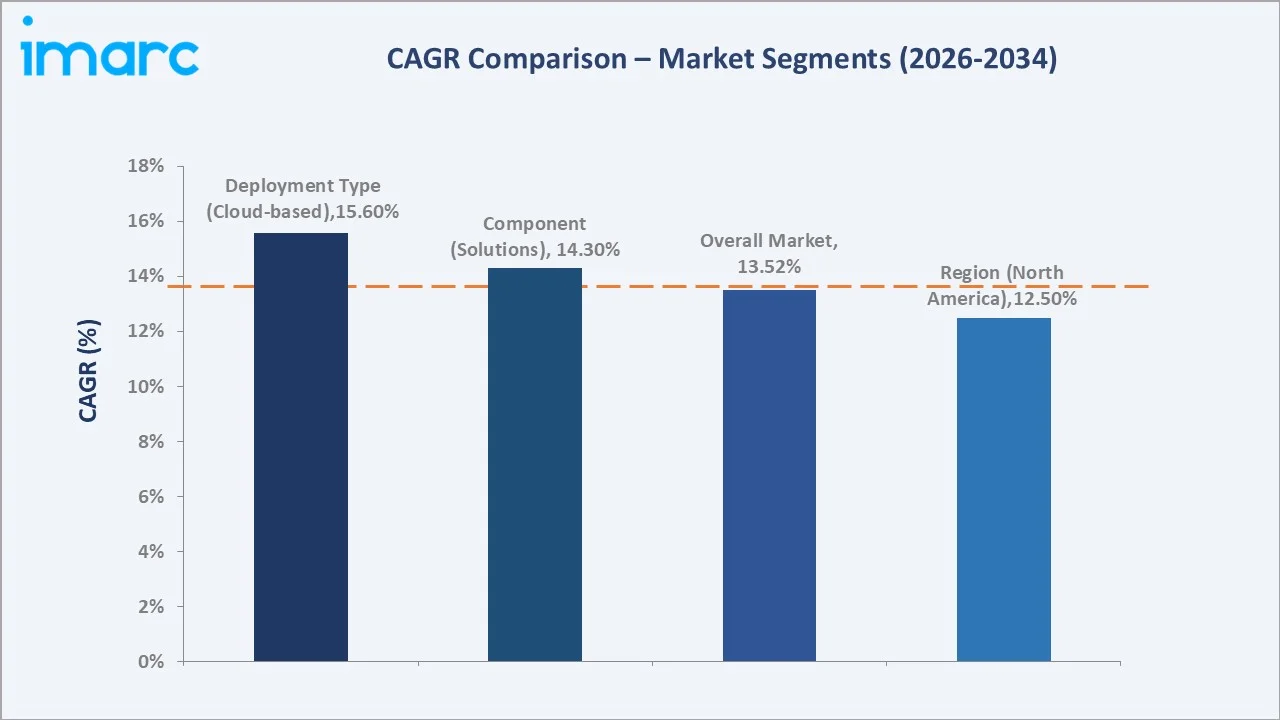

CAGR trajectories across component and deployment type sub-segments indicate cloud-based and solutions expanding faster than the overall 13.52% market CAGR, driven by enterprise demand for scalable, subscription-based security architectures that reduce capital expenditure while improving coverage and update cycles.

Executive Summary

The secure web gateway market is on a robust growth trajectory, expanding from USD 7.47 Billion in 2020 to USD 45.54 Billion by 2034 at a CAGR of 13.52%. The market has undergone structural transformation from premise-hosted proxy appliances to cloud-native, API-driven platforms embedded within unified SASE and zero-trust security architectures. This shift is driven by near-universal SaaS adoption, proliferation of unmanaged devices, and the need to enforce consistent web access policies across globally distributed workforces.

Solutions account for 67.8% of the component segment, supported by high enterprise investment in URL filtering, content inspection, advanced threat protection, and data loss prevention. On the basis of deployment type, cloud-based leads at 61.4%, driven by scalability, ease of deployment, and growing adoption of cloud-first security architectures. North America dominates at 36.9%, fueled by large enterprise adoption, regulatory mandates, and high concentration of solution providers.

Key Market Insights

|

Insight |

Data |

|

Leading Component |

Solutions – 67.8% share (2025) |

|

Second Largest Component |

Services – 32.2% share (2025) |

|

Leading Deployment Type |

Cloud-based – 61.4% share (2025) |

|

Second Largest Deployment Type |

On-premises – 38.6% share (2025) |

|

Leading Region |

North America – 36.9% share (2025) |

|

Second Largest Region |

Europe – 25.1% share (2025) |

|

Top Companies |

Zscaler, Inc., Cisco Systems, Inc., Palo Alto Networks, Broadcom, Forcepoint |

Key Analytical Observations Expanding On The Data Above:

- Solutions dominance at 67.8% reflects strong enterprise investment in URL filtering, malware sandboxing, and application control bundled within integrated secure web gateway platforms, enabling comprehensive web security without requiring multiple point products.

- Services at 32.2% are expanding as organizations increasingly outsource secure web gateway configuration, monitoring, and incident response to managed security service providers, reducing the in-house security operations burden while accelerating time to protection.

- Cloud-based at 61.4% is supported by the widespread shift to SaaS-first infrastructure, elastic scaling requirements, and native integration with identity providers, SD-WAN, and CASB platforms within converged SASE architectures.

- On-premises share at 38.6% remains relevant for highly regulated verticals including banking, defense, and healthcare, where data residency requirements, latency sensitivity, and internal compliance mandates constrain full migration to cloud-delivered security.

- North America leadership at 36.9% dominates the regional landscape, anchored by a mature cybersecurity ecosystem in the United States, large enterprise and government spending on web security, and early SASE adoption across the financial services, technology, and government sectors. As per IMARC Group, the United States cybersecurity market size reached USD 91.6 Billion in 2025.

Secure Web Gateway Market Overview

A secure web gateway is a network security solution that monitors, filters, and controls outbound web traffic originating from enterprise users, preventing access to malicious websites, enforcing acceptable use policies, inspecting encrypted traffic via SSL/TLS decryption, and protecting against data exfiltration and advanced web-borne threats.

The ecosystem integrates threat intelligence providers, secure web gateway technology developers, professional services and systems integrators, managed security service providers, enterprise IT and security operations teams, regulatory compliance functions, and end-user access channels spanning managed devices, BYOD environments, and remote work endpoints. Macroeconomic drivers, including accelerating digital transformation investment, growing geopolitical cyber threat landscapes, and expanding regulatory requirements for data protection, are collectively reinforcing demand across all market segments.

Market Dynamics

To evaluate market opportunities, Request Sample

Market Drivers

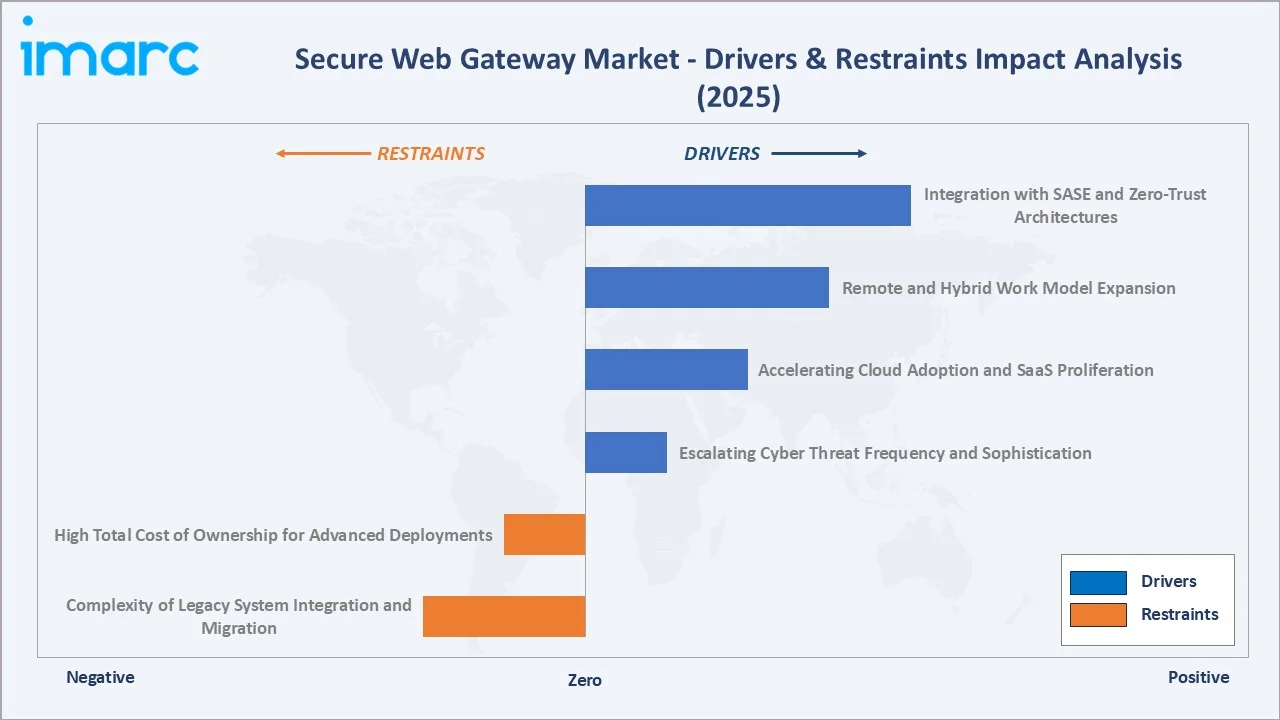

- Escalating Cyber Threat Frequency and Sophistication: Rising volumes of ransomware, phishing, zero-day exploits, and supply chain attacks targeting web traffic are compelling organizations across every sector to invest in enterprise-grade secure web gateway solutions equipped with real-time threat intelligence, behavioral analytics, and AI-driven anomaly detection to intercept threats before they reach end-user devices. Over two-fifths of UK companies experienced a cyber breach or attack in 2025/26, based on a government report released in April 2026.

- Accelerating Cloud Adoption and SaaS Proliferation: The broad migration of enterprise workloads to cloud infrastructure and near-universal adoption of SaaS applications have expanded the web attack surface beyond traditional network perimeters, necessitating cloud-delivered secure web gateway solutions capable of enforcing consistent policies across on-premises, cloud, and edge access environments regardless of user location or device type.

- Remote and Hybrid Work Model Expansion: The structural normalization of distributed work environments has increased the volume and diversity of internet-bound traffic from unmanaged networks and personal devices, creating enforcement gaps in legacy proxy architectures and driving adoption of cloud-native secure web gateway platforms that apply zero-trust access controls at the point of user-to-internet connection without requiring traffic backhauling.

- Integration with SASE and Zero-Trust Architectures: Enterprise adoption of SASE frameworks is converging multiple security functions onto unified cloud-delivered platforms, simplifying policy management, reducing operational complexity, and enabling consistent security enforcement across diverse access scenarios from a single control plane.

Market Restraints

- High Total Cost of Ownership for Advanced Deployments: Enterprise-grade secure web gateway implementations involving SSL inspection at scale, advanced threat sandboxing, behavioral DLP, and integration with SIEM and identity management platforms require significant investment in licensing, professional services, and ongoing management, creating barriers for mid-market organizations and public sector entities operating under constrained security budgets.

- Complexity of Legacy System Integration and Migration: Many large enterprises operate hybrid environments combining legacy on-premises proxy infrastructure with newer cloud-delivered security layers, creating integration complexity, policy inconsistencies, and latency challenges during multi-year migration programs that can delay adoption of modern secure web gateway architectures.

Market Opportunities

- AI and ML-Enhanced Threat Detection: Integration of generative AI and advanced ML models into secure web gateway platforms is enabling real-time detection of zero-day threats, polymorphic malware, and sophisticated social engineering attacks that evade conventional signature-based detection, creating differentiation opportunities for solution providers investing in AI-native security architectures.

- Expansion into Small and Medium Enterprise Segments: Growing awareness of cybersecurity risks among smaller businesses, combined with subscription-based, low-overhead cloud secure web gateway solutions, is creating a substantial underserved market that represents a significant growth runway for vendors offering simplified deployment and managed service options.

Market Challenges

- Privacy and Regulatory Compliance Complexity: Enterprise deployment of SSL/TLS traffic inspection introduces legal and regulatory complexity related to user privacy, employee monitoring obligations, and jurisdiction-specific data protection laws including GDPR in Europe and evolving state-level privacy frameworks in the United States, requiring policy frameworks that can delay deployment timelines.

- Bandwidth and Latency Impact on User Experience: Routing all web traffic through cloud secure web gateway infrastructure introduces latency overhead that can degrade application performance for latency-sensitive workloads including video conferencing and real-time collaboration tools, requiring continuous optimization of traffic steering and points of presence coverage to maintain acceptable user experience at scale.

Emerging Market Trends

1. Convergence of Secure Web Gateway with SASE and SSE Platforms

Enterprise security architecture is undergoing fundamental consolidation as organizations retire point-product proxy solutions in favor of unified SSE platforms that combine multiple security functions under a single cloud-delivered control plane. This convergence reduces vendor sprawl, simplifies policy administration, and enables consistent policy enforcement for users accessing corporate and internet resources from any location or device type.

2. AI-Driven Autonomous Threat Detection and Response

Vendors are embedding generative AI and large language models into web security pipelines to automate detection, triage, and response to web-borne threats at machine speed. AI models trained on real-time global threat intelligence feeds enable identification of novel phishing campaigns, obfuscated malware, and credential theft attempts that evade conventional detection engines.

3. Remote Browser Isolation Integration

Remote browser isolation is being embedded directly into cloud secure web gateway platforms as a complementary layer that executes web content in isolated cloud-based containers, preventing malicious code from reaching user endpoints even on zero-day or previously unknown malicious websites. Risk-adaptive rendering applies isolation selectively based on site category, user risk score, and content classification, balancing security effectiveness with performance overhead.

4. Data Loss Prevention Integration and Web Traffic Inspection

Advanced secure web gateway platforms are incorporating inline DLP capabilities that inspect outbound web traffic for sensitive data patterns including payment card numbers, personally identifiable information, intellectual property, and regulated healthcare data, enabling organizations to prevent inadvertent or malicious exfiltration through web upload channels, cloud storage platforms, and personal email access within the existing secure web gateway traffic inspection pipeline.

Industry Value Chain Analysis

The secure web gateway market value chain spans five primary stages from threat intelligence supply through end-user protection and compliance management. Technology development and cloud platform delivery capture the highest value-add, while integration services and managed operations represent the largest incremental revenue opportunity for professional services providers.

|

Stage |

Key Players / Examples |

|

Threat Intelligence & Research |

Cybersecurity research firms, threat data aggregators, vulnerability intelligence services, and open-source intelligence communities supplying real-time threat feeds and indicators of compromise |

|

Secure Web Gateway Technology Development |

Software vendors, cloud security platform providers, and R&D teams developing URL filtering engines, malware detection modules, SSL inspection capabilities, and zero-trust policy enforcement components |

|

Integration & Professional Services |

Systems integrators, managed security service providers, and consulting firms enabling deployment, configuration, and integration of secure web gateway solutions with enterprise IT environments and cloud infrastructure |

|

Security Operations & Management |

Internal IT and security operations centers, managed detection and response providers, and analytics platforms monitoring web traffic, enforcing policies, and investigating security incidents |

|

End-User Access & Compliance |

Enterprise employees, government users, and third-party contractors accessing corporate and internet resources through secure web gateway-protected channels, supported by compliance and audit functions |

Vertically integrated vendors controlling proprietary threat intelligence feeds, cloud delivery infrastructure, and direct enterprise relationships are positioned to capture greater margin than channel-dependent providers. Managed security service providers operating secure web gateway platforms at scale for multiple enterprise clients are increasingly competing with direct vendor cloud service models as the market commoditizes baseline URL filtering and centralizes differentiation on AI-driven threat detection and SASE integration breadth.

Technology Landscape in the Secure Web Gateway Industry

URL Filtering and Content Classification Engines

Modern secure web gateway platforms deploy ML-based URL categorization engines that classify web destinations across millions of categories in real time, applying policy enforcement before connection establishment. These engines are continuously updated through cloud-sourced threat intelligence, crowdsourced reputation signals, and automated content crawling, enabling enforcement accuracy that significantly exceeds statically maintained category databases.

SSL/TLS Traffic Inspection

Full SSL inspection at scale is a core differentiator among enterprise secure web gateway vendors, with leading platforms capable of decrypting, inspecting, and re-encrypting web traffic flows at multi-gigabit throughput. Selective bypass policies, certificate pinning handling, and compliance with privacy regulations govern SSL inspection deployment in regulated environments.

Cloud-Native Architecture and Global Points of Presence

Cloud-delivered secure web gateway platforms leverage globally distributed points of presence to minimize latency for geographically dispersed users, applying consistent policy enforcement close to user locations. Container-based architecture enables elastic scaling to handle peak traffic volumes, auto-patching against emerging threats, and multi-tenant isolation for enterprise deployments.

Zero-Trust Policy Enforcement and Identity Integration

Integration with enterprise identity and access management platforms enables secure web gateway solutions to apply identity-aware access policies that adapt to device posture, user risk levels, and contextual signals, aligning web access control with zero-trust principles of continuous verification and least-privilege enforcement across all web-bound sessions.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Component |

Solutions |

67.8% |

2025 |

|

Deployment Type |

Cloud-based |

61.4% |

2025 |

|

Organization Size |

Large Enterprises |

🔒 |

2025 |

|

Vertical |

Banking, Financial Services and Insurance (BFSI) |

🔒 |

2025 |

|

Region |

North America |

36.9% |

2025 |

By Component

Solutions command a 67.8% majority share in 2025, driven by enterprise investment in integrated secure web gateway capabilities encompassing URL filtering, malware detection, SSL inspection, advanced threat protection, application control, and data loss prevention. They deliver the core functional value of web security enforcement and represent the primary spend category for both cloud-native and on-premises secure web gateway deployments.

To access detailed market analysis, Request Sample

Services at 32.2% in 2025 cover professional services, including deployment, integration, and custom configuration, as well as managed security services where providers operate secure web gateway infrastructure on behalf of enterprise clients.

By Deployment Type

Cloud-based leads at 61.4% in 2025, reflecting the structural shift toward cloud-first enterprise security architectures, subscription-based SaaS security consumption models, and the ability of cloud-delivered secure web gateways to enforce consistent policies across remote users, branch offices, and cloud workloads without the capital investment and maintenance burden of on-premises proxy infrastructure.

On-premises at 38.6% in 2025 remain a significant segment driven by regulated verticals including financial services, defense, and healthcare where data sovereignty requirements, air-gapped network mandates, and internal security policies limit or prohibit cloud traffic routing.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

|

North America |

36.9% |

Large concentration of enterprises and government agencies, strong regulatory compliance requirements, high cybersecurity spending, and rapid adoption of cloud-based security frameworks |

|

Europe |

25.1% |

Stringent data protection regulations, growing cloud adoption, increasing awareness of advanced persistent threats, and rising investment in enterprise cybersecurity infrastructure |

|

Asia-Pacific |

24.4% |

Rapid digital transformation, expanding enterprise IT infrastructure, growing e-commerce activity, rising cyber threat awareness, and supportive government cybersecurity initiatives |

|

Latin America |

7.1% |

Growing internet penetration, expanding small and medium enterprise adoption of cloud services, and increasing regulatory focus on data security and privacy |

|

Middle East and Africa |

6.5% |

Rising digital infrastructure investments, increasing government and enterprise focus on cybersecurity resilience, and growing cloud service adoption across key economies |

North America at 36.9% in 2025 leads the regional landscape, anchored by the United States which houses a large concentration of enterprise secure web gateway buyers, major solution providers, and a mature cybersecurity services ecosystem. Strong regulatory compliance drivers, including SEC cybersecurity disclosure rules, federal zero-trust mandates, and sector-specific requirements across financial services, healthcare, and defense, sustain high and growing enterprise web security investment through 2034.

Europe at 25.1% is supported by stringent data protection regulations, widespread adoption of cloud security solutions, growing zero-trust implementation, and strong demand for secure access controls across enterprises and public sector organizations.

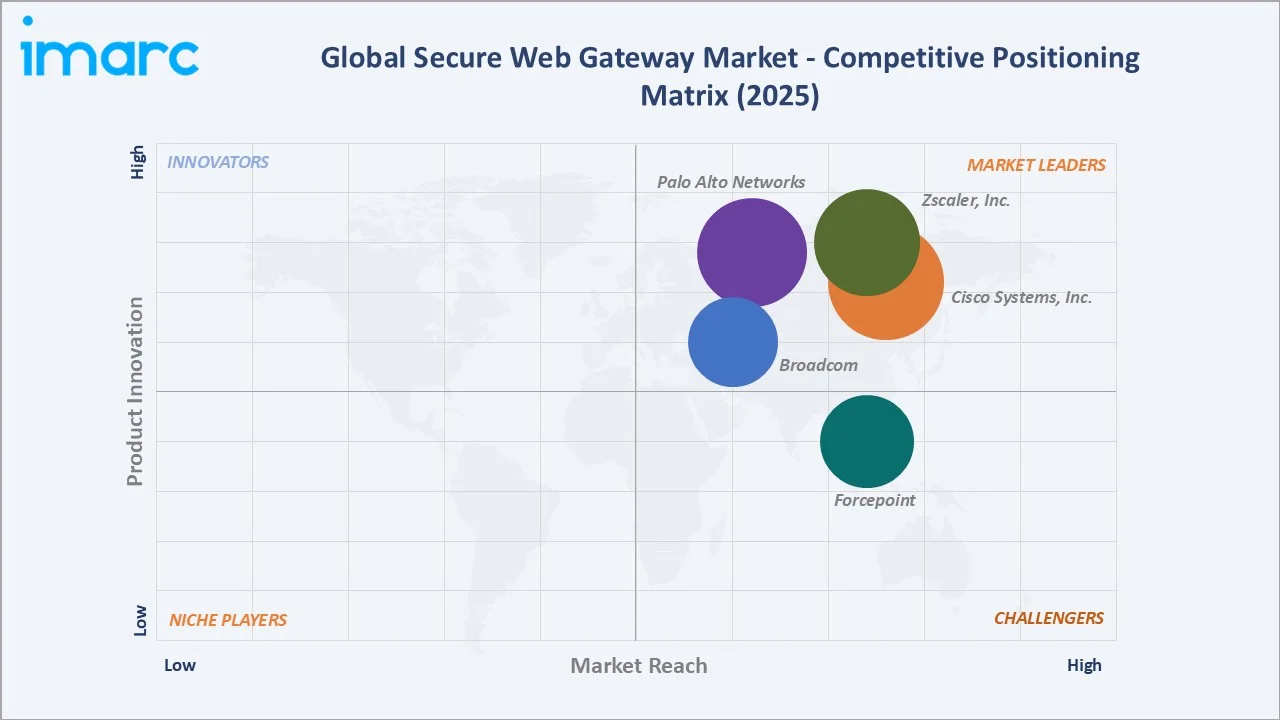

Competitive Landscape

The secure web gateway market is moderately concentrated, with established cybersecurity vendors holding significant market share through broad enterprise relationships, integrated platform offerings, and continuous investment in threat intelligence infrastructure. Market leadership is defined by inspection throughput at scale, breadth of SASE integration, AI-driven detection capability, global points of presence coverage, and depth of compliance certification across regulated verticals.

|

Company Name |

Brand / Key Product |

Position |

Strategic Focus |

|

Zscaler, Inc. |

Zscaler Internet Access (ZIA) |

Leader |

Cloud-native zero-trust secure web gateway platform for globally distributed enterprises |

|

Cisco Systems, Inc. |

Cisco Umbrella |

Leader |

DNS-layer and cloud-delivered secure web gateway integrated with enterprise networking and SASE |

|

Palo Alto Networks |

Prisma Access |

Leader |

AI-powered secure web gateway and SSE platform through unified cloud-native security architecture |

|

Broadcom |

Symantec Cloud Secure Web Gateway |

Leader |

Enterprise secure web gateway with advanced threat protection and hybrid deployment options |

|

Forcepoint |

Forcepoint ONE SWG |

Challenger |

Risk-adaptive secure web gateway with behavioral analytics and deep DLP integration |

Key players include Zscaler, Inc., Cisco Systems, Inc., Palo Alto Networks, Broadcom, and Forcepoint, among others.

Key Company Profiles

Zscaler, Inc.

Zscaler, Inc. is a cloud-native cybersecurity company headquartered in San Jose, California, United States. The company delivers a globally distributed cloud security platform that provides secure access to the internet and cloud applications, replacing legacy network security appliances with a scalable, cloud-delivered architecture serving enterprises across more than 185 countries.

- Product Portfolio: Zscaler Internet Access (ZIA) providing cloud-native secure web gateway capabilities, including URL filtering, SSL inspection, advanced threat protection, malware prevention, and data loss prevention.

- Recent Developments: Zscaler, Inc. has been expanding its AI-powered capabilities through its integrated Zero Trust Exchange platform, enhancing generative AI security controls, data protection for AI tool usage, and autonomous threat detection and response through its Zscaler Deception and Zscaler Risk360 offerings.

- Strategic Focus: Delivering cloud-native zero-trust security across globally distributed enterprise environments, with emphasis on AI-driven threat detection, SASE architecture integration, and digital experience monitoring.

Cisco Systems, Inc.

Cisco Systems, Inc. is a global technology company headquartered in San Jose, California, United States. As one of the world's largest networking and cybersecurity vendors, Cisco provides a comprehensive security portfolio spanning network security, cloud security, identity, and threat intelligence, delivered through integrated hardware and cloud-based platforms.

- Product Portfolio: Cisco Umbrella providing cloud-delivered DNS-layer security and secure web gateway capabilities, including URL filtering, malware detection, and cloud application visibility.

- Recent Developments: Cisco Systems, Inc. has been consolidating its security offerings under the Cisco Security Cloud platform, integrating secure web gateway capabilities with identity services, SD-WAN, and extended detection and response to deliver unified visibility and policy enforcement across enterprise environments.

- Strategic Focus: Integrating secure web gateway capabilities within a comprehensive enterprise security and networking architecture, leveraging deep enterprise networking relationships to deliver converged SASE solutions.

Palo Alto Networks

Palo Alto Networks is a global cybersecurity company headquartered in Santa Clara, California, United States. The company offers an integrated platform of network security, cloud security, and security operations solutions, serving large enterprises and government organizations across several countries through a cloud-delivered architecture.

- Product Portfolio: Prisma Access delivering cloud-native secure web gateway and SSE capabilities including AI-powered threat prevention, URL filtering, and application control.

- Recent Developments: Palo Alto Networks has been advancing its Prisma SASE platform, deepening AI-powered inline threat prevention capabilities, expanding its global points of presence network, and integrating secure web gateway with its broader security operations and extended detection and response offerings.

- Strategic Focus: Delivering a unified, AI-powered cybersecurity platform spanning network security, cloud security, and security operations, with secure web gateway embedded as a core component of its Prisma SASE and zero-trust architecture.

Market Concentration Analysis

The secure web gateway market exhibits moderate-to-high concentration, with the top five vendors – Zscaler, Inc., Cisco Systems, Inc., Palo Alto Networks, Broadcom, and Forcepoint – collectively accounting for a substantial share of global enterprise secure web gateway revenue through established enterprise relationships, comprehensive platform portfolios, and global support infrastructure.

Barriers to entry are significant in the enterprise segment, including the requirement for a globally distributed points of presence network, massive ongoing investment in real-time threat intelligence, comprehensive compliance certifications, and the challenge of displacing entrenched multi-year enterprise contracts. These factors favor well-capitalized incumbents and consolidate competitive positioning around a small group of full-platform providers.

Consolidation is an ongoing trend as larger cybersecurity platforms acquire niche secure web gateway and adjacent security vendors to fill capability gaps, accelerate SASE portfolio completeness, and access enterprise customer bases. Emerging vendors focusing on AI-native inspection architectures and endpoint-local secure web gateway enforcement are carving differentiated positions in segments underserved by incumbent platform approaches.

Investment & Growth Opportunities

Fastest-Growing Segments

Cloud-based is expanding the fastest among deployment types, driven by enterprise migration to subscription-based security consumption, SASE adoption, and the operational advantages of cloud-native architectures. AI-driven advanced threat protection and integrated DLP capabilities represent the fastest-growing functional areas within the component category, commanding premium pricing and displacing stand-alone point solutions.

Emerging Markets

Asia-Pacific is the fastest-growing regional opportunity, driven by rapid digital transformation across India, Southeast Asia, and East Asia, expanding enterprise cloud adoption, rising regulatory cybersecurity requirements, and a growing base of organizations deploying secure web gateway for the first time as they transition from traditional perimeter security to cloud-delivered controls.

Venture & Investment Trends

Venture and strategic investment in the secure web gateway and adjacent SASE sector is concentrated in AI-native security startups building next-generation inspection engines, endpoint-local secure web gateway architectures, and cloud security posture management platforms. Large cybersecurity platform vendors are investing through acquisitions targeting AI security, data classification, remote browser isolation, and identity-aware access control capabilities that enhance secure web gateway platform differentiation.

Future Market Outlook (2026-2034)

The secure web gateway market is forecast to expand from USD 14.08 Billion in 2025 to USD 45.54 Billion by 2034 at a CAGR of 13.52%, adding approximately USD 31.46 Billion in annual market value over the forecast period.

Four forces will define the market through 2034: the continued convergence of secure web gateway within unified SASE and SSE platforms; the emergence of AI-autonomous threat detection reducing analyst dependence and accelerating response velocity; the extension of secure web gateway controls to cover AI tool usage and generative AI prompt inspection as new risk vectors; and the expansion of secure web gateway adoption into mid-market and small enterprise segments globally as cloud-delivered secure web gateway reaches cost and complexity parity with traditional perimeter controls.

By 2034, secure web access is expected to be a foundational capability embedded within broader enterprise security platforms, with secure web gateway functionality increasingly consumed as a component of unified SASE and zero-trust architectures rather than as a discrete product category.

Research Methodology

Primary Research

Primary research included structured interviews with enterprise security architects, chief information security officers, IT procurement decision-makers, secure web gateway platform vendors, managed security service providers, and channel partners, validating market sizing, segmentation dynamics, competitive positioning, and deployment trend data across regions and verticals.

Secondary Research

Secondary sources included vendor annual reports and SEC filings, industry association publications from the Cloud Security Alliance and Information Systems Security Association, regulatory guidance from CISA, ENISA, and the National Institute of Standards and Technology, analyst publications, enterprise security buyer surveys, and publicly disclosed partnership and acquisition announcements.

Forecasting Models

Market forecasts applied top-down and bottom-up modeling combining enterprise cybersecurity spending growth rates, secure web gateway adoption penetration by organization size and vertical, deployment type transition dynamics, regional digital transformation indices, and macroeconomic variables. Scenario analysis addressed regulatory acceleration, AI-driven technology disruption pace, and consolidation rate among platform vendors.

Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Segment Coverage | Component, Deployment Type, Organization Size, Vertical, Region |

| Region Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | Zscaler Inc., Cisco Systems Inc., Palo Alto Networks, Broadcom, Forcepoint, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the Secure Web Gateway Market Report

The secure web gateway market was valued at USD 14.08 Billion in 2025, driven by rising cyber threats, enterprise cloud migration, and accelerating adoption of zero-trust and SASE security frameworks.

The market is projected to grow at a CAGR of 13.52% from 2026 to 2034, reaching USD 45.54 Billion, supported by cloud-first security architecture adoption and AI-driven threat detection integration.

Solutions lead at 67.8% in 2025, encompassing URL filtering, SSL inspection, malware detection, and advanced threat protection.

Cloud-based dominates at 61.4% in 2025, driven by SASE adoption, remote workforce security requirements, and enterprise migration toward subscription-based security consumption models.

North America commands 36.9% in 2025, led by the United States, driven by large enterprise cybersecurity budgets, regulatory compliance requirements, and high concentration of secure web gateway solution providers.

Leading players include Zscaler, Inc., Cisco Systems, Inc., Palo Alto Networks, Broadcom, and Forcepoint, among others.

Growth is driven by escalating web-borne cyber threats, accelerating enterprise cloud adoption, expansion of remote and hybrid work models, and integration of secure web gateway within SASE and zero-trust security frameworks.

AI and ML enable real-time detection of zero-day threats, behavioral anomalies, and novel malware variants in web traffic, improving detection accuracy and reducing false positives while enabling autonomous response.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)

Related Reports

Choose your plan

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Single User License

- 1 User License, Access on 2 Devices

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- No Printing Rights

- 10% Free Report Customization

- 10–12 Weeks of Analyst Support

Five User License

- Access for 5 Users, 2 Devices per User

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- Dedicated Account Manager

- 12–14 Weeks of Analyst Support

- No Printing Rights

- 15% Free Report Customization

- 25% Discount on Your Next Purchase

Corporate User License

- Unlimited User Access (Within Your Organization)

- PDF Report + Excel Dataset

- Lifetime Access

- Dedicated Account Manager

- 14–20 Weeks of Analyst Support

- No Printing Rights

- 20% Free Report Customization

- 30% Discount on Your Next Purchase

Essential Insights

What's included:

3 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 2 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Professional Access

What's included:

5 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 8 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Business Advantage

What's included:

8 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 14 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Enterprise Intelligence

What's included:

10 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 20 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade