South Korea Cosmetics Market Report by Product Type, Category, Gender, Distribution Channel, and Region, 2026-2034

South Korea Cosmetics Market Size, Share, Trends & Forecast (2026-2034)

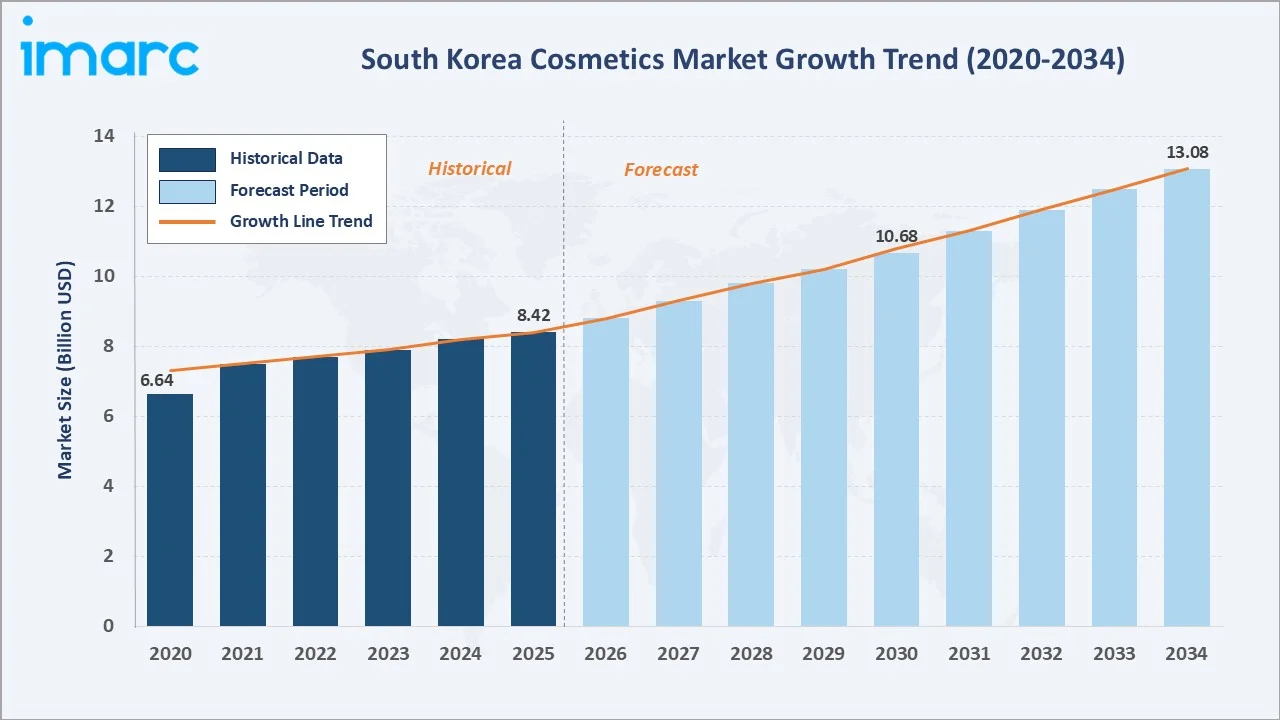

The South Korea cosmetics market size reached USD 8.42 Billion in 2025 and is projected to reach USD 13.08 Billion by 2034, exhibiting a CAGR of 4.87% during 2026-2034. Growing K-beauty global influence, rising disposable incomes, rapid e-commerce adoption, and government-backed export promotion are the primary forces driving the market.

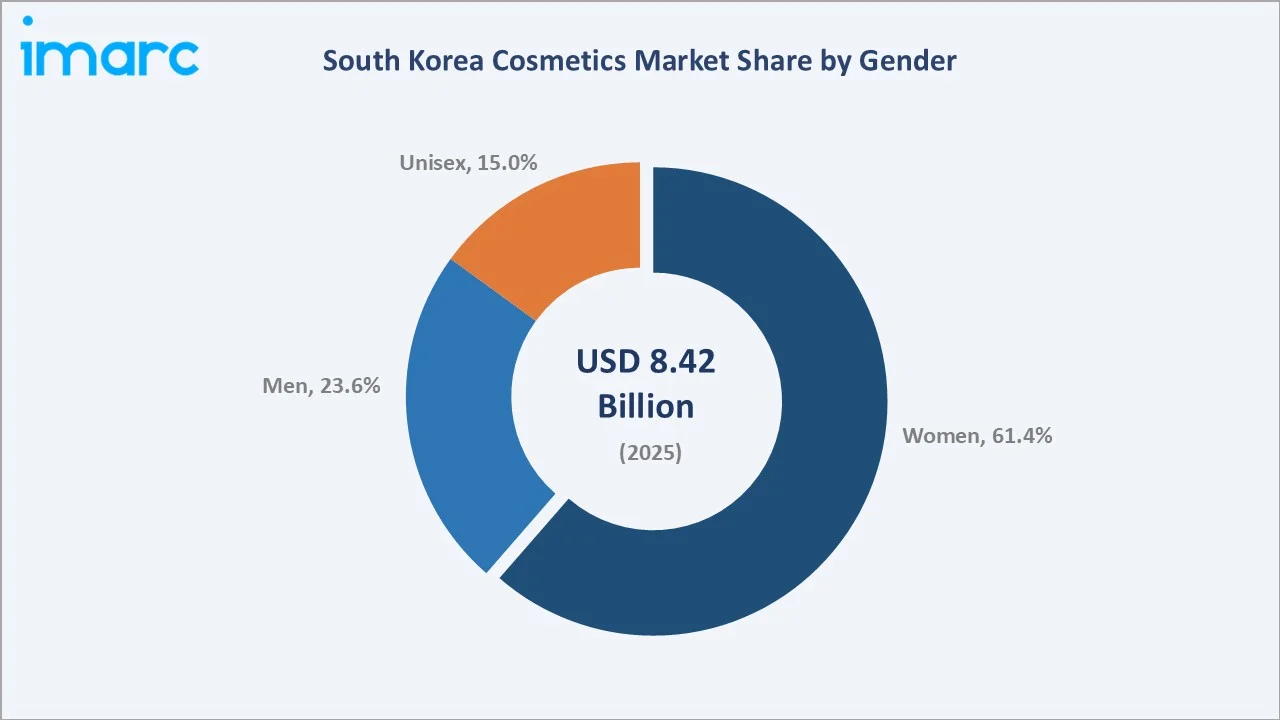

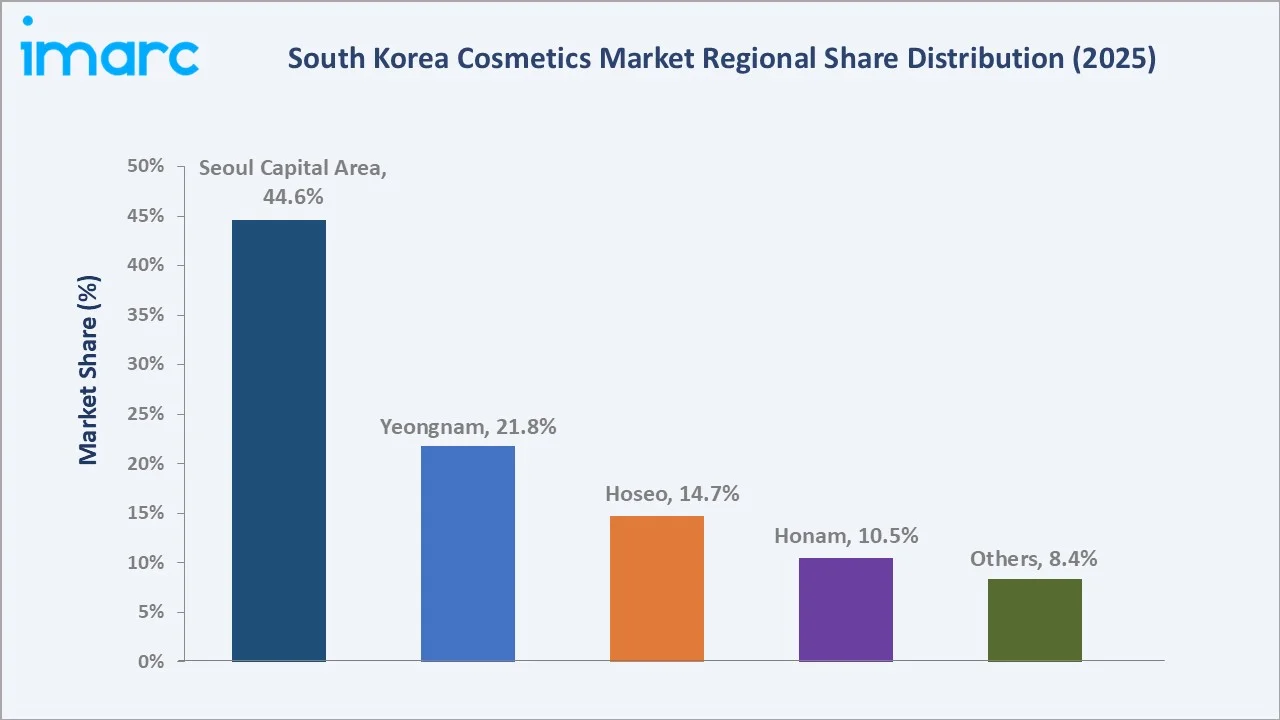

Women lead gender demand at 61.4%, skin and sun care products dominate at 46.8%, and Seoul Capital Area commands 44.6% regional share in 2025.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 8.42 Billion |

|

Forecast Market Size (2034) |

USD 13.08 Billion |

|

CAGR (2026-2034) |

4.87% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

Seoul Capital Area (44.6% share, 2025) |

|

Second Largest Region |

Yeongnam – Southeastern Region (21.8% share, 2025) |

|

Leading Gender Segment |

Women (61.4%, 2025) |

|

Leading Product Type |

Skin and Sun Care Products (46.8%, 2025) |

The South Korea cosmetics market growth trajectory from 2020 through 2034, with historical expansion to USD 8.42 Billion in 2025, reflects consistent demand for K-beauty products, while the forecast to USD 13.08 Billion captures accelerating premium skincare adoption and digital retail growth.

To get more information on this market, Request Sample

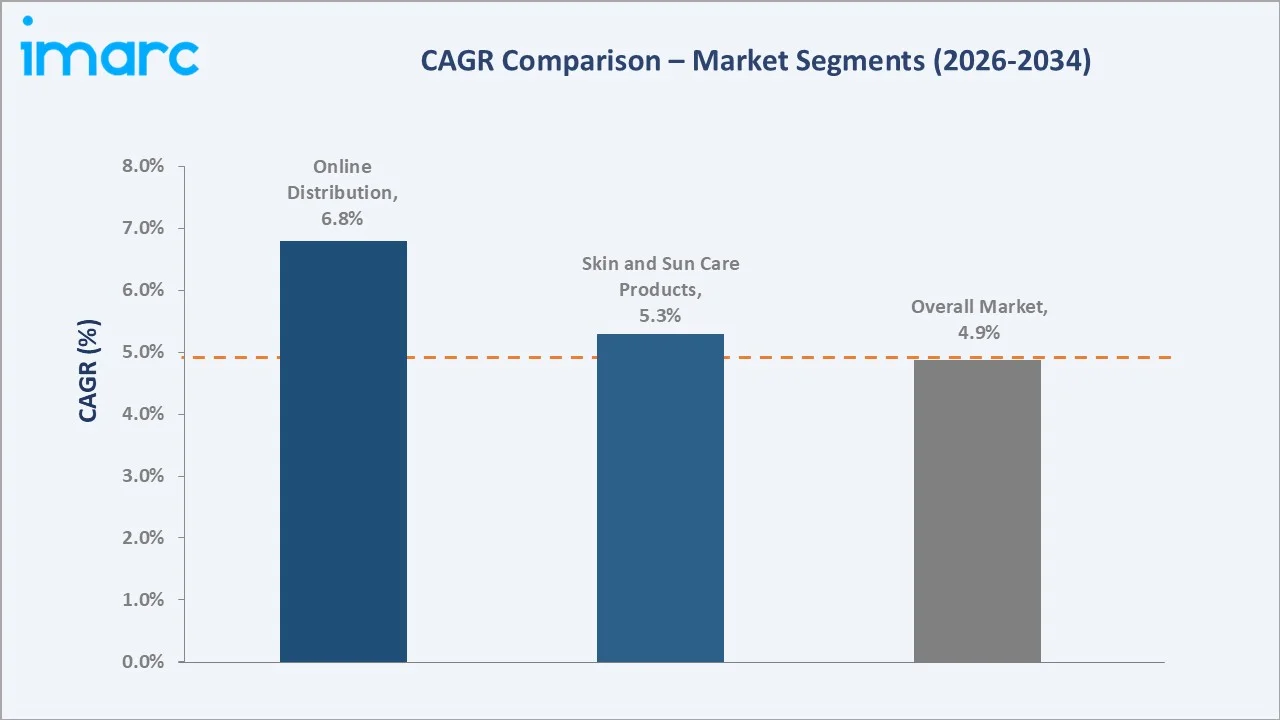

The CAGR trajectories across key gender, product type, and regional sub-segments, with skin and sun care products at ~5.3% CAGR and the online distribution channel at ~6.8% CAGR, are the fastest-growing categories within the South Korea cosmetics industry through 2034.

Executive Summary

The South Korea cosmetics market is on a sustained growth trajectory from USD 8.42 Billion in 2025 to USD 13.08 Billion by 2034. Cosmetics encompass skincare, makeup, hair care, and fragrance products used for personal care, grooming, and aesthetic enhancement, underpinned by Korea's globally recognized K-beauty innovation ecosystem.

Women represent the dominant consumer at 61.4% in 2025, driven by deeply ingrained multi-step skincare routines and high engagement with digital beauty content. Men's cosmetics at 23.6% constitute the fastest-growing gender segment as social norms evolve, while unisex products capture 15.0%.

Skin and sun care products lead product type at 46.8% in 2025, reflecting Korea's globally recognized skincare formulation expertise. SPF products, serums, and sheet masks drive the category. Makeup and color cosmetics at 21.7% follow, with K-pop aesthetic influence as the primary demand catalyst.

Seoul Capital Area commands 44.6% regional share in 2025, concentrated in Gangnam, Myeongdong, and Hongdae beauty districts. Yeongnam (21.8%) and Hoseo (14.7%) regions contribute through growing retail and manufacturing infrastructure.

Key Market Insights

|

Insight |

Data |

|

Leading Gender Segment |

Women – 61.4% share (2025) |

|

Second Gender Segment |

Men – 23.6% share (2025) |

|

Leading Product Type |

Skin and Sun Care Products – 46.8% share (2025) |

|

Second Product Type |

Makeup and Color Cosmetics – 21.7% share (2025) |

|

Leading Region |

Seoul Capital Area – 44.6% share (2025) |

|

Second Largest Region |

Yeongnam (Southeastern Region) – 21.8% share (2025) |

|

Top Companies |

Amorepacific, LG H&H Co., Ltd., Cosmax INC., Kolmar Korea., Able C&C., Clio Cosmetics |

Key Analytical Observations Expanding on the Above Data:

- Women's dominance at 61.4% in 2025 reflects Korea's deeply embedded multi-step skincare culture, where high frequency repurchase demand for cleansers, toners, essences, serums, and moisturizers sustains category volume and premiumization simultaneously.

- Skin and sun care products at 46.8% in 2025 dominate because UV protection is a non-negotiable daily requirement in Korean beauty culture, with SPF products accounting for approximately 28% of this category, driven by skin-brightening preferences and dermatologist guidance.

- Seoul Capital Area's 44.6% dominance reflects its concentration of flagship beauty retail, duty-free channels, and proximity to entertainment-industry trend generation that continuously refreshes consumer demand for new cosmetics categories.

- Men's cosmetics at 23.6% represents a structurally growing segment as K-pop idols normalize male grooming. BB creams, sunscreens, and tinted moisturizers lead male adoption, with per-consumer spending rising consistently each year since 2021.

South Korea Cosmetics Market Overview

Cosmetics in South Korea encompass skincare, color cosmetics, hair care, fragrances, and deodorants, formulated with advanced biotechnology, fermentation science, and traditional Oriental botanical ingredients. The Korean cosmetics ecosystem uniquely integrates heritage herbal formulation with modern AI-driven personalization, setting it apart from all other global cosmetics markets.

The domestic ecosystem spans ingredient suppliers, contract ODM/OEM manufacturers, brand owner-operators, multi-brand specialty retailers, e-commerce platforms, and export logistics networks. This integrated value chain enables rapid product innovation cycles—from formulation concept to market launch—that constitute a core K-beauty competitive advantage over international counterparts.

Market Dynamics

To evaluate market opportunities, Request Sample

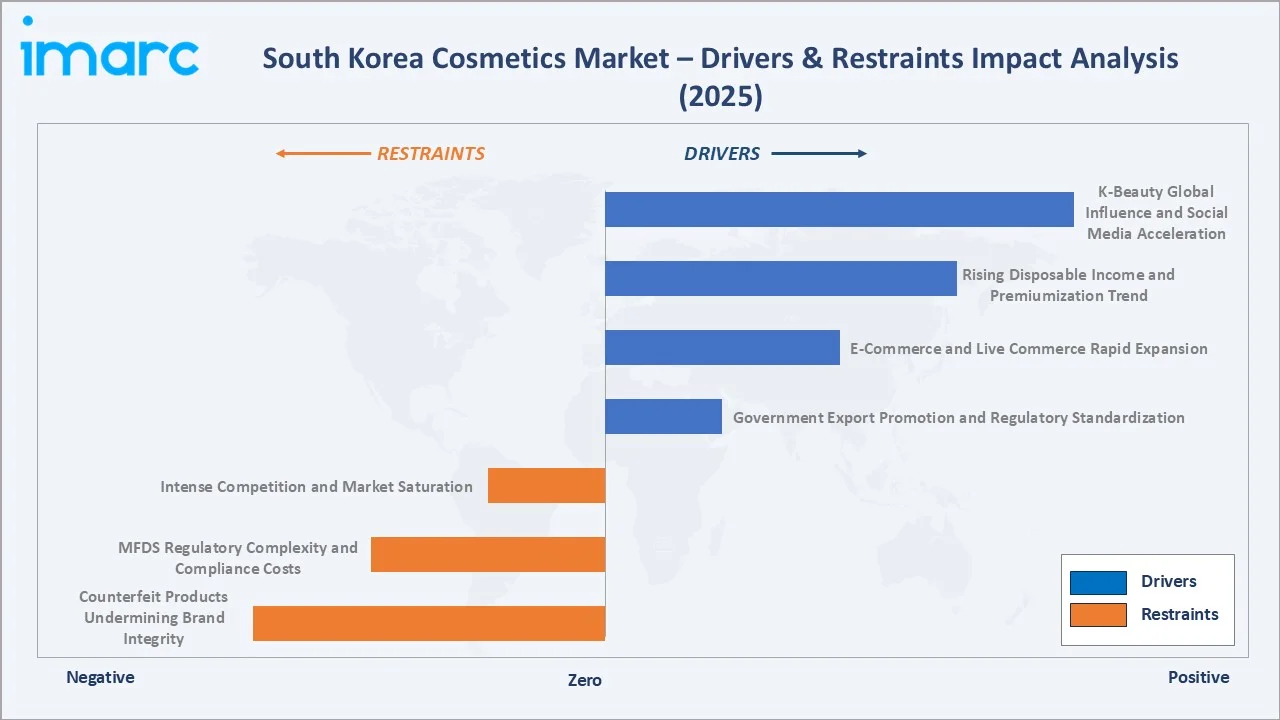

Market Drivers

- K-Beauty Global Influence and Social Media Acceleration: The global K-beauty wave, amplified by Korean pop culture, K-dramas, and beauty influencer content reaching hundreds of millions globally, is the dominant structural force driving sustained premium cosmetics demand both domestically and through export channels that reinforce domestic brand prestige.

- Rising Disposable Income and Premiumization Trend: South Korea's strong per capita income supports continued trading-up to premium skincare lines. Luxury serums and targeted treatment products are gaining domestic market traction, demonstrating robust premium demand across skin care, makeup, and hair care categories among urban consumers.

- E-Commerce and Live Commerce Rapid Expansion: Real-time interactive live commerce channels have transformed beauty product discovery and purchase. Online beauty category sales continue to grow strongly year-over-year, accelerating product trial for new indie brand launches and reaching consumers beyond major metropolitan areas.

- Government Export Promotion and Regulatory Standardization: Korea's MFDS cosmetics regulatory framework is internationally recognized, enabling faster market entry across ASEAN, Middle Eastern, and North American markets. Active free trade agreements covering numerous countries eliminate or reduce import duties, significantly improving export competitiveness of Korean beauty brands.

Market Restraints

- Intense Competition and Market Saturation: The Korea Cosmetics Association registered tens of thousands of cosmetics companies, creating extreme brand proliferation. Price competition from incoming foreign beauty platforms and private-label mass-market products erodes margins for mid-tier Korean brands unable to differentiate on technology or heritage storytelling.

- MFDS Regulatory Complexity and Compliance Costs: Frequent revisions to the Cosmetics Act, functional cosmetics notification requirements, and increasingly stringent ingredient safety evaluation protocols raise R&D and regulatory compliance costs. These barriers disproportionately affect smaller brands, limiting market diversity and slowing product innovation cycles.

- Counterfeit Products Undermining Brand Integrity: The proliferation of counterfeit K-beauty products sold through gray market channels in export markets damages brand equity, undermines pricing power, and erodes consumer trust in authentic Korean cosmetics, requiring significant brand protection and consumer education investment by legitimate manufacturers.

Market Opportunities

- Personalized Beauty and AI Diagnostics: AI-powered skin analysis platforms combining machine learning and clinical dermatology data enable hyper-personalized formulation recommendations. The personalized cosmetics segment is projected to grow strongly through 2034, representing a premium revenue opportunity for technology-forward brands investing in diagnostic beauty infrastructure.

- Men's Grooming Segment Expansion: With Korean men's cosmetics penetration high among younger age groups, the segment offers significant premiumization headroom. Brands launching dedicated men's skincare lines with performance-focused, dermatologically validated claims are capturing disproportionate share in this rapidly growing sub-segment.

Market Challenges

- Geopolitical Risks and Export Market Concentration: Significant dependence on a small number of export markets creates revenue concentration risk. Ongoing geopolitical sensitivities, domestic beauty brand nationalism in key export destinations, and trade friction create structural uncertainty for Korean beauty companies reliant on international demand.

- Sustainability Compliance and ESG Pressures: Growing consumer demand for cruelty-free certification, biodegradable packaging, and transparent ingredient sourcing adds formulation complexity and cost. Brands unable to credibly communicate sustainability claims face growing purchase resistance from environmentally conscious younger consumers who form the market's growth cohort.

Emerging Market Trends

1. AI-Powered Personalization and Smart Beauty Technology

AI-driven beauty personalization, combining facial scanning, skin microbiome analysis, and climate data, is reshaping product recommendation and formulation. Leading cosmetics companies have partnered with major technology platforms to launch AI-powered beauty counselors providing real-time personalized skin analysis and regimen recommendations.

2. Clean Beauty and Natural Ingredient Transparency

Consumer demand for ingredient-transparent, cruelty-free, and microbiome-friendly formulations is accelerating product reformulation. Traditional Korean herbal ingredients are gaining clinical validation, elevating their positioning from heritage inputs to scientifically substantiated efficacy actives across premium skincare categories.

3. Expansion of Men's Grooming and Gender-Inclusive Beauty

K-pop idols' normalization of male grooming has structurally shifted Korean men's cosmetics adoption. Brands launching gender-neutral formulations, unisex packaging, and performance-driven skin health claims are collectively capturing nearly 39% of the 2025 market across men's and unisex segments.

4. Cross-Border E-Commerce and Live Commerce Globalization

Korean beauty brands are leveraging global e-commerce and live selling platforms to reach consumers directly. Major beauty retail apps have surpassed millions of global downloads, while live commerce beauty categories continue recording strong double-digit growth annually, demonstrating digital retail's structural market role.

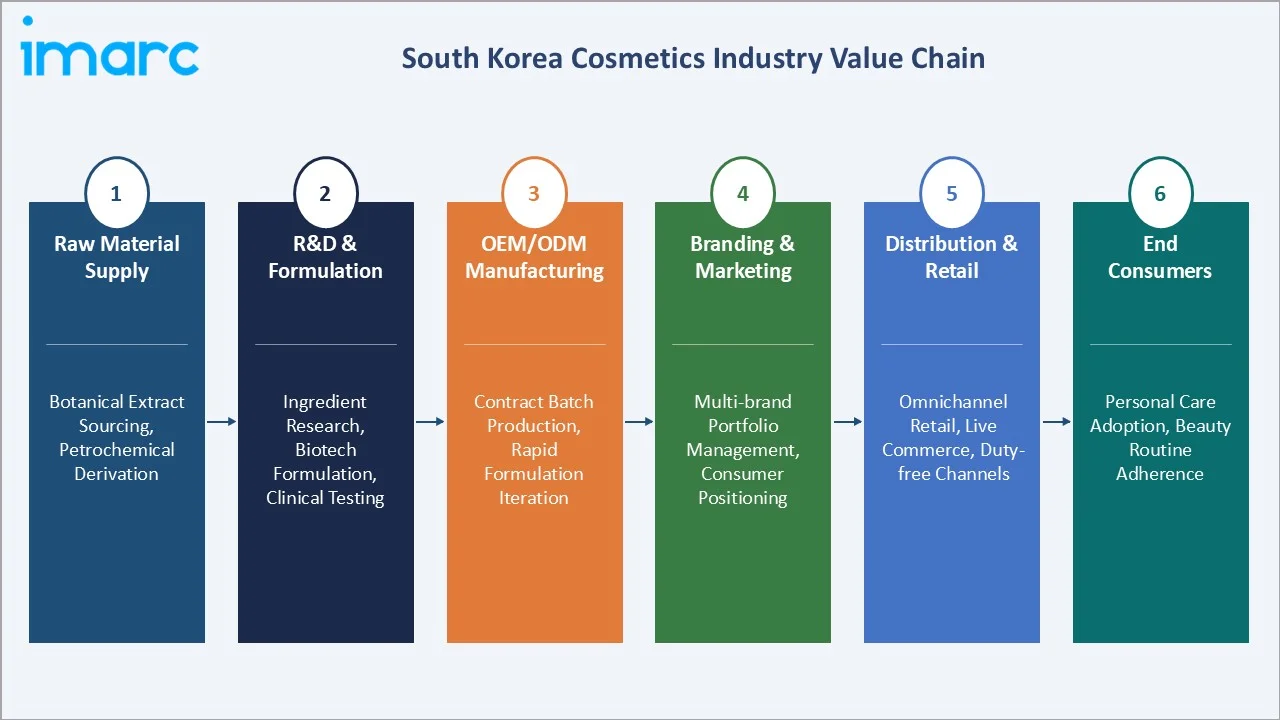

Industry Value Chain Analysis

The South Korea cosmetics value chain spans six stages from raw material supply through end-consumer delivery. R&D formulation and ODM manufacturing capture the highest value-add margins, while digital distribution and social commerce generate significant customer acquisition leverage for emerging and established brands alike.

|

Stage |

Key Activities |

|

Raw Material Supply |

Botanical extract sourcing, petrochemical derivation |

|

R&D & Formulation |

Ingredient research, biotech formulation, clinical testing |

|

OEM/ODM Manufacturing |

Contract batch production, rapid formulation iteration |

|

Branding & Marketing |

Multi-brand portfolio management, consumer positioning |

|

Distribution & Retail |

Omnichannel retail, live commerce, duty-free channels |

|

End Consumers |

Personal care adoption, beauty routine adherence |

Digital distribution and live commerce channels generate significant customer acquisition leverage, while duty-free retail and e-commerce platforms enable both domestic sales growth and international consumer reach.

Technology Landscape in the South Korea Cosmetics Industry

Biotechnology and Fermentation: Core Korean Innovation Platform

Fermentation technology transforms conventional herbal ingredients into bioavailable, microbiome-compatible actives. Korean cosmetics manufacturers hold thousands of cosmetics-related patents globally, with fermentation biotechnology representing a significant share of the active IP portfolio across leading conglomerates and mid-tier specialists.

AI and Data Analytics: Personalization Infrastructure

Machine learning-powered skin diagnosis platforms analyze dozens of skin parameters to generate individualized regimen recommendations. In-store AI mirror kiosks in flagship beauty retail destinations have processed millions of skin scans, generating high-conversion personalized sales with measurable basket value uplift.

Sustainable Formulation and Green Chemistry

Lab-grown and upcycled ingredients, including fermented marine extracts, agricultural by-product actives, and bioengineered hyaluronic acid, are reducing dependence on environmentally sensitive raw materials. Proprietary microbiome-safe formulation platforms enable brands to develop cleaner products within accelerated development cycles.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Product Type |

Skin and Sun Care Products |

46.8% |

2025 |

|

Category |

🔒 |

🔒 |

2025 |

|

Gender |

Women |

61.4% |

2025 |

|

Distribution Channel |

🔒 |

🔒 |

2025 |

|

Region |

Seoul Capital Area |

44.6% |

2025 |

By Gender

Women command a 61.4% majority share in 2025, driven by Korea's multi-step skincare culture and the global K-beauty phenomenon. The average South Korean female consumer maintains extensive daily skincare routines, sustaining high-frequency repurchase demand and strong premiumization across cleansers, toners, essences, and treatment serums.

To access detailed market analysis, Request Sample

Men's cosmetics at 23.6% in 2025 represent the fastest-growing gender sub-segment, with cultural acceptance of male grooming accelerated by entertainment industry influence. BB creams, tinted moisturizers, and SPF products are the primary entry points. Unisex products at 15.0% are gaining traction through gender-neutral branding and inclusive formulations targeting Gen Z consumers.

By Product Type

Skin and sun care products dominate at 46.8% in 2025 owing to Korea's globally recognized skincare expertise and cultural emphasis on skin health maintenance. The category encompasses cleansers, toners, essences, serums, moisturizers, and SPF products, with UV protection constituting the largest product subcategory driven by skin-brightening preferences and strong dermatological guidance.

Makeup and color cosmetics at 21.7% in 2025 benefit from entertainment aesthetic influence and the global popularity of Korean cushion compact, lip tint, and gradient blush techniques. Hair care at 14.6% addresses scalp health alongside styling. Deodorants and fragrances at 9.3% and other products at 7.6% complete the market mix.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

|

Seoul Capital Area |

44.6% |

Flagship beauty retail; duty-free beauty corridors; K-beauty brand headquarters |

|

Yeongnam (Southeastern) |

21.8% |

Major urban retail expansion; growing consumer spending; manufacturing base |

|

Hoseo (Central Region) |

14.7% |

R&D cluster proximity; distribution logistics; rising mid-tier brand presence |

|

Honam (Southwestern Region) |

10.5% |

Cultural tourism beauty economy; growing online retail penetration |

|

Others |

8.4% |

Ecotourism-linked skincare demand; regional indie brand growth |

Seoul Capital Area's 44.6% dominance in 2025 is driven by the highest concentration of flagship beauty stores, a thriving duty-free beauty corridor attracting international visitors, and proximity to entertainment companies whose idol culture continuously generates beauty trend demand and drives trial of new product categories.

Yeongnam (Southeastern Region) at 21.8% in 2025 is experiencing growing premium retail expansion in major urban centres, supported by rising disposable incomes and an expanding tourist beauty economy. Hoseo (Central Region) at 14.7% benefits from Korea's cosmetics manufacturing and R&D corridors, where ingredient suppliers and contract manufacturers concentrate, enabling strong distribution logistics access.

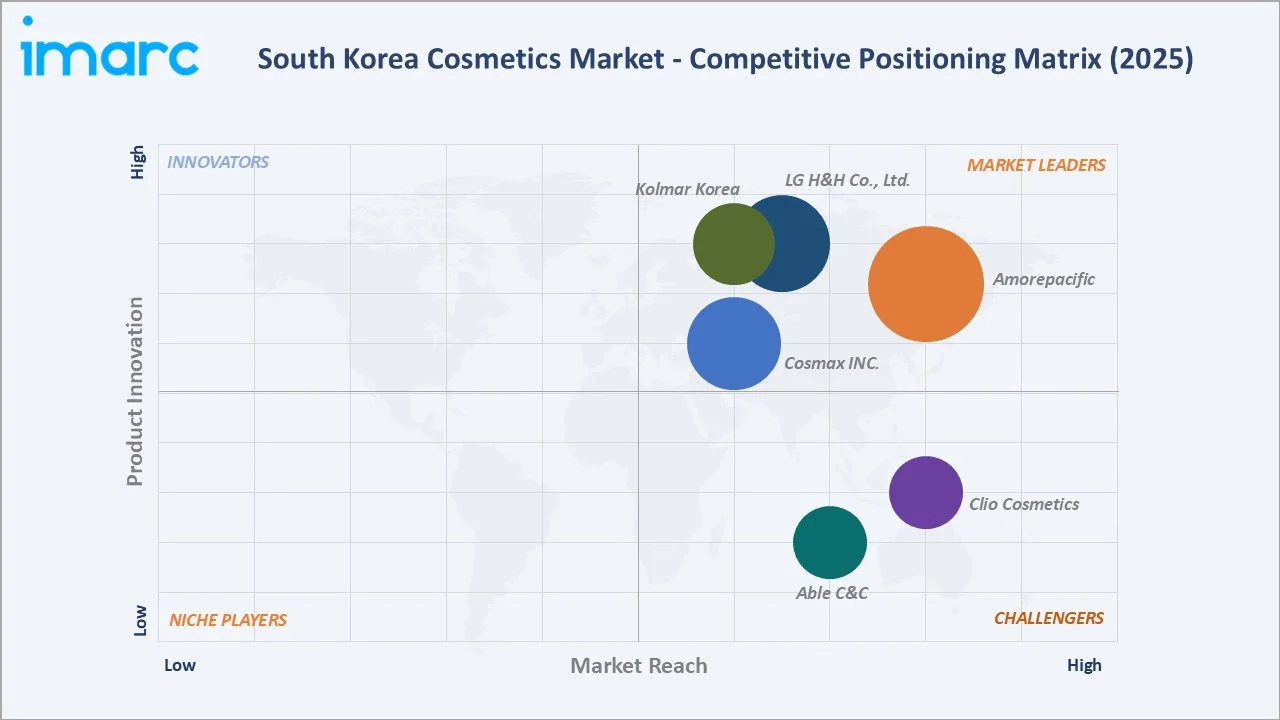

Competitive Landscape

The South Korea cosmetics market is moderately concentrated, with leading domestic conglomerates collectively commanding a significant domestic market value share. ODM manufacturers underpin the agility of hundreds of indie brands by providing rapid-cycle manufacturing at competitive cost structures, sustaining a dynamic multi-tier competitive ecosystem.

|

Company Name |

Key Products |

Market Position |

Strategic Focus |

| Amorepacific | Sulwhasoo, LANEIGE, INNISFREE, HERA, Primera, IOPE, Mamonde, HANYUL, espoir, ETUDE, ODYSSEY, HOLITUAL, Tata Harper, COSRX | Leader | Multi-brand K-beauty leadership; global expansion |

| LG H&H Co., Ltd. | VDL, Beyond, OHUI, The Face Shop, Isa Knox, The History of Whoo, SU:M37° | Leader | Luxury heritage positioning; premium channel focus |

| Cosmax INC. | ODM formulations across skincare, makeup, hair care | Leader | Global ODM manufacturing; rapid formulation cycles |

| Kolmar Korea | Toner, lotion, ampoule, essence, cream, mask sheet, mask pack, and lip balm, Makeup base, primer, foundation/concealer(liquid), cushion foundation, and mascara | Leader | ODM manufacturing; North America capacity expansion |

| Able C&C | MISSHA, A’pieu, CHOGONGJIN, Stila, Cellapy | Challenger | Digital-first; accessible pricing; SEA expansion |

| Clio Cosmetics | CLUBCLIO, CLIO, peripera, goodal, Dermatory, Healing Bird | Challenger | Multi-brand; Gen Z targeting; online-first strategy |

Key players include Amorepacific, LG H&H Co., Ltd., Cosmax INC., Kolmar Korea., Able C&C., Clio Cosmetics, and others.

Key Company Profiles

Amorepacific

Amorepacific is South Korea's largest cosmetics conglomerate, operating a diverse portfolio of premium and accessible beauty brands across skincare, makeup, hair care, and fragrance categories. The company commands a leading position in the domestic market and has built substantial international presence across Asia, North America, and Europe through flagship retail and digital commerce channels.

- Product Portfolio: Offers Sulwhasoo, LANEIGE, INNISFREE, HERA, Primera, IOPE, Mamonde, HANYUL, espoir, ETUDE, ODYSSEY, HOLITUAL, Tata Harper, COSRX, and others

- Recent Developments: In May 2026, Amorepacific developed a next-generation nano-delivery technology for cosmetics in collaboration with the Korea Advanced Institute of Science and Technology (KAIST). The company stated that the newly developed technology enables the creation of approximately 20nm-sized nano carriers that maintain structural stability while enhancing the penetration of active ingredients into deeper layers of the skin.

- Strategic Focus: Amorepacific's strategy leverages its multi-brand architecture to serve premium-to-accessible consumer segments simultaneously, while investing in biotech R&D to develop next-generation active ingredients. The company is expanding direct-to-consumer digital channels globally, targeting premium skincare consumers in high-growth international markets.

LG H&H Co., Ltd.

LG H&H Co., Ltd. is South Korea's second-largest cosmetics company, operating across cosmetics, home care, and beverages. Its luxury cosmetics portfolio is anchored in premium Oriental medicine-inspired skincare and modern fermentation-based brands, with particularly strong positioning in duty-free and department store channels targeting high-value domestic and international consumers.

- Product Portfolio: Offers VDL, Beyond, OHUI, The Face Shop, Isa Knox, The History of Whoo, SU:M37°, and others.

- Recent Developments: In May 2025, LG H&H completed the acquisition of U.S.-based beauty brand The Crème Shop by purchasing the remaining 35% stake in the company for approximately USD 67 million. The transaction gives LG H&H full ownership of the Los Angeles-based cosmetics and skincare company, further strengthening its presence in the North American beauty market.

- Strategic Focus: LG H&H differentiates through luxury heritage positioning, targeting premium consumer segments in Korea and key international markets through duty-free channels, flagship stores, and premium department store counters. The company continues investing in premium brand storytelling and cultural narrative to command price premiums.

Market Concentration Analysis

The South Korea cosmetics market is moderately concentrated at the brand ownership level, with leading domestic conglomerates collectively representing a significant share of domestic market value, while remaining highly fragmented among tens of thousands of registered companies. The ODM manufacturing layer reduces barriers to brand creation, sustaining continuous indie brand entry.

Regional concentration is most pronounced in Seoul Capital Area, where flagship store presence, duty-free channel access, and digital marketing infrastructure create meaningful competitive advantages. Consolidation through M&A is increasing, with global beauty majors acquiring Korean specialist brands, reflecting the market's strategic attractiveness for international portfolio diversification.

Investment & Growth Opportunities

Fastest-Growing Segments

Men's cosmetics is the highest-growth gender segment through 2034. Online and live commerce distribution channels represent the fastest-growing retail format. Organic and natural category formulations address a structurally growing clean beauty consumer preference across both domestic and export markets.

Emerging Markets Within South Korea

Regional beauty tourism destinations built around unique local natural ingredients present premium positioning opportunities for heritage-driven skincare brands. Government investment in natural cosmetics clusters is developing globally recognized natural ingredient origin appellations, attracting both domestic and international cosmetics brand investment into regional ingredient sourcing.

Venture & Investment Trends

Private equity and strategic investment in Korean indie beauty brands is accelerating, with significant K-beauty brand funding activity in recent years. Cross-border e-commerce infrastructure, AI beauty-technology platforms, and sustainable packaging companies are attracting VC capital as the K-beauty export economy scales globally.

Future Market Outlook (2026-2034)

The South Korea cosmetics market is forecast to expand from USD 8.42 Billion in 2025 to USD 13.08 Billion by 2034 at a CAGR of 4.87%, adding USD 4.66 Billion in incremental annual market value. This sustained growth reflects structural K-beauty demand expansion, digital retail adoption, and men's grooming normalization across age groups.

Three forces will most significantly shape the market through 2034: AI-driven personalization creating a new customized cosmetics category commanding price premiums; the global K-beauty expansion reinforcing domestic brand prestige; and biotechnology innovations in fermentation and microbiome science generating ingredient differentiation that is difficult to replicate at commodity price points by international competitors.

Research Methodology

Primary Research

Primary research encompassed structured interviews with South Korea cosmetics industry stakeholders, including brand managers at leading Korean cosmetics companies, ODM procurement specialists, specialty beauty retail category managers, digital beauty platform executives, and regulatory advisors. Primary data validated market sizing, segment shares, regional demand estimates, and technology adoption timelines.

Secondary Research

Key secondary sources include Korea Cosmetics Association industry data, MFDS cosmetics market surveillance reports, Korea Customs Service export statistics, Korea International Trade Association trade flow data, Statistics Korea consumer expenditure surveys, and trade publications covering cosmetics and beauty industry developments, formulation science, and packaging innovation.

Forecasting Models

Market size estimations and growth projections were derived using top-down and bottom-up forecasting models, incorporating GDP growth rates, cosmetics penetration benchmarks, e-commerce adoption curves, and historical market evolution patterns. Scenario analysis covering base, optimistic, and conservative cases was performed to account for geopolitical and regulatory risk factors.

South Korea Cosmetics Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical and Forecast Trends, Industry Catalysts and Challenges, Segment-Wise Historical and Predictive Market Assessment:

|

| Product Types Covered | Skin and Sun Care Products, Hair Care Products, Deodorants and Fragrances, Makeup and Color Cosmetics, Others |

| Categories Covered | Conventional, Organic |

| Genders Covered | Men, Women, Unisex |

| Distribution Channels Covered | Supermarkets and Hypermarkets, Specialty Stores, Pharmacies, Online Stores, Others |

| Regions Covered | Seoul Capital Area, Yeongnam (Southeastern Region), Honam (Southwestern Region), Hoseo (Central Region), Others |

| Companies Covered | Amorepacific, LG H&H Co., Ltd., Cosmax INC., Kolmar Korea, Able C&C, Clio Cosmetics, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the South Korea cosmetics market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the South Korea cosmetics market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the South Korea cosmetics industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the South Korea Cosmetics Market Report

The South Korea cosmetics market reached USD 8.42 Billion in 2025, driven by K-beauty global popularity, rising disposable incomes, and rapid e-commerce adoption across domestic and export channels.

The market is projected to reach USD 13.08 Billion by 2034, growing at a CAGR of 4.87% during 2026-2034, driven by premiumization, men's grooming expansion, and AI-powered beauty personalization.

Women lead with a 61.4% share in 2025, reflecting deeply embedded multi-step skincare culture, with men representing the fastest-growing segment at 23.6% through expanding grooming culture acceptance.

Skin and sun care products dominate at 46.8% in 2025, driven by Korea's global skincare formulation expertise, SPF product cultural importance, and high usage frequency of serums and essences in daily routines.

Seoul Capital Area commands 44.6% market share in 2025, driven by flagship beauty retail concentration, a major duty-free beauty corridor, and proximity to the entertainment industry that continuously generates beauty trends.

Online stores and live commerce platforms are the fastest-growing channels, driven by interactive live selling platforms, beauty-focused e-commerce apps, and social commerce enabling direct brand-to-consumer transactions at scale.

Leading companies include Amorepacific, LG H&H Co., Ltd., Cosmax INC., Kolmar Korea., Able C&C., Clio Cosmetics, and others.

Key challenges include intense brand competition, MFDS regulatory compliance complexity, counterfeit products undermining brand equity, and geopolitical risks associated with concentration of exports to specific international markets.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)