Sparkling Wine Market Size, Share, Trends and Forecast by Type, Product, Price Point, Sales Channel, and Region, 2026-2034

Sparkling Wine Market Size and Share:

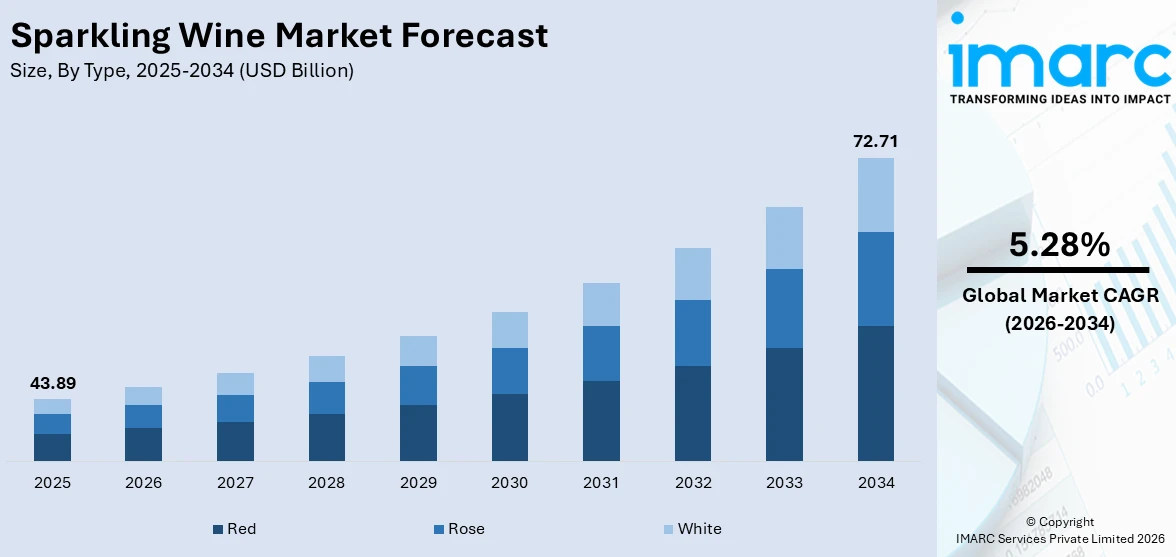

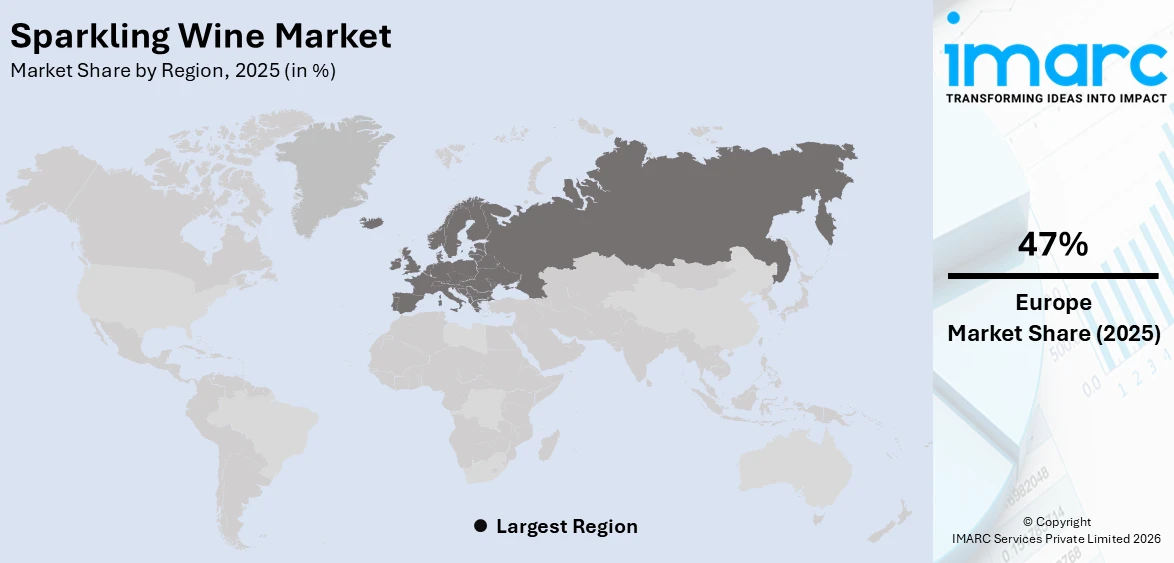

The global sparkling wine market size was valued at USD 43.89 Billion in 2025. Looking forward, IMARC Group estimates the market to reach USD 72.71 Billion by 2034, exhibiting a CAGR of 5.28% from 2026-2034. Europe currently dominates the market, holding a market share of 47% in 2025. The region benefits from its rich winemaking heritage, well-established viticulture traditions, and strong consumer preference for sparkling wine varieties across celebrations, dining occasions, and everyday casual consumption, along with robust export networks, all contributing to the sparkling wine market share.

The global sparkling wine market is being propelled by several interconnected factors that are collectively enhancing production and consumption worldwide. The growing culture of social celebrations, coupled with the increasing acceptance of sparkling wine as an everyday beverage rather than a luxury reserved for special occasions, is broadening its consumer base significantly. Evolving consumer tastes toward lighter, refreshing alcoholic beverages with lower alcohol content are favoring sparkling wine over traditional still wines and spirits. The expanding middle-class population in developing economies is driving heightened demand, supported by rising disposable incomes and greater exposure to Western dining customs. Furthermore, the diversification of sparkling wine offerings, including organic, vegan, and low-sugar variants, is attracting health-conscious consumers and younger demographics.

The United States has emerged as a major region in the sparkling wine market owing to many factors. The country is experiencing a notable shift in consumer behavior, with sparkling wine increasingly becoming a preferred choice for both celebratory and casual drinking occasions. In October 2025, U.S. premium sparkling wines priced above $15 led market growth, with La Marca increasing 6.5% and Mionetto 8.5% in retail volume year-to-date. Moreover, the millennial and Generation Z demographics are driving significant demand, favoring sparkling wine for its versatility, lower alcohol content, and association with premium lifestyle experiences. Additionally, the growing domestic production of sparkling wines, particularly in regions like California, Oregon, and New Mexico, is boosting local supply and fostering innovation in product offerings. The sparkling wine market growth in the United States is further supported by increasing restaurant and hospitality sector demand for diverse wine selections.

To get more information on this market Request Sample

Sparkling Wine Market Trends:

Premiumization Driving Consumer Preferences

The sparkling wine industry is experiencing a significant shift toward premiumization as consumers increasingly seek higher-quality products with distinctive flavor profiles and artisanal production methods. This trend is particularly evident in the growing demand for estate-produced sparkling wines that emphasize terroir-specific characteristics and traditional production techniques such as méthode champenoise. In December 2025, the historic Mumm Napa sparkling wine house in California was acquired by Trinchero Family Wine & Spirits, demonstrating investor interest in high-end domestic bubbly and traditional production heritage. Retailers are responding by expanding their premium sparkling wine selections and creating dedicated tasting experiences that educate consumers about quality differentiators. The sparkling wine market outlook remains positive as premiumization continues reshaping purchasing patterns and encouraging producers to invest in quality-driven production methodologies across all major wine-producing regions worldwide.

Expanding Online Retail Distribution Channels

The digital transformation of beverage retail is significantly impacting the sparkling wine industry, with online distribution channels experiencing remarkable expansion across global markets. E-commerce platforms, dedicated wine subscription services, and direct-to-consumer websites are creating unprecedented access to diverse sparkling wine selections from international producers. According to reports, Gruppo Italiano Vini reported that sparkling wines generated 56% of the revenue on its Vinicum.com e‑commerce platform, reflecting robust online demand for bubbly offerings. This shift is particularly benefiting smaller, boutique sparkling wine producers who previously struggled to reach consumers through traditional retail networks dominated by established brands. The sparkling wine market forecast indicates that online retail will continue gaining market share as digital infrastructure improves and consumer comfort with online alcohol purchasing strengthens across emerging and established economies.

Rising Popularity of Low-Alcohol Variants

The growing health and wellness consciousness among global consumers is driving substantial demand for low-alcohol and alcohol-free sparkling wine alternatives, representing a transformative sparkling wine market trends development. Producers are investing heavily in advanced dealcoholization technologies and innovative fermentation techniques to create products that maintain the effervescence, flavor complexity, and sensory appeal of traditional sparkling wines while significantly reducing alcohol content. As per sources, Henkell Freixenet launched its new alcohol‑free sparkling wine “Henkell 0.0%” to meet rising consumer demand for health‑oriented, zero‑alcohol bubbly alternatives. This trend aligns with broader societal movements toward mindful drinking, moderation, and sober-curious lifestyles that are gaining momentum particularly among younger adult consumers in developed markets.

Sparkling Wine Industry Segmentation:

IMARC Group provides an analysis of the key trends in each segment of the global sparkling wine market, along with forecast at the global, regional, and country levels from 2026-2034. The market has been categorized based on type, product, price point, and sales channel.

Analysis by Type:

- Red

- Rose

- White

Red holds 52% of the market share, establishing a commanding presence in the global market, driven by its distinctive flavor profile that combines the robust characteristics of red grape varieties with the effervescence and refreshing quality of sparkling wine production methods. The popularity of red sparkling wines is increasing as consumers explore beyond traditional white and rosé varieties, seeking bolder taste experiences that complement diverse culinary pairings. In February 2026, supermodel and entrepreneur Ashley Graham launched “Lucci,” a modern Lambrusco sparkling red wine made in Italy and distributed nationwide across major U.S. retailers, highlighting renewed commercial interest in red bubbly styles. Red sparkling wine variants, including Lambrusco, sparkling Shiraz, and Brachetto, are gaining traction across European and Asia-Pacific markets where consumers appreciate their versatility in food pairing and their suitability for both formal dining and casual consumption occasions. The growing interest in regional wine specialties and authentic production methods is further supporting demand for red sparkling wines.

Analysis by Product:

- Cava

- Champagne

- Cremant

- Prosecco

- Others

Prosecco leads the market with a share of 33%, emerging as the most popular sparkling wine product category globally, driven by its approachable flavor profile, competitive pricing, and strong brand recognition among diverse consumer segments. Originating from the Veneto and Friuli Venezia Giulia regions of Italy, Prosecco benefits from well-established geographical indication protections that ensure quality standards and authenticity. The versatility of Prosecco as both a standalone aperitif and a base for popular cocktails such as Aperol Spritz and Bellini has significantly expanded its consumption occasions beyond traditional celebrations. Its lighter, fruitier taste profile appeals to a broad demographic, including younger consumers who are entering the sparkling wine category for the first time. Export volumes of Prosecco continue to grow steadily, particularly in North American and European markets where consumer awareness and appreciation for Italian sparkling wines remain strong and expanding consistently.

Analysis by Price Point:

- Economy

- Mid-range

- Luxury

Economy dominates the market, with a share of 44%, maintaining its dominant position in the sparkling wine market, reflecting the strong consumer preference for affordable sparkling wine options that deliver consistent quality and satisfying effervescence at accessible price points. Large retail distribution networks, effective supply chain management, and high-volume production capabilities all help this market segment by guaranteeing that products are widely available in supermarkets, convenience stores, and online marketplaces. Economy sparkling wines are entry-level offerings that draw new customers to the market, especially in markets where affordability is still a top consideration. Sparkling wine's increasing appeal in informal dining environments and social events, where high volume consumption calls for affordable options, is another factor driving the market. In order to maintain their competitive positioning, producers in this segment are concentrating on upholding quality standards while maximizing production costs through technological advancements in vinification and packaging processes.

Analysis by Sales Channel:

Access the comprehensive market breakdown Request Sample

- Supermarket and Hypermarket

- Specialty Stores

- On Trade

- Others

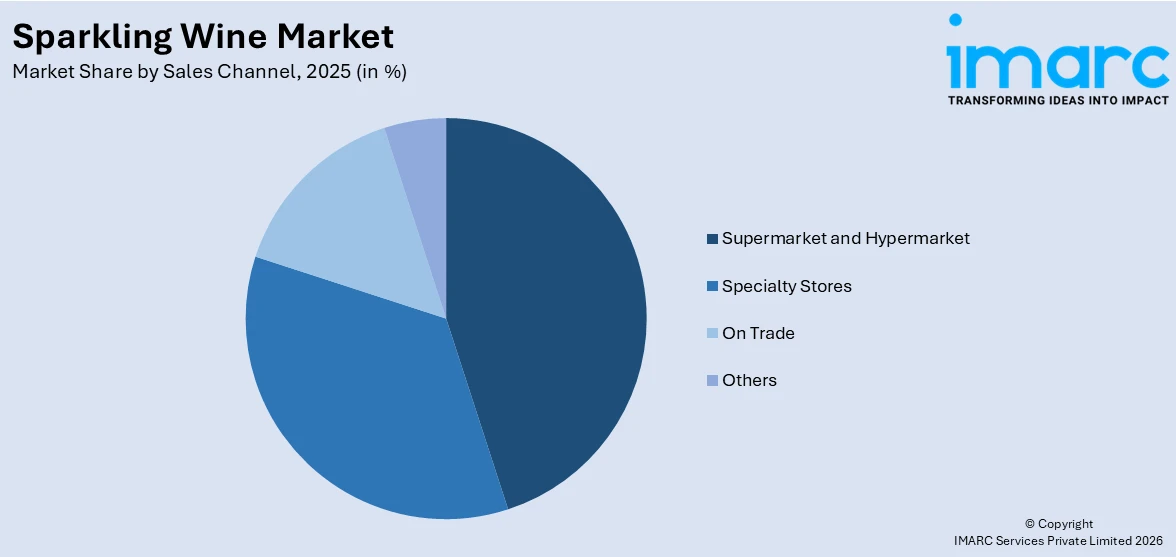

Supermarket and hypermarket represent the leading segment, with a market share of 43%, continuing to dominate sparkling wine distribution globally It is the main retail channel that customers use to find, evaluate, and buy sparkling wine products. Using visual merchandising, promotional pricing, and product information at the point of sale, these large-format retail establishments allow customers to make well-informed purchasing decisions by offering wide product assortments that span multiple price points, brands, and origins. Channel preference is strongly influenced by the ease of one-stop shopping, where customers can buy sparkling wine in addition to other groceries and home goods. Additionally, supermarkets and hypermarkets use their purchasing power to bargain with producers for competitive pricing, allowing for alluring promotional offers that encourage trial and repeat purchases. Seasonal promotional campaigns, end-cap displays, and festive period marketing initiatives conducted by these retailers significantly influence sparkling wine purchasing volumes throughout the year.

Regional Analysis:

To get more information on the regional analysis of this market Request Sample

- North America

- United States

- Canada

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Indonesia

- Others

- Europe

- Germany

- France

- United Kingdom

- Italy

- Spain

- Russia

- Others

- Latin America

- Brazil

- Mexico

- Others

- Middle East and Africa

Europe, accounting for 47% of the share, maintaining the leading position in the market. Europe maintains its dominant position in the global sparkling wine market, supported by centuries of winemaking tradition, extensive vineyard acreage dedicated to sparkling wine production, and deeply embedded cultural consumption patterns that integrate sparkling wine into everyday dining and celebrations. The region is home to the world's most prestigious sparkling wine appellations, including Champagne, Prosecco, and Cava, which collectively drive significant production volumes and export revenues. European consumers demonstrate sophisticated preferences for quality, provenance, and production methodology, sustaining robust demand across premium and economy segments alike. The regulatory framework governing sparkling wine production in Europe, including protected designation of origin systems, ensures quality standards that strengthen consumer confidence and brand value. Growing wine tourism, vineyard experiences, and culinary integration are further reinforcing the cultural significance of sparkling wine consumption across the continent.

Key Regional Takeaways:

North America Sparkling Wine Market Analysis

North America represents a significant and rapidly expanding market for sparkling wine, driven by evolving consumer demographics, shifting beverage preferences, and expanding retail accessibility across the region. The United States serves as the primary growth engine within North America, with consumers increasingly embracing sparkling wine as a versatile beverage suitable for diverse occasions ranging from formal celebrations to casual social gatherings and everyday meals. The millennial and Generation Z cohorts are particularly influential in driving market expansion, demonstrating strong preferences for sparkling wines that offer approachable flavor profiles, attractive packaging, and alignment with premium lifestyle aspirations. Canadian consumers are also contributing meaningfully to regional demand, supported by a growing wine culture and expanding retail availability through provincial liquor distribution systems. The direct-to-consumer distribution channel is strengthening through wine club memberships, tasting room experiences, and e-commerce platforms that provide consumers with convenient access to diverse sparkling wine selections. Restaurant and hospitality venues across the region are expanding their sparkling wine offerings, incorporating by-the-glass programs that encourage trial and discovery among new consumers seeking refreshing and celebratory beverage options.

United States Sparkling Wine Market Analysis

The United States represents one of the fastest-growing sparkling wine markets globally, driven by evolving consumer demographics, shifting beverage preferences, and expanding retail accessibility. American consumers are increasingly embracing sparkling wine as a versatile beverage suitable for diverse occasions ranging from formal celebrations to casual social gatherings and everyday meals. The millennial and Generation Z cohorts are particularly influential in driving market expansion, demonstrating strong preferences for sparkling wines that offer approachable flavor profiles, attractive packaging, and alignment with premium lifestyle aspirations. In March 2025, California’s Rack & Riddle—the #1 custom sparkling wine producer in the U.S.—introduced “CALSECCO,” a new California sparkling wine category designed to attract Gen Z and millennial consumers with Italian‑style bubbles made from locally grown grapes. The domestic sparkling wine production sector is experiencing significant growth, with established and emerging wineries in California, Oregon, Virginia, and other states investing in expanded production capabilities and quality improvement initiatives. The direct-to-consumer distribution channel is strengthening through wine club memberships, tasting room experiences, and e-commerce platforms that provide consumers with convenient access to diverse sparkling wine selections. Restaurant and hospitality venues across the country are expanding their sparkling wine offerings, incorporating by-the-glass programs that encourage trial and discovery.

Europe Sparkling Wine Market Analysis

Europe remains the cornerstone of global sparkling wine production and consumption, anchored by its unparalleled winemaking heritage and deeply rooted cultural affinity for effervescent wines. The region encompasses the world's most renowned sparkling wine regions, with France, Italy, Spain, and Germany serving as major production hubs that supply both domestic and international markets. European consumers display sophisticated purchasing behaviors characterized by strong preferences for quality designations, regional authenticity, and traditional production methods that ensure premium taste and effervescence. The expansion of organic and sustainable viticulture practices across European vineyards is creating new product categories that appeal to environmentally conscious consumers seeking responsibly produced sparkling wines. Wine tourism initiatives, particularly in champagne, prosecco, and cava producing regions, are strengthening consumer engagement and brand loyalty while attracting international visitors. The hospitality sector across European metropolitan areas continues driving on-trade sparkling wine consumption through innovative beverage programs and pairing menus that showcase regional sparkling wine diversity and excellence.

Asia Pacific Sparkling Wine Market Analysis

The Asia Pacific represents a dynamic and rapidly expanding market for sparkling wine, driven by rising disposable incomes, urbanization, and growing Western cultural influences that are reshaping beverage consumption patterns across the region. Countries including China, Japan, Australia, South Korea, and India are experiencing increasing consumer interest in sparkling wine as a symbol of sophistication and celebratory culture. The expanding middle-class population, particularly in China and India, is creating substantial new demand for both imported premium sparkling wines and affordable domestic alternatives. Australian sparkling wine production continues gaining international recognition for quality and innovation. E-commerce platforms and modern retail formats are improving product accessibility across the region, while hospitality and food service sectors in major metropolitan areas are actively promoting sparkling wine consumption through curated beverage experiences and seasonal promotional campaigns.

Latin America Sparkling Wine Market Analysis

Latin America is emerging as a promising market for sparkling wine, supported by growing consumer sophistication, increasing urbanization, and rising disposable incomes across the region. Brazil represents the largest market within the region, benefiting from a well-established domestic sparkling wine production industry concentrated in the Rio Grande do Sul region. The cultural integration of sparkling wine into festive celebrations, particularly during New Year and carnival seasons, sustains consistent seasonal demand. Mexican consumers are increasingly exploring sparkling wine options beyond traditional beverage choices. The expanding modern retail infrastructure and growing e-commerce penetration are improving product availability and consumer access to diverse sparkling wine selections across Latin American markets.

Middle East and Africa Sparkling Wine Market Analysis

The Middle East and Africa region presents a developing market for sparkling wine, characterized by diverse regulatory environments and varying levels of consumer acceptance across different countries. South Africa stands as the primary sparkling wine producing and consuming country in the region, with its established wine industry producing quality sparkling wines through both traditional and charmat production methods. The tourism and hospitality sectors in countries like the United Arab Emirates and South Africa are driving on-trade sparkling wine consumption through luxury hotel and restaurant offerings. Growing expatriate populations in Gulf countries are sustaining demand for imported sparkling wines. The expanding duty-free retail channel across regional airports is further contributing to sparkling wine accessibility and market development.

Competitive Landscape:

The global sparkling wine market is characterized by a moderately fragmented competitive structure, with a mix of large multinational corporations, established regional producers, and emerging boutique wineries competing across diverse product categories and price segments. Leading market participants are pursuing strategic initiatives including mergers and acquisitions, production capacity expansions, and new product launches to strengthen their market positioning and capture emerging consumer demand. Innovation in production techniques, packaging design, and flavor development represents a key competitive differentiator as producers seek to attract evolving consumer preferences. Sustainability and environmental responsibility are becoming increasingly important competitive factors, with leading producers investing in organic viticulture, carbon-neutral production processes, and sustainable packaging solutions. Distribution network optimization and digital marketing capabilities are additional areas where competitive advantages are being established.

The report provides a comprehensive analysis of the competitive landscape in the sparkling wine market with detailed profiles of all major companies, including:

- Accolade Wines

- Bacardi Limited

- Bronco Wine Company

- Casella Family Brands

- Caviro Extra S.p.A.

- Constellation Brands Inc.

- Freixenet Sa (Henkell & Co. Sektkellerei)

- Giulio Cocchi Spumanti Srl

- Illinois Sparkling Co.

- Quady Winery

- Treasury Wine Estates

- Vina Concha Y Toro

Latest News and Developments:

- In October 2025, Chandon India unveiled a limited edition Celebration Pack for Diwali, featuring its globally awarded Chandon Brut and Chandon Rosé paired with a stylish flute, designed for festive occasions, weddings, and gifting, emphasizing India’s sparkling wine heritage, craftsmanship, and global recognition across key states.

- In July 2024, Serena Wines 1881 debuted its first zero-alcohol sparkling wine “Zero” at Prowein in Düsseldorf, alongside the Più Spritz aperitif, targeting international markets and export growth, showcasing the brand’s commitment to innovation, moderate-alcohol beverages, and premium sparkling wine offerings.

Sparkling Wine Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Types Covered | Red, Rose, White |

| Products Covered | Cava, Champagne, Crémant, Prosecco, Others |

| Price Points Covered | Economy, Mid-Range, Luxury |

| Sales Channels Covered | Supermarket and Hypermarket, Specialty Stores, On Trade, Others |

| Regions Covered | North America, Asia-Pacific, Europe, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, China, Japan, India, South Korea, Australia, Indonesia, Germany, France, United Kingdom, Italy, Spain, Russia, Brazil, Mexico |

| Companies Covered | Accolade Wines, Bacardi Limited, Bronco Wine Company, Casella Family Brands, Caviro Extra S.p.A., Constellation Brands Inc., Freixenet Sa (Henkell & Co. Sektkellerei), Giulio Cocchi Spumanti Srl, Illinois Sparkling Co., Quady Winery, Treasury Wine Estates, Vina Concha Y Toro, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the sparkling wine market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the global sparkling wine market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's Five Forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the sparkling wine industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Sparkling Wine Market Report

The sparkling wine market was valued at USD 43.9 Billion in 2025.

The sparkling wine market is projected to exhibit a CAGR of 5.28% during 2026-2034, reaching a value of USD 72.7 Billion by 2034.

The sparkling wine market is primarily driven by rising consumer preference for premium and celebratory beverages, expanding middle-class populations in developing economies, growing acceptance of sparkling wine for casual consumption occasions, diversification of product offerings including organic and low-alcohol variants, and strengthening e-commerce distribution channels.

Europe currently dominates the sparkling wine market, accounting for a share of 47%. The region benefits from established winemaking traditions, prestigious appellations, strong domestic consumption, and extensive production infrastructure that supports both premium and economy sparkling wine segments.

Some of the major players in the sparkling wine market include Accolade Wines, Bacardi Limited, Bronco Wine Company, Casella Family Brands, Caviro Extra S.p.A., Constellation Brands Inc., Freixenet Sa (Henkell & Co. Sektkellerei), Giulio Cocchi Spumanti Srl, Illinois Sparkling Co., Quady Winery, Treasury Wine Estates, Vina Concha Y Toro, etc.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)