Single-Use Bioreactors Market Size, Share, Trends and Forecast by Product Type, Type, Cell Type, Molecule Typ, End User, and Region, 2026-2034

Single-Use Bioreactors Market Size, Share, Trends & Forecast (2026-2034)

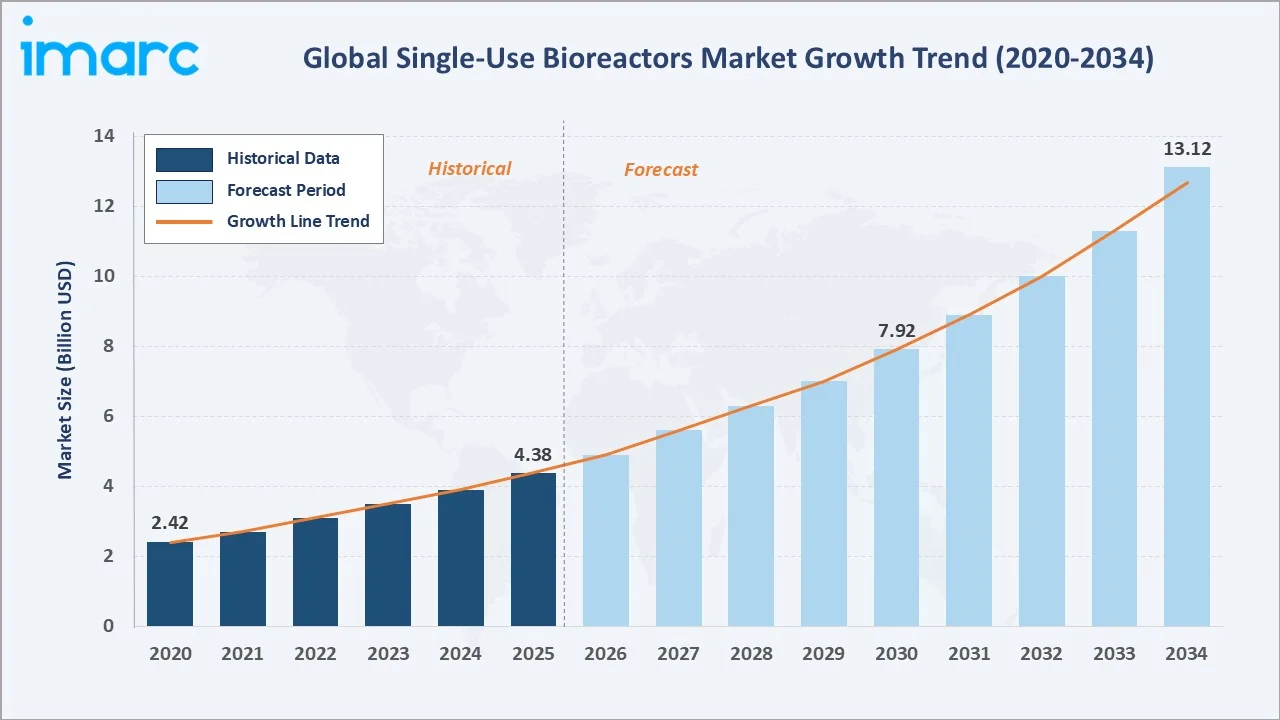

The global single-use bioreactors market reached USD 4.38 Billion in 2025 and is projected to reach USD 13.12 Billion by 2034, growing at a CAGR of 12.58% during 2026-2034. Surging demand for biopharmaceuticals including monoclonal antibodies, vaccines, and cell and gene therapies; the cost efficiency and operational flexibility of disposable systems versus stainless steel infrastructure; accelerating adoption across contract development and manufacturing organizations; and continuous advancements in single-use bag, sensor, and control technology are the key single-use bioreactors market growth drivers sustaining the market's high-growth trajectory.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 4.38 Billion |

|

Forecast Market Size (2034) |

USD 13.12 Billion |

|

CAGR (2026-2034) |

12.58% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

These systems offer biopharmaceutical manufacturers flexibility, faster batch changeovers, reduced contamination risk, and lower operating costs compared with traditional stainless-steel reactors, driving adoption among CMOs, CDMOs, and biotech firms.

To get more information on this market, Request Sample

The single-use bioreactors market is underpinned by three structural forces: the global biopharmaceutical industry's shift toward flexible, multi-product manufacturing facilities; the rapid expansion of cell and gene therapy programs requiring smaller, highly adaptable bioreactor configurations; and the proliferation of contract manufacturing organizations globally that prefer single-use infrastructure for rapid changeover between client products and biologics manufacturing campaigns.

Executive Summary

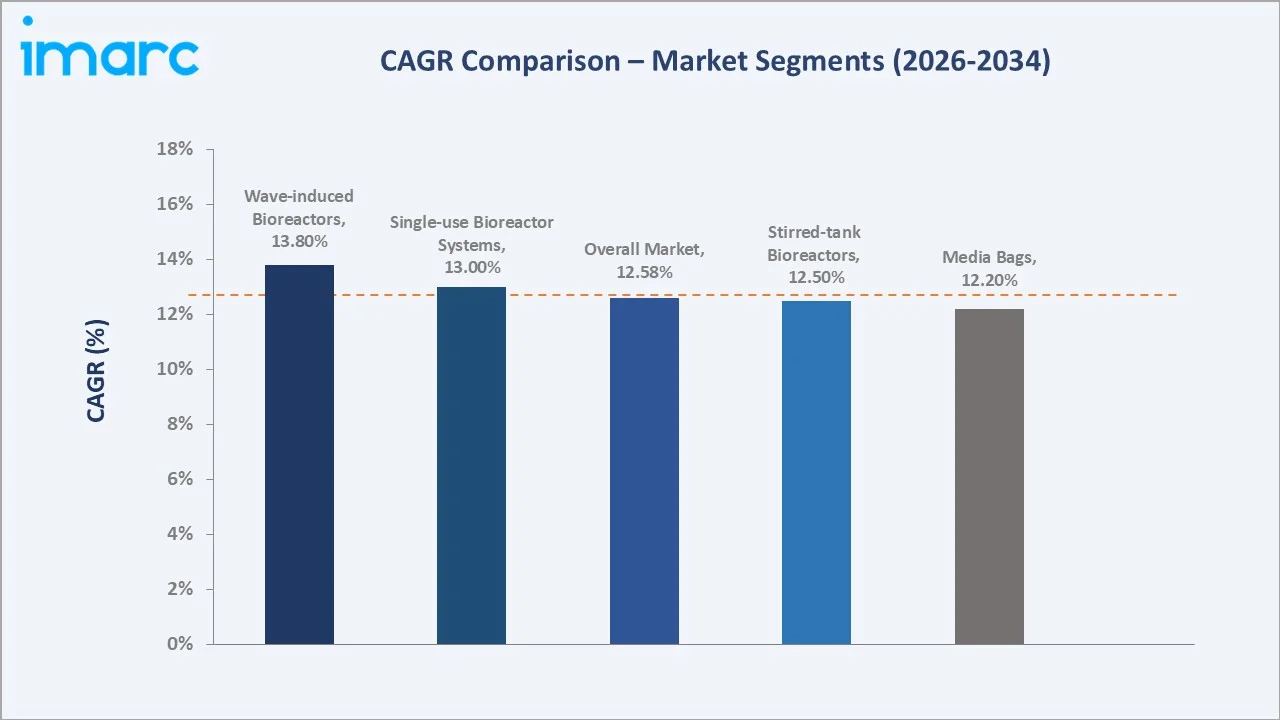

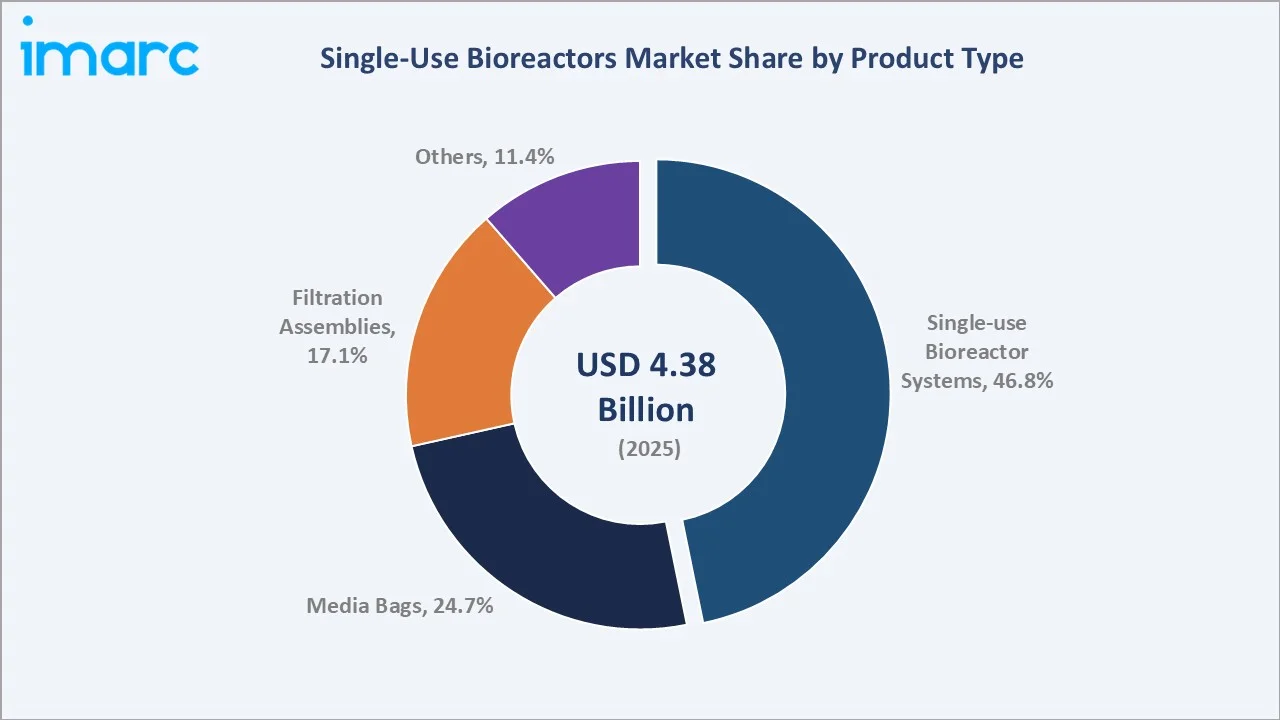

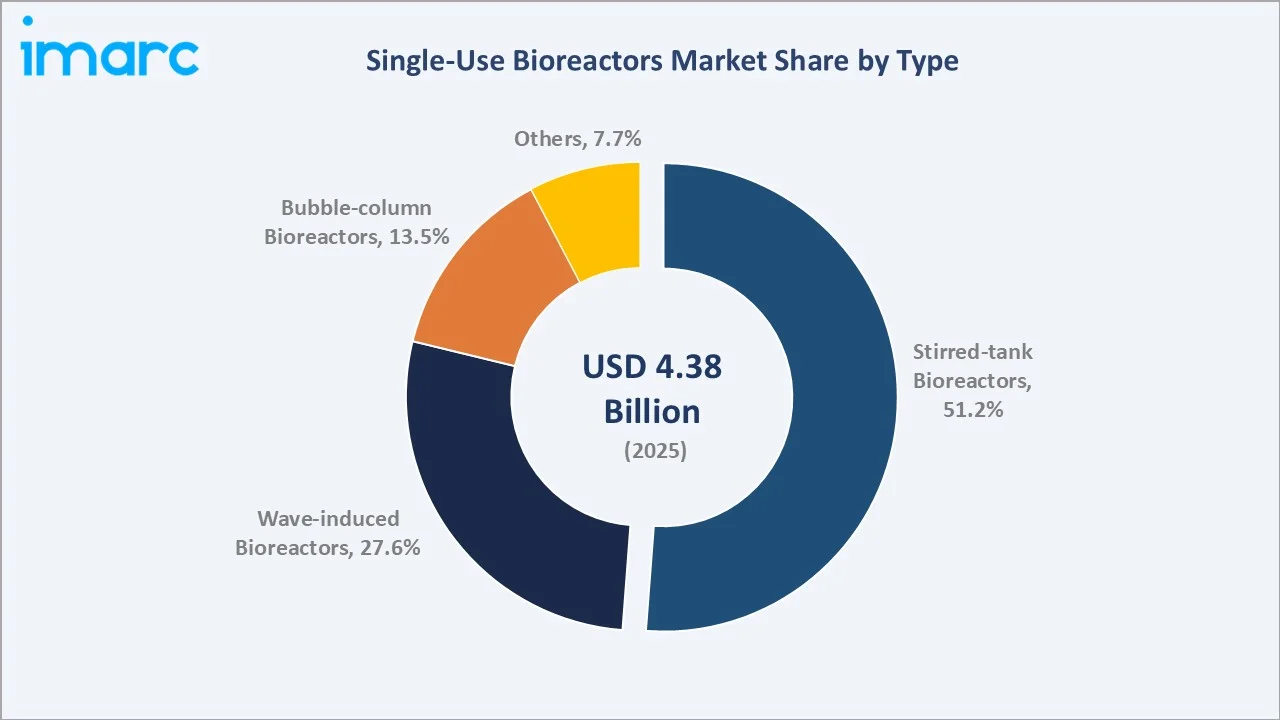

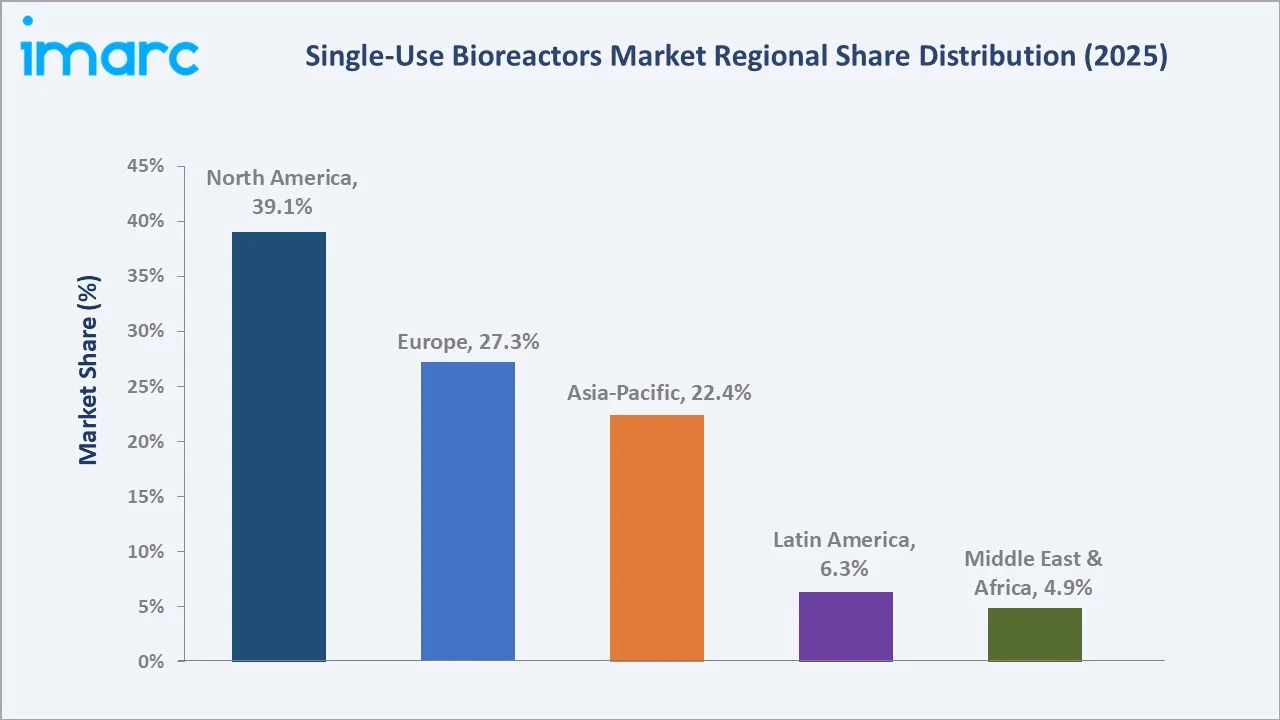

The global single-use bioreactors market was valued at USD 4.38 Billion in 2025 and is forecast to reach USD 13.12 Billion by 2034 at a CAGR of 12.58%. Single-use bioreactor systems dominate with 46.8% product type share, while stirred-tank bioreactors lead the type breakdown at 51.2%. North America commands 39.1% of global revenue, supported by the world's most advanced biopharmaceutical manufacturing ecosystem.

The single-use bioreactors market outlook is shaped by the simultaneous growth of biologics demand, CDMO capacity expansion, and the commercialization of advanced cell and gene therapies that require flexible, disposable manufacturing platforms throughout the forecast period.

Key Market Insights

|

Insight |

Data |

|

Largest Product Type Segment |

Single-use Bioreactor Systems – 46.8% share (2025) |

|

Fastest Growing Product Type |

Single-use Bioreactor Systems – ~13.0% CAGR (2026-2034) |

|

Largest Type Segment |

Stirred-tank Bioreactors – 51.2% share (2025) |

|

Fastest Growing Type |

Wave-induced Bioreactors – ~13.8% CAGR (2026-2034) |

|

Leading Region |

North America – 39.1% share (2025) |

|

Top Companies |

Sartorius AG, Thermo Fisher Scientific Inc., Danaher Corporation, Merck KGaA, Eppendorf SE |

Key Analytical Observations For 2025:

- Single-use Bioreactor Systems (46.8%): Dominates the product type landscape as the primary revenue driver, representing the complete integrated bioreactor platform including bag, control system, and automation.

- Stirred-tank Bioreactors (51.2%): Lead the type segment as the most versatile and widely adopted configuration across cell culture applications including monoclonal antibody production, vaccine manufacturing, and biosimilar development.

- Wave-induced Bioreactors (27.6%): Represent the fastest-growing type segment at ~13.8% CAGR from 2026 to 2034, driven by accelerating cell and gene therapy manufacturing adoption where gentle rocking motion prevents shear stress on fragile cell lines including stem cells, T cells, and viral vector-producing cells used in advanced therapy manufacturing.

- North America (39.1%): Market leadership anchored by the United States, which hosts the world's highest concentration of biopharmaceutical manufacturers, CDMOs, and research institutions, supported by FDA regulatory frameworks actively facilitating single-use technology adoption and a mature biologics reimbursement environment.

Single-Use Bioreactors Market Overview

Single-use bioreactors, also known as disposable bioreactors, are bioprocessing systems in which the vessel contacting product is replaced between manufacturing runs, eliminating the need for cleaning, sterilization-in-place, and the associated validation burden that characterizes stainless steel systems.

The global market encompasses four principal product categories: complete single-use bioreactor systems, single-use media bags, filtration assemblies, and ancillary consumables, serving biopharmaceutical manufacturers, contract development and manufacturing organizations, contract research organizations, and academic research institutions globally.

The single-use bioreactors market forecast is shaped by the biopharmaceutical industry's structural transition toward flexible manufacturing facilities capable of producing multiple biological entities within a single physical plant using modular, reconfigurable process trains. Single-use technology directly enables this manufacturing agility by eliminating the fixed-product contamination risk associated with reusable vessels.

The market benefits from the continued expansion of the global biologics pipeline, as in 2025, the U.S. Food and Drug Administration (FDA) approved 46 new drugs, of which 25% were biologics, and the growth of biosimilar manufacturing in Asia-Pacific and Latin America, where cost-competitive single-use systems enable smaller-scale, flexible production facilities.

Market Dynamics

To evaluate market opportunities, Request Sample

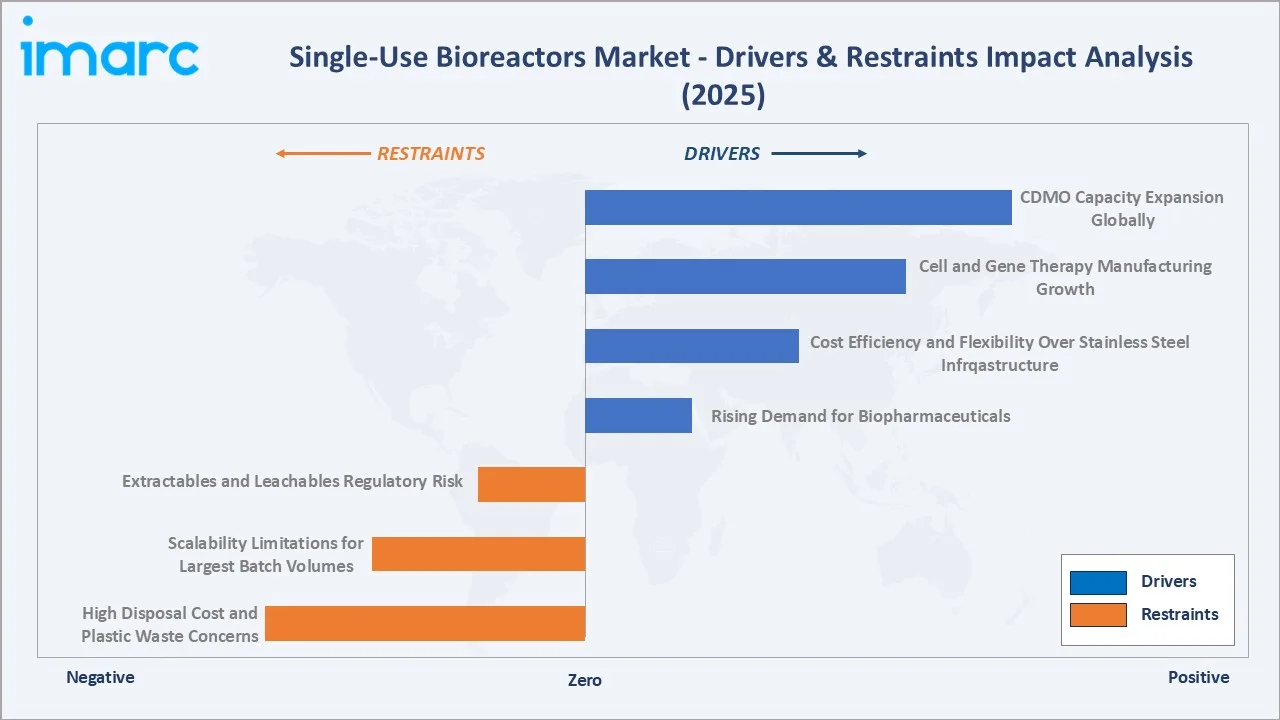

Market Drivers

- Rising Demand for Biopharmaceuticals: The global biologics market, comprising monoclonal antibodies, recombinant proteins, vaccines, and cell and gene therapies, continues its structural expansion. Monoclonal antibodies alone represent a USD 250+ Billion global market in 2025, with pipeline growth driving sustained capital investment in single-use manufacturing capacity.

- Cost Efficiency and Flexibility Over Stainless Steel Infrastructure: Single-use systems procurement costs for new facilities are approximately 40% less compared to stainless steel equivalents, eliminate cleaning validation costs, reduce turnaround time between production campaigns, and lower energy and water consumption by 45–50%, making them economically superior for most new facility investments.

- Cell and Gene Therapy Manufacturing Growth: The clinical and commercial pipeline for CAR-T cells, gene therapies, and stem cell products is generating substantial demand for wave-induced and stirred-tank single-use bioreactors configured for gentle, low-shear cell expansion at volumes incompatible with conventional manufacturing approaches.

- CDMO Capacity Expansion Globally: The contract development and manufacturing organization sector is investing heavily in single-use manufacturing infrastructure to serve multiple biologics clients simultaneously, creating concentrated procurement demand for large-volume single-use bioreactor systems and consumables.

Market Restraints

- High Disposal Cost and Plastic Waste Concerns: The recurring cost of single-use bags, filters, and assemblies can exceed the annualized cost of equivalent stainless steel infrastructure at very high production volumes. Growing regulatory and public scrutiny on pharmaceutical plastic waste is also driving sustainability pressure on manufacturers.

- Scalability Limitations for Largest Batch Volumes: Commercially available single-use bioreactors are primarily established in the 50L–2000L range, while stainless steel remains dominant for 10,000L+ production vessels used in the largest-scale monoclonal antibody manufacturing campaigns.

- Extractables and Leachables Regulatory Risk: Polymeric single-use components may leach chemical compounds into the bioprocess fluid, creating extractables and leachables compliance requirements that add validation burden and potential regulatory risk, particularly for parenteral biological products.

Market Opportunities

- Scale-Up of Single-Use Bioreactors Beyond 2000L: Technology development programs targeting 5,000L–10,000L single-use systems would dramatically expand the addressable market into large-volume monoclonal antibody manufacturing, where the total installed base of stainless steel vessels represents a multi-billion-dollar replacement opportunity.

- Biosimilar Manufacturing Growth in Emerging Markets: India, China, South Korea, and Brazil are rapidly expanding biosimilar production capacity, with single-use systems preferred for new facility investments in these cost-sensitive manufacturing environments.

Market Challenges

- Supply Chain Concentration and Disruption Risk: The single-use bioreactor supply chain is concentrated among a small number of polymer film, sensor, and bag manufacturers, creating supply disruption risk as demonstrated during the COVID-19 pandemic when unprecedented vaccine manufacturing demand created industry-wide shortages.

- Regulatory Harmonization Complexity: Divergent regulatory expectations for extractables and leachables testing, biocompatibility validation, and supply chain documentation across FDA, EMA, PMDA, and NMPA jurisdictions increase compliance costs for global single-use bioreactor suppliers and their biopharmaceutical customers.

Emerging Market Trends

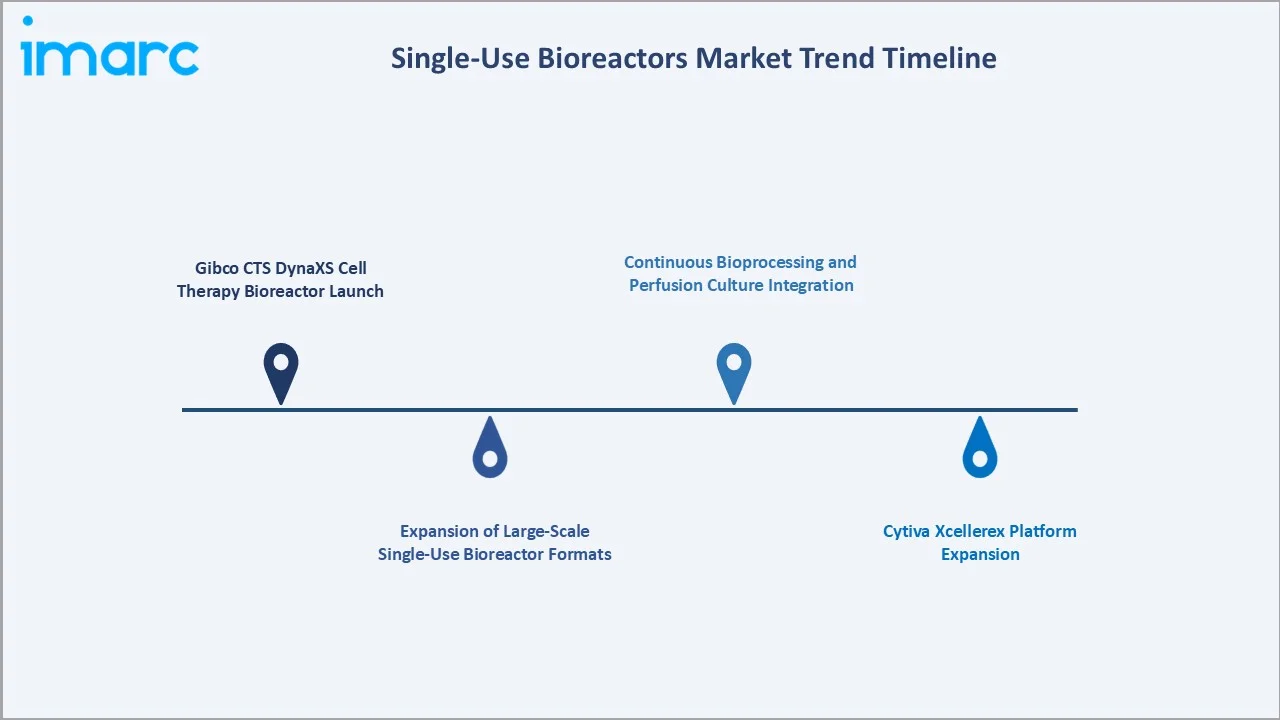

1. Gibco CTS DynaXS Cell Therapy Bioreactor Launch

In May 2026, Thermo Fisher Scientific introduced the Gibco CTS DynaXS Single‑Use Bioreactor, a scalable, cGMP‑ready platform designed to help cell therapy developers expand from early process development to clinical and commercial manufacturing with precise control and flexibility. The stirred‑tank, single‑use system supports workflows from cell isolation and activation through expansion, enabling consistent quality and automation‑ready scalability for a range of therapeutic applications.

2. Expansion of Large-Scale Single-Use Bioreactor Formats

In November 2025, Thermo Fisher Scientific expanded its bioprocessing capabilities across Asia by opening a new Bioprocess Design Center in Hyderabad, India, and upgrading existing hubs in Incheon, Korea, and Singapore to support regional biopharma growth. This geographic and scale expansion reflects the broader single-use bioreactors market trends toward distributed, regionally proximate manufacturing.

3. Cytiva Xcellerex Platform Expansion

In March 2025, Cytiva (subsidiary of Danaher Corporation) expanded its Xcellerex X‑platform by adding 500 L and 2,000 L single‑use bioreactors, enabling scalable bioprocessing from early‑stage research through to commercial manufacturing. The enhanced portfolio aims to increase operational efficiency, production capacity, and flexibility for advanced therapeutic development while helping reduce costs and risks.

4. Continuous Bioprocessing and Perfusion Culture Integration

Continuous bioprocessing, in which cells are maintained in sustained culture at high density using perfusion feeding and continuous product harvest, is gaining significant traction as an alternative to fed-batch manufacturing that can substantially increase volumetric productivity from smaller bioreactor volumes. Single-use bioreactor manufacturers are developing perfusion-optimized disposable configurations that integrate retention devices, feeding manifolds, and harvest assemblies into pre-assembled, gamma-irradiated sets.

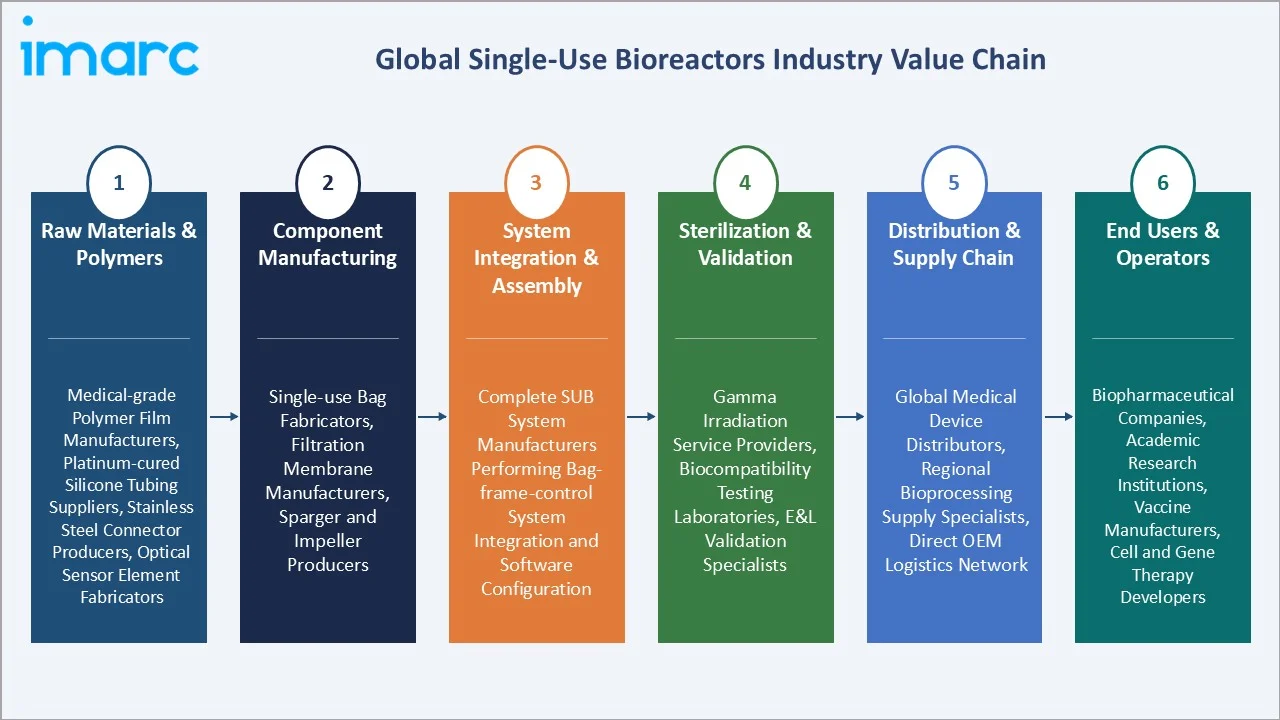

Industry Value Chain Analysis

|

Stage |

Key Players / Examples |

|

Raw Materials & Polymers |

Medical-grade polymer film manufacturers, platinum-cured silicone tubing suppliers, stainless steel connector producers, optical sensor element fabricators |

|

Component Manufacturing |

Single-use bag fabricators, filtration membrane manufacturers, sparger and impeller producers |

|

System Integration & Assembly |

Complete SUB system manufacturers performing bag-frame-control system integration, hardware assembly, and software configuration |

|

Sterilization & Validation |

Gamma irradiation service providers, biocompatibility testing laboratories, extractables and leachables validation specialists |

|

Distribution & Supply Chain |

Global medical device distributors, regional bioprocessing supply specialists, direct OEM logistics networks |

|

End Users & Operators |

Biopharmaceutical companies, academic research institutions, vaccine manufacturers, cell and gene therapy developers |

Technology Landscape in the Single-Use Bioreactors Industry

Stirred-Tank Single-Use Bioreactor Technology

Stirred-tank single-use bioreactors represent the dominant technology configuration globally, accounting for 51.2% of market revenue in 2025. These systems adapt the established stirred-tank bioreactor engineering principle to a disposable bag format using magnetically coupled impeller drives that eliminate shaft seal penetrations and enable completely closed-system operation.

Wave-Induced (Rocking Motion) Bioreactor Technology

Wave-induced bioreactors operate by rocking a partially filled culture bag on an oscillating platform, generating wave motion that drives gas-liquid mass transfer and mixing without mechanical impellers or spargers. This low-shear operating principle makes wave-induced systems the preferred configuration for sensitive cell lines including CAR-T cells, mesenchymal stem cells, and viral vector-producing cells in cell and gene therapy manufacturing.

Bubble-Column Single-Use Bioreactor Technology

Bubble-column single-use bioreactors achieve mixing and oxygenation through direct gas sparging into the culture vessel without mechanical agitation, offering a mechanically simple design that minimizes shear stress and reduces component complexity. These systems are primarily deployed in microbial fermentation applications and early-stage process development where simplicity, low cost, and ease of scale-up modeling are prioritized over the mass transfer performance achievable with stirred-tank configurations.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Product Type |

Single-use Bioreactor Systems |

46.8% |

2025 |

|

Type |

Stirred-tank Bioreactors |

51.2% |

2025 |

|

Cell Type |

🔒 |

🔒 |

2025 |

|

Molecule Type |

🔒 |

🔒 |

2025 |

|

End User |

🔒 |

🔒 |

2025 |

|

Region |

North America |

39.1% |

2025 |

By Product Type

Single-use bioreactor systems dominate at 46.8% share in 2025, representing the highest-value product category comprising complete bioreactor platforms including the flexible bioprocess container, agitation and aeration system, control hardware, and process monitoring software. Capital expenditure on complete bioreactor systems drives the largest proportion of market revenue, particularly as biopharma facilities and CDMOs invest in new manufacturing trains at the 200L–2000L scale.

To access detailed market analysis, Request Sample

Media bags at 24.7% generate highly predictable recurring revenue as consumable components are replaced at every production run, providing manufacturers with a stable base of contracted supply relationships independent of capital equipment procurement cycles.

By Type

Stirred-tank bioreactors lead with 51.2% share in 2025, underpinned by their superior mass transfer performance, compatibility with a wide range of cell lines and bioprocess modes, established scale-up precedent, and the availability of extensive regulatory precedent supporting product filings based on stirred-tank culture data.

Wave-induced bioreactors at 27.6% are experiencing the highest growth velocity at ~13.8% CAGR, as cell and gene therapy commercial manufacturing scale-up generates concentrated procurement demand for gentle, closed-system cell expansion platforms. T cell immunotherapy, NK cell therapy, and viral vector manufacturing programs are each creating distinct wave bioreactor demand segments.

Regional Market Insights

North America's market leadership at 39.1% in 2025 reflects the world's most advanced biopharmaceutical manufacturing and R&D ecosystem, anchored by the United States, which hosts the highest global concentration of biologics manufacturers, CDMOs, and cell therapy developers.

Asia-Pacific at 22.4% is the fastest-growing regional market, driven by China's ambitious domestic biologics manufacturing capacity expansion programs, India's position as the world's largest biosimilar producer scaling toward single-use systems, and substantial government-backed investment in CDMO infrastructure across South Korea, Singapore, and Japan.

|

Region |

Share (2025) |

Key Growth Drivers |

|

North America |

39.1% |

World-leading biopharmaceutical R&D and manufacturing hub, high CDMO density, strong cell and gene therapy commercialization pipeline |

|

Europe |

27.3% |

Strong biopharmaceutical manufacturing base in Germany, Switzerland, and Ireland, European manufacturing investment, and growing biosimilar production capacity |

|

Asia-Pacific |

22.4% |

Rapid biologics manufacturing capacity expansion in China and India, government-supported bioprocess infrastructure investment, growing CDMO sector, and expanding domestic biosimilar manufacturing |

|

Latin America |

6.3% |

Brazil and Mexico biosimilar manufacturing programs, government investment in domestic vaccine production capacity, and growing private sector biopharma manufacturing infrastructure |

|

Middle East & Africa |

4.9% |

UAE and Saudi Arabia biopharma sector development initiatives, government-led healthcare localization programs, and emerging academic and research biomanufacturing capacity |

Competitive Landscape

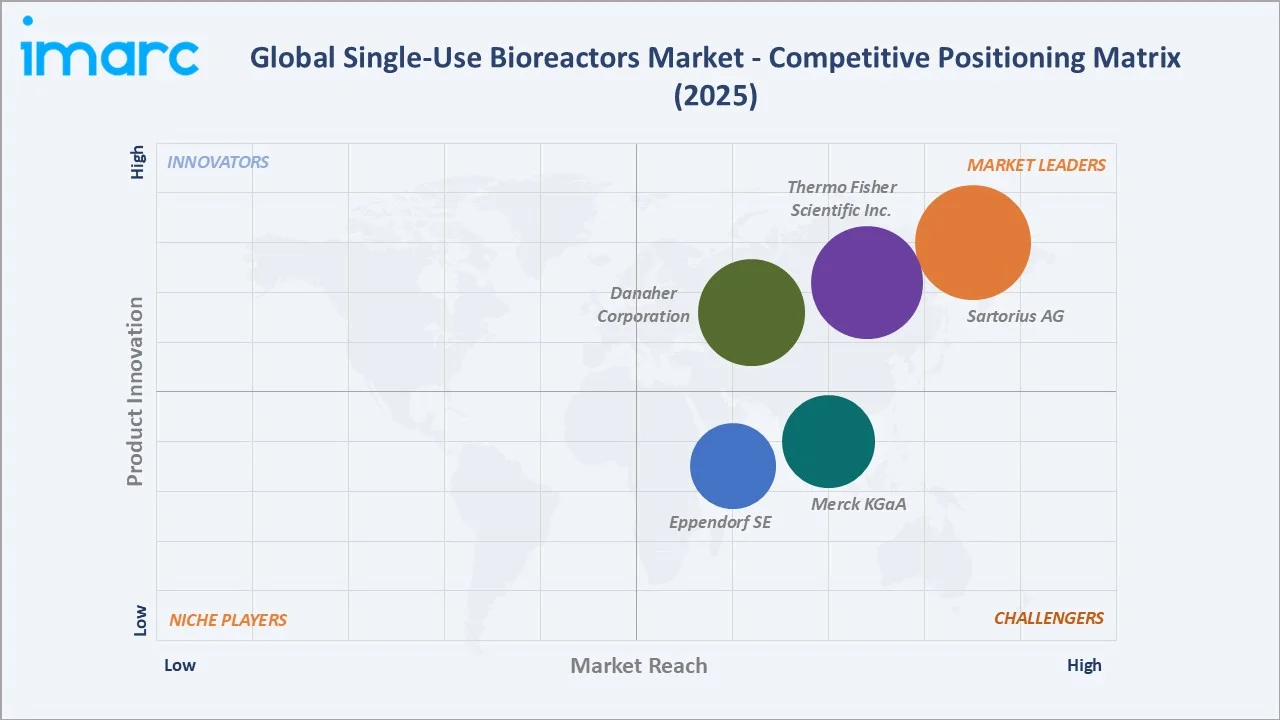

The global single-use bioreactors market exhibits moderate-to-high concentration, with Sartorius AG, Thermo Fisher Scientific Inc., Danaher Corporation, Merck KGaA, and Eppendorf SE collectively commanding approximately 70–80% of total global revenue in 2025, reflecting the capital-intensive nature of building validated global supply chains for single-use bioprocess components.

| Company Name | Brands/Products | Market Position | Core Strength |

|---|---|---|---|

| Sartorius AG | Biostat STR, Biostat RM, Biostat RM TX, Flexsafe, Flexsafe STR, Flexsafe RM, Flexsafe RM TX, Univessel, Ambr | Market Leader | Full single-use portfolio; sensor integration; ideal for mammalian cell culture including very demanding high cell-density or microcarrier-based processes |

| Thermo Fisher Scientific Inc. | HyPerforma, DynaDrive, Thermo Scientific bioprocessing systems | Market Leader | HyPerforma single-use bioreactors platform; Asia-Pacific large-scale manufacturing |

| Danaher Corporation (Cytiva) | Xcellerex, iCELLis bioprocess systems | Market Leader | Integrated bioprocessing workflow solutions |

| Merck KGaA | Mobius single-use bioprocess systems | Strong Challenger | Mobius single-use platform; continuous bioprocessing |

| Eppendorf SE | BioBLU single-use bioreactors | Strong Challenger | Lab-scale and benchtop single-use systems; gene therapy and stem cell research focus |

Portfolio breadth and integration capability are paramount, as biopharmaceutical customers and CDMOs consistently prefer vendors that supply the complete single-use process train from bioreactor and media bags through filtration assemblies and downstream purification components, enabling single-source procurement, unified extractables and leachables data packages, and integrated process development support.

Key Company Profiles

Sartorius AG

Sartorius AG is one of the global market leaders in single-use bioreactor systems. The company provides a comprehensive portfolio spanning single-use bioreactors, media bags, filtration assemblies, sensors, and bioprocess control software that spans laboratory scale through commercial manufacturing.

- Product Portfolio: Biostat STR (stirred-tank), Biostat RM TX (wave-induced, for cell therapy), Flexsafe media bags, Biostat RM, Flexsafe STR, Flexsafe RM, Flexsafe RM TX, Univessel, and Ambr micro-scale bioreactor systems.

- Recent Developments: In June 2025, Sartorius AG’s subsidiary Sartorius Stedim Biotech completed the capacity expansion at its Aubagne, France headquarters, nearly doubling cleanroom space, installing automated production lines for single‑use bioprocessing components, and adding expanded labs and logistics facilities.

- Strategic Focus: Digital bioprocessing platform integration; expanding single-use coverage beyond 2000L; cell and gene therapy manufacturing solutions; biosimilar market penetration in Asia-Pacific.

Thermo Fisher Scientific Inc.

Thermo Fisher Scientific Inc. is one of the world's largest single-use bioreactor suppliers and a provider of life science products globally. Its bioproduction segment encompasses a complete portfolio of single-use bioprocessing solutions serving biopharmaceutical manufacturers and CDMOs across all scales.

- Product Portfolio: HyPerforma single-use bioreactor (50L–2000L), DynaDrive single-use bioreactor, Thermo Scientific bioreactors, and single-use filtration and purification systems.

- Recent Developments: In April 2025, Thermo Fisher Scientific Inc. introduced the 5 L DynaDrive single‑use bioreactor, designed to simplify and accelerate upstream process development with enhanced mixing, control, and scalability for early‑stage biologics workflows.

- Strategic Focus: Building end-to-end single-use bioprocessing solutions; expanding Asia-Pacific manufacturing capacity; strengthening filtration and purification single-use portfolio integration.

Market Concentration Analysis

The global single-use bioreactors market exhibits high concentration at the top tier, with Sartorius AG, Thermo Fisher Scientific Inc., Danaher Corporation, Merck KGaA, and Eppendorf SE, collectively commanding 70–80% of global revenue in 2025. This concentration reflects significant barriers to entry, including the capital requirements for gamma irradiation facilities and the investment needed to establish WHO and FDA-compliant supply chain validation.

In January 2025, PBS Biotech raised USD 17 Million to accelerate new product development, demonstrating that well-differentiated challengers can attract institutional capital to compete in high-growth niches such as cell therapy bioreactors.

Investment and Growth Opportunities

Fastest Growing Segments

Wave-induced bioreactors (~13.8% CAGR), cell and gene therapy manufacturing platforms (~18–20% CAGR), digital-integrated bioreactor control systems (~15% CAGR), and continuous perfusion bioprocessing consumables (~16% CAGR) represent the highest-growth investment vectors through 2034. These sub-categories address a combined incremental addressable market of approximately USD 4.5 Billion beyond current base projections by 2030.

Emerging Market Expansion

Asia-Pacific, specifically China and India, represents the primary geographic growth opportunity, with government-backed biologics manufacturing investment programs creating large procurement pipelines for single-use bioreactor systems and consumables.

Entry strategies include local technical service network investment, regional manufacturing partnerships to meet domestic content preferences, and direct engagement with national CDMO champions that serve as anchor customers for new facility investments in these markets.

Venture and Institutional Investment Trends

- Digital bioprocessing platform ventures combining single-use hardware with cloud analytics and AI-driven process optimization are attracting Series B and C venture funding, seeking to capture recurring software and analytics revenue on installed single-use bioreactor bases.

- Sustainable single-use technology startups developing biodegradable or recyclable single-use bioprocess components are attracting ESG-aligned impact investment, with validated sustainable alternatives expected to command pricing premiums in the European market.

Future Market Outlook (2026-2034)

The global single-use bioreactors market is positioned for sustained high-growth expansion through 2034. From a base of USD 4.38 Billion in 2025, the market is projected to reach USD 13.12 Billion by 2034, representing total incremental value creation of USD 8.74 Billion at a CAGR of 12.58%.

This trajectory is anchored by the inexorable growth of the global biologics pipeline, the technology transition away from stainless steel in new facility investments globally, and the commercial launch of multiple cell and gene therapy products requiring flexible, scalable single-use manufacturing platforms.

Research Methodology

Primary Research

Primary research comprised structured interviews with over 90 industry participants during 2024–2025, including single-use bioreactor manufacturers, biopharmaceutical manufacturing directors, CDMO process development scientists, bioprocess equipment procurement specialists, and institutional investors, validating market sizing assumptions and technology adoption timelines across all key regions.

Secondary Research

Secondary research encompassed manufacturer annual reports, FDA Guidance for Industry on Process Validation, EMA single-use technology guidance documents, BPOG extractables and leachables guidelines, industry publications including BioProcess International and Pharmaceutical Technology, and institutional investor research on bioprocessing equipment manufacturers.

Forecasting Models

Market size estimations derived using top-down and bottom-up forecasting incorporating biologics production volume projections by molecule type, single-use system penetration rates by manufacturing scale and region, average selling price trajectories by product type, and vendor revenue disclosures. Base-case CAGR of 12.58% reflects consensus estimates validated against announced CDMO and biopharmaceutical facility investment pipelines through 2034.

Single-Use Bioreactors Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Product Types Covered | Single-Use Bioreactor Systems, Media Bags, Filtration Assemblies, Others |

| Types Covered | Stirred-tank Bioreactors, Wave-induced Bioreactors, Bubble-column Bioreactors, Others |

| Cell Types Covered | Mammalian Cell, Bacteria, Yeast, Others |

| Molecule Types Covered | Vaccines, Monoclonal Antibodies, Stem Cells, Recombinant Proteins, Others |

| End Users Covered | Pharmaceutical and Biopharmaceutical Companies, Contract Research Organizations, Academic and Research Institutes, Others |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | Sartorius AG, Thermo Fisher Scientific Inc., Danaher Corporation, Merck KGaA, Eppendorf SE, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the single-use bioreactors market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the global single-use bioreactors market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's five forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the single-use bioreactors industry and its attractiveness.

- The competitive landscape allows stakeholders to understand their competitive environment and provides insight into the current positions of key players in the market.

Frequently Asked Questions About the Single-Use Bioreactors Market Report

The global single-use bioreactors market reached USD 4.38 Billion in 2025.

The market is projected to grow at a CAGR of 12.58%, reaching USD 13.12 Billion by 2034.

Key drivers include surging biopharmaceutical demand, cost and flexibility advantages over stainless steel infrastructure, cell and gene therapy manufacturing growth, CDMO capacity expansion, and continuous advancements in single-use bag, sensor, and control technology.

Single-use bioreactor systems dominate with a 46.8% product type share in 2025, representing complete bioreactor platforms inclusive of bags, control hardware, and process monitoring systems.

Wave-induced bioreactors are the fastest-growing type at ~13.8% CAGR during 2026–2034, driven by accelerating cell and gene therapy manufacturing adoption requiring gentle, low-shear cell expansion.

Stirred-tank bioreactors lead with a 51.2% type segment share in 2025, underpinned by superior mass transfer, broad cell line compatibility, and extensive regulatory precedent supporting biologics submissions.

North America leads with 39.1% global share in 2025, anchored by the United States biopharmaceutical manufacturing ecosystem and FDA regulatory facilitation of single-use technology adoption.

Asia-Pacific at 22.4% is the fastest-growing region, driven by China's biologics manufacturing expansion, India's biosimilar scale-up, and Thermo Fisher's Singapore facility investment.

Major players include Sartorius AG, Thermo Fisher Scientific Inc., Danaher Corporation, Merck KGaA, and Eppendorf SE.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)

Choose your plan

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Single User License

- 1 User License, Access on 2 Devices

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- No Printing Rights

- 10% Free Report Customization

- 10–12 Weeks of Analyst Support

Five User License

- Access for 5 Users, 2 Devices per User

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- Dedicated Account Manager

- 12–14 Weeks of Analyst Support

- No Printing Rights

- 15% Free Report Customization

- 25% Discount on Your Next Purchase

Corporate User License

- Unlimited User Access (Within Your Organization)

- PDF Report + Excel Dataset

- Lifetime Access

- Dedicated Account Manager

- 14–20 Weeks of Analyst Support

- No Printing Rights

- 20% Free Report Customization

- 30% Discount on Your Next Purchase

Essential Insights

What's included:

3 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 2 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Professional Access

What's included:

5 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 8 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Business Advantage

What's included:

8 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 14 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Enterprise Intelligence

What's included:

10 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 20 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade