Solar-Powered UAV Market Size, Share, Trends and Forecast by Type, Range, Component, Mode of Operation, Application, and Region, 2026-2034

Solar-Powered UAV Market Size and Share:

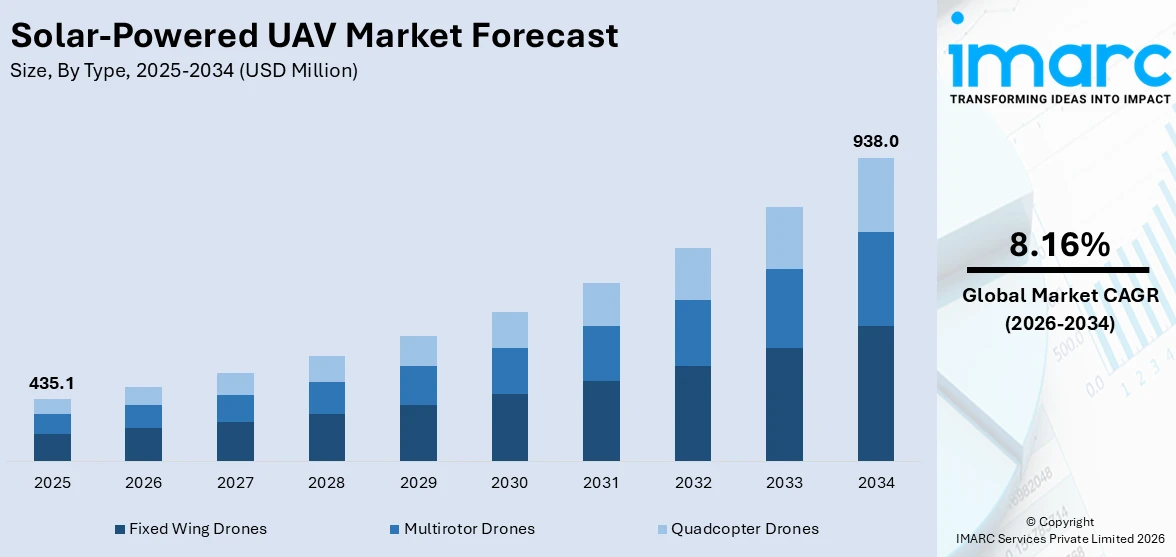

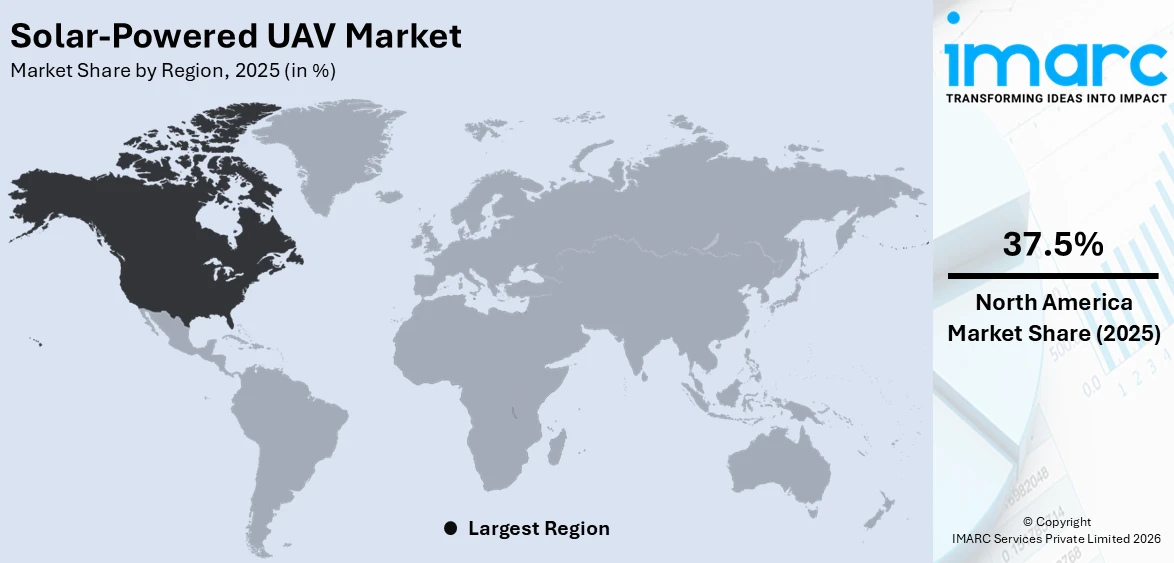

The global solar-powered UAV market size was valued at USD 435.1 Million in 2025. Looking forward, IMARC Group estimates the market to reach USD 938.0 Million by 2034, exhibiting a CAGR of 8.16% from 2026-2034. North America currently dominates the market, holding a market share of 37.5% in 2025. The region benefits from substantial government defense spending on unmanned aerial systems, robust aerospace research and development infrastructure, widespread commercial drone adoption across agriculture and energy sectors, and growing demand for long-endurance surveillance platforms, all contributing to the solar-powered UAV market share.

The rising demand for sustainable and long-endurance aerial platforms is a primary factor propelling the global solar-powered UAV market. Increasing adoption of unmanned aerial vehicles across defense, surveillance, agriculture, and environmental monitoring applications is generating significant demand for solar-powered alternatives that reduce reliance on conventional fuel sources. The integration of advanced photovoltaic cells and lightweight composite materials into UAV airframes has substantially improved flight endurance and payload capacity, making these platforms viable for extended missions. Furthermore, growing global emphasis on reducing carbon emissions in aviation operations is encouraging the development and deployment of clean energy-powered drones. The expanding use of solar-powered UAVs for border security, disaster management, telecommunications relay, and precision farming is broadening the addressable market. Rising defense modernization programs worldwide and increasing solar-powered UAV market growth are further augmenting demand for these advanced unmanned systems.

The United States has emerged as a major region in the solar-powered UAV market owing to many factors. The country's robust defense budget and strategic focus on unmanned systems modernization are catalyzing demand for solar-powered aerial platforms. Extensive government-funded research programs conducted by agencies such as DARPA and NASA continue to advance solar UAV propulsion and energy storage technologies. For instance, the Pentagon's fiscal year 2026 budget allocated USD 13.4 billion for autonomy and autonomous systems, including USD 9.4 billion specifically for unmanned and remotely-operated aerial vehicles, reflecting the strong institutional commitment to expanding drone capabilities. The expanding commercial drone sector in the United States, supported by regulatory frameworks from the Federal Aviation Administration, is further driving adoption of solar-powered UAVs across agriculture, infrastructure inspection, and environmental monitoring applications.

To get more information on this market Request Sample

Solar-Powered UAV Market Trends:

Rising Defense Sector Investments

Escalating defense budgets and the strategic prioritization of unmanned systems by governments worldwide are significantly boosting the adoption of solar-powered UAVs in military operations. Armed forces are increasingly deploying these platforms for persistent surveillance, intelligence gathering, reconnaissance, and communication relay missions, leveraging their ability to operate for extended durations without fuel resupply logistics. The growing emphasis on lightweight, low-observable drone platforms that can sustain high-altitude flights for days or weeks is further propelling demand. For instance, in October 2024, the Pentagon awarded USD 20 million through its Accelerate the Procurement and Fielding of Innovative Technologies program for Kraus Hamdani Aerospace K1000ULE solar-powered drones for the Army's 1st Multi-Domain Task Force and Joint Special Operations Command. These platforms are designed to silently glide through the air while generating clean onboard energy from wing-mounted solar panels, supporting extended missions across contested operational environments.

Advancements in Hybrid Propulsion Technologies

Continuous technological innovation in hybrid propulsion systems combining solar energy with advanced battery and hydrogen fuel cell technologies is transforming the capabilities of unmanned aerial vehicles. Manufacturers are developing multi-source energy architectures that dynamically manage power from photovoltaic arrays, rechargeable batteries, and fuel cells to maximize flight endurance and operational flexibility. These advancements are enabling solar-powered UAVs to sustain operations during nighttime hours and adverse weather conditions, overcoming a key limitation of purely solar-dependent systems. For instance, in July 2025, French aerospace companies XSun and H3 Dynamics announced the development of the first UAV powered by a combination of solar energy, hydrogen fuel cells, and battery storage. This tri-source electric propulsion system aims to significantly extend flight endurance for larger UAVs across diverse mission profiles, creating a positive solar-powered UAV market outlook. The ongoing maturation of these technologies continues to expand the operational scope and commercial viability of solar-powered drone platforms.

Expanding Agricultural Applications

The increasing utilization of solar-powered UAVs in the agricultural sector for precision farming, crop monitoring, pest detection, and resource optimization is driving substantial market expansion. These platforms offer significant advantages over conventional battery-powered drones by providing longer flight durations and lower operational costs, enabling comprehensive coverage of large agricultural areas. The integration of multispectral sensors and advanced data analytics with solar-powered UAV platforms is empowering farmers to make data-driven decisions for improved crop yields and resource management. For instance, in January 2026, India's Hindustan Petroleum Corporation Limited invested INR 2 crore in IIT Kanpur-incubated startup Maraal Aerospace to support development of India's first solar-powered long-endurance UAV designed for agricultural and infrastructure applications, offering up to 12 hours of endurance and a 150-kilometer operational range. This is creating a positive solar-powered UAV market forecast. The rapid adoption of drone-based agricultural solutions across developing economies is further expanding the commercial potential of solar-powered aerial platforms.

Solar-Powered UAV Industry Segmentation:

IMARC Group provides an analysis of the key trends in each segment of the global solar-powered UAV market, along with forecast at the global, regional, and country levels from 2026-2034. The market has been categorized based on type, range, component, mode of operation, and application.

Analysis by Type:

- Fixed Wing Drones

- Multirotor Drones

- Quadcopter Drones

Fixed wing drones holds 41.6% of the market share. Fixed wing solar-powered UAVs represent the most widely deployed configuration, leveraging their superior aerodynamic efficiency and large wing surface area to maximize solar energy absorption during extended flight operations. These platforms resemble small aircraft and offer significantly longer flight times and higher operational efficiency compared to rotary-wing alternatives, making them particularly well-suited for surveillance, mapping, and environmental monitoring missions. The integration of advanced photovoltaic arrays into wing structures enables continuous energy harvesting, while lightweight composite materials minimize airframe weight and drag. For instance, in December 2024, BAE Systems' PHASA-35 solar-powered HAPS aircraft completed stratospheric test flights, flying for 24 hours and climbing to more than 66,000 feet at Spaceport America in New Mexico, with the company targeting operational activity by 2026. Their ability to cover expansive geographical areas with minimal energy consumption makes fixed wing solar UAVs indispensable for long-range defense and commercial applications.

Analysis by Range:

- Less Than 300 KM

- More Than 300 KM

More than 300 KM leads the market with a share of 61.1%. Solar-powered UAVs capable of operating beyond the 300-kilometer range threshold are increasingly demanded across defense and commercial sectors due to their ability to conduct long-distance missions without frequent recharging or refueling. These extended-range platforms are particularly suited for border surveillance, pipeline monitoring, maritime patrol, and large-scale environmental surveys, where continuous coverage of vast areas is essential. The advancement of solar energy harvesting and battery storage technologies has substantially improved the range capabilities of these systems, reducing logistical constraints and operational costs. For instance, XSun's SolarXOne platform, featuring a distinctive tandem wing design with four solar wings generating up to 400 watts of power, achieves endurance of up to 12 hours and a range of 600 kilometers, enabling comprehensive beyond-visual-line-of-sight operations for infrastructure inspection and environmental monitoring. The growing requirement for persistent wide-area surveillance continues to strengthen demand for long-range solar-powered UAV platforms.

Analysis by Component:

- Propulsion System

- Airframe

- Guidance Navigation

- Control System

- Payload

Propulsion system dominates the market, with a share of 45.6%. The propulsion system represents the critical technological backbone of solar-powered UAVs, encompassing electric motors, solar panels, energy management systems, and onboard battery storage that collectively enable sustained autonomous flight. Continuous innovation in lightweight electric motor design, high-efficiency photovoltaic cells, and intelligent power management architectures is driving significant improvements in overall UAV performance and endurance. Manufacturers are developing increasingly sophisticated propulsion solutions that dynamically optimize energy harvesting, storage, and distribution to maximize operational efficiency across varying flight conditions and mission profiles. For instance, in 2025, Sesame Solar and Heven AeroTech announced the Drone Refueling Nanogrid, a trailer-sized mobile system that generates hydrogen fuel from solar power and atmospheric moisture, enabling military drones to operate continuously for up to six months in remote areas without fuel resupply. This ongoing advancement in propulsion technology is essential for expanding the operational capabilities of solar-powered UAV platforms.

Analysis by Mode of Operation:

- Semi-Autonomous

- Autonomous

Semi-autonomous represents the leading segment, with a market share of 57.8%. Semi-autonomous solar-powered UAVs combine solar energy harvesting with partial autonomous control capabilities, enabling pre-programmed flight paths and automated operations such as takeoff, landing, and navigation while retaining human oversight for mission-critical decision-making. This operational mode provides an optimal balance between automation and human control, meeting regulatory requirements while delivering extended flight durations that reduce operator workload. The growing preference for semi-autonomous configurations reflects the current regulatory landscape, where full autonomous operations remain subject to restrictive airspace management requirements in most jurisdictions. For instance, in January 2026, the Indian Army ordered the Medium Altitude Pseudo Satellite System solar-electric drone from NewSpace Research and Technologies, which demonstrated flights exceeding 27 hours at altitudes surpassing 26,000 feet at the Aeronautical Test Range in Chitradurga. The progressive evolution of semi-autonomous systems toward greater autonomy is supporting the continued expansion of this operational segment.

Analysis by Application:

Access the comprehensive market breakdown Request Sample

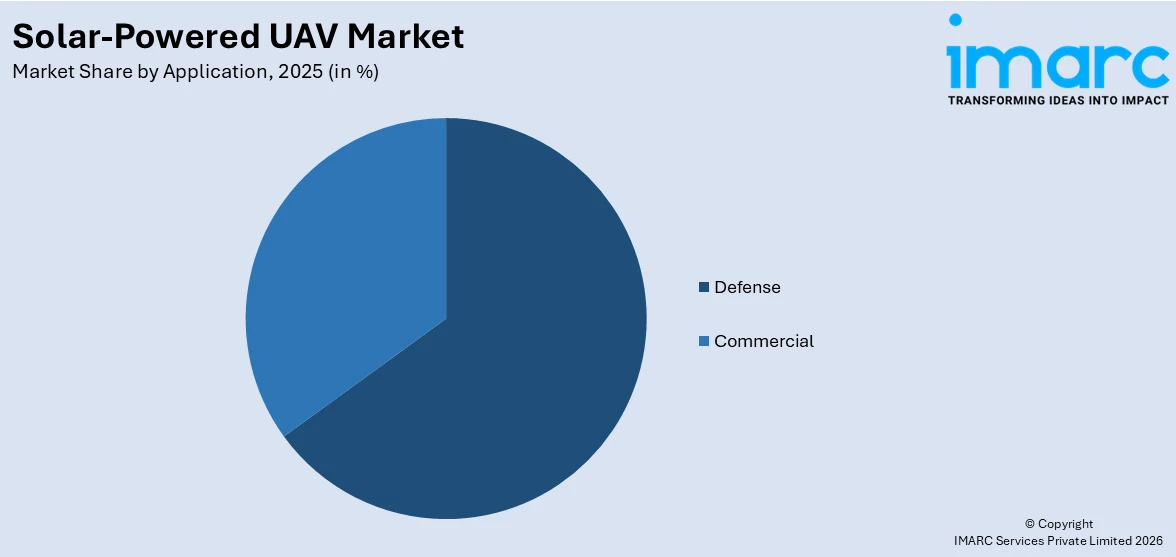

- Defense

- Commercial

Defense holds the dominant position in the solar-powered UAV market, accounting for 64.7% of the total market share. Military and defense organizations worldwide are increasingly deploying solar-powered UAVs for persistent surveillance, intelligence gathering, reconnaissance, communication relay, and border security operations, capitalizing on their extended flight endurance and reduced logistical footprint. These platforms offer significant strategic advantages by enabling continuous aerial coverage without the fuel supply constraints associated with conventional military drones, making them particularly valuable for operations in contested or remote environments. The growing emphasis on unmanned warfare and the increasing integration of solar-powered platforms into multi-domain operational concepts are further strengthening the defense application segment.

Regional Analysis:

To get more information on the regional analysis of this market Request Sample

- North America

- United States

- Canada

- Asia Pacific

- China

- Japan

- India

- South Korea

- Australia

- Indonesia

- Others

- Europe

- Germany

- France

- United Kingdom

- Italy

- Spain

- Russia

- Others

- Latin America

- Brazil

- Mexico

- Others

- Middle East and Africa

North America, accounting for 37.5% of the share, enjoys the leading position in the market. The region's dominance is driven by substantial government investment in defense modernization and unmanned systems development, robust aerospace research infrastructure, and strong commercial adoption of drone technologies across agriculture, energy, and telecommunications sectors. The United States military's strategic focus on expanding autonomous aerial capabilities, combined with significant funding through programs like APFIT and the Drone Dominance Initiative, is generating sustained demand for advanced solar-powered UAV platforms. For instance, in the fiscal year 2026, the Pentagon designated USD 13.4 billion specifically for autonomy and autonomous systems, with USD 9.4 billion allocated for unmanned and remotely-operated aerial vehicle development and procurement. The presence of leading defense contractors and innovative startups specializing in solar UAV technology further reinforces North America's position as the primary market for solar-powered unmanned aerial vehicles.

Key Regional Takeaways:

United States Solar-Powered UAV Market Analysis

The United States represents the dominant contributor to the North American solar-powered UAV market, driven by the country's expansive defense spending and strategic prioritization of unmanned aerial systems for military and homeland security applications. The Department of Defense's commitment to integrating autonomous platforms across air, land, and sea domains is generating significant procurement demand for advanced solar-powered UAVs capable of extended-endurance surveillance and reconnaissance missions. Federal agencies including DARPA and NASA continue to fund cutting-edge research programs exploring next-generation solar propulsion, energy storage, and autonomous flight control technologies. The growing commercial drone sector, supported by the Federal Aviation Administration's evolving regulatory framework for beyond-visual-line-of-sight operations, is expanding the addressable market for solar-powered UAV platforms in agriculture, infrastructure inspection, and environmental monitoring. For instance, the United States defense authorization for fiscal year 2026 allocated approximately USD 1.4 billion to expand the industrial base for drones and USD 500 million for the Defense Autonomous Warfare Group, demonstrating the strong institutional commitment to advancing unmanned capabilities. The combination of robust defense investment and commercial innovation continues to position the United States as the primary growth engine for the global solar-powered UAV market.

Europe Solar-Powered UAV Market Analysis

Europe represents a significant and rapidly growing market for solar-powered UAVs, driven by the region's increasing defense spending, strong commitment to sustainability, and expanding commercial drone applications. The European Union's strategic focus on defense autonomy and domestic drone manufacturing capabilities is generating substantial investment in unmanned aerial systems development and procurement. Countries including Germany, France, and the United Kingdom are leading regional adoption of solar-powered UAV platforms for military surveillance, agricultural monitoring, infrastructure inspection, and environmental conservation applications. The European Defence Fund's allocation of EUR 2.7 billion for collaborative defense research and development is supporting the advancement of specialized UAV technologies. For instance, in March 2025, the Netherlands announced a EUR 500 million investment in a large-scale drone project aimed at bolstering defense capabilities, as part of a broader EUR 2 billion aid package. The growing regulatory harmonization across EU member states for commercial drone operations, combined with increasing private sector investment in solar UAV technology, is supporting the continued expansion of the European market, with the solar-powered UAV market trends indicating strong regional growth potential.

Asia-Pacific Solar-Powered UAV Market Analysis

The Asia-Pacific region is experiencing robust growth in the solar-powered UAV market, driven by increasing defense modernization programs, expanding agricultural drone adoption, and growing investments in indigenous UAV development. Countries including China, India, Japan, and South Korea are actively pursuing solar-powered UAV technologies for military surveillance, border security, precision farming, and environmental monitoring applications. The region's diverse geographical landscape and varying environmental conditions make solar-powered UAVs particularly suitable for wide-area coverage and persistent operations. For instance, in late 2025, India's Defence Acquisition Council approved nearly INR 30,000 crore in additional drone acquisition. The growing emphasis on indigenous defense manufacturing and the increasing adoption of drone-based precision agriculture are strengthening the demand for solar-powered UAV platforms across the Asia-Pacific region.

Latin America Solar-Powered UAV Market Analysis

Latin America is gradually emerging as a promising market for solar-powered UAVs, with countries including Brazil and Mexico exploring unmanned aerial vehicle applications in agriculture, environmental monitoring, and border security operations. The region's extensive agricultural sector is increasingly adopting drone technology for precision farming, crop monitoring, and pest management, creating favorable conditions for solar-powered UAV deployment that offers extended flight durations and reduced operational costs. Growing government interest in utilizing unmanned systems for environmental protection, deforestation monitoring, and natural disaster response is further driving market development across the region.

Middle East and Africa Solar-Powered UAV Market Analysis

The Middle East and Africa region is witnessing growing interest in solar-powered UAV technologies, driven by increasing defense spending, strategic security requirements, and environmental monitoring needs. Countries across the Middle East are investing significantly in advanced unmanned aerial systems for border surveillance, counterterrorism operations, and critical infrastructure protection, leveraging the region's abundant solar irradiance conditions for optimal solar-powered UAV performance. The expanding adoption of drone technologies for oil and gas pipeline inspection, desert environmental monitoring, and agricultural applications is further supporting market development across the region.

Competitive Landscape:

The global solar-powered UAV market features a competitive landscape characterized by strategic collaborations, technological innovation, and increasing investment in research and development activities by key industry participants. Market players are focusing on advancing solar cell efficiency, lightweight composite materials, and hybrid energy management systems to enhance UAV flight endurance and operational capabilities. Companies are pursuing partnerships with defense agencies and commercial customers to expand their market presence and secure procurement contracts for next-generation solar-powered platforms. The growing emphasis on modular design approaches that enable rapid customization for diverse mission profiles is emerging as a key competitive differentiator. Several leading manufacturers are investing in the development of high-altitude pseudo-satellite platforms capable of stratospheric operations lasting weeks or months, targeting defense surveillance and telecommunications relay applications.

The report provides a comprehensive analysis of the competitive landscape in the solar-powered UAV market with detailed profiles of all major companies, including:

- BAE Systems Plc

- Barnard Microsystems Ltd

- Eos Technologie

- Sunlight Aerospace

- UAV Instruments S.L

- Xsun

Solar-Powered UAV Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Types Covered | Fixed Wing Drones, Multirotor Drones, Quadcopter Drones |

| Ranges Covered | Less Than 300 KM, More Than 300 KM |

| Components Covered | Propulsion System, Airframe, Guidance Navigation, Control System, Payload |

| Modes of Operation Covered | Semi-Autonomous, Autonomous |

| Applications Covered | Defense, Commercial |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | BAE Systems Plc, Barnard Microsystems Ltd, Eos Technologie, Sunlight Aerospace, UAV Instruments S.L, Xsun, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the solar-powered UAV market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the global solar-powered UAV market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's Five Forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the solar-powered UAV industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Solar-Powered UAV Market Report

The solar-powered UAV market was valued at USD 435.1 Million in 2025.

The solar-powered UAV market is projected to exhibit a CAGR of 8.16% during 2026-2034, reaching a value of USD 938.0 Million by 2034.

The growing demand for long-endurance unmanned aerial platforms in defense surveillance and reconnaissance operations, advancements in solar photovoltaic cell efficiency and lightweight composite materials, increasing adoption of drones in precision agriculture and environmental monitoring, and rising government investments in autonomous systems modernization are key factors driving the market.

North America currently dominates the solar-powered UAV market, accounting for a share of 37.5%. The region benefits from substantial defense spending on unmanned systems, robust aerospace research infrastructure, strong commercial drone adoption, and the presence of leading manufacturers driving continuous technological innovation.

Some of the major players in the solar-powered UAV market include BAE Systems Plc, Barnard Microsystems Ltd, Eos Technologie, Sunlight Aerospace, UAV Instruments S.L, Xsun, etc.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)