Turkey Diabetes Market Report Size, Share, Trends and Forecast by Segment, Distribution Channel, 2026-2034

Turkey Diabetes Market Size, Share, Trends & Forecast (2026-2034)

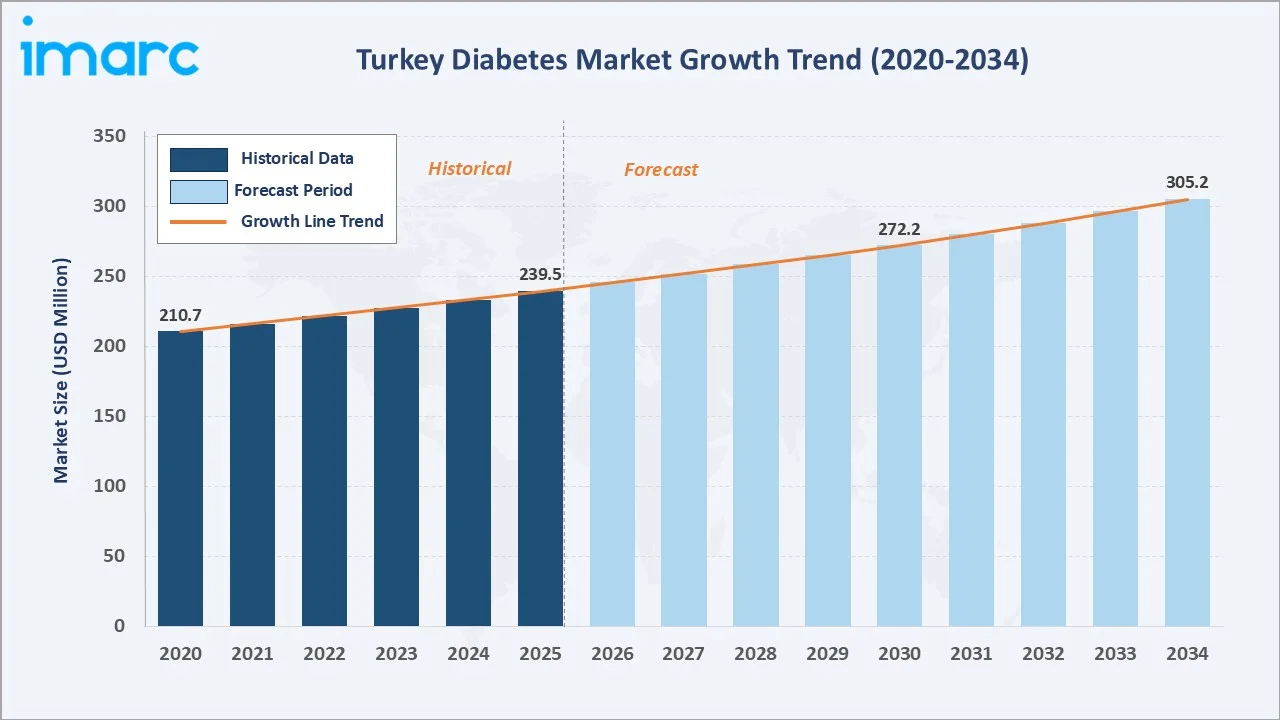

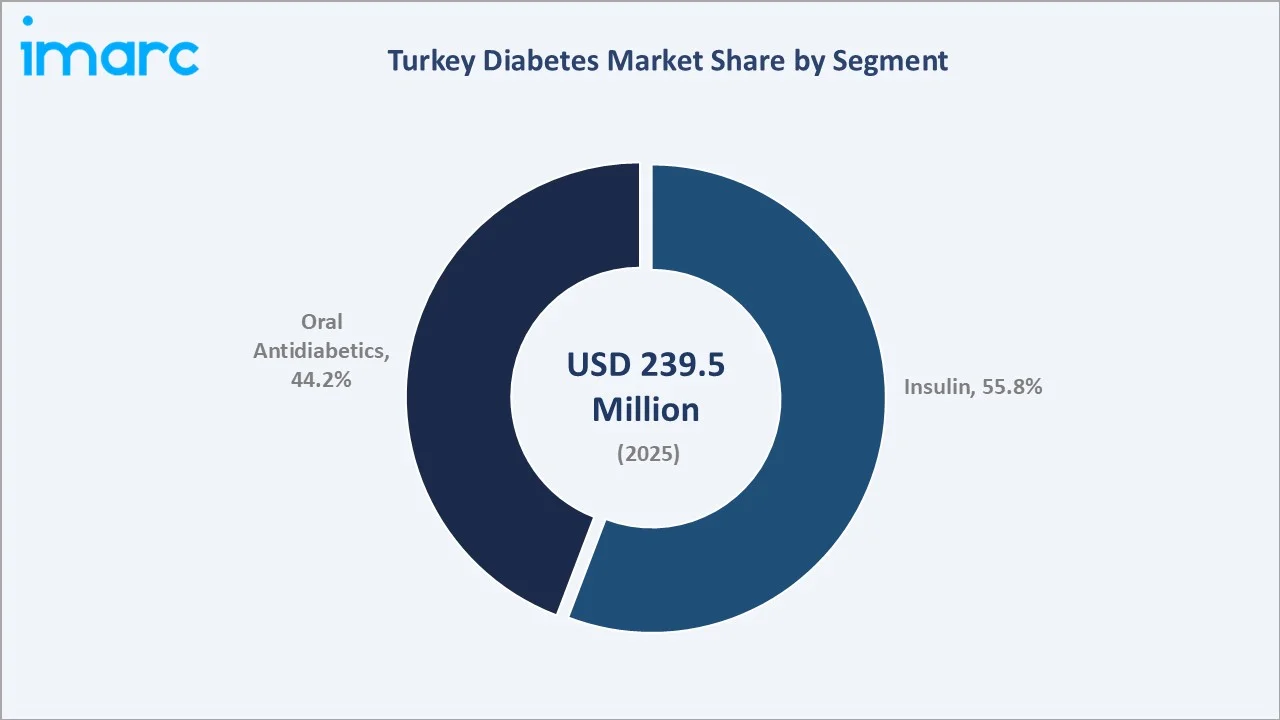

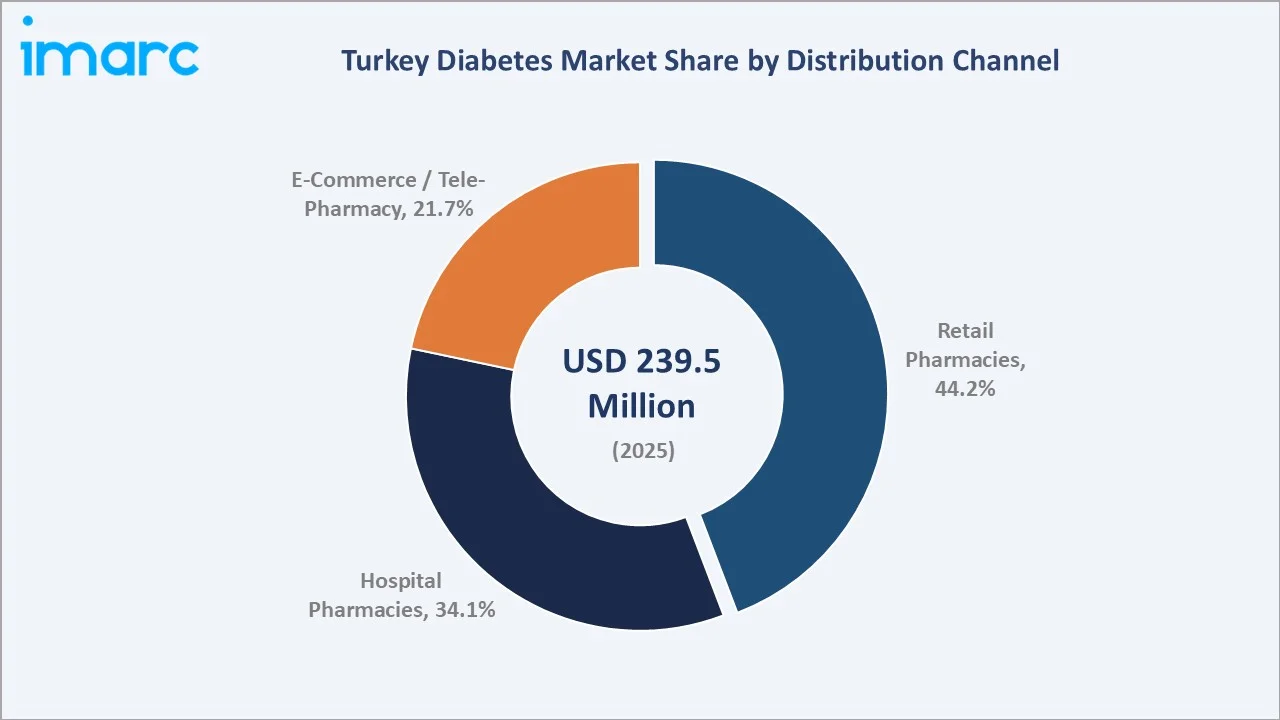

The Turkey diabetes market size was valued at USD 239.5 Million in 2025 and is projected to reach USD 305.2 Million by 2034, exhibiting a CAGR of 2.60% during the forecast period 2026-2034. Rising adult diabetes prevalence, expanding obesity rates, accelerating urbanization, and the national digital health agenda are driving Turkey diabetes market growth. Insulin therapies lead at 55.8% share in 2025, while retail pharmacies account for 44.2% of national dispensing volumes.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 239.5 Million |

|

Forecast Market Size (2034) |

USD 305.2 Million |

|

CAGR (2026-2034) |

2.60% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Leading Segment |

Insulin (55.8%, 2025) |

|

Leading Distribution Channel |

Retail Pharmacies (44.2%, 2025) |

The Turkey diabetes market growth trajectory from 2020 through 2034 reflects a steady expansion powered by chronic disease burden, rapid urbanization, and the scale-up of digital pharmacy and tele-diabetes channels across public and private care networks.

To get more information on this market, Request Sample

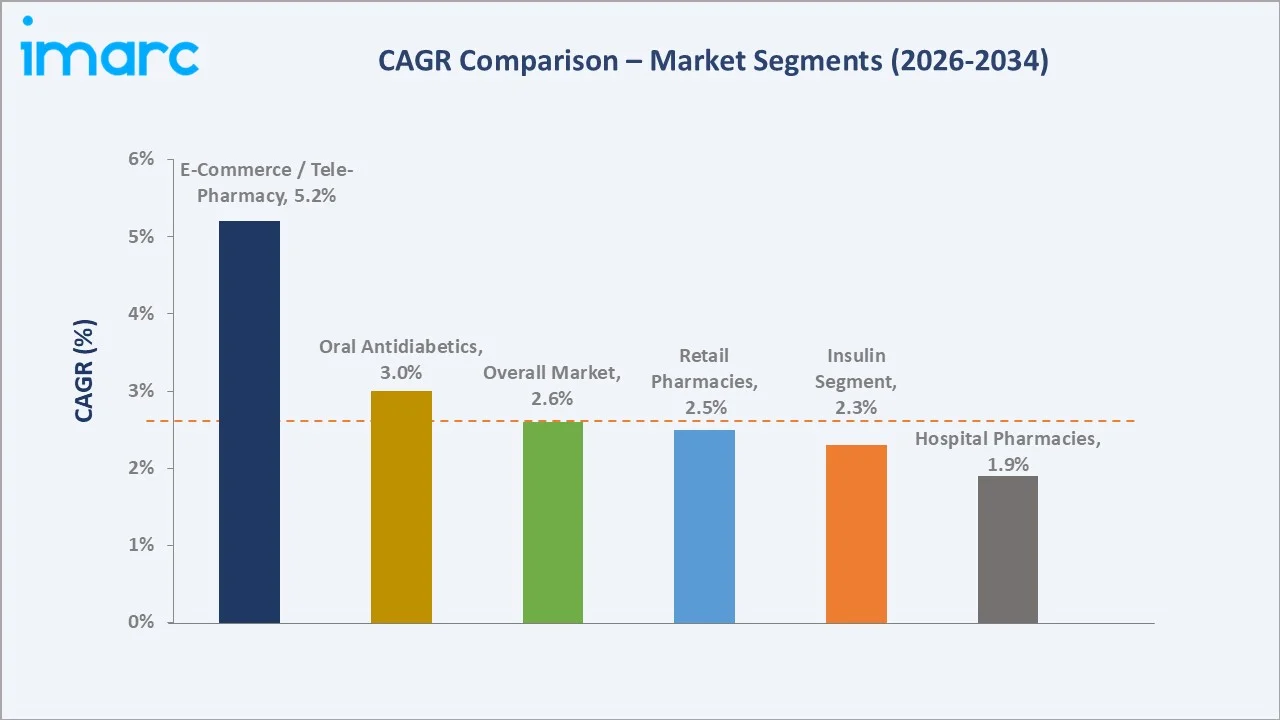

Sub-segment CAGR comparisons highlight e-commerce and tele-pharmacy as the fastest-growing distribution channel through 2034, while oral antidiabetics outpace insulin on a growth-rate basis on the back of GLP-1 and SGLT-2 momentum.

Executive Summary

The Turkey diabetes market is undergoing structural transformation, driven by adult diabetes prevalence, adult obesity, and a rapidly urbanizing population of over 85 million. Valued at USD 239.5 Million in 2025, the market is forecast to reach USD 305.2 Million by 2034 at a CAGR of 2.60%.

Insulin therapies command a 55.8% share in 2025, reflecting a large type-1 patient base and advanced type-2 cases. Oral antidiabetics represent 44.2% of national demand, growing faster on SGLT-2 and GLP-1 momentum. Retail pharmacies account for 44.2% of dispensing across more than 27,000 community pharmacies nationwide.

Key Market Insights

|

Insight |

Data |

|

Largest Segment |

Insulin - 55.8% share (2025) |

|

Second Segment |

Oral Antidiabetics - 44.2% share (2025) |

|

Leading Distribution Channel |

Retail Pharmacies - 44.2% share (2025) |

|

Fastest Growing Channel |

E-Commerce / Tele-Pharmacy - ~5.2% CAGR |

|

Top Companies |

Novo Nordisk, Sanofi, Eli Lilly, AstraZeneca, Abdi Ibrahim |

Key Analytical Observations Supporting the Above Data:

- Insulin's 55.8% dominance in Turkey has over 7 million people living with diabetes, of whom approximately 1 million are insulin users. The insulin market is primarily driven by originator products, while biosimilar penetration remains in the early stages of adoption under SGK’s centralized reimbursement and tender-based procurement system. However, detailed national market share breakdowns for insulin and biosimilars are not consistently published in official datasets.

- Oral antidiabetics' 44.2% share is underpinned by expanding type-2 diagnoses and strong SGLT-2 uptake. GLP-1 receptor agonist prescriptions rose 24% in 2025 as obesity-linked demand accelerated in urban centers.

- Retail pharmacies' 44.2% lead is supported by more than 27,000 community pharmacies nationwide - one of the densest networks in the Middle East and Southeast Europe, underpinned by SGK-driven reimbursement pathways.

- E-Commerce's 21.7% share is expanding rapidly at ~5.2% CAGR, led by platforms such as Dermocare, Eczane Online, and Nobel e-Pharmacy. Digital-first tele-pharmacy orders grew 25-30% year-on-year in 2025.

- Biosimilar and local manufacturing reached ~24% of total diabetes therapy volumes in 2025, reflecting Turkey's strong localization under the Global Pharma Turkey strategy and incentives from TITCK.

Turkey Diabetes Market Overview

Diabetes therapies in Turkey span insulin formulations, oral antidiabetics, GLP-1 receptor agonists, SGLT-2 inhibitors, and adjunct medical devices. The market includes rapid-acting analogs, long-acting basal insulins, fixed-ratio combinations, biosimilar insulins, and smart delivery devices - serving patients across type-1 and type-2 diabetes management within a highly centralized public-private care system.

The industry operates under oversight from the Turkish Medicines and Medical Devices Agency (TITCK) and reimbursement administered by the Social Security Institution (SGK). Growth is supported by healthcare expenditure at 4.6% of GDP in 2024, rising per-capita health spending, and structured national diabetes control programs. The market is undergoing a structural shift toward connected, digital, and value-based diabetes care aligned with the Vision 2053 health agenda.

Market Dynamics

To evaluate market opportunities, Request Sample

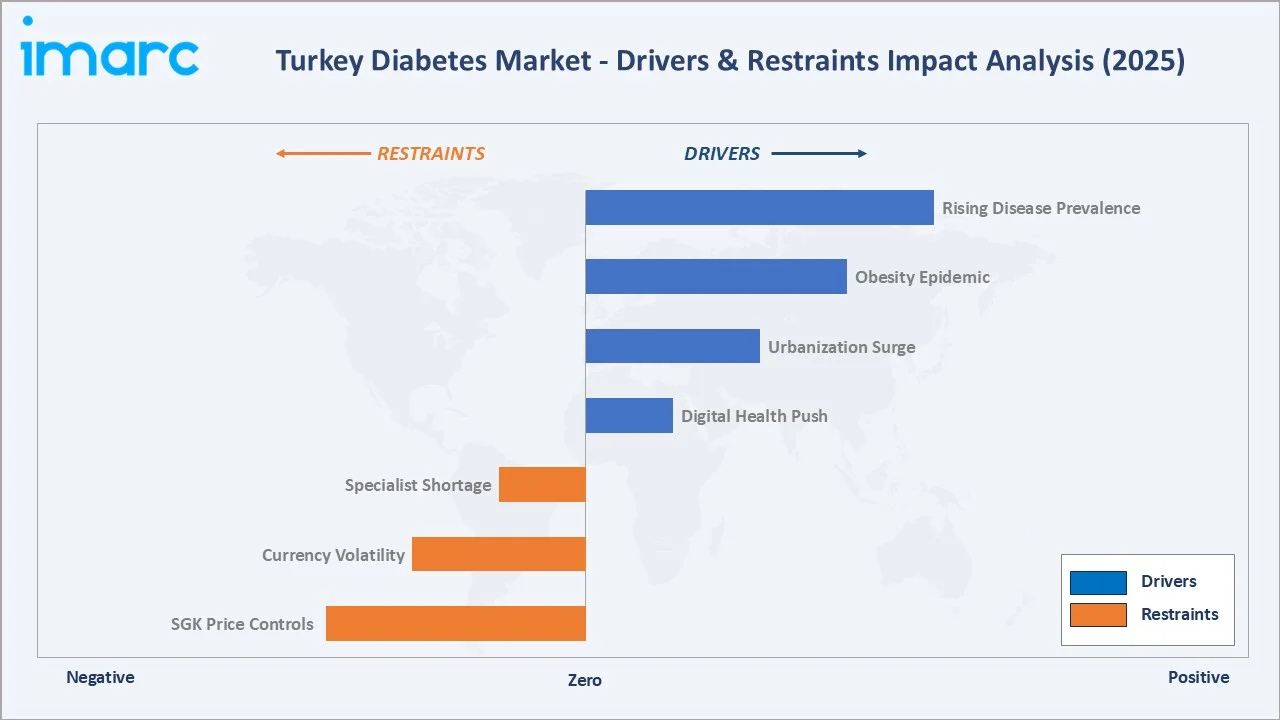

Market Drivers

- Rising Disease Prevalence: Adult diabetes prevalence reached 14.5% in Turkey in 2025, among the highest in the Middle East and Southeast Europe region. Türkiye’s healthcare system continues to reflect a large and growing disease burden, with diabetes prevalence exceeding 7 million diagnosed individuals and rising steadily over time, supported by increasing annual new cases that continue to expand the treatment-eligible population.

- Obesity Epidemic: Turkish adult obesity rates exceeded 32% in 2024 - the highest in the OECD. This structurally elevates type-2 diabetes incidence, long-term therapy demand, and adoption of GLP-1 and dual GIP/GLP-1 agonists across urban centers.

- Urbanization Surge: Urban population reached 77% in 2024, concentrated in Istanbul, Ankara, Izmir, and Bursa. Urbanization elevates sedentary lifestyles, processed food consumption, and screening density - directly expanding the diagnosed patient pool each year.

- Digital Health Push: The Ministry of Health expanded e-Nabiz, the national digital health platform, to serve over 75 million citizens in 2024. Integrated diabetes care modules drive earlier diagnosis, better titration, and CGM uptake across public hospital networks.

Market Restraints

- SGK Price Controls: The Social Security Institution's reference pricing and mandatory tender-based reimbursement compress manufacturer margins, particularly for off-patent insulins and mature oral antidiabetics. Average unit prices for older analogs fell ~17% between 2022 and 2025.

- Currency Volatility: Turkish lira depreciation pressured import-reliant therapy pricing. With more than 68% of finished dosage forms imported in 2025, foreign exchange swings translate directly into cost inflation and tender margin pressure for multinationals.

- Specialist Shortage: Turkey has a comparatively low physician supply within the OECD context, with around 2–3 doctors per 1,000 population and significantly fewer specialist physicians per capita, including endocrinologists, than the OECD average, reflecting broader health workforce constraints across the system. Specialist bottlenecks limit uptake of complex regimens and device-based therapies beyond Istanbul, Ankara, and Izmir.

Market Opportunities

- Biosimilar and Localization: Turkey's Global Pharma Turkey strategy positions local manufacturers such as Abdi Ibrahim, Deva, and Bilim Ilac for biosimilar insulin and GLP-1 production.

- CGM Reimbursement Expansion: SGK progressively expanded CGM reimbursement to type-1 pediatric patients in 2023. Broader insulin-treated type-2 coverage is expected by 2027, potentially unlocking a multi-million-dollar device and data services opportunity.

- Obesity-Diabetes Crossover: Obesity rates exceeding 32% directly expand eligibility for GLP-1 and dual GIP/GLP-1 therapies.

Market Challenges

- Reimbursement Lag: Average SGK reimbursement timelines for novel biologics reached 16 months in 2024, including price negotiation. This lag delays patient access to next-generation incretin therapies relative to EU peers such as Germany and Spain.

- Complication Burden: Diabetes-related complications - nephropathy, retinopathy, and neuropathy - exceed 43% among diagnosed Turkish patients. Complications elevate total cost of care and strain SGK budgets, prompting stricter formulary controls and tender preferences.

- Regional Access Gaps: Rural and Eastern Anatolia regions face therapy access limitations, with endocrinologist availability below 0.6 per 100,000 in several provinces. This fragmentation delays uniform national adoption of advanced therapies and devices.

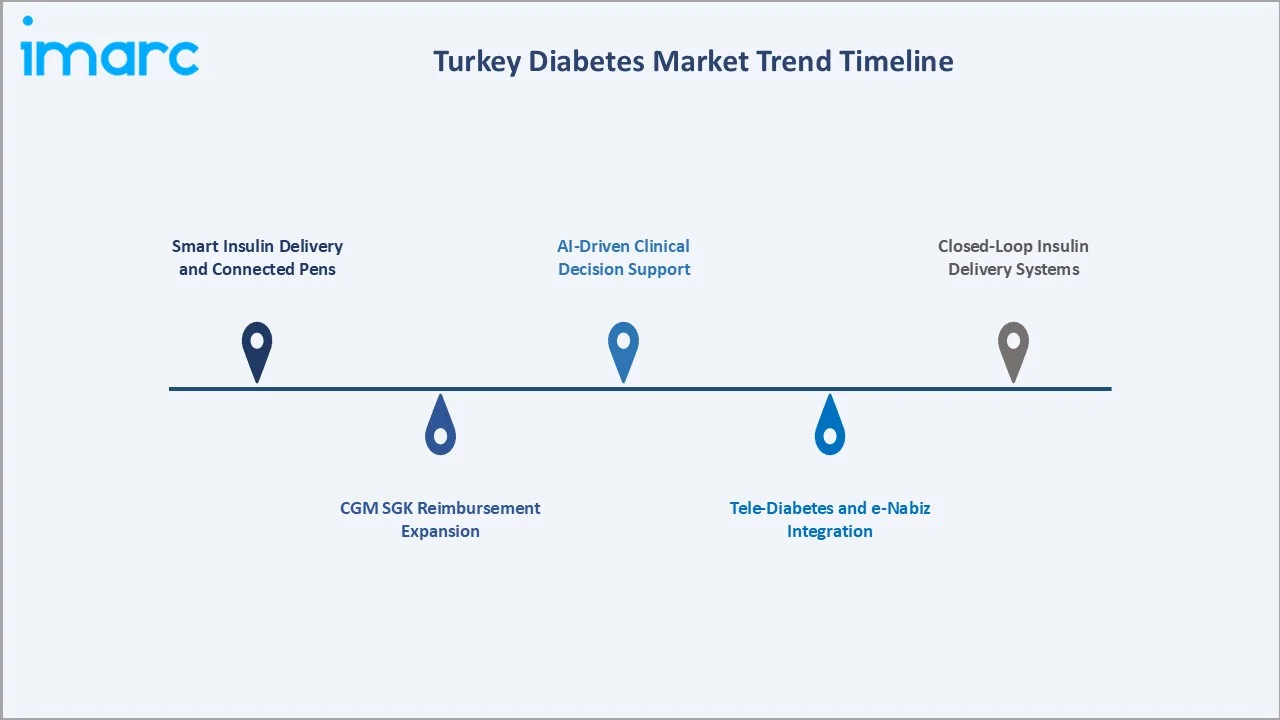

Emerging Market Trends

1. Smart Insulin Delivery and Connected Pens

Smart insulin pens with Bluetooth dose tracking grew 21% in unit sales during 2025. These devices integrate with e-Nabiz and third-party apps such as mySugr to improve adherence and support remote titration among type-1 and advanced type-2 patients across Istanbul and Ankara tertiary centers.

2. CGM SGK Reimbursement Expansion

SGK expanded CGM reimbursement to type-1 pediatric patients in 2023. CGM penetration is projected to increase steadily over the coming years, with Abbott FreeStyle Libre and Medtronic leading device share. Broader coverage among insulin-treated type 2 patients is also expected to expand in the medium term.

3. Tele-Diabetes and e-Nabiz Integration

Over 17 tele-diabetes programs were piloted across Turkish tertiary hospitals in 2024, integrated with the national e-Nabiz platform. Engagement rates reflect strong patient receptivity, particularly in urban centers and among working-age type 2 populations.

4. AI-Driven Clinical Decision Support

AI-based risk stratification tools were deployed in at least 11 tertiary hospitals across Istanbul, Ankara, and Izmir by mid-2025. Early adopters observed enhanced precision in targeting blood sugar levels and a notable decrease in emergency hospitalizations related to diabetes complications during the initial rollout period.

5. Closed-Loop Insulin Delivery Systems

Closed-loop systems, often called artificial pancreas devices, entered limited commercial launch in Turkey in 2025. Market analysts anticipate that these systems will eventually reach a portion of the type-1 patient population, with adoption driven largely by private insurance providers and high-end specialized medical networks.

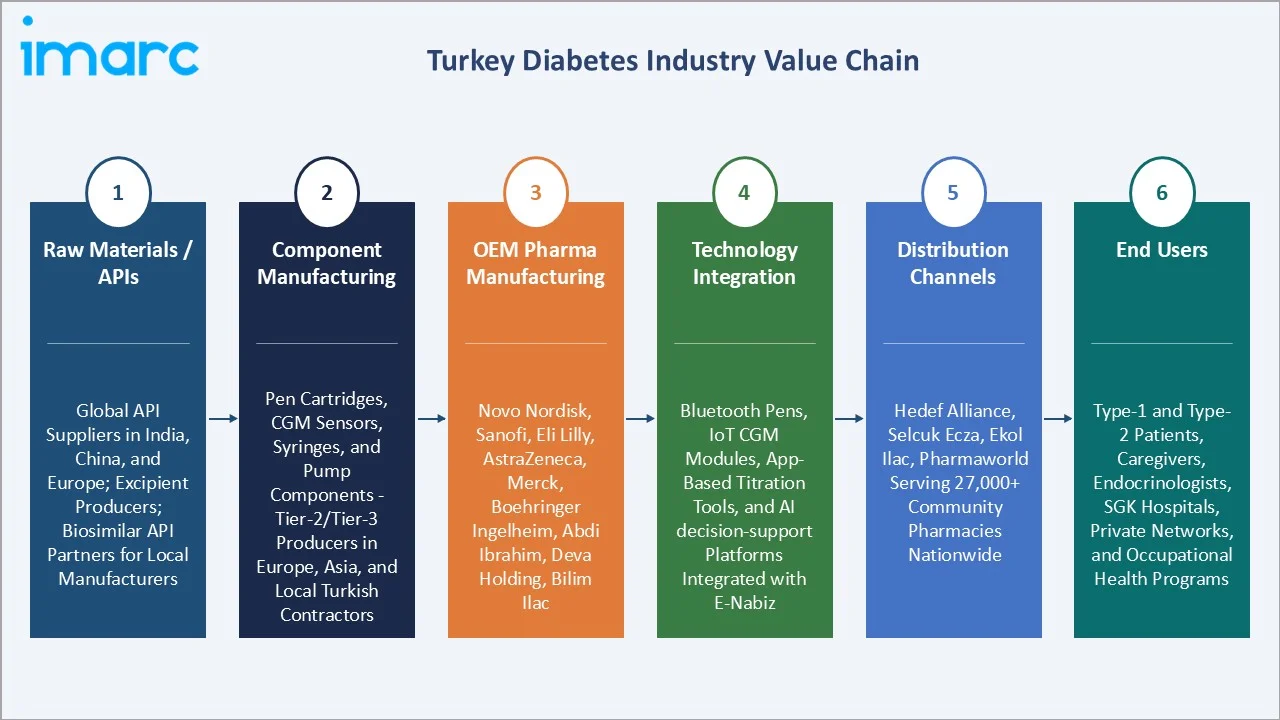

Industry Value Chain Analysis

The Turkey diabetes value chain spans six integrated stages from upstream API supply through patient-facing dispensing. Each stage presents distinct competitive dynamics, margin profiles, and technology investment requirements relevant to the overall Turkey diabetes market analysis.

|

Value Chain Stage |

Key Participants / Role |

|

Raw Materials / APIs |

Global API suppliers in India, China, and Europe; excipient producers; biosimilar API partners for local manufacturers |

|

Component Manufacturing |

Pen cartridges, CGM sensors, syringes, and pump components - Tier-2/Tier-3 producers in Europe, Asia, and local Turkish contractors |

|

OEM Pharma Manufacturing |

Novo Nordisk, Sanofi, Eli Lilly, AstraZeneca, Merck, Boehringer Ingelheim, Abdi Ibrahim, Deva Holding, Bilim Ilac |

|

Technology Integration |

Bluetooth pens, IoT CGM modules, app-based titration tools, and AI decision-support platforms integrated with e-Nabiz |

|

Distribution Channels |

Hedef Alliance, Selcuk Ecza Deposu, Ekol Ilac, Pharmaworld - serving 27,000+ community pharmacies nationwide |

|

End Users |

Type-1 and type-2 patients, caregivers, family physicians, endocrinologists, SGK hospitals, private networks, and occupational health programs |

OEM pharma manufacturers hold the highest strategic value by integrating APIs, device components, and technology into turnkey therapy platforms. Meanwhile, tele-pharmacy and e-commerce channels are reshaping distribution, letting manufacturers deepen patient relationships and streamline chronic-therapy refills with subscription-based models integrated into e-Nabiz.

Technology Landscape in the Turkey Diabetes Industry

Advanced Insulin Analogs and Biologics

Long-acting basal analogs such as insulin degludec and glargine U300 dominate the analog insulin category. GLP-1 receptor agonists were among the fastest-growing classes in 2025, with prescription volumes up 24% year-on-year. Dual GIP/GLP-1 agonists entered the Turkish market in 2024, expanding therapy options for obesity-diabetes crossover patients across private and SGK channels.

Device and Materials Innovation

Ultra-thin pen needles, microneedle patches, and biocompatible polymer sensors gained traction in 2025. Local CGM trials demonstrated accuracy with mean absolute relative difference (MARD) below 9%. Medical-grade polymer and stainless steel innovations underpin the shift toward durable, user-friendly delivery devices across Turkish tertiary centers.

Smart Connectivity and IoT Integration

Bluetooth-enabled insulin pens and connected diabetes devices are an expanding segment of digital diabetes care globally, supporting dose tracking and integration with mobile health applications. In Turkey, the national e-Nabız system provides centralized access to patient health records, while digital diabetes apps such as mySugr operate as standalone self-management tools. However, large-scale interoperability between smart insulin devices, mobile apps, and national electronic health records is not yet documented as a fully integrated system in published sources.

Automation and Clinical AI

Automated insulin titration algorithms and AI-based decision support systems have been evaluated in multiple hospital-based clinical studies, demonstrating non-inferiority to physician-led insulin adjustment and improvements in glycemic outcomes such as HbA1c and time-in-range. In parallel, closed-loop systems combining continuous glucose monitoring with algorithm-driven insulin delivery are increasingly improving glycemic control in type 1 diabetes and are considered a key advancement in modern diabetes management, although large-scale city-specific implementation data and standardized operational efficiency metrics are not consistently reported.

Market Segmentation Analysis

IMARC Group provides an analysis of the key trends in each segment of the Turkey diabetes market, along with forecasts at the national and regional levels from 2026 to 2034. The market has been categorized based on type and distribution channel as per the quantitative data available.

The report covers the following segments:

| Segment Category | Leading Segment | Market Share | Year |

|---|---|---|---|

| Segment | Insulin | 55.8% | 2025 |

| Distribution Channel | Retail Pharmacies | 44.2% | 2025 |

By Segment

Insulin leads the Turkey diabetes market with a 55.8% share in 2025. Demand is driven by roughly 430,000 type-1 patients and advanced type-2 cases requiring basal-bolus regimens. The Turkish insulin sub-segment is projected to grow at a 2.3% CAGR through 2030. Long-acting analog insulins account for ~44% of insulin revenues, reflecting preference for once-daily dosing and lower hypoglycemia risk. Biosimilar insulins captured approximately 9% of insulin revenues by 2025.

To access detailed market analysis, Request Sample

Oral antidiabetics account for 44.2% of market revenues in 2025, worth approximately USD 105.9 Million. Demand is driven by expanding type-2 diagnoses and strong SGLT-2 uptake. GLP-1 receptor agonist prescriptions rose ~24% in 2025 as obesity-linked demand surged. Consumer preference for once-weekly dosing and dual GIP/GLP-1 agonists is expanding average selling prices across this class.

By Distribution Channel

Retail pharmacies dominate the distribution landscape with a 44.2% share in 2025, generating approximately USD 105.9 Million in diabetes-related revenue. Turkey's network of more than 27,000 community pharmacies provides nationwide proximity-based dispensing, supported by SGK-driven reimbursement pathways. Hedef Alliance, Selcuk Ecza, and Ekol Ilac are the primary wholesale distributors serving these outlets.

Hospital pharmacies represent 34.1% of dispensing volumes in 2025. These outlets are central to first-fill insulin initiation, CGM provisioning, and complex therapy management, anchored by Ministry of Health facilities and private networks such as Acibadem, Medical Park, and Memorial. E-commerce and tele-pharmacy reached 21.7% share, translating to roughly USD 52.0 Million, with 5.2% CAGR momentum supported by platforms such as Dermocare, Eczane Online, and Nobel e-Pharmacy.

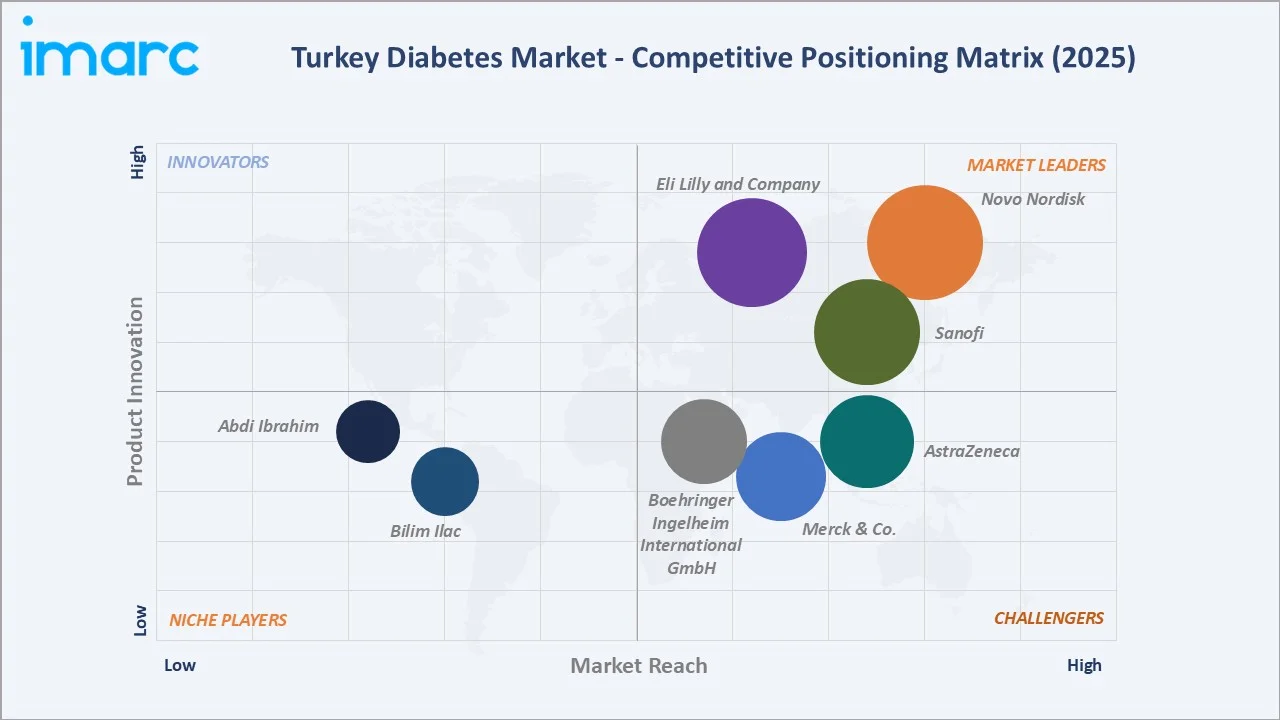

Competitive Landscape

|

Company Name |

Key Brand(s) |

Market Position |

Core Strength |

|

Novo Nordisk |

NovoRapid, Levemir, Ozempic |

Leader |

Insulin analog leadership, GLP-1 franchise, adherence programs |

|

Sanofi |

Lantus, Toujeo, Soliqua |

Leader |

Long-acting analogs, fixed-ratio combinations, tender depth |

|

Eli Lilly and Company |

Humalog, Trulicity, Mounjaro |

Leader |

Dual GIP/GLP-1 platform, rapid uptake, specialist engagement |

|

AstraZeneca |

Forxiga, Bydureon |

Challenger |

SGLT-2 leadership, cardiorenal outcomes positioning |

|

Merck & Co. |

Januvia, Janumet |

Challenger |

DPP-4 class defense, combination products, primary care reach |

|

Boehringer Ingelheim International GmbH |

Jardiance, Tradjenta |

Challenger |

Cardiorenal evidence base, heart failure crossover |

|

Abdi Ibrahim |

Basalog One |

Emerging |

Largest Turkish pharma, biosimilar pipeline, SGK tender strength |

|

Bilim Ilac |

Metformin, SGLT2 Inhibitors |

Emerging |

Cerkezkoy manufacturing, MENA export growth, localization |

The Turkey diabetes market's competitive landscape is moderately consolidated, with global innovators competing alongside strong Turkish manufacturers positioning for biosimilars and localization. Leading players compete on product innovation, IoT integration, SGK tender participation, and sustainability credentials. Strategic partnerships are a key tool - Abdi Ibrahim expanded biosimilar capacity in 2025, while Deva Holding deepened MENA export partnerships through 2025 agreements.

Key Company Profiles

Novo Nordisk

Novo Nordisk is the global leader in insulin and GLP-1 therapies, headquartered in Bagsværd, Denmark. Founded in 1923, it operates through Novo Nordisk Saglik Urunleri Ticaret Ltd. with its Turkey headquarters in Istanbul and a dedicated commercial, medical affairs, and clinical trials team.

- Product & Platform Portfolio: Novo Nordisk's Turkey portfolio spans NovoRapid, Levemir, Tresiba, Ozempic, Victoza, and Xultophy - covering rapid-acting, long-acting, and GLP-1 classes with adherence-supporting smart pen accessories.

- Recent Developments: In 2026, Team Novo Nordisk, the world’s first all-diabetes professional cycling team, competed in the Presidential Cycling Tour of Türkiye, completing eight days of racing across the country. The team used the race not only as a sporting event but also as a platform to raise awareness about type 1 diabetes, including engaging with children living with the condition in Türkiye.

- Strategic Focus: Novo Nordisk's strategy centers on premium innovation, obesity-diabetes crossover therapies, and digital adherence tools aligned with Turkey's national diabetes control priorities and Vision 2053 health agenda.

Sanofi

Sanofi is a French multinational with a strong diabetes and cardiovascular franchise in Turkey. It operates Sanofi Saglik Urunleri Ltd. with its Turkey headquarters in Istanbul and maintains a local manufacturing partnership with Turkish contract manufacturers for SGK tender fulfillment.

- Product & Platform Portfolio: Sanofi's Turkey portfolio includes Lantus, Toujeo, Apidra, Soliqua, and Admelog - covering basal, rapid, and fixed-ratio combination therapies aligned with updated TITCK and SGK clinical guidelines.

- Recent Developments: In 2025, Sanofi partnered with Kuehne+Nagel in Türkiye to strengthen its pharmaceutical supply chain operations. Under this agreement, Kuehne+Nagel manages Sanofi’s fulfilment and warehousing facility in Tuzla, Istanbul, handling storage, packaging, and value-added logistics services for pharmaceutical and consumer health products.

- Strategic Focus: Sanofi's focus is on portfolio consolidation around long-acting analogs and fixed-ratio combinations, deeper SGK tender participation, and leveraging local partnerships to manage currency exposure.

Eli Lilly and company

Eli Lilly is a US-based innovator with leading GLP-1 and dual agonist assets. Turkish operations are supported by Lilly Ilac Ticaret Ltd. with headquarters in Istanbul and a long-established clinical trials network across Turkish university hospitals.

- Product & Platform Portfolio: Eli Lilly's Turkey portfolio includes Humalog, Humulin, Trulicity, Mounjaro, and co-promoted Jardiance. Mounjaro is a flagship growth driver for obesity-diabetes crossover care.

- Recent Developments: In 2025, Eli Lilly appointed Roberta Marinelli to lead its Middle East and Türkiye region as part of a strategy to accelerate growth. Her role focuses on expanding commercial operations, strengthening regulatory and healthcare partnerships, and improving access to innovative medicines across Türkiye and nearby markets.

- Strategic Focus: Eli Lilly's strategy focuses on aggressive expansion of GIP/GLP-1 dual agonists, targeted obesity-diabetes clinical programs, and deeper commercial coverage in Istanbul, Ankara, and Izmir tertiary centers.

Market Concentration Analysis

The Turkey diabetes market exhibits moderate concentration. The top five players - Novo Nordisk, Sanofi, Eli Lilly, AstraZeneca, and Merck - collectively account for approximately 59% of national market revenue in 2025. Novo Nordisk alone holds an estimated 21.3% share, reflecting its deep insulin franchise and growing GLP-1 footprint across SGK and private channels.

The market is experiencing a bifurcated dynamic. At the premium OEM tier, consolidation is occurring around brand equity, IoT platform capabilities, and clinical evidence depth. Simultaneously, Turkish domestic manufacturers such as Abdi Ibrahim, Deva Holding, and Bilim Ilac are generating competitive pressure through biosimilar insulin capabilities and cost-competitive generics aligned with the Global Pharma Turkey localization strategy.

The Herfindahl-Hirschman Index is estimated above 1500 for 2025, sitting just below the high-concentration threshold. The long tail of over 30 local manufacturers ensures competitive dynamics, with at least two anticipated M&A transactions expected in the Turkish diabetes space over the next 36 months as biosimilar consolidation accelerates.

Investment & Growth Opportunities

Fastest-Growing Segments

E-commerce and tele-pharmacy sales are projected to grow steadily through the next decade, outpacing offline channels. Oral antidiabetics remain a leading drug category, driven by strong momentum from SGLT-2 and GLP-1 therapies. Smart insulin and CGM-enabled therapies represent a premium technology growth opportunity, with device adoption among insulin-treated patients continuing to expand.

Emerging Sub-Market Opportunities

Pediatric type-1 diabetes care - affecting approximately 26,000 Turkish children in 2024 - is significantly underpenetrated by advanced pumps and closed-loop systems. Obesity-diabetes combined programs align with Turkey's 2024 national obesity strategy addressing the highest OECD obesity rate. Biosimilar insulin and GLP-1 manufacturing opportunities are emerging as Global Pharma Turkey incentives mature.

Venture and Strategic Investment Trends

Turkish healthtech startups funding crossed USD 1 Billion in 2024, with diabetes and chronic-care startups attracting ~18% of deals. Digital therapeutics platforms integrated with e-Nabiz expanded their investor bases in 2024. Investments in IoT connectivity platforms, biosimilar R&D, and AI-powered titration systems are the primary focus areas for venture and corporate capital through 2034.

Future Market Outlook (2026-2034)

The Turkey diabetes market forecast projects steady value expansion from USD 239.5 Million in 2025 to USD 305.2 Million by 2034 at a CAGR of 2.60%. The Istanbul Region will retain national leadership while the Aegean Region accelerates structurally on aging demographics and hospital expansion. Ankara will sustain steady growth through regulatory proximity and university hospital density.

Three key shifts will reshape the Turkey diabetes market through 2034. First, CGM reimbursement expansion and e-Nabiz integration will embed diabetes management into integrated care pathways, making connected devices standard in new insulin initiations by 2028-2030.

Research Methodology

Primary Research

Primary research encompassed structured interviews conducted in 2024-2025 with 45 Turkish diabetes industry stakeholders, including endocrinologists, SGK tender specialists, hospital pharmacy directors, private hospital category managers, Hedef Alliance and Selcuk Ecza leadership, and multinational commercial heads. Primary insights validated market sizing, segmentation estimates, regional splits, and technology adoption timelines.

Secondary Research

Secondary sources include TITCK filings, Ministry of Health statistics, International Diabetes Federation (IDF) atlas editions, SGK tender disclosures, IQVIA Turkey retail audits, and annual reports of listed Turkish pharma companies such as Abdi Ibrahim, and Bilim Ilac. Regulatory updates from TITCK and public statements from Ministry of Health leadership were also incorporated.

Forecasting Models

Market size estimations and growth projections were derived using a combination of bottom-up forecasting by drug class and distribution channel, cross-validated with top-down macro drivers such as diabetes prevalence, diagnosis rates, currency movements, and per-capita health spending. Scenario analysis (base, optimistic, and conservative cases) was performed with CAGR sensitivity of +/- 90 basis points to account for macroeconomic and regulatory uncertainty.

Turkey Diabetes Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Segments Covered | Oral Antidiabetics, Insulin |

| Distribution Channels Covered | E-commerce and Tele-pharmacy, Hospital Pharmacies, Retail Pharmacies |

| Companies Covered | Novo Nordisk, Sanofi, Eli Lilly and Company, AstraZeneca, Merck & Co., Boehringer Ingelheim International GmbH, Abdi Ibrahim, Bilim Ilac, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the Turkey Diabetes Market Report

The Turkey diabetes market was valued at USD 239.5 Million in 2025, driven by 14.5% adult diabetes prevalence, 32%+ obesity rates, rapid urbanization, and expanding digital health integration through the e-Nabiz platform.

The market is projected to reach USD 305.2 Million by 2034, growing at a CAGR of 2.60% during 2026-2034, supported by therapy innovation, biosimilar scale-up, and digital pharmacy channel expansion.

Insulin leads with a 55.8% share in 2025, driven by roughly 430,000 type-1 patients and a significant insulin-dependent type-2 cohort, supported by biosimilar insulin adoption under SGK tenders.

Retail pharmacies dominate with a 44.2% share in 2025, underpinned by more than 27,000 community pharmacies nationwide and strong SGK-driven reimbursement pathways.

E-commerce and tele-pharmacy are the fastest-growing channel at 21.7% share in 2025, expanding at approximately 5.2% CAGR through 2034 as digital health adoption accelerates via e-Nabiz integration.

Key drivers include diabetes prevalence of 14.5%, adult obesity exceeding 32% (highest in OECD), rapid urbanization at 77%, e-Nabiz digital health integration, and expanding private insurance coverage.

Major players include Novo Nordisk, Sanofi, Eli Lilly, AstraZeneca, Merck & Co., Boehringer Ingelheim, Abdi Ibrahim, and Bilim Ilac - collectively holding ~59% of market share.

Continuous glucose monitoring (CGM) is the fastest-growing technology, projected to rise from ~12% penetration in 2025 to ~28% by 2029, driven by progressive SGK reimbursement expansion.

Key restraints include SGK price controls and reference pricing, Turkish lira currency volatility, endocrinologist shortage at 1.4 per 100,000, and regional access gaps across Eastern Anatolia.

Key opportunities include biosimilar insulin and GLP-1 manufacturing, CGM platform expansion, pediatric type-1 care, obesity-diabetes combined programs, and digital therapeutics integrated with e-Nabiz.

The Turkey diabetes market is moderately consolidated, with the top five players holding ~59% share in 2025 and an HHI near 1,140, while a long tail of 30+ local manufacturers preserves competition.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)