Stored Grain Insecticide Market Size, Share, Trends and Forecast by Product Type, Application, and Region, 2026-2034

Stored Grain Insecticide Market Size, Share, Trends & Forecast (2026-2034)

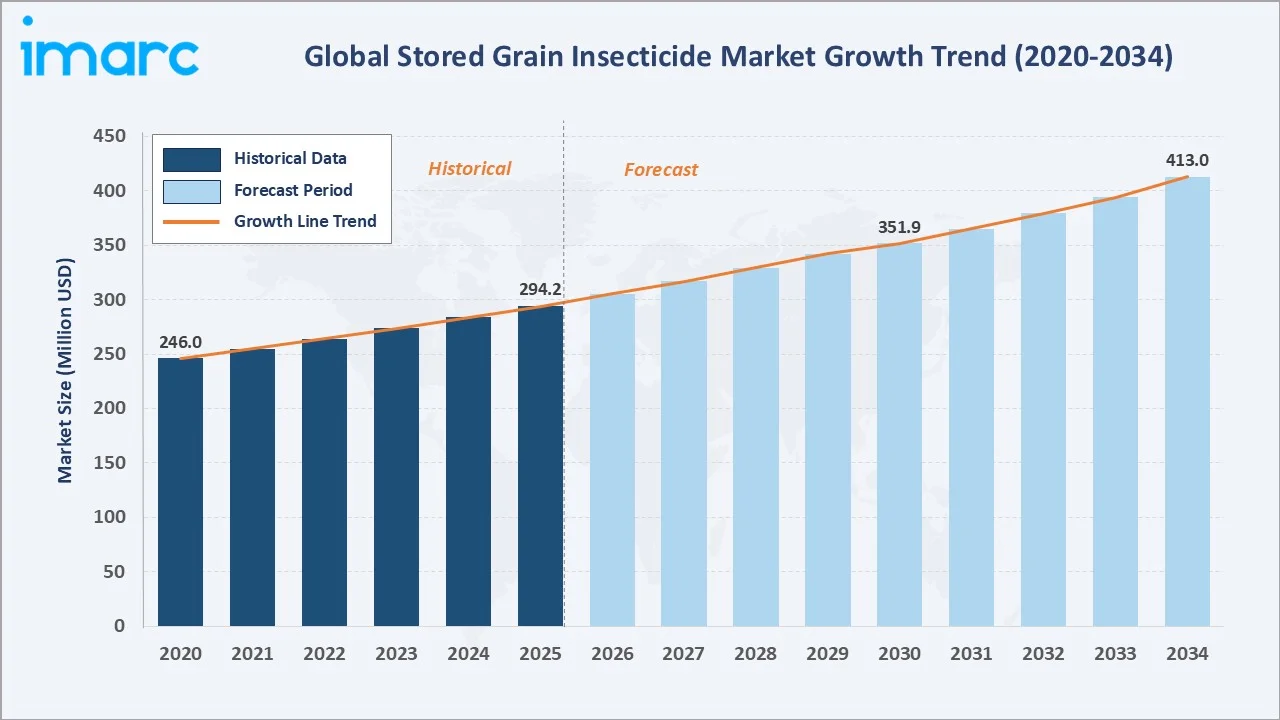

The global stored grain insecticide market reached USD 294.2 Million in 2025 and is projected to reach USD 413.0 Million by 2034, growing at a CAGR of 3.65% during 2026-2034. The market is driven by rising grain production, food security policies, and bio-insecticide adoption.

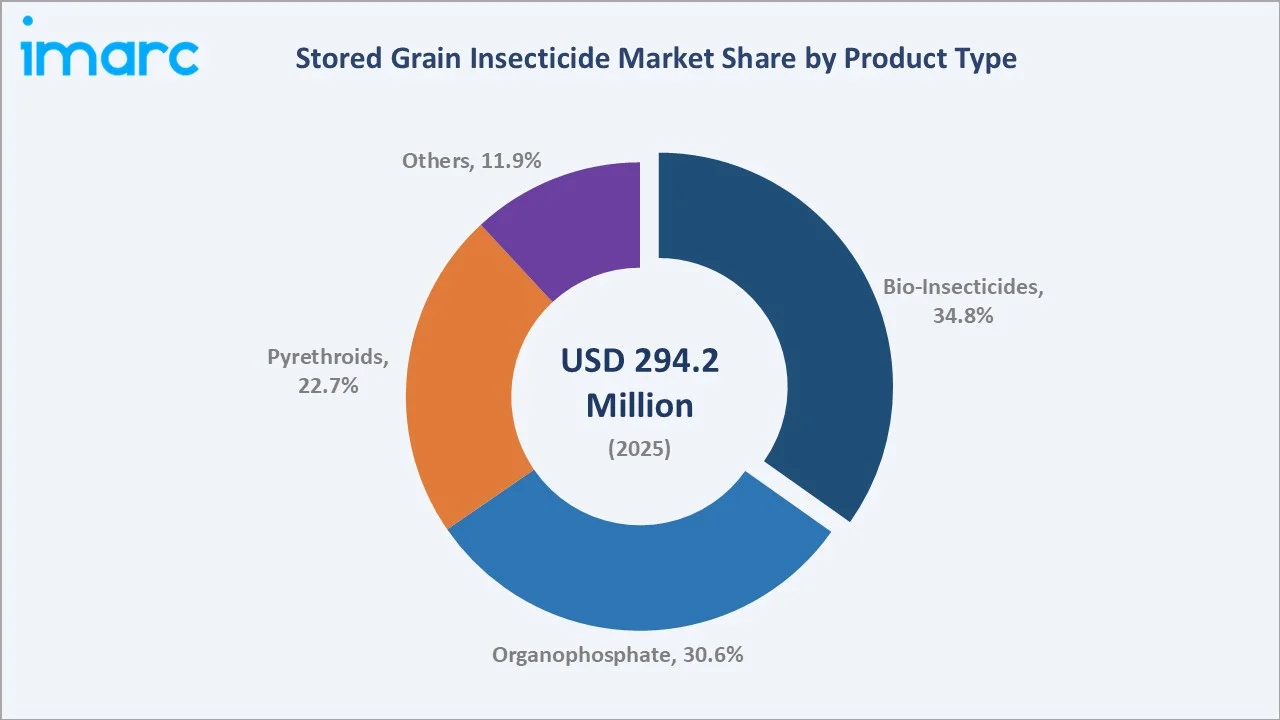

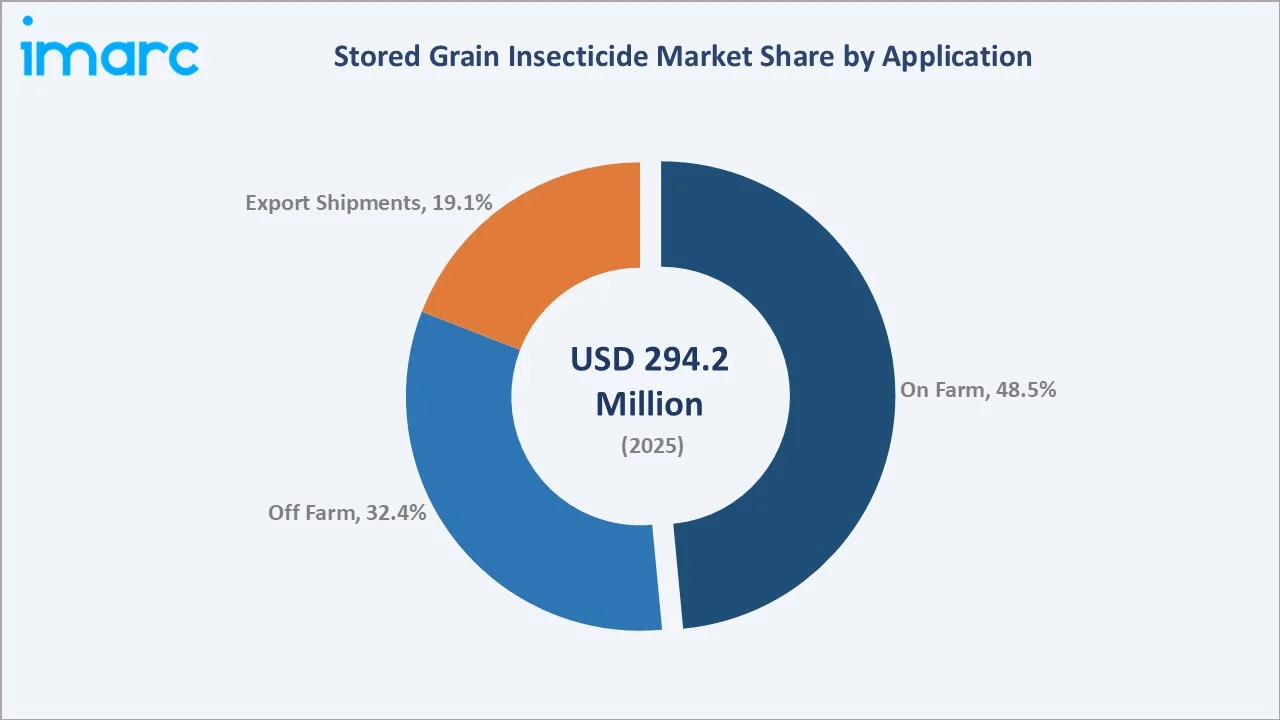

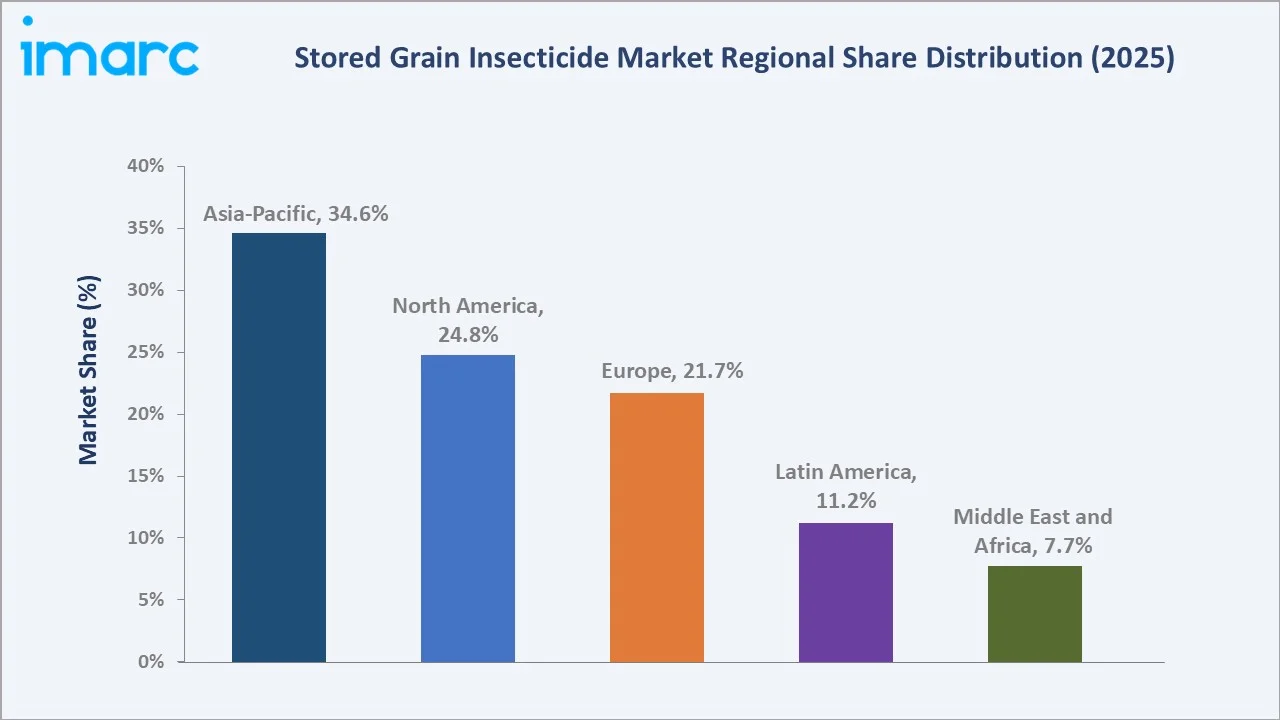

Bio-insecticides dominate at 34.8%. On Farm leads at 48.5%. Asia-Pacific commands 34.6% of global share.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 294.2 Million |

|

Forecast Market Size (2034) |

USD 413.0 Million |

|

CAGR (2026-2034) |

3.65% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Dominant Product Type |

Bio-Insecticides (34.8%, 2025) |

|

Dominant Application |

On Farm (48.5%, 2025) |

|

Leading Region |

Asia-Pacific (34.6%, 2025) |

The market expanded from USD 246.0 Million in 2020 to USD 294.2 Million in 2025, anchored at USD 351.9 Million in 2030 and forecast to reach USD 413.0 Million by 2034. Consistent demand for post-harvest grain protection and the regulatory-driven shift toward bio-insecticides underpin the steady growth trajectory throughout the historical and forecast periods.

To get more information on this market, Request Sample

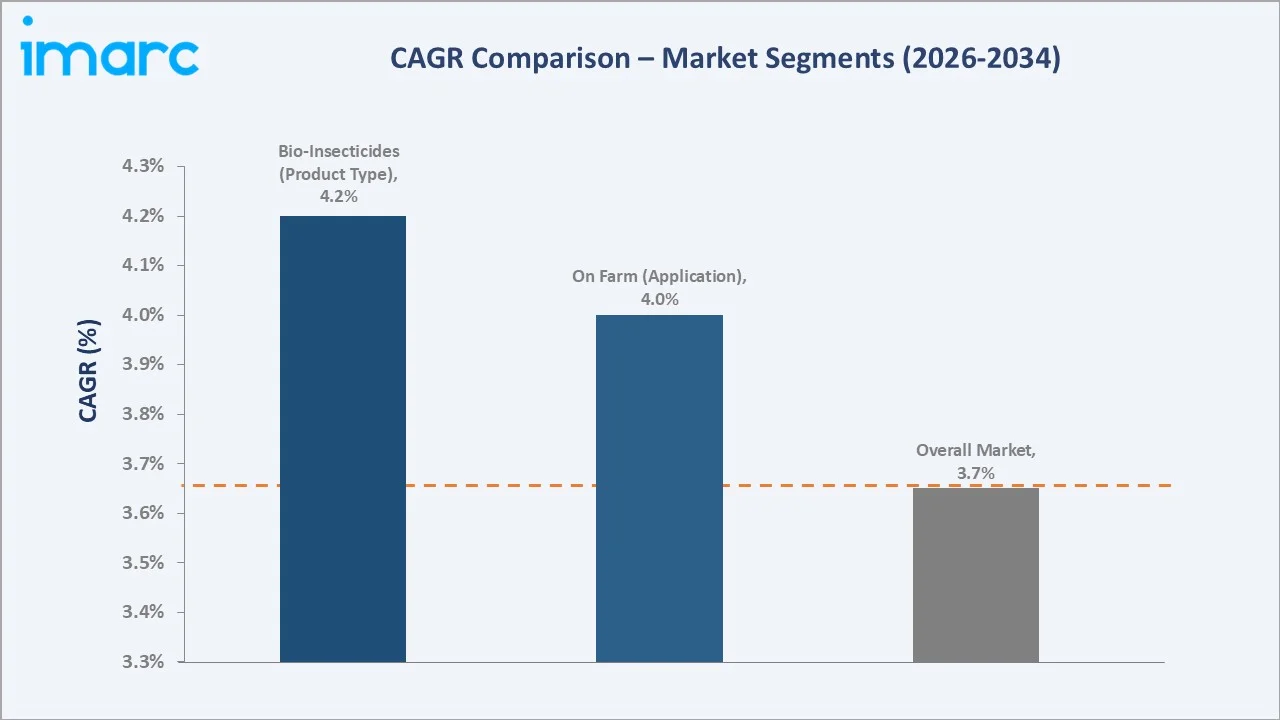

Bio-insecticides grow fastest at ~4.2% CAGR as organic farming policies and export residue compliance requirements accelerate the substitution of synthetic actives. On Farm application leads growth at ~4.0% CAGR as grain farmers adopt integrated pest management protocols to reduce storage losses and comply with national food safety standards.

Executive Summary

The global stored grain insecticide market reached USD 294.2 Million in 2025, representing a critical segment of the post-harvest crop protection industry. Stored grain insecticides protect wheat, corn, rice, and barley from beetles, weevils, and moths during storage and transit. The market is projected to reach USD 413.0 Million by 2034 at a CAGR of 3.65%.

Bio-insecticides at 34.8% dominate through organic certification requirements and export MRL compliance demand. On Farm application at 48.5% leads via direct farmer adoption at grain storage facilities. Asia-Pacific at 34.6% leads globally through India and China's combined grain production scale and high post-harvest loss exposure.

Key Market Insights

|

Insight |

Data |

|

Dominant Product Type |

Bio-Insecticides – 34.8% share (2025) |

|

Dominant Application |

On Farm – 48.5% market share (2025) |

|

Leading Region |

Asia-Pacific – 34.6% market share (2025) |

|

Market Opportunity |

Microencapsulation technology; smart silo IoT integration; bio-fumigant scale-up in emerging markets |

Key Analytical Observations Supporting the Above Data:

- Bio-Insecticides at 34.8%: Bio-insecticides dominate as they align with regulatory restrictions on synthetic pesticide residues in exported grain and rising organic grain certification demand. Their microbial and botanical active ingredients offer efficacy against weevils and storage beetles while ensuring superior residue safety profiles for export compliance.

- On Farm at 48.5%: On Farm application leads through the highest grain volume treated at farm-level storage. Farmers apply direct-to-grain insecticide dusts, admixtures, and sprays during harvest and storage loading cycles, supported by government extension programs and integrated pest management adoption.

- Asia-Pacific at 34.6%: Asia-Pacific leads through India's and China's massive grain production bases. India stores over 80 million metric tons of food grains annually through public and private networks, generating substantial recurring institutional and farm-level demand for stored grain insecticide protection solutions.

Stored Grain Insecticide Market Overview

The global stored grain insecticide market encompasses the supply of fumigants, contact insecticides, and bio-based pest control agents protecting grains during post-harvest storage and transit. It covers on-farm storage, commercial silo operations, and export shipping facilities across all major grain-producing regions globally.

The ecosystem integrates active ingredient manufacturers, formulation companies, distribution networks, grain storage operators, regulatory agencies, and end-user farmers and cooperatives. Macroeconomic factors include global food demand, post-harvest loss reduction policies, organic grain trade growth, and evolving pesticide residue regulations across importing nations.

Market Dynamics

To evaluate market opportunities, Request Sample

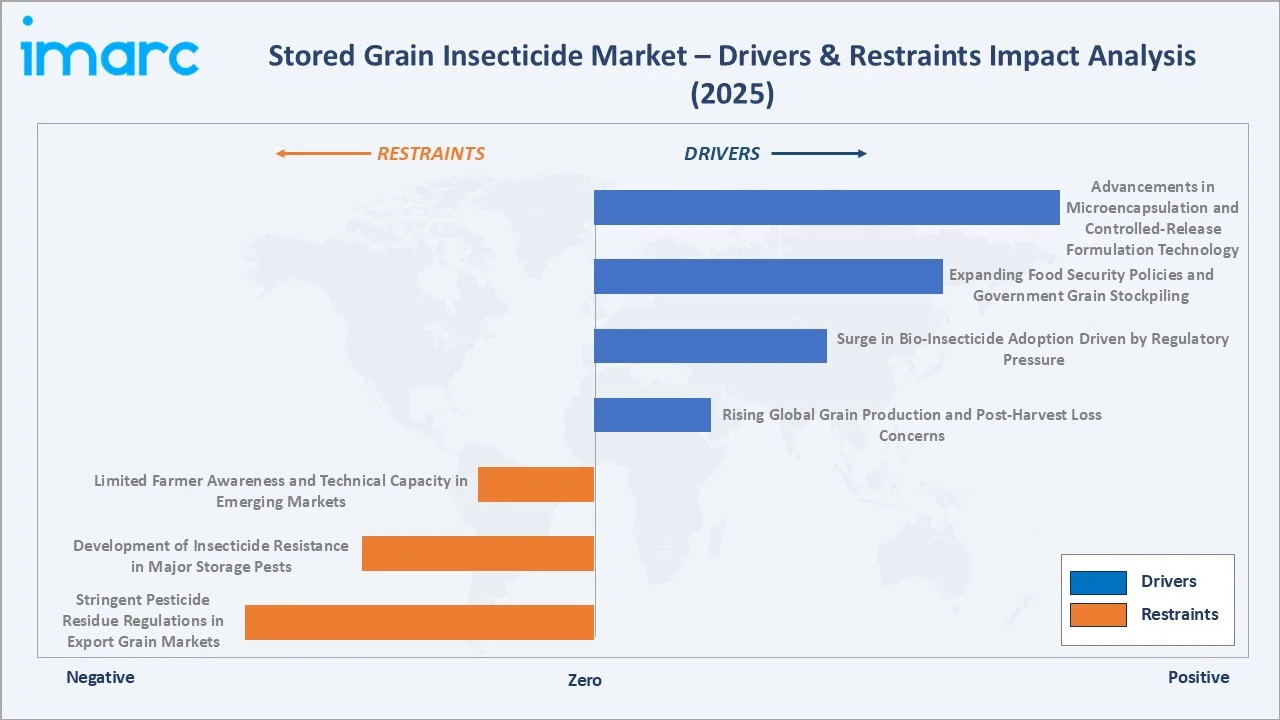

Market Drivers

- Rising Global Grain Production and Post-Harvest Loss Concerns: Global cereal production is projected to rise from its current level by approximately 3.2 billion metric ton by 2033, with insect infestation causing 5–10% annual post-harvest losses. Rising awareness among farmers and governments about storage loss reduction is directly increasing demand for effective stored grain insecticides across all major producing regions.

- Surge in Bio-Insecticide Adoption Driven by Regulatory Pressure: Stringent restrictions on organophosphate and pyrethroid residues in exported grain are compelling grain handlers to adopt bio-insecticides. EU pesticide MRL compliance requirements and USDA National Organic Program requirements are accelerating the structural substitution of synthetic actives with bio-based alternatives in premium export markets.

- Expanding Food Security Policies and Government Grain Buffer Stockpiling: Governments across Asia-Pacific, Latin America, and Africa are increasing strategic grain reserve programs, creating institutional demand for bulk grain insecticide treatment. As of July 1, 2025, the Total Covered and CAP Storage Capacity available with FCI and State agencies for the storage of Central Pool foodgrains stood at 917.83 Lakh Metric Tonnes (LMT), representing a large recurring institutional insecticide procurement opportunity.

- Advancements in Microencapsulation and Controlled-Release Formulation Technology: Microencapsulation enhances insecticide efficacy through prolonged residual activity, reduced volatility, and targeted release. These formulations minimize active ingredient waste and improve grain safety profiles, making them highly attractive for export-oriented grain handlers facing strict residue compliance requirements in destination markets.

Market Restraints

- Stringent Pesticide Residue Regulations in Export Grain Markets: Increasingly restrictive MRL thresholds in the EU, Japan, and South Korea create compliance complexity for grain exporters using conventional insecticides. Non-compliance risks cargo rejection, trade penalties, and reputational damage, limiting the addressable market for certain synthetic insecticide classes in premium export grain channels.

- Development of Insecticide Resistance in Major Storage Pests: Prolonged use of organophosphates has driven documented resistance in Tribolium castaneum, Rhyzopertha dominica, and Sitophilus granarius. Resistance reduces product efficacy, increases application rates, and compels reformulation investment, raising operating costs for both manufacturers and commercial grain handlers.

- Limited Farmer Awareness and Technical Capacity in Emerging Markets: In sub-Saharan Africa and South and Southeast Asia, inadequate knowledge of proper application rates, timing, and storage hygiene limits effective product utilization. Underdeveloped agricultural extension networks and poor cold-chain infrastructure constrain market penetration in high-potential emerging economies.

Market Opportunities

- Microencapsulated Bio-Fumigant Commercialization: Bio-fumigants based on essential oil actives and CO2-generating systems represent emerging eco-friendly alternatives to methyl bromide and aluminum phosphide. Growing regulatory phase-outs of conventional fumigants in developed markets create structurally expanding demand for novel bio-fumigant solutions with compliant residue profiles.

- IoT-Integrated Smart Silo Systems Creating Precision Insecticide Demand: IoT sensor networks integrated into modern grain silos are creating demand for precision-dosed insecticide systems compatible with automated fumigation. Smart storage infrastructure investments by agribusiness operators in North America and Europe are shifting procurement toward data-driven grain protection solutions.

Market Challenges

- Complex Multi-Jurisdiction Regulatory Approval Processes: Registering a stored grain insecticide across the EU, US, Australia, and ASEAN markets requires separate submissions, toxicological packages, and residue studies per jurisdiction. Multi-year, multi-million-dollar approval costs create barriers for smaller manufacturers and slow bio-based product commercialization timelines.

- Price Competitiveness of Generic Organophosphates Constraining Bio-Insecticide Penetration: Commodity-priced generic organophosphates are available at substantially lower cost than bio-insecticides and novel formulations. In price-sensitive emerging markets where compliance requirements are less stringent, generics maintain dominant share, constraining the penetration of higher-value bio-insecticide segments.

Emerging Market Trends

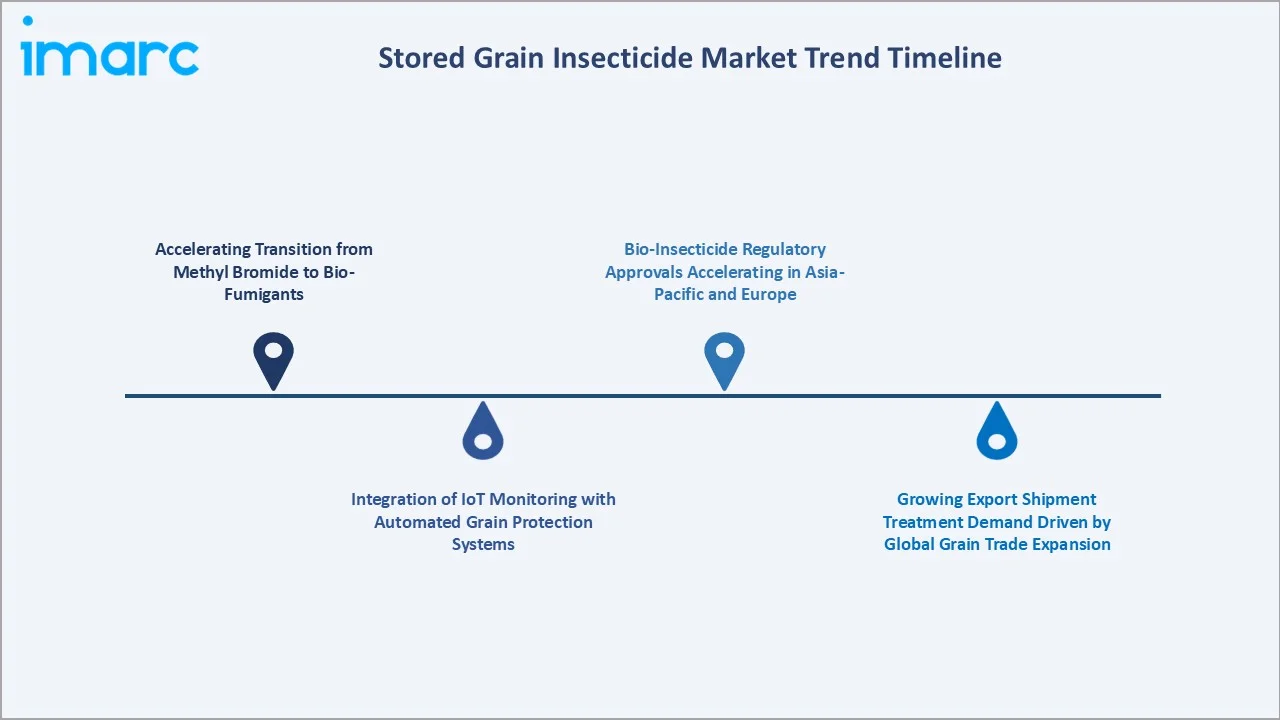

1. Accelerating Transition from Methyl Bromide to Bio-Fumigants

The global phase-out of methyl bromide under the Montreal Protocol is creating structurally growing demand for alternative fumigation solutions. Bio-based fumigants including phosphine-generation systems, essential oil formulations, and CO2 treatments are scaling commercially. Developed markets with narrowing critical-use exemptions are compelling grain exporters to qualify alternative fumigation protocols.

2. Integration of IoT Monitoring with Automated Grain Protection Systems

IoT-enabled grain storage systems incorporating real-time temperature, moisture, and CO2 sensors are enabling precision-timed insecticide application. Automated aeration and fumigation systems reduce waste, improve efficacy, and provide traceability documentation for export compliance. Commercial grain elevator operators in North America and Australia are leading this adoption at scale.

3. Bio-Insecticide Regulatory Approvals Accelerating in Asia-Pacific and Europe

Regulatory bodies in the EU and key Asia-Pacific markets are fast-tracking approval pathways for bio-insecticides including Bacillus thuringiensis formulations, diatomaceous earth, and plant essential oil actives. The EU Farm to Fork Strategy's target to reduce chemical pesticide use by 50% by 2030 creates a favorable regulatory environment for bio-insecticide expansion.

4. Growing Export Shipment Treatment Demand Driven by Global Grain Trade Expansion

Expanding global grain trade volumes from major exporters including the US, Australia, Canada, and Brazil are increasing demand for export-grade grain fumigation and contact insecticide treatment. Importing countries' phytosanitary requirements and MRL compliance standards are driving adoption of compliant, premium insecticide solutions in export grain handling channels.

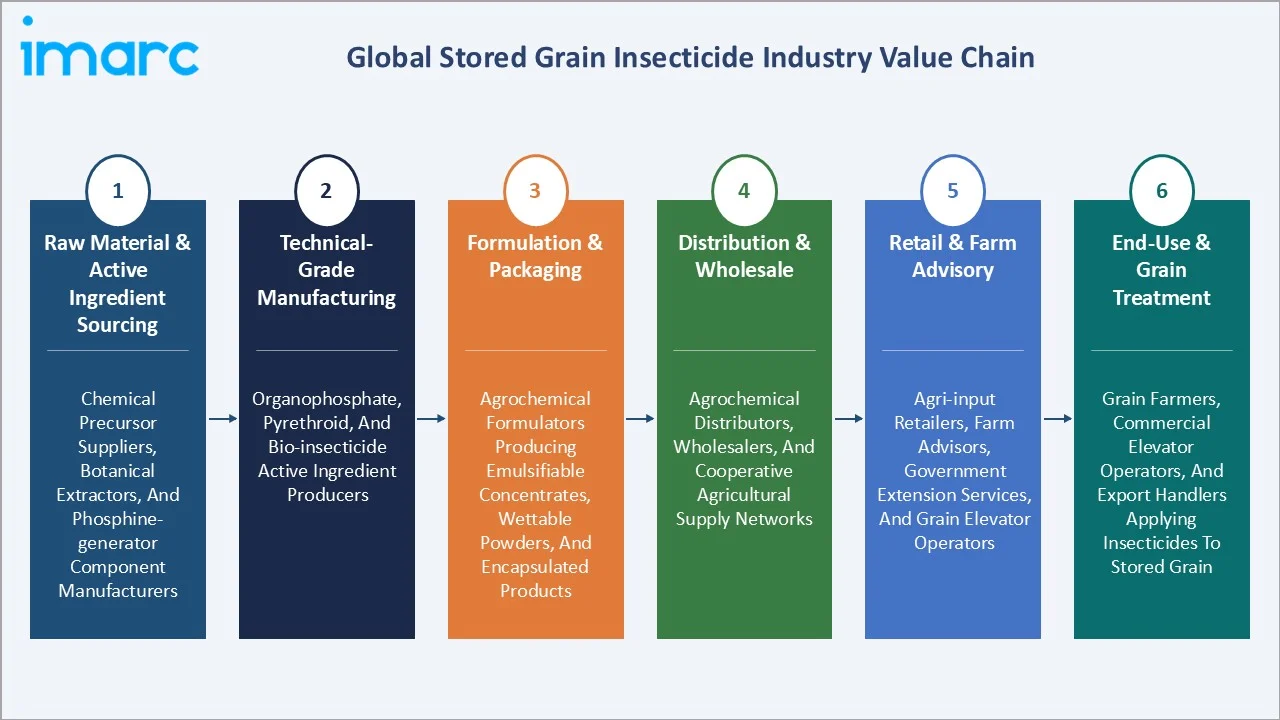

Industry Value Chain Analysis

The stored grain insecticide value chain integrates raw material and active ingredient sourcing, technical-grade manufacturing, formulation and packaging, distribution logistics, retail and farm advisory services, and end-user grain treatment application. The chain is moderately fragmented at distribution and retail tiers with consolidation at active ingredient manufacturing.

|

Stage |

Key Participants |

|

Raw Material & Active Ingredient Sourcing |

Chemical precursor suppliers, botanical extractors, and phosphine-generator component manufacturers |

|

Technical-Grade Manufacturing |

Organophosphate, pyrethroid, and bio-insecticide active ingredient producers |

|

Formulation & Packaging |

Agrochemical formulators producing emulsifiable concentrates, wettable powders, dusts, and encapsulated products |

|

Distribution & Wholesale |

Agrochemical distributors, wholesalers, and cooperative agricultural supply networks |

|

Retail & Farm Advisory |

Agri-input retailers, farm advisors, government extension services, and grain elevator operators |

|

End-Use & Grain Treatment |

Farmers, grain cooperatives, commercial silo operators, and export grain terminal handlers |

Formulation and packaging generate the highest margins through branded microencapsulated and controlled-release products. Digital agri-input platforms are compressing traditional distribution margins by enabling direct-to-farmer sales with integrated application guidance, reshaping the downstream commercial architecture of the value chain.

Technology Landscape in the Stored Grain Insecticide Industry

Phosphine Fumigation Technology

Phosphine (PH3) generated from aluminum phosphide and magnesium phosphide formulations remains the dominant global fumigation technology due to broad-spectrum efficacy, low residue profiles, and cost-effectiveness. Controlled atmosphere fumigation systems using automated phosphine generation and recirculation are improving treatment efficiency and reducing environmental exposure risks in commercial grain facilities.

Bio-Insecticide and Microbial Formulation Technology

Bio-insecticide technology includes diatomaceous earth physical-mode actives, spinosad-based formulations, Beauveria bassiana entomopathogenic fungi, and plant essential oil vapor-phase actives. These technologies offer complementary or replacement efficacy to synthetic chemicals with superior environmental and residue safety profiles, driving their adoption in organic and export-grade grain markets globally.

Microencapsulation and Controlled-Release Formulation Technology

Microencapsulation encapsulates active ingredients in polymer shells enabling controlled release over extended storage periods. This extends residual activity, reduces volatility loss, minimizes non-target organism exposure, and improves grain safety profiles for export compliance.

AI-Integrated Precision Monitoring and Application Technology

AI-powered pest detection systems analyze grain storage imagery to identify key pest species—including Lesser Grain Borer, Red Flour Beetle, and Maize Weevil—achieving detection accuracies above 95%, enabling precision-triggered insecticide application. Integration with IoT sensor networks allows real-time dosing decisions, reducing insecticide consumption, improving efficacy, and generating auditable compliance records for export grain trade documentation.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Product Type |

Bio-Insecticides |

34.8% |

2025 |

|

Application |

On Farm |

48.5% |

2025 |

|

Region |

Asia-Pacific |

34.6% |

2025 |

By Product Type

Bio-insecticides lead at 34.8% in 2025, capturing the highest-growth segment driven by organic grain certification demand and regulatory restrictions on synthetic actives in export markets. Their natural active ingredients deliver efficacy against primary storage pests including Tribolium castaneum and Sitophilus species without generating synthetic chemical residue concerns.

To access detailed market analysis, Request Sample

Organophosphates at 30.6% retain significant share through commodity pricing and established farm-level familiarity, particularly in emerging markets. Pyrethroids at 22.7% serve as effective contact insecticides for surface treatment of storage facilities. Others at 11.9% include fumigants, neonicotinoids, and newer actives addressing insecticide resistance management needs.

By Application

On Farm application leads at 48.5% through the highest grain volume treated at farm-level storage. Direct-to-grain treatment during harvest and storage loading is the primary application method, with farmers applying insecticide dusts, admixtures, and sprays to protect grain in on-farm bins, bags, and silos during the storage period preceding sale or consumption.

Off Farm at 32.4% covers commercial grain elevator, cooperative, and government warehouse storage operations. Export Shipments at 19.1% represent the highest per-unit-value application, driven by phytosanitary compliance requirements for grain exported to premium markets including the EU, Japan, and South Korea that enforce stringent insect-free and residue-compliant import standards.

Regional Market Insights

|

Region |

Share (2025) |

Key Drivers & Characteristics |

|

Asia-Pacific |

34.6% |

Large grain production base, high on-farm storage losses, government food security programs, and growing organic grain export demand |

|

North America |

24.8% |

Advanced commercial grain infrastructure, export compliance requirements, bio-insecticide adoption, and precision storage technology integration |

|

Europe |

21.7% |

Stringent EU pesticide regulations, Farm to Fork bio-insecticide transition, methyl bromide phase-out compliance, and organic grain demand |

|

Latin America |

11.2% |

Expanding grain export capacity, growing soybean and corn storage infrastructure, and increasing awareness of post-harvest loss reduction |

|

Middle East and Africa |

7.7% |

Growing grain import storage treatment demand, government food security stockpiling programs, and emerging modern warehouse infrastructure |

Asia-Pacific at 34.6% leads through India's large public food grain storage network and China's commercial grain reserve system. North America at 24.8% reflects the US and Canadian grain export industries' high compliance standards and growing adoption of smart storage insecticide technologies.

Europe at 21.7% is undergoing a structural shift toward bio-insecticides under the EU's Farm to Fork Strategy. Latin America at 11.2% and MEA at 7.7% represent early-stage but growing markets, with Brazil's soybean export infrastructure and Gulf Cooperation Council government grain reserve programs emerging as key regional growth drivers.

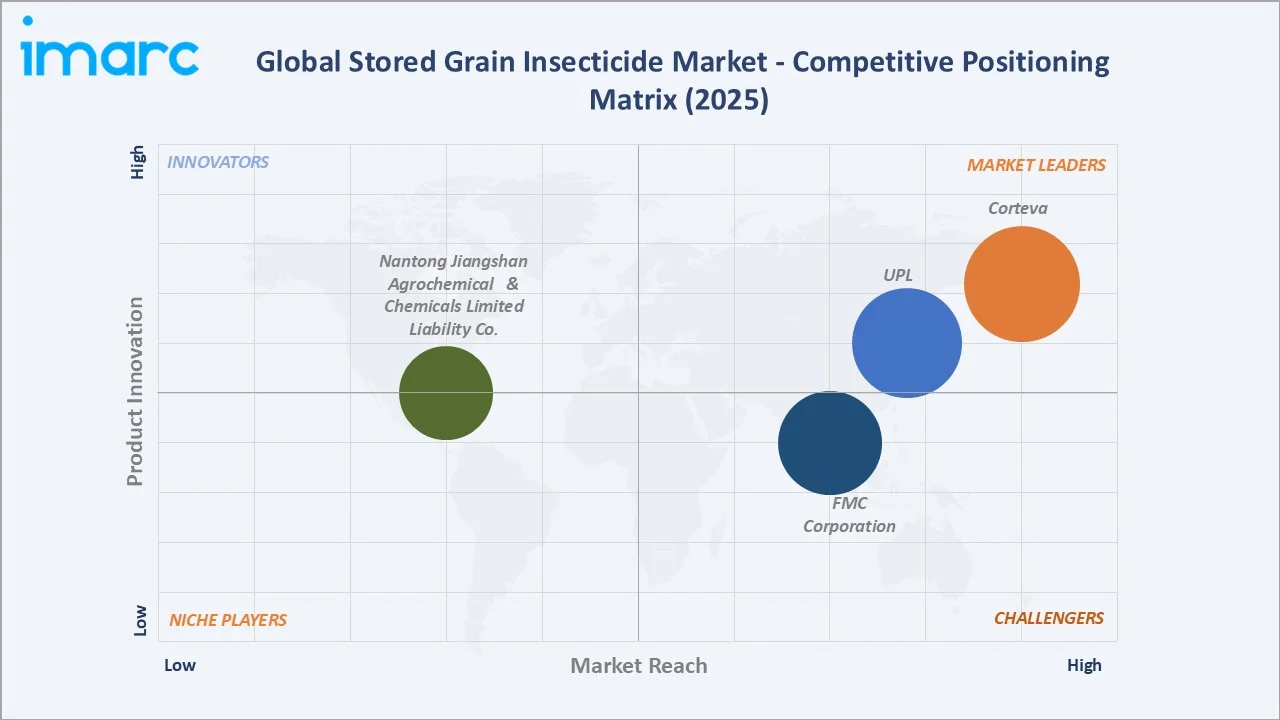

Competitive Landscape

The global stored grain insecticide market is moderately consolidated at the multinational agrochemical level, with three distinct competitive tiers: global crop protection majors, regional agrochemical specialists, and generic manufacturer segments competing primarily on price in cost-sensitive emerging markets.

|

Company Name |

Key Products |

Market Position |

Core Strength |

|

FMC Corporation |

Brigade, talstar |

Strong Challenger |

Phosphine fumigation product leadership with strong distribution in major grain belt markets |

|

Corteva |

Qalcova Active and Jemvelva Active (Spinosyns) |

Leader |

Bio-derived spinosad active ingredient with export-compliant residue profile for premium grain markets |

|

UPL |

Bisect Duo 100EC, Chlorban 500EC, Hunter 150G |

Leader |

Strong emerging market distribution network with cost-competitive fumigant and contact insecticide portfolio |

|

Nantong Jiangshan Agrochemical & Chemicals Limited Liability Co. |

Dichlorvos, Trichlorfon |

Emerging Player |

Low-cost active ingredient manufacturing capability serving price-sensitive Asian and African markets |

Key players include FMC Corporation, Corteva, UPL, Nantong Jiangshan Agrochemical & Chemicals Limited Liability Co., and others.

Key Company Profiles

FMC Corporation

FMC Corporation is a US-based agricultural sciences company with a presence in the stored grain insecticide market through its bifenthrin-based contact insecticide portfolio, offering grain bin surface treatment and storage facility protection solutions distributed across North America, Asia-Pacific, and Latin American grain markets.

- Key Products: Brigade, talstar

- Strategic Focus: Strengthening broad-spectrum bifenthrin-based grain storage facility protection programs alongside its diamide insecticide franchise for pre-harvest field crop pest management, targeting grain belt markets in North America, Brazil, and Australia where integrated pre- and post-harvest insect control programs create cross-portfolio demand.

Corteva

Corteva is a US-based pure-play agriculture company with a growing presence in the stored grain insecticide market through its naturally derived spinosyn insecticide portfolio, offering bio-based grain protection solutions registered for direct grain treatment in organic and conventional storage systems across major grain-producing markets globally.

- Key Products: Qalcova Active and Jemvelva Active (Spinosyns)

- Strategic Focus: Advancing the global spinosyn portfolio through broader registration of products providing farmers worldwide with effective, naturally derived insect control options across more than 250 crops, including expanding stored grain and post-harvest applications in organic-certified and export-compliant grain markets.

UPL

UPL is an India-headquartered global crop protection company with a significant presence in the stored grain insecticide market through its pirimiphos-methyl and organophosphate-based grain protectant portfolio, offering cost-competitive post-harvest insecticide solutions across Asia-Pacific, Africa, Latin America, and Europe.

- Key Products: Bisect Duo 100EC, Chlorban 500EC, Hunter 150G

- Strategic Focus: UPL Limited plays a competitive role through its wide agrochemical portfolio and strong presence in emerging markets, with cost-effective product offerings that appeal to price-sensitive regions where post-harvest losses remain a significant concern, and a global manufacturing footprint and distribution partnerships that enable broad access to stored grain insecticide solutions. The company is advancing novel formulation technologies to address growing insecticide resistance in primary storage pests across South Asia, Sub-Saharan Africa, and Southeast Asia.

Market Concentration Analysis

The stored grain insecticide market is moderately concentrated at the global multinational level. Top 4-5 companies collectively account for approximately 45–55% of global market revenue. Generic organophosphate manufacturers from China and India account for an estimated 20–25% of global volume through cost-competitive commodity products.

Market concentration is expected to decline moderately over the forecast period as bio-insecticide specialists gain share, new bio-based active ingredient registrations expand the competitive field, and regional agrochemical companies in Asia-Pacific develop higher-value formulation capabilities serving domestic export grain markets.

Investment & Growth Opportunities

Highest Growth Segments

Bio-insecticides (~4.2% CAGR), On Farm application (~4.0% CAGR), Asia-Pacific region (~4.5% CAGR), microencapsulated formulations (~5.0% CAGR), and export shipment treatment segment (~3.8% CAGR from growing global grain trade volumes) represent the highest-growth investment vectors through 2034.

Emerging Investment Opportunities

Smart grain storage fumigation systems integrating IoT sensors with automated insecticide dosing represent the highest-value emerging segment. Bio-based fumigants addressing the methyl bromide phase-out gap represent an underpenetrated high-value opportunity for export-grade grain treatment in North America and Europe.

Investment Themes

- Bio-insecticide formulation technology investment: capturing the regulatory-driven substitution of synthetic actives in developed markets through registered bio-based alternatives with export-compliant residue profiles and organic certification compatibility.

- Asia-Pacific distribution network expansion: targeting India and Southeast Asian grain belt markets where post-harvest loss reduction programs and food security infrastructure investments are creating structurally growing demand for effective grain protection solutions.

Future Market Outlook (2026-2034)

The global stored grain insecticide market is projected to grow from USD 294.2 Million in 2025 to USD 413.0 Million by 2034, delivering a 3.65% CAGR. The market's anchor value of USD 351.9 Million in 2030 reflects structural growth across all geographies, with bio-insecticide substitution and smart storage adoption accelerating in the latter forecast years.

Bio-insecticides are projected to surpass 40% market share by 2030 as EU Farm to Fork mandates, US organic grain premiums, and Asian export compliance requirements collectively accelerate the substitution of synthetic organophosphate and pyrethroid actives with bio-derived and microencapsulated alternatives across commercial and institutional grain storage.

AI-integrated precision detection and automated dosing technology will create differentiated demand for compatible precision-dosed insecticide systems. This will establish premium market segments within the broader stored grain insecticide industry, concentrating value creation in innovation-oriented companies with both product and technology platform capabilities.

Research Methodology

Primary Research

Primary research comprised structured interviews with 45+ industry stakeholders (2025), including agrochemical company executives, grain storage facility managers, agricultural extension officers, export grain terminal operators, and national food safety regulatory officials across key grain-producing regions.

Secondary Research

Secondary research encompassed company annual reports, FAO food loss and waste reports, USDA grain storage and trade data, EU pesticide MRL regulatory updates, APVMA Australian pesticide registration data, and national grain board procurement records. Over 55 secondary sources were reviewed across all major producing regions.

Forecasting Models

Market revenue forecasts were developed using a grain production-based bottom-up model: (i) global grain production forecast by crop type; (ii) proportion of grain requiring post-harvest insecticide treatment; (iii) average treatment cost per metric ton by insecticide segment; and (iv) technology premium adjustment for bio-insecticide and controlled-release formulations versus commodity generics.

Stored Grain Insecticide Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Product Types Covered | Organophosphate, Pyrethroids, Bio-Insecticides, Others |

| Applications Covered | On Farm, Off Farm, Export Shipment |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | FMC Corporation, Corteva, UPL, Nantong Jiangshan Agrochemical & Chemicals Limited Liability Co., etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the stored grain insecticide market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the global stored grain insecticide market.

- The study maps the leading as well as the fastest growing regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the stored grain insecticide industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and?provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Stored Grain Insecticide Market Report

The market reached USD 294.2 Million in 2025, driven by bio-insecticides leading at 34.8%, On Farm application at 48.5%, rising grain production, and Asia-Pacific commanding 34.6% market share through India's and China's large grain storage insecticide demand base.

The market grows at 3.65% CAGR during 2026-2034, reaching USD 413.0 Million by 2034. Growth reflects post-harvest loss reduction mandates, bio-insecticide regulatory substitution trends, and expanding global grain trade compliance requirements driving premium insecticide adoption.

Bio-insecticides lead at 34.8% in 2025, capturing organic certification and export MRL compliance demand. This segment grows fastest at ~4.2% CAGR through regulatory-driven substitution of organophosphates and pyrethroids in developed export grain markets globally.

On Farm application leads at 48.5% through direct farmer grain treatment at point-of-harvest storage. This reflects the largest grain volume treated globally, supported by government post-harvest loss reduction programs and increasing farm-level storage infrastructure investments.

Asia-Pacific leads at 34.6% through India's large public food grain storage programs, China's commercial grain reserve system, and the region's combined annual cereal production exceeding 1.5 billion metric tons requiring regular post-harvest insect protection treatment.

Leading companies include FMC Corporation, Corteva, UPL, and Nantong Jiangshan Agrochemical & Chemicals Limited Liability Co., among others.

The market is projected to reach USD 351.9 Million by 2030, with bio-insecticides surpassing 38% market share, smart silo-integrated treatment systems gaining commercial adoption, and Asia-Pacific government stockpiling programs generating sustained institutional procurement volumes.

Three priority investment opportunities: bio-insecticide formulation technology for export-compliant grain protection; smart silo IoT-integrated precision fumigation systems; and Asia-Pacific distribution network expansion targeting India and Southeast Asia's high post-harvest loss reduction potential markets.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)