United States Aircraft Health Monitoring System Market Size, Share, Trends and Forecast by Component, Subsystem, End User, Installation, Fit, Operation Time, Operation Type, and Region, 2026-2034

United States Aircraft Health Monitoring System Market Size, Share, Trends & Forecast (2026-2034)

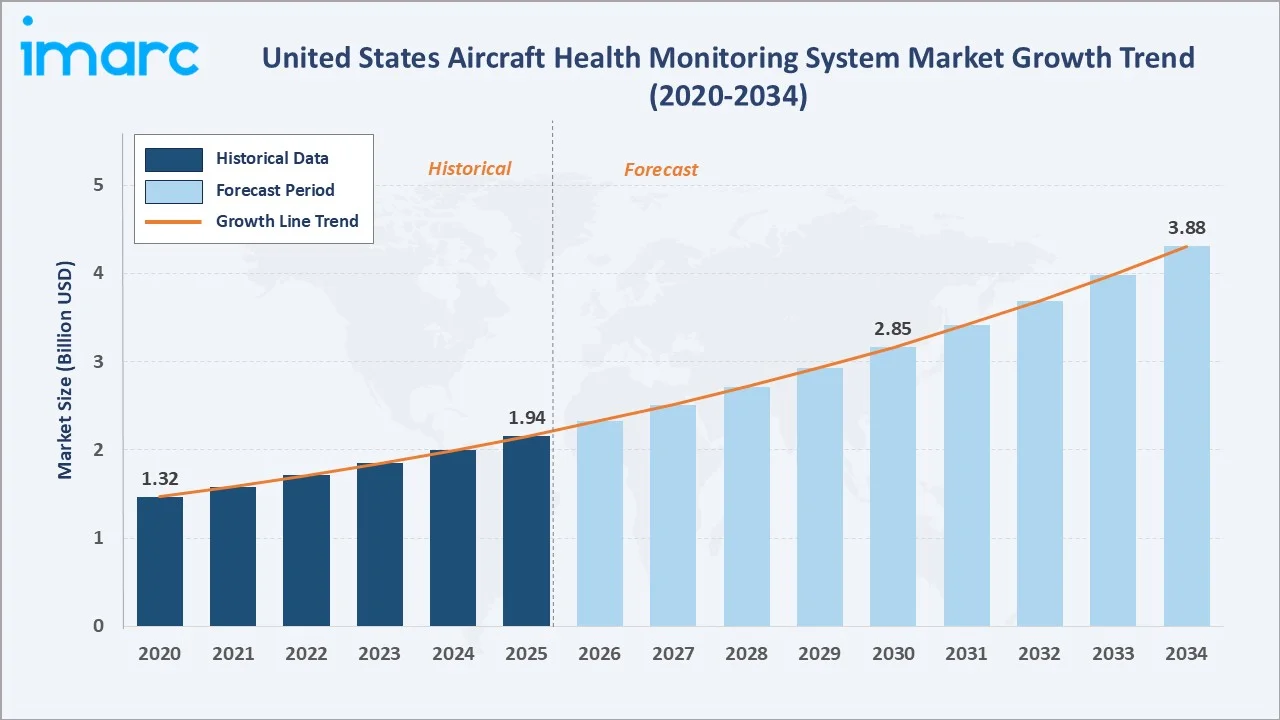

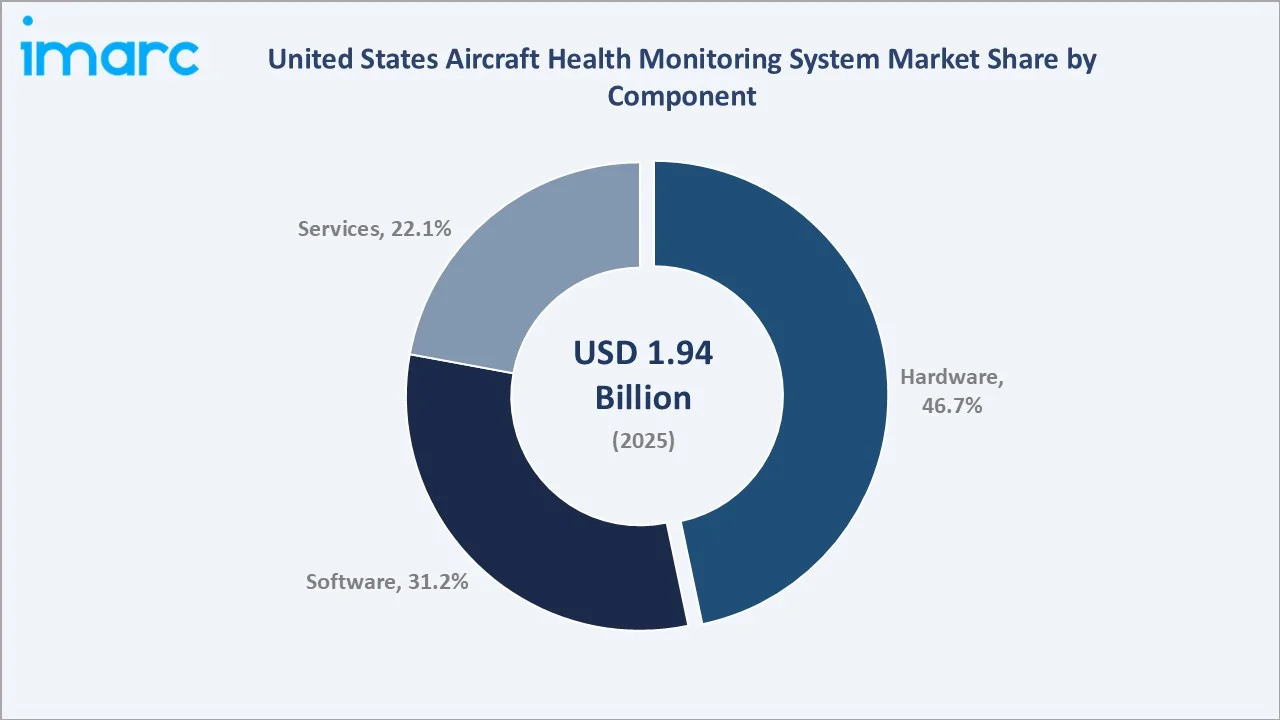

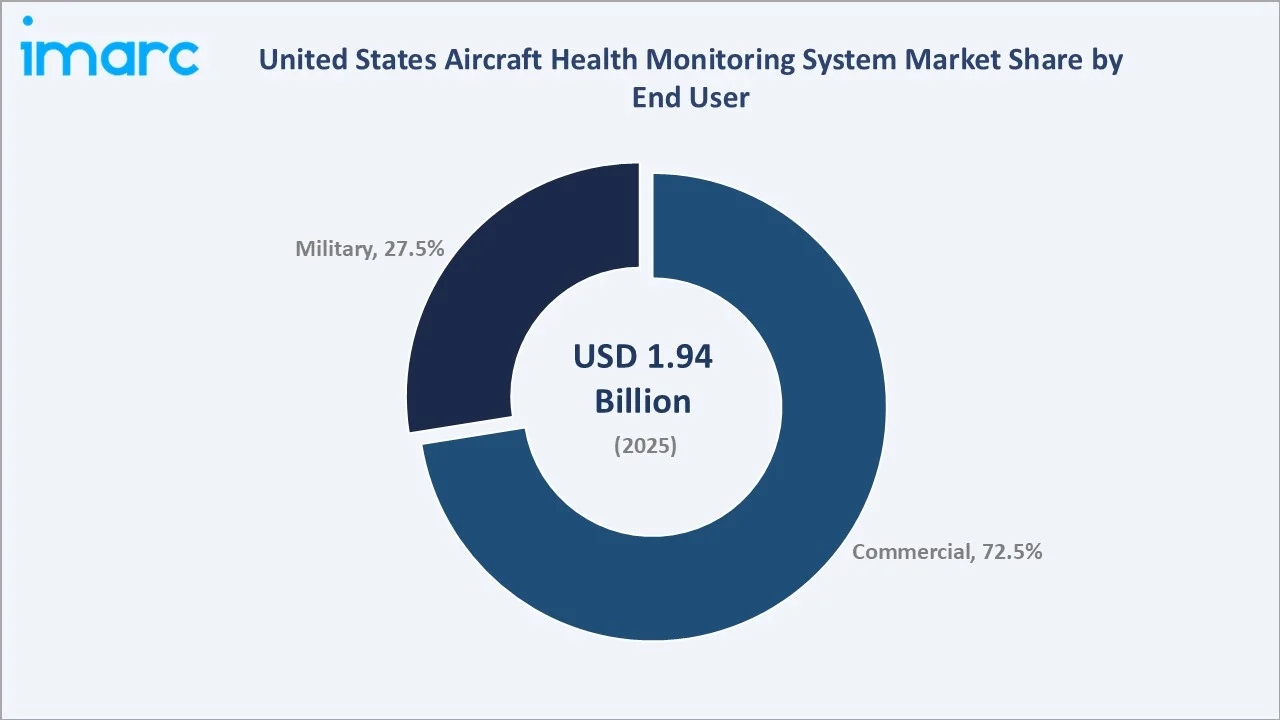

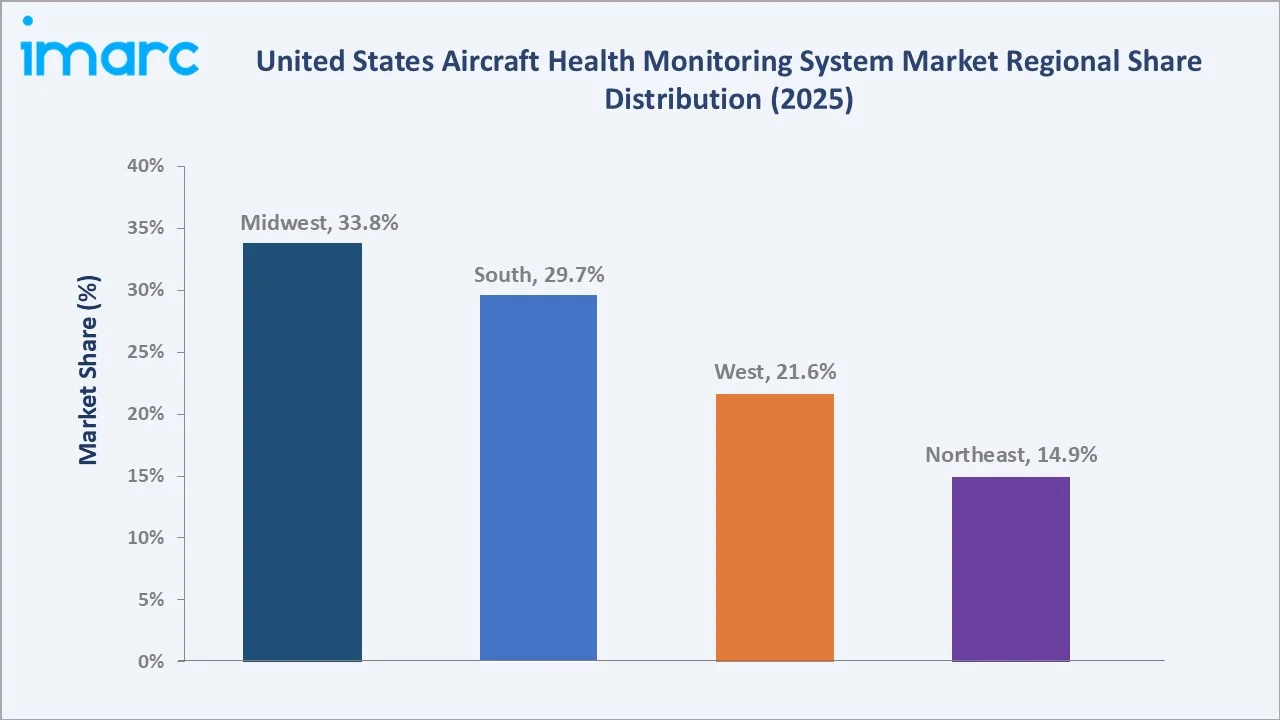

The United States aircraft health monitoring system market reached USD 1.94 Billion in 2025 and is projected to reach USD 3.88 Billion by 2034, growing at a CAGR of 7.96% during 2026-2034. Growing adoption of connected aircraft technologies, real-time diagnostics, and condition-based maintenance solutions by commercial airlines, defense operators, and MRO providers is accelerating market growth. Commercial aviation is a major contributor to the US economy, accounting for around 5% of GDP, or nearly USD 1.54 trillion in 2025. US airlines operate more than 28,000 daily flights, carrying approximately 2.7 million passengers to and from nearly 80 countries, along with about 61,000 tons of cargo across more than 220 countries. As airlines manage large passenger and cargo operations, AHMS helps reduce unplanned downtime, improve safety, optimize maintenance schedules, and lower operating costs. Hardware leads the component at 46.7%. Commercial leads end user at 72.5%. Midwest leads regionally at 33.8%.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 1.94 Billion |

|

Forecast Market Size (2034) |

USD 3.88 Billion |

|

CAGR (2026-2034 |

7.96% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Dominant Component |

Hardware (46.7%, 2025) |

|

Dominant End User |

Commercial (72.5%, 2025) |

|

Leading Region |

Midwest (33.8%, 2025) |

The United States aircraft health monitoring system (AHMS) market grew from USD 1.32 billion in 2020 to USD 1.94 billion in 2025, reflecting strong adoption of predictive maintenance and real-time aircraft diagnostics. The market is projected to reach USD 2.85 billion by 2030 as airlines, defense operators, and MRO providers expand digital fleet monitoring. By 2034, the market is forecast to reach USD 3.88 billion, supported by connected aircraft technologies, rising fleet utilization, and increasing focus on safety, reliability, and maintenance cost optimization.

To get more information on this market, Request Sample

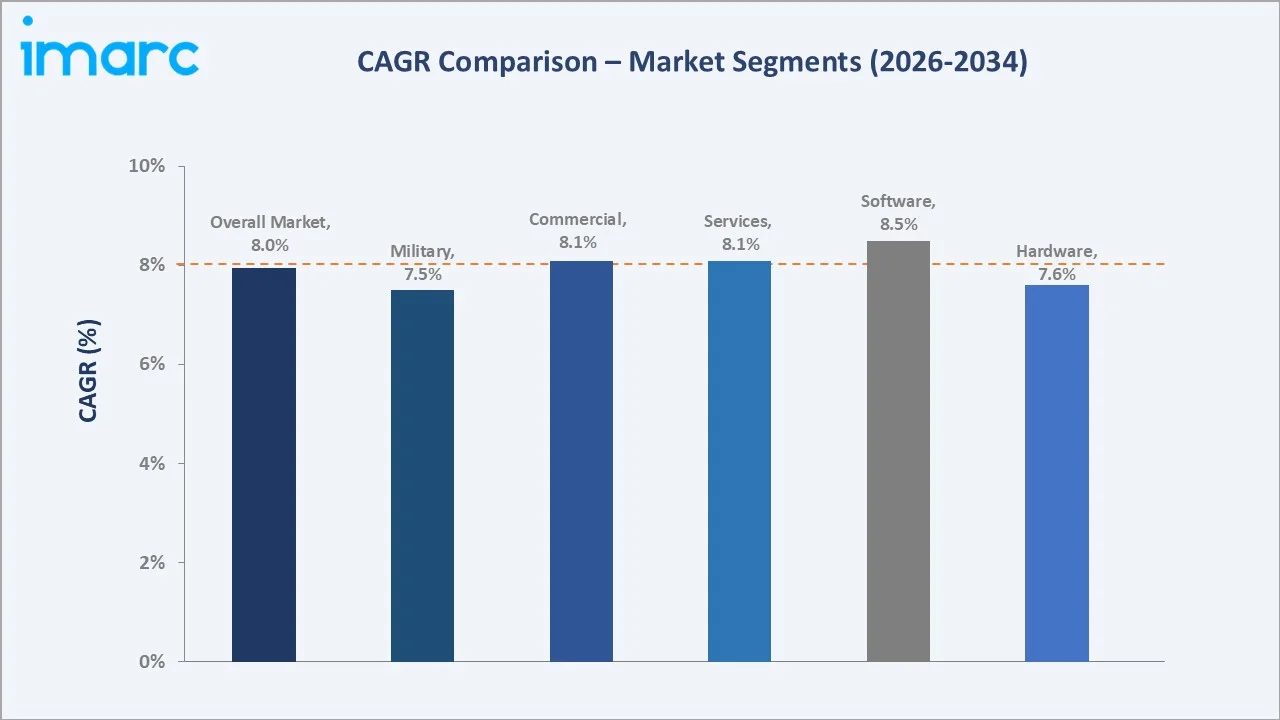

Software grows fastest at ~8.5% CAGR through AI/ML predictive maintenance platform, digital twin, cloud AHMS analytics, and edge AI sensor fusion. Services grow at ~8.1% CAGR through MRO data-driven maintenance, AHMS-as-a-Service subscription, and fleet management consulting. Hardware's ~7.6% CAGR through next-generation sensors and DAU hardware refresh.

Executive Summary

The United States aircraft health monitoring system market is growing steadily, supported by rising aircraft fleet utilization and increasing focus on operational reliability. The market expanded from USD 1.32 billion in 2020 to USD 1.94 billion in 2025 and is projected to reach USD 3.88 billion by 2034. Airlines, defense operators, and MRO providers are increasingly adopting real-time diagnostics and predictive maintenance tools to reduce downtime and maintenance costs. Connected aircraft technologies, sensor-based monitoring, and data analytics are further strengthening AHMS adoption. Stringent aviation safety standards and growing demand for efficient fleet management continue to support long-term market growth. Hardware at 46.7% leads through sensors and DAUs. Commercial at 72.5% leads through US airlines. Midwest leads regionally at 33.8%.

Key Market Insights

|

Insight |

Data |

|

Dominant Component |

Hardware - 46.7% share (2025) |

|

Dominant End User |

Commercial - 72.5% market share (2025) |

|

Leading Region |

Midwest - 33.8% share (2025) |

|

Market Opportunity |

AI/ML predictive maintenance digital twin; connected aircraft IIoT cloud AHMS; military HUMS for rotorcraft |

Key Analytical Observations Supporting the Above Data:

- Hardware at 46.7%: Hardware segment dominates as sensors, onboard diagnostic units, data acquisition systems, and connectivity modules form the core infrastructure of aircraft health monitoring. These components enable real-time fault detection, condition monitoring, and predictive maintenance across aircraft systems.

- Commercial at 72.5%: The commercial segment dominates due to high aircraft utilization, large fleet sizes, and strong demand for predictive maintenance among airlines. Real-time health monitoring helps commercial operators reduce downtime, improve safety, and optimize maintenance costs.

- Midwest at 33.8%: The Midwest region dominates due to its strong aerospace manufacturing base, MRO activity, and proximity to major aviation supply chain hubs. The region’s defense, commercial aviation, and component production ecosystem supports steady adoption of aircraft health monitoring systems.

United States Aircraft Health Monitoring System Market Overview

The United States aircraft health monitoring system market encompasses ground-based and onboard technologies that continuously acquire, transmit, and analyze aircraft structural, engine, and systems health data throughout flight and ground operations. The AHMS ecosystem integrates onboard sensors, data acquisition units, flight data recorders, aircraft communications addressing and reporting system, and ground station software. Macroeconomic factors include air passenger traffic growth, airline profitability, defense spending, and commercial aircraft fleet expansion.

Market Dynamics

To evaluate market opportunities, Request Sample

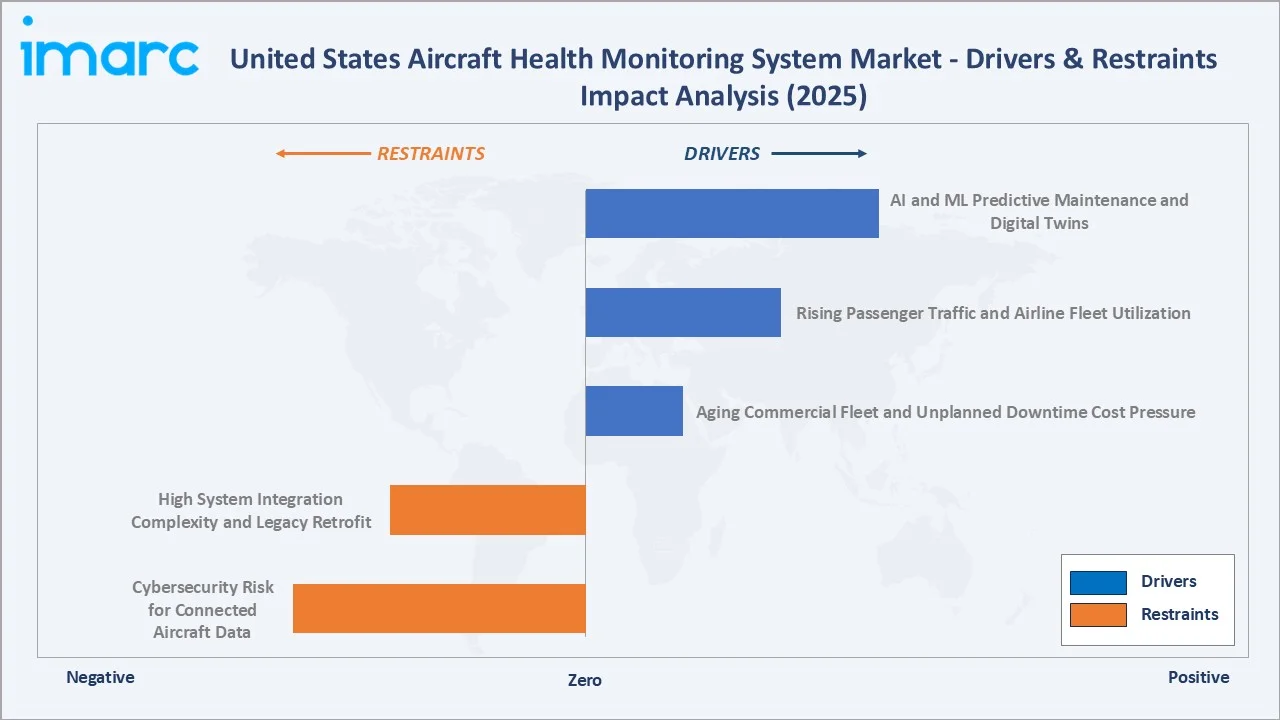

Market Drivers

- AI and ML Predictive Maintenance and Digital Twins: AI and ML-based predictive maintenance and digital twins analyze real-time aircraft data to identify potential component failures before they occur, reducing unscheduled maintenance and operational disruptions. Digital twins create virtual replicas of aircraft systems, enabling continuous performance monitoring, simulation, and maintenance optimization. As airlines and MRO providers seek to improve fleet reliability, safety, and cost efficiency, adoption of AI-powered health monitoring solutions continues to accelerate.

- Rising Passenger Traffic and Airline Fleet Utilization: The FAA’s Air Traffic Organization manages more than 44,000 flights and over 3 million airline passengers daily across more than 29 million square miles of airspace. This rising passenger traffic and airline fleet utilization are driving the market as airlines operate more flights and keep aircraft in service for longer hours. Higher utilization increases wear on engines, avionics, landing gear, and structural components, creating a greater need for real-time health monitoring. AHMS helps airlines detect faults early, plan maintenance efficiently, and reduce flight delays.

- Aging Commercial Fleet and Unplanned Downtime Cost Pressure: Aging commercial fleets and unplanned downtime cost pressure are strongly driving the market as airlines seek to extend aircraft service life while maintaining safety and reliability. Older aircraft require more frequent inspections, component monitoring, and maintenance planning, increasing the need for real-time health tracking systems. AHMS helps detect faults early, reduce unexpected failures, and avoid costly flight delays or cancellations. As operators face pressure to improve fleet availability and control maintenance expenses, predictive monitoring solutions are becoming essential.

Market Restraints

- High System Integration Complexity and Legacy Retrofit: Older aircraft often have diverse avionics, sensor architectures, and data systems that are difficult to connect with modern health monitoring platforms. Retrofitting these systems can require aircraft downtime, certification approvals, wiring upgrades, and software validation. This increases implementation cost and extends deployment timelines for airlines and MRO providers. As a result, some operators delay AHMS adoption, especially for aging fleets with limited remaining service life.

- Cybersecurity Risk for Connected Aircraft Data: Health monitoring systems increasingly rely on real-time data transmission, cloud platforms, and connected avionics. Sensitive aircraft performance, maintenance, and operational data must be protected from unauthorized access or cyberattacks. Airlines and OEMs, therefore, need strong encryption, secure data architecture, and regulatory compliance, which raises implementation cost and complexity. These concerns can slow AHMS adoption, especially among operators with legacy IT and aircraft systems.

Market Opportunities

- AI-Powered Structural Health Trending and Monitoring: AI-powered structural health trending and monitoring enabling continuous assessment of aircraft structures, including fuselage sections, wings, and critical load-bearing components. In June 2026, Platinum Eagle Aerospace launched FLEX AI, an AI-based structural health trending and monitoring platform. The system continuously tracks aircraft structural loads, stress, strain, and fatigue buildup, helping identify emerging anomalies before they become visible or safety-critical issues. This supports predictive maintenance, extends aircraft service life, and reduces costly unscheduled inspections. As airlines and defense operators seek higher fleet availability and lower lifecycle costs, demand for AI-driven structural monitoring solutions is expected to increase.

- Expansion of MRO Digitalization and Condition-Based Maintenance: Expansion of MRO digitalization and condition-based maintenance presents a major opportunity as maintenance providers increasingly adopt data-driven maintenance strategies. AHMS enables continuous monitoring of aircraft systems, allowing maintenance actions to be scheduled based on actual equipment condition rather than fixed intervals. This improves aircraft availability, reduces maintenance costs, and minimizes unscheduled downtime. As airlines and MRO organizations accelerate digital transformation initiatives, demand for advanced health monitoring and predictive analytics solutions is expected to grow significantly.

Market Challenges

- Limited Standardization Across Aircraft Platforms: Different aircraft models often use proprietary avionics, sensors, communication protocols, and data formats. This makes it difficult to integrate a single health monitoring solution across mixed fleets operated by airlines and defense organizations. The lack of common standards increases implementation complexity, customization requirements, and maintenance costs. As a result, operators may face delays in deployment and reduced interoperability between aircraft, OEMs, and MRO systems.

- Data Management and Interoperability Challenges: Aircraft generate large volumes of sensor, maintenance, and operational data from multiple systems. Different OEM platforms, avionics architectures, and MRO software often use incompatible formats, making data integration difficult. This increases the need for customized interfaces, secure data pipelines, and advanced analytics infrastructure. As a result, airlines may face higher costs, slower deployment, and reduced efficiency in fleet-wide health monitoring.

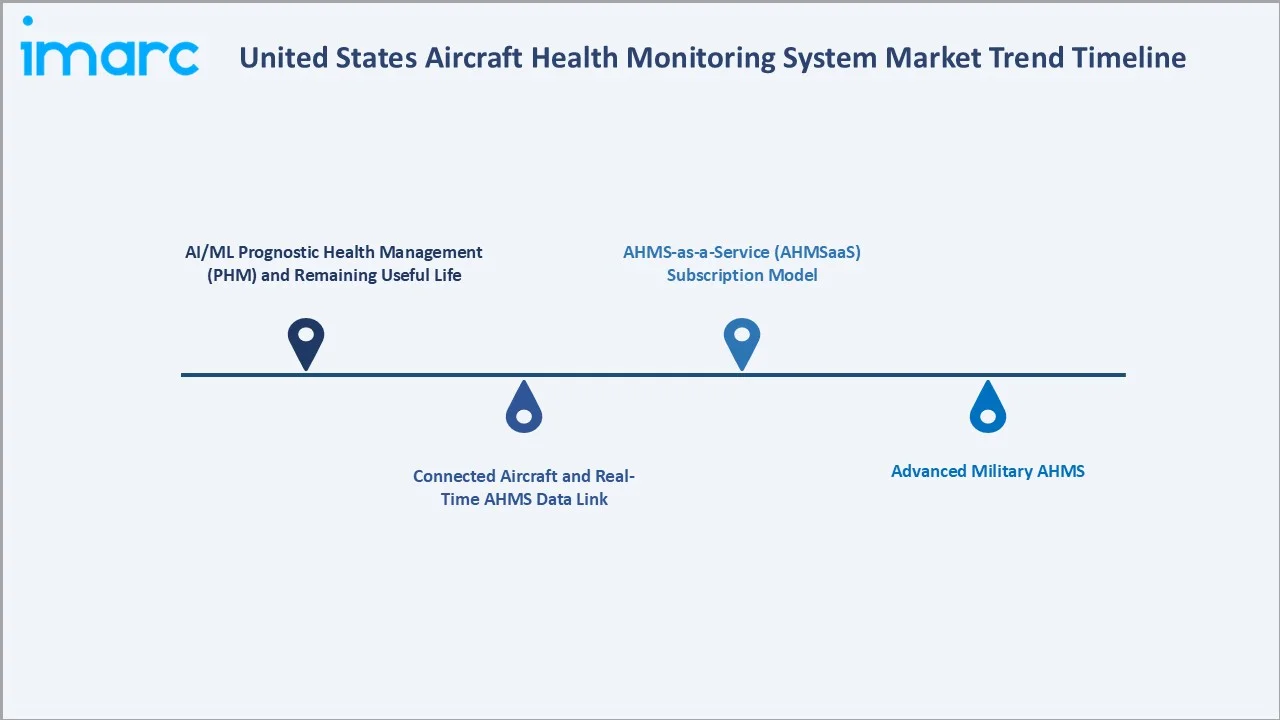

Emerging Market Trends

1. AI/ML Prognostic Health Management (PHM) and Remaining Useful Life

AI/ML prognostic health management (PHM) and remaining useful life are emerging as operators move from reactive maintenance to predictive decision-making. AI models analyze sensor data, fault history, and operating conditions to estimate how long components can safely function. This helps airlines plan maintenance before failures occur, reduce aircraft-on-ground events, and optimize spare parts inventory. As fleet utilization rises, PHM and RUL analytics are becoming essential for improving safety, reliability, and lifecycle cost efficiency.

2. Connected Aircraft and Real-Time AHMS Data Link

Connected aircraft and real-time AHMS data links are emerging as airlines increasingly transmit aircraft health data during flight and immediately after landing. Real-time connectivity enables faster fault detection, remote diagnostics, and proactive maintenance planning before the aircraft reaches the gate. This helps reduce turnaround delays, improve fleet availability, and support condition-based maintenance. As aircraft become more digitally connected, demand for secure, high-speed data links and integrated health monitoring platforms is expected to grow.

3. Advanced Military AHMS

Advanced military AHMS is emerging as defense operators prioritize aircraft readiness, mission availability, and lifecycle cost reduction. These systems monitor engines, avionics, structures, and mission-critical components in real time to detect faults before they affect operations. Integration with predictive analytics supports condition-based maintenance for fighter jets, transport aircraft, helicopters, and UAVs. This trend is strengthening demand for rugged, secure, and mission-ready health monitoring platforms across the US defense aviation sector.

4. AHMS-as-a-Service (AHMSaaS) Subscription Model

AHMS-as-a-Service (AHMSaaS) subscription models are emerging as airlines seek flexible, lower-upfront-cost access to aircraft health monitoring capabilities. Instead of large one-time software investments, operators can use cloud-based diagnostics, predictive analytics, and fleet monitoring through recurring service contracts. This model supports faster deployment, continuous software upgrades, and scalable monitoring across mixed fleets. It also creates recurring revenue opportunities for OEMs, MRO providers, and aviation software companies.

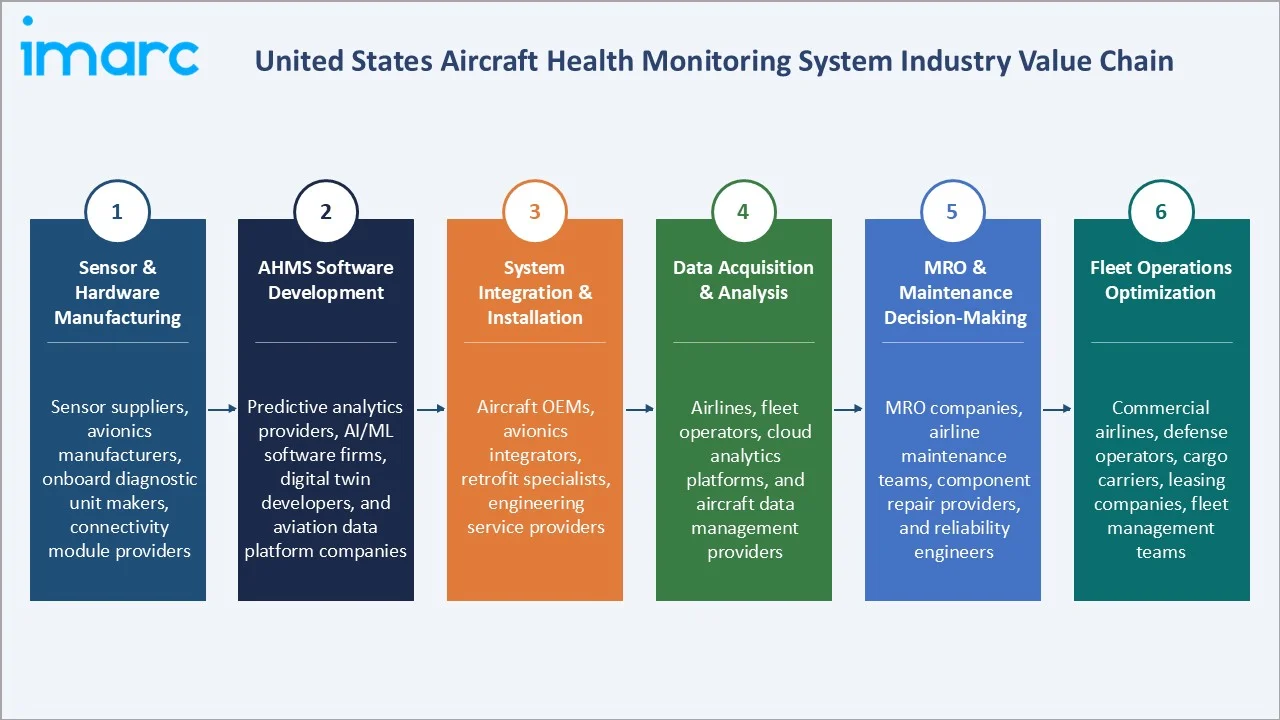

Industry Value Chain Analysis

The United States aircraft health monitoring system value chain integrates sensor & hardware manufacturing, AHMS software development, system integration & installation, data acquisition & analysis, MRO & maintenance decision-making, and fleet operations optimization.

|

Stage |

Key Participants |

|

Sensor & Hardware Manufacturing |

Sensor suppliers, avionics manufacturers, onboard diagnostic unit makers, connectivity module providers |

|

AHMS Software Development |

Predictive analytics providers, AI/ML software firms, digital twin developers, and aviation data platform companies |

|

System Integration & Installation |

Aircraft OEMs, avionics integrators, retrofit specialists, engineering service providers |

|

Data Acquisition & Analysis |

Airlines, fleet operators, cloud analytics platforms, and aircraft data management providers |

|

MRO & Maintenance Decision-Making |

MRO companies, airline maintenance teams, component repair providers, and reliability engineers |

|

Fleet Operations Optimization |

Commercial airlines, defense operators, cargo carriers, leasing companies, fleet management teams |

The AHMS software development stage is the most value-added segment of the aircraft health monitoring system value chain. This stage generates the highest differentiation through AI/ML algorithms, predictive maintenance models, digital twins, and real-time diagnostic capabilities that convert raw aircraft data into actionable insights. The ability to reduce downtime, optimize maintenance schedules, and improve fleet reliability enables software and analytics providers to capture higher margins than hardware manufacturing or system installation activities.

Technology Landscape in the United States Aircraft Health Monitoring System Industry

Sensor and Data Acquisition Technology

Sensor and data acquisition technology enables continuous collection of performance and condition data from engines, avionics, structures, and other critical aircraft systems. Advances in smart sensors, wireless monitoring devices, and onboard data acquisition units are improving the accuracy and volume of operational data captured during flight. These technologies support real-time fault detection, predictive maintenance, and condition-based monitoring strategies. As aircraft become increasingly connected, demand for high-reliability sensing and data collection solutions continues to grow across commercial and defense aviation fleets.

Engine Health Monitoring (EHM) Technology

Engine health monitoring (EHM) technology enables continuous tracking of engine performance, temperature, vibration, pressure, and fuel efficiency parameters. Advanced EHM systems use real-time sensor data and analytics to detect anomalies and predict potential engine failures before they occur. In October 2025, MTU Maintenance and Teledyne Controls partnered to offer improved engine health monitoring and predictive maintenance solutions. Through Teledyne’s Data Delivery Solutions, MTU Maintenance will gain access to detailed full-series flight data for faster and deeper engine performance analysis. As engines represent one of the most critical and costly aircraft systems, EHM adoption is increasing across both commercial and military aviation fleets.

Cybersecurity Solutions for Connected Aircraft

Cybersecurity solutions for connected aircraft are becoming a critical component of the U.S. aircraft health monitoring system technology landscape as aircraft generate and transmit increasing volumes of operational and maintenance data. Advanced cybersecurity technologies such as encryption, secure communication protocols, intrusion detection systems, and zero-trust architectures help protect aircraft networks from cyber threats. These solutions ensure the integrity, confidentiality, and availability of real-time health monitoring data across aircraft, ground stations, and cloud platforms. As connected aircraft adoption grows, cybersecurity is evolving from a compliance requirement into a core enabler of digital aviation and AHMS deployment.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Component |

Hardware |

46.7% |

2025 |

|

Subsystem |

Aero-Propulsion |

🔒 |

2025 |

|

End User |

Commercial |

72.5% |

2025 |

|

Installation |

On Ground |

🔒 |

2025 |

|

Fit |

Linefit |

🔒 |

2025 |

|

Operation Time |

Real-Time |

🔒 |

2025 |

|

Operation Type |

Detection |

🔒 |

2025 |

|

Region |

Midwest |

33.8% |

2025 |

By Component

Hardware leads at 46.7% (2025), as sensors, onboard diagnostic units, data acquisition systems, and connectivity modules form the core foundation of AHMS deployment. These components are essential for collecting real-time aircraft performance, engine, structural, and system health data. Rising aircraft connectivity and predictive maintenance adoption continue to support strong hardware demand.

To access detailed market analysis, Request Sample

Software at 31.2% grows fastest at ~8.5% CAGR through AI/ML predictive maintenance, digital twin, cloud AHMS analytics platform, and edge AI onboard inference. Services at 22.1% grow at ~8.1% CAGR through MRO data analytics service, AHMS-as-a-Service per-aircraft subscription, and fleet management consulting.

By End User

Commercial leads at 72.5% due to high fleet utilization, large aircraft volumes, and strong demand for predictive maintenance among airlines. AHMS helps commercial operators reduce delays, avoid unplanned downtime, improve safety, and optimize maintenance costs across large fleets.

Military at 27.5% driven by the need for higher mission readiness, aircraft availability, and lifecycle cost reduction. AHMS supports predictive maintenance across fighter jets, transport aircraft, helicopters, and UAVs.

Regional Market Insights

|

Region |

Share (2025) |

Key US AHMS Market Drivers & Characteristics |

|

Midwest |

33.8% |

Reflecting its strong aerospace manufacturing base, aircraft component production facilities, MRO hubs, and defense aviation activities. |

|

South |

29.7% |

Reflects significant defense aviation operations, military aircraft fleets, aerospace technology investments, and growing airline maintenance infrastructure. |

|

West |

21.6% |

Reflects the concentration of aerospace innovation, commercial aviation activity, aircraft technology development, and digital aviation solution providers. |

|

Northeast |

14.9% |

Reflects high commercial air traffic density, major airline operations, and increasing investment in predictive maintenance technologies. |

Midwest's 33.8% dominance is supported by its strong aerospace manufacturing base, component suppliers, MRO facilities, and defense aviation ecosystem. South's 29.7% due to significant military aviation activity, defense spending, and expanding aircraft maintenance infrastructure.

West's 21.6% benefits from aerospace innovation, connected aircraft technologies, and digital aviation solution providers. Northeast's 14.9% supported by dense commercial air traffic, major airline operations, and growing adoption of predictive maintenance.

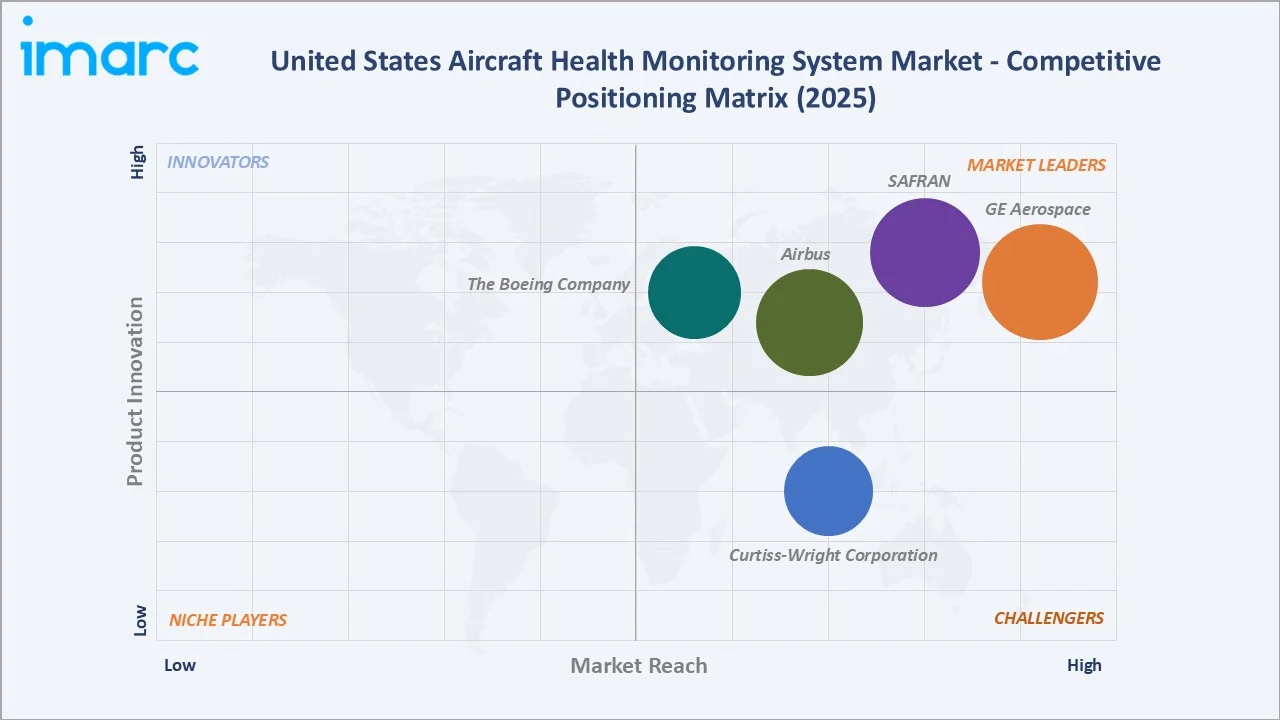

Competitive Landscape

The United States aircraft health monitoring system market is moderately concentrated, with competition driven by aircraft OEMs, avionics providers, aerospace software companies, and predictive maintenance specialists. Market participants focus on expanding AI-driven diagnostics, predictive maintenance capabilities, digital twin technologies, and real-time aircraft connectivity solutions. Strategic partnerships between airlines, MRO providers, and technology firms are becoming increasingly common to enhance fleet performance and operational efficiency.

|

Company |

Key Offerings |

Market Position |

Core Strength |

|

GE Aerospace |

Engine Health Monitoring |

Market Leader |

GE Aerospace plays a pioneering, foundational role in the United States aircraft health monitoring system market, holding a massive footprint as the largest jet engine provider and a leading diagnostic tech developer. |

|

SAFRAN |

Engine Health Monitoring |

Market Leader |

SAFRAN plays a major role in the United States aircraft health monitoring system (AHMS) market by providing predictive maintenance, real-time diagnostic services, and advanced sensor technologies for commercial and military aviation. |

|

Airbus |

Skywise Core [X3] |

Market Leader |

Airbus plays a foundational role in the US aircraft health and usage monitoring system market by deploying its Skywise aviation data platform. |

|

The Boeing Company |

Airplane Health Management (AHM) |

Market Leader |

The Boeing Company acts as a primary market leader and innovator in the US aircraft health monitoring system landscape. Through its proprietary Airplane Health Management (AHM) platform and predictive software like Insight Accelerator, the company provides real-time maintenance analytics, fault isolation, and prognostics to minimize airline disruptions and aircraft-on-ground (AOG) time. |

|

Curtiss-Wright Corporation |

Fortress |

Challenger |

Curtiss-Wright Corporation is a premier technology provider in the United States aircraft health monitoring system (AHMS) market, specializing in rugged Commercial-off-the-Shelf (COTS) hardware and software for data acquisition, flight testing, and avionics recording Defense Solutions. |

Companies are also investing in cloud-based analytics platforms, cybersecurity solutions, and condition-based maintenance systems to strengthen their market positions. As connected aircraft adoption accelerates, innovation in data analytics, automation, and integrated health monitoring platforms remains a key competitive differentiator.

Key Company Profiles

GE Aerospace

GE Aerospace is one of the leading aerospace technology companies in the United States and a prominent participant in the aircraft health monitoring system (AHMS) market. The company provides advanced engine health monitoring, predictive maintenance, digital analytics, and fleet performance management solutions for commercial and military aircraft.

- Key Products: Engine Health Monitoring.

- Strategic Focus: Expanding predictive maintenance, engine health monitoring, and AI-driven analytics capabilities across commercial and military aviation fleets. The company leverages its extensive installed base of aircraft engines to enhance real-time performance monitoring, digital twin applications, and condition-based maintenance solutions.

SAFRAN

Safran is a leading aerospace and defense company with a strong presence in the US aircraft health monitoring system market through its aircraft propulsion, avionics, landing systems, and digital aviation solutions businesses. The company provides advanced engine health monitoring, predictive maintenance, data analytics, and fleet support services for commercial, military, and business aviation customers.

- Key Products: Engine Health Monitoring

- Strategic Focus: Strengthening its predictive maintenance, engine health monitoring, and connected aircraft services capabilities across commercial and military aviation. The company leverages advanced analytics, real-time equipment monitoring, and data-driven maintenance solutions to improve aircraft reliability and operational efficiency.

Market Concentration Analysis

The United States aircraft health monitoring system market exhibits a moderately concentrated structure, with a mix of large aerospace OEMs, avionics suppliers, engine manufacturers, and specialized predictive maintenance software providers. Major companies hold strong positions due to their extensive installed aircraft base, proprietary data ecosystems, and long-term airline relationships. Market competition is increasingly centered on AI-driven analytics, digital twin technology, engine health monitoring, and connected aircraft solutions. Strategic partnerships between OEMs, MRO providers, airlines, and data analytics firms are becoming a key competitive strategy. While established aerospace companies dominate large commercial and defense programs, emerging software-focused firms are gaining traction through cloud-based monitoring and predictive maintenance platforms.

Investment & Growth Opportunities

Highest Growth Segments

Software AI/ML predictive AHMS (~8.5% CAGR), Services AHMS-as-a-Service (~8.1% CAGR), commercial AHMS (~8.1% CAGR), West region (~8.5% CAGR), eVTOL and UAM health monitoring (~15-20% CAGR), and military F-35 ODIN upgrade represent the US AHMS highest-growth investment vectors through 2034.

Investment Themes

- AI/ML predictive maintenance AHMS digital twin: AI/ML-powered digital twin platforms create a virtual replica of aircraft systems and continuously analyze real-time operational data to predict failures before they occur. This investment theme is attractive because it helps airlines reduce maintenance costs, minimize aircraft downtime, and improve fleet availability through predictive and condition-based maintenance strategies.

- eVTOL and UAM health monitoring system: The emergence of electric vertical take-off and landing (eVTOL) aircraft and urban air mobility (UAM) networks is creating demand for next-generation health monitoring systems tailored to electric propulsion, batteries, and autonomous flight systems. Early investment in this segment offers exposure to a rapidly developing aviation market expected to require advanced real-time diagnostics, predictive maintenance, and safety monitoring solutions.

Future Market Outlook (2026-2034)

The US aircraft health monitoring system market is projected to grow from USD 1.94 Billion in 2025 to USD 3.88 Billion by 2034, delivering a 7.96% CAGR over the forecast period through AI/ML predictive maintenance transformation, commercial fleet expansion, military AHMS modernization, and emerging eVTOL health monitoring. The market's anchor value of USD 2.85 Billion in 2030 represents US AHMS at AI and cloud inflection.

Three structural forces define the United States aircraft health monitoring system market growth through 2034: the expansion of commercial and defense aircraft fleets, the shift toward predictive and condition-based maintenance, and the increasing adoption of connected aircraft technologies. Airlines and military operators are investing in AHMS solutions to reduce unplanned downtime, improve safety, and optimize maintenance costs. Advances in AI, machine learning, digital twins, and real-time data analytics are enhancing fault prediction and fleet management capabilities. At the same time, growing aircraft connectivity and digitalization are enabling continuous health monitoring across increasingly complex aviation ecosystems.

Research Methodology

Primary Research

Primary research comprised interviews with aircraft OEMs, AHMS solution providers, airlines, MRO companies, defense operators, and aviation technology experts. The research captured insights on predictive maintenance adoption, fleet monitoring needs, integration challenges, pricing, and technology preferences. These inputs helped validate market sizing, competitive positioning, and growth opportunities in the market.

Secondary Research

Secondary research encompassed company websites, annual reports, investor presentations, FAA and defense aviation publications, industry journals, and MRO technology sources. It also included analysis of fleet expansion, aircraft utilization, predictive maintenance adoption, connected aircraft trends, and competitive developments.

Forecasting Models

Forecasting models combined historical market trends, aircraft fleet expansion forecasts, airline maintenance spending, and AHMS adoption rates across commercial and military aviation. A bottom-up approach was used to assess demand by component, end user, and region, while a top-down analysis validated overall market potential. The forecasts also incorporated technology adoption trends such as AI-driven predictive maintenance, connected aircraft, and digital twin solutions to project market growth through 2034.

Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Components Covered | Hardware, Software, Services |

| Subsystems Covered | Aero-Propulsion, Avionics, Ancillary Systems, Aircraft Structures, Others |

| End Users Covered | Commercial, Military |

| Installations Covered | Onboard, On Ground |

| Fits Covered | Linefit, Retrofit |

| Operation Times Covered | Real-Time, Non-Real-Time |

| Operation Types Covered | Detection, Diagnostics, Condition-Based Maintenance and Adaptive Control, Others |

| Regions Covered | Northeast, Midwest, South, West |

| Companies Covered | GE Aerospace, SAFRAN, Airbus, The Boeing Company, Curtiss-Wright Corporation, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the United States Aircraft Health Monitoring System Market Report

The US aircraft health monitoring system market reached USD 1.94 Billion in 2025, driven by rising fleet utilization, growing passenger and cargo traffic, and the need to reduce unplanned aircraft downtime. Airlines, defense operators, and MRO providers are increasingly adopting predictive maintenance, real-time diagnostics, and condition-based monitoring solutions. Growth in connected aircraft, AI/ML analytics, digital twins, and engine health monitoring is further strengthening market expansion.

The United States aircraft health monitoring system market grows at 7.96% CAGR during 2026-2034, reaching USD 3.88 Billion by 2034. The CAGR reflects AI predictive maintenance transformation, fleet expansion, military AHMS modernization, and eVTOL emerging.

Hardware leads at 46.7% as sensors, onboard diagnostic units, data acquisition systems, and connectivity modules form the core foundation of AHMS deployment. These components enable continuous aircraft data capture, real-time fault detection, and system health monitoring across commercial and military fleets.

Commercial leads at 72.5% due to high aircraft utilization, large airline fleet sizes, and a strong need to reduce maintenance-related delays. AHMS helps airlines improve safety, monitor aircraft performance in real time, and lower unplanned downtime across daily operations.

Midwest leads at 33.8% due to its strong aerospace manufacturing base, aircraft component suppliers, MRO hubs, and defense aviation activities. The region also benefits from established aviation engineering capabilities and growing adoption of predictive maintenance solutions.

Leading companies include GE Aerospace, SAFRAN, Airbus, The Boeing Company, and Curtiss-Wright Corporation, among others.

The market is projected to reach approximately USD 2.85 Billion by 2030, supported by the rising adoption of predictive maintenance, connected aircraft, and real-time diagnostics. Growth will be driven by commercial fleet expansion, higher aircraft utilization, and increasing focus on reducing downtime and maintenance costs.

Three priority investment opportunities in the market include AI/ML-based predictive maintenance and digital twin platforms, which enable proactive fault detection and maintenance optimization. Another attractive area is engine health monitoring and condition-based maintenance solutions, driven by airlines' focus on reducing downtime and operating costs. Additionally, health monitoring systems for next-generation aircraft, including eVTOLs and advanced military platforms, present significant long-term growth potential as aviation becomes increasingly connected, autonomous, and data-driven.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)