United States Secondhand Luxury Goods Market Size, Share, Trends and Forecast by Product Type, Demography, Distribution Channel, and Region, 2026-2034

United States Secondhand Luxury Goods Market Size, Share, Trends & Forecast (2026-2034)

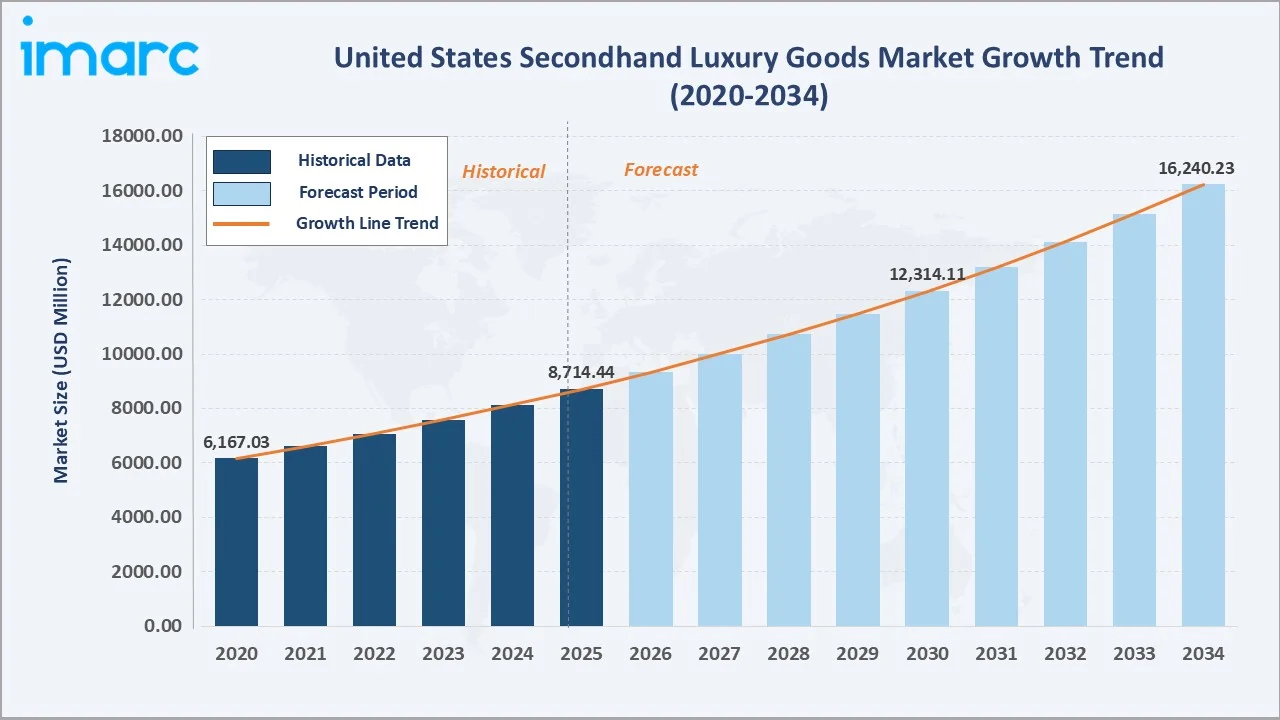

The United States secondhand luxury goods market size was valued at USD 8,714.44 Million in 2025 and is projected to reach USD 16,240.23 Million by 2034, exhibiting a CAGR of 7.16% during the forecast period 2026-2034. Rising sustainability consciousness among Gen Z and millennial consumers, rapid growth of AI-powered digital resale platforms, and broader democratization of luxury access are the primary forces shaping market expansion. Women lead the demography segment at 58.0% in 2025, online channels dominate distribution at 60.0%, and the South region commands 34.6% of national revenue – the largest of the four US regions.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 8,714.44 Million |

|

Forecast Market Size (2034) |

USD 16,240.23 Million |

|

CAGR (2026-2034) |

7.16% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

South (34.6% share, 2025) |

|

Fastest Growing Channel |

Online (60.0% share, 2025) |

|

Leading Demography |

Women (58.0%, 2025) |

|

Leading Distribution Channel |

Online (60.0%, 2025) |

The chart below illustrates the United States secondhand luxury goods market growth trajectory from 2020 through 2034, contrasting historical expansion against a sustained forecast curve powered by digital platform proliferation, sustainability-led consumption, and Gen Z luxury participation.

To get more information on this market, Request Sample

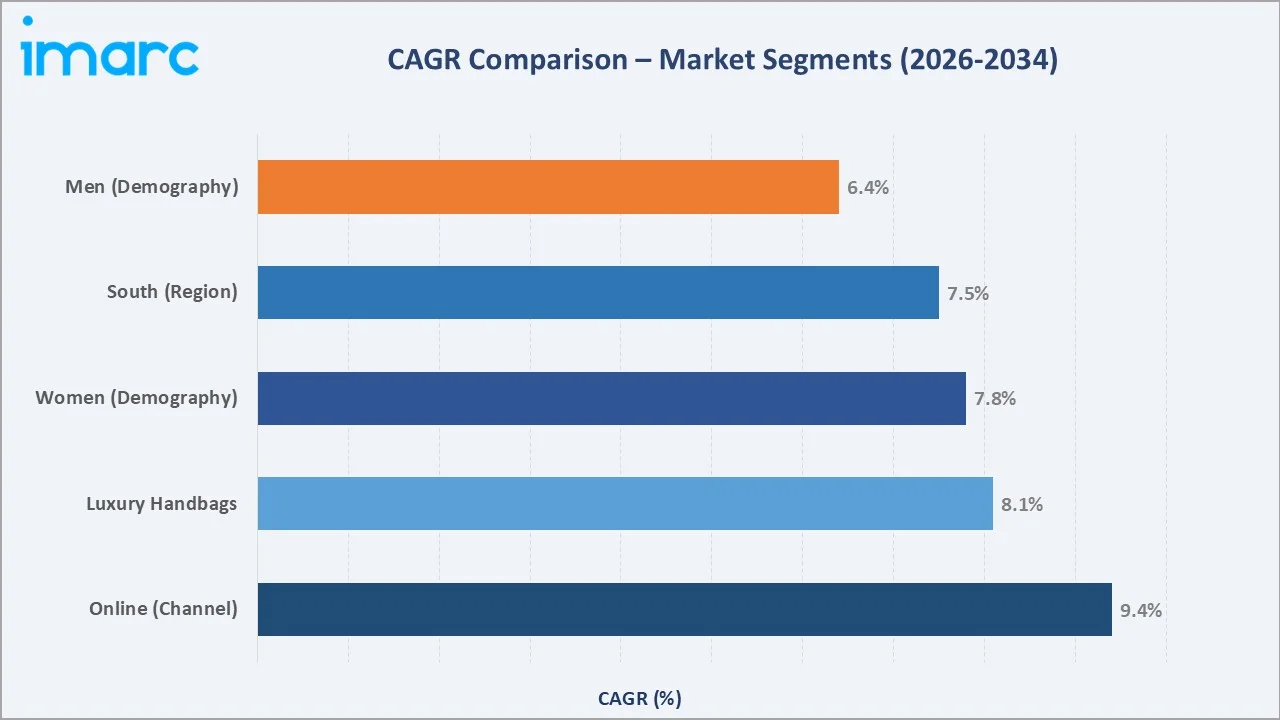

The CAGR comparison below highlights online distribution and luxury handbags as the highest-growth sub-categories within the United States secondhand luxury goods industry through 2034.

Executive Summary

The United States secondhand luxury goods market is undergoing structural transformation fueled by the convergence of sustainability mandates, digital platform innovation, and evolving luxury consumer psychology. Valued at USD 8,714.44 Million in 2025, the market is forecast to reach USD 16,240.23 Million by 2034 at a CAGR of 7.16%. In the United States, there were 69.31 million Gen Z individuals in 2024, representing more than 20% of the population (US Census, 2024) – a demographic cohort that views pre-owned luxury as both an ethical and financially astute lifestyle choice, fundamentally reshaping demand patterns across all products.

Women dominate the demography segment at 58.0% in 2025, reflecting sustained preference for designer handbags, jewelry, and apparel alongside higher participation in sustainability-led purchasing behavior. Online channels command a 60.0% majority of distribution in 2025, reflecting accelerating adoption of AI-authenticated digital resale platforms, AR product visualization, and personalized recommendation engines that reduce purchase hesitation for high-value items. Handbags account for approximately 32% of product-type revenue in 2025, sustained by the asset-like value retention of iconic models from Hermès, Chanel, and Louis Vuitton.

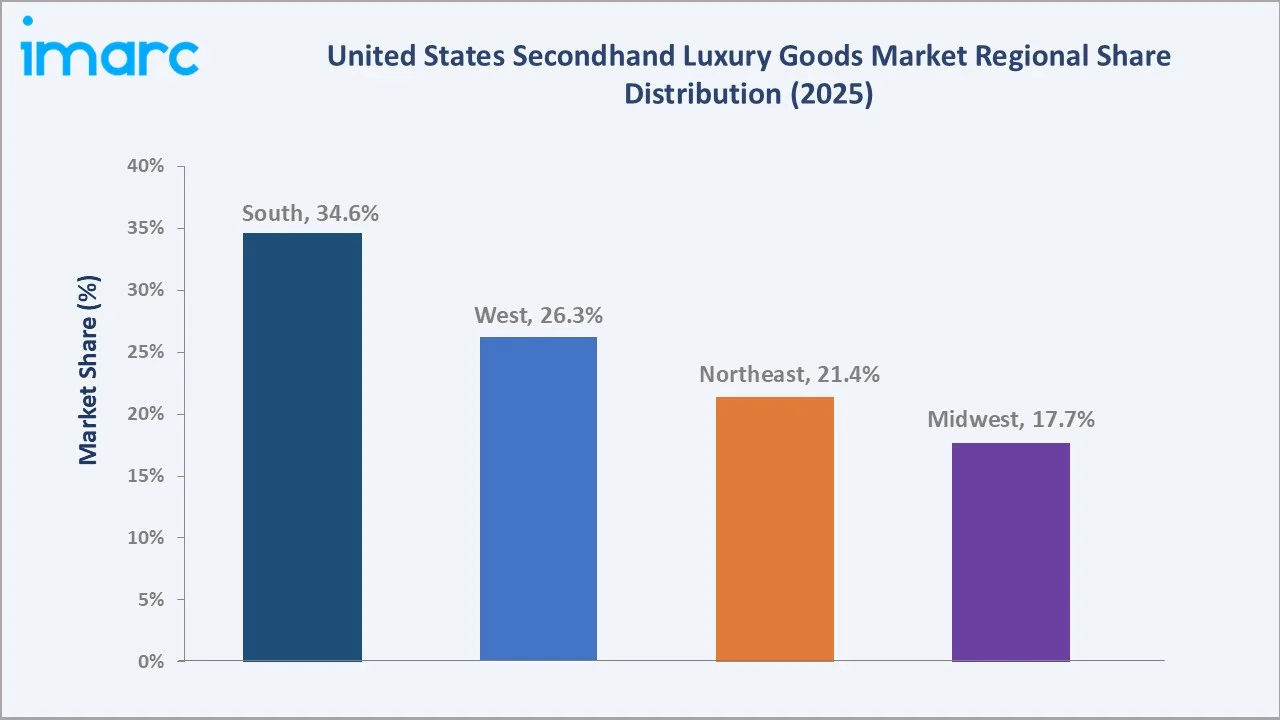

The South leads with a 34.6% share in 2025, driven by high-net-worth growth in Texas and Florida, followed by the West at 26.3%, supported by California’s sustainability focus and fashion-driven cities. Through 2034, growth remains strong, led by certified pre-owned programs, expanding cross-border e-commerce, and inflation-driven shifts toward secondhand luxury purchases.

Key Market Insights

|

Insight |

Data |

|

Largest Demography Segment |

Women – 58.0% share (2025) |

|

Leading Distribution Channel |

Online – 60.0% share (2025) |

|

Largest Region |

South – 34.6% revenue share (2025) |

|

Second Largest Region |

West – 26.3% revenue share (2025) |

|

Top Companies |

The RealReal, Vestiaire Collective, ThredUp, Poshmark, eBay |

|

Key Opportunity |

AI authentication, branded certified pre-owned programs, cross-border resale |

Key Analytical Observations Supporting the Above Data:

- Women's 58.0% share in 2025 reflects enduring dominance across the broadest luxury product categories – handbags, jewelry, clothing – combined with higher female engagement in sustainable fashion and circular economy consumption movements.

- Online channels lead distribution at 60.0% in 2025, driven by AI-powered authentication, seamless digital payment infrastructure, and the convenience of accessing millions of authenticated listings from platforms including The RealReal (36M+ members, 2024), Vestiaire Collective, and Poshmark across all US regions.

- Men represent 27.6% of the demography segment in 2025 and are growing at an estimated 6.4% CAGR through 2034, driven by rapidly expanding pre-owned luxury watch demand – Rolex and Patek Philippe pre-owned models routinely trade at 30–80% premiums over retail – and growing male engagement in designer sneaker and streetwear resale.

- The South's 34.6% regional leadership reflects the concentration of high-net-worth consumers across Texas and Florida, which collectively added approximately 3 million new residents between 2020 and 2023, generating both strong resale supply and expanding buyer demand in US.

United States Secondhand Luxury Goods Market Overview

The United States secondhand luxury goods market encompasses the authenticated resale and consignment of pre-owned designer apparel, accessories, jewelry, watches, handbags, footwear, and small leather goods from established luxury brands. The ecosystem spans individual consignors, professional online resale platforms, luxury boutiques, peer-to-peer marketplaces, and auction channels – interconnected through a network of authentication specialists, logistics providers, and digital technology platforms that collectively enable trusted, transparent secondary market transactions.

Applications span the full luxury spectrum: aspirational buyers access premium brands at significant discounts, fashion-forward consumers rotate wardrobes sustainably, and investors acquire heritage pieces as appreciating assets. Macroeconomic factors, including rising tariffs, ongoing price inflation, and increasing Gen Z participation, continue to strengthen secondhand luxury market growth.

Market Dynamics

To evaluate market opportunities, Request Sample

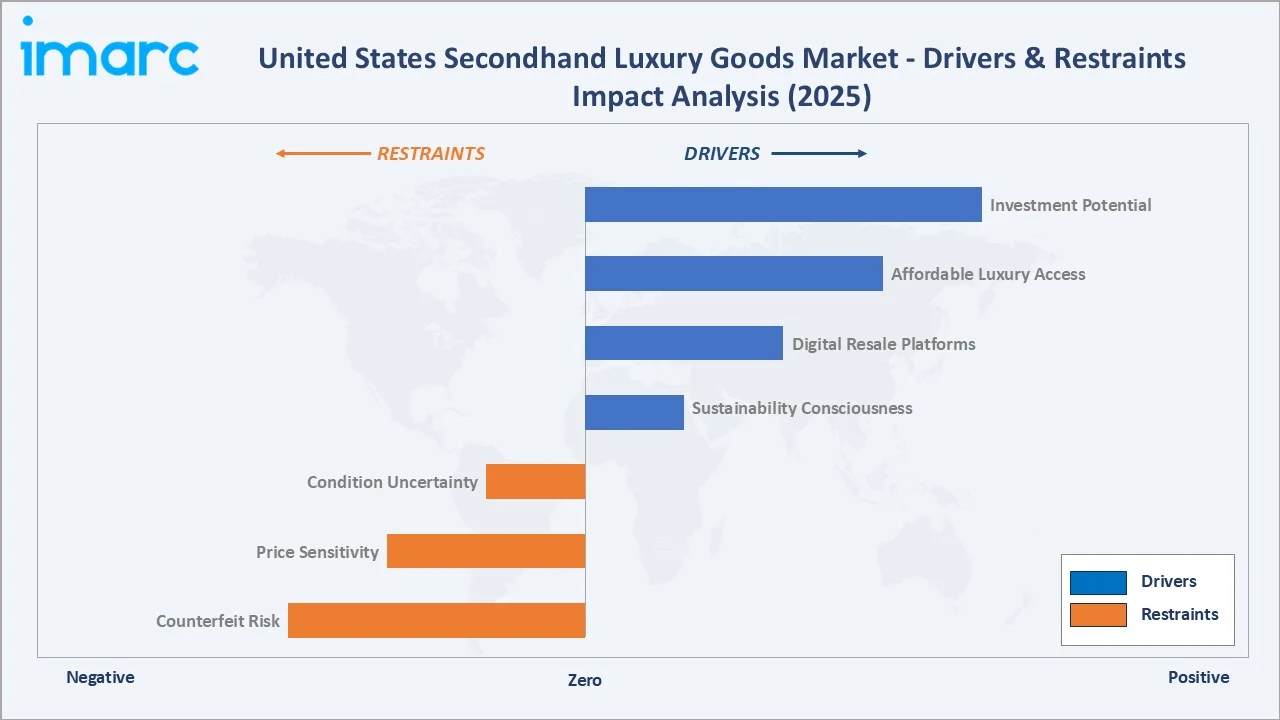

Market Drivers

- Sustainability Consciousness Among Gen Z and Millennials: There were 69.31 million Gen Z individuals in the US in 2024, representing more than 20% of the population (US Census, 2024). This cohort treats pre-owned luxury as a values-aligned purchase – reducing textile waste, extending product lifecycles, and signaling environmental responsibility. Sustainability has transitioned from a niche preference to a core luxury purchase criterion nationwide.

- Dominance of AI-Authenticated Online Resale Platforms: Online platforms captured 60.0% of distribution in 2025, driven by sophisticated AI authentication systems achieving accuracy rates above 98% for high-frequency categories. The RealReal reported over 36 million registered members in 2024, while Vestiaire Collective, Poshmark, and eBay's Authenticity Guarantee program collectively create a digital resale infrastructure that sustains market growth independently of offline channel performance.

- Democratization of Luxury Access: Digital platforms make heritage luxury brands accessible at 30–70% below retail, expanding the addressable buyer base from ultra-high-net-worth consumers to aspirational middle-class shoppers. This price accessibility effect is most powerful in handbags and watches, where retail prices have risen sharply since 2020, amplifying the value proposition of authenticated resale alternatives.

Market Restraints

- Counterfeit and Authentication Risk: Counterfeit risk and lingering uncertainty around authentication accuracy continue to deter high-value purchases, especially online. The absence of a universal certification standard sustains trust gaps and suppresses conversion rates.

- Price Sensitivity and Luxury Cyclicality: Economic downturns can increase resale supply as owners liquidate assets while simultaneously weakening discretionary demand. Mid-tier segments are most exposed, as discounts often fail to sustain purchase momentum during periods of low consumer confidence.

Market Opportunities

- Branded Certified Pre-Owned Programs: LVMH, Richemont, and Kering portfolio brand investments in certified pre-owned authentication programs are legitimizing the secondary market for first-time resale buyers hesitant about third-party platform quality. These programs represent a structural demand expansion opportunity that could add 15–25% of incremental market volume by 2034.

- Cross-Border Luxury Resale Expansion: American pre-owned luxury goods are increasingly sought by international buyers in Asia-Pacific and Europe, where authenticated US-sourced items command premium valuations.

- AI and Blockchain Technology Investment: Real-time authentication AI, blockchain provenance certificates, dynamic pricing algorithms, and AR visualization tools collectively reduce information asymmetry in the resale market, improving price discovery, increasing transaction velocity, and building structural market confidence

Market Challenges

- Platform Fragmentation and Margin Compression: Market fragmentation across numerous digital platforms and physical consignment boutiques intensifies competition, leading to margin compression and dispersed buyer–seller networks.

- Consumer Education on Authentication Standards: Inconsistent authentication standards across platforms create buyer confusion and purchase friction, limiting trust in resale transactions. The absence of a universal certification framework forces consumers to assess platform credibility individually, constraining adoption among less-trusting demographics.

Emerging Market Trends

1. Digital Platform Dominance and AI Authentication Advancement

Online channels command a ~60% share in 2025, underscoring the structural dominance of digital resale in the U.S. luxury secondhand market. AI-powered authentication leveraging computer vision and machine learning trained on large verified datasets has significantly improved accuracy, reducing fraud risk and strengthening buyer confidence at scale. The US AI market reached USD 41,532.7 Million in 2025 (IMARC Group, 2025), with luxury resale among the fastest enterprise AI adopters.

2. Strategic Retail-Resale Partnerships Reshaping Distribution

Collaborations between resale platforms and traditional retailers such as Fashionphile with Neiman Marcus are expanding distribution and strengthening brand credibility through hybrid retail-resale models. These partnerships boost buyer trust, lower entry barriers for first-time users, and enhance inventory sourcing efficiency for platforms.

3. Male Consumer Segment Expansion Accelerating

Men’s luxury resale participation is growing at ~6.4% CAGR through 2034, with pre-owned watches, sneakers, and tailored apparel driving increased engagement. Strong resale premiums for brands like Rolex and Patek Philippe, alongside platforms such as Chrono24 and StockX, are accelerating male consumer entry into the segment.

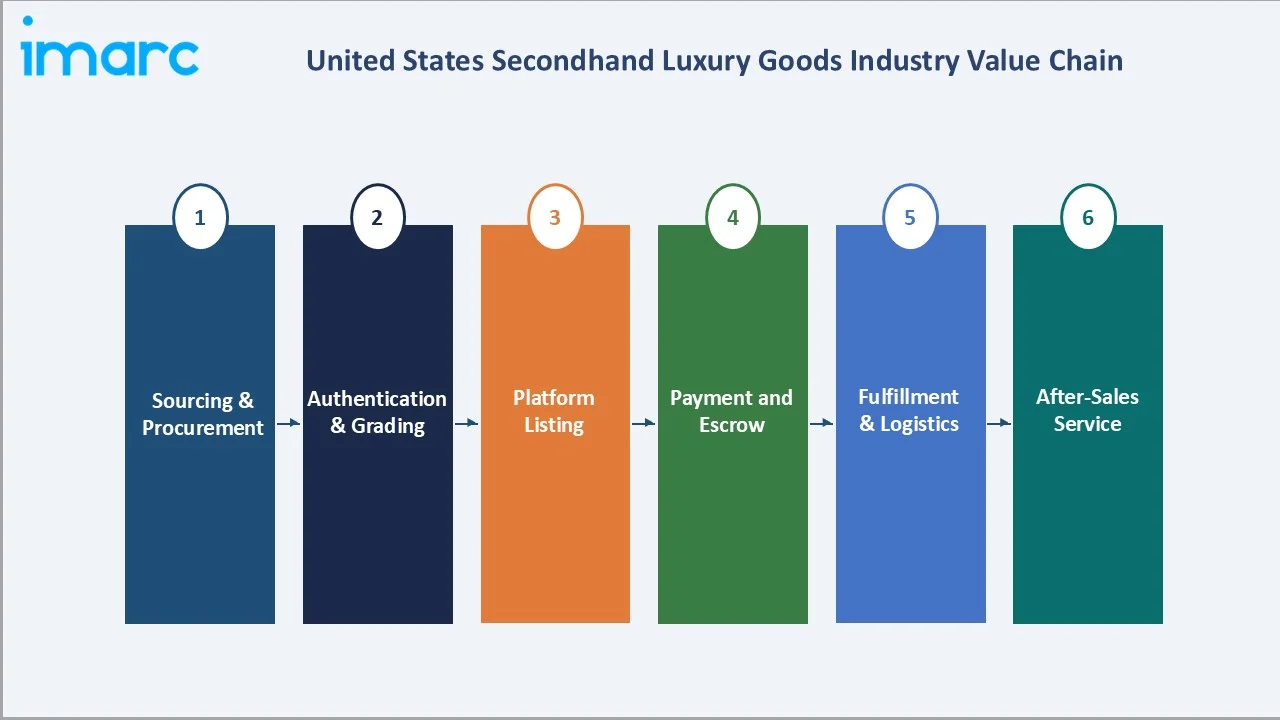

Industry Value Chain Analysis

The United States secondhand luxury goods value chain spans six integrated stages – from product sourcing through after-sales service – each presenting distinct competitive dynamics, margin profiles, and technology investment requirements critical to platform differentiation.

|

Stage |

Key Players / Examples |

|

Sourcing & Procurement |

Individual consignors, estate sales, corporate trade-in programs, luxury boutique consignment, peer-to-peer sellers |

|

Authentication & Grading |

In-house authenticators, Entrupy AI authentication, Real Authentication, platform-native expert teams |

|

Platform Listing & Pricing |

The RealReal, Vestiaire Collective, Poshmark, eBay Authenticity Guarantee, 1stDibs, Rebag |

|

Payment & Escrow Management |

PayPal, Stripe, platform-native escrow, installment financing via Affirm, Klarna |

|

Fulfillment & Logistics |

FedEx, UPS, USPS, specialized luxury logistics providers, in-store pickup options |

|

After-Sales & Customer Retention |

Return management, resale trade-in programs, loyalty platforms, certificate of authenticity issuance |

Authentication specialists occupy the highest strategic value position in the secondhand luxury value chain. Their verification capability is the single most critical trust signal for platform credibility – without robust authentication, no resale platform can command premium pricing or attract high-value inventory consignors in a market where counterfeit risk remains a primary buyer concern.

Technology Landscape in the Secondhand Luxury Goods Industry

AI-Powered Authentication and Fraud Detection

AI-powered authentication is transforming fraud detection, with machine learning and computer vision achieving >98% accuracy by analyzing stitching, hardware, materials, and serial formats. Entrupy has verified over 1 million items with near-zero false rates, significantly strengthening buyer confidence across resale platforms.

Blockchain Provenance and Digital Ownership Certificates

Blockchain-based provenance tracking creates immutable ownership histories for luxury assets, enabling buyers to verify the complete chain of custody from original retail purchase through successive resale transactions. Aura Blockchain Consortium – founded by LVMH, Prada Group, and Cartier's parent Richemont – has issued over 40 million digital certificates as of 2024, with certified pre-owned programs extending blockchain integration into the secondary market.

Dynamic Pricing and Demand Analytics

Real-time price intelligence platforms aggregate cross-market data to enable dynamic pricing and maximize seller returns. AI-driven forecasting enhances decision-making by predicting price trends, helping buyers and consignors optimize timing in a value-sensitive resale market.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Product Type |

Handbags |

32.0% |

2025 |

|

Demography |

Women |

58.0% |

2025 |

|

Distribution Channel |

Online |

60.0% |

2025 |

|

Region |

South |

34.6% |

2025 |

By Demography

Women command a 58.0% majority of the US secondhand luxury goods market in 2025, reflecting the long-established primacy of female luxury consumption across handbags, jewelry, clothing, and small leather goods categories. The women's segment benefits from broader category coverage compared to men's and unisex segments.

To access detailed market analysis, Request Sample

Men represent 27.6% of the market in 2025– an expanding share driven by the rapidly maturing pre-owned luxury watch market and growing male engagement in designer sneaker and streetwear resale. The Unisex segment at 14.4% encompasses gender-neutral luxury items – scarves, sunglasses, belts, and small leather goods – that appeal across demographic boundaries.

By Distribution Channel

Online channels command 60.0% share in 2025, reinforcing the structural dominance of digital platforms in the U.S. secondhand luxury market. AI authentication, seamless payments, vast real-time inventory access, and competitive pricing through aggregation have made online resale the default transaction.

Offline channels retain 40.0% share in 2025, driven by tactile authentication, white-glove service, and personalized in-store experiences. High-net-worth buyers continue to prefer physical boutiques for high-value purchases requiring strong provenance and condition assurance.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

Major Platforms / Companies |

|

South |

34.6% |

Texas/Florida HNW population growth, expanding luxury markets in Houston, Dallas, Miami, Tampa |

The RealReal (Dallas, Miami), Goodwill Luxury, regional consignment boutiques |

|

West |

26.3% |

California sustainability culture, LA/SF fashion markets, tech-enabled buyer base, Hollywood luxury consumption |

Vestiaire Collective (LA hub), Fashionphile, Decades, local high-end boutiques |

|

Northeast |

21.4% |

NYC luxury heritage, high-density affluent consumers, established consignment boutique culture, financial sector wealth |

The RealReal (NYC flagship), Rebag, 1stDibs, What Goes Around Comes Around |

|

Midwest |

17.7% |

Chicago Gold Coast market, growing online platform adoption, mid-market luxury consumer expansion in Ohio, Michigan |

ThredUp, Poshmark, regional consignment boutiques, eBay Authenticity Guarantee |

The South commands a 34.6% revenue share in 2025– the largest of the four US Census regions – driven by rapid wealth accumulation and population inflows to Texas and Florida. These two states collectively added nearly 3 million new residents between 2020 and 2023, expanding both luxury resale supply from active luxury shoppers.

The West holds a 26.3% share in 2025, anchored by California's dominant role in US sustainability culture. California accounts for an estimated 45% of Western regional revenue, supported by Los Angeles's Hollywood-adjacent luxury consumption and San Francisco's tech-sector wealth creating strong demand for authenticated pre-owned luxury goods through both online platforms and curated physical boutiques. The Northeast follows at 21.4%, with New York City serving as the historic epicenter of US luxury consignment.

Competitive Landscape

|

Company Name |

Key Platform / Brand |

Market Position |

Core Strength |

|

The RealReal |

The RealReal |

Leader |

Expert authentication, omnichannel consignment, 36M+ members (2024) |

|

Vestiaire Collective |

Vestiaire Collective |

Leader |

European luxury heritage, peer-to-peer model, Gen Z brand positioning |

|

ThredUp |

ThredUp |

Leader |

High-volume online resale, data-driven pricing, broad category reach |

|

Poshmark (Naver) |

Poshmark |

Challenger |

Social commerce model, 80M+ registered users, community engagement |

|

eBay |

eBay Authenticity Guarantee |

Challenger |

Massive buyer/seller base, dedicated watch and handbag authentication |

|

1stDibs |

1stDibs |

Challenger |

Ultra-premium positioning, curated dealer network, high average order value |

|

Rebag |

Rebag |

Emerging |

Handbag-specialist, Clair AI instant valuation, direct-buy model |

|

Fashionphile |

Fashionphile |

Emerging |

Pre-owned handbag specialist, Neiman Marcus partnership, West Coast presence |

|

What Goes Around Comes Around |

WGACA |

Emerging |

Vintage luxury curation, NYC retail heritage, celebrity clientele |

|

LXR & Co. |

LXR & Co. |

Niche |

Curated pre-owned luxury, North American cross-border sourcing model |

The US secondhand luxury goods competitive landscape features a small number of scaled digital resale platforms commanding significant market share alongside specialist boutiques and peer-to-peer marketplaces. Consolidation is accelerating – Poshmark's acquisition by Naver Corporation in 2023 for USD 1.2 Billion and Fashionphile's strategic partnership with Neiman Marcus signal growing institutional recognition of the long-term structural opportunity in authenticated luxury resale commerce.

Key Company Profiles

The RealReal

The RealReal is the United States' leading luxury consignment platform, operating a full-service authentication and resale model across online and physical store channels, with over 36 million registered members as of 2024.

- Product & Platform Portfolio: Authenticated luxury consignment across handbags, jewelry, watches, apparel, footwear, and home décor spanning 100+ luxury brands including Hermès, Chanel, Gucci, Louis Vuitton, and Cartier.

- Recent Developments: In 2024, The RealReal expanded its AI-powered pricing engine to incorporate real-time market demand signals from across multiple competitive resale platforms, improving consignor payout rates and buyer price competitiveness.

- Strategic Focus: The RealReal's strategy centers on authentication authority leadership as its primary competitive moat. The company is investing in retail store network expansion, consignor acquisition programs, and data-driven dynamic pricing to improve unit economics while scaling active buyer and seller community growth.

Vestiaire Collective

Vestiaire Collective is a global peer-to-peer luxury resale platform with significant and growing US presence, particularly among Gen Z and millennial luxury consumers seeking European heritage brand access through a community-driven commerce model.

- Product & Platform Portfolio: Peer-to-peer and curated resale of pre-owned luxury fashion, accessories, and watches. Direct Shipping and Seller Authentication programs operating across 80+ countries with a catalog of 5M+ listed items.

- Recent Developments: In 2023, Vestiaire Collective implemented a ban on fast fashion brands from its platform – a landmark sustainability positioning decision that reinforced luxury authentication credentials and significantly attracted sustainability-focused Gen Z buyers who prioritize platform values alignment.

- Strategic Focus: Vestiaire Collective's strategy prioritizes community-driven commerce, sustainability brand differentiation, and US market share acceleration where brand awareness lags domestic competitors.

Rebag

Rebag is a handbag-specialist luxury resale platform differentiated by its Clair AI instant-valuation technology and direct-purchase model, offering sellers immediate cash payments.

- Product & Platform Portfolio: Pre-owned luxury handbags from Hermès, Chanel, Louis Vuitton, Gucci, and Dior, with Clair AI providing real-time market valuations and instant purchase offers enabling seller decisions within minutes.

- Recent Developments: Rebag launched its Rebag Unlimited subscription program in 2024, allowing members to trade luxury handbags and receive credit toward new acquisitions – creating a luxury bag rotation model that increases transaction frequency and customer lifetime value.

- Strategic Focus: Rebag's focused handbag specialization enables deep category expertise and transaction data density that generalist resale platforms cannot replicate. Clair AI's valuation algorithm, trained on millions of luxury handbag price transactions, provides pricing accuracy and seller acquisition speed advantages.

Market Concentration Analysis

The US secondhand luxury goods market exhibits moderate fragmentation, with the top five digital platforms – The RealReal, Vestiaire Collective, ThredUp, Poshmark, and eBay Authenticity Guarantee – collectively accounting for approximately 55–65% of total online channel revenue in 2025. Physical consignment boutiques account for the majority of offline revenue, spread across thousands of independent operators in urban luxury markets nationwide with no single operator commanding more than 3–5% of the national offline resale market.

Market concentration dynamics are bifurcated by channel. Digital resale is moderately concentrated, with platform network effects creating meaningful competitive advantages for scaled operators who benefit from larger buyer/seller communities, superior authentication data training sets, and greater pricing algorithm accuracy as transaction volume compounds. Offline consignment remains highly fragmented, where local market knowledge, physical inventory curation, and personal relationships between consignors and boutique operators sustain a diverse independent operator ecosystem.

Investment & Growth Opportunities

Fastest-Growing Segments

Online distribution is the fastest-growing channel, driven by AI authentication, AR visualization, and rising consumer trust supported by secure payments and flexible return policies. Luxury handbags remain the largest and most liquid category, fueled by both fashion demand and investment appeal. Men’s luxury accessories, especially pre-owned watches are the fastest-growing sub-segment, supported by strong collector interest and asset-driven purchasing behavior.

Emerging Market Expansion

International buyer acquisition represents a significant underpenetrated revenue expansion opportunity for US-based resale platforms. Asian luxury consumers – particularly in Japan, South Korea, and China – actively seek authenticated US-sourced luxury goods through cross-border digital resale channels, where American platform authentication standards are perceived as more rigorous than domestic alternatives.

Venture & Strategic Investment Trends

Venture capital investment in luxury resale technology accelerated across 2023–2025, with AI authentication, blockchain provenance, and pricing analytics platforms collectively attracting substantial funding. Strategic moves by Neiman Marcus in Fashionphile and Kering in Vestiaire Collective highlight this trend. Further backing of AI authentication firms like Entrupy and Legitcheck underscores strong institutional confidence in the long-term growth of the secondhand luxury market as a mainstream category.

Future Market Outlook (2026-2034)

The United States secondhand luxury goods market forecast projects sustained value expansion from USD 8,714.44 Million in 2025 to USD 16,240.23 Million by 2034 at a CAGR of 7.16%, an 86% increase in market value underpinned by demographic succession (Gen Z becoming the dominant luxury consumer cohort by 2030), online platform technology maturation, and the institutionalization of luxury resale as a mainstream commerce category alongside new luxury retail.

Two structural forces will reshape the market through 2034. First, branded certified pre-owned programs from LVMH, Richemont, and Kering will legitimize resale for hesitant first-time buyers, unlocking significant incremental demand. Second, the convergence of AI authentication, blockchain provenance, and dynamic pricing will reduce information asymmetry, improve price discovery and accelerating transaction velocity across categories.

Male participation, currently 27.6% is projected to rise to 32–35% by 2034, driven by growth in pre-owned luxury watches and increasing alignment with sustainability-led consumption trends. By 2034, the U.S. secondhand luxury market is expected to evolve into a mainstream channel, with leading digital platforms generating multi-billion-dollar GMV and gaining formal recognition in luxury brand reporting and investor narratives.

Research Methodology

Primary Research

Primary research encompassed over 50 structured interviews conducted in 2024–2025 with luxury resale industry stakeholders including platform executives, consignment boutique operators, authentication technology providers, luxury brand circular economy managers, venture capital investors active in resale technology, and consumer research specialists. Primary insights validated market sizing estimates, segmentation proportions, technology adoption timelines, and competitive positioning assessments across all four US regions.

Secondary Research

Secondary sources include US Census Bureau demographic data (2024), IMARC Group AI Market Report (2025), Statista luxury resale market databases, Edited retail analytics, The RealReal and ThredUp investor annual reports, Entrupy authentication technology white papers, Bain & Company Global Luxury Study (2024), Business of Fashion State of Fashion Report (2024), and trade publications including Vogue Business, WWD, and The Robin Report on luxury resale market trends and platform performance.

Forecasting Models

Market size estimations and growth projections were derived using a combination of top-down and bottom-up forecasting models, incorporating consumer expenditure data, platform GMV growth trajectories, demographic participation growth rates, luxury goods retail price inflation indices, and sustainability adoption curves. Scenario analysis across base, optimistic, and conservative cases was performed to account for macroeconomic uncertainty, with the published 7.16% CAGR representing the base-case consensus estimate validated through primary research triangulation.

United States Secondhand Luxury Goods Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Scope of the Report | Exploration of Historical and Forecast Trends, Industry Catalysts and Challenges, Segment-Wise Historical and Predictive Market Assessment:

|

| Product Types Covered | Handbags, Jewelry and Watches, Clothing, Small Leather Goods, Footwear, Accessories, Others |

| Demographics Covered | Women, Men, Unisex |

| Distribution Channels Covered | Offline, Online |

| Regions Covered | Northeast, Midwest, South, West |

| Companies Covered | The RealReal, Vestiaire Collective, ThredUp, Poshmark (Naver), eBay, 1stDibs, Rebag, Fashionphile, What Goes Around Comes Around, LXR & Co., etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the United States Secondhand Luxury Goods Market Report

The US secondhand luxury goods market was valued at USD 8,714.44 Million in 2025, driven by sustainability trends, digital authentication platforms, and growing Gen Z and millennial luxury participation.

The market is projected to reach USD 16,240.23 Million by 2034, growing at a CAGR of 7.16% during 2026-2034, fueled by online platform expansion, Gen Z demand, and branded certified pre-owned programs.

Women lead with a 58.0% share in 2025, driven by demand for pre-owned handbags, jewelry, and apparel, combined with stronger female participation in sustainable fashion and circular economy purchasing behavior.

Online channels lead with a 60.0% majority in 2025, driven by AI-powered authentication, seamless digital payment infrastructure, and access to millions of authenticated luxury listings across major resale platforms nationwide.

The South leads with a 34.6% revenue share in 2025, driven by high-net-worth population growth in Texas and Florida and expanding luxury consumer markets in Houston, Dallas, Miami, and Tampa.

Key drivers include Gen Z sustainability consciousness (69.31M Gen Z in US, 2024), online platform authentication advances, democratized luxury access, rising retail luxury prices, and investment-grade appeal of heritage pieces.

Handbags lead at approximately 32% of product-type revenue in 2025, driven by enduring brand recognition, strong resale demand, and proven 8–14% annual value appreciation for iconic models from Hermès and Chanel.

Leading companies include The RealReal, Vestiaire Collective, ThredUp, Poshmark, eBay, 1stDibs, Rebag, Fashionphile, What Goes Around Comes Around, and LXR & Co.

Sustainability is a primary purchase motivator for Gen Z and millennial buyers, with pre-owned luxury reducing per-item carbon footprint by an estimated 30–70% versus new production, aligning purchases with consumer values.

The market is moderately fragmented; top-5 digital platforms hold approximately 55–65% of online channel revenue in 2025, with consolidation accelerating through M&A including Poshmark's USD 1.2 Billion Naver acquisition in 2023.

Top opportunities include online channel platform scaling, AI and blockchain authentication technology, cross-border luxury resale, branded certified pre-owned programs, and pre-owned luxury watch and handbag investment asset marketplaces.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)