South Korea Luxury Goods Market Size, Share, Trends and Forecast by Type, Distribution Channel, and Region, 2026-2034

South Korea Luxury Goods Market Size, Share, Trends & Forecast (2026-2034)

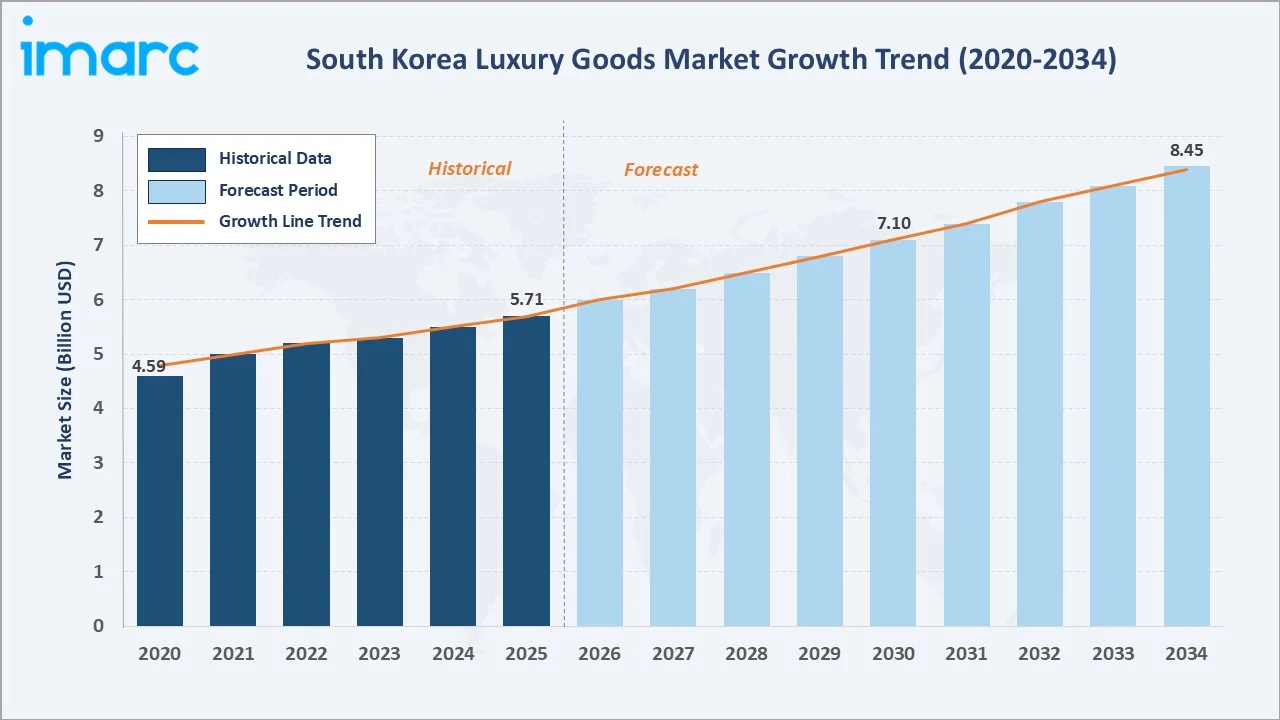

The South Korea luxury goods market size reached USD 5.71 Billion in 2025 and is projected to reach USD 8.45 Billion by 2034, exhibiting a CAGR of 4.47% during 2026-2034. Rising affluence among South Korea's millennial and Gen Z cohorts, strong brand consciousness, Hallyu-amplified aspirational demand, and expanding single-brand flagship retail are the primary growth forces.

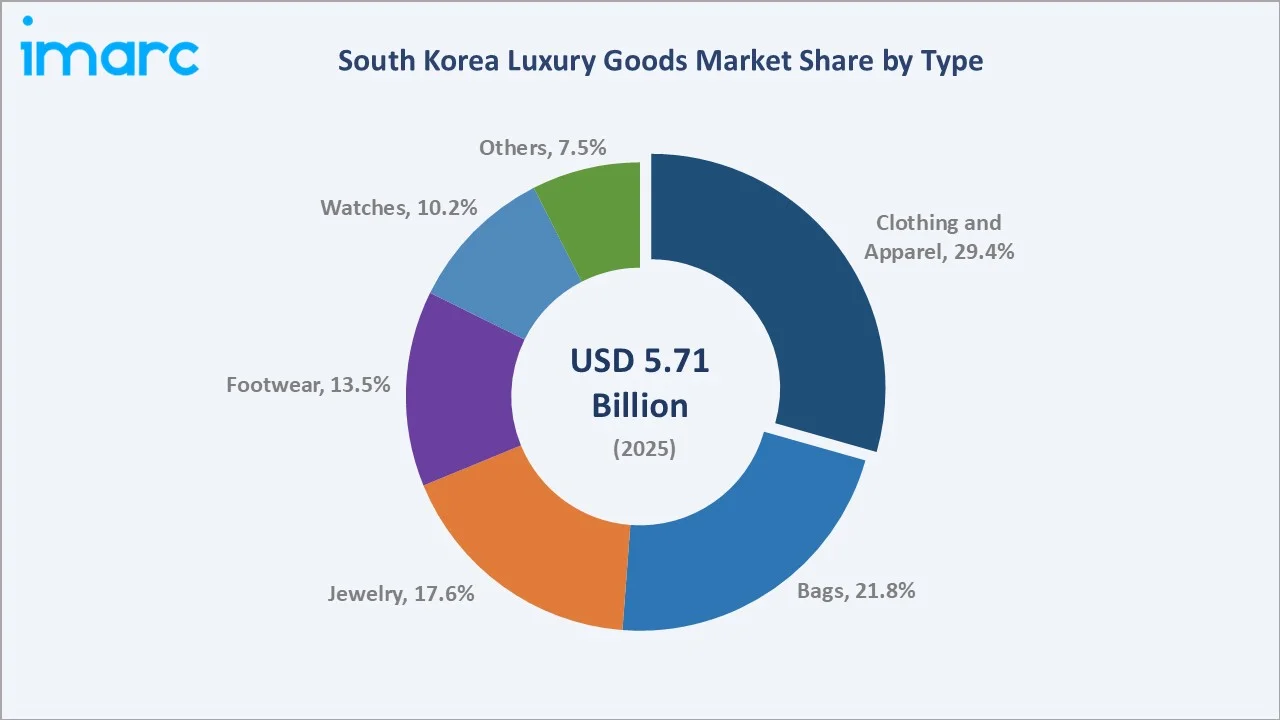

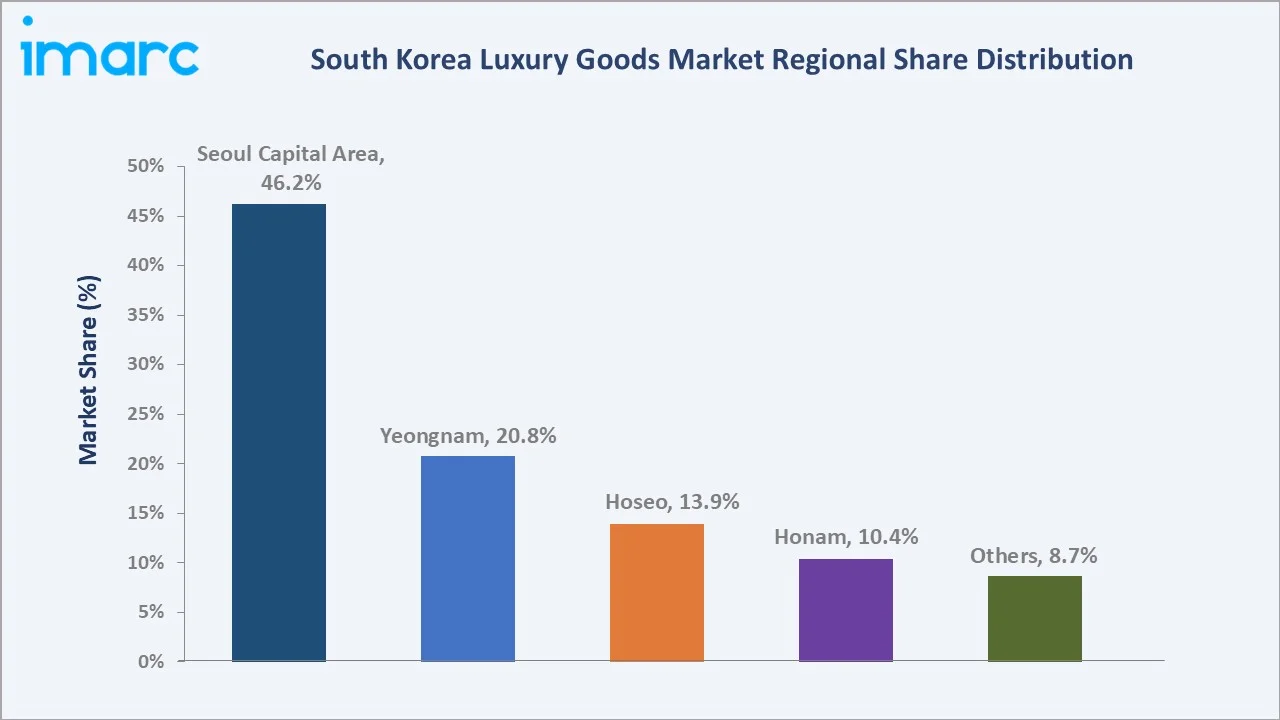

Clothing and Apparel leads type at 29.4% in 2025, Single-Brand Stores lead distribution at 38.6%, and Seoul Capital Area commands 46.2% regional share, reflecting its unparalleled concentration of luxury retail and high-income consumers.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 5.71 Billion |

|

Forecast Market Size (2034) |

USD 8.45 Billion |

|

CAGR (2026-2034) |

4.47% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Type |

Clothing and Apparel (29.4% share, 2025) |

|

Leading Distribution Channel |

Single-Brand Stores (38.6% share, 2025) |

|

Leading Region |

Seoul Capital Area (46.2% share, 2025) |

The South Korea luxury goods market trajectory from 2020 through 2034, with historical expansion to USD 5.71 Billion in 2025, reflects consistent demand driven by a growing affluent consumer base and sustained brand loyalty. The forecast to USD 8.45 Billion by 2034 captures accelerating digital luxury commerce, premiumization trends, and Seoul's growing stature as a globally recognized luxury capital.

To get more information on this market, Request Sample

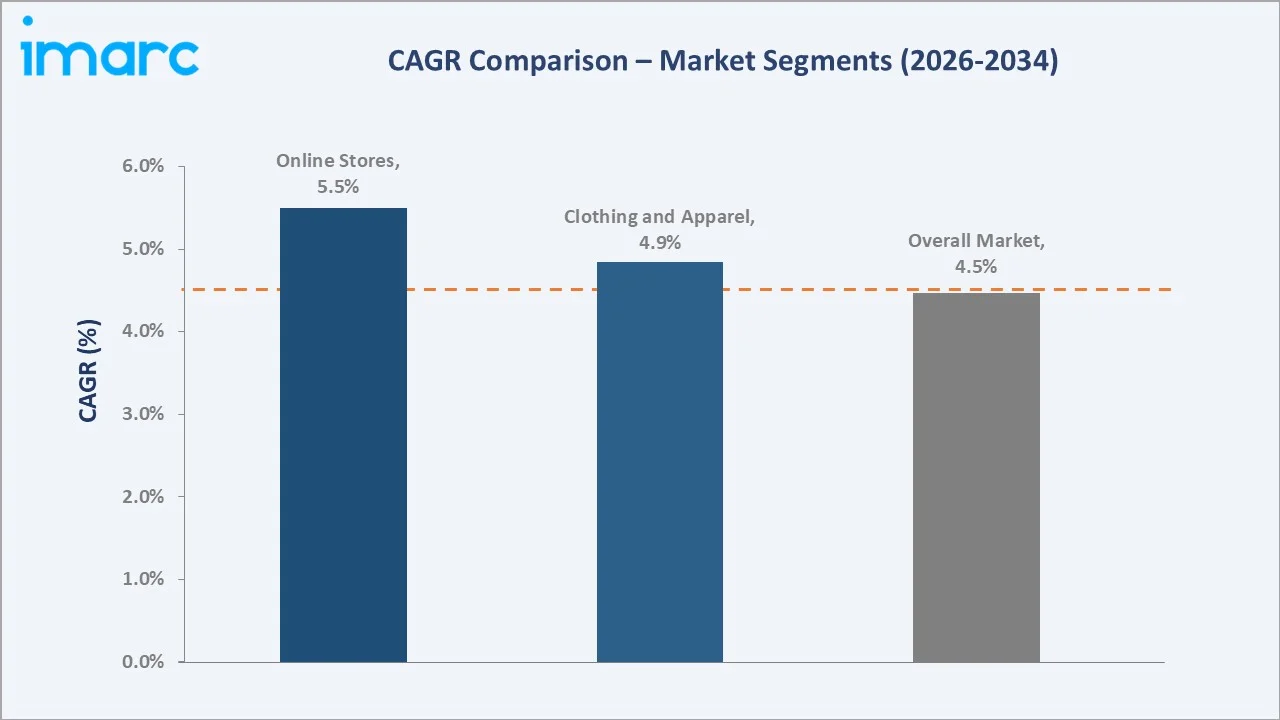

The CAGR trajectories across key type, distribution channel, and regional sub-segments highlight Online Stores at approximately 5.5% CAGR and Clothing and Apparel at approximately 4.85% CAGR as the fastest-growing categories within the South Korea luxury goods market analysis through 2034.

Executive Summary

The South Korea luxury goods market is on a sustained growth trajectory from USD 5.71 Billion in 2025 to USD 8.45 Billion by 2034. Luxury goods, comprising high-end fashion, premium accessories, fine jewelry, luxury watches, and designer footwear, benefit from aspirational consumption and status-driven purchasing behavior among Korean consumers across a widening demographic base.

Clothing and Apparel leads type at 29.4% in 2025 due to its broad product range and strong brand association with European fashion houses. Bags (21.8%) command premium positioning with iconic styles generating high repeat purchase intent. Jewelry (17.6%) grows on occasion-driven gifting and investment purchasing, while Footwear (13.5%) and Watches (10.2%) serve complementary luxury consumer needs.

Single-Brand Stores lead distribution at 38.6% in 2025, driven by consumers' preference for immersive brand experiences and personalized service in flagship retail environments. Online Stores (21.3%) are the fastest-growing channel, powered by Korea's digitally native millennial and Gen Z consumers who demand authenticated and seamless digital luxury retail access.

Seoul Capital Area dominates at 46.2% in 2025, home to the country's densest concentration of luxury flagships and premier retail corridors. Yeongnam (20.8%) follows, supported by industrial wealth and an expanding affluent consumer base in Korea's southeastern metropolitan clusters.

Key Market Insights

|

Insight |

Data |

|

Largest Type |

Clothing and Apparel – 29.4% share (2025) |

|

Leading Distribution Channel |

Single-Brand Stores – 38.6% share (2025) |

|

Leading Region |

Seoul Capital Area – 46.2% share (2025) |

|

Second Region |

Yeongnam (Southeastern Region) – 20.8% share (2025) |

|

Top Companies |

Kering, Compagnie Financière Richemont SA, Hermès, DINT, ELIE SAAB |

Key Analytical Observations Expanding on the Above Data:

- Clothing and Apparel, at 29.4% in 2025, dominates because Korean consumers allocate significant discretionary spend to fashion items that signal taste and social standing. The Korean Wave continuously amplifies global luxury fashion appeal through high-reach celebrity endorsements and media-driven aspirational imagery that reinforces brand desirability across consumer cohorts.

- Single-Brand Stores, at 38.6% in 2025, lead distribution because luxury consumers in South Korea demand curated, immersive brand experiences. Flagship stores in premium retail districts offer exclusive events, personalized styling services, and VIP programs that build long-term brand loyalty and drive repeat high value purchases unavailable in multi-brand environments.

- Seoul Capital Area's 46.2% dominance reflects the city's role as Northeast Asia's premier luxury retail hub, with iconic retail corridors and luxury department store galleries attracting both domestic affluent consumers and high-spending international visitors seeking concentrated, authenticated brand experiences within an internationally recognized shopping destination.

- Online Stores, growing at approximately 5.5% CAGR, are accelerated by tech-savvy Gen MZ consumers who prefer authenticated digital luxury platforms offering seamless purchase journeys, exclusive digital-first releases, and integrated social commerce features that combine discovery with direct transaction capabilities in familiar digital environments.

South Korea Luxury Goods Market Overview

The South Korea luxury goods market encompasses designer fashion, premium accessories, luxury watches, fine jewelry, and high-end footwear marketed by globally recognized luxury maisons and aspirational lifestyle brands. The market structure integrates department store luxury galleries, single-brand flagships, duty-free retail channels, and rapidly growing digital commerce platforms serving a sophisticated and brand-conscious consumer base.

The ecosystem integrates global luxury conglomerates, domestic Korean department store operators, duty-free channel operators, authenticated online luxury platforms, and end consumers spanning upper-income millennials, corporate and occasion-based purchasers, and inbound luxury tourists visiting South Korea's premier retail destinations in the capital and major regional cities.

Market Dynamics

To evaluate market opportunities, Request Sample

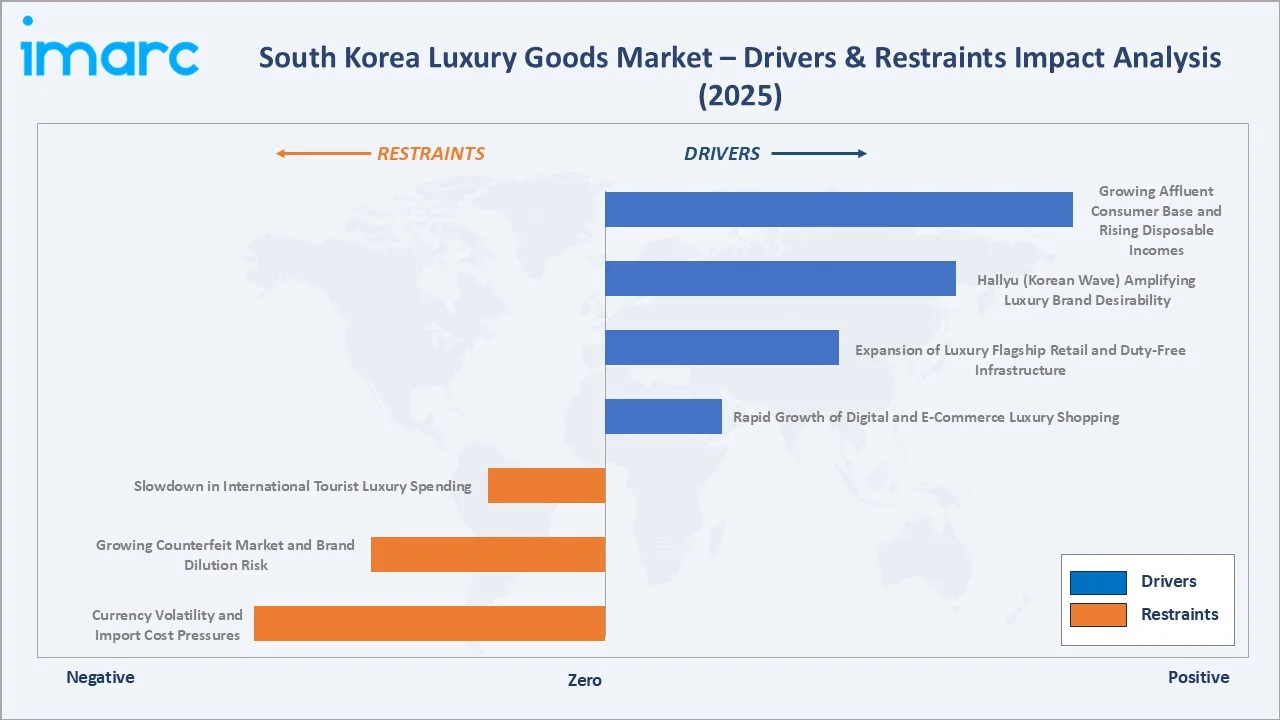

Market Drivers

- Growing Affluent Consumer Base and Rising Disposable Incomes: South Korea's robust economic growth, high per-capita income levels, and expanding high-net-worth individual population provide the primary demand foundation for premium and ultra-luxury goods. Rising household affluence enables consistent discretionary spending on aspirational branded fashion, accessories, jewelry, and watches across an increasingly broad and demographically diverse consumer base in South Korea.

- Hallyu (Korean Wave) Amplifying Luxury Brand Desirability: K-pop artists and Korean drama celebrities serving as brand ambassadors for leading luxury houses generate mass cultural endorsement and aspirational demand that operates both domestically and globally. Korean celebrity collaborations create significant social media engagement, elevate brand visibility and purchase intent, and continuously reinforce the luxury market's aspirational appeal among younger Korean consumer cohorts.

- Expansion of Luxury Flagship Retail and Duty-Free Infrastructure: South Korea maintains one of the world's most developed duty-free luxury markets, and the continued expansion of luxury flagship retail in premier metropolitan corridors provides a growing omnichannel retail footprint for global luxury brands. This infrastructure growth creates more brand touchpoints, increases accessibility to luxury purchase occasions, and supports both domestic consumer and tourist-driven luxury spending across the country.

- Rapid Growth of Digital and E-Commerce Luxury Shopping: The integration of authenticated luxury e-commerce platforms, brand-owned digital stores, and social commerce features is fundamentally transforming luxury accessibility in South Korea. High smartphone penetration, advanced digital payments infrastructure, and tech-savvy consumer behavior accelerate online luxury adoption, expanding the addressable consumer base well beyond traditional brick-and-mortar retail geography constraints.

Market Restraints

- Currency Volatility and Import Cost Pressures: As South Korea imports most of its luxury goods from European manufacturing origins, Korean Won depreciation against the Euro and US Dollar directly increases product cost bases for luxury brands operating in the country. This creates pressure on brand margins or necessitates retail price increases that may soften volume growth among price-sensitive aspirational consumer segments within the broader South Korean luxury market.

- Growing Counterfeit Market and Brand Dilution Risk: South Korea's proximity to low-cost manufacturing regions creates persistent counterfeit product circulation risks across both physical and digital retail channels. Luxury brands invest substantially in authentication technology, legal enforcement, and consumer education programs, but counterfeit availability can undermine brand equity and constrain market value expansion, particularly in aspirational and lower-tier city consumer segments.

- Slowdown in International Tourist Luxury Spending: Recovery in inbound tourist volumes to South Korea, historically a significant driver of duty-free luxury channel revenue and overall market performance, remains subject to geopolitical sensitivities and macroeconomic uncertainties affecting major source markets. Slower recovery in high-spending tourist segments constrains near-term duty-free channel revenue realization and overall market growth projections.

Market Opportunities

- Sustainable and Ethical Luxury: Korean luxury consumers, particularly among younger demographics, are increasingly prioritizing sustainability credentials, ethical supply chains, and circular luxury offerings in their purchase decisions. Brands incorporating verifiable sustainability practices, transparent sourcing credentials, and pre-owned luxury authentication programs are well-positioned to capture this expanding, values-driven consumer segment in the South Korean market.

- Digital Luxury Commerce and AI-Powered Personalization: Integration of AI-powered personalization, augmented reality virtual try-ons, and luxury livestream commerce is transforming the online luxury retail experience in South Korea. Brands building sophisticated digital consumer relationship management ecosystems and virtual boutique experiences are effectively capturing Korea's leading-edge digital consumer cohort while expanding premium channel revenue beyond physical retail boundaries.

Market Challenges

- Premiumization Ceiling and Aspirational Consumer Trade-Down Risk: While South Korea's core luxury consumer base demonstrates resilience, macroeconomic uncertainty and elevated household debt levels create potential for aspirational consumers to shift toward accessible luxury or premium mass-market alternatives during periods of economic softening, constraining volume growth in the broader luxury goods market across key product categories.

- Intensifying Competition from Global and Domestic Accessible Luxury Brands: The growing presence of accessible luxury brands in South Korea's retail landscape creates competitive pressure on mid-tier luxury positioning. As more brands enter the Korean market with aspirational value propositions, consumer attention and discretionary wallet share become more fragmented, requiring increased marketing investment and clear differentiation strategies from established luxury houses.

Emerging Market Trends

1. Gen MZ Reshaping Luxury Consumption Patterns

Millennials and Gen Z now account for the majority of South Korea's luxury expenditure, prioritizing authenticity, brand storytelling, and exclusive limited-edition collaborations over traditional status markers alone. This cohort drives resale platform growth and demands digital-first purchase journeys with seamless social media integration, fundamentally reshaping how luxury brands market, distribute, and engage with Korean consumers.

2. Omnichannel Retail Experience Integration

Luxury brands are investing in seamless omnichannel integration across flagship stores, app-based VIP programs, and social commerce platforms. South Korean luxury consumers expect fully synchronized online and offline brand experiences, driving significant flagship store digitalization investment and motivating brands to build unified consumer data ecosystems enabling personalized engagement across every consumer interaction channel.

3. Accessible Luxury and Ultra-Premium Bifurcation

The market is bifurcating between ultra-luxury houses deploying scarcity and heritage marketing to sustain exceptional pricing power, and aspirational accessible luxury brands capturing an expanding middle-affluent consumer tier. Both segments are growing, driven by distinct consumer motivations, and demand different brand strategies, distribution approaches, and digital engagement models that luxury companies must calibrate.

4. Pre-Owned and Circular Luxury Market Expansion

South Korea's authenticated pre-owned luxury market is expanding rapidly, driven by sustainability consciousness, value-seeking behavior, and growing acceptance of circular luxury as a legitimate entry point to brand ownership. Certified pre-owned programs from major luxury houses and dedicated resale platforms are formalizing and growing this channel, broadening luxury participation to a wider consumer base.

Industry Value Chain Analysis

The South Korea luxury goods value chain spans five integrated stages from premium raw material sourcing through consumer engagement and after-sales service. Brand design and creative direction capture the highest intangible value, while flagship retail and digital channels command significant distribution margin and serve as critical brand equity touchpoints for luxury houses operating in the South Korean market.

|

Stage |

Key Activities / Participants |

|

Raw Material & Input Sourcing |

Premium leather, precious metals, gemstones, luxury textiles, exotic materials, and specialist components sourced from certified premium suppliers across global sourcing networks |

|

Brand Design & Creative Direction |

Creative direction, heritage craftsmanship development, seasonal collection design, product innovation, intellectual property development, and limited-edition strategy by creative leadership |

|

Manufacturing & Quality Control |

Atelier and factory production, skilled artisan manufacturing, rigorous quality control processes, global logistics coordination, and customs compliance across international supply chains |

|

Distribution & Retail Channels |

Single-brand flagship stores, luxury department store concessions, authenticated online platforms, duty-free operators, and emerging social commerce channels serving diverse consumer touchpoints |

|

After-Sales & Consumer Engagement |

VIP clienteling programs, product authentication and repair services, personalized consumer relationship management, loyalty programs, and ongoing brand experience delivery to retain high-value consumers |

Technology Landscape in the South Korea Luxury Goods Industry

Digital Authentication and Anti-Counterfeiting Technology

Blockchain-based authentication platforms, NFC-embedded product tags, and AI-powered image recognition are being deployed by leading luxury brands to provide verifiable product provenance certificates and digital ownership records. These technologies enhance consumer trust, support the growing pre-owned luxury market, and establish robust defenses against counterfeit goods proliferation in both physical and digital retail environments across South Korea.

AI-Powered Personalization and Consumer Relationship Management

Luxury brands are deploying artificial intelligence-driven consumer relationship management systems that analyze purchase history, browsing behavior, and lifestyle preferences to deliver hyper-personalized product recommendations, exclusive event invitations, and proactive clienteling outreach. South Korean luxury consumers' high digital engagement and platform sophistication make AI-powered personalization a particularly impactful competitive differentiator in this market.

Augmented Reality and Virtual Try-On Technology

Leading luxury brands are integrating augmented reality-powered virtual try-on capabilities for watches, jewelry, bags, and eyewear into their mobile applications and e-commerce platforms. These immersive digital experiences reduce purchase hesitation for high-value luxury items, increase consumer engagement with online luxury channels, and enable brands to deliver brand experience touchpoints beyond the physical limitations of retail geography.

Social Commerce and Livestream Luxury Integration

South Korea's highly connected social media environment is driving direct social commerce integration for luxury brands. Luxury-focused livestream events, influencer-collaborated limited releases, and integrated social platform purchasing are creating efficient discovery-to-transaction pathways that capture impulse luxury purchase moments among highly engaged Korean digital consumers across multiple social platforms.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Type |

Clothing and Apparel |

29.4% |

2025 |

|

Distribution Channel |

Single-Brand Stores |

38.6% |

2025 |

|

Region |

Seoul Capital Area |

46.2% |

2025 |

By Type

Clothing and Apparel commands a 29.4% majority share in 2025 owing to its category breadth spanning ready-to-wear seasonal collections, iconic heritage outerwear, and aspirational fashion items positioned at diverse luxury price points. Korean consumers' strong fashion consciousness and media-amplified trend adoption make apparel the most frequently purchased and broadly accessible luxury category across diverse consumer segments.

To access detailed market analysis, Request Sample

Bags (21.8%) command premium positioning as trophy purchases with strong investment value perception, particularly for iconic styles from heritage European fashion houses with proven secondary market value retention. Jewelry (17.6%) grows on occasion-driven gifting and investment-grade purchasing. Footwear (13.5%) benefits from luxury sneaker culture and premium dress footwear demand. Watches (10.2%) serve investment-grade and aspirational status-signaling demand from established Swiss and European luxury watch brands.

By Distribution Channel

Single-Brand Stores lead distribution at 38.6% in 2025, providing immersive branded retail environments that reinforce luxury brand equity through personalized service and exclusive in-store experiences unavailable in multi-brand settings. These flagship stores function as brand marketing platforms as much as transactional sales channels, delivering enduring value through VIP programs, exclusive product access, and curated consumer events.

Multi-Brand Stores (27.4%), principally luxury department store galleries, serve comparison-shopping occasions and attract consumers seeking brand breadth within a single premium environment. Online Stores (21.3%) are the fastest-growing distribution channel, expanding at approximately 5.5% CAGR through 2034. Others (12.7%) encompasses duty-free channels, authenticated luxury resale platforms, and limited-edition pop-up retail activations.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

|

Seoul Capital Area |

46.2% |

High concentration of luxury flagship retail; dense affluent urban population; premier shopping districts driving consumer footfall and luxury spending |

|

Yeongnam (Southeastern Region) |

20.8% |

Industrially driven wealth base; expanding luxury retail presence in major metropolitan hubs; growing aspirational consumer segment |

|

Hoseo (Central Region) |

13.9% |

Rising disposable incomes among urban professionals; proximity to capital region influencing luxury consumption patterns and retail preferences |

|

Honam (Southwestern Region) |

10.4% |

Growing middle-class and upper-income base; expanding luxury retail infrastructure in regional commercial and cultural centers |

|

Others |

8.7% |

Tourism-driven luxury demand in coastal and island regions; emerging luxury market penetration in secondary and tertiary cities across the country |

Seoul Capital Area's 46.2% market dominance in 2025 is driven by the city's role as South Korea's commercial, cultural, and fashion capital, concentrating the highest density of luxury flagships and premium department store luxury galleries in the country. International visitors arriving in Seoul further amplify luxury demand through duty-free and retail channel purchases in the capital region's iconic luxury retail destinations.

Yeongnam (Southeastern Region), at 20.8% in 2025, benefits from a growing affluent consumer base in Korea's major southeastern metropolitan hubs, supported by industrial and commercial wealth generation. The region's expanding luxury retail infrastructure, including premium department stores and flagship openings, reflects the broadening geographic footprint of South Korea's luxury consumer market beyond the Seoul Capital Area.

Competitive Landscape

The South Korea luxury goods market is moderately concentrated at the brand-portfolio level, with global luxury conglomerates commanding the largest aggregate market shares. European heritage luxury houses dominate consumer preference in South Korea, leveraging strong brand equity, aspirational positioning, and cultural resonance reinforced through celebrity brand ambassador programs and high-impact marketing activations tailored to Korean consumer sensibilities.

|

Company Name |

Key Products |

Market Position |

Global Strategic Focus |

|

Kering |

Gucci, Saint Laurent, Bottega Veneta, Balenciaga, Alexander McQueen, Brioni |

Leader |

Broad luxury fashion portfolio; strong Gen Z and millennial market penetration through culturally resonant brand activations; expanding digital commerce presence |

|

Compagnie Financière Richemont SA |

Cartier, IWC, Piaget, Van Cleef & Arpels, Dunhill |

Leader |

Dominant positioning in watches and jewelry; strong premium department store and flagship boutique network; leading investment and gifting occasion luxury brand |

|

Hermès |

Birkin, Kelly, Constance bags; silk scarves; Hermès watches; homeware collections |

Leader |

Ultra-luxury positioning; tightly controlled single-brand retail strategy generating sustained premium demand, waitlist dynamics, and exceptional brand exclusivity |

|

DINT |

Dresses, Tops, Bottoms, Outerwear, Shoes, Accessories |

Emerging |

Korean contemporary luxury brand; minimalist and sophisticated design aesthetic targeting young affluent domestic consumers; growing presence in premium multi-brand and online channels |

|

ELIE SAAB |

Clothes, Accessories, Handbags, Fragrances |

Emerging |

Lebanese luxury fashion house renowned for haute couture and occasion wear; expanding ready-to-wear and accessories footprint in premium Asian markets; growing brand awareness among South Korean luxury consumers |

Key players include Kering, Compagnie Financière Richemont SA, Hermès, DINT, ELIE SAAB, and others.

Key Company Profiles

Kering

Kering is a global luxury group encompassing a curated portfolio of iconic fashion and leather goods houses, each with distinctive brand identities, creative heritages, and dedicated consumer followings. In South Korea, the company's brands have established strong market positions across both traditional retail channels and digital platforms, particularly resonating with the country's influential younger luxury consumer cohort through targeted activations and brand-specific marketing strategies.

- Product Portfolio: Gucci, Saint Laurent, Bottega Veneta, Balenciaga, Alexander McQueen, Brioni, and others.

- Recent Developments: In April 2026, Kering announced a strategic partnership with Chinese fashion group ICCF centered around its flagship luxury brand ICICLE, while also acquiring a minority stake in the company. The move is aimed at combining ICCF’s strong understanding of the Chinese luxury market with Kering’s expertise in craftsmanship, operations, and global brand development. As part of the partnership, Kering’s investment will support the next phase of growth for ICICLE, including its international expansion and the development of new product categories.

- Strategic Focus: The company is executing a brand elevation and premiumization strategy across its South Korean portfolio, deepening direct consumer relationships through flagship retail excellence and personalized digital engagement, while targeting younger affluent Korean consumers through culturally relevant collaborations and compelling brand storytelling that connects with local sensibilities.

Compagnie Financière Richemont SA

Compagnie Financière Richemont SA is the world's leading luxury watches and jewelry group, with a portfolio of distinguished maisons renowned for exceptional craftsmanship, enduring heritage, and precision manufacturing. In South Korea, the company's portfolio brands command premium positioning in the watches and jewelry segments, serving the market's demand for investment-grade and occasion-driven luxury purchases through flagship boutiques and premier department store concessions.

- Product Portfolio: Cartier, IWC, Piaget, Van Cleef & Arpels, Dunhill, and others

- Recent Developments: In July 2023, Richemont acquired a controlling stake in Italian luxury footwear brand Gianvito Rossi as part of its strategy to strengthen its fashion and accessories portfolio. The transaction marks a new partnership between the Swiss luxury group and the renowned shoemaking maison founded by Gianvito Rossi.

- Strategic Focus: The company's South Korea strategy is anchored on the exceptional brand equity of its flagship maisons in the watches and jewelry segments, executing a controlled single-brand retail distribution approach that preserves ultra-premium positioning while investing in digital authentication, personalized client relationship management, and boutique experience enhancement.

Market Concentration Analysis

The South Korea luxury goods market is moderately concentrated at the conglomerate level, with leading global luxury groups collectively accounting for a dominant share of total market revenue through their multi-brand portfolios. At the individual brand level, concentration is more distributed, reflecting broad consumer appeal across diverse brand identities, price tiers, and product category preferences among South Korean luxury consumers.

Korean department store operators exert significant distribution channel influence, controlling the majority of multi-brand luxury retail floor space across the country. Their luxury gallery curation decisions and brand space allocations meaningfully influence brand visibility, consumer footfall, and sales performance for luxury houses operating through these critical distribution channels, representing an important structural dynamic in the South Korean luxury goods market.

Investment & Growth Opportunities

Fastest-Growing Segments

Online Stores represent the highest-growth distribution channel through 2034, capturing digitally native Gen MZ luxury shoppers and enabling brands to reach consumers beyond traditional physical retail geographies and operating hours. Clothing and Apparel benefits from ongoing luxury fashion premiumization, sustained Korean Wave-driven aspirational demand, and the category's broad accessibility across multiple luxury price tiers.

Emerging Markets

Yeongnam and Hoseo regions are emerging as significant luxury market expansion frontiers as South Korean luxury retail infrastructure extends beyond the Seoul Capital Area. Brands previously Seoul-exclusive are making first investments in premier regional locations, reflecting the broadening geographic distribution of South Korea's affluent consumer base and the corresponding opportunity to penetrate underpenetrated regional luxury markets.

Venture & Investment Trends

Global luxury conglomerates are increasing South Korea capital allocation for flagship store investments, digital consumer relationship management platforms, and culturally targeted celebrity ambassador programs leveraging South Korea's global cultural influence through Hallyu. The pre-owned luxury market is attracting significant platform investment, reflecting the growing commercial opportunity in authenticated circular luxury commerce targeting Korea's values-driven younger consumer cohort.

Future Market Outlook (2026-2034)

The South Korea luxury goods market is forecast to expand from USD 5.71 Billion in 2025 to USD 8.45 Billion by 2034 at a CAGR of 4.47%, driven by Korea's enduring status-driven consumption culture, an expanding affluent consumer base, and Seoul's strengthening position as a globally recognized luxury capital that attracts both domestic high-value spending and international tourist luxury purchases across its world-class retail infrastructure.

Three structural forces will shape the market through 2034: Hallyu-amplified brand desirability will sustain premium pricing power for established luxury houses; online luxury commerce will grow substantially as a share of total distribution, reshaping channel economics and brand investment priorities; and ultra-luxury premiumization will drive revenue concentration among top-tier houses as Korean consumers progressively shift from accessible luxury toward true luxury expenditure enabled by rising household affluence levels.

Research Methodology

Primary Research

Primary research encompassed structured interviews with luxury retail professionals, department store luxury gallery buyers, Korean consumer insight specialists, brand-side commercial managers, and duty-free channel operators across South Korea. Primary data validated market sizing, type and distribution channel segment shares, regional demand estimates, and evolving consumer behavior trends shaping the South Korean luxury goods market.

Secondary Research

Key secondary sources include Korea Tourism Organization duty-free sales data, Statistics Korea household expenditure surveys, leading global luxury industry studies and reports, Euromonitor International luxury goods database, annual reports from leading luxury conglomerates, and trade publications covering global and South Korean luxury retail market developments and consumer behavior research.

Forecasting Models

Market size estimations and growth projections were derived using a combination of top-down and bottom-up forecasting models, incorporating South Korea GDP growth rates, household income distribution data, luxury price index trends, and channel-specific retail sales data. Scenario analysis encompassing base, optimistic, and conservative cases was performed to account for macroeconomic uncertainty, currency fluctuation risk, and inbound tourist recovery variables.

South Korea Luxury Goods Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Types Covered | Clothing and Apparel, Footwear, Bags, Watches, Jewelry, Others |

| Distribution Channels Covered | Single-Brand Stores, Multi-Brand Stores, Online Stores, Others |

| Regions Covered | Seoul Capital Area, Yeongnam (Southeastern Region), Honam (Southwestern Region), Hoseo (Central Region), Others |

| Companies Covered | Kering, Compagnie Financière Richemont SA, Hermès, DINT, ELIE SAAB, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the South Korea luxury goods market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the South Korea luxury goods market.

- Porter's Five Forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the South Korea luxury goods industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the South Korea Luxury Goods Market Report

The South Korea luxury goods market reached USD 5.71 Billion in 2025, reflecting sustained demand from the country's growing affluent consumer base, strong brand loyalty toward European luxury houses, and the continued expansion of flagship retail and duty-free channels across major metropolitan areas of South Korea.

The market is projected to reach USD 8.45 Billion by 2034, growing at a CAGR of 4.47% during 2026-2034, driven by rising affluent consumer demographics, accelerating digital luxury commerce adoption, Hallyu-amplified brand desirability, and the sustained expansion of single-brand flagship retail infrastructure across South Korea.

Clothing and Apparel leads with a 29.4% market share in 2025, valued for its category breadth and strong aspirational appeal amplified by Korean celebrity fashion culture. Bags (21.8%) are the second-largest type, with iconic styles from heritage luxury houses commanding strong consumer demand and investment value perception in the South Korean market.

Single-Brand Stores dominate with a 38.6% share in 2025, providing immersive brand experiences and personalized service that resonate strongly with South Korean luxury consumers seeking premium in-store engagement. Online Stores (21.3%) are the fastest-growing channel, driven by digital luxury platform adoption among younger consumer segments.

Seoul Capital Area leads with a 46.2% market share in 2025, driven by the city's role as the country's commercial and cultural capital with the highest concentration of luxury flagships, department store luxury galleries, and affluent consumers. Yeongnam follows with a 20.8% share, reflecting growing regional luxury consumption.

Online Stores represent the fastest-growing distribution channel at approximately 5.5% CAGR through 2034, driven by authenticated digital luxury platforms and brand-owned e-commerce investments serving Korea's digital-first consumer base. Clothing and Apparel is the fastest-growing product type at approximately 4.85% CAGR through 2034.

Leading companies include Kering, Compagnie Financière Richemont SA, Hermès, DINT, ELIE SAAB, and others.

Key drivers include the growing affluent consumer base with rising disposable incomes, Hallyu-driven luxury brand desirability amplified through celebrity ambassador programs, expansion of luxury flagship retail and duty-free infrastructure, and rapid growth of digital and e-commerce luxury shopping adoption among younger Korean consumers.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)